cryptocurrencies

Auto Added by WPeMatico

Auto Added by WPeMatico

The speed at which gaming has proliferated is matched only by the pace of new buzzwords inundating the ecosystem. Marketers and decision-makers, already suffering from FOMO about opportunities within gaming, have latched onto buzzy trends like the applications of blockchain in gaming and the “metaverse” in an effort to get ahead of the trend rather than constantly play catch-up.

The allure is obvious, as the relationship between the blockchain, metaverse and gaming makes sense. Gaming has always been on the forefront of digital ownership (one can credit gaming platform Steam for normalizing the concept for games, and arguably other media such as movies), and most agreed upon visions of the metaverse rely upon virtual environments common in games with decentralized digital ownership.

Whatever your opinion of either, I believe they both have an interrelated future in gaming. However, the success or relevance of either of these buzzy topics is dependent upon a crucial step that is being skipped at this point.

Let’s start with the example of blockchain and, more specifically, NFTs. Collecting items of varying rarities and often random distribution form some of the core “loops” in many games (e.g., kill monster, get better weapon, kill tougher monster, get even better weapon, etc.), and collecting “skins” (i.e., different outfits/permutation of game character) is one of the most embraced paradigms of microtransactions in games.

The way NFTs are currently being discussed in relation to gaming are very much in danger of falling into this very trap: Killing the core gameplay loop via a financial fast track.

Now, NFTs are positioned to be a natural fit with various rare items having permanent, trackable and open value. Recent releases such as “Loot (for Adventurers)” have introduced a novel approach wherein the NFTs are simply descriptions of fantasy-inspired gear and offered in a way that other creators can use them as tools to build worlds around. It’s not hard to imagine a game built around NFT items, à la Loot.

But that’s been done before … kind of. Developers of games with a “loot loop” like the one described above have long had a problem with “farmers,” who acquire game currencies and items to sell to players for real money, against the terms of service of the game. The solution was to implement in-game “auction houses” where players could instead use real money to purchase items from one another.

Unfortunately, this had an unwanted side effect. As noted by renowned game psychologist Jamie Madigan, our brains are evolved to pay special attention to rewards that are both unexpected and beneficial. When much of the joy in some games comes from an unexpected or randomized reward, being able to easily acquire a known reward with real money robbed the game of what made it fun.

The way NFTs are currently being discussed in relation to gaming are very much in danger of falling into this very trap: Killing the core gameplay loop via a financial fast track. The most extreme examples of this phenomena commit the biggest cardinal sin in gaming — a game that is “pay to win,” where a player with a big bankroll can acquire a material advantage in a competitive game.

Blockchain games such as Axie Infinity have rapidly increased enthusiasm around the concept of “play to earn,” where players can potentially earn money by selling tokenized resources or characters earned within a blockchain game environment. If this sounds like a scenario that can come dangerously close to “pay to win,” that’s because it is.

What is less clear is whether it matters in this context. Does anyone care enough about the core game itself rather than the potential market value of NFTs or earning potential through playing? More fundamentally, if real-world earnings are the point, is it truly a game or just a gamified micro-economy, where “farming” as described above is not an illicit activity, but rather the core game mechanic?

The technology culture around blockchain has elevated solving for very hard problems that very few people care about. The solution (like many problems in tech) involves reevaluation from a more humanist approach. In the case of gaming, there are some fundamental gameplay and game psychology issues to be tackled before these technologies can gain mainstream traction.

We can turn to the metaverse for a related example. Even if you aren’t particularly interested in gaming, you’ve almost certainly heard of the concept after Mark Zuckerberg staked the future of Facebook upon it. For all the excitement, the fundamental issue is that it simply doesn’t exist, and the closest analogs are massive digital game spaces (such as Fortnite) or sandboxes (such as Roblox). Yet, many brands and marketers who haven’t really done the work to understand gaming are trying to fast-track to an opportunity that isn’t likely to materialize for a long time.

Gaming can be seen as the training wheels for the metaverse — the ways we communicate within, navigate and think about virtual spaces are all based upon mechanics and systems with foundations in gaming. I’d go so far as to predict the first adopters of any “metaverse” will indeed be gamers who have honed these skills and find themselves comfortable within virtual environments.

By now, you might be seeing a pattern: We’re far more interested in the “future” applications of gaming without having much of a perspective on the “now” of gaming. Game scholarship has proliferated since the early aughts due to a recognition of how games were influencing thought in fields ranging from sociology to medicine, and yet the business world hasn’t paid it much attention until recently.

The result is that marketers and decision-makers are doing what they do best (chasing the next big thing) without the usual history of why said thing should be big, or what to do with it when they get there. The growth of gaming has yielded an immense opportunity, but the sophistication of the conversations around these possibilities remains stunted, due in part to our misdirected attention.

There is no “pay to win” fast track out of this blind spot. We have to put in the work to win.

Powered by WPeMatico

Cent was founded in 2017 as an ad-free creator network that allows users to offer each other crypto rewards for good posts and comments — it’s like gifting awards on Reddit, but with Ethereum. But in late 2020, Cent’s small, San Francisco-based team created Valuables, an NFT market for tweets, and by March, the small blockchain startup was thrown a serendipitous curveball.

“We just wrapped up for the day, and I was about to go eat dinner, and all these people started texting me,” remembers CEO Cameron Hejazi. Then, he realized that Twitter CEO Jack Dorsey had minted Twitter’s first-ever Tweet through Cent’s Valuables application. “I was basically like, mildly shivering for the rest of the night. The whole team, we were like, ‘Okay, battle stations, prepare to get hacked!’ ”

Dorsey ended up selling his NFT for $2.9 million, and he donated the proceeds to Give Directly’s Africa Response fund for COVID-19 relief. But for Cent, it was as if the small company had just been handed a free marketing campaign. Now, about five months later, Cent is announcing a $3 million round of seed funding with investors like Galaxy Interactive, former Disney chairman Jeffrey Katzenberg, will.i.am and Zynga founder Mark Pincus.

On Valuables, anyone on the internet can place an offer on any tweet, which then makes it possible for someone else to make a counter-offer. If the author of the tweet accepts an offer (logging into Valuables requires you to validate your Twitter account), then Cent will mint the tweet on the blockchain and create a 1-of-1 NFT.

The NFT itself contains the text of the tweet, the username of the creator, the time it was minted and the creator’s digital signature. The NFT also includes a link to the tweet, though the linked content lives outside the blockchain.

Image Credits: Cent (opens in a new window)

There’s nothing proprietary about minting tweets as NFTs — another company could do the same thing that Cent is doing. Even Twitter itself has recently dabbled in giving away free NFT art, though it hasn’t tried to sell actual tweets as NFTs like Cent. Still, Hejazi sees Dorsey’s use of Cent like an endorsement — he thinks it would be difficult for Twitter to shut them down, since Dorsey made $2.9 million on the platform himself. After all, Dorsey chose Cent instead of taking a screenshot of his first tweet, minting the .JPG as an NFT and posting it on a larger NFT platform, like OpenSea.

“We’ve spoken with people at Twitter. I’m positive that we have a healthy relationship going,” Hejazi said (Twitter declined to comment on or confirm whether that’s true). “We thought about applying this approach to other social platforms, like Instagram and TikTok, but we hypothesized that this is particularly suited for Twitter, because it’s a conversation platform, and it’s where all of the crypto people are actually living.”

With Cent’s seed funding Hejazi hopes to continue building the platform. The company’s goal is to enable anyone creative to make an income through the use of NFTs — that means developing tools to make it simpler for its users to mint NFTs, but also, building out its existing creator-focused social network. The content people post on Cent is usually creative work, like art and writing, rather than short posts — it’s closer to DeviantArt than it is to Reddit. These are lofty goals for a $3 million seed funding round, but there are aspects of Cent’s Beta platform that make it promising.

“There’s already value in what we post on social media. It’s just being proxied through ad dollars, and it doesn’t have to be the case that there’s so much wealth concentration in a single entity. We can work toward a system that decentralizes that wealth,” said Hejazi. “These networks as they exist have monopolies on distribution — you can’t take your Twitter audience, download it as a .CSV and send them all an email.”

A screenshot of Cent’s social platform.

In addition to independent distribution lists, Hejazi wants to move away from the ad-supported internet. He references Substack as an example of a company where the creator has control of their list, and at the same time, the platform can remain ad-free, since the money that propels it comes from the users who pay to subscribe to newsletters (and also, venture capital helps).

But Cent does something different by allowing users to essentially invest in creators who they think have the potential to take off on their platform.

Users can “seed” a post, which is how you subscribe to a creator participating on the creatives side of Cent’s platform. As the seeder, you pay a set fee of at least one dollar per month. There’s an incentive to support up-and-coming creators on the platform, because seeders get a portion of the creators’ future profit — it’s like making a bet on them that they will continue to make great content in the future. Five percent of profits go toward Cent, but the remaining 95% is split 50/50 between the creator and all of their past seeders. Participating on this platform would allow creators to network and show support for one another, but doesn’t prevent them from more directly monetizing their work on other creator platforms, like Patreon.

In addition to seeding posts, users can also “spot” other people’s posts — Cent’s version of a “like” button. Each “spot” is the equivalent of one cent from the user’s crypto wallet. Cent’s argument is that getting 1,000 likes on a post on other platforms yields nothing but a vague sensation of social clout. But on Cent, if a user gets 1,000 “spots,” that’s $10. Still, a project like this can only work if enough people use the platform.

“When we started Cent, we chose cryptocurrencies because we loved the idea of someone being able to earn money with nothing more than their creativity and a crypto address,” Hejazi said. “Over time, we’ve found it to be limiting as a payment type — very few people actually own it and have it ready to spend. We’re working on ways to make payments to creators using Cent easier, and are exploring both crypto-native and non-crypto options.”

This mindset echoes other NFT startups like Yat, which allows payments via credit card as part of its “progressive decentralization” model. So much of these companies’ success depends on public buy-in toward an eventual decentralized, blockchain-based internet. But until then, companies like Cent will continue to experiment in reimagining how creatives can get paid online.

Powered by WPeMatico

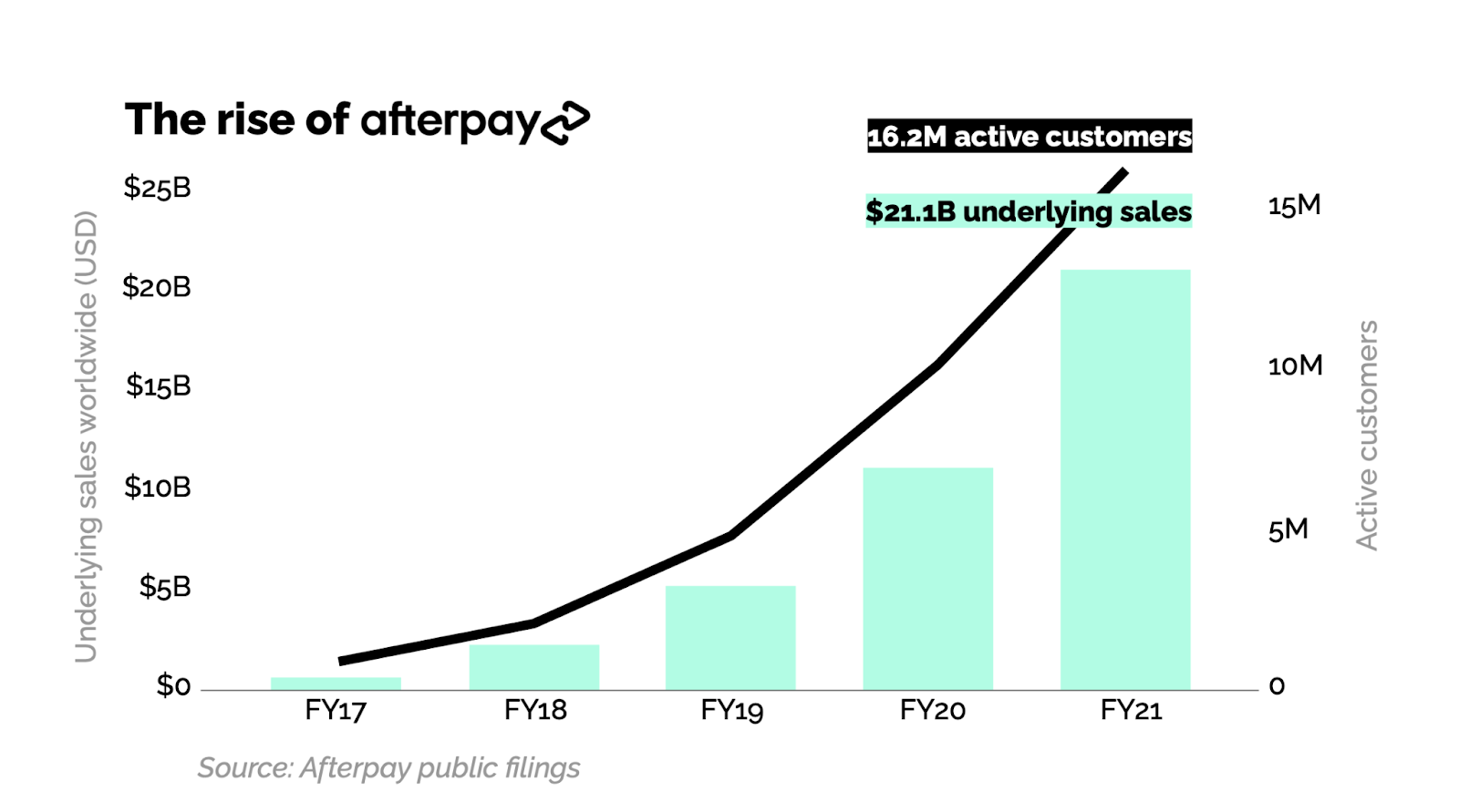

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

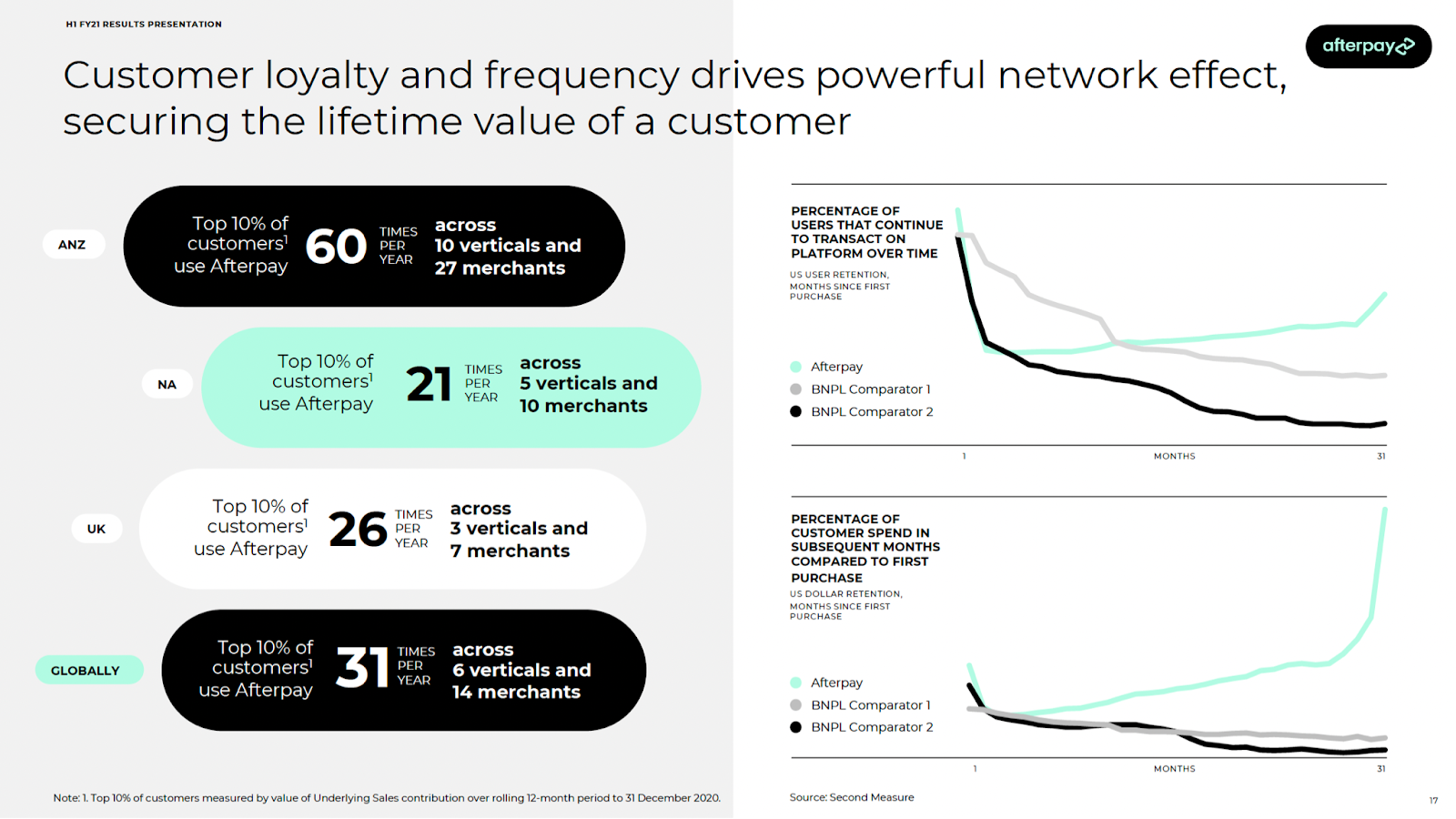

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

I learned about Yat in April, when a friend sent our group chat a link to a story about how the key emoji sold as an “internet identity” for $425,000. “I hate the universe,” she texted.

Sure, the universe would be better if people with a spare $425,000 spent it on mutual aid or something, but minutes later, we were trying to figure out what this whole Yat thing was all about. And few more minutes later, I spent $5 (in U.S. dollars, not crypto) to buy

, an emoji string that I think tells a moving story about my caffeine dependency and sensitive stomach. I didn’t think I would be writing about this when I made that choice.

, an emoji string that I think tells a moving story about my caffeine dependency and sensitive stomach. I didn’t think I would be writing about this when I made that choice.

Kesha’s Yat URL on Twitter

On the surface, Yat is a platform that lets you buy a URL with emojis in it — even Kesha (y.at/

), Lil Wayne (y.at/

), Lil Wayne (y.at/ ), and Disclosure (y.at/

), and Disclosure (y.at/ ) are using them in their Twitter bios. Like any URL on the internet, Yats can redirect to another website, or they can function like a more eye-catching Linktree. While users could purchase their own domain name that supports emojis and use it instead of a Yat, many people don’t have the technical expertise or time to do so. Instead, they can make a one-time purchase from Yat, which owns the Y.at domain, and the company will provide you with your own y.at link for you.

) are using them in their Twitter bios. Like any URL on the internet, Yats can redirect to another website, or they can function like a more eye-catching Linktree. While users could purchase their own domain name that supports emojis and use it instead of a Yat, many people don’t have the technical expertise or time to do so. Instead, they can make a one-time purchase from Yat, which owns the Y.at domain, and the company will provide you with your own y.at link for you.

This convenience, however, comes at a premium. Yat uses an algorithm to determine your Yat’s “rhythm score,” its metric for determining how to price your emoji combo based on its rarity. Yats with one or two emojis are so expensive that you have to contact the company directly to buy them, but you can easily find a four- or five-emoji identity that’ll only put you out $4.

Beyond that, CEO Naveen Jain — a Y Combinator alumnus, founder of digital marketing company Sparkart and angel investor — thinks that Yat is ultimately an internet privacy product. Jain wants people to be able to use their Yats in any way they’re able to use an online identity now, whether that’s to make payments, send messages, host a website or log in to a platform.

“Objectively, it’s a strange norm. You go on the internet, you register accounts with ad-supported platforms, and your username isn’t universal. You have many accounts, many usernames,” Jain said. “And you don’t control them. If an account wants to shut you down, they shut you down. How many stories are there of people trying to email some social network, and they don’t respond because they don’t have to?”

Image Credits: Yat (opens in a new window)

Yat doesn’t plan to fuel itself with ad money, since users pay for the product when they purchase their Yat, whether they get it for $4 or $400,000.

In the long run, Yat’s CEO says the company plans to use blockchain technology as a way to become self-sovereign. Yats would become assets issued on decentralized, distributed databases. Today, there are several projects working to create a decentralized alternative to the current domain name system (DNS), which is managed by internet regulatory authority ICANN. DNS is how you find things on the internet, but uses a centralized, hierarchical system. A blockchain domain name system would have no central authority, and some believe this could be the foundation of a next-gen web, or “Web 3.0.”

Today, words like “blockchain” and “cryptocurrency” don’t appear on the Yat website. Jain doesn’t think that’s compelling to average consumers — he believes in progressive decentralization, which explains why Yats are currently purchased with dollars, not ethereum.

“Something we think is really funny about the cryptocurrency world is that anyone who’s a part of it spends a lot of time talking about databases,” Jain said. “People don’t care about databases. When’s the last time you went to a website and it said ‘powered by MySQL’?”

Y.at, however, was registered at a traditional internet registrar, not on the blockchain.

“This is laying the foundation — there are certain elements of the vision that are certainly more of a social contract than actual implementation at this point in time,” says Jain. “But this is the vision that we’ve set forth, and we’re working continuously towards that goal.”

Still, until Yat becomes more decentralized, it can’t yet give users the complete control it aspires to. At present, the Terms & Conditions give Yat the authority to terminate or suspend users at its discretion, but the company claims it hasn’t yet booted anyone from the system.

“As Yat becomes more decentralized, our terms and conditions won’t be important,” Jain said. “This is the nature of pursuing a progressive decentralization strategy.”

In its “generation zero” phase (an open beta), Yat claims to have sold almost $20 million worth of emoji identities. Now, as the waitlist to get a Yat ends, Yat is posting some rare emoji identities on OpenSea, the NFT marketplace that recently reached a valuation of $1.5 billion.

A still image of a Yat visualizer creation

“For the first time ever, we’re going to be auctioning some Yats on OpenSea, and we’re going to be launching minting of Yats on Ethereum,” Jain said. Before minting Yats as NFTs, users can create a digital art landscape for their Yats through a Visualizer. These features, as well as new emojis in the Yat emoji set, will launch this evening at a virtual event called Yat Horizon.

“Yat Creators will now have more rights,” Jain said about the new ability to mint Yats as NFTs. “We are going to continue to pursue progressive decentralization until we achieve our ultimate goal: making Yat the best self-directed, self-sovereign identity system for all.”

Consumers have a demonstrated interest in retaining greater privacy on the internet — data shows that in iOS 14.5, 96% of users opted out of ad tracking. But the decentralization movement hasn’t yet been able to market its privacy advantages to the mainstream. Yat helps solve this problem because even if you don’t understand what blockchain means, you understand that having a personal string of emojis is pretty fun. But, before you spend $425,000 on a single-emoji username, keep in mind that Yat’s vision will only completely materialize with the advent of Web 3.0, and we don’t yet know when or if that will happen.

Powered by WPeMatico

PayPal’s plan to morph itself into a “super app” has been given a go for launch.

According to PayPal CEO Dan Schulman, speaking to investors during this week’s second-quarter earnings call, the initial version of PayPal’s new consumer digital wallet app is now “code complete” and the company is preparing to slowly ramp up. Over the next several months, PayPal expects to be fully ramped up in the U.S., with new payment services, financial services, commerce and shopping tools arriving every quarter.

The company has spoken for some time about its “super app” ambitions — a shift in product direction that would make PayPal a U.S.-based version of something like China’s WeChat or Alipay or India’s Paytm. Like those apps, PayPal aims to offer a host of consumer services under one roof, beyond just mobile payments.

In previous quarters, PayPal said these new features may include things like enhanced direct deposit, check cashing, budgeting tools, bill pay, crypto support, subscription management, and buy now, pay later functionality. It also said it would integrate commerce, thanks to the mobile shopping tools acquired by way of its $4 billion Honey acquisition in 2019.

So far, PayPal has continued to run Honey as a standalone application, website and browser extension, but the super app could incorporate more of its deal-finding functions, price-tracking features and other benefits.

On Wednesday’s earnings call, Schulman revealed the super app would have a few other features as well, including high-yield savings, early access to direct deposit funds and messaging functionality outside of peer-to-peer payments — meaning you could chat with family and friends directly through the app’s user interface.

PayPal hadn’t announced its plans to include a messaging component until now, but the feature makes sense in terms of how people often combine chat and peer-to-peer payments today. For example, someone may want to make a personal request for the funds instead of just sending an automated request through an app. Or, after receiving payment, a user may want to respond with a “thank you,” or other acknowledgment. Currently, these conversations take place outside of the payment app itself on platforms like iMessage. Now, that could change.

“We think that’s going to drive a lot of engagement on the platform,” said Schulman. “You don’t have to leave the platform to message back and forth.”

With the increased user engagement, the company expects to see a bump in average revenue per active account.

Schulman also hinted at “additional crypto capabilities,” which were not detailed. However, PayPal earlier this month increased the crypto purchase limit from $20,000 to $100,000 for eligible PayPal customers in the U.S., with no annual purchase limit. The company also this year made it possible for consumers to check out at millions of online businesses using their cryptocurrencies, by first converting the crypto to cash then settling with the merchant in U.S. dollars.

Though the app’s code is now complete, Schulman said the plan is to continue to iterate on the product experience, noting that the initial version will not be “the be-all and end-all.” Instead, the app will see steady releases and new functionality on a quarterly basis.

However, he did say that early on, the new features would include the high-yield savings, improved bill pay with a better user experience, and more billers and aggregators, as well as early access to direct deposit, budgeting tools and the new two-way messaging feature.

To integrate all the new features into the super app, PayPal will undergo a major overhaul of its user interface.

“Obviously, the [user experience] is being redesigned,” Schulman noted. “We’ve got rewards and shopping. We’ve got a whole giving hub around crowdsourcing, giving to charities. And then, obviously, buy now, pay later will be fully integrated into it. … The last time I counted, it was like 25 new capabilities that we’re going to put into the super app.”

The digital wallet app will also be personalized to the end user, so no two apps are the same. This will be done using both artificial intelligence and machine learning capabilities to “enhance each customer’s experiences and opportunities,” said Schulman.

PayPal delivered an earnings beat in the second quarter with $6.24 billion in revenue, versus the $6.27 billion Wall Street expected, and earnings per share of $1.15, versus the $1.12 expected. Total payment volume from merchant customers also jumped 40% to $311 billion, while analysts had projected $295.2 billion. But the company’s stock slipped due to a lowered outlook for Q3, impacted by eBay’s transition to its own managed payments service.

In addition, PayPal gained 11.4 million net new active accounts in the quarter, to reach 403 million total active accounts.

Powered by WPeMatico

Sila announced Monday it raised $13 million in Series A funding for its banking and payment platform that gives software teams tools to build the next generation of financial products and services.

Revolution Ventures led the round and was joined by existing investors Madrona Venture Group, Oregon Venture Fund and Mucker Capital, as well as Wise co-founder Taavet Hinrikus. The funding brings the total investment to date for Portland, Oregon-based Sila to $20 million.

The company was founded in 2018 by Shamir Karkal, Angela Angelovska, Isaac Hines and Alex Lipton to simplify digital payments and storage in a regulatory compliant way and build on blockchain technology. CEO Karkal has a long history in the fintech space, co-founding Simple, an app unifying various accounts into one accessible bank card, in 2009. It was acquired by BBVA in 2014 for $117 million and shuttered earlier this year.

Karkal told TechCrunch that the idea for Sila was born out of frustration while starting another bank. He saw a need for financial application development, but was hindered by a banking system “still stuck in the 20th century.” He thought consumers expected a different level of service, which is why many flock to fintechs.

However, whenever a business tried to connect existing banking systems, fintechs and cryptocurrency innovators, as it built and scale, would always run into technology and compliance issues, Karkal said.

“The problem with working with banks, is that you have to figure out how to integrate with their mainframe,” he added. “In the process, you end up having to also be compliance experts just to be able to do it.”

Whereas it took Karkal three years to get bank processes set up for other companies, it took Sila 18 months. Its banking APIs enable developers to create their own digital wallets, replacing the need to integrate with legacy financial institutions. Sila also has partnerships with fintech platforms, including Plaid, Alloy, Lithic and Arcus to move money, and is backed by Evolve Bank and Trust.

Sila can now get customers up-and-running in six to eight weeks. And unlike competitors that focus almost exclusively on e-commerce, most of Sila’s customers are doing regulated payments within the fintech, insurtech, commercial real estate and cryptocurrency spaces that tend to be more complex from a compliance basis, Karkal said.

Since the company launched its platform, business was building steadily, and took off in the second half of 2020. The company raised a $7.7 million seed round earlier in the year. In the last 12 months, Sila grew its revenue 10 times and customers’ end users grew over 500% in the last seven months.

Sila will use the new funding to increase headcount, target additional partners and expand product features, including its Ethereum MainNet stablecoin issuance and interoperability between FedWire and the Nacha Automated Clearing House network.

“There is a massive wave of fintechs emerging in the U.S., and we have barely scratched the surface,” Karkal said. “Places like India, Africa and Latin America could accelerate at the same time because they are mainly starting from zero. We are here to ‘arm the rebels’ and help those innovators build applications to give all end users a much better financial experience.”

As part of the investment, Clara Sieg, partner at Revolution Ventures, is joining the company’s board. She told TechCrunch she met the company’s co-founders through the Portland ecosystem.

Revolution tends to look at fintech startups from a consumer angle. Recognizing that the problem with building infrastructure meant dealing with banks, the firm set out how to find a company building the pipes to solve it, she said.

In the landscape of fintech, she considers Dwolla to be a competitor to Sila. Last week, the company raised $21 million to continue developing its API that allows companies to build and facilitate fast payments, specifically with a focus on ACH. However, it comes down to actually signing up customers, and that competitive landscape is pretty thin, Sieg added.

“Sila is building an easy way for people to program money and taking a regulatory eye to things,” Sieg said. “When Shamir was building Simple, he could see how challenging it was for incumbents to provide the tools developers need to embed financial services, and this is why we have confidence in his ability to win.”

Powered by WPeMatico

Is the trading boom of 2020 and 2021 slowing?

That’s a question The Exchange has had on its mind since Robinhood released its latest IPO filing. The popular U.S. consumer-focused investing app told investors in the document that it expects revenues to decline in the third quarter compared to its Q2 performance. The company highlighted historically strong crypto volumes in preceding quarters as part of the reason for its anticipated revenue decline.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Naturally, we got to thinking about Coinbase.

It’s likely fair to say that Coinbase and Robinhood are bullish enough about the cryptocurrency market to be unbothered by short-term changes to crypto trading volumes. Coinbase discussed rising and falling consumer interest in trading cryptos in its own IPO filings, for example.

The now-public unicorn has lived through crypto ups and crypto downs. A decline in consumer interest in the next few months or quarters is not a huge deal, assuming one keeps a long enough perspective and the crypto-infused future that its fans expect comes to pass.

The boom in crypto demand among U.S. consumers lifted many a boat in recent quarters. Coinbase posted insanely good early-2021 results thanks to a bull run in cryptocurrency prices that drove retail interest and trading fees. Robinhood also saw a rush of crypto demand, something that TechCrunch explored here. And Square itself has seen crypto revenues explode.

The boom in crypto demand among U.S. consumers lifted many a boat in recent quarters. Coinbase posted insanely good early-2021 results thanks to a bull run in cryptocurrency prices that drove retail interest and trading fees. Robinhood also saw a rush of crypto demand, something that TechCrunch explored here. And Square itself has seen crypto revenues explode.

Sure, equities interest and demand for options also elevated the fortune of many consumer fintechs during the COVID-19 savings and investing boom. But crypto revenues had a big part to play. Let’s examine both situations through the lens of the latest from Robinhood.

There are some 316 mentions of “cryptocurrency” in Robinhood’s latest IPO filing. We’re going to stick to those we consider the most important.

As context, Robinhood shared preliminary Q2 data. We discussed it here if you want to go deeper into the aggregate figures. But after its disclosure of hard numbers, Robinhood had some interesting notes about the current quarter (emphasis TechCrunch):

Trading activity was particularly high during the first two months of the 2021 period, returning to levels more in line with prior periods during the last few weeks of the quarter ended June 30, 2021, and remained at similar levels into the early part of the third quarter. We expect our revenue for the three months ending September 30, 2021 to be lower, as compared to the three months ended June 30, 2021, as a result of decreased levels of trading activity relative to the record highs in trading activity, particularly in cryptocurrencies, during the three months ended June 30, 2021, and expected seasonality.

And in a discussion of some other performance metrics, including funded accounts and the like, Robinhood had this to say (emphasis TechCrunch):

We anticipate the rate of growth in these Key Performance Metrics will be lower for the period ended September 30, 2021, as compared to the three months ended June 30, 2021, due to the exceptionally strong interest in trading, particularly in cryptocurrencies, we experienced in the three months ended June 30, 2021, and seasonality in overall trading activities.

Falling revenue and slowing KPM growth is not really the world’s best set of metrics to flash up during an IPO run. But a quick scan of Robinhood’s 2020 revenues indicates it’s unlikely that the unicorn will be able to post year-over-year growth in the final two quarters of 2021. Still, its period of rapid-fire revenue growth appears to have come to an end after Robinhood posted top-line expansion in every quarter since Q4 2019.

Powered by WPeMatico

While retail investors grew more comfortable buying cryptocurrencies like Bitcoin and Ethereum in 2021, the decentralized application world still has a lot of work to do when it comes to onboarding a mainstream user base.

Phantom is part of a new class of crypto startups looking to build infrastructure that streamlines blockchain-based applications and provides a more user-friendly UX for navigating the crypto world, something that can make the entire space more approachable to a non-developer audience. Users can download the Phantom wallet to their browsers to interact with applications, swap tokens and collect NFTs.

The crypto wallet startup has banked a $9 million Series A round led by Andreessen Horowitz (a16z), with Variant Fund, Jump Capital, DeFi Alliance, Solana Foundation and Garry Tan also participating. The round, which closed earlier this summer, comes as some venture capital firms embrace a crypto future even as volatility continues to envelop the broader market. Last month, a16z announced a whopping 2.2 billion crypto fund, the firm’s largest vertical-specific investment vehicle ever.

Image via Phantom

The co-founding team of CEO Brandon Millman, CPO Chris Kalani and CTO Francesco Agosti all come aboard from crypto infrastructure startup 0x.

At the moment, Phantom is best-known among the Solana community, where it has become the go-to wallet for applications on that blockchain. The startup’s ambition is to interface with more and more networks, currently building out compatibility with Ethereum and looking to embrace other blockchains, aiming to be a product built for a “multichain world,” Millman tells TechCrunch.

Alongside building out support for other networks, Phantom wants to build more sophisticated DeFi mechanisms right into their wallet, allowing users to stake cryptocurrencies and swap more tokens inside the wallet.

The startup says they have some 40,000 users of their existing wallet product.

Building out a presence on the popular Ethereum blockchain, which already has a handful of popular wallet providers, will be a challenge, but Phantom’s broadest challenge is helping a new breed of crypto-curious users interface with a network of apps that still have a long way to go when it comes to being mainstream-friendly.

“The entire space is kind of stuck in this ‘built by developers for other developers mode,’ ” Millman says. “This bar has been kind of stuck there, and no one is really stepping up to push the bar up higher.”

Powered by WPeMatico

In the wake of Coinbase’s direct listing earlier this year, other crypto companies may be looking to go public sooner than later. That appears to be the case with Circle, a Boston-based technology company that provides API-delivered financial services and a stablecoin.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Circle will not direct list or pursue a traditional IPO. Instead, the company is combining with Concord Acquisition Corp., a SPAC, or blank-check company. The transaction values the crypto shop at an enterprise value of $4.5 billion and an equity value of around $5.4 billion.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

Circle’s SPAC presentation details a company whose core business deals with a stablecoin — a crypto asset pegged to an external currency, in this case, the U.S. dollar — and a set of APIs that provide crypto-powered financial services to other companies. It also owns SeedInvest, an equity crowdfunding platform, though Circle appears to generate the bulk of its anticipated revenues from its other businesses.

For more on the deal itself, TechCrunch’s Romain Dillet has a piece focused on the transaction. Here, we’ll dig into the company’s investor presentation, talk about its business model, and riff on its historical and anticipated results and valuation multiples.

In short, we get to have a little fun. Let’s begin.

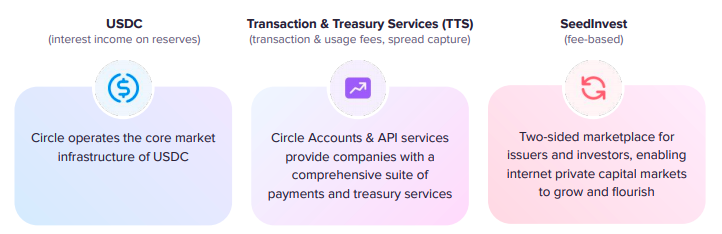

As noted above, Circle has three main business operations. Here’s how it describes them in its deck:

Image Credits: Circle investor presentation

Let’s consider each one, starting with USDC.

Stablecoins have become popular in recent quarters. Because they are pegged to an external currency, they operate as an interesting form of cash inside the crypto world. If you want to have on-chain buying power, but don’t want to have all your value stored in more volatile, and tax-inducing, cryptos that you might have to sell to buy anything else, stablecoins can operate as a more stable sort of liquid currency. They can combine the stability of the U.S. dollar, say, and the crypto world’s interesting financial web.

Powered by WPeMatico

Mercuryo, a startup that has built a cross-border payments network, has raised $7.5 million in a Series A round of funding.

The London-based company describes itself as “a crypto infrastructure company” that aims to make blockchain useful for businesses via its “digital asset payment gateway.” Specifically, it aggregates various payment solutions and provides fiat and crypto payments and payouts for businesses.

Put more simply, Mercuryo aims to use cryptocurrencies as a tool for putting in motion next-gen, cross-border transfers or, as it puts it, “to allow any business to become a fintech company without the need to keep up with its complications.”

“The need for fast and efficient international payments, especially for businesses, is as relevant as ever,” said Petr Kozyakov, Mercuryo’s co-founder and CEO. While there is no shortage of companies enabling cross-border payments, the startup’s emphasis on crypto is a differentiator.

“Our team has a clear plan on making crypto universally available by enabling cheap and straightforward transactions,” Kozyakov said. “Cryptocurrency assets can then be used to process global money transfers, mass payouts and facilitate acquiring services, among other things.”

Image Credits: Left to right: Alexander Vasiliev, Greg Waisman, Petr Kozyakov / MercuryO

Mercuryo began onboarding customers at the beginning of 2019, and has seen impressive growth since with annual recurring revenue (ARR) in April surpassing over $50 million. Its customer base is approaching 1 million, and the company has partnerships with a number of large crypto players including Binance, Bitfinex, Trezor, Trust Wallet, Bithumb and Bybit. In 2020, the company said its turnover spiked by 50 times while run-rate turnover crossed $2.5 billion in April 2021.

To build on that momentum, Mercuryo has begun expanding to new markets, including the United States, where it launched its crypto payments offering for B2B customers in all states earlier this year. It also plans to “gradually” expand to Africa, South America and Southeast Asia.

Target Global led Mercuryo’s Series A, which also included participation from a group of angel investors and brings the startup’s total raised since its 2018 inception to over $10 million.

The company plans to use its new capital to launch a cryptocurrency debit card (spending globally directly from the crypto balance in the wallet) and continuing to expand to new markets, such as Latin America and Asia-Pacific.

Mercuryo’s various products include a multicurrency wallet with a built-in crypto exchange and digital asset purchasing functionality, a widget and high-volume cryptocurrency acquiring and OTC services.

Kozyakov says the company doesn’t charge for currency conversion and has no other “hidden fees.”

“We enable instant and easy cross-border transactions for our partners and their customers,” he said. “Also, the money transfer services lack intermediaries and require no additional steps to finalize transactions. Instead, the process narrows down to only two operations: a fiat-to-crypto exchange when sending a transfer and a crypto-to-fiat conversion when receiving funds.”

Mercuryo also offers crypto SaaS products, giving customers a way to buy crypto via their fiat accounts while delegating digital asset management to the company.

“Whether it be virtual accounts or third-party customer wallets, the company handles most cryptocurrency-related processes for banks, so they can focus more on their core operations,” Kozyakov said.

Mike Lobanov, Target Global’s co-founder, said that as an experiment, his firm tested numerous solutions to buy Bitcoin.

“Doing our diligence, we measured ‘time to crypto’ – how long it takes from going to the App Store and downloading the app until the digital assets arrive in the wallet,” he said.

Mercuryo came first with 6 minutes, including everything from KYC and funding to getting the cryptocurrency, according to Lobanov.

“The second-best result was 20 minutes, while some apps took forever to process our transaction,” he added. “This company is a game-changer in the field, and we are delighted to have been their supporters since the early days.”

Looking ahead, the startup plans to release a product that will give businesses a way to send instant mass payments to multiple customers and gig workers simultaneously, no matter where the receiver is located.

Powered by WPeMatico