cryptocurrencies

Auto Added by WPeMatico

Auto Added by WPeMatico

To become a global fintech player, locate your company in San Francisco and Africa.

That’s the approach of payments company Flutterwave, digital lending startup Mines, and mobile-money venture Chipper Cash—Africa-founded ventures that maintain headquarters in San Francisco and operations in Africa to tap the best of both worlds in VC, developers, clients, and the frontier of digital finance.

This arrangement wasn’t exactly coordinated across the ventures, but TechCrunch coverage picked up the trend and some common motives among these rising fintech firms.

Founded in 2016 by Nigerians Iyinoluwa Aboyeji and Olugbenga Agboola, Flutterwave has positioned itself as a global B2B payments solutions platform for companies in Africa to pay other companies on the continent and abroad.

Clients can tap its APIs and work with Flutterwave developers to customize payments applications. Existing customers include Uber, Booking.com and African e-commerce unicorn Jumia.com.

The Y-Combinator backed company is headquartered in San Francisco, runs its operations center in Nigeria, and plans to add offices in South Africa and Cameroon.

Flutterwave opened an office in Uganda in June and raised a $10 million Series A round in October. The company also plugged into ledger activity in 2018, becoming a payment processing partner to the Ripple and Stellar blockchain networks.

Powered by WPeMatico

Social investing and trading platform eToro announced that it has acquired Danish smart contract infrastructure provider Firmo for an undisclosed purchase price.

Firmo’s platform enables exchanges to execute smart financial contracts across various assets, including crypto derivatives, and across all major blockchains. Firmo founder and CEO Dr. Omri Ross described the company’s mission as “…enabl[ing] our users to trade any asset globally with instant settlement by tokenizing assets and executing all essential trade processes on the blockchain.” Firmo’s only disclosed investment, according to data from Pitchbook, came in the form of a modest pre-seed round from the Copenhagen Fintech Lab accelerator.

Firmo’s mission aligns well with that of eToro — which is equal parts trading platform, social network and educational resource for beginner investors — with the company having long communicated hopes of making the capital markets more open, transparent and accessible to all users and across all assets. By gobbling up Firmo, eToro will be able to accelerate its development of offerings for tokenized assets.

The acquisition represents the latest step in eToro’s broader growth plan, which has ramped up as of late. Earlier in March, the company launched a crypto-only version of its platform in the US, as well as a multi-signature digital wallet where users can store, send and receive cryptocurrencies.

The Firmo deal and eToro’s other expansion activities fit squarely into the company’s belief in the tokenization of assets and the immense, sector-defining opportunity that it creates. Etoro believes that asset tokenization and the movement of financial services onto the blockchain are all but inevitable and the company has employed the long-tailed strategy of investing heavily in related blockchain and crypto technologies despite the ongoing crypto winter.

“Blockchain and the tokenization of assets will play a major role in the future of finance,” said eToro co-founder and CEO Yoni Assia. “We believe that in time all investible assets will be tokenized and that we will see the greatest transfer of wealth ever onto the blockchain.” Assia expressed a similar sentiment in a recent conversation with TechCrunch, stating “We think [the tokenization of assets] is a bigger opportunity than the internet…”

After the acquisition, Firmo will operate as an internal R&D arm within eToro focused on developing blockchain-oriented trade execution and the infrastructure behind the digital representation of tokenized assets.

“The Firmo team has done ground-breaking work in developing practical applications for blockchain technology which will facilitate friction-less global trading,” said Assia.

“The adoption of smart contracts on the blockchain increases trust and transparency in financial services. We are incredibly proud and excited that [Firmo] will be joining the eToro family. We believe that together we have a very bright future and look forward to pursuing our shared goal to become the first truly global service provider allowing people to trade, invest and save.”

Powered by WPeMatico

Crypto represent a “border-less” asset that anyone can own, but actually getting hold of it isn’t easy for everyone. Amun, a company that wants to make buying crypto as easy as stock, has pulled in $4 million in funding to offer more established channels for crypto ownership.

The startup currently offers punters an ETP (exchange-traded product) on the Swiss Stock Exchange that pulls together five of the most popular crypto assets: Bitcoin, Ethereum, Bitcoin Cash, XRP and Litecoin. HODL — as it is called after “holding” crypto rather than selling it (LOL) — can be purchased just like any stock.

That five-crypto basket is just the start for Amun, which is developing ETPs for other crypto assets individually. The first one is for Bitcoin — ABTC — with others planned to come soon; you’d imagine the usual suspects such as Ethereum and co will follow. Indeed, Amun has licenses to the five crypto assets in HODL as well as EOS.

While the products are ETP and not covered by Collective Investment Schemes Act (CISA), they are protected in custody and by insurance. They are collateralized and backed by an identical amount of crypto assets.

Personally, I’ve been able to buy crypto — just base tokens like Bitcoin and Ethereum rather than company-specific ICO tokens — but it certainly is true that it takes some learning. While, speaking for me and likely many others, exchange-based products aren’t easier to me, it does appeal to more institutionally minded individuals or companies for whom holding an account with an exchange or a crypto wallet isn’t feasible. That’s the target that Amun has in mind, as well as outlier cases, too.

Amun CEO and co-founder Hany Rashwan told TechCrunch that growing up in Egypt, he saw the government ban Bitcoin despite the fact that it offered an alternative to the Egyptian pound, which saw its valuation tank massively in 2016. He believes that products like Amun allow anyone to take part in crypto even when they face local restrictions, as was the case in Egypt and other countries.

“We want to make investing in crypto as easy as buying a stock. Institutional investors around the world are looking for a secure, easy and regulated way of accessing the crypto asset class. Amun’s products do that at a low price in one of the most reputable financial hubs in the world,” Rashwan told TechCrunch.

Investors share his optimism and those who took part in this round include Boost VC founder Adam Draper — son of outspoken pro-Bitcoin VC Tim Draper — Graham Tuckwell, founder of ETFS Capital who built ETF products for gold, and Greg Kidd, co-founder of investment firm Hard Yaka. Four undisclosed family offices also took part.

One reason for their optimism is the fact that Amun is developing technology that could, in theory, be licensed out to allow others to develop their own ETFs.

“We invest a ton of resources in both our product development and underlying tech infrastructure. This allows us to come up with innovative but professional and safe ways of accessing the crypto asset class, as well as do all this on a tech platform that can be used by not just us, but any issuer that wishes to do the same as well,” Rashwan said.

“The world needs a company like Amun to make crypto as easy as buying a stock. Now that they were the first to do that, they can now provide the toolset and be the de facto platform for anyone else looking to take their crypto assets/securities to the public markets,” Draper added.

Still, just giving people access doesn’t guarantee returns — that’s on the crypto market itself.

Last year was a dud across the board in terms of pricing, as Bitcoin, for example, plummeted from a record high of nearly $20,000 at the end of 2017 to $3,930-ish at the time of writing. Plenty in the industry are optimistic that will change as genuine value comes out of blockchain technology.

HODL itself debuted at $15.64 last November; today it is at $12.83

Note: The author owns a small amount of cryptocurrency. Enough to gain an understanding, not enough to change a life.

Powered by WPeMatico

Taiwanese technology giant Foxconn International is backing Carbon Relay, a Boston-based startup emerging from stealth today that’s harnessing the algorithms used by companies like Facebook and Google for artificial intelligence to curb greenhouse gas emissions in the technology industry’s own backyard — the data center.

Already, the computing demands of the technology industry are responsible for 3 percent of total energy consumption — and the addition of new technologies like Bitcoin to the mix could add another half a percent to that figure within the next few years, according to Carbon Relay’s chief executive, Matt Provo.

That’s $25 billion in spending on energy per year across the industry, Provo says.

A former Apple employee, Provo went to Harvard Business School because he knew he wanted to be an entrepreneur and start his own business — and he wanted that business to solve a meaningful problem, he said.

Variability and dynamic nature of the data center relating to thermodynamics and the makeup of a facility or building is interesting for AI because humans can’t keep up.

“We knew what we wanted to focus on,” said Provo of himself and his two co-founders. “All three of us have an environmental sciences background as well… We were fired up about building something that was true AI that has positive value… the risk associated [with climate change] is going to hit in our lifetime, we were very inspired to build a company whose technology would have an impact on that.”

Carbon Relay’s mission and founding team, including Thibaut Perol and John Platt (two Harvard graduates with doctorates in applied mathematics) was able to attract some big backers.

The company has raised $6 million from industry giants like Foxconn and Boston-based angel investors, including Dr. James Cash — a director on the boards of Walmart, Microsoft, GE and State Street; Black Duck Software founder, Douglas Levin; Karim Lakhani, a director on the Mozilla Corporation board; and Paul Deninger, a director on the board of the building operations management company, Resideo (formerly Honeywell).

Provo and his team didn’t just raise the money to tackle data centers — and Foxconn’s involvement hints at the company’s broader goals. “My vision is that commercial HVAC systems or any machinery that operates in a business would not ship without our intelligence inside of it,” says Provo.

What’s more compelling is that the company’s technology works without exposing the underlying business to significant security risks, Provo says.

“In the end all we’re doing are sending these floats… these values. These values are mathematical directions for the actions that need to be taken,” he says.

Carbon Relay is already profitable, generating $4 million in revenue last year and on track for another year of steady growth, according to Provo.

Carbon Relay offers two products: Optimize and Predict, that gather information from existing HVAC devices and then control those systems continuously and automatically with continuous decision making.

“Each data center is unique and enormously complex, requiring its own approach to managing energy use over time,” said Cash, who’s serving as the company’s chairman. “The Carbon Relay team is comprised of people who are passionate about creating a solution that will adapt to the needs of every large data center, creating a tangible and rapid impact on the way these organizations do business.”

Powered by WPeMatico

The Intercontinental Exchange’s (ICE) cryptocurrency project Bakkt celebrated New Year’s Eve with the announcement of a $182.5 million equity round from a slew of notable institutional investors. ICE, the operator of several global exchanges, including the New York Stock Exchange, established Bakkt to build a trading platform that enables consumers and institutions to buy, sell, store and spend digital assets.

This is Bakkt’s first institutional funding round; it was not a token sale. Participating in the round are Horizons Ventures, Microsoft’s venture capital arm (M12), Pantera Capital, Naspers’ fintech arm (PayU), Protocol Ventures, Boston Consulting Group, CMT Digital, Eagle Seven, Galaxy Digital, Goldfinch Partners and more.

Bakkt is currently seeking regulatory approval to launch a one-day physically delivered Bitcoin futures contract along with physical warehousing. The startup initially planned for a November 2018 launch, but confirmed this morning an earlier CoinDesk report that it was delaying the launch to “early 2019” as it awaits permission from the Commodity Futures Trading Commission. Along with the funding, crypto news blog The Block Crypto also reports Bakkt has hired Balaji Devarasetty, a former vice president at Vantiv, as its head technology.

ICE’s crypto project was first announced in August and is led by chief executive officer Kelly Loeffler, ICE’s long-time chief communications and marketing officer. Bakkt quickly inked partnerships with Microsoft, which provides cloud infrastructure to the service, and Starbucks, to develop “practical, trusted and regulated applications for consumers to convert their digital assets into U.S. dollars for use at Starbucks,” Starbucks vice president of payments Maria Smith said in a statement at the time.

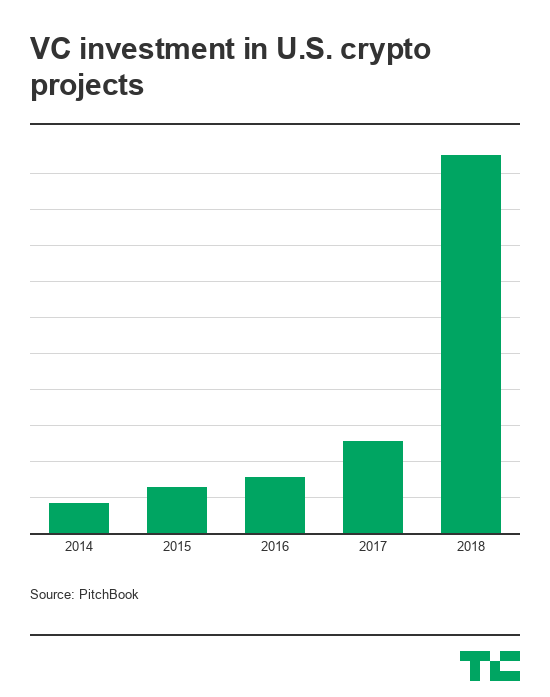

Many Bitcoin startups floundered in 2018, despite record amounts of venture capital invested in the industry. This was as a result of failed initial coin offerings, an inability to scale following periods of rapid growth and the falling price of Bitcoin. Still, VCs remained bullish on Bitcoin and blockchain technology in 2018, funneling a total of $2.2 billion in U.S.-based crypto projects — a nearly 4x increase year-over-year. Around the globe, investment hit a high of $4.6 billion — a more than 4x increase from last year, according to PitchBook.

“Notably, 2018 was the most active year for crypto in its brief ten-year history,” Loeffler wrote. “This was evidenced by rising investment in distributed ledger technology and digital assets, as well as by blockchain network metrics such as daily bitcoin transaction value and active addresses. Yet, these milestones tend to be overshadowed by the more narrow focus on bitcoin’s price, which has been seen by some, as a proxy for the potential of the technology.”

Today, the price of Bitcoin is hovering around $3,700 one year after a historic run valued the cryptocurrency at roughly $20,000. The crash caused many to dismiss Bitcoin and its underlying technology, while others remained committed to the tech and its potential for complete financial disruption. A project like Bakkt, created in-house at a respected financial institution with support from noteworthy businesses, is a logical bet for crypto and traditional private investors alike.

“The path to developing new markets is rarely linear: progress tends to modulate between innovation, dismissal, reinvention, and, finally, acceptance,” Loeffler added. “Each step, whether part of discovery or adversity, ultimately strengthens the product. Twenty years ago, it was controversial to suggest that commodities or bonds could trade electronically on a screen, and many steps were required for that evolution to play out.”

Powered by WPeMatico

Chris Hays and Mark Jeffrey wanted to create a way for everyone to be able to tell their loved ones if they were in trouble. Their first product, Guardian Circle, did just that, netting a mention a few years ago. Now the same team is truly decentralizing alerts with a new token called, obviously, Guardium.

The plan is to create an ad hoc network of helpers and first responders. “Guardium and Guardian Circle together open the emergency response grid to vetted citizens, private response and compatible devices for the very first time,” write the founders. “Providing an economic framework on our global distributed emergency response network; Guardium brings first responders to the 4 billion people on the planet without government-sponsored emergency response.”

Because the product already works, the team is taking on the token sale as a new challenge.

“We’re serial entrepreneurs — both of us have been venture-backed in the past by names like SoftBank and Intel, and we’ve been senior execs in companies backed by Sequoia and Elon Musk. Transitioning to the token sale-backed universe has been an interesting study in contrasts,” said Hays. “There are a number of ‘panic button apps’ — but without exception, all of them have forgotten ‘the second half of the problem’ — organizing the response. Getting people who do not know one another into instant communication and location sharing during an emergency — the importance of that cannot be overstated.”

The founders found that their idea wasn’t fundable in the valley. After all, what VC wants to help people when they can invest in Snapchat? Instead, Hays and Jeffrey are aiming bigger.

“We’re rebooting the world’s safety grid,” said Hays. “We’re creating a new global public utility. And we want it to service everyone, everywhere on earth. Although it is a very big vision, and it is a capitalist, multibillion dollar ecosystem that we’re chasing — it’s still a very different vision, and not the one venture capitalists are looking for.”

The token works to create a flash mob of help. Guard tokens pay first responders and dispatchers and “cities, campuses, and resorts stake $GUARD to access Alerts created within their geofenced borders,” allowing local folks to help immediately. They’ve sold half of their hard cap of $10 million thus far.

While tokens are always an iffy investment, this team has produced product and, more important, it’s clear they’ll never raise venture. A token, no matter how it’s used in the future, seems like a solid solution.

Powered by WPeMatico

Bitcoin turned 10 years old, a milestone for a technology that few have used and even fewer understand. Ultimately, the blockchain it wrought could be the biggest change to banking, finance and politics ever — or it could be a dud. The jury is still out, but let’s take a walk down memory lane and see just how the product grew from White Paper to world beater.

Powered by WPeMatico

Minds, a decentralized social network, has raised $6 million in Series A funding from Medici Ventures, Overstock.com’s venture arm. Overstock CEO Patrick Byrne will join the Minds Board of Directors.

What is a decentralized social network? The creators, who originally crowdfunded their product, see it as an anti-surveillance, anti-censorship, and anti-“big tech” platform that ensures that no one party controls your online presence. And Minds is already seeing solid movement.

“In June 2018, Minds saw an enormous uptick in new Vietnamese of hundreds of thousands users as a direct response to new laws in the country implementing an invasive ‘cybersecurity’ law which included uninhibited access to user data on social networks like Facebook and Google (who are complying so far) and the ability to censor user content,” said Minds founder Bill Ottman.

“There has been increasing excitement in recent years over the power of blockchain technology to liberate individuals and organizations,” said Byrne. “Minds’ work employing blockchain technology as a social media application is the next great innovation toward the mainstream use of this world-changing technology.”

Interestingly, Minds is a model for the future of hybrid investing, a process of raising some cash via token and raising further cash via VC. This model ensures a level of independence from investors but also allows expertise and experience to presumably flow into the company.

Ottman, for his part, just wants to build something revolutionary.

“The rise of an open source, encrypted and decentralized social network is crucial to combat the big-tech monopolies that have abused and ignored users for years. With systemic data breaches, shadow-banning and censorship, people over the world are demanding a digital revolution. User-safety, fair economies, and global freedom of expression depend on it – we are all in this battle together,” said Ottman.

Powered by WPeMatico

Many doubted The Civil Media Company‘s ambitious plan to sell $8 million worth of its cryptocurrency, called CVL.

The skeptics, as it turns out, were right. Civil’s initial coin offering, meant to fund the company’s effort to create a new economy for journalism using the blockchain, failed to attract sufficient interest. The company announced today that it would provide refunds to all CVL token buyers by October 29.

Civil’s goal was to sell 34 million CVL tokens for between $8 million and $24 million. The sale began on September 18 and concluded yesterday. Ultimately, 1,012 buyers purchased $1,435,491 worth of CVL tokens. A spokesperson for Civil told TechCrunch an additional 1,738 buyers successfully registered for the sale, but never completed their transaction.

Civil isn’t giving up. The company says “a new, much simpler token sale is in the works,” details of which will be shared soon. Once those new tokens are distributed, Civil will launch three new features: a blockchain-publishing plugin for WordPress, a community governance application called The Civil Registry and a developer tool for non-blockchain developers to build apps on Civil.

ConsenSys, a blockchain venture studio that invested $5 million in Civil last fall, has agreed to purchase $3.5 million worth of those new tokens. The purchase is not an equity; all capital from the token sale is committed to the Civil Foundation, an independent nonprofit initially funded by Civil that funds grants to the newsrooms in Civil’s network.

In a blog post today, Civil chief executive officer Matthew Iles wrote that the token sale failure was a disappointment but not a shock. Days prior, he’d authored a separate post where he admitted things weren’t looking good.

“This isn’t how we saw this going,” Iles wrote. “The numbers will show clearly enough that we are not where we wanted to be at this point in the sale when we started out. But one thing we want to say at the top is that until the clock strikes midnight on Monday, we are still working nonstop on the goal of making our soft cap of $8 million.”

A recent Wall Street Journal report claimed Civil had reached out to The New York Times, The Washington Post, Dow Jones and Axios, among others, but failed to incite interest in its token.

Separate from its token sale, Civil has inked strategic partnerships with media companies like the Associated Press and Forbes, both of which confirmed to TechCrunch today that the failed token sale doesn’t impact their partnerships with Civil.

Forbes became the first major media brand to test Civil’s technology when it announced earlier this month that it would experiment with publishing content to the Civil platform. As for the AP, it granted the newsrooms in Civil’s network licenses to its content.

Civil, of course, isn’t the only blockchain startup targeting journalism. Nwzer, Userfeeds, Factmata and Po.et, which was founded by Jarrod Dicker, a former vice president at The Washington Post, are all trying their hand at bringing the new technology to the content industry.

Which, if any, will actually find success in the complicated space, is the question.

Powered by WPeMatico

SpankChain, a cryptocurrency aimed at decentralized sex cams, has announced that a hacker stole about $38,000 from their payment channel thanks to a broken smart contract. They wrote:

At 6pm PST Saturday, an unknown attacker drained 165.38 ETH (~$38,000) from our payment channel smart contract which also resulted in $4,000 worth of BOOTY on the contract becoming immobilized. Of the stolen/immobilized ETH/BOOTY, 34.99 ETH (~$8,000) and 1271.88 BOOTY belongs to users (~$9,300 total), and the rest belonged to SpankChain.

Our immediate priority has been to provide complete reimbursements to all users who lost funds. We are preparing an ETH airdrop to cover all $9,300 worth of ETH and BOOTY that belonged to users. Funds will be sent directly to users’ SpankPay accounts, and will be available as soon as we reboot Spank.Live.

The hacker used a ‘reentrancy’ bug in which the user calls the same transfer multiple times, draining a little Ethereum each time. The bug is the same one that previously affected the DAO.

The company pointed out that a security audit on their smart contract would have cost $50,000, a bit more than the amount lost. “As we move forward and grow, we will be stepping up our security practices, and making sure to get multiple internal audits for any smart contract code we publish, as well as at least one professional external audit,” they wrote.

I’ve reached out to the company for clarification but in short it seems the spanker has become the spankee.

Powered by WPeMatico