Dropbox

Auto Added by WPeMatico

Auto Added by WPeMatico

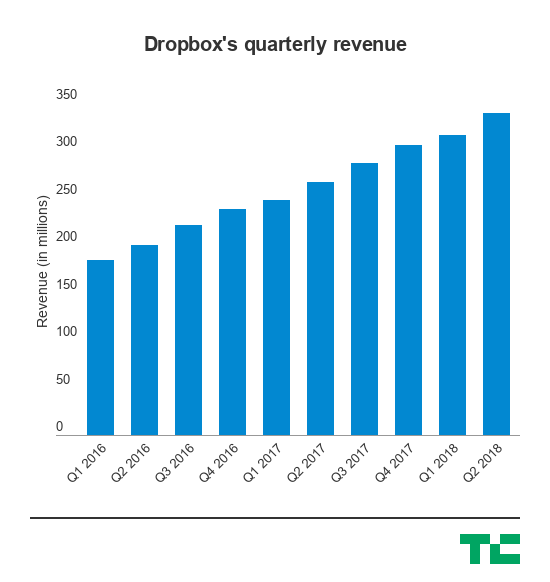

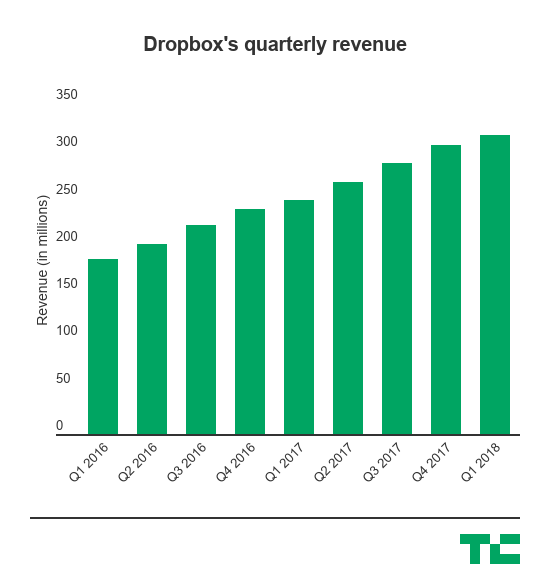

Back when Dennis Woodside joined Dropbox as its chief operating officer more than four years ago, the company was trying to justify the $10 billion valuation it had hit in its rapid rise as a Web 2.0 darling. Now, Dropbox is a public company with a nearly $14 billion valuation, and it once again showed Wall Street that it’s able to beat expectations with a now more robust enterprise business alongside its consumer roots.

Dropbox’s second quarter results came in ahead of Wall Street’s expectations on both the earnings and revenue front. The company also announced that Dennis Woodside will be leaving the company. Woodside joined at a time when Dropbox was starting to figure out its enterprise business, which it was able to grow and transform into a strong case for Wall Street that it could finally be a successful publicly traded company. The IPO was indeed successful, with the company’s shares soaring more than 40 percent in its debut, so it makes sense that Woodside has essentially accomplished his job by getting it into a business ready for Wall Street.

“I think as a team we accomplished a ton over the last four and a half years,” Woodside said in an interview. “When I joined they were a couple hundred million in revenue and a little under 500 people. [CEO] Drew [Houston] and Arash [Ferdowsi] have built a great business, since then we’ve scaled globally. Close to half our revenue is outside the U.S., we have well over 300,000 teams for our Dropbox business product, which was nascent there. These are accomplishments of the team, and I’m pretty proud.”

The stock initially exploded in extended trading by rising more than 7 percent, though even prior to the market close and the company reporting its earnings, the stock had risen as much as 10 percent. But following that spike, Dropbox shares are now down around 5 percent. Dropbox is one of a number of SaaS companies that have gone public in recent months, including DocuSign, that have seen considerable success. While Dropbox has managed to make its case with a strong enterprise business, the company was born with consumer roots and has tried to carry over that simplicity with the enterprise products it rolls out, like its collaboration tool Dropbox Paper.

Here’s a quick rundown of the numbers:

So, not only is Dropbox able to show that it can continue to grow that revenue, the actual value of its users is also going up. That’s important, because Dropbox has to show that it can continue to acquire higher-value customers — meaning it’s gradually moving up the Fortune 100 chain and getting larger and more established companies on board that can offer it bigger and bigger contracts. It also gives it the room to make larger strategic moves, like migrating onto its own architecture late last year, which, in the long run could turn out to drastically improve the margins on its business.

“We did talk earlier in the quarter about our investment over the last couple years in SMR technology, an innovative storage technology that allows us to optimize cost and performance,” Woodside said. “We continue to innovate ways that allow us to drive better performance, and that drives better economics.”

The company is still looking to make significant moves in the form of new hires, including recently announcing that it has a new VP of product and VP of product marketing, Adam Nash and Naman Khan, respectively. Dropbox’s new team under CEO Drew Houston are tasked with continuing the company’s path to cracking into larger enterprises, which can give it a much more predictable and robust business alongside the average consumers that pay to host their files online and access them from pretty much anywhere.

In addition, there are a couple executive changes as Woodside transitions out. Yamini Rangan, currently VP of Business Strategy & Operations, will become Chief Customer Officer reporting to Houston, and comms VP Lin-Hua Wu will also report to Houston.

Dropbox had its first quarterly earnings check-in and slid past the expectations that Wall Street had, though its GAAP gross margin slipped a little bit and may have offered a slight negative signal for the company. But since then, Dropbox’s stock hasn’t had any major missteps, giving it more credibility on the public markets — and more resources to attract and retain talent with compensation packages linked to that stock.

“Our retention has been quite strong,” Woodside said. “We see strong retention characteristics across the customer set we have, whether it’s large or small. Obviously larger companies have more opportunity to expand over time, so our expansion metrics are quite strong in customers of over several hundred employees. But even among small businesses, Dropbox is the kind of product that has gravity. Once you start using it and start sharing it, it becomes a place where your business is small or large is managing all its content, it tends to be a sticky experience.”

Powered by WPeMatico

After a largely successful IPO, Dropbox is adding another couple of hires today as it looks to continue its consumer-slash-enterprise growth playbook: bringing on a new VP of product in former CEO and president of Wealthfront Adam Nash; and a new VP of product marketing and global campaigns in Naman Khan.

Both have extensive experience from products that span multiple different verticals, with Nash previously working at LinkedIn and eBay and Khan spending time with Microsoft Office and Autodesk. The company went public earlier this year to a pretty successful IPO, though the stock hasn’t seen any dramatic fireworks, and has accumulated more than 500 million registered users in its decade-plus life. But it’s also gone through a kind of transition as it starts expanding into more enterprise-focused collaboration tools as it looks to woo businesses, which represent a substantial opportunity for growth for the company that started off as a dead-simple file-sharing service.

Previously an entrepreneur-in-residence for Greylock, Nash is now going to oversee a wide range of products that span consumer-focused file storage and sharing services all the way up to its Google Docs competitor Paper — each of which has a kind of consumer-born aesthetic that’s targeting use cases within enterprises, whether that’s building tools to get documents into its service or to actually helping teams spec out products within a kind of continuous document like Paper. But as it focuses on simplicity, Dropbox has to take care not to end up feature-creeping its way out of what made it successful initially, so the final product decisions may be a bit different. Naman will also inherit that challenge of marketing a consumer-oriented product that’s targeting businesses.

As Dropbox looks to continue to mature as a public company, it has to ensure that it still brings on talent that understands where it’s going now as it tries to wrangle larger enterprise customers that have a complex set of needs beyond just the typical consumer. Going public certainly helps with that credibility a little bit, but it’s hires like these that will determine what kinds of products actually make it out the door and the messaging that goes with them — and whether larger enterprises will actually adopt them.

Powered by WPeMatico

Dropbox announced several enhancements today designed to beef up its mobile offering and help employees on the go keep up with changes to files stored in Dropbox .

In a typical team scenario, a Dropbox user shared a file with a team member for review or approval. If they wanted to check the progress of this process, the only way to do it up until now was to send an email or text message explicitly asking if the person looked at it yet — not a terribly efficient workflow.

Dropbox recognized this and has built in a fix in the latest mobile release. Now users can can simply see who has looked at or taken action on a file directly from the mobile application without having to leave the application.

In addition, those being asked to review files can see those notifications right at the top of the Home screen in the mobile app, making the whole feedback cycle much more organized.

Photo: Dropbox

Joey Loi, product manager at Dropbox says this is a much more streamlined way to understand activity inside of Dropbox. “With this feature, we think about the closing loop on collaboration. At its heart, collaboration is feedback flows. When I change something on a file, there are a few steps before [my co-worker] knows I’ve changed it,” Loi explained. With this feature that feedback loop can close much faster.

The company also changed the way it organizes and displays files putting the files that you opened most recently at the top of the Home screen, which is somewhat like Recents in Google Drive. It also provides a way to favorite a file and puts those files that are most important at the top of the list, making it easier to find the files that are likely most important to you more quickly when you access the mobile app.

Finally you can now drag and drop a file from an email into a Dropbox folder in a mobile context.

While none of these individual updates are earth shattering changes by any means, they do make it easier for users to access, share and work with files in Dropbox on a mobile device. “All the features are to help teams collaborate and be efficient on mobile,” Loi said.

Powered by WPeMatico

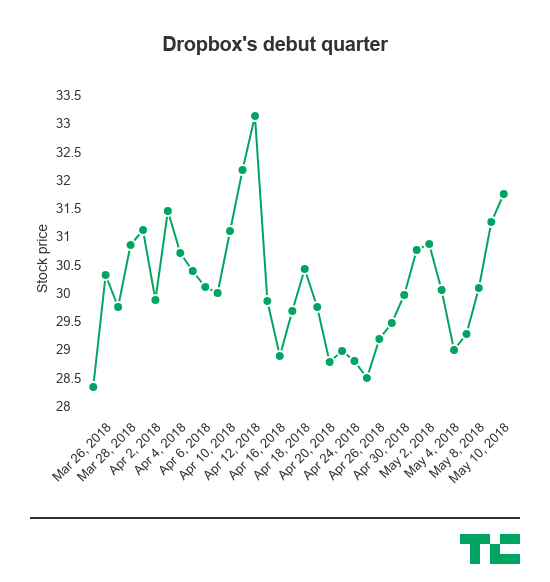

Dropbox made its debut as a public company earlier this year and today passed through its first milestone of reporting its results to public investors, and it more or less beat expectations set for Wall Street on the top and bottom line.

The company reported more revenue and beat expectations for earnings that Wall Street set, bringing in $316.3 million in revenue and appearing to pick up momentum among its paying user base. It also said it had 11.5 million paying users, a jump from last year. However, the stock was largely flat in extended trading. One small negative signal — and it definitely appears to be a small one — was that its GAAP gross margin slipped slightly to 61.9% from 62.3% a year earlier. Dropbox is a software company that’s supposed to have great margins as it begins to ramp up its own hardware, but that slipping margin may end up being something that investors will zero in on going forward. Still, as the company continues to ramp up the enterprise component of its business, the calculus of its business may change over time.

This is a pretty important moment for the company, as it was a darling in Silicon Valley and rocketed to a $10 billion valuation in the early phases of the Web 2.0 era but began to face a ton of criticism as to whether it could be a robust business as larger companies started to offer cloud storage as a perk and not a business. Dropbox then found itself going up against companies like Box and Microsoft as it worked to create an enterprise business, but all this was behind closed doors — and it wasn’t clear if it was able to successfully maneuver its way into a second big business. Now the company is beholden to public shareholders and has to show all this in the open, and it serves as a good barometer of not just storage and collaboration businesses, but also some companies that are looking to drastically simplify workflow processes and convert that into a real business (like Slack, for example).

Here’s the final scorecard for the company:

(The GAAP and non-GAAP comparison is typically related to share-based compensation, which is a key component of employee compensation and retention.)

Dropbox was largely considered to be a successful IPO, rising more than 40% in its trading debut. That does mean that it may have left some money on the table, but its operating losses have been largely stable, even as it looks to woo larger enterprise customers as it — which is a bit of a taller order than its typical growth amid consumers that’s heavily driven by organic growth. Those larger enterprise customers offer more stable, and larger, revenue streams than a consumer base that faces a variety of options as many companies start to offer free storage. The company is now worth well over that original $10 billion valuation as a public company. Dropbox says it has more than 500 million users.

Since going public, the stock has had its ups and downs, but for the most part hasn’t dipped below that significant jump it saw from day one. Keeping that number propped up — and growing — is an important part of growing a business as a public company as it waves off more intense scrutiny and pressure for change from public shareholders, as well as offering competitive compensation packages for incoming employees in order to attract the best talent. It’s also good for morale as it offers a kind of grade for how the company is doing in the eyes of the public, though CEOs of companies often say they are committed toward long-term goals. The company’s shares are up around 11% since going public.

While there have been a wave of enterprise IPOs this year, including zScalar and Pluralsight’s upcoming IPO, Dropbox was largely considered to be a potential gauge of whether the IPO window was still open this year because of its hybrid nature. Dropbox started off as a consumer company based around a dead-simple approach of hosting and sharing files online, and used that to build a massive user base even as the cost of cloud storage was rapidly commoditized. But it also is building a robust enterprise-focus business, and continues to roll out a variety of tools to woo those businesses with consistent updates to products like its document tool Paper. Last month, the company started rolling out templates, as it looked to make traditional workflow processes easier and easier for companies in order to capture their interest much in the same way it captured the interest of consumers at large.

Powered by WPeMatico

Why has San Francisco’s startup scene generated so many hugely valuable companies over the past decade?

That’s the question we asked over the past few weeks while analyzing San Francisco startup funding, exit, and unicorn creation data. After all, it’s not as if founders of Uber, Airbnb, Lyft, Dropbox and Twitter had to get office space within a couple of miles of each other.

We hadn’t thought our data-centric approach would yield a clear recipe for success. San Francisco private and newly public unicorns are a diverse bunch, numbering more than 30, in areas ranging from ridesharing to online lending. Surely the path to billion-plus valuations would be equally varied.

But surprisingly, many of their secrets to success seem formulaic. The most valuable San Francisco companies to arise in the era of the smartphone have a number of shared traits, including a willingness and ability to post massive, sustained losses; high-powered investors; and a preponderance of easy-to-explain business models.

No, it’s not a recipe that’s likely replicable without talent, drive, connections and timing. But if you’ve got those ingredients, following the principles below might provide a good shot at unicorn status.

First, lose money until you’ve left your rivals in the dust. This is the most important rule. It is the collective glue that holds the narratives of San Francisco startup success stories together. And while companies in other places have thrived with the same practice, arguably San Franciscans do it best.

It’s no secret that a majority of the most valuable internet and technology companies citywide lose gobs of money or post tiny profits relative to valuations. Uber, called the world’s most valuable startup, reportedly lost $4.5 billion last year. Dropbox lost more than $100 million after losing more than $200 million the year before and more than $300 million the year before that. Even Airbnb, whose model of taking a share of homestay revenues sounds like an easy recipe for returns, took nine years to post its first annual profit.

Not making money can be the ultimate competitive advantage, if you can afford it.

Industry stalwarts lose money, too. Salesforce, with a market cap of $88 billion, has posted losses for the vast majority of its operating history. Square, valued at nearly $20 billion, has never been profitable on a GAAP basis. DocuSign, the 15-year-old newly public company that dominates the e-signature space, lost more than $50 million in its last fiscal year (and more than $100 million in each of the two preceding years). Of course, these companies, like their unicorn brethren, invest heavily in growing revenues, attracting investors who value this approach.

We could go on. But the basic takeaway is this: Losing money is not a bug. It’s a feature. One might even argue that entrepreneurs in metro areas with a more fiscally restrained investment culture are missing out.

What’s also noteworthy is the propensity of so many city startups to wreak havoc on existing, profitable industries without generating big profits themselves. Craigslist, a San Francisco nonprofit, may have started the trend in the 1990s by blowing up the newspaper classified business. Today, Uber and Lyft have decimated the value of taxi medallions.

Not making money can be the ultimate competitive advantage, if you can afford it, as it prevents others from entering the space or catching up as your startup gobbles up greater and greater market share. Then, when rivals are out of the picture, it’s possible to raise prices and start focusing on operating in the black.

You can’t lose money on your own. And you can’t lose any old money, either. To succeed as a San Francisco unicorn, it helps to lose money provided by one of a short list of prestigious investors who have previously backed valuable, unprofitable Northern California startups.

It’s not a mysterious list. Most of the names are well-known venture and seed investors who’ve been actively investing in local startups for many years and commonly feature on rankings like the Midas List. We’ve put together a few names here.

You might wonder why it’s so much better to lose money provided by Sequoia Capital than, say, a lower-profile but still wealthy investor. We could speculate that the following factors are at play: a firm’s reputation for selecting winning startups, a willingness of later investors to follow these VCs at higher valuations and these firms’ skill in shepherding portfolio companies through rapid growth cycles to an eventual exit.

Whatever the exact connection, the data speaks for itself. The vast majority of San Francisco’s most valuable private and recently public internet and technology companies have backing from investors on the short list, commonly beginning with early-stage rounds.

Generally speaking, you don’t need to know a lot about semiconductor technology or networking infrastructure to explain what a high-valuation San Francisco company does. Instead, it’s more along the lines of: “They have an app for getting rides from strangers,” or “They have an app for renting rooms in your house to strangers.” It may sound strange at first, but pretty soon it’s something everyone seems to be doing.

It’s not a recipe that’s likely replicable without talent, drive, connections and timing.

A list of 32 San Francisco-based unicorns and near-unicorns is populated mostly with companies that have widely understood brands, including Pinterest, Instacart and Slack, along with Uber, Lyft and Airbnb. While there are some lesser-known enterprise software names, they’re not among the largest investment recipients.

Part of the consumer-facing, high brand recognition qualities of San Francisco startups may be tied to the decision to locate in an urban center. If you were planning to manufacture semiconductor components, for instance, you would probably set up headquarters in a less space-constrained suburban setting.

While it can be frustrating to watch a company lurch from quarter to quarter without a profit in sight, there is ample evidence the approach can be wildly successful over time.

Seattle’s Amazon is probably the poster child for this strategy. Jeff Bezos, recently declared the world’s richest man, led the company for more than a decade before reporting the first annual profit.

These days, San Francisco seems to be ground central for this company-building technique. While it’s certainly not necessary to locate here, it does seem to be the single urban location most closely associated with massively scalable, money-losing consumer-facing startups.

Perhaps it’s just one of those things that after a while becomes status quo. If you want to be a movie star, you go to Hollywood. And if you want to make it on Wall Street, you go to Wall Street. Likewise, if you want to make it by launching an industry-altering business with a good shot at a multi-billion-dollar valuation, all while losing eye-popping sums of money, then you go to San Francisco.

Powered by WPeMatico

As Dropbox looks to woo larger and larger businesses with its strategy of building simpler collaboration tools than what’s on the market, it’s making some moves in its online document tool Paper to further reduce that friction today.

Dropbox said it was rolling out a new tool for Dropbox Paper that allows users to get a paper document up and running through a set of templates. It may seem like something that would be table stakes for a company looking to create an online document tool like Google Docs, but figuring out what Paper’s core use cases look like can take a lot of thinking and user research before finally pulling the trigger. Dropbox at its heart hopes to have a consumer feel for its products, so preserving that as it looks to build more robust tools presents a bigger challenge for the freshly-public company.

The templates tool behaves pretty much like other tools out there: you open Dropbox Paper, and you’ll get the option to create a document from a number of templates. Some common use cases for Dropbox Paper include continuous product development timelines and design specs, but it seems the company hopes to broaden that by continuing to integrate new features like document previews. Dropbox Paper started off as a blank slate, but given the number of options out there, it has to figure out a way to differentiate itself eventually.

The company said it’s also rolling out a number of other small features. That includes a way to pin documents, launch presentations, format text and insert docs and stickers. There’s also a new meeting widget and increased formatting options in the comments section in Paper. Finally, it’s adding a number of small quality-of-life updates like viewing recent Paper docs by alphabetical order and the ability to unsubscribe to comment notifications and archive docs on iOS, as well as aggregating to-do lists across docs.

Dropbox went public earlier this year to dramatic success, immediately getting that desired “pop” and more or less holding it throughout the past month or so as one of the first blockbuster IPOs of 2018. There have been a wave that have followed since, including DocuSign, and it’s one of a batch of several enterprise companies looking to get out the door now that it appears the window is open for investor demand for fresh IPOs.

Paper, to that end, appears to be a key piece of the puzzle for Dropbox. The company has always sought to be a company centered around simple collaboration tools, coming from its roots as a consumer company to start. It’s an approach that has served it — and others, like Slack — well as the company looks to expand more and more into larger enterprises. While it’s been able to snap up users thanks to its simpler approach, those enterprise deals are always more lucrative and serve as a stronger business line for Dropbox.

Dropbox will have to continue to not only differentiate itself from Google Docs and other tools, but also an emerging class of startups that’s looking to figure out ways to snap up some of the core use cases of online document tools. Slite, for example, hopes to capture the internal wiki and note-taking portion of an online doc system like Google Docs. That startup raised $4.4 million earlier this month. There’s also Coda, a startup that’s looking to rethink what a document looks altogether, which raised $60 million. Templates are one way of reducing that friction and keeping it feeling like a simple document tool and hopefully getting larger businesses excited about its products.

Powered by WPeMatico

Dropbox is a critically important tool for more than 500 million people, which is why we’re so excited to have founder and CEO Drew Houston on the Disrupt stage in September.

Dropbox launched back in 2007 and Houston has spent the last decade growing Dropbox to the behemoth it is today.

During that time, Houston has made some tough decisions.

A few years ago, Houston decided to move the Dropbox infrastructure off of AWS. In 2014, Houston chose to raise $500 million in debt financing to keep up pace with Box, which was considering an IPO at the time. And in March 2017, Dropbox took another $600 million in debt financing from JP Morgan.

Houston also reportedly turned down a nine-figure acquisition offer from Apple.

All the while, Houston led Dropbox to be cash-flow positive and grew the company to see a $1 billion revenue run rate as of last year.

And, of course, we can’t forget the decision to go public earlier this year.

Interestingly, Houston first told his story to a TechCrunch audience at TC50 in 2008 as part of the Startup Battlefield. In fact, you can check out the original pitch from TC50 right here.

At Disrupt SF in September, we’re excited to sit down with Houston to discuss his journey thus far, the decision to go public and the future of Dropbox.

The show runs from September 5 to September 7, and for the next week, our super early-bird tickets are still available.

Powered by WPeMatico

Dropbox’s surge on the stock market has continued, with the company going up another 7 percent on its second day on the stock market.

The company saw its shares close at $30.45, giving the company above a $13 billion market cap, fully diluted.

When it priced its IPO, there was a question as to whether Dropbox would surpass the $10 billion valuation it achieved in its last private round. It eliminated those concerns overnight.

The first few days have been a strong indicator of investor demand for the cloud storage company.

To recap, Dropbox initially hoped to price its IPO between $16 and $18, then raised it from $18 to $20. Then it ultimately priced its IPO at $21, closing the day above $28. And it still continues to go up.

Bankers price IPOs to “pop” or go up about 20 percent on the first day. The surge implies that Dropbox exceeded Wall Street’s expectations. It also means that Dropbox could have priced its shares higher and raised more money.

It priced shares at $21, raising $756 million. If Dropbox had priced shares at $24, it would have raised $864 million and new investors would have still seen big gains.

It was certainly a win for stock market investors, which like the company’s improving financials.

It brought in $1.1 billion in revenue in its most recent year. This is up from $845 million in revenue the year before and $604 million for 2015.

Yet while it’s been cash flow positive since 2016, it is not profitable. Dropbox lost nearly $112 million last year. But its margins are looking better when compared with losses of $210 million for 2016 and $326 million for 2015.

Monday was a good day on the stock market in general. The Dow surged 600 points, partly due to gains from tech stocks like Microsoft and Apple.

Co-founder and CEO Drew Houston is the largest shareholder, owning 25.3 percent of the company ahead of its IPO. Sequoia Capital owned 23.2 percent of Dropbox.

Although Dropbox is very different from Spotify, which intends to list next week, investors will view this favorable debut as a sign that the IPO window is “open,” meaning that there is strong demand for newly public tech companies.

Zuora, Pivotal and Smartsheet also unveiled IPO filings recently, suggesting that they will go public in April. And we broke the news that DocuSign’s IPO is coming up.

The last few years have been slow for tech IPOs, but experts are hoping that this year will be different. John Tuttle, global head of listings at the New York Stock Exchange, says he expects “a strong year if market conditions hold constant.”

Powered by WPeMatico

Dropbox went public this morning to great fanfare, with the stock shooting up more than 40% in the initial moments of trading as the enterprise-slash-consumer company looked to convince investors that it could be a viable publicly-traded company.

And for one that Steve Jobs famously called a feature, and not a company, it certainly was an uphill battle to convince the world that it was worth even the $10 billion its last private financing round set. It’s now worth more than that, but that follows a long series of events, including an increased focus on enterprise customers and finding ways to make its business more efficient — like installing their own infrastructure. Dropbox CEO Drew Houston acknowledged a lot of this, as well as the fact that it’s going to continue to face the challenge of ensuring that its users and enterprises will trust Dropbox with some of their most sensitive files.

We spoke with Houston on the day of the IPO to talk a little bit about what it took to get here during the road show and even prior. Here’s a lightly-edited transcript of the conversation:

TC: In light of the problems that Facebook has had surrounding user data and user trust, how has that changed how you think about security and privacy as a priority?

DH: Our business is built on our customers’ trust. Whether we’re private or public, that’s super important to us. I think, to our customers, whether we’re private or public doesn’t change their view. I wouldn’t say that our philosophy changes as we get to bigger and bigger scale. As you can imagine we make big investments here. We have an awesome security team, our first cultural principle is be worthy of trust. This is existential for us.

TC: How’s the vibe now that longtime employees are going to have an opportunity to get rewarded for their work now that you’re a public company?

DH: I think everyone’s just really excited. This is the culmination of a lot of hard work by a lot of people. We’re really proud of the business we’ve built. I mean, building a great company or doing anything important takes time.

TC: Was there something that changed that convinced you to go public after more than a decade of going private, and how do you feel about the pop?

DH: We felt that we were ready. Our business was in great shape. We had a good balance of scale and profitability and growth. As a private company, there are a lot of reasons why it’s been easier to stay private for longer. We’re all proud of the business we’ve built. We see the numbers. We think we’re on to not just a great business, but pioneering a whole new model. We’re taking the best of our consumer roots, combining them with the best parts of software as a service, and it was really gratifying to see investors be excited about it and for the rest of the world to catch on.

TC: As you were on your road show, what were some of the big questions investors were asking?

DH: We don’t fit neatly into any one mold. We’re not a consumer company, and we’re not a traditional enterprise company. We’re basically taking that consumer internet playbook and applying it to business software, combining the virality and scale. Over the last couple years, as we’ve been building that engine, investors are starting to understand that we don’t fit into a traditional mold. The numbers speak to themselves, they can appreciate the unusual combination.

TC: What did you tell them to convince them?

DH: We’re just able to get adoption. Just the fact that we have hundreds of millions of users and we’ve found Dropbox is adopted in millions of companies [was enough evidence]. More than 300,000 of those users are Dropbox Business companies. We spend about half on sales of marketing as a percentage of revenue of a typical software as a service company. Efficiency and scale are the distinctive elements, and investors zero in on that. To be able to acquire customers at that scale and also really efficiently, that’s what makes us stand out. They’ve seen Atlassian be successful with self-serve products, but you can layer on top of that leveraging our freemium and viral elements and our focus on design and building great products.

TC: How do you think about deploying the capital you’ve picked up from the IPO?

DH: So, we’re public because they wanted us to be a public company. But our approach is still the same. First, it’s about getting the best talent in the building and making sure we build the best products, and if you do those things, make sure customers are happy, that’s what works.

TC: What about recruiting?

DH: It’s a big day for dropbox. We’re all really excited about it and hopefully a lot of other people are too.

TC: When you look at your customer acquisition ramp, what does that look like?

DH: I mean, we’ve been making a lot of progress in the past couple of years if you look at growth in subscribers. That will continue. We look at numbers, we have 11 million subscribers, 80% use dropbox for work. But at the same time, we look at the world, there’s 1 billion knowledge workers and growing. We’re not gonna run out of people who need Dropbox.

TC: What about convincing investors about the consumer part of the business? How did you do that?

DH: I think, when you explain that our consumer and cloud storage roots have really become a way for us to efficiently acquire business customers at scale, that helps them understand. Second, it’s easy to focus on how in the consumer realm that the business has been commoditized. There’s all this free space and all this competition. On the other hand, we’ve never lowered prices, we’ve never even given more free space, we know that what our customers really value is the sharing and collaboration, not just the storage. It’s been good to move investors beyond the 2010 understanding of our business.

TC: How did creating your own infrastructure play into your readiness to go public?

DH: When I say that today is the culmination of a lot of events, that’s a great example. We made a many-year investment to migrate off the public cloud. Certainly that was one of the more eye-popping investors watching our gross margins literally double over the last couple of years from burning cash to being cash flow positive. We’ll continue reaching larger and larger scale, and those investments will.

TC: Getting a new guitar any time soon?

DH: I probably should.

Powered by WPeMatico

Dropbox was off to the races on its first day as a public company.

It’s surely a sign of public investor enthusiasm for the cloud storage business, which had initially hoped to price its IPO between $16 and $18, then raised it from $18 to $20.

It also means that Dropbox closed well above the $10 billion it was valued at its last private round. Its market cap is now above $12 billion, fully diluted.

Dropbox brought in $1.1 billion in revenue for the last year. This compares to $845 million in revenue the year before and $604 million for 2015.

While it’s been cash flow positive since 2016, it is not yet profitable, having lost nearly $112 million last year. But it has significantly improved margins when compared to losses of $210 million for 2016 and $326 million for 2015.

Its average revenue per paying user is $111.91.

There has been a debate about whether to value Dropbox, which has a freemium model, as a consumer company or an enterprise business. It has convinced just 11 million of its 500 million registered customers to pay for its services.

Dropbox “combines the scale and virality of a consumer company with the recurring revenue of a software company,” said Bryan Schreier, a partner at Sequoia Capital and board member at the company. He said that now was the time for Dropbox to list because “the business had reached a level of scale and also cash flow that warranted a public debut.”

He also talked about the early days of Dropbox pitching at a TechCrunch event in 2008 and how disappointed they were that the slides stopped working during the presentation. We have footage of that here.

Sequoia Capital owned 23.2 percent of the overall shares outstanding at the time of the IPO. They shared Dropbox’s original seed pitch from 2007.

Accel was the next largest shareholder, owning 5 percent overall. Sameer Gandhi made the investment at Sequoia and then invested in Dropbox again when he went over to Accel.

Founder and CEO Drew Houston owned 25.3 percent of the company.

Greylock Partners also had a small stake. John Lilly, a general partner there, said he “invested in Dropbox because Drew and the team had an exceptionally clear vision of what the future of work would look like and built a product that would meet the demands of the modern workforce.”

But there are quite a few other businesses with similar products to Dropbox. The prospectus warned of the competitive landscape.

“The market for content collaboration platforms is competitive and rapidly changing. Certain features of our platform compete in the cloud storage market with products offered by Amazon, Apple, Google, and Microsoft, and in the content collaboration market with products offered by Atlassian, Google, and Microsoft. We compete with Box on a more limited basis in the cloud storage market for deployments by large enterprises.”

Note that it downplayed its competition with Box, a company that’s often mentioned in the same sentence as Dropbox. While the products are similar, the two have different business models and Dropbox was hoping that this would be respected with a better revenue multiple. If the first day is any indication, it looks like that strategy worked.

The company listed on the Nasdaq, under the ticker “DBX.”

We talked about Dropbox’s first day and the outlook for upcoming public debuts like Spotify on our “Equity” podcast episode below. We were joined by Eric Kim, managing partner at Goodwater Capital. He authored a research report here.

Powered by WPeMatico