CrunchBase

Auto Added by WPeMatico

Auto Added by WPeMatico

Golden is announcing that it has raised $14.5 million in Series A funding. The round was led by previous investor Andreessen Horowitz, with the firm’s co-founder Marc Andreessen joining the startup’s board of directors.

When Golden launched last year, founder and CEO Jude Gomila told me that his goal was to create a knowledge base focused on areas where Wikipedia’s coverage is often spotty, particularly emerging technology and startups.

Gomila told me this week that “companies, technologies and the people involved in them” remain Golden’s strength. In that sense, you could see it as a competitor to Crunchbase, but with a much bigger emphasis on explaining and “clustering” information on big topics like quantum computing and COVID-19, rather than just aggregating key data about companies and people. (By the way, both TechCrunch and the author of this post have their own profile pages, though the latter is woefully empty.)

In contrast to Wikipedia, which relies on community editors, Gomila said most of the data in Golden is gathered using artificial intelligence and natural language processing: “We’re using AI to extract information from the news, from websites, from public databases.

This is supplemented by Golden staff (former TechCrunch copy editor Holden Page leads the startup’s research team), while the larger community can also pitch in by flagging things that are incorrect or need to be updated. (As one example of this “human in the loop” editing process, Gomila showed me a tool where someone could paste in an article link and Golden would automatically summarize it.)

“The ultimate aim is to try and automate as much of this as possible,” Gomila said. “[For now,] this hybrid is the most effective method.”

Golden has also started working with paying customers including private equity firms, hedge funds, VCs, biotechnology companies, corporate innovation offices and government agencies — in fact, it says it signed a $1 million contract with the U.S. Air Force this year. These customers are paying for access to Golden’s research engine, which includes the company’s Query Tool and the ability to request that the startup prepare research on a particular topic.

Golden has now raised a total of $19.5 million. Other investors in the new funding include DCVC, Harpoon Ventures and Gigafund .

“Golden’s knowledge base and research engine aggregates information about emerging technologies and the companies, investors, and the builders behind them,” Andreessen said in a statement. “Human and machine intelligence, working together on Golden’s platform, results in knowledge which gives people the edge in making decisions and navigating uncertainty.”

Powered by WPeMatico

Astute, a customer engagement platform headquartered in Columbus, Ohio, is announcing that it has acquired social media marketing company Socialbakers.

The financial terms of the acquisition were not disclosed. Socialbakers CEO Yuval Ben-Itzhak will become president of Socialbakers for the combined company, and he told me via email that the entire Socialbakers team will be joining as well, resulting in a combined organization with more than 600 employees and $100 million in annual recurring revenue.

Socialbakers was one of the last independent players from the first wave of social analytics. Founded in 2008 and based in Prague, the company raised a total of $34 million in funding, according to Crunchbase, from investors including Earlybird Venture Capital and Index Ventures. And it’s used by more than 2,500 brands globally.

Astute, meanwhile, has been around for 25 years, and focuses on unifying customer data. Ben-Itzhak said that by acquiring Socialbakers, Astute will be able to add social media-focused features like audience insights, content planning, influencer marketing and ad analytics.

“Socialbakers and Astute are already sharing dozens of mutual brand customers in the enterprise segment,” he said. “This is, in fact, how the acquisition talks came about. The platform integration process has already started and is expected to continue through Q4.”

In a statement, Astute CEO Mark Zablan also emphasized the comprehensiveness of the resulting platform.

“The lines between customer care, customer experience, and marketing have become increasingly blurred, presenting real challenges for companies,” Zablan said. “Combining the market-leading social media marketing capabilities of Socialbakers with Astute’s engagement suite not only helps our customers tackle this challenge more effectively, but also marks a major milestone along Astute’s journey towards becoming the end-to-end customer engagement platform that the Chief Customer Officer needs to succeed.”

Powered by WPeMatico

Before the coronavirus made edtech more relevant, companies in the sector were historically likely to see slow, low exits. Despite successful IPOs by 2U, Chegg and Instructure in the United States, public markets are not crowded with edtech companies.

Some of the largest exits in the space include LinkedIn’s scoop of Lynda for a $1.5 billion in cash and stock and TPG’s purchase of Ellucian for $3.5 billion.

But both of those deals happened in 2015. Five years later, edtech is cooler and surging — but is it seeing exits? Are Lynda and Ellucian one-off success stories?

2U’s co-founder and CEO, Chip Paucek, said he is optimistic.

“We are a rare edtech IPO,” he told TechCrunch last week. “For a long time in edtech it was either ‘sell to Pearson or not.’”

Despite the sector’s slow past, Paucek said now is a good time to start an edtech company because the sector “is finally starting to hit its stride” with more back-end infrastructure and demand for online education.

This morning, let’s use some data to paint a picture of the landscape of edtech exits and bring some balance to this stodgy stereotype.

Boot the growth

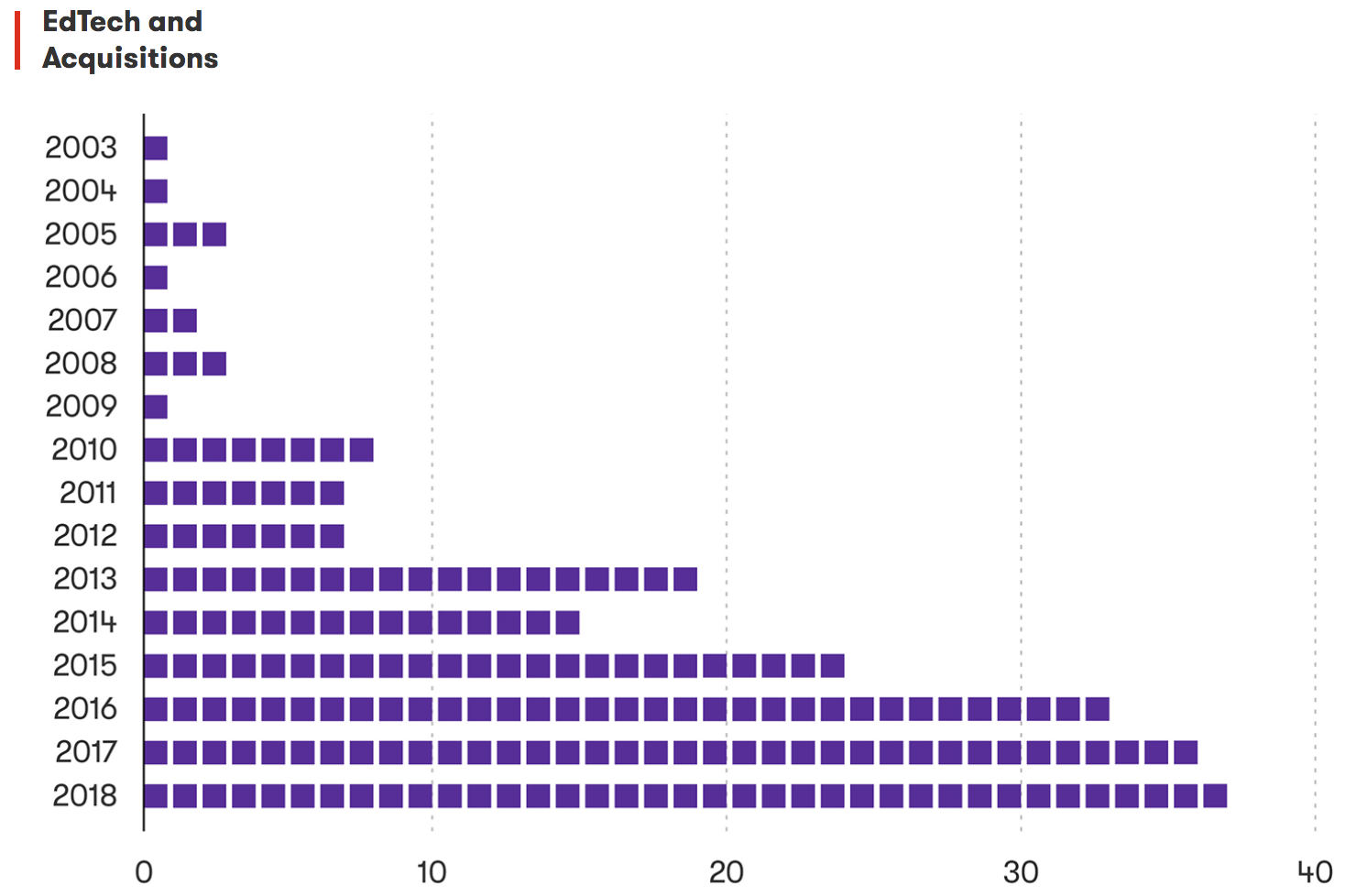

Boot the growthThere have been approximately 225 acquisitions in edtech between 2003 and 2018, according to Crunchbase data. RS Components sent me a graph in March to contextualize this timeframe a bit more:

Edtech deals over time. Graph credit: RS Components.

Powered by WPeMatico

The Q2 2020 venture capital market did not bring a catastrophic slowdown to either the global private investment scene or the U.S.’s own VC scene. But inside the rosier-than-anticipated private capital results of the second quarter, there were pockets of weakness, and strength, that we should understand as we look to the rest of 2020 and the continuance of the pandemic-driven economy.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, and you can now receive it in your inbox. Sign up for The Exchange newsletter, which will drop Saturdays starting July 25.

This morning we’re exploring trends detailed in the PitchBook-NVCA Q2 venture report, adding to our coverage of similar data sets produced by competing venture and private business information sources CB Insights and Crunchbase.

The NVCA data provides a useful cross section of venture activity beyond the usual quarterly totals, allowing us to better understand the diverging fortunes of domestic venture investment into business-serving startups (which appear strong), and investments into consumer-serving startups (which appear weak).

The NVCA data provides a useful cross section of venture activity beyond the usual quarterly totals, allowing us to better understand the diverging fortunes of domestic venture investment into business-serving startups (which appear strong), and investments into consumer-serving startups (which appear weak).

It also provides a peek into AI/ML-focused investing, a topic that TechCrunch has covered extensively this year. And, finally, we have a lens into recent U.S. VC results for startups that have at least one female founder, or were founded by all-women teams.

Some of the news is positive, and some of it is less so. But we owe it to ourselves to understand all of it. So to wrap up our week’s dive into Q2 VC activity, let’s get into our final look at the data, focusing today on the nuances of the United States’s own venture results.

As 2019 came to a close, TechCrunch wrote about a notable trend: Seed investors shifted their attention from consumer-focused startups to business-focused startups. Seed deals had moved from majority-B2C to majority-B2B, in other words.

Powered by WPeMatico

The second quarter’s venture capital results are coming into focus.

The Exchange will have more notes on Q2’s venture results this week, but this morning we’re digging into our first dataset concerning what happened in the world of private capital from April through June.

Crunchbase News — a place I used to work, it feels fair to note — ran its usual dig through the quarter’s venture results, effectively coming up with two answers to the question of what happened in Q2 VC. As it turns out, a single company’s fundraising made the quarter’s results look far better than they really were. Once we strip out that firm’s nonventure funding rounds, a clearer picture emerges.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, and now you can receive it in your inbox. Sign up for The Exchange newsletter, which will drop every Saturday starting July 25.

If you discount Reliance Jio’s epic — and continuing — ability to attract billions of dollars, the private investment market was slack in the second quarter. Per Crunchbase News, including the Reliance Jio deals, “Crunchbase recorded $69.5 billion invested across all funding stages for the second quarter specifically. This is up 17% quarter-over-quarter and down 2% year-over-year.” (Crunchbase has moved away from making projections, notably, and now discloses reported data in its quarterly results).

A gain of about one-sixth from Q1 2020 results was probably not what you expected, given the quarter’s nearly comical turbulence. But, with Reliance Jio’s fundraising bacchanal stripped out, results are much worse.

A gain of about one-sixth from Q1 2020 results was probably not what you expected, given the quarter’s nearly comical turbulence. But, with Reliance Jio’s fundraising bacchanal stripped out, results are much worse.

Let’s talk about whether it’s fair to lean more on Reliance Jio-free data, and dig into what the data means for startups around the globe. We’ll also look at a few other megarounds from the period to see if there are any other distortive funding events lurking in the data.

Final global Q2 data exclusive of Reliance Jio’s Q2 deals, per Crunchbase data, shows investment declines in the period of -9% compared to Q1 2020, and -23% compared to the year-ago quarter. While some of that will be due to reporting lag — the thing that projections were initially built to countermand — the dips are still stark.

Global Q2 VC does not look strong from this perspective.

Powered by WPeMatico

Couchbase, the Santa Clara-based company behind the eponymous NoSQL cloud database service, today announced that it has raised a $105 million all-equity Series G round “to expand product development and global go-to-market capabilities.”

The oversubscribed round was led by GPI Capital, with participation from existing investors Accel, Sorenson Capital, North Bridge Venture Partners, Glynn Capital, Adams Street Partners and Mayfield. With this, the company has now raised a total of $251 million, according to Crunchbase.

Back in 2016, Couchbase raised a $30 million down round, which at the time was meant to be the company’s last round before an IPO. That IPO hasn’t materialized, but the company continues to grow, with 30% of the Fortune 100 now using its database. Couchbase also today announced that, over the course of the last fiscal year, it saw 70% total contract value growth, more than 50% new business growth and over 35% growth in average subscription deal size. In total, Couchbase said today, it is now seeing almost $100 million in committed annual recurring revenue.

“To be competitive today, enterprises must transform digitally, and use technology to get closer to their customers and improve the productivity of their workforces,” Couchbase President and CEO Matt Cain said in today’s announcement. “To do so, they require a cloud-native database built specifically to support modern web, mobile and IoT applications. Application developers and enterprise architects rely on Couchbase to enable agile application development on a platform that performs at scale, from the public cloud to the edge, and provides operational simplicity and reliability. More and more, the largest companies in the world truly run their businesses on Couchbase, architecting their most business-critical applications on our platform.”

The company is playing in a large but competitive market, with the likes of MongoDB, DataStax and all the major cloud vendors vying for similar customers in the NoSQL space. One feature that has always made Couchbase stand out is Couchbase Mobile, which extends the service to the cloud. Like some of its competitors, the company has also recently placed its bets on the Kubernetes container orchestration tools with, for example the launch of its Autonomous Operator for Kubernetes 2.0. More importantly, though, the company also introduced its fully managed Couchbase Cloud Database-as-a-Service in February, which allows businesses to run the database within their own virtual private cloud on public clouds like AWS and Microsoft Azure.

“We are excited to partner with Couchbase and view Couchbase Server’s highly performant, distributed architecture as purpose-built to support mission-critical use cases at scale,” said Alex Migon, a partner at GPI Capital and a new member of the company’s board of directors. “Couchbase has developed a truly enterprise-grade product, with leading support for cutting-edge application development and deployment needs. We are thrilled to contribute to the next stage of the company’s growth.”

The company tells me that it plans to use the new funding to continue its “accelerated trajectory with investment in each of their three core pillars: sustained differentiation, profitable growth, and world class teams.” Of course, Couchbase will also continue to build new features for its NoSQL server, mobile platform and Couchbase Cloud — in addition, the company will continue to expand geographically to serve its global customer operations.

Powered by WPeMatico

Starting today, TechCrunch readers can send an Extra Crunch annual membership as a gift to a friend, family member or co-worker. For a limited time we’re offering the gift at a discounted rate of $99/year (plus tax).

The gifting feature can be found here.

Extra Crunch membership is designed for startup teams, entrepreneurs, investors and business school students, and it includes more than 100 exclusive articles per month:

Extra Crunch membership can save you time time with an exclusive newsletter, no banner ads, Rapid Read mode and our List Builder tool. Annual and two-year members can also save money with discounts on events and access to Partner Perks. Our Partner Perks provide discounted access to services from companies like AWS, Brex, DocSend, Crunchbase, Typeform and more.

Gifting is currently supported in the U.S., Canada, U.K. and select countries in Europe. Purchases can be made through Visa, Mastercard and PayPal in all supported countries, but Amex support is limited to the U.S. and Canada.

If there are other features you’d like to see us add to Extra Crunch, please let us know by leaving a comment on this post or emailing me directly at travis@techcrunch.com.

TechCrunch readers can find the Extra Crunch gifting feature here.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re taking a look at the world of esports venture capital investment, largely through the lens of preliminary data that we’ll caveat given how reported VC data lags reality. That phenomenon is likely doubly true in the current moment, as COVID-19 absorbs all news cycles and some venture rounds’ announcements are delayed even more than usual.

All the same, the data we do have paints a picture of a change in esports venture investment, one sufficient in size to indicate that an esports VC slowdown could be afoot. As with all early looks, we’re extending ourselves to reach a conclusion. But… no risk, no reward.

We’ll start by looking at Q1 2020 esports venture totals to date, compare them to year-ago results, and then peek at Q4 2019’s results and its year-ago comparison to get a handle on what else has happened lately in the niche. The picture that the quarters draw will help us understand how esports investing is starting a year that isn’t going as anyone expected.

Today we’re using Crunchbase data, looking at both global and U.S.-specific venture totals in both round and dollar volume. To get a picture of the competitive gaming world, we’re examining investments into companies that are tagged as “esports” related in the Crunchbase database. Given that this is a somewhat wide cut, the data below is more directional than precise and should be treated as such.

Powered by WPeMatico

In a world where ad rates are declining for traditional broadcast media, the corporations responsible for making the fictions that millions devour daily need to find a new business model.

Subscription services are on the rise — with every major broadcaster launching an on-demand service — and so are ad-supported video streaming services to replace the traditional networks.

But there’s another Holy Grail of the advertising industry, long thought to be too technologically difficult to achieve, that may finally be within reach. It’s the on-demand product placement of branded goods in a video, and it’s the technology that Ryff has been developing since it was founded in early 2018.

Product placement is an increasingly big business in the U.S., raking in some $11.44 billion in 2019, according to data collected by Statista. That figure is up from $4.75 billion in 2012. The same report indicated that roughly 49% of Americans took action after seeing product placement in media.

The effectiveness of product placement has even been proven by researchers from Indiana University and Emory University. They found that “prominent product placement embedded in television programming does have a net positive impact on online conversations and web traffic for the brand.”

And while streaming services enjoy the dollars their subscribers are throwing at them, they’re also looking at ways to diversify their revenue streams. Netflix and Hulu are both expanding their product marketing divisions and analysts like those from Forrester Research predict that product placement will be a huge moneymaker for the company as traditional ad rates decline.

There are companies that handle product placement already. Startups like Branded Entertainment Network, which works with brands and producers to place real brands into contextually relevant scenes in movies and television, and Mirriad, which adds branded billboards to scenes, are working to bring more money to platforms and producers.

Ryff takes the technology to the next level, using computer vision, machine learning and rendering technologies to identify objects in a scene and replace them with branded products that can be tailored based on customer data.

“The infusion of SVOD/streaming platforms into the market, combined with platforms like Netflix that are unsuccessfully trying to grow their subscriber base will force those same platforms to explore and embrace alternative revenue streams,” said Marlon Nichols, managing general partner at MaC Venture Capital, and a new director on the Ryff board. “In addition, consumers on paid platforms do not want their content consumption interrupted by ads. As such, product placement will be an important growth channel and Ryff’s new marketplace and unique technology set it up to be the unequivocal growth market leader.”

To continue its technology development and ramp up sales and marketing, the company has raised $5 million in financing. According to Crunchbase, Ryff had previously raised $3.6 million from investors, including a subsidiary of the Mahindra Group and undisclosed investors. The new financing came from Valor Siren Ventures, MaC Venture Capital, Moneta Ventures and Vulcan Capital.

“Ryff’s offering is well-timed with the rapidly increasing demand for solutions that extend the reach of a brand’s content and drive business results,” said Uday Ghare, vice president for media and entertainment at Tech Mahindra, in a statement at the time of the company’s investment. “We believe the market will continue to see a shift of brand dollars to both content marketing and programmatic advertising as brands increase their reliance on content-centric programs and look to scale those efforts.”

Ryff’s ads can be tailored to the viewer’s taste, the platform on which video is being distributed, the geography of the broadcast, the date and time of the broadcast and a broader demographic profile, according to the company. Basically it’s like AdWords for videos.

In a blog post writing about the rationale behind his investment firm’s capital commitment to the company, Marlon Nichols of MaC Ventures wrote:

Imagine a future where an IP owner can maximize the value of its content by putting it on the Ryff marketplace, where that content will be mapped for dozens if not hundreds of product placement opportunities and be layered with restrictions that comply with creative needs. Those opportunities will be ranked and priced by their effectiveness to drive marketing goals for brands. Brands can bid on in-video placement opportunities that fit their marketing strategies and budgets. 3D brand assets can be uploaded and inserted dynamically into content right before the moment of video delivery.

Ryff’s first disclosed partnership is with the “reality” television producer Endemol Shine.

“Ryff successfully takes the concept of product placement, the only advertising format that can’t be skipped by the viewer, and delivers a scalable and adaptable advertising solution that can be applied to any content, at any time and in any market,” said Roy Taylor, founder and CEO of Ryff, in a statement. “The result benefits all — content free from annoying distractions, audience-specific brand placement and delivering a new means towards monetizing video assets.”

Powered by WPeMatico

The internet and search engines like Google have made the world our oyster when it comes to sourcing information, but in the world of business, there remains a persistent need for more targeted market intelligence, a way to get reliable data quickly to get on with your work. Today, one of the startups hoping to build a lucrative operation of its own around that premise is announcing a round of funding to get there.

Crunchbase — a directory and database of company-related information that originally got its start as a part of TechCrunch before being spun off into a separate business several years ago — has raised $30 million, a Series C that it plans to use to continue expanding its base of paid subscribers and expanding its product to include more predictive, personalised information for its users by way of more machine learning and other AI-based technology.

CEO Jager McConnell, who has long viewed Crunchbase as the “LinkedIn for company profiles,” said that of the 55 million people who visit the site each year, the company currently has “tens of thousands” of subscribers — subscriptions are priced at $29/user/month varying by size of company contract — which works out to less than 1% of its active users. That’s “growing quickly,” he added, speaking to site’s potential.

Indeed, he noted that since its last round in 2017, when it raised $18 million, Crunchbase has tripled its employees to 120 and has 10 times more annual revenue run rate. It’s also more than doubled its traffic since being spun out.

This latest round was led by Omers Ventures, the prolific investment arm of the giant Canadian pension fund of the same name (which is, incidentally, also now opening an office in Silicon Valley to get even more active with startups there).

Existing backers Emergence, Mayfield, Cowboy Ventures and Verizon (which still owns TC) also participated. McConnell said Crunchbase is not disclosing its valuation with this round, but he did note that it was “well within the target range” that the startup had set, that it was an oversubscribed upround and that it was on the more practical than exuberant side.

“I believe we are seeing too many high valuations with low annual revenue rates, and it’s catching up with people, and we were very focused on not hitting that valuation trap in order to be successful in the future,” he said. “This is a good round but not something insane.” Strong logic I suspect could be supported by Crunchbase data. For some context, Crunchbase had a post-money valuation of $70 million in its previous round in 2017 (having raised $26 million), according to PitchBook — ironically, one of Crunchbase’s big competitors (CB Insights, Owler being others.)

With its start as a side project of TechCrunch, the DNA of Crunchbase has always been in tech companies, and that is still very much the heart of the data that is in the system today. The kind of data you can get via the site includes basics on when a company was founded, who the founders are, who the current executive leadership is, how much money it has raised and from whom and what has been written about it in the media. You also can find original content on the site by way of its own team of writers covering funding rounds and other Crunchbase-relevant content.

Then, via a number of third-party integrations with companies like Siftery and SimilarWeb, you can get deeper data around competitors and more (most of which you can only see if you are a paying, not free, user).

The company notes that it currently makes 3.9 billion annual updates to its data set — which people upload themselves in the old wiki style, or are manually or automatically uploaded, by way of some 4,000 data partnerships and syndication deals (these include the likes of Yahoo! Finance, LinkedIn, Business Insider and Amazon Alexa, which in turn make some 1.6 billion annual calls to the Crunchbase API).

The growth of that information trove, and more interesting ways of parsing it to drive subscriptions and potential licensing revenues, will be of paramount importance to the company’s bottom line. Today there is some advertising on the site, but McConnell confirmed to me that Crunchbase is in the process of winding down advertising on the platform.

“The impact on the business was not material enough to sacrifice the user experience to have ads,” he said.

On the subject of the self-styled LinkedIn comparison, you’ve probably already noticed that LinkedIn does have company profile pages, but McConnell’s argument is that the site was built with individuals’ profiles and recruitment in mind. That makes the company pages more of an add-on and not something that can be effectively developed at this point in the way that Crunchbase has done.

“Once you do that, it’s hard to change,” he said of the direction that LinkedIn has grown. “Its company profiles are more brand representations, not a source of truth about the companies themselves.”

What’s interesting to me is to see which direction Crunchbase will evolve in the longer term. As the world has continued to grow into the bigger vision of “every company is a tech company, and every problem has a tech solution,” it seems that Crunchbase’s own ambitions have also grown.

In the company’s blog post and press release announcing the fundraise, it’s notable to me that the word technology, or any variation of it, isn’t mentioned even once in the text (the only exception being the boilerplate description of Omers).

That could point to how — as Crunchbase expands its horizons in terms of the kinds of information on businesses it can provide to users — it might see a role for itself not unlike that of LinkedIn, spanning across multiple verticals and the communities of people (or in CB’s case, businesses) that have built around them.

“We are thrilled to partner with Jager and the talented leadership team at Crunchbase,” commented Michael Yang, managing partner at OMERS Ventures, in a statement. “Crunchbase continues to show significant traction as the leader in research, information, and prospecting for private companies – an incredibly large and valuable market to address and service. By utilizing and collecting aggregated data, adding tools and apps, and continuing to customize each user experience, the lead generation and deal value Crunchbase can provide is unprecedented, and we are proud to support this next phase of growth.”

Powered by WPeMatico