Dell

Auto Added by WPeMatico

Auto Added by WPeMatico

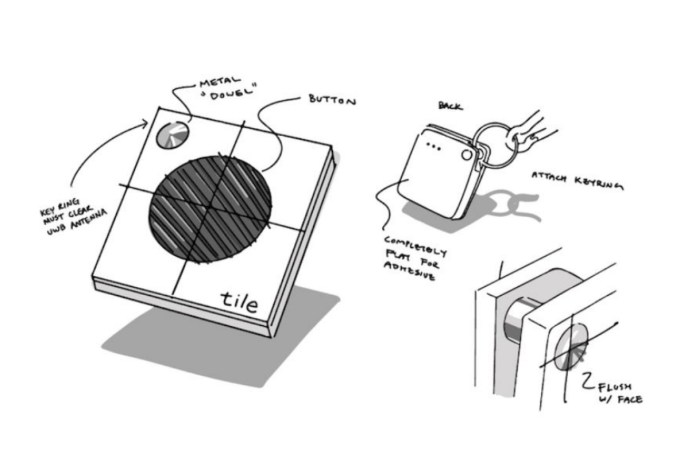

Tile, the maker of Bluetooth-powered lost item finder beacons and, more recently, a staunch Apple critic, announced today it has raised $40 million in non-dilutive debt financing from Capital IP. The funding will be put toward investment in Tile’s finding technologies, ahead of the company’s plan to unveil a new slate of products and features that the company believes will help it to better compete with Apple’s AirTags and further expand its market.

The company has been a longtime leader in the lost item finder space, offering consumers small devices they can attach to items — like handbags, luggage, bikes, wallets, keys and more — which can then be tracked using the Tile smartphone app for iOS or Android. When items go missing, the Tile app leverages Bluetooth to find the items and can make them play a sound. If the items are further afield, Tile taps into its broader finding network consisting of everyone who has the app installed on their phone and other access points. Through this network, Tile is able to automatically and anonymously communicate the lost item’s location back to its owner through their own Tile app.

Image Credits: Tile

Tile has also formed partnerships focused on integrating its finding network into over 40 different third-party devices, including those across audio, travel, wearables and PC categories. Notable brand partners include HP, Dell, Fitbit, Skullcandy, Away, Xfinity, Plantronics, Sennheiser, Bose, Intel and others. Tile says it’s seen 200% year-over-year growth on activations of these devices with its service embedded.

To date, Tile has sold more than 40 million devices and has over 425,000 paying customers — a metric it’s revealing for the first time. It doesn’t disclose its total number of users, both free and paid combined, however. During the first half of 2021, Tile says revenues increased by over 50%, but didn’t provide hard numbers.

While Tile admits that the COVID-19 pandemic had some impacts on international expansions, as some markets have been slower to rebound, it has still seen strong performance outside the U.S., and considers that a continued focus.

The pandemic, however, hasn’t been Tile’s only speed bump.

When Apple announced its plans to compete with the launch of AirTags, Tile went on record to call it unfair competition. Unlike Tile devices, Apple’s products could tap into the iPhone’s U1 chip to allow for more accurate finding through the use of ultra-wideband technologies available on newer iPhone models. Tile, meanwhile, has plans for its own ultra-wideband-powered device, but hadn’t been provided the same access. In other words, Apple gave its own lost item finder early, exclusive access to a feature that would allow it to differentiate itself from the competition. (Apple has since announced it’s making ultra-wideband APIs available to third-party developers, but this access wasn’t available from day one of AirTag’s arrival.)

Image Credits: Tile internal concept art

Tile has been vocal on the matter of Apple’s anti-competitive behavior, having testified in multiple congressional hearings alongside other Apple critics, like Spotify and Match. As a result of increased regulatory pressure, Apple later opened up its Find My network to third-party devices, in an effort to placate Tile and the other rivals its AirTags would disadvantage.

But Tile doesn’t want to route its customers to Apple’s first-party app — it intends to use its own app in order to compete based on its proprietary features and services. Among other things, this includes Tile’s subscriptions. A base plan is $29.99 per year, offering features like free battery replacement, smart alerts and location history. A $99.99 per year plan also adds insurance of sorts — it pays up to $1,000 per year for items it can’t find. (AirTag doesn’t do that.)

Despite its many differentiators, Tile faces steep competition from the ultra-wideband-capable AirTags, which have the advantage of tapping into Apple’s own finding network of potentially hundreds of millions of iPhone owners.

However, Tile CEO CJ Prober — who joined the company in 2018 — claims AirTag hasn’t impacted the company’s revenue or device sales.

“But that doesn’t take away from the fact that they’re making things harder for us,” he says of Apple. “We’re a growing business. We’re winning the hearts and minds of consumers… and they’re competing unfairly.”

“When you own the platform, you shouldn’t be able to identify a category that you want to enter, disadvantage the incumbents in that category, and then advantage yourself — like they did in our case,” he adds.

Tile is preparing to announce an upcoming product refresh that may allow it to better take on the AirTag. Presumably, this will include the pre-announced ultra-wideband version of Tile, but the company says full details will be shared next week. Tile may also expand its lineup in other ways that will allow it to better compete based on look and feel, size and shape, and functionality.

Tile’s last round of funding was $45 million in growth equity in 2019. Now it’s shifted to debt. In addition to new debt financing, Tile is also refinancing some of its existing debt with this fundraise, it says.

“My philosophy is it’s always good to have a mix of debt and equity. So some amount of debt on the balance sheet is good. And it doesn’t incur dilution to our shareholders,” Prober says. “We felt this was the right mix of capital choice for us.”

The company chose to work with Capital IP, a group it’s had a relationship with over the last three years, and who Tile had considered bringing on as an investor. The group has remained interested in Tile and excited about its trajectory, Prober notes.

“We are excited to partner with the Tile team as they continue to define and lead the finding category through hardware and software-based innovations,” said Capital IP’s Managing Partner Riyad Shahjahan, in a statement. “The impressive revenue growth and fast-climbing subscriber trends underline the value proposition that Tile delivers in a platform-agnostic manner, and were a critical driver in our decision to invest. The Tile team has an ambitious roadmap ahead and we look forward to supporting their entry into new markets and applications to further cement their market leadership,” he added.

Powered by WPeMatico

Five months after it was announced that Pal Gelsinger would be stepping down as CEO of VMware to take the top job at Intel, the virtualization giant has finally appointed a permanent successor. Raghu Raghuram — a longtime employee of the company — has been appointed the new CEO. He will be taking on the new role on June 1. Until then, CFO Zane Rowe will continue in the role in the interim.

Raghuram has been with the company for 17 years in a variety of roles, most recently COO of products and cloud services. He’s also held positions at the company overseeing areas like data centers and VMware’s server business. Putting a veteran at the helm sends a clear message that VMware has picked someone clearly dedicated to the company and its culture. No drama here.

Indeed, the move is coming at a time when there is already a lot of other change underway and speaks to the company looking for stability and continuity to lead it through that. About a month ago, Dell confirmed long-anticipated news that it would be spinning out its stake in VMware in a deal that’s expected to bring Dell at least $9 billion — putting to an end a financial partnership that initially kicked off with an eye-watering acquisition of EMC in 2016. That partnership will not end the strategic relationship, however, which is set to continue and now Raghuram will be in charge of building and leading.

For that reason, you might look at this as a deal nodded through significantly by Dell.

“I am thrilled to have Raghu step into the role of CEO at VMware. Throughout his career, he has led with integrity and conviction, playing an instrumental role in the success of VMware,” said Michael Dell, chairman of the VMware board of directors, in a statement. “Raghu is now in position to architect VMware’s future, helping customers and partners accelerate their digital businesses in this multicloud world.”

Raghuram has not only been the person overseeing some of VMware’s biggest divisions and newer areas like software-defined networking and cloud computing, but he’s had a central role in building and driving strategy for the company’s core virtualization business, been involved with M&A and, as VMware points out, “key in driving partnerships with Dell Technologies,” among other partners.

“VMware is uniquely poised to lead the multicloud computing era with an end-to-end software platform spanning clouds, the data center and the edge, helping to accelerate our customers’ digital transformations,” said Raghuram in a statement. “I am honored, humbled and excited to have been chosen to lead this company to a new phase of growth. We have enormous opportunity, we have the right solutions, the right team and we will continue to execute with focus, passion and agility.”

The company also took the moment to update on guidance for its Q1 results, which will be coming out on May 27. Revenues are expected to come in at $2.994 billion, up 9.5% versus the same quarter a year ago. Subscription and SaaS and license revenue, meanwhile, is expected to be $1.387 billion, up 12.5%. GAAP net income per diluted share is expected to be $1.01 per diluted share, and non-GAAP net income per diluted share is expected to be $1.76 per diluted share, it said.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here.

This morning was a notable one in the life of TechCrunch the publication, as our parent company’s parent company decided to sell our parent company to a different parent company. And now we’re going to have to get new corporate IDs, again, as it appears that our new parent company’s parent company wants to rebrand our parent company. As Yahoo.

Cool.

Anyway, a bunch of other stuff happened as well:

We’re back Wednesday with something special. Chat then!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

It’s widely known that Dell has a debt problem left over from its massive acquisition of EMC in 2016, and it seems to be moving this year to eliminate part of it in multi-billion-dollar chunks. The first step was spinning out VMware as a separate company last month, a move expected to net close to $10 billion.

The second step, long expected, finally dropped last night when the company announced it was selling Boomi to a couple of private equity firms for $4 billion. Francisco Partners is joining forces with TPG to make the deal to buy the integration platform.

Boomi is not unlike MuleSoft, a company that Salesforce purchased in 2018 for $6.5 billion, although a bit longer in the tooth. They both help companies with integration problems by creating connections between disparate systems. With so many pieces in place from various acquisitions over the years, it seems like a highly useful asset for Dell to help pull these pieces together and make them work, but the cash is trumping that need.

Providing integration services is a growing requirement as companies look for ways to make better use of data locked in siloed systems. Boomi could help, and that’s one of the primary reasons for the acquisition, according to Francisco executives.

“The ability to integrate and connect data and workflows across any combination of applications or domains is a critical business capability, and we strongly believe that Boomi is well positioned to help companies of all sizes turn data into their most valuable asset,” Francisco CEO Dipanjan Deb and partner Brian Decker said in a statement.

As you would expect, Boomi’s CEO Chris McNabb put a positive spin on the deal about how his new bosses were going to fuel growth for his company. “By partnering with two tier-one investment firms like Francisco Partners and TPG, we can accelerate our ability for our customers to use data to drive competitive advantage. In this next phase of growth, Boomi will be in a position of strength to further advance our innovation and market trajectory while delivering even more value to our customers,” McNabb said in a statement.

All of this may have some truth to it, but the company goes from being part of a large amorphous corporation to getting absorbed in the machinery of two private equity firms. What happens next is hard to say.

The company was founded in 2000, and sold to Dell in 2010. Today, it has 15,000 customer, but Dell’s debt has been well documented, and when you string together a couple of multi-billion-dollar deals as Dell has recently, pretty soon you’re talking real money. While the company has not stated it will explicitly use the proceeds of this deal to pay off debt as it did with the VMware announcement, it stands to reason that this will be the case.

The deal is expected to close later this year, although it will have to pass the typical regulatory scrutiny prior to that.

Powered by WPeMatico

MasterClass, which sells a subscription to celebrity-taught classes, sits on the cusp of entertainment and education. It offers virtual, yet aspirational learning: an online tennis class with Serena Williams, a cooking session with Gordon Ramsay. While there’s the off chance that an instructor might actually talk to you — it has happened before — the platform mostly just offers paywalled documentary-style content.

The vision has received attention. MasterClass is raising funding that would value it at $2.5 billion, as scooped by Axios and confirmed independently by a source to TechCrunch. But while MasterClass has found a sweet spot, can the success be replicated?

Investors certainly think so. Outlier, founded by MasterClass’ co-founder, closed a $30 million Series C this week, for affordable, digital college courses. The similarities between Outlier and its founder’s alma mater aren’t subtle: It’s literally trying to apply MasterClass’ high-quality videography to college classes. This comes a week after I wrote about a “MasterClass for Chess lovers” platform launched by former Chess World Champion Garry Kasparov.

Two back-to-back MasterClass copycats raising millions in venture capital makes me think about if the model can truly be verticalized and focused down into specific niches. After 2020 and the rise of Zoom University, we know edtech needs to be more engaging, but we don’t know the exact way to get there. Is it by creating micro-learning communities around shared loves? Is it about gamification? Aspirational learning has different incentives than for-credit learning. In order to be successful, Outlier needs to prove to universities it can use MasterClass magic for true outcomes that rival in-person lectures. It’s a harder, and more ambtious promise.

My riff aside, I turned to two edtech founders to understand how they see the MasterClass effect panning out, and to cross-check my gut reaction.

Taylor Nieman, the founder of language learning startup Toucan:

Although I do love how these models try to lean into this theme of “invisible learning” like we leverage with Toucan, it faces the same issues as so many other consumer products that try to steal time out of people’s very busy days. Constantly competing for time leads to terrible engagement metrics and very high churn. That leads me to question what true learning outcomes could occur from little to no usage of the product itself.

Amanda DoAmaral, the founder of Fiveable, a learning platform for high school students:

Masterclass is important for showing us why educational content should be treated more like entertainment. All of our bars for content quality is much higher now than it ever was before and I’m excited to see how that affects learning across the board.

For students, it’s about creating environments that support them holistically and giving them space to collaborate openly. It feels so obvious that these spaces should exist for young people, but we’ve lost sight of what students actually need. At my school, we built policies that assumed the worst in students. I want to flip that. Assume the best, be proactive to keep them safe, and create ways to react when we need to.

Anyways, that’s just some nuance to chew on during this fine day. In the rest of this newsletter, we will focus a lot on tactical advice for founders, from the money they raise to the peacock dance they might want to do one day. Make sure to follow me on Twitter @nmasc_ so we can talk during the week, too!

You know when male peacocks fan their feathers to court a lover? That, but for startups trying to get acquired. As one of our many rabbit holes on Equity this week, we talk about Discord walking away from a Microsoft deal, and if that deal ever existed in the first place or if it was just a way to drum up investor excitement in the audio gaming platform.

Here’s what to know: Discord is reportedly pursuing an IPO after walking away from talks with multiple companies that were looking to acquire the audio gaming giant.

Discord aside, the consolidation environment continues to be hot for some sectors.

Image Credits: VectorInspiration / Getty Images

Clearbanc, a Toronto-based fintech startup that gives non-dilutive financing to businesses, has rebranded alongside a $100 million financing that valued it at $2 billion. Now rebranded as Clearco, the startup wants to be more than just a capital provider, but a services provider, too.

Here’s what to know: The startup has been on a tear of product development for the past year, launching services such as valuation calculators or runway tools. It’s a step away from what Clearbanc originally flexed: the 20-minute term sheet and rapid-fire investment. I talk about some of the levers at play in my piece:

Many of Clearco’s newest products are still in their infancy, but the potential success of the startup could nearly be tied to the general growth of startups looking for alternatives to venture capital when financing their startups. Similar to how AngelList’s growth is neatly tied to the growth of emerging fund managers, Clearco’s growth is cleanly related to the growth of founders who see financing as beyond a seed check from Y Combinator.

Abstract human brain made out of dollar bills isolated on white background. Image Credits: Iaremenko / Getty Images

Keeping on the theme of tactical advice for founders, let’s move onto talking about marketing. Tim Parkin, president of Parkin Consulting, explained how startup founders can use marketing as a tool to stand out in the noisy environment. Differentiation has never been harder, but also more imperative.

Here’s what to know: Parkin outlines four ways that martech will shift in 2021, strapped with anecdotes and a nod to the importance of investing in influencers.

Red ball on curved light blue paper, blue background. Image Credits: PM Images / Getty Images

Your humble yet favorite startup podcast, Equity, got nominated for a Webby! Me and the team need your help to win, so please vote for us here. Your support means a ton.

This newsletter will always be free, but if you do want to support me, feel free to use code STARTUPSWEEKLY for 25% off a subscription to Extra Crunch.

Seen on TechCrunch

The rise of the next Coinbase, thanks to Coinbase

Tiger Global backs Indian crypto startup at over $500M valuation

Early Coinbase backer Garry Tan is keeping the ‘vast majority’ of his shares because of this deal

Seen on Extra Crunch

Dear Sophie: How can I get my startup off the ground and visit the US?

How to pivot your startup, save cash and maintain trust with investors and customers

How startups can ensure CCPA and GDPR compliance in 2021

Image Credits: TechCrunch

Thanks for reading along today and everyday. Sending love to my readers in India and everyone around the world that is facing yet another deadly surge of this horrible disease. I’m rooting for you.

Powered by WPeMatico

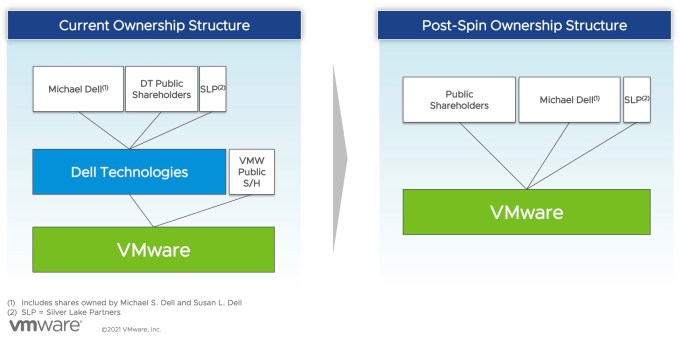

TechCrunch has spilled much digital ink tracking the fate of VMware since it was brought to Dell’s orbit thanks to the latter company’s epic purchase of EMC in 2016 for $58 billion. That transaction saddled the well-known Texas tech company with heavy debts. Because the deal left VMware a public company, albeit one controlled by Dell, how it might be used to pay down some of its parent company’s arrears was a constant question.

Dell made its move earlier this week, agreeing to spin out VMware in exchange for a huge one-time dividend, a five-year commercial partnership agreement, lots of stock for existing Dell shareholders and Michael Dell retaining his role as chairman of its board.

So, where does the deal leave VMware in terms of independence, and in terms of Dell influence? Dell no longer will hold formal control over VMware as part of the deal, though its shareholders will retain a large stake in the virtualization giant. And with Michael Dell staying on VMware’s board, it will retain influence.

Here’s how VMware described it to shareholders in a presentation this week. The graphic shows that under the new agreement, VMware is no longer a subsidiary of Dell and will now be an independent company.

Image Credits: VMware

But with VMware tipped to become independent once again, it could become something of a takeover target. When Dell controlled VMware thanks to majority ownership, a hostile takeover felt out of the question. Now, VMware is a more possible target to the right company with the right offer — provided that the Dell spinout works as planned.

Buying VMware would be an expensive effort, however. It’s worth around $67 billion today. Presuming a large premium would be needed to take this particular technology chess piece off the competitive board, it could cost $100 billion or more to snag VMware from the public markets.

So VMware will soon be more free to pursue a transaction that might be favorable to its shareholders — which will still include every Dell shareholder, because they are receiving stock in VMware as part of its spinout — without worrying about its parent company simply saying no.

Powered by WPeMatico

This is not a boast, but a warning: I could write a how-to article on almost any topic.

Give me enough time to do some research, and I can put together a reliable step-by-step for building a custom gaming PC, installing a hot water heater or interpreting public health data. But since I’ve never actually done those things, I would encourage you to ignore any advice I have to offer.

Trusted advice comes from experience. That’s why Ron Miller interviewed three entrepreneurs who have each built multiple companies to uncover some essential truths about achieving product-market fit:

The basic tenets presented in Ron’s story will resonate with anyone who’s launched a startup.

Alex Wilhelm was particularly prolific this morning: For The Exchange, he studied UiPath’s 2020 quarterly results to get a clearer picture of its first S-1/A filing. Is the “somewhat slack news regarding UiPath’s potential IPO valuation” a harbinger of things to come?

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

In a follow-up, he recapped news from the public debuts of Coinbase, UiPath, Zenvia, AppLovin and Grab, all of which “adds up to a somewhat muddled picture of the current IPO market.” It feels like we’re in a turbulent window, but it’s also possible that we’re in the calm after the storm, he suggests.

Final note: I asked TechCrunch graphic designer/illustrator Bryce Durbin to create an image to accompany this primer on raising a Series A round. He didn’t just exceed my expectations — it’s my favorite TechCrunch illustration ever. Thanks, Bryce!

I hope you got something out of reading Extra Crunch this week. Have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Bryce Durbin/TechCrunch

From building out Facebook’s first office in Austin to putting together most of Quora’s team, Bain Capital Ventures managing director Sarah Smith has done a bit of everything when it comes to hiring.

At TechCrunch Early Stage, she spoke about how to ensure the critical early hires are the right ones to grow a business. As an investor, Smith has a broad view into the problems companies face as they search for the right candidates to spur organizational success.

She touched on a number of issues, such as who to hire and when, when to fire and how to ensure diversity from the earliest days.

Image Credits: Bryce Durbin/TechCrunch

During a seed-funding round, a founder needs to convince a venture capital investor on a vision. But during a Series A fundraise, napkin-stage ideas don’t make the cut — a founder needs product progress, numbers and revenue (or at least a plan to eventually generate some).

In many ways, the stakes are higher for a Series A — and Bucky Moore, a partner at Kleiner Perkins, joined TechCrunch Early Stage last week to give founders tactical advice on the process of raising one.

Moore spoke about storytelling over semantics, pricing and where his firm sees itself “raising the bar” for startups.

For a long time, “revenue” seemed to be a taboo word in the startup world. Fortunately, things have changed with the rise of SaaS and alternative funding sources such as revenue-based investing VCs.

Still, revenue modeling remains a challenge for founders. How do you predict earnings when you’re still figuring it out?

Image Credits: erhui1979 / Getty Images

If you have a great idea within the open-core framework, expect your risks to be much lower than with a traditional business structure.

Clearly communicate this fact to venture capitalists for the best chance at securing the seed funding your organization needs.

But it takes more: Boasting a strong community around an emerging open-source product essentially serves as an “introduction letter” to venture capitalists. It highlights the founders’ ability to successfully execute their vision, as well as the mission to bring their product to a commercial reality.

Additionally, the iterative nature of open-source projects leads to fostering a sense of teamwork between the founders, their team and investors and stakeholders.

Image Credits: Ureeka

Melissa Bradley is the co-founder of a startup called Ureeka, an investor at 1863 Ventures and a professor at Georgetown’s business school. So it’s not an understatement to say that she understands the fundraising process from every angle.

She both invested and fundraised for her own startup during this last year, where the landscape has shifted drastically. At TechCrunch Early Stage, she led a session on how to nail your virtual pitch meeting.

Bradley covered how to allocate your time during the meeting, how to prepare, how to close out the meetings with a clear list of action items and what to avoid.

Image Credits: Eric Millette / Scale AI

Scale CEO and co-founder Alex Wang credits its success since founding — which includes raising over $277 million and achieving breakeven status in terms of revenue — to early support from investors, including Accel’s Dan Levine.

Accel haș participated in four of Scale’s financing rounds, and Levine wrote one of the company’s very first checks. So on this past week’s episode of Extra Crunch Live, we spoke with Levine and Wang about how that first deal came together, and what their working relationship has been like in the years since.

Image Credits: Nigel Sussman (opens in a new window)

Let’s parse Uber’s latest, vet its profit promise, consider its rivals and their performance, then ask ourselves if the great ride-hailing and food-delivery booms will ever make back the money they cost to scale.

Image Credits: Noam Galai/Getty Images

For UiPath, its initial IPO price interval is a disappointment, though the company could see an upward revision in its valuation before it does sell shares and begins to trade.

But more to the point, the company’s private-market valuation bump followed by a quick public-market correction stands out as a counter-example to something that we’ve seen so frequently in recent months.

Is UiPath’s first IPO price interval another indicator that the IPO market is cooling?

Image Credits: alexsl / Getty Images

As artificial intelligence becomes more advanced, previously cutting-edge — but generic — AI models are becoming commonplace, such as Google Cloud’s Vision AI or Amazon Rekognition.

While effective in some use cases, these solutions do not suit industry-specific needs right out of the box. Organizations that seek the most accurate results from their AI projects will simply have to turn to industry-specific models.

Any team looking to expand its AI capabilities should first apply its data and use cases to a generic model and assess the results.

Let’s dive into each of these approaches and how businesses can decide which one works for their distinct circumstances.

Image Credits: Atomico

In the earliest stages of building a startup, it can be hard to justify focusing on anything other than creating a great product or service and meeting the needs of customers or users.

However, there are still a number of surefire measures that any early-stage company can and should put in place to achieve “people ops” success as they begin scaling, according to venture capital firm Atomico‘s talent partners, Caro Chayot and Dan Hynes.

Long story short: You need to recruit for what you need, but you also need to think about what is coming down the line.

Image Credits: Roslan Rahman/Getty Images

Southeast Asian superapp Grab is going public via a SPAC.

Grab, which provides ride-hailing, payments and food delivery, will trade under the ticker symbol “GRAB” on the Nasdaq exchange when the combination is complete.

Let’s walk through several key points from Grab’s SPAC investor deck, including growth, segment profitability, aggregate costs and COVID-19, among other factors.

Image Credits: Nigel Sussman (opens in a new window)

Microsoft’s huge purchase of health tech AI company Nuance led the technology news cycle this week. The $19.7 billion transaction is Microsoft’s second-largest to date, only beaten by its purchase of LinkedIn some years ago.

For the AI space, the sale is a coup. Nuance was already a public company, but to see Microsoft offer a firm premium over its public-market value demonstrates the value that AI technology can have to wealthy companies. For startups working in the AI space, the Nuance deal is good news; the value of AI revenue was repriced by the acquisition’s announcement — and for the better.

In light of the megadeal, The Exchange dug into the AI venture capital market. What’s happening on the startup side of the coin in the artificial intelligence and machine learning (AI/ML) space?

Image Credits: Bryce Durbin

When the word “hydrogen” is uttered today, the average non-insider’s mind likely gravitates toward transportation — cars, buses, maybe trains or 18-wheelers, all powered by the gas.

But hydrogen is, and does, a lot of things, and a better understanding of its other roles — and challenges within those roles — is necessary to its success in transportation.

Hydrogen is now capturing the attention of governments and private sector players, fueled by new tech, global green energy legislation and post-pandemic “green recovery” schemes.

Image Credits: LaylaBird / Getty Images

Before a startup can achieve product-market fit, founders must first listen to their customers, build what they require and fashion a business plan that makes the whole enterprise worthwhile.

The numbers will tell the true story, but when it happens, you’ll feel it in your bones because sales will be good, customers will be happy and revenue will be growing.

Reaching that tipping point can be a slog, especially for first-time founders. To uncover some basic truths about building products, we spoke to three entrepreneurs who have each built more than one company.

Image Credits: Nigel Sussman (opens in a new window)

In broad strokes, the United States had a crushing venture capital start to the new year, pandemic be damned.

That is especially true when we consider 2020’s full-year figures. Last year, venture capitalists deployed some $166 billion into U.S.-based startups across 12,546 rounds. In contrast, if the first quarter’s pace was maintained during the rest of 2021, the United States would see around 16,000 rounds worth around $280 billion.

Of course, we cannot see the future, so those projections are merely shared to underscore how active the first quarter proved to be.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

For the past few years, our company has put very promising candidates into the annual H-1B lottery. None of them have been selected — and none of them meet the requirements for other work visas like an O-1A.

We lost out again in this year’s H-1B lottery. Are there any other ways we can obtain H-1Bs for our team members?

— Soldiering on in Sunnyvale

Image Credits: Alexa von Tobel

Few people are more knowledgeable on the topic of how founders should manage their finances than Alexa von Tobel.

She is a certified financial planner, started her own company in the midst of the recession (which happened to be a wildly successful personal finance startup that sold for hundreds of millions of dollars) and is now a VC who invests and advises founders.

At Early Stage 2021, she gave a presentation on how founders should think about managing their own wealth. Startup founders can often put all their money into their venture and end up paying more attention to the finances of their company than their own bank account.

Von Tobel outlined the various steps you can take to stay out of debt, build credit and accumulate wealth through investments to ensure you have financial peace of mind as you take on the most stressful venture of your life: Starting a company.

Image Credits: Olive

A few years ago, founder Sean Lane thought he’d achieved product-market fit.

Speaking to attendees at TechCrunch’s Early Stage virtual event, Lane said Queue, a secure digital check-in tablet for hospital waiting rooms that reduced wait times by uniting and correcting electronic medical records, was “selling like hotcakes.” But once Lane realized it would only ever address one piece of a much bigger market opportunity, he sold off the product, laid off two-thirds of the people affiliated with it and redirected the employees who were left.

Lane explained that what he really wanted to build is what his company — since renamed Olive — has now become, a robotic process automation (RPA) company that takes on hospital workers’ most tedious tasks so nurses and physicians can spend more time with patients.

Image Credits: jayk7 (opens in a new window) / Getty Images

In business today, many believe that consumer privacy and business results are mutually exclusive — to excel in one area is to lack in the other. Consumer privacy is seen by many in the technology industry as an area to be managed.

But the truth is that the companies that champion privacy will be better-positioned to win in all areas. This is especially true as the digital industry continues to undergo tectonic shifts in privacy — both in government regulation and browser updates.

Image Credits: Chris Jongkind (opens in a new window)/ Getty Images

Founders shouldn’t be worried about starting companies that rely on other platforms.

Platforms exist to help startups get to users and customers faster and should be used as a means to an end, but everyone must get their piece.

Image Credits: Nigel Sussman (opens in a new window)

Coinbase’s direct listing was a massive finance, startup and cryptocurrency event, and the transaction’s effects will be felt for some time in the public market, but also among the startups and capital that comprise the private market.

In the buildup to Coinbase’s flotation — and we’d argue especially after it released its blockbuster Q1 2021 results — there was a general expectation that the unicorn’s direct listing would provide a halo effect for other startups in the space.

The widely held perspective raised two questions: Will the success of Coinbase’s direct listing bolster private investment in crypto-focused startups, and will that success help other areas of financially focused startup work garner more investor attention?

Image Credits: twomeows (opens in a new window)/ Getty Images

The “billion-dollar B2B” paradigm refers to the forces shaping a new class of cloud-first, enterprise-tech behemoths with the potential to reach $1 billion in ARR — and achieve market capitalizations in excess of $50 billion or even $100 billion.

One of the biggest factors driving billion-dollar B2Bs is a simple but important shift in how organizations buy enterprise technology today.

Image Credits: tumsasedgars (opens in a new window) / Getty Images

Data is the most valuable asset for any business in 2021. If your business is online and collecting customer personal information, your business is dealing in data, which means data privacy compliance regulations will apply to everyone — no matter the company’s size.

Small startups might not think the world’s strictest data privacy laws — the California Consumer Privacy Act (CCPA) and Europe’s General Data Protection Regulation (GDPR) — apply to them, but it’s important to enact best data management practices before a legal situation arises.

Image Credits: Bloomberg / Getty Images

When Dell announced it was spinning out VMware, the move itself wasn’t surprising; there had been public speculation for some time.

But Dell could have gone a number of ways in this deal, despite its choice to spin VMware out as a separate company with a constituent dividend instead of an outright sale.

It seems Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned.

Image Credits: Nigel Sussman (opens in a new window)

Robotic process automation platform UiPath filed its first S-1/A this week, setting an initial price range for its shares. The numbers were impressive, if slightly disappointing because what UiPath indicated in terms of its potential IPO value was a lower valuation than it earned during its final private fundraising.

Here at The Exchange, we wondered if the somewhat slack news regarding UiPath’s potential IPO valuation was a warning to late-stage investors.

But in good news for UiPath shareholders, most everyone — ourselves included! — who discussed the company’s price range didn’t dig into the fact that the company first disclosed quarterly results to the same S-1/A filing that included its IPO valuation interval. And those numbers are very interesting, so much so that The Exchange is now generally expecting UiPath to target a higher price interval before it debuts.

But let’s dig into the company’s quarterly results to get a clearer picture of UiPath.

Image Credits: Mohd Hafiez Mohd Razali/EyeEm (opens in a new window) / Getty Images

If you only stayed up to date with the Coinbase direct listing this week, you’re forgiven. It was, after all, one heck of a flotation.

But underneath the cryptocurrency exchange’s public debut, other IPO news that matters did happen this week. And the news adds up to a somewhat muddled picture of the current IPO market.

To cap off the week, let’s run through IPO news from UiPath, Coinbase, Grab, AppLovin and Zenvia. The aggregate dataset should help you form your own perspective about where today’s IPO markets really are in terms of warmth for the often unprofitable unicorns of the world.

Powered by WPeMatico

When Dell announced it was spinning out VMware yesterday, the move itself wasn’t surprising; there had been public speculation for some time. But Dell could have gone a number of ways in this deal, despite its choice to spin VMware out as a separate company with a constituent dividend instead of an outright sale.

The dividend route, which involves a payment to shareholders between $11.5 billion and $12 billion, has the advantage of being tax-free (or at least that’s what Dell hopes as it petitions the IRS). For Dell, which owns 81% of VMware, the dividend translates to somewhere between $9.3 billion and $9.7 billion in cash, which the company plans to use to pay down a portion of the huge debt it still holds from its $58 billion EMC purchase in 2016.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned.

VMware was the crown jewel in that transaction, giving Dell an inroad to the cloud it had lacked prior to the deal. For context, VMware popularized the notion of the virtual machine, a concept that led to the development of cloud computing as we know it today. It has since expanded much more broadly beyond that, giving Dell a solid foothold in cloud native computing.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned. Dell CEO Michael Dell will remain chairman of the VMware board, which should help smooth the post-spinout relationship.

But could Dell have extracted more cash out of the deal?

Patrick Moorhead, principal analyst at Moor Insights and Strategies, says that beyond the cash transaction, the deal provides a way for the companies to continue working closely together with the least amount of disruption.

“In the end, this move is more about maximizing the Dell and VMware stock price [in a way that] doesn’t impact customers, ISVs or the channel. Wall Street wasn’t valuing the two companies together nearly as [strongly] as I believe it will as separate entities,” Moorhead said.

Powered by WPeMatico

Dell announced this afternoon that it’s spinning out VMware, a move that has been suspected for some time. Dell acquired VMware as part of the massive $58 billion EMC acquisition (announced as $67 billion) in 2015.

The way that the deal works is that Dell plans to offer VMware shareholders a special dividend of between $11.5 and $12 billion. As Dell owns approximately 81% of those shares that would work out to somewhere between $9.3 and $9.7 billion coming into Dell’s coffers when the deal closes later this year.

“By spinning off VMware, we expect to drive additional growth opportunities for Dell Technologies as well as VMware, and unlock significant value for stakeholders. Both companies will remain important partners, with a differentiated advantage in how we bring solutions to customers,” Dell CEO Michael Dell said in a statement.

While there is a fair amount of CEO speak in that statement, it appears to mean that the move is mostly administrative as the companies will continue to work closely together, even after the spin-off is official. Dell will remain as chairman of both companies.

In a presentation to investors, the companies indicated that the plan to work together is more than lip service. There is a five-year deal commercial agreement in place with plans to revisit that deal each year thereafter. In addition, there is a plan to sell VMware products through the Dell sales team and for VMware to continue to work with Dell Financial Services. Finally, there is a formalized governance process in place related to achieving the commercial goals under the agreement, so it’s pretty firm that these companies will continue to work closely together at least for another five years.

For its part, VMware said in a separate release that the deal will allow it “increased freedom to execute its strategy, a simplified capital structure and governance model and additional strategic, operational and financial flexibility, while maintaining the strength of the two companies’ strategic partnership.”

Dell shares are up more than 8% following the announcement. The company intends on using parts of its proceeds to deleverage, writing in a release that it will use “net proceeds to pay down debt, positioning the company well for Investment Grade ratings.” By that it means that Dell will reduce its net debt position and, it hopes, garner a stronger credit rating that will limit its future borrowing costs.

Even when it was part of EMC, VMware had a special status in that it operates as a separate entity with its own executive team and board of directors, and the stock has been sold separately as well.

The deal is expected to close at the end of this year, but it has to clear a number of regulatory hurdles first. That includes garnering a favorable ruling from the IRS that the deal qualifies for a tax-free spin-off, which could prove to be a considerable hurdle for a deal like this.

The transaction is not a surprise. The company has been open about its intention to shake up its broader corporate structure. And with Dell bloated in debt terms and, perhaps, in product scope as well, the VMware deal could be an intelligent way forward. Dell investors are more excited about the transaction than VMware shareholders, with the latter company’s stock is up a more modest 1.4%.

VMware’s most recent earnings release notes that it had $4.715 billion in “total cash, cash equivalents and short-term investments.” Perhaps its shareholders aren’t enthused at the prospect of levering VMware’s balance sheet to help Dell do the opposite.

Powered by WPeMatico

If you develop software for a large enterprise company, chances are you’ve heard of Tricentis. If you don’t develop software for a large enterprise company, chances are you haven’t. The software testing company with a focus on modern cloud and enterprise applications was founded in Austria in 2007 and grew from a small consulting firm to a major player in this field, with customers like Allianz, BMW, Starbucks, Deutsche Bank, Toyota and UBS. In 2017, the company raised a $165 million Series B round led by Insight Venture Partners.

Today, Tricentis announced that it has acquired Neotys, a popular performance testing service with a focus on modern enterprise applications and a tests-as-code philosophy. The two companies did not disclose the price of the acquisition. France-based Neotys launched in 2005 and raised about €3 million before the acquisition. Today, it has about 600 customers for its NeoLoad platform. These include BNP Paribas, Dell, Lufthansa, McKesson and TechCrunch’s own corporate parent, Verizon.

As Tricentis CEO Sandeep Johri noted, testing tools were traditionally script-based, which also meant they were very fragile whenever an application changed. Early on, Tricentis introduced a low-code tool that made the automation process both easier and resilient. Now, as even traditional enterprises move to DevOps and release code at a faster speed than ever before, testing is becoming both more important and harder for these companies to implement.

“You have to have automation and you cannot have it be fragile, where it breaks, because then you spend as much time fixing the automation as you do testing the software,” Johri said. “Our core differentiator was the fact that we were a low-code, model-based automation engine. That’s what allowed us to go from $6 million in recurring revenue eight years ago to $200 million this year.”

Tricentis, he added, wants to be the testing platform of choice for large enterprises. “We want to make sure we do everything that a customer would need, from a testing perspective, end to end. Automation, test management, test data, test case design,” he said.

The acquisition of Neotys allows the company to expand this portfolio by adding load and performance testing as well. It’s one thing to do the standard kind of functional testing that Tricentis already did before launching an update, but once an application goes into production, load and performance testing becomes critical as well.

“Before you put it into production — or before you deploy it — you need to make sure that your application not only works as you expect it, you need to make sure that it can handle the workload and that it has acceptable performance,” Johri noted. “That’s where load and performance testing comes in and that’s why we acquired Neotys. We have some capability there, but that was primarily focused on the developers. But we needed something that would allow us to do end-to-end performance testing and load testing.”

The two companies already had an existing partnership and had integrated their tools before the acquisition — and many of its customers were already using both tools, too.

“We are looking forward to joining Tricentis, the industry leader in continuous testing,” said Thibaud Bussière, president and co-founder at Neotys. “Today’s Agile and DevOps teams are looking for ways to be more strategic and eliminate manual tasks and implement automated solutions to work more efficiently and effectively. As part of Tricentis, we’ll be able to eliminate laborious testing tasks to allow teams to focus on high-value analysis and performance engineering.”

NeoLoad will continue to exist as a stand-alone product, but users will likely see deeper integrations with Tricentis’ existing tools over time, include Tricentis Analytics, for example.

Johri tells me that he considers Tricentis one of the “best kept secrets in Silicon Valley” because the company not only started out in Europe (even though its headquarters is now in Silicon Valley) but also because it hasn’t raised a lot of venture rounds over the years. But that’s very much in line with Johri’s philosophy of building a company.

“A lot of Silicon Valley tends to pay attention only when you raise money,” he told me. “I actually think every time you raise money, you’re diluting yourself and everybody else. So if you can succeed without raising too much money, that’s the best thing. We feel pretty good that we have been very capital efficient and now we’re recognized as a leader in the category — which is a huge category with $30 billion spend in the category. So we’re feeling pretty good about it.”

Powered by WPeMatico