CrunchBase

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about Stripe’s grand plans. Before that, I noted Peloton’s secret weapons.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

The best companies are built by people who have personally experienced the problem they’re attempting to solve. Lauren Jonas, the founder and chief executive officer of Part & Parcel, is intimately familiar with the struggles faced by the women she’s building for.

San Francisco-based Part & Parcel is a plus-sized clothing and shoe startup providing dimensional sizing to women across the U.S. The company operates a bit differently than your standard direct-to-consumer business by seeking to include the women who wear and evangelize the Part & Parcel designs by giving them a cut of their sales.

Here’s how it works: Ambassadors sign up to receive signature styles from Part & Parcel, which they then share and sell to women in their network. Ultimately, the sellers are eligible to receive up to 30% of the profit per sale. The out-of-the-box model, which might remind you somewhat of Mary Kay or Tupperware’s business strategy, is meant to encourage a sense of community and usher in a new era in which plus-sized women can facilitate other plus-sized women’s access to great clothes.

“I bought a brown men’s polyester suit and wore it to an interview,” Jonas, an early employee at Poshmark and the long-time author of the popular blog, ‘The Pear Shape,’ tells TechCrunch. “I was that kid wearing a men’s suit.”

Clothing tailored to plus-sized women has long been missing from the retail market. Increasingly, however, new brands are building thriving businesses by catering precisely to the historically forgotten demographic. Dia&Co., for example, raised another $70 million in venture capital funding last fall from Sequoia and USV. And Walmart recently acquired another brand in the space, ELOQUII, for an undisclosed amount. Part & Parcel, for its part, has raised $4 million in seed funding in a round led by Lightspeed Venture Partners’ Jeremy Liew.

The startup launched earlier this year in Anchorage, “a clothing desert,” and has since grown its network to include women in several other underserved markets. Given her own history struggling to find a fitted woman’s suit, Jonas launched her line with structured pieces, including suits and blouses — though the startup’s biggest success yet, she says, has been its boots, which come in three different calf width options.

“Seventy percent of women in this country are plus-sized,” Jonas said. “I’m bringing plus out of the dark corner of the department store.”

Image: Bryce Durbin / TechCrunch

TechCrunch’s Megan Rose Dickey published a highly anticipated deep dive on the state of sex tech this week. The piece provides new data on funding in sex tech and wellness companies, analysis on sex tech startup’s battle for public advertising and responses from industry leaders on how we can destigmatize sex with technology. Here’s a short passage from the story:

Cindy Gallop sees a market opportunity in every type of business obstacle she encounters. That’s why All The Sky will also seek to invest in startups that tackle the infrastructural tools needed to fuel sextech, like payments, hosting providers and e-commerce sites.

“I want to fund the sextech ecosystem to maintain and sustain a portfolio for All the Skies, to create a bloody huge sextech ecosystem and three, to monopolistically build out the ecosystem to be a multi-trillion-dollar market,” Gallop says.

I swung by Contrary Capital‘s Demo Day this week, in which a number of startups gave a 4- to 5-minute pitch. Next on my list is Alchemist‘s Demo Day in Menlo Park. The accelerator welcomes enterprise startups for a six-month program focused on early customer adoption, company development and mentorship.

Also on my radar is Females To The Front. The event began this week in Palm Springs and if I were based in SoCal, I would have swung by. Led by Amy Margolis, the event is said to be the largest gathering of female cannabis founders and funders to date. Here’s how the group describes the event: “Females to the Front Retreat will mix immersive and hands-on workshops, pitch training, investment deck preparation and business skill set education with investor meetings and plenty of shared meals, pool time, yoga, connections, rest and rejuvenation. Every workshop is built to directly engage attendees instead of powerpoint and panels. Be prepared to return home inspired, engaged and with so many more tools in your toolbox.”

For the record, I don’t advertise events in my newsletter just wanted to give props to this one because it’s a great development for the cannabis tech ecosystem.

We are just weeks away from our flagship conference, TechCrunch Disrupt San Francisco. We have dozens of amazing speakers lined up. In addition to taking in the great line-up of speakers, ticket holders can roam around Startup Alley to catch the more than 1,000 companies showcasing their products and technologies. And, of course, you’ll get the opportunity to watch the Startup Battlefield competition live. Past competitors include Dropbox, Cloudflare and Mint… You never know which future unicorn will compete next.

You can take a look at the full agenda here. And if you still need convincing, here’s five reasons to attend this year’s conference from our COO himself.

This week, the lovely Alex Wilhelm, editor-in-chief of Crunchbase News, and I gathered to discuss a number of topics including WeWork’s IPO and Uber’s attempts to bypass a new law meant to protect gig workers. Listen here.

Powered by WPeMatico

Where are all the biotechnology companies raising these days? We crunched some numbers to arrive at an answer.

Using funding rounds data from Crunchbase, we plotted the count of venture capital funding rounds raised by companies in the fairly expansive biotechnology category in Crunchbase. Click the chart below and you can hover over individual data points to see the number of venture rounds raised in a given metro area between the start of 2018 and late May 2019 (as of publication). Although there are biotechnology companies located throughout the world, we focused here on just the U.S.

Unlike in the software-funding business, where New York City (and its surrounding area) ranks second in overall deal volume, the greater Boston metro area outranks the Big Apple in biotech venture deal volume. The SF Bay Area (which includes both San Francisco and the towns in Silicon Valley north and west of San Jose) outranks Boston in biotech deal volume, but, then again, it’s also a much larger geographic area with a higher density of startups overall.

Crunchbase News recently covered a $120 million round raised by immunotherapy upstart AlloVir. In the software business, a raise that large would be notable; however, in the business of biology, not so much.

Just for reference, the average Series B round raised by U.S. enterprise software startups between 2018 and May 2019 was about $22.7 million. The average Series B for biotech companies from that same time period: just about $40 million on the dot.

Spinning up a cluster of cells at a lab bench is costlier, harder to do and the outcomes of experiments are less certain than the results of implementing a new software framework. Add to that the tremendous cost of performing clinical trials and clearing regulatory hurdles — all before costly sales and marketing campaigns to get treatments in front of doctors and end users — and it’s easy to understand why many biotechnology companies need to raise so much money in the early stages of the startup cycle.

Powered by WPeMatico

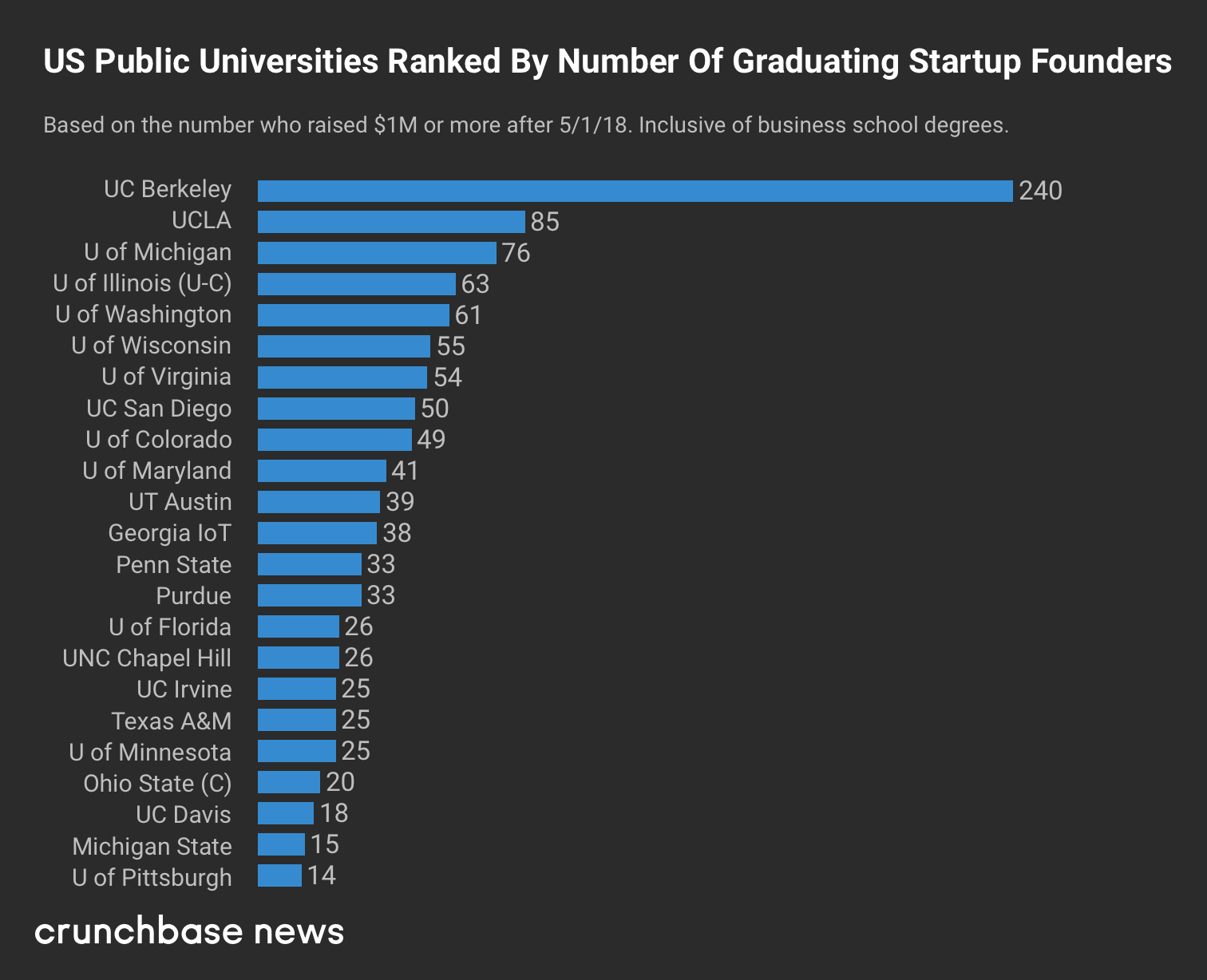

A lot of students attend public universities to lessen the financial burden of higher education. At last tally, tuition and fees at American public colleges and universities averaged around $6,800 a year, per the federal government. That’s far below the $32,600 mean price tag for private, nonprofit institutions.

Yet when it comes to public universities, the old adage “you get what you pay for” clearly does not apply. Leading public research universities in particular have a track record of turning out enviably knowledgeable and successful graduates. That includes a whole lot of funded startup founders.

And that leads us to our latest ranking. At Crunchbase News, we’ve been tracking the intersection of alumni affiliation and startup funding for the past few years. In a story published earlier this week, we looked at which U.S. universities graduated the most founders of startups that raised $1 million or more in roughly the past year.

For today’s follow-up, we’re focusing exclusively on public universities. Starting with a list of top-ranking research universities, we looked to see which have graduated the highest number of funded founders.

For the most part, we used the same criteria as the public-and-private list, focusing on startups that raised $1 million or more after May, 2018. The public list, however, does not separate out business school grads.

Without further ado, here’s the list:

Looking at the list above, a few things stand out. First, our top ranker, University of California at Berkeley, is multiples above the rest of the field when it comes to graduating funded founders.

Berkeley is a school that’s generally hard to get into, prominent in STEM and located in the VC-rich San Francisco Bay Area. So seeing it top the list isn’t necessarily surprising. However, the magnitude of its lead — with nearly three times the funded founders of runner-up UCLA — does warrant attention.

Big Midwestern schools also did well, with University of Michigan and University of Illinois, Urbana-Champaign nabbing the third and fourth spots.

More broadly, the list includes schools from all U.S. regions, including the East Coast, West Coast, South, Midwest and Southwest. So no particular region has a lock on graduating funded entrepreneurs. That’s also not surprising. But it’s good to have some more numbers to back up that notion.

Powered by WPeMatico

Every company’s online acquisition strategy is out in the open. If you know where to look.

This post shows you exactly where to look, and how to reverse engineer their growth tactics.

Why is this important? Competitive analysis de-risks your own growth experiments: You find the best growth ideas to adopt and the worst ones to avoid.

First, a warning: Your goal is not to repurpose another company’s hard work. That makes you a thief. Your goal is to identify other companies who face the same growth challenges as you, then to study their approaches for solutions to draw from.

As I walk through uncovering a competitor’s tactics, keep in mind which competitors are worth looking at: For instance, you should rarely over-analyze early-stage companies. They’re unlikely to be methodical at growth.

Meaning, if you blindly copy their site and their ads, it’s possible you’ll be copying tactics that are not actually responsible for their growth. Their success may instead be from network effects or other hidden factors.

Instead, it’s safest to get inspiration from companies who’ve sustained high growth rates for a long time, and who face the same growth challenges as you. They’re likely to have sophisticated growth operations worth studying deeply. Examples include:

If these aren’t your direct competitors, don’t worry. You don’t need to audit a direct competitor’s tactics to get incredibly valuable insights.

You’ll gain useful insights from auditing the user acquisition funnel of any company who has a similar audience and business model.

Examples of audiences:

Audiences matter because their behaviors and needs differ wildly. Each requires its own growth strategy. You want to audit a company whose audiences is similar to yours.

You also want to ensure the company shares your business model. Examples include:

Each model may necessitate different ads, landing pages, automated emails, and sales collateral.

Never implement another company’s tactics blindly.

There’s an effective process for growth analysis, and it looks like this:

Here’s a brief example before we dive into tactics.

Let’s pretend we’re a SaaS company offering consumer banking tools, and that we’re struggling to get users to onboard our app. Our hypothesis is that visitors are bouncing because they don’t trust us with their sensitive information.

Our first step is to define both our audience and our business model:

Our next step is to look for companies who share those two aspects. (We can find them on Crunchbase.)

Once we have a few in hand, we look for how they handle customers’ sensitive information throughout their funnel. Specifically, we audit their:

It’s time to learn how we audit all that. I’ll share how our marketer training program teaches marketers to do this on the job.

Powered by WPeMatico

Greetings from Seattle, the land of Amazon, Microsoft, two of the world’s richest men and some startups.

I’m always surprised the Seattle startup ecosystem hasn’t grown to compete with the likes of Silicon Valley — or at least Boston and New York City — since the dot-com boom. Today, it’s the strongest it’s been due to the successes of companies like the newly minted unicorn Outreach, trucking business Convoy and, of course, the dog walking startup Rover. But the city still lags behind, failing to adopt the culture of entrepreneurship that defines San Francisco.

I spent a lot of time wondering why it hasn’t reached its full potential. Is it because Microsoft and Amazon pay their employees so well they don’t have the same urge to build something from the ground up? Is it a lack of access to capital? Is the city not attracting top talent? If you have thoughts, send them my way.

“We think part of the issue is a lack of capital and a lack of help,” Rover and Pioneer Square Labs co-founder Greg Gottesman told TechCrunch earlier this year. “If we can provide a little bit of both of those things, we can really put Seattle where it deserves to be, should be and will be.”

Despite its shortcomings, there is still some action in the city I want to highlight this week. A same-day delivery business, Dolly, is on the rise. The startup told me on Thursday it had raised a $7.5 million round from Unlock Venture Partners, Maveron and Jeff Wilke, the chief executive officer of Amazon Worldwide Consumer. Maveron, if you remember, is the VC fund co-founded by Starbucks founder Howard Schultz.

In other Seattle news, Madrona Venture Group, a well-regarded fund, raised an additional $100 million this week. Typically, Madrona focuses on companies based in the Pacific Northwest, but this fund will deploy capital throughout the entire U.S. Hmmm, that’s not necessarily a good sign for Seattle founders, but great progress for the ecosystem nonetheless.

If you’re interested in learning more about Seattle tech, I’ve covered it a bit because it’s my hometown! Start with this story, which dives deep into a Seattle accelerator that’s working hard to encourage entrepreneurship in the city. Alright, on to other news.

Want more TechCrunch newsletters? Sign up here.

WeWork: The co-working giant now known as The We Company submitted confidential IPO documents to the SEC, the company confirmed in a press release Monday. Is this the next massive startup win or a house of cards waiting to be toppled by the glare of the public markets? TechCrunch’s Danny Crichton investigates.

Slack: The business is in its final steps toward a much-anticipated direct listing, with one source telling TechCrunch the listing will be complete within 45 days. The WSJ reported this week that Slack will make an online presentation to potential shareholders on May 13. This week, we dug deep into Slack’s S-1 and decided to evaluate just how well the tech press, us included, did in covering the company. For the most part, the tech press did decently well, except for one curious, $162 million gap.

Uber: Finally! That ride-hailing company is going public next week. That latest news? Uber co-founder Travis Kalanick won’t be ringing the opening bell. Uber would not be where it is today without Kalanick, but him being there would surely be a reminder of Uber’s rocky past.

Beyond Meat: Shares of the company surged up 135 percent in their market opener last week, valuing the company as high as $3.52 billion. Volatility was so high on the company’s stock that the Nasdaq had to pause trading of “BYND” shares.

Ofo has run into its fair share of issues, laying off hundreds of workers, shutting down its international division and more. Now, you can buy a piece of the startup’s history.

Now you can buy a piece of startup history… Ofo bikes for ~$60 https://t.co/LLJbDOXm0C

— Jon Russell (@jonrussell) April 29, 2019

In other micro-mobility news, Lyft’s head of scooter & bikes Liam O’Connor, who was hired to help transportation company Lyft build its bike and scooter operations, has left after seven months with the newly-public company. TechCrunch’s Ingrid Lunden has the scoop. Plus, Bird, the electric scooter unicorn doing its best to overcome regulatory barriers, has made its way back to San Francisco. Bird is using its business license in San Francisco to introduce monthly personal rentals in the city. The program enables people to rent a scooter for $24.99 a month with no cap on the number of rides. We’ll how that goes.

For some reason, people are giving Magic Leap more money. The company has secured another $280 million in a deal with Japan’s largest mobile operator, Docomo. Do you know what that means? The developer fo AR/VR headsets has raised a total of $2.6 billion. We’re just as confused as you.

Brand new venture capital funds:

Unshackled Ventures raised $20 million.

Exclusive: @UnshackledVC has a new $20M pre-seed fund to invest only in immigrants. Why? Because immigrants are “inherently more entrepreneurial:” https://t.co/ZLiZ1UczJV

— Kate Clark (@KateClarkTweets) May 2, 2019

Jungle Ventures closed on $175 million.

And Toyota AI Ventures launched a $100 million fund.

I have the inside story on Menlo Ventures early Uber stake and TechCrunch’s Connie Loizos goes deep with early Uber backer Bradley Tusk.

This week, we offer TechCrunch Extra Crunch subscribers exclusive tips on building extraordinary teams. Plus, the final piece in TechCrunch’s Greg Kumparak’s series on Niantic, the fast-growing developer of Pokemon Go. If you recall, we’ve captured much of Niantic’s ongoing story in the first three parts of our EC-1, from its beginnings as an “entrepreneurial lab” within Google, to its spin-out as an independent company and the launch of Pokémon GO, to its ongoing focus on becoming a platform for others to build augmented reality products upon.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and TechCrunch’s Danny Crichton chat about updates at the Vision Fund, Cheddar’s big exit and more of this week’s headlines.

Powered by WPeMatico

The San Francisco Bay Area is a global powerhouse at launching startups that go on to dominate their industries. For locals, this has long been a blessing and a curse.

On the bright side, the tech startup machine produces well-paid tech jobs and dollars flowing into local economies. On the flip side, it also exacerbates housing scarcity and sky-high living costs.

These issues were top-of-mind long before the unicorn boom: After all, tech giants from Intel to Google to Facebook have been scaling up in Northern California for over four decades. Lately however, the question of how many tech giants the region can sustainably support is getting fresh attention, as Pinterest, Uber and other super-valuable local companies embark on the IPO path.

The worries of techie oversaturation led us at Crunchbase News to take a look at the question: To what extent do tech companies launched and based in the Bay Area continue to grow here? And what portion of employees work elsewhere?

For those agonizing about the inflationary impact of the local unicorn boom, the data offers a bit of reassurance. While companies founded in the Bay Area rarely move their headquarters, their workforces tend to become much more geographically dispersed as they grow.

Just because a company is based in Northern California doesn’t mean most workers are there also. Headquarters, our survey shows, does not always translate into headcount.

“Headquarters location can often be the wrong benchmark to use to identify where employees are located,” said Steve Cadigan, founder of Cadigan Talent Ventures, a Silicon Valley-based talent consultancy. That’s particularly the case for large tech companies.

Among the largest technology employers in Northern California, Crunchbase News found most have fewer than 25 percent of their full-time employees working in the city where they’re headquartered. We lay out the details for 10 of the most valuable regional tech companies in the chart below.

With the exception of Intel, all of these companies have a double-digit percentage of employees at headquarters, so it’s not as if they’re leaving town. However, if you’re a new hire at Silicon Valley’s most valuable companies, it appears chances are greater that you’ll be based outside of headquarters.

Tesla, meanwhile, is somewhat of a unique case. The company is based in Palo Alto, but doesn’t crack the city’s list of top 10 employers. In nearby Fremont, Calif., however, Tesla is the largest city employer, with roughly 10,000 reportedly working at its auto plant there.(Tesla has about 49,000 employees globally.)

High-valuation private and recently public tech companies can also be pretty dispersed.

Although they tend to have a larger percentage of employees at headquarters than more-established technology giants, the unicorn crowd does like to spread its wings.

Take Uber, the poster child for this trend. Although based in San Francisco, the ride-hailing giant has fewer than one-fourth of its employees there. Out of a global workforce of around 22,300, only about 5,000 are SF-based.

It’s unclear if that kind of breakdown is typical. We had trouble assembling similar geographic employee counts at other Bay Area unicorns, mainly because cities break out numbers only for their 10 largest employers. The lion’s share of regional unicorns are San Francisco-based, and of them only Uber made the Top 10.

That said, there is another, rougher methodology for assessing who works at headquarters: job postings. At a number of the most valuable Bay Area-based unicorns — including Airbnb, Juul, Lime, Instacart, Stripe and the now-public Lyft — a high number of open positions are far from the home office. And as we wrote last year, private companies have been actively seeking out cities to set up secondary hubs.

Even for earlier-stage startups, it’s not uncommon to set up headquarters in the San Francisco area for access to financing and networking, while doing the bulk of hiring in another location, Cadigan said. The evolution of collaborative work tools has also enabled more companies to add staff working remotely or in secondary offices.

Plus, of course, unicorn startups tend to be national or global in focus, and that necessitates hiring where their customers are located.

As we wrap up, it’s worth bringing up how unusual it once was for denizens of a metro area to oppose a big influx of high-skill jobs. In the past couple of years, however, these attitudes have become more common. Witness Queens residents’ mixed reactions to Amazon’s HQ2 plans. And in San Francisco, a potential surge of newly minted IPO millionaires is causing some consternation among locals, along with jubilation among the realtor crowd.

Just as college towns retain room for new students by graduating older ones, however, it seems reasonable that sustaining Northern California’s strength as a startup hub requires locating jobs out-of-area as companies scale. That could be good news for other cities, including Austin, Phoenix, Nashville, Portland and others, which have emerged as popular secondary locations for fast-growing unicorns.

That said, we’re not predicting near-term contraction in Bay Area tech employment, particularly of the startup variety. The region’s massive entrepreneurial and venture ecosystem keeps on producing valuable newcomers well-capitalized to keep hiring.

Methodology

We looked only at employment at company headquarters (except for Apple) . Companies on the list may have additional employees based in other Northern California cities. For Apple, we included all Silicon Valley employees, per estimates by the Silicon Valley Business Journal.

Numbers are rounded to the nearest hundred for the largest employers. Most of the data is for full-time employees only. Large tech employers hire predominantly full-time for staff positions, so part-time, whether included or not, is expected to reflect only a very small percentage of employment.

Cities list their 10 largest employers in annual reports. We used either the annual reports themselves or data excerpted in Wikipedia, using calendar year 2017 or 2018.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Kate and Alex are back (again), bringing you the latest on the IPO front. As Friday is coming to a close, we’ll keep this post short to leave plenty of room for you to dig into the audio. Welcome to the weekend.

Up first we dug into Uber’s latest S-1 filing. This time, the company set a price range for itself (TechCrunch’s coverage here), valuing itself at $84 billion and also detailing estimates of its first-quarter results (Crunchbase News’s notes here).

We suspect Uber will ultimately price a top that range. Time will tell.

And then we turned to Slack, who’s direct listing will help set the historical tone for the unicorn era; screw your money, Slack says, we have our own. Well maybe not, but the company has impressive growth, killer margins, and, to our surprise, larger GAAP deficits than we expected. The company’s filing was fascinating.

But worry not, we can figure out how to value Slack. It’s Uber that left us scratching our heads. Expect next week to be another blizzard of news and numbers.

Thanks as always for listening to the show. We’ve never had more downloads than these last few weeks. It means a lot that you want to hang out with us. Don’t forget that we have an email address (equitypod@techcrunch.com), and a hashtag that Alex needs to learn to use: #equitypod.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Venture investors are pouring billions of dollars into feeding their hunger for food and agriculture startups. Whether that trend line is due to enthusiasm for the sector or just broader heavy investing in the VC space is much less clear.

According to a recent report published by AgFunder – a VC and investing marketplace focused on the agriculture and food sectors – the “AgriFood” space is booming. Using data from Crunchbase and several other data partners, the organization published its “2018 AgriFood Tech Investing Report” this morning, finding that investment in AgriFood companies increased 43% year-over-year, reaching $16.9 billion in 2018.

AgFunder classifies AgriFood tech as “the small but growing segment of the startup and venture capital universe that’s aiming to improve or disrupt the global food and agriculture industry.” Their definition is intentionally broad, encompassing everything from crop and livestock biotech, property management systems, and payments, to biomaterials and meat alternatives, all the way up to tech platforms for restaurants, grocers, deliveries and at-home cooks.

While some of the AgriFood tech categories – such as delivery or restaurant software – have long been popular destinations for venture capital, we’re now seeing a more diverse array of startups innovating across the entire food supply chain. According to the report, expansion in AgriFood is fairly consistent across upstream (agricultural and farming) subsectors to downstream (more consumer-facing) subsectors, with each group growing roughly 44% and 42% year-over-year respectively.

The data also shows growth occurring across almost all deal stages. AgriFood saw huge increases in the average deal size and total investment for late-stage companies in particular, as venture-backed startups have grown to global scale. And penetrating and attracting capital from international markets seems more feasible than ever. AgriFood investing, which traditionally has been largely US-centric, is rapidly becoming a global phenomenon, with more than half of total funding – and some of the largest rounds – now coming from companies and investors outside the US.

Powered by WPeMatico

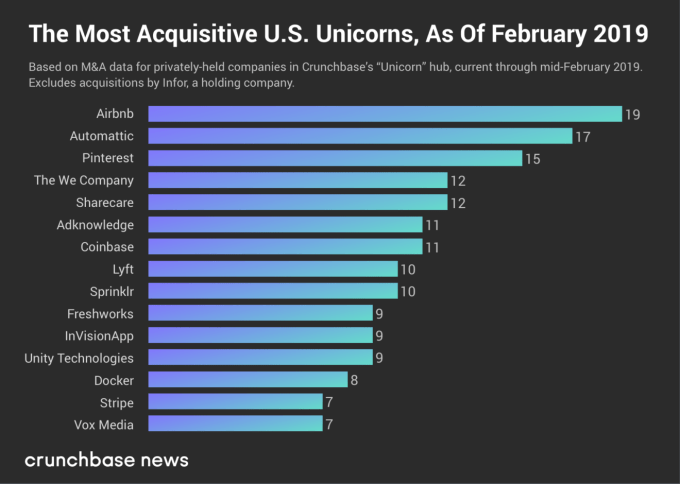

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

Greetings from Chittorgarh, one of my stops on a two-week excursion through Goa and Rajasthan, India. I’ve been a little too busy exploring, photographing cows and monkeys and eating a lot of delicious food to keep up with *all* the tech news, but I’ve still got the highlights.

For starters, if you haven’t heard yet, TechCrunch launched Extra Crunch, a paid premium subscription offering full of amazing content. As part of Extra Crunch, we’ll be doing deep dives on select businesses, beginning with Patreon. Read Patreon’s founding story here and learn how two college roommates built the world’s leading creator platform. Plus, we’ve got insights on Patreon’s product, business strategy, competitors and more.

Sign up for Extra Crunch membership here.

On to other news…

Y Combinator’s latest batch of startups is huge

So huge the Silicon Valley accelerator had to move locations and set up two stages at its upcoming demo days (March 18-19) to accommodate the more than 200 startups ready to pitch investors (who will have to hop between stages at the event). There will also be a virtual demo day live-streamed for some investors to watch “because there are so few seats.” Here’s what I’m wondering… At what point is a YC cohort too big? If investors aren’t even able to view all the companies at Demo Day, what exactly is the point? Send me your thoughts.

Another week, another SoftBank deal. The Vision Fund’s latest bet is autonomous delivery. The Japanese telecom giant has invested $940 million in Nuro, the developer of a custom unmanned vehicle designed for last-mile delivery of local goods and services. The startup, also backed by Greylock and Gaorong Capital, will use the cash to expand its delivery service, add new partners, hire employees and scale up its fleet of self-driving bots. And while we’re on the subject of autonomous, TuSimple, a self-driving truck startup, has raised a $95 million Series D at a unicorn valuation.

Mamoon Hamid and Ilya Fushman

TechCrunch’s Connie Loizos spoke with Mamoon Hamid and Ilya Fushman, who joined Kleiner Perkins from Social Capital and Index Ventures, respectively. The pair talked about Kleiner Perkins, touching on people who’ve left the firm, how its decision-making process now works, why there are no senior women in its ranks and what they make of SoftBank’s Vision Fund.

Here’s your weekly reminder to send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

Facebook CEO Mark Zuckerberg considered a multi-billion-dollar purchase of Unity, a game development platform. This is according to a new book coming out next week, “The History of the Future,” by Blake Harris, which digs deep into the founding story of Oculus and the drama surrounding the Facebook acquisition, subsequent lawsuits and personal politics of founder Palmer Luckey. Here’s more on the acquisition-that-could-have-been from TechCrunch’s Lucas Matney.

Indonesia-focused Intudo Ventures raised a new $50 million fund this week to invest in the world’s fourth most populated country; InReach Ventures, the “AI-powered” European VC, closed a new €53 million early-stage vehicle; and btov Partners closed an €80 million fund aimed at industrial tech startups.

Xiaomi-backed electric toothbrush startup Soocas raises $30M

Jobvite raises $200M+ and acquires three recruitment startups to expand its platform play

Opendoor files to raise another $200M

DriveNets emerges from stealth with $110M for its cloud-based alternative to network routers

Figma gets $40M Series C to put design tools in the cloud

Xiaomi-backed electric toothbrush Soocas raises $30 million Series C

Malt raises $28.6 million for its freelancer platform

Elevate Security announces $8M Series A to alter employee security behavior

Massless raises $2M to build an Apple Pencil for virtual reality

Just when you thought the scooter boom and the subscription-boom wouldn’t intersect, Grover arrived to prove you wrong. The startup is launching an e-scooter monthly subscription service in Germany. Their big idea is that instead of purchasing an e-scooter outright, GroverGo customers can enjoy unlimited e-scooter rides without the upfront costs or commitment of owning an e-scooter.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and General Catalyst’s Niko Bonatsos chat startups.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico