Dell

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s (virtual) Microsoft Ignite this week, Microsoft’s annual IT-centric conference and its largest, with more than 26,000 people attending the last in-person event in 2019. Given its focus, it’s no surprise that Microsoft Teams is taking center stage in the announcements this year. Teams, after all, is now core to Microsoft’s productivity suite. Today’s announcements span the gamut from new meeting features to conference room hardware.

At the core of Teams — or its competitors like Slack for that matter — is the ability to collaborate across teams, but increasingly, that also includes collaboration with others outside of your organization. Today, Microsoft is announcing the preview of Teams Connect to allow users to share channels with anyone, internal or external. These channels will appear alongside other teams and channels and allow for all of the standard Teams use cases. Admins will keep full control over these channels to ensure that external users only get access to the data they need, for example. This feature will roll out widely later this year.

What’s maybe more important to individual users, though, is that Teams will get a new PowerPoint Live feature that will allow presenters to present as usual — but with the added benefit of seeing all their notes, slides and meeting chats in a single view. And for those suffering through yet another PowerPoint presentation while trying to look engaged, PowerPoint Live lets them scroll through the presentation at will — or use a screen reader to make the content more accessible. This new feature is now available in Teams.

Image Credits: Microsoft

Also new on the presentation side is a set of presentation modes that use some visual wizardry to make presentations more engaging. “Standout mode” shows the speaker’s video feed in front of the content, for example, while “Reporter mode” shows the content above the speaker’s shoulder, just like in your local news show. And side-by-side view — well, you can guess it. This feature will launch in March, but it will only feature the Standout mode first. Reporter mode and side-by-side will launch “soon.”

Another new view meant to visually spice up your meetings is the “Dynamic view.” With this, Teams will try to arrange all of the elements of a meeting “for an optimal viewing experience,” personalized for each viewer. “As people join, turn on video, start to speak, or begin to present in a meeting, Teams automatically adjusts and personalizes your layout,” Microsoft says. What’s maybe more useful, though, is that Teams will put a gallery of participants at the top of the screen to help you maintain a natural eye gaze (without any AI trickery).

Image Credits: Microsoft

As for large-scale meetings, Teams users can now hold interactive webinars with up to 1,000 people inside and outside of their organization. And for all of those occasions where your CEO just has to give a presentation to everybody, Teams supports broadcast-only meetings with up to 20,000 viewers. That’ll go down to 10,000 attendees after June 30, 2021, based on the idea that the pandemic will be mostly over then and the heightened demand for visual events will subside around that time. Good luck to us all.

For that time when we’ll go back to an office, Microsoft is building intelligent speakers for conference rooms that are able to differentiate between the voices of up to 10 speakers to provide more accurate transcripts. It’s also teaming up with Dell and others to launch new conference room monitors and speaker bars.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, legal, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included in each for audience questions and discussion.

Powered by WPeMatico

In a move that could have wide ramifications across the tech landscape, Intel announced that VMware CEO Pat Gelsinger would be replacing interim CEO Bob Swan at Intel on February 15th. The question is why would he leave his job to run a struggling chip giant.

The bottom line is he has a long history with Intel, working with some of the biggest names in chip industry lore before he joined VMware in 2009. It has to be a thrill for him to go back to his roots and try to jump start the company.

“I was 18 years old when I joined Intel, fresh out of the Lincoln Technical Institute. Over the next 30 years of my tenure at Intel, I had the honor to be mentored at the feet of Grove, Noyce and Moore,” Gelsinger wrote in a blog post announcing his new position.

Certainly Intel recognized that the history and that Gelsinger’s deep executive experience should help as the company attempts to compete in an increasingly aggressive chip industry landscape. “Pat is a proven technology leader with a distinguished track record of innovation, talent development, and a deep knowledge of Intel. He will continue a values-based cultural leadership approach with a hyper focus on operational execution,” Omar Ishrak, independent chairman of the Intel board, said in a statement.

But Gelsinger is walking into a bit of a mess. As my colleague Danny Crichton wrote in his year-end review of the chip industry last month, Intel is far behind its competitors, and it’s going to be tough to play catch-up:

Intel has made numerous strategic blunders in the past two decades, most notably completely missing out on the smartphone revolution and also the custom silicon market that has come to prominence in recent years. It’s also just generally fallen behind in chip fabrication, an area it once dominated and is now behind Taiwan-based TSMC, Crichton wrote.

Patrick Moorhead, founder and principal analyst at Moor Insights & Strategy, agrees with this assertion, saying that Swan was dealt a bad hand, walking in to clean up a mess that has years long timelines. While Gelsinger faces similar issues, Moorhead thinks he can refocus the company. “I am not foreseeing any major strategic changes with Gelsinger, but I do expect him to focus on the company’s engineering culture and get it back to an execution culture,” Moorhead told me.

The announcement comes against the backdrop of massive chip industry consolidation last year with over $100 billion changing hands in four deals, with Nvidia nabbing ARM for $40 billion, the $35 billion AMD-Xilink deal, Analog snagging Maxim for $21 billion and Marvell grabbing Inphi for a mere $10 billion, not to mention Intel dumping its memory unit to SK Hynix for $9 billion.

As for VMware, it has to find a new CEO now. As Moorhead says, the obvious choice would be current COO Sanjay Poonen, but for the time being, it will be CFO Zane Rowe serving as interim CEO, rather than Poonen. In fact, it appears that the company will be casting a wider net than internal options. The official announcement states, “VMware’s Board of Directors is initiating a global executive search process to name a permanent CEO…”

Holger Mueller, an analyst at Constellation Research, says it will be up to Michael Dell to decide who to hand the reins to, but he believes Gelsinger was stuck at Dell and would not get a broader role, so he left.

“VMware has a deep bench, but it will be up to Michael Dell to get a CEO who can innovate on the software side and keep the unique DNA of VMware inside the Dell portfolio going strong, Dell needs the deeper profits of this business for its turnaround,” he said.

The stock market seems to like the move for Intel, with the company stock up 7.26%, but not so much for VMware, whose stock was down close to the same amount at 7.72% as we went to publication.

Powered by WPeMatico

After going private in 2016 after accepting a $32 per share, or $4.3 billion, price from Apollo Global Management, Rackspace is looking once again to the public markets. First going public in 2008, Rackspace is taking second aim at a public offering around 12 years after its initial debut.

The company describes its business as a “multicloud technology services” vendor, helping its customers “design, build and operate” cloud environments. That Rackspace is highlighting a services focus is useful context to understand its financial profile, as we’ll see in a moment.

But first, some basics. The company’s S-1 filing denotes a $100 million placeholder figure for how much the company may raise in its public offering. That figure will change, but does tell us that firm is likely to target a share sale that will net it closer to $100 million than $500 million, another popular placeholder figure.

Rackspace will list on the Nasdaq with the ticker symbol “RXT.” Goldman, Citi, J.P. Morgan, RBC Capital Markets and other banks are helping underwrite its (second) debut.

Similar to other companies that went private, only later to debut once again as a public company, Rackspace has oceans of debt.

The company’s balance sheet reported cash and equivalents of $125.2 million as of March 31, 2020. On the other side of the ledger, Rackspace has debts of $3.99 billion, made up of a $2.82 billion term loan facility, and $1.12 billion in senior notes that cost the firm an 8.625% coupon, among other debts. The term loan costs a lower 4% rate, and stems from the initial transaction to take Rackspace private ($2 billion), and another $800 million that was later taken on “in connection with the Datapipe Acquisition.”

The senior notes, originally worth a total of $1,200 million or $1.20 billion, also came from the acquisition of the company during its 2016 transaction; private equity’s ability to buy companies with borrowed money, later taking them public again and using those proceeds to limit the resulting debt profile while maintaining financial control is lucrative, if a bit cheeky.

Rackspace intends to use IPO proceeds to lower its debt-load, including both its term loan and senior notes. Precisely how much Rackspace can put against its debts will depend on its IPO pricing.

Those debts take a company that is comfortably profitable on an operating basis and make it deeply unprofitable on a net basis. Observe:

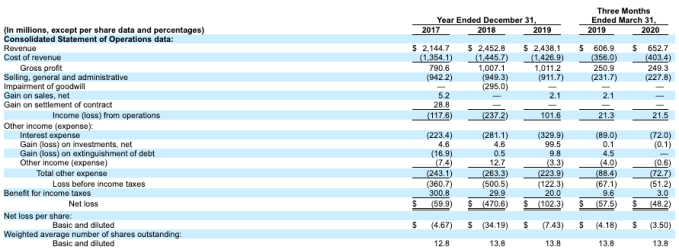

Image Credits: SEC

Looking at the far-right column, we can see a company with material revenues, though slim gross margins for a putatively tech company. It generated $21.5 million in Q1 2020 operating profit from its $652.7 million in revenue from the quarter. However, interest expenses of $72 million in the quarter helped lead Rackspace to a deep $48.2 million net loss.

Not all is lost, however, as Rackspace does have positive operating cash flow in the same three-month period. Still, the company’s multi-billion-dollar debt load is still steep, and burdensome.

Returning to our discussion of Rackspace’s business, recall that it said that it sells “multicloud technology services,” which tells us that its gross margins will be service-focused, which is to say that they won’t be software-level. And they are not. In Q1 2020 Rackspace had gross margins of 38.2%, down from 41.3% in the year-ago Q1. That trend is worrisome.

The company’s growth profile is also slightly uneven. From 2017 to 2018, Rackspace saw its revenue expand from $2.14 billion to $2.45 billion, growth of 14.4%. The company shrank slightly in 2019, falling from $2.45 billion in revenue in 2018 to $2.44 billion the next year. Given the economy that year, and the importance of cloud in 2019, the results are a little surprising.

Rackspace did grow in Q1 2020, however. The firm’s $652.7 million in first-quarter top-line easily bested in its Q1 2019 result of $606.9 million. The company grew 7.6% in Q1 2020. That’s not much, especially during a period in which its gross margins eroded, but the return-to-growth is likely welcome all the same.

TechCrunch did not see Q2 2020 results in its S-1 today while reading the document, so we presume that the firm will re-file shortly to include more recent financial results; it would be hard for the company to debut at an attractive price in the COVID-19 era without sharing Q2 figures, we reckon.

How to value Rackspace is a puzzle. The company is tech-ish, which means it will find some interest. But its slow growth rate, heavy debts and lackluster margins make it hard to pin a fair multiple onto. More when we have it.

Powered by WPeMatico

Last week, we discussed the possibility that Dell could be exploring a sale of VMware as a way to deal with its hefty debt load, a weight that continues to linger since its $67 billion acquisition of EMC in 2016. VMware was the most valuable asset in the EMC family of companies, and it remains central to Dell’s hybrid cloud strategy today.

As CNBC pointed out last week, VMware is a far more valuable company than Dell itself, with a market cap of almost $62 billion. Dell, on the other hand, has a market cap of around $39 billion.

How is Dell, which owns 81% of VMware, worth less than the company it controls? We believe it’s related to that debt, and if we’re right, Dell could unlock lots of its own value by reducing its indebtedness. In that light, the sale, partial or otherwise, of VMware starts to look like a no-brainer from a financial perspective.

At the end of its most recent quarter, Dell had $8.4 billion in short-term debt and long-term debts totaling $48.4 billion. That’s a lot, but Dell has the ability to pay down a significant portion of that by leveraging the value locked inside its stake in VMware.

Nothing is ever as simple as it seems. As Holger Mueller from Constellation Research pointed out in our article last week, VMware is the one piece of the Dell family that is really continuing to innovate. Meanwhile, Dell and EMC are stuck in hardware hell at a time when companies are moving faster than ever expected to the cloud due to the pandemic.

Dell is essentially being handicapped by a core business that involves selling computers, storage and the like to in-house data centers. While it’s also looking to modernize that approach by trying to be the hybrid link between on-premise and the cloud, the economy is also working against it. The pandemic has made the difficult prospect of large enterprise selling even more challenging without large conferences, golf outings and business lunches to grease the skids of commerce.

Powered by WPeMatico

When Dell bought EMC in 2016 for $67 billion it was one of the biggest acquisitions in tech history, and it brought with it a boatload of debt. Since then Dell has been working on ways to mitigate that debt by selling off various pieces of the corporate empire and going public again, but one of its most valuable assets remains VMware, a company that came over as part of the huge EMC deal.

The Wall Street Journal reported yesterday that Dell is considering selling part of its stake in VMware. The news sent the stock of both companies soaring.

It’s important to understand that even though VMware is part of the Dell family, it runs as a separate company, with its own stock and operations, just as it did when it was part of EMC. Still, Dell owns 81% of that stock, so it could sell a substantial stake and still own a majority of the company, or it could sell it all, or incorporate into the Dell family, or of course it could do nothing at all.

Patrick Moorhead, founder and principal analyst at Moor Insights & Strategy, thinks this might just be about floating a trial balloon. “Companies do things like this all the time to gauge value, together and apart, and my hunch is this is one of those pieces of research,” Moorhead told TechCrunch.

But as Holger Mueller, an analyst with Constellation Research, points out, it’s an idea that could make sense. “It’s plausible. VMware is more valuable than Dell, and their innovation track record is better than Dell’s over the last few years,” he said.

Mueller added that Dell has been juggling its debts since the EMC acquisition, and it will struggle to innovate its way out of that situation. What’s more, Dell has to wait on any decision until September 2021 when it can move some or all of VMware tax-free, five years after the EMC acquisition closed.

“While Dell can juggle finances, it cannot master innovation. The company’s cloud strategy is only working on a shrinking market and that ain’t easy to execute and grow on. So yeah, next year makes sense after the five-year tax-free thing kicks in,” he said.

VMware is worth $63.9 billion today, while Dell is valued at a far more modest $38.9 billion, according to Yahoo Finance data. But beyond the fact that the companies’ market caps differ, they are also quite different in terms of their ability to generate profit.

Looking at their most recent quarters each ending May 1, 2020, Dell turned $21.9 billion in revenue into just $143 million in net income after all expenses were counted. In contrast, VMware generated just $2.73 billion in revenue, but managed to turn that top line into $386 million worth of net income.

So, VMware is far more profitable than Dell from a far smaller revenue base. Even more, VMware grew more last year (from $2.45 billion to $2.73 billion in revenue in its most recent quarter) than Dell, which shrank from $21.91 billion in Q1 F2020 revenue to $21.90 billion in its own most recent three-month period.

VMware also has growing subscription software (SaaS) revenues. Investors love that top line varietal in 2020, having pushed the valuation of SaaS companies to new heights. VMware grew its SaaS revenues from $411 million in the year-ago period to $572 million in its most recent quarter. That’s not rocketship growth mind you, but the business category was VMware’s fastest growing segment in percentage and gross dollar terms.

So VMware is worth more than Dell, and there are some understandable reasons for the situation. Why wouldn’t Dell sell some VMware to lower its debts if the market is willing to price the virtualization company so strongly? Heck, with less debt perhaps Dell’s own market value would rise.

Almost four years after the deal closed, Dell is still struggling to figure out how to handle all the debt, and in a weak economy, that’s an even bigger challenge now. At some point, it would make sense for Dell to cash in some of its valuable chips, and its most valuable one is clearly VMware.

Nothing is imminent because of the five-year tax break business, but could something happen? September 2021 is a long time away, and a lot could change between now and then, but on its face, VMware offers a good avenue to erase a bunch of that outstanding debt very quickly and get Dell on much firmer financial ground. Time will tell if that’s what happens.

Powered by WPeMatico

Dell’s 2015 decision to buy EMC for $67 billion remains the largest pure tech deal in history, but a transaction of such magnitude created a mountain of debt for the Texas-based company and its primary backer, Silver Lake.

Dell would eventually take on close to $50 billion in debt. Years later, where are they in terms of paying that back, and has the deal paid for itself?

When EMC put itself up for sale, it was under pressure from activist investors Elliott Management to break up the company. In particular, Elliott reportedly wanted the company to sell one of its most valuable parts, VMware, which it believed would help boost EMC’s share price. (Elliott is currently turning the screws on Twitter and SoftBank.)

Whatever the reason, once the company went up for sale, Dell and private equity firm Silver Lake came ‘a callin with an offer EMC CEO Joe Tucci couldn’t refuse. The arrangement represented great returns for his shareholders, and Tucci got to exit on his terms, telling Elliott to take a hike (even if it was Elliott that got the ball rolling in the first place).

Dell eventually took itself public again in late 2018, probably to help raise some of the money it needed to pay off its debts. We are more than three years past the point where the Dell-EMC deal closed, so we decided to take a look back and see if Dell was wise to take on such debt or not.

Powered by WPeMatico

Contract management service DocuSign today announced that it is acquiring Seal Software for $188 million in cash. The acquisition is expected to close later this year. DocuSign, it’s worth noting, previously invested $15 million in Seal Software in 2019.

Seal Software was founded in 2010, and, while it may not be a mainstream brand, its customers include the likes of PayPal, Dell, Nokia and DocuSign itself. These companies use Seal for its contract management tools, but also for its analytics, discovery and data extraction services. And it’s these AI smarts the company developed over time to help businesses analyze their contracts that made DocuSign acquire the company. This can help them significantly reduce their time for legal reviews, for example.

“Seal was built to make finding, analyzing, and extracting data from contracts simpler and faster,” DocuSign CEO John O’Melia said in today’s announcement. “We have a natural synergy with DocuSign, and our team is excited to leverage our AI expertise to help make the Agreement Cloud even smarter. Also, given the company’s scale and expansive vision, becoming part of DocuSign will provide great opportunities for our customers and partners.”

DocuSign says it will continue to sell Seal’s analytics tools. What’s surely more important to DocuSign, though, is that it will also leverage the company’s AI tools to bolster its DocuSign CLM offering. CLM is DocuSign’s service for automating the full contract life cycle, with a graphical interface for creating workflows and collaboration tools for reviewing and tracking changes, among other things. And integration with Seal’s tools, DocuSign argues, will allow it to provide its customers with a “faster, more efficient agreement process,” while Seal’s customers will benefit from deeper integrations with the DocuSign Agreement Cloud.

Powered by WPeMatico

Dell Technologies announced today that it was selling legacy security firm RSA for $2.075 billion to a consortium of investors led by Symphony Technology Group. Other investors include Ontario Teachers’ Pension Plan Board and AlpInvest Partners.

RSA came to Dell when it bought EMC for $67 billion in 2015. EMC bought the company in 2006 for a similar price it was sold for today, $2.1 billion. The deal includes several pieces, including the RSA security conference held each year in San Francisco.

As for products, the consortium gets RSA Archer, RSA NetWitness Platform, RSA SecurID, RSA Fraud and Risk Intelligence — in addition to the conference. At the time of the EMC acquisition, in a letter to customers, Michael Dell actually called out RSA as one of the companies he looked forward to welcoming to the Dell family after the deal was completed:

I am excited to work with the EMC, VMware, Pivotal, VCE, Virtustream and RSA teams, and I am personally committed to the success of our new company, our partners and above all, to you, our customers.

Times change however, and perhaps Dell decided it was simply time to get some cash and jettison the veteran security company to go a bit more modern, as RSA’s approach no longer aligned with Dell’s company-wide security strategy.

“The strategies of RSA and Dell Technologies have evolved to address different business needs with different go-to-market models. The sale of RSA gives us greater flexibility to focus on integrated innovation across Dell Technologies, while allowing RSA to focus on its strategy of providing risk, security and fraud teams with the ability to holistically manage digital risk,” Dell Technology’s chief operating officer and vice chairman Jeff Clarke, wrote in a blog post announcing the deal.

Meanwhile, RSA president Rohit Ghai tried to put a happy spin on the outcome, framing it as the next step in the company’s long and storied history. “The one constant in every episode of our existence has been our focus on the success of our customers and our ability to endure through market disruption by innovating on behalf of our customers,” he wrote in a blog post on the RSA company website.

The deal is subject to the normal kinds of regulatory approval before it is finalized.

Powered by WPeMatico

VMware is closing the year with a significant new component in its arsenal. Today it announced it has closed the $2.7 billion Pivotal acquisition it originally announced in August.

The acquisition gives VMware another component in its march to transform from a pure virtual machine company into a cloud native vendor that can manage infrastructure wherever it lives. It fits alongside other recent deals like buying Heptio and Bitnami, two other deals that closed this year.

They hope this all fits neatly into VMware Tanzu, which is designed to bring Kubernetes containers and VMware virtual machines together in a single management platform.

“VMware Tanzu is built upon our recognized infrastructure products and further expanded with the technologies that Pivotal, Heptio, Bitnami and many other VMware teams bring to this new portfolio of products and services,” Ray O’Farrell, executive vice president and general manager of the Modern Application Platforms Business Unit at VMware, wrote in a blog post announcing the deal had closed.

Craig McLuckie, who came over in the Heptio deal and is now VP of R&D at VMware, told TechCrunch in November at KubeCon that while the deal hadn’t closed at that point, he saw a future where Pivotal could help at a professional services level, as well.

“In the future when Pivotal is a part of this story, they won’t be just delivering technology, but also deep expertise to support application transformation initiatives,” he said.

Up until the closing, the company had been publicly traded on the New York Stock Exchange, but as of today, Pivotal becomes a wholly owned subsidiary of VMware. It’s important to note that this transaction didn’t happen in a vacuum, where two random companies came together.

In fact, VMware and Pivotal were part of the consortium of companies that Dell purchased when it acquired EMC in 2015 for $67 billion. While both were part of EMC and then Dell, each one operated separately and independently. At the time of the sale to Dell, Pivotal was considered a key piece, one that could stand strongly on its own.

Pivotal and VMware had another strong connection. Pivotal was originally created by a combination of EMC, VMware and GE (which owned a 10% stake for a time) to give these large organizations a separate company to undertake transformation initiatives.

It raised a hefty $1.7 billion before going public in 2018. A big chunk of that came in one heady day in 2016 when it announced $650 million in funding led by Ford’s $180 million investment.

The future looked bright at that point, but life as a public company was rough, and after a catastrophic June earnings report, things began to fall apart. The stock dropped 42% in one day. As I wrote in an analysis of the deal:

The stock price plunged from a high of $21.44 on May 30th to a low of $8.30 on August 14th. The company’s market cap plunged in that same time period falling from $5.828 billion on May 30th to $2.257 billion on August 14th. That’s when VMware admitted it was thinking about buying the struggling company.

VMware came to the rescue and offered $15.00 a share, a substantial premium above that August low point. As of today, it’s part of VMware.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about a new e-commerce startup, Pietra. Before that, I wrote about the flurry of IPO filings.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

Peloton revealed its S-1 this week, taking a big step toward an IPO expected later this year. The filing was packed with interesting tidbits, including that the company, which manufacturers internet-connected stationary bikes and sells an affiliated subscription to its growing library of on-demand fitness content, is raking in more than $900 million in annual revenue. Sure, it’s not profitable, and it’s losing an increasing amount of money to sales and marketing efforts, but for a company that many people wrote off from the very beginning, it’s an impressive feat.

Despite being a hardware, media, interactive software, product design, social connection, apparel and logistics company, according to its S-1, the future of Peloton relies on its talent. Not the employees developing the bikes and software but the 29 instructors teaching its digital fitness courses. Ally Love, Alex Toussaint and the 27 other teachers have developed cult followings, fans who will happily pay Peloton’s steep $39 per month content subscription to get their daily dose of Ben or Christine.

“To create Peloton, we needed to build what we believed to be the best indoor bike on the market, recruit the best instructors in the world, and engineer a state-of-the-art software platform to tie it all together,” founder and CEO John Foley writes in the IPO prospectus. “Against prevailing conventional wisdom, and despite countless investor conference rooms full of very smart skeptics, we were determined for Peloton to build a vertically integrated platform to deliver a seamless end-to-end experience as physically rewarding and addictive as attending a live, in-studio class.”

Peloton succeeded in poaching the best of the best. The question is, can they keep them? Will competition in the fast-growing fitness technology sector swoop in and scoop Peloton’s stars?

Last week I published a long feature on the state of seed investing in the Bay Area. The TL;DR? Mega-funds are increasingly battling seed-stage investors for access to the hottest companies. As a result, seed investors are getting a little more creative about how they source deals. It’s a dog-eat-dog world out there, and everyone wants a stake in The Next Big Thing. Read the story here.

")

Don’t miss out on our flagship Disrupt, which takes place October 2-4. It’s the quintessential tech conference for anyone focused on early-stage startups. Join more than 10,000 attendees — including over 1,200 exhibiting startups — for three jam-packed days of programming. We’re talking four different stages with interactive workshops, Q&A sessions and interviews with some of the industry’s top tech titans, founders, investors, movers and shakers. Check out our list of speakers and the Disrupt agenda. I will be there interviewing a bunch of tech leaders, including Bastian Lehmann and Charles Hudson. Buy tickets here.

This week on Equity, TechCrunch’s venture capital-focused podcast, we had Floodgate’s Iris Choi on to discuss Peloton’s upcoming IPO. You can listen to it here. Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast and Spotify.

We published a number of new deep dives on Extra Crunch, our paid subscription product, this week. Here’s a quick look at the top stories:

Powered by WPeMatico