Dropbox

Auto Added by WPeMatico

Auto Added by WPeMatico

Dropbox, after more than a decade, finally went public this morning — and the stock soared more than 40% in its initial trading, making it a marquee success for one of the original Web 2.0 companies (at least for now).

While we still have to wait for the dust to settle, it’s been a very long road for Dropbox. From starting off as a file-sharing service, to hitting a $10 billion valuation in the middle of a massive hype cycle, to expectations dropping and then the announcement of a $1 billion revenue run rate. Dropbox has been a rollercoaster, but it’s another big moment this afternoon: it’s Y Combinator’s first big IPO. And Y Combinator still has a very deep bench of startups that are, thus far, obvious IPO candidates down the line like Airbnb and Stripe.

That isn’t to take away anything from the work of CEO Drew Houston and the rest of Dropbox’s team, but Y Combinator’s job is to basically take a bunch of shots in the dark based on good ideas and potentially savvy founders. Houston was one of the first of a firm that now takes in a hundred-odd founders per class. Y Combinator Founder and partner Jessica Livingston was there for the start of it, recalling back to the day that Houston rushed to her and Paul Graham to show him his little side project.

We caught up with Livingston this morning ahead of the IPO for a short interview. Here’s the conversation, which was lightly edited for clarity:

TC: Can you tell us a little bit about what it’s like to finally see the first Y Combinator company to go public?

JL: I feel like 13 years ago, it was just this dream of ours. It was this seemingly unattainable dream that goes, ‘maybe one of the startups we fund could go public someday.’ That was the holy grail. It’s an exciting day for Y Combinator. It shows what a long game investing is in early-stage startups. I do feel kind of validated.

TC: How did Y Combinator first end up in touch with Houston?

JL: He applied as a solo founder. We had met Drew the summer before. Back then, we were so small that we always encouraged people to bring friends to a Y Combinator dinner. [Xobni founder Adam Smith] brought [Houston], and we met him then and talked it through. When he applied, we invited him to come to an interview, and Paul [Graham] before the interview reached out to [Houston]. He said, “I see you’re a solo founder, and you should find a cofounder.” Three weeks later Drew showed up with [co-founder Arash Ferdowsi]. It was a great match that worked well.

TC: As Dropbox has grown, what’s stood out to you the most during changes in the market?

JL: They’re a classic example of founders who are programmers who built something to solve their own problem. Clearly, this is a perfect example of that. Drew gets on the bus, he forgets his files, and he can’t work on the whole trip down. He then creates something that will allow him to access files from everywhere. At the time, when he came on the scene with that, there were a lot of companies doing it but none were very good. I feel like Dropbox, regardless of market dynamics, from the very beginning was always dedicated to wanting to do well by building a better solution. They wanted to build one that actually works. I feel like they’ve stuck to that and that’s been driving them since. That’s been their guidepost.

TC: What was your first meeting with Houston like, and do you think he has changed in the past 10 years?

JL: When I first met him, he was young — he was very young — and he was always a good hacker, and very earnest. During Y Combinator he was very focused on building this product and was not distracted by other things. That’s when there were just two people. He’s really evolved over the years as an incredible leader. He’s grown this company and he’s navigated through all different parts of his life cycle. I’ve witnessed his growth as a leader and as a human being. He’s always been a great person. It’s sort of exciting to see where he is now that he’s come a long way, it’s really cool.

TC: Houston and Ferdowsi still own significant portions of the company even after raising a lot of venture capital. Do you think Y Combinator had any effect on companies looking for more founder friendly deals?

JL: I think when Y Combinator started, our goal in many ways was to empower founders. It was to level the playing field. You don’t have to have a connection in Silicon Valley to get funding. You just have to apply on our website. You don’t have to have gone to an Ivy League school. We [try to tell them], don’t let investors take advantage of you because you’re young and have never done this before. In general, times have changed over the past 15 years. Hopefully Y Combinator played a small role in some of those changes in making things a little more found friendly.

TC: What’s one of your favorite stories about Houston?

JL: He was always very calm, cool, and collected under pressure. I remember that was definitely a quality about him. His feathers didn’t get ruffled easily. One of the things I remember most clearly is from that summer when we had demo day. Back then it was, like, 40 people tops. Still, there was a lot of pressure. I remember Paul [Graham] came up with this idea that, ‘hey, Drew, during your demo day you should show people how well Dropbox actually works by deleting your presentation live and restoring it through Dropbox.’ That’s kind of risky, right? To delete your presentation. You’re just standing up there without anything. And he did it and he nailed the presentation. It sounds a little gimmicky, but it really worked and showed his product worked. I remember thinking, like, wow, he’s pretty calm. If it were me I don’t think I could hit the delete button in front of these people. That’s an important quality in someone, not to get flustered.

By the way, we funded them in 2007. If you asked me in 2008 how were they doing, I would say, well, they’re making progress. But it wasn’t like we funded them and we could say, ‘this is gonna be a great one.’ We just knew, yeah they’re making progress, but it’s always hard to know there.

TC: Back then, what were you just expecting? M&A? Did you even anticipate an IPO?

JL: As we were formulating the idea, the hope was rather than going to work at Microsoft — I use them as an example because that was the company back then — and rather than going to get a job out of college, why not build a company and make Microsoft acquire you to get you to work for them? We had low expectations back then. We were hoping there’d be some small acquisitions. But yes, the hope was always acquisitions, but maybe someday in our wildest dreams there’d be an IPO. We didn’t even think YC would work when we started, people didn’t believe in YC’s models for many years.

TC: Looking back, what would you say is one of the biggest things you’ve learned throughout this experience?

JL: What a long road it is for startups. When we started YC back then, it wasn’t a popular thing to do a startup. Now, thank goodness, more people are starting them, and more types of people are starting them. It’s not just super high-tech companies. That’s exciting, but what I think a lot of people don’t realize is how hard startups are. You say, yeah, I know how hard, but people don’t realize how difficult they are and how long the commitment is. If you’re successful, it takes such a long time. For [someone like Houston] to make it to that point, they’ve committed a lot of their life and energy and all their intellectual capacity to making this work. To me, that’s so exciting, but I think it would surprise people to know realistically how long that could take.

TC: What would you tell startups with the hindsight of what happened with Dropbox’s valuation hype cycle?

JL: I will say, with startups, sometimes you just have to stick to what you’re doing. There’s a lot of stuff going on around you, especially now with social media and things like that. With a startup, you just have to keep moving forward with building a company and building a great product.

Powered by WPeMatico

Dropbox today said it is pricing above the range it originally set ahead of its public listing tomorrow, handing the company a valuation inching ever-closer to its original $10 billion valuation.

Dropbox earlier this week said it would price its initial public offering in a range between $18 and $20 per share, settling on a valuation near $8 billion at the high end of the range (or closer to $8.75 billion, based on its fully-diluted share count). With the new pricing, Dropbox will be valuing itself at around $8.4 billion — or a hair above $9 billion based on its fully-diluted share count. That $18 to $20 range, too, was a step up from its original proposed range, which fell between $16 and $18. Dropbox will be raising more than $700 million in the IPO, in addition to existing shareholders selling more than 9 million shares as part of the process.

What all this means is that Dropbox initially tested the waters to gauge interest, and clearly there was a lot. Companies sometimes set conservative price ranges (though this isn’t always the case) and then revise upwards as they see how much interest there is in potential investors buying shares at that price. Dropbox will make its public debut tomorrow, and the usual process here aims to get as much value for the company as possible while still ensuring the so-called IPO “pop” — usually a jump of around 20%. We’ll probably get the formal price in the form of an SEC filing this evening as it gets ready to list tomorrow.

Should that be successful, Dropbox would fall above the valuation of its last financing round, which gave the company a $10 billion valuation amid a hype wave of consumer startups. Dropbox, one of the original pioneers of online storage, in recent years has found itself looking to slowly scoop up more and more enterprise customers as it tries to create a second lucrative line of business. The company deploys a classic playbook of attracting initial customers within teams and then growing up to the point it reaches the C-Suite of companies, though the reverse is certainly possible as Dropbox matures over time.

CNBC first reported the news.

Powered by WPeMatico

Dropbox said it would be increasing its IPO price range – the range for which it will sell its shares for its initial public offering — from $16-$18 per share to $18-$20 per share, giving the company a valuation that could reach close to $8 billion, according to an updated filing with the Securities and Exchange Commission.

Including all shares offered from stockholders selling in this offering, the “greenshoe” and the actual IPO, Dropbox will have a valuation between $7.2 billion and $7.96 billion. Based on a fully-diluted share count, Dropbox’s valuation should land between $7.8 billion to $8.75 billion. It’s below Dropbox’s previous $10 billion valuation, but it’s still a signal that investors are interested in buying up Dropbox’s IPO, which will be the most well-known enterprise name to go public this year. Cloud security company Zscaler went public earlier this month and immediately saw a massive pop, but Dropbox will probably be lumped into a similar boat as Snap as a signal to whether investors are going to be interested in hyped startups.

There will indeed be some shareholders selling stock in this offering, though it looks like for the most part the ownership is going to stay the same. There are a lot of reasons to sell a stock beyond just getting liquidation, such as paying taxes for other share options and exercises, so it’s not clear exactly what the motivations are for some employees for now.

Dropbox has more than 500 million users, 11 million of which are paying users. While originally born as a consumer service, the company has sought to crack into the enterprise in order to help build a robust second line of business to tack alongside its typical consumer operations. Dropbox at the start had the benefit of spreading via word of mouth thanks to its dead-simple interface, but since then has started building out new tools geared toward larger businesses, such as Dropbox Paper.

It’s also what’s made this IPO a somewhat tricky one. The process for this is normally the same, with the company setting a price range and then throwing it out there to see who bites. If things go well, the range goes up. If things go poorly, like the case of Blue Apron, the range is going to drop. This could always change at the last minute, but you can take this as another step toward its eventual listing, which is expected to happen later this week.

Powered by WPeMatico

Zuora, which helps businesses handle subscription billing and forecasting, filed for an initial public offering this afternoon following on the heels of Dropbox’s filing earlier this month.

Zuora’s IPO may signal that Dropbox going public, and seeing a price range that while under its previous valuation seems relatively reasonable, may open the door for coming enterprise initial public offerings. Cloud security company Zscaler also made its debut earlier this week, with the stock doubling once it began trading on the Nasdaq. Zuora will list on the New York Stock Exchange under the ticker “ZUO.” Zuora CEO Tien Tzuo told The Information in October last year that it expected to go public this year.

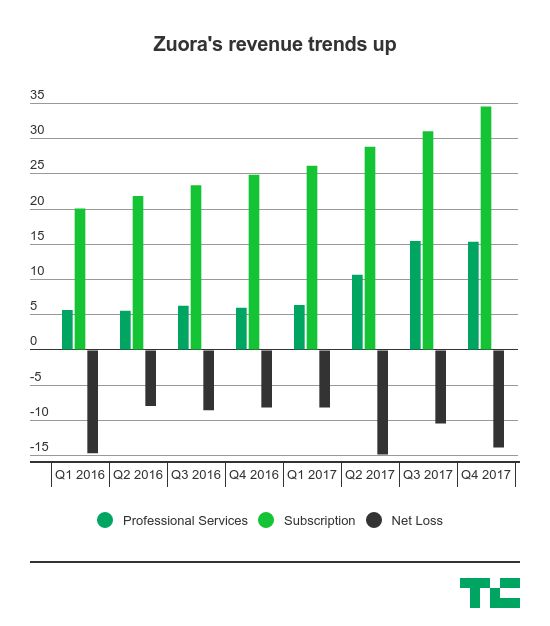

Zuora’s numbers show some revenue growth, with its subscriptions services continue to grow. But its losses are a bit all over the place. While the costs for its subscription revenues is trending up, the costs for its professional services are also increasing dramatically, going from $6.2 million in Q4 2016 to $15.6 million in Q4 2017. The company had nearly $50 million in overall revenue in the fourth quarter last year, up from $30 million in Q4 2016.

But, as we can see, Zuora’s “professional services” revenue is an increasing share of the pie. In Q1 2016, professional services only amounted to 22% of Zuora’s revenue, and it’s up to 31% in the fourth quarter last year. It also accounts for a bigger share of Zuora’s costs of revenue, but it’s an area that it appears to be investing more.

Zuora’s core business revolves around helping companies with subscription businesses — like, say, Dropbox — better track their metrics like recurring revenue and retention rates. Zuora is riding a wave of enterprise companies finding traction within smaller teams as a free product and then graduating them into a subscription product as more and more people get on board. Eventually those companies hope to have a formal relationship with the company at a CIO level, and Zuora would hopefully grow up along with them.

Snap effectively opened the so-called “IPO window” in March last year, but both high-profile consumer IPOs — Blue Apron and Snap — have had significant issues since going public. While both consumer companies, it did spark a wave of enterprise IPOs looking to get out the door like Okta, Cardlytics, SailPoint and Aquantia. There have been other consumer IPOs like Stitch Fix, but for many firms, enterprise IPOs serve as the kinds of consistent returns with predictable revenue growth as they eventually march toward an IPO.

The filing says it will raise up to $100 million, but you can usually ignore that as it’s a placeholder. Zuora last raised $115 million in 2015, and was PitchBook data pegged the valuation at around $740 million, according to the Silicon Valley Business Journal. Benchmark Capital and Shasta Ventures are two big investors in the company, with Benchmark still owning around 11.1% of the company and Shasta Ventures owning 6.5%. CEO Tien Tzuo owns 10.2% of the company.

Powered by WPeMatico

Dropbox is not messing around. Two weeks ago it announced its IPO. Just last week it announced a big partnership with Google and today comes news that it is integrating more deeply with Salesforce. Dropbox and Salesforce have danced a bit in the past as cloud companies tend to do, but today’s announcement is a bit broader. It involves having Dropbox folders embedded in Salesforce… Read More

Dropbox is not messing around. Two weeks ago it announced its IPO. Just last week it announced a big partnership with Google and today comes news that it is integrating more deeply with Salesforce. Dropbox and Salesforce have danced a bit in the past as cloud companies tend to do, but today’s announcement is a bit broader. It involves having Dropbox folders embedded in Salesforce… Read More

Powered by WPeMatico

It’s been an eventful week for Dropbox coming off its announcement last Friday that it was finally going public, but that doesn’t mean the business stops. The company announced plans to partner with Google today to bring native G Suite integration to Dropbox storage. The fact is that more than 50 percent of Dropbox users have a G Suite account — which includes GMail along… Read More

It’s been an eventful week for Dropbox coming off its announcement last Friday that it was finally going public, but that doesn’t mean the business stops. The company announced plans to partner with Google today to bring native G Suite integration to Dropbox storage. The fact is that more than 50 percent of Dropbox users have a G Suite account — which includes GMail along… Read More

Powered by WPeMatico

It’s official, the Dropbox IPO filing is here. Going public is a huge milestone for Dropbox and has been one of the most anticipated tech IPOs for several years now. We knew that it had already filed confidentially, but the company has now unveiled its filing, meaning the actual IPO is likely very soon, probably late March. Read More

It’s official, the Dropbox IPO filing is here. Going public is a huge milestone for Dropbox and has been one of the most anticipated tech IPOs for several years now. We knew that it had already filed confidentially, but the company has now unveiled its filing, meaning the actual IPO is likely very soon, probably late March. Read More

Powered by WPeMatico

As Dropbox continues its inevitable march toward an IPO, it’s going to look to bring in people with a lot of experience handling the operations of larger public companies — and it’s getting one today. Dropbox today said it is adding former Nike CFO Don Blair to the company’s board of directors. Blair will be joining the audit committee, the company said, and comes in with… Read More

As Dropbox continues its inevitable march toward an IPO, it’s going to look to bring in people with a lot of experience handling the operations of larger public companies — and it’s getting one today. Dropbox today said it is adding former Nike CFO Don Blair to the company’s board of directors. Blair will be joining the audit committee, the company said, and comes in with… Read More

Powered by WPeMatico

The team behind Verst is joining Dropbox, in an acquisition that marks the end of the Verst publishing platform. The startup actually started life as DWNLD, a platform that transformed websites into mobile apps. It raised a $12 million Series A led by Grelock Partners before shifting focus to Verst, which launched earlier this year as a blogging platform that has traffic and revenue… Read More

The team behind Verst is joining Dropbox, in an acquisition that marks the end of the Verst publishing platform. The startup actually started life as DWNLD, a platform that transformed websites into mobile apps. It raised a $12 million Series A led by Grelock Partners before shifting focus to Verst, which launched earlier this year as a blogging platform that has traffic and revenue… Read More

Powered by WPeMatico

Dropbox announced a couple of products today to make it easier for Autodesk users to access and share large design files. The products include an integrated desktop app for opening and saving Autodesk files stored in Dropbox and an app for viewing design files without the need for owning Autodesk. These products are long overdue given that Dropbox’s Ross Piper, who is head of ecosystem… Read More

Powered by WPeMatico