Earnings

Auto Added by WPeMatico

Auto Added by WPeMatico

Box has been in an ongoing dispute with activist investors Starboard Value over control of the board, an argument that is expected to come to a head on September 9th at the annual shareholder meeting. In an effort to show shareholders that the numbers are continuing to improve under the current leadership, Box took the unusual move of releasing its earning report this morning, two weeks ahead of the expected August 25th report date.

Companies don’t normally report ahead of schedule, but perhaps Box sees the opportunity to do some lobbying, or conversely, to counter any negative lobbying that Starboard may be doing with its fellow investors ahead of the vote.

It’s also worth noting that in spite of the meeting being on September 9th, like a lot of voting these days, people will be sending in votes throughout this month, ahead of that day. Box wants to get its latest financial information out there sooner rather than later to catch those early voters before they cast their ballots.

Fortunately for Box and CEO Aaron Levie, the numbers look decent.

It’s not hard to see why Box released its earnings early, as the numbers provide an argument for keeping the company’s current leadership in place.

In the three-month period ending July 31, 2021 — the second quarter of Box’s fiscal 2022 — the company generated $214 million in revenue, up 11% on a year-over-year basis. And, as Box is quick to point out, its second consecutive quarter of “accelerating revenue growth.” The company bested its own guidance of $211 to $212 million in revenue for the period.

It matters that Box is showing an ability to accelerate its revenue growth. First, because doing so puts wind in the sales of its stock; quickly growing companies are worth more per dollar of revenue than more slowly growing concerns, and accelerating revenue growth over time is investor catnip.

The accelerating pace of growth over the last half year also provides footing for Box’s leadership to argue that their product choices have been sound, directly supporting their positions that they should remain in charge of the company. If they made good product decisions quarters ago, and those choices are leading to accelerating revenue growth, why swap out the CEO?

Box had more quarterly good news apart from its revenue numbers to disclose. It also reported improved GAAP and non-GAAP operating margins — a key measure of profitability — better billings results than it had previously anticipated for the period. Box’s net retention rate also expanded to 106% from 103% in the sequentially preceding period.

And the company boosted its guidance for its fiscal year from “$845 million to $853 million” to “$856 million to $860 million.”

The counter arguments are somewhat easy to generate, however. Yes, Box’s revenue growth is accelerating, but from an admittedly reduced base; it’s not as hard to accelerate revenue expansion from low numbers as it is from higher base levels. And the company’s net retention is lower than what any business-focused SaaS company would want to report.

Will the good news be enough? Shares of Box are up around 1.5% in today’s regular trading, despite a somewhat mixed overall market. Investors now have to vote with more than just their dollars.

Starboard bought approximately 7.5% of the company in 2019, and actually stayed fairly quiet for the first year, but at the end of 2020 it started making itself heard with rumors of pressure to sell the company. In what appeared to be a defensive move, Box took a $500 million investment from private equity firm KKR and gave the investor a board seat in April.

The activist investor did not take kindly to that move, writing in a letter to investors in early May, “The only viable explanation for this financing is a shameless and utterly transparent attempt to “buy the vote” and shows complete disregard for proper corporate governance and fiscal discipline.” In that same letter, Starboard made it official that it wanted to take over several board seats, outlining a litany of complaints it had about the way the company was being run. It also made clear that it wanted co-founder and CEO Aaron Levie gone or the company sold.

Box pushed back that the letter and another on May 10th did not accurately reflect the progress that the company had made. In July, Box took the battle public in an SEC filing detailing the back and forth dance that had been going between Box and Starboard since it bought its stake in the company

So far, the cloud content management company has staved off all attempts to force its hand and sell the company or fire Levie, but this is all going to culminate with the shareholder’s vote. It’s truly a battle for the soul of the company.

If Starboard convinces shareholders to give it several seats on the Box board, it would probably be able to push out Levie, take control of the company and likely sell it to the highest bidder. The early financial report released today, while not exactly stellar, shows a pattern of increasingly good quarters, and that’s what Box is hoping voters will focus on when they fill out their ballots.

Powered by WPeMatico

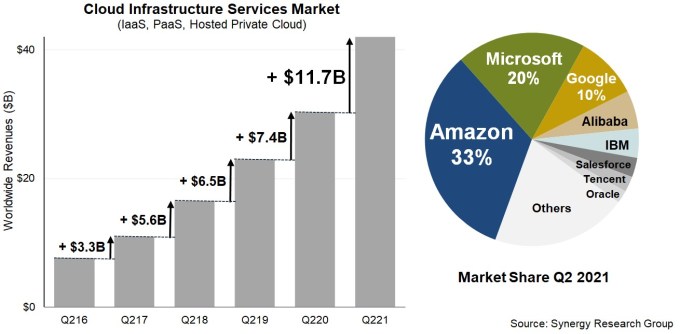

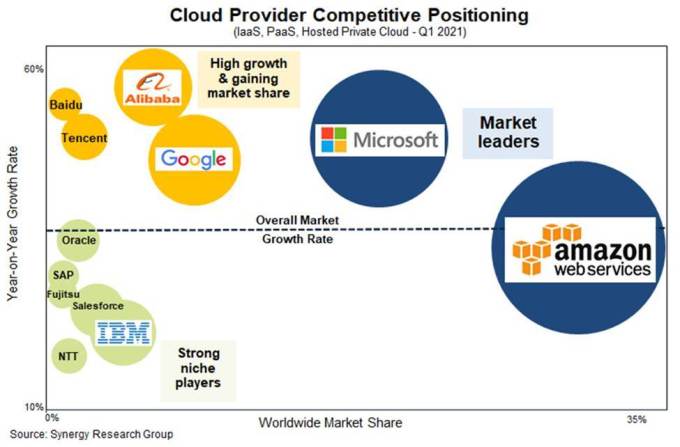

It’s often said in baseball that a prospect has a high ceiling, reflecting the tremendous potential of a young player with plenty of room to get better. The same could be said for the cloud infrastructure market, which just keeps growing, with little sign of slowing down any time soon. The market hit $42 billion in total revenue with all major vendors reporting, up $2 billion from Q1.

Synergy Research reports that the revenue grew at a speedy 39% clip, the fourth consecutive quarter that it has increased. AWS led the way per usual, but Microsoft continued growing at a rapid pace and Google also kept the momentum going.

AWS continues to defy market logic, actually increasing growth by 5% over the previous quarter at 37%, an amazing feat for a company with the market maturity of AWS. That accounted for $14.81 billion in revenue for Amazon’s cloud division, putting it close to a $60 billion run rate, good for a market leading 33% share. While that share has remained fairly steady for a number of years, the revenue continues to grow as the market pie grows ever larger.

Microsoft grew even faster at 51%, and while Microsoft cloud infrastructure data isn’t always easy to nail down, with 20% of market share according to Synergy Research, that puts it at $8.4 billion as it continues to push upward with revenue up from $7.8 billion last quarter.

Google too continued its slow and steady progress under the leadership of Thomas Kurian, leading the growth numbers with a 54% increase in cloud revenue in Q2 on revenue of $4.2 billion, good for 10% market share, the first time Google Cloud has reached double figures in Synergy’s quarterly tracking data. That’s up from $3.5 billion last quarter.

Image Credits: Synergy Research

After the Big 3, Alibaba held steady over Q1 at 6% (but will only report this week), with IBM falling a point from Q1 to 4% as Big Blue continues to struggle in pure infrastructure as it makes the transition to more of a hybrid cloud management player.

John Dinsdale, chief analyst at Synergy, says that the Big 3 are spending big to help fuel this growth. “Amazon, Microsoft and Google in aggregate are typically investing over $25 billion in capex per quarter, much of which is going towards building and equipping their fleet of over 340 hyperscale data centers,” he said in a statement.

Meanwhile, Canalys had similar numbers, but saw the overall market slightly higher at $47 billion. Their market share broke down to Amazon with 31%, Microsoft with 22% and Google with 8% of that total number.

Canalys analyst Blake Murray says that part of the reason companies are shifting workloads to the cloud is to help achieve environmental sustainability goals as the cloud vendors are working toward using more renewable energy to run their massive data centers.

“The best practices and technology utilized by these companies will filter to the rest of the industry, while customers will increasingly use cloud services to relieve some of their environmental responsibilities and meet sustainability goals,” Murray said in a statement.

Regardless of whether companies are moving to the cloud to get out of the data center business or because they hope to piggyback on the sustainability efforts of the Big 3, companies are continuing a steady march to the cloud. With some estimates of worldwide cloud usage at around 25%, the potential for continued growth remains strong, especially with many markets still untapped outside the U.S.

That bodes well for the Big 3 and for other smaller operators who can find a way to tap into slices of market share that add up to big revenue. “There remains a wealth of opportunity for smaller, more focused cloud providers, but it can be hard to look away from the eye-popping numbers coming out of the Big 3,” Dinsdale said.

In fact, it’s hard to see the ceiling for these companies any time in the foreseeable future.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

We were a smaller team this week, with Natasha and Alex joined by Grace and Chris to sort through a week that brought together both this quarter’s earnings cycle and the Q3 IPO rush. So, it was just a little busy!

Before we get to topics, however, a note that we are having a lot of fun recording these live on Twitter Spaces. We’ve found a hacky way to capture local audio and also share the chats live. So, hit us up on Twitter so you can hang out with us. It’s fun — and we may even bring you up on stage to play guest host.

OK, now, to the Great List of Subjects:

Powered by WPeMatico

The notion of digital transformation evolved from a buzzword joke to a critical and accelerating fact during the COVID-19 pandemic. The changes wrought by a global shift to remote work and schooling are myriad, but in the business realm they have yielded a change in corporate behavior and consumer expectation — changes that showed up in a bushel of earnings reports this week.

TechCrunch may tend to have a private-company focus, but we do keep tabs on public companies in the tech world as they often provide hints, notes and other pointers on how startups may be faring. In this case, however, we’re working in reverse; startups have told us for several quarters now that their markets are picking up momentum as customers shake up their buying behavior with a distinct advantage for companies helping customers move into the digital realm. And public company results are now confirming the startups’ perspective.

The accelerating digital transformation is real, and we have the data to support the point.

What follows is a digest of notes concerning the recent earnings results from Box, Sprout Social, Yext, Snowflake and Salesforce. We’ll approach each in micro to save time, but as always there’s more digging to be done if you have time. Let’s go!

Kicking off with Yext, the company beat expectations in its most recent quarter. Today its shares are up 18%. And a call with the company’s CEO Howard Lerman underscored our general thesis regarding the digital transformation’s acceleration.

In brief, Yext’s evolution from a company that plugged corporate information into external search engines to building and selling search tech itself has been resonating in the market. Why? Lerman explained that consumers more and more expect digital service in response to their questions — “who wants to call a 1-800 number,” he asked rhetorically — which is forcing companies to rethink the way they handle customer inquiries.

In turn, those companies are looking to companies like Yext that offer technology to better answer customer queries in a digital format. It’s customer-friendly, and could save companies money as call centers are expensive. A change in behavior accelerated by the pandemic is forcing companies to adapt, driving their purchase of more digital technologies like this.

It’s proof that a transformation doesn’t have to be dramatic to have pretty strong impacts on how corporations buy and sell online.

Powered by WPeMatico

Box executives have been dealing with activist investor Starboard Value over the last year, along with fighting through the pandemic like the rest of us. Today the company reported earnings for the first quarter of its fiscal 2022. Overall, it was a good quarter for the cloud content management company.

The firm reported revenue of $202.4 million, up 10% compared to its year-ago result, numbers that beat Box projections of between $200 million to $201 million. Yahoo Finance reports the analyst consensus was $200.5 million, so the company also bested street expectations.

The company has faced strong headwinds the past year, in spite of a climate that has been generally favorable to cloud companies like Box. A report like this was badly needed by the company as it faces a board fight with Starboard over its direction and leadership.

Company co-founder and CEO Aaron Levie is hoping this report will mark the beginning of a positive trend. “I think you’ve got a better economic climate right now for IT investment. And then secondarily, I think the trends of hybrid work, and the sort of long-term trends of digital transformation are very much supportive of our strategy,” he told TechCrunch in a post-earnings interview.

While Box acquired e-signature startup SignRequest in February, it won’t actually be incorporating that functionality into the platform until this summer. Levie said that what’s been driving the modest revenue growth is Box Shield, the company’s content security product and the platform tools, which enable customers to customize workflows and build applications on top of Box.

The company is also seeing success with large accounts. Levie says that he saw the number of customers spending more than $100,000 with it grow by nearly 50% compared to the year-ago quarter. One of Box’s growth strategies has been to expand the platform and then upsell additional platform services over time, and those numbers suggest that the effort is working.

While Levie was keeping his M&A cards close to the vest, he did say if the right opportunity came along to fuel additional growth through acquisition, he would definitely give strong consideration to further inorganic growth. “We’re going to continue to be very thoughtful on M&A. So we will only do M&A that we think is attractive in terms of price and the ability to accelerate our roadmap, or the ability to get into a part of a market that we’re not currently in,” Levie said.

Box managed modest growth acceleration for the quarter, existing only if we consider the company’s results on a sequential basis. In simpler terms, Box’s newly reported 10% growth in the first quarter of its fiscal 2022 was better than the 8% growth it earned during the fourth quarter of its fiscal 2021, but worse than the 13% growth it managed in its year-ago Q1.

With Box, however, instead of judging it by normal rules, we’re hunting in its numbers each quarter for signs of promised acceleration. By that standard, Box met its own goals.

How did investors react? Shares of the company were mixed after-hours, including a sharp dip and recovery in the value of its equity. The street appears to be confused by the results, weighing the report and working out whether its moderately accelerating growth is sufficiently enticing to warrant holding onto its equity, or more perversely if its growth is not expansive enough to fend off external parties hunting for more dramatic changes at the firm.

Sticking to a high-level view of Box’s results, apart from its growth numbers Box has done a good job shaking fluff out of its operations. The company’s operating margins (GAAP and not) improved, and cash generation also picked up.

Perhaps most importantly, Box raised its guidance from “the range of $840 million to $848 million” to “$845 to $853 million.” Is that a lot? No. It’s +$5 million to both the lower and upper-bounds of its targets. But if you squint, the company’s Q4 to Q1 revenue acceleration, and upgraded guidance, could be an early indicator of a return to form.

Levie admitted that 2020 was a tough year for Box. “Obviously, last year was a complicated year in terms of the macro environment, the pandemic, just lots of different variables to deal with…” he said. But the CEO continues to think that his organization is set up for future growth.

Will Box manage to perform well enough to keep activist shareholders content? Levie thinks if he can string together more quarters like this one, he can keep Starboard at bay. “I think when you look at the next three quarters, the ability to guide up on revenue, the ability to guide up on profitability. We think it’s a very very strong earnings report and we think it shows a lot of the momentum in the business that we have right now.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here.

This morning was a notable one in the life of TechCrunch the publication, as our parent company’s parent company decided to sell our parent company to a different parent company. And now we’re going to have to get new corporate IDs, again, as it appears that our new parent company’s parent company wants to rebrand our parent company. As Yahoo.

Cool.

Anyway, a bunch of other stuff happened as well:

We’re back Wednesday with something special. Chat then!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Conventional wisdom over the last year has suggested that the pandemic has driven companies to the cloud much faster than they ever would have gone without that forcing event, with some suggesting it has compressed years of transformation into months. This quarter’s cloud infrastructure revenue numbers appear to be proving that thesis correct.

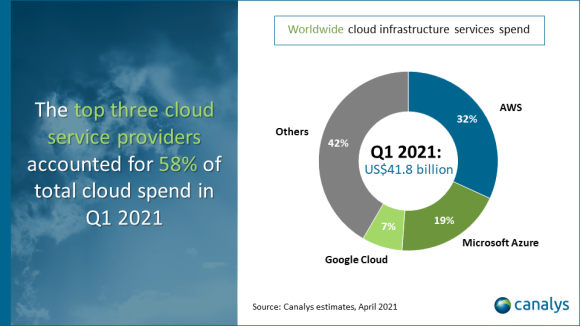

With The Big Three — Amazon, Microsoft and Google — all reporting this week, the market generated almost $40 billion in revenue, according to Synergy Research data. That’s up $2 billion from last quarter and up 37% over the same period last year. Canalys’s numbers were slightly higher at $42 billion.

As you might expect if you follow this market, AWS led the way with $13.5 billion for the quarter, up 32% year over year. That’s a run rate of $54 billion. While that is an eye-popping number, what’s really remarkable is the yearly revenue growth, especially for a company the size and maturity of Amazon. The law of large numbers would suggest this isn’t sustainable, but the pie keeps growing and Amazon continues to take a substantial chunk.

Overall AWS held steady with 32% market share. While the revenue numbers keep going up, Amazon’s market share has remained firm for years at around this number. It’s the other companies down market that are gaining share over time, most notably Microsoft, which is now at around 20% share — good for about $7.8 billion this quarter.

Google continues to show signs of promise under Thomas Kurian, hitting $3.5 billion, good for 9% as it makes a steady march toward double digits. Even IBM had a positive quarter, led by Red Hat and cloud revenue, good for 5% or about $2 billion overall.

Image Credits: Synergy Research

John Dinsdale, chief analyst at Synergy, says that even though AWS and Microsoft have firm control of the market, that doesn’t mean there isn’t money to be made by the companies playing behind them.

“These two don’t have to spend too much time looking in their rearview mirrors and worrying about the competition. However, that is not to say that there aren’t some excellent opportunities for other players. Taking Amazon and Microsoft out of the picture, the remaining market is generating over $18 billion in quarterly revenues and growing at over 30% per year. Cloud providers that focus on specific regions, services or user groups can target several years of strong growth,” Dinsdale said in a statement.

Canalys, another firm that watches the same market as Synergy, had similar findings with slight variations, certainly close enough to confirm one another’s findings. They have AWS with 32%, Microsoft 19% and Google with 7%.

Image Credits: Canalys

Canalys analyst Blake Murray says that there is still plenty of room for growth, and we will likely continue to see big numbers in this market for several years. “Though 2020 saw large-scale cloud infrastructure spending, most enterprise workloads have not yet transitioned to the cloud. Migration and cloud spend will continue as customer confidence rises during 2021. Large projects that were postponed last year will resurface, while new use cases will expand the addressable market,” he said.

The numbers we see are hardly a surprise anymore, and as companies push more workloads into the cloud, the numbers will continue to impress. The only question now is if Microsoft can continue to close the market share gap with Amazon.

Powered by WPeMatico

For IBM, much of the last eight years simply posting positive revenue growth was a challenge. In fact, the company had a period between 2013 and 2018 when it experienced an astonishing 22 straight quarters of negative revenue growth. So when Big Blue reported yesterday that revenue was up slightly, I’m sure the company took that as a win. Investors appear to be happy with the results, with the stock up 4.73% this morning as of publication.

Consider that over the last eight quarters encompassing FY2019 and FY2020, the company had only one positive revenue quarter when it was up 0.1% in Q42019. It had had five losing quarters prior to that one. When you look at yesterday’s report in that light, and combine it with growth in the Cloud and Cognitive Services group, it adds up to a decent quarter for IBM, one it badly needed after another negative report in the prior quarter.

Looking back at the January report, the company reported Cloud and Cognitive Services revenues down 4.5% at $6.8 billion, which was a big blow, considering the company has been betting much of its future on those very areas, fueled in large part by the $34 billion Red Hat acquisition in 2018.

Its most recent quarterly report proved much better, with the company reporting Cloud and Cognitive Services revenues of $5.4 billion, up 3.8% YoY. Interestingly quarter-on-quarter revenue for the segment was down, but rose on a year-over-year basis. Perhaps a year-end enterprise revenue push could account for the difference between Q4 2020 and Q1 2021.

At any rate, IBM CEO Arvind Krishna saw today’s report as a positive sign that his attempts to push the company toward a future focused on hybrid computing and AI were starting to take root. He also saw enough in the report to predict some growth this year.

“In our last call, we shared our financial expectations for the year, revenue growth and $11 billion to $12 billion of adjusted free cash flow. While it’s still early in the year and a lot remains to be done, we are confident enough to say that we are on track,” Krishna said in the earnings call with analysts yesterday.

The company has made a number of smaller acquisitions over the last year, including a couple of consulting companies, which should help as they try to work with customers around the transition to hybrid computing and artificial intelligence, both of which tend to require a lot of hand-holding to get done.

At the same time, of course, the company is continuing apace with its spin out of the legacy infrastructure services division, which it announced last year. The plan at this point is to rename the company Kyndryl (an unfortunate choice) and complete the spin out by year’s end.

CFO Jim Kavanaugh also sees the modestly positive quarter as something the company can build on. “…in fact we are even more confident in the position we put in place with regards to our two most important measures, one, revenue growth, and second, adjusted free cash flow, which is going to provide the fuel for the investments needed for us to capture that hybrid cloud $1 trillion TAM,” Kavanaugh said in the earnings call with analysts.

All of this is being pushed by Red Hat, which grew revenue 15% in the most recent quarter, something the company is banking will continue to advance it deeper into positive territory throughout the rest of 2021.

Krishna is not looking for booming growth by any means. He just wants growth, and even sustained single-digit top line expansion will make him happy. “Our systems if I take a two-year to three-year view kind of flattish, but in any given year it might increase or decrease but not by a whole lot. It doesn’t impact the top line a lot and that’s how sort of we get to the mid-single-digit sustainably,” Krishna said in the call.

The CEO simply wants to bring some long-term stability back to the company it has been sadly lacking in recent years. Of course, it’s hard to know if this quarter was a temporary upward blip on IBM’s earnings chart, one of those fluctuations up or down he spoke of, or if it is the corner the company has been looking to turn for years. Only time will tell whether IBM can sustain the modest revenue goals Krishna has set for the organization, or if it will fall back into the revenue doldrums that have plagued the company for the last eight years.

Powered by WPeMatico

Snowflake reported earnings this week, and the results look strong with revenue more than doubling year-over-year.

However, while the company’s fourth quarter revenue rose 117% to $190.5 million, it apparently wasn’t good enough for investors, who have sent the company’s stock tumbling since it reported Wednesday after the bell.

It was similar to the reaction that Salesforce received from Wall Street last week after it announced a positive earnings report. Snowflake’s stock closed down around 4% today, a recovery compared to its midday lows when it was off nearly 12%.

Why the declines? Wall Street’s reaction to earnings can lean more on what a company will do next more than its most recent results. But Snowflake’s guidance for its current quarter appeared strong as well, with a predicted $195 million to $200 million in revenue, numbers in line with analysts’ expectations.

Sounds good, right? Apparently being in line with analyst expectations isn’t good enough for investors for certain companies. You see, it didn’t exceed the stated expectations, so the results must be bad. I am not sure how meeting expectations is as good as a miss, but there you are.

It’s worth noting of course that tech stocks have taken a beating so far in 2021. And as my colleague Alex Wilhelm reported this morning, that trend only got worse this week. Consider that the tech-heavy Nasdaq is down 11.4% from its 52-week high, so perhaps investors are flogging everyone and Snowflake is merely caught up in the punishment.

Snowflake CEO Frank Slootman pointed out in the earnings call this week that Snowflake is well positioned, something proven by the fact that his company has removed the data limitations of on-prem infrastructure. The beauty of the cloud is limitless resources, and that forces the company to help customers manage consumption instead of usage, an evolution that works in Snowflake’s favor.

“The big change in paradigm is that historically in on-premise data centers, people have to manage capacity. And now they don’t manage capacity anymore, but they need to manage consumption. And that’s a new thing for — not for everybody but for most people — and people that are in the public cloud. I have gotten used to the notion of consumption obviously because it applies equally to the infrastructure clouds,” Slootman said in the earnings call.

Snowflake has to manage expectations, something that translated into a dozen customers paying $5 million or more per month to Snowflake. That’s a nice chunk of change by any measure. It’s also clear that while there is a clear tilt toward the cloud, the amount of data that has been moved there is still a small percentage of overall enterprise workloads, meaning there is lots of growth opportunity for Snowflake.

What’s more, Snowflake executives pointed out that there is a significant ramp up time for customers as they shift data into the Snowflake data lake, but before they push the consumption button. That means that as long as customers continue to move data onto Snowflake’s platform, they will pay more over time, even if it will take time for new clients to get started.

So why is Snowflake’s quarterly percentage growth not expanding? Well, as a company gets to the size of Snowflake, it gets harder to maintain those gaudy percentage growth numbers as the law of large numbers begins to kick in.

I’m not here to tell Wall Street investors how to do their job, anymore than I would expect them to tell me how to do mine. But when you look at the company’s overall financial picture, the amount of untapped cloud potential and the nature of Snowflake’s approach to billing, it’s hard not to be positive about this company’s outlook, regardless of the reaction of investors in the short term.

Powered by WPeMatico

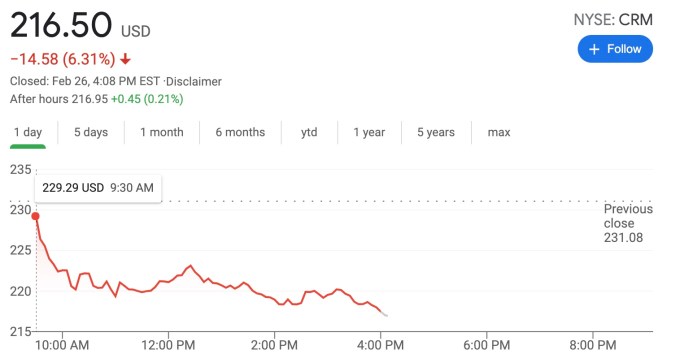

Wall Street investors can be fickle beasts. Take Salesforce as an example. The CRM giant announced a $5.82 billion quarter when it reported earnings yesterday. Revenue was up 20% year over year. The company also reported $21.25 billion in total revenue for the just-closed FY2021, up 24% YoY. If that wasn’t enough, it raised its FY2022 guidance (its upcoming fiscal year) to over $25 billion. What’s not to like?

You want higher quarterly revenue, Salesforce gave you higher revenue. You want high growth and solid projected revenue — check and check. In fact, it’s hard to find anything to complain about in the report. The company is performing and growing at a rate that is remarkable for an organization of its size and maturity — and it is expected to continue to perform and grow.

How did Wall Street react to this stellar report? It punished the stock with the price down over 6%, a pretty dismal day considering the company brought home such a promising report card.

Image Credits: Google

So what is going on here? It could be that investors simply don’t believe the growth is sustainable or that the company overpaid when it bought Slack at the end of last year for over $27 billion. It could be it’s just people overreacting to a cooling market this week. But if investors are looking for a high-growth company, Salesforce is delivering that.

While Slack was expensive, it reported revenue over $250 million yesterday, pushing it over the $1 billion run rate with more than 100 customers paying over $1 million in ARR. Those numbers will eventually get added to Salesforce’s bottom line.

Canaccord Genuity analyst David Hynes Jr. wrote that he was baffled by investors’ reaction to this report. Like me, he saw a lot of positives. Yet Wall Street decided to focus on the negative, and see “the glass half empty,” as he put it in his note to investors.

“The stock is clearly in the show-me camp, which means it’s likely to take another couple of quarters for investors to buy into the idea that fundamentals are actually quite solid here, and that Slack was opportunistic (and yes, pricey), but not an attempt to mask suddenly deteriorating growth,” Hynes wrote.

During the call with analysts yesterday, Brad Zelnick from Credit Suisse asked how well the company could accelerate out of the pandemic-induced economic malaise, and Gavin Patterson, Salesforce’s president and chief revenue officer, says the company is ready whenever the world moves past the pandemic.

“And let me reassure you, we are building the capability in terms of the sales force. You’d be delighted to hear that we’re investing significantly in terms of our direct sales force to take advantage of that demand. And I’m very confident we’ll be able to meet it. So I think you’re hearing today a message from us all that the business is strong, the pipeline is strong and we’ve got confidence going into the year,” Patterson said.

While Salesforce execs were clearly pumped up yesterday with good reason, there’s still doubt out in investor land that manifested itself in the stock starting down and staying down all day. It will be, as Hynes suggested, up to Salesforce to keep proving them wrong. As long as they keep producing quarters like the one they had this week, they should be just fine, regardless of what the naysayers on Wall Street may be thinking today.

Powered by WPeMatico