Column

Auto Added by WPeMatico

Auto Added by WPeMatico

At Battery, a central part of our consumer investing practice involves tracking the evolution of where and how consumers find and purchase goods and services. From our annual Battery Marketplace Index, we’ve seen seismic shifts in how consumer purchasing behavior has changed over the years, starting with the move to the web and, more recently, to mobile and on-demand via smartphones.

The evolution looks like this in a nutshell: In the early days, listing sites like Craigslist, Angie’s List* and Yelp effectively put the Yellow Pages online — you could find a new restaurant or plumber on the web, but the process of contacting them was largely still offline. As consumers grew more comfortable with the web, marketplaces like eBay, Etsy, Expedia and Wayfair* emerged, enabling historically offline transactions to occur online.

More recently, and spurred in large part by mobile, on-demand use cases, managed marketplaces like Uber, DoorDash, Instacart and StockX* have taken online consumer purchasing a step further. They play a greater role in the operations of the marketplace, from automatically matching demand with supply, to verifying the supply side for quality, to dynamic pricing.

The key purpose of being end-to-end is to deliver an even better value proposition to consumers relative to incumbent alternatives.

Each stage of this evolution unlocked billions of dollars in value, and many of the names listed above remain the largest consumer internet companies today.

At their core, these companies are facilitators, matching consumer demand with existing supply of a product or service. While there is no doubt these companies play a hugely valuable role in our lives, we increasingly believe that simply facilitating a transaction or service isn’t enough. Particularly in industries where supply is scarce, or in old-guard industries where innovation in the underlying product or service is slow, a digitized marketplace — even when managed — can produce underwhelming experiences for consumers.

In these instances, starting from the ground up is what is really required to deliver an optimal consumer experience. Back in 2014, Chris Dixon wrote a bit about this phenomenon in his post on “Full stack startups.” Fast forward several years, and more startups than ever are “full stack” or as we call it, “end-to-end operators.”

These businesses are fundamentally reimagining their product experience by owning the entire value chain, from end to end, thereby creating a step-functionally better experience for consumers. Owning more in the stack of operations gives these companies better control over quality, customer service, delivery, pricing and more — which gives consumers a better, faster and cheaper experience.

It’s worth noting that these end-to-end models typically require more capital to reach scale, as greater upfront investment is necessary to get them off the ground than other, more narrowly focused marketplaces. But in our experience, the additional capital required is often outweighed by the value captured from owning the entire experience.

Many of these businesses have reached meaningful scale across industries:

Image Credits: Battery Ventures (opens in a new window)

All of these companies have recognized they can deliver more value to consumers by “owning” every aspect of the underlying product or service — from the bike to the workout content in Peloton’s case, or the bank account to the credit card in Chime’s case. They have reinvented and reimagined the entire consumer experience, from end to end.

As investors, we’ve had the privilege of meeting with many of these next-generation end-to-end operators over the years and found that those with the greatest success tend to exhibit the five key elements below:

The end-to-end approach makes the most sense when disrupting very large markets. In the graphic above, notice that most of these companies play in the largest, but notoriously archaic industries like banking, insurance, real estate, healthcare, etc. Incumbents in these industries are very large and entrenched, but they are legacy players, making them slow to adopt new technology. For the most part, they have failed to meet the needs of our digital-native, mobile-savvy generation and their experiences lag behind consumer expectations of today (evidenced by low, or sometimes even negative, NPS scores). Rebuilding the experience from the ground up is sometimes the only way to satisfy today’s consumers in these massive markets.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie:

I work in HR for a tech firm. I understand that Biden is rolling out a new immigration plan today.

What is your sense as to how the new administration will change business, corporate and startup founder immigration to the U.S.?

—Free in Fremont

Dear Free:

Today is a historic day. The pace of change is accelerating now, especially in Washington. At the time of this writing, Biden is expected to imminently launch a new legislative proposal for comprehensive immigration reform. As the world sits back and watches, we are focusing great collective attention on upgrading our political, sociological and technological structures so that each human has the chance to succeed.

One of the things I adore about my practice of supporting international professionals with U.S. immigration is bearing witness to the process of individual transformation; it is an honor to support people in their personal journey from living in a world of effects to becoming the cause.

The immediate focus of the proposed legislation is centered around a solution for Dreamers (who are in the U.S. without documentation) as well as supporting the rights of refugees and asylum-seekers and children. For more of my recent thoughts on this topic, check out my recent podcast explaining many of the changes. The draft bill is expected to span hundreds of pages, so please follow this Dear Sophie column for more updates as I track and explore the details, especially related to tech immigration.

Innovation will be supported by many new immigration opportunities coming into greater focus. Biden’s campaign platform celebrated how “Immigrants are essential to the strength of our country and the U.S. economy.” The Biden team has prioritized immigration as a key focus within COVID, with an immediate goal of rewriting most Trump-era rules. For context, Trump issued more than 400 immigration-related executive orders and proclamations during his term.

H-1Bs: Although H-1Bs have been in the news a lot regarding new wage rules changing the order of the lottery and litigation, the lottery is still happening this spring, and if you want to sponsor candidates, the time to act is now, regardless of what is happening in Washington. If your company is planning on sponsoring individuals for an H-1B visa — whether they’re already living in the U.S. or are living abroad — I suggest that you continue to prepare for the upcoming H-1B registration period.

Powered by WPeMatico

Last week, Procter & Gamble (P&G) announced that it was terminating plans to acquire razor startup Billie following a U.S. Federal Trade Commission lawsuit to stop the deal.

Last year, Edgewell Personal Care ditched its debt-heavy $1.37 billion deal for Harry’s, Inc, formerly valued at $1 billion after the FTC sought to block the acquisition.

In addition to these FTC challenges, it is also now becoming clear that relying on VC-subsidized products and celebrating outrageous valuations can be problematic for D2C brands. With a few wonderful and rare exceptions such as Rothy’s (which raised $42 million but was profitable from the beginning and generated $140 million in revenue within two years of launching), D2C unicorns are addicted to the cycle of venture funding to feed growth in order to maintain a high valuation multiple.

The path to profitability has become a more important part of the startup story versus growth at all costs.

This works for a while; however, when the path to profitability appears murky and exit options either don’t appear or only appear from nontech companies with very conservative multiples, the walls start crumbling.

In a WWD article, Odile Roujol, the former CEO of Lancôme who launched venture fund FAB Ventures, said, “Generally speaking, the era of $1 billion valuations for beauty companies is over. The people that struggle have been the companies that spend so much money in just a few years.” She went on to say, “The big corporations now … are not ready to spend $1.2 billion, $1.5 billion on such a brand like Glossier.”

This change in sentiment from acquirers is further fueled by recent research on the challenges of turning hypergrowth companies profitable. In his Harvard Business School case study “Direct to Consumer Brands,” Professor Sunil Gupta wrote, “Acquiring DTC brands is easy for incumbent conglomerates, but making them profitable is challenging. More than three years after Unilever acquired Dollar Shave Club, it was still unprofitable.”

Unilever executives learned that the average cost of acquiring a new customer online was about the same as in stores. David Taylor, CEO of P&G, said his company was still figuring out how to turn recently acquired direct-to-consumer brands into profitable businesses.

Taylor summarized this dilemma, saying, “There are many, many launches that grow fast … a business model that makes money is a higher challenge.” Since making these realizations, incumbent conglomerates will be more cautious when considering the acquisition of hyped D2C brands that raised lots of venture capital.

What’s cooler than beauty companies that are (or were) valued at $1 billion? Beauty tech SaaS companies that are worth $5.2 billion at IPO. We don’t hear much about the leading global beauty tech companies such as Meitu and Perfect Corp. because their founders are not celebrity influencers, they don’t have massive Instagram followings here in the U.S. and they are not celebrated in our media. Although their companies are based in Asia and they raised money mostly from Chinese investors, their companies are global successes.

Powered by WPeMatico

Previously, we introduced the concept of flexible VC: structures that allow founders to access immediate risk capital while preserving exit and ownership optionality. We list here all the active flexible VCs we have identified, broken into these categories:

These investors are paid back primarily based on a percentage of revenues.

Chattanooga, TN-based Capacity Capital was launched in 2020 with a primary focus on the southeastern U.S. Jonathan Bragdon, its CEO, describes Capacity as “a team of founders-turned-funders making non-dilutive, founder-aligned investments of $50,000-$300,000 in post-startup, post-revenue businesses planning to 2x revenues in 12-24 months. Investments are typically in exchange for a capped, single-digit revenue share and a right to equity under certain circumstances.

If the company sells or raises enough capital, the investment converts into an agreed-upon percentage of equity. If the company grows without raising additional equity funding, founders redeem most of the equity right, based on a pre-agreed return amount. With a portfolio that includes food, tech and services, the fund is industry-agnostic and focused on the overlooked and underrepresented with high-margin business models.”

Jonathan sometimes refers to their investments as “micro-mezzanine” because “mezz is typically structured as a contractual periodic payment, with some equity-like upside, but subordinate to other debt … so most lenders look at it like equity. But, it is typically shorter term with fewer control mechanisms than equity (i.e., not VC). I wanted [a term for] something similar (between debt and equity) but on an extremely small scale.”

In addition to a fund, the overall Capacity organization provides direct mentorship, consulting and connects founders to a broad network of talent, diverse forms of capital and existing resources focused on the post-startup stage of growth. The founders, LPs and venture partners have a long history in local startup ecosystems in the Southeast including LaunchTN, The Company Lab, CO.STARTERS and several other regional funds and resources.

Greater Colorado Venture Fund (GCVF) is a $17 million seed fund that invests in high-growth startups in rural Colorado using equity and flexible VC structuring.

A typical GCVF flexible VC investment is $100,000-$250,000 for up to 10% ownership, of which 9% is redeemable, with a sub-10% revenue share and 12-month-plus holiday period. GCVF specializes in providing critical support to founders based in small communities, while connecting them to an unfair network well-beyond their small-town headquarters.

GCVF is pioneering the future of venture capital and high-growth startups for all small communities. With Colorado as an ideal pilot community, the GCVF team (which includes Jamie Finney, a co-author of this article) has helped grow multiple staple initiatives in the rural Colorado startup ecosystem, including West Slope Startup Week, Telluride Venture Accelerator, Startup Colorado, Energize Colorado Gap Fund and the Greater Colorado Pitch Series.

Recognizing the need for creative investment structures in their Colorado market, they co-founded the Alternative Capital Summit, creating the first community of flexible VCs and alternative startup investors.

They share their learnings on flexible VC and pioneering rural startup ecosystems on the GCVF blog.

Powered by WPeMatico

Of the Inc. 5000 companies, only 6.5% raised money from VCs and 7.7% raised from angels. Where else can fast-growing companies get funding?

More and more startups are pursuing revenue-based VCs, but it’s not a good fit for everyone. A new category of investors has emerged offering a hybrid between VC and revenue-based investment (RBI), which we call “flexible VC.”

From RBI, flexible VCs borrow the ability to reap meaningful returns without demanding founders build for an exit. From traditional equity VC, flexible VC borrows the option to pursue and reap the rewards of an outsized exit. Every flexible VC structure allows founders to access immediate risk capital while preserving exit, growth trajectory and ownership optionality.

Before raising capital, we encourage founders to dig into the nuances between different flexible VC structures.

Our categorization is not a technical one. Rather, we want to accommodate the wide variety of instruments currently offered by flexible VC investors, detailed below. As two fund managers employing flexible VC, we think it is a healthy addition to the ecosystem and will yield more predictable and stable healthy returns for investors.

This is currently the most common investment structure: The flexible VC investor purchases either equity ownership, or a convertible right to equity, and a right to regularly scheduled payments based on a percentage of revenues.

By tying payments to actual revenues, founders and investors remain aligned around the company’s real-time performance, good or bad.

“Too often, investment structures force the management team to make decisions between misaligned growth and investment (return) objectives. This structure allows for alignment on the front end, and real-time flexibility for performance metrics,” says Samira Salman, a family office investor and advisor.

Payments are commonly delayed for a grace period of 12-36 months. John Berger, director of Operations and Impact Solutions at Toniic, observed that this has clear investor benefits: “The grace period became a feature because it benefits investors in regions like the U.S. where there can be tax differences between short- and long-term gains. It has moved from its origins as a tax benefit and can be viewed as a feature that benefits founders.” After the grace period, the return payments begin, often lasting until a return cap is hit, such as 2-5 times the original investment.

To account for these revenue share payments, the investor’s ownership (or convertible right to ownership) is simultaneously reduced. Once the return cap is reached, the investor is typically left with a residual stake — a fraction of the pre-revenue share ownership. At any point, should the founder wish to pursue a traditional equity VC round, or get bought, the revenue share is paused, and the investor’s then-current ownership converts to equate to a traditional equity VC investor.

Flexible VCs have created structures based on other company performance metrics than revenues, such as profits or founder salaries. These different company performance metrics provide a slight variation in how the investor and founder relationship is defined. For example, profit-sharing structures ensure payments do not begin until the company is profitable, though likely delaying returns to the investor and complicating payment calculations.

Similarly, when flexible VC structures are based off of the founder’s own compensation (often via salary or dividends), investors are specifically tying their returns to the financial success of the founder. This translates less directly to company performance compared to a revenue or profit share, but offers uniquely personal alignment. These variations in founder alignment allow flexible VCs to specialize in the types of companies they work with.

In all these cases, capital is provided to fuel forecasted growth without creating a commitment to a particular vision for future funding rounds, exit goals and associated blitzscaling. The founder retains full control over whether they want to optimize for hypergrowth (usually at the expense of profitability) or for organic, profitable growth. Flexible VC opens up a new risk capital option for bootstrappers, minorities, family-owned and countless other founder segments left out by the traditional funding landscape.

A range of small VCs are deploying with flexible VC structures, but we believe the total amount of AUM deployed with this strategy is well under $50 million. Similar to the explosion of seed funds in the past decade, we (and some limited partners too) believe these Flexible VCs are on the forefront of what will become a major segment of the venture ecosystem.

We detail below the major categories of VC:

| Funder category | Equity ownership | Returns primarily based on | Composition of returns | Example VC |

| Equity VC | Yes, typically preferred equity.

15%-20% sold per round. On average, founders own just 43% of equity by Series B, declining thereafter. |

The value ascribed by subsequent investors (in a secondary); buyers (acquisition); or the public markets (IPO). | Volatile, uncapped. | Andressen Horowitz, ff Venture Capital, HOF Capital, Sequoia. |

| Flexible VC: Revenue-based | Yes, nonvoting common shares (if converted).

5%-20% initial stake, with 50%-90% of this redeemable. |

Gross revenues (generally 2%-8%). | 2x-5x return cap + path to uncapped equity returns. | Capacity Capital, Greater Colorado Venture Fund, Indie.VC, Reformation Partners, UP Fund, Versatile VC. |

| Flexible VC: Compensation-based | Yes, via conversion rights at a valuation cap. | “Founder earnings” (Founder salaries + dividends + retained earnings). | 2x-5x return cap + path to uncapped equity returns. | Chisos. |

| Flexible VC: Blended Return | Yes, via conversion rights at a valuation cap. | Profits, founder salaries, and/or dividends declared. | Typically ~3x+ return cap + path to uncapped equity returns. Discretionary dividends and salary share built in. | Collab Capital, Earnest Capital, TinySeed. |

| Revenue-share investing | No. | Gross revenues (generally 2%-8%). | 1.35x-2.2x return cap. | Novel Growth Partners, Lighter Capital, Rev Up, Corl. |

Flexible VC investors offer founders some of the same advantages as equity VCs:

Flexible VCs also offer investors some of the same advantages as RBI:

Flexible VC also offers some unique advantages:

That said, nothing is cost-free. The unique disadvantages of flexible VC include:

Powered by WPeMatico

Revenue-based investing (RBI), also known as revenue-based financing, or revenue-share investing,1 is a natural next step for the private equity and early-stage venture investment industry. However, due to RBI being a relatively new model, publicly available data is limited.

To address this foundational gap in market information, we have developed a proprietary data set of 32 RBI investment firms, 57 distinct funds and 134 companies that have secured revenue-based investing.

Bootstrapp developed this extensive analysis on revenue-based investing for the purpose of accelerating the shift toward greater transparency and standardization within the industry.

Upon thoroughly analyzing the data, we’ve been able to identify the total number of investment firms and amount of capital that comprise the RBI industry, the specific verticals and business models that are most actively leveraging RBI, and the typical profile of companies that access this form of capital.

These findings are summarized below; a full industry-spanning report that defines the overall revenue-based investing market as it stands today is available to download here.

As context, the financial structures used by VCs haven’t evolved much since they first emerged in 1957. Today, the model is almost precisely the same, with only incremental changes such as more efficient capital markets and industry standards for structuring deals, pricing companies and more.

More recently, we have seen numerous new investment models and financing instruments, including shared earnings agreements and point-of-sale capital. One of the most prominent and popular new models for investors is revenue-based investing (RBI).

However, because the model is new, there is a lack of publicly available data, industry standards have not yet been fully established, and similarly to the equity investment market, there is little transparency into the cost of capital that investees truly pay in exchange for taking on a revenue-based investment.

Thankfully, there have been some notable efforts to drive transparency in the RBI market. For example, Bigfoot Capital open-sourced its RBI model, outlining it in a blog post and sharing their RBI financial model and anonymized term sheet, but a thorough, quantitative, industry-wide analysis has not been conducted until now.

In order to raise RBI, the company must normally be generating revenue, but is not necessarily required to be profitable, although profitability, or at least a near-term path to profitability, is often an important criteria for many investors. “For startups with revenue, RBI may be a good option because, even though the startup may not be profitable, it can reduce dilution — especially for founders,” said Emily Campbell of The Campbell Firm PLLC, a law firm that represents serial entrepreneurs and venture-backed businesses.

“Taking in some smart equity or convertible debt and balancing that money with other financing can be a good strategy for a startup,” she said. Profitability decreases the risk of default and assures that the investee has the ability to service the debt.

In regards to the applications that are best suited to RBI, B2B software-as-a-service (SaaS) companies rise to the top of the list primarily because one is able to — in essence — securitize the revenue being generated by a company and then lend capital against that theoretical security. In addition to SaaS companies, RBI is being used quite frequently in the impact investing community as it solves the problem of a lack of normal M&A or IPO exit paths for impact-driven companies and are sometimes marketed as a nonextractive form of investment structure.

Beyond B2B SaaS and impact investing, many other verticals are adopting the model as well, including e-commerce/D2C, consumer software, food and beverage, and more. It ought to be noted, however, that regardless of the specific business model a company employs, the investee is typically required to have repeatable sales and a track record that demonstrates a strong revenue stream, and therefore a clear ability to return the capital to the investors.

We have identified 32 U.S.-based firms actively investing via a revenue-based investing instrument, with those firms managing 57 distinct funds representing an estimated $4.31 billion in capital. Through our analysis of those firms, funds and investees, we found that:

Firms were included in the data set (and by extension, determined to be actively making revenue-based investments) if they:

The specific number of firms we believe to be quite accurate, representing only active, U.S.-based revenue-based investing firms. The number of funds, however, may be underestimated. This is due to the fact that, although each firm is associated with at least one fund, we did not include additional funds beyond that unless they were confirmed through other sources, such as the firms’ public communications, their SEC Form D or other sources as outlined in the methodology section at the conclusion of the full report.

The total amount of RBI capital that has already been allocated to companies across all firms and all years is $2.1 billion. However, it should be noted that this includes the outliers in our dataset, namely Kapitus, Clearbanc, Braavo and United Capital Source. Once we remove those firms, the remaining 28 firms, representing 51 funds, have allocated $592.8 million.

This figure of $592.8 million is almost certainly an underestimate due to the fact that only 19 of 32 firms had a known “amount of allocated capital,” whereas the remaining 13 firms have unknown values (i.e., zeros) for the amount of capital they have allocated thus far. Therefore, if all 32 firms had a valid and confirmed amount of allocated capital, we can logically conclude that the number would rise dramatically from the current figure of $592.8 million.

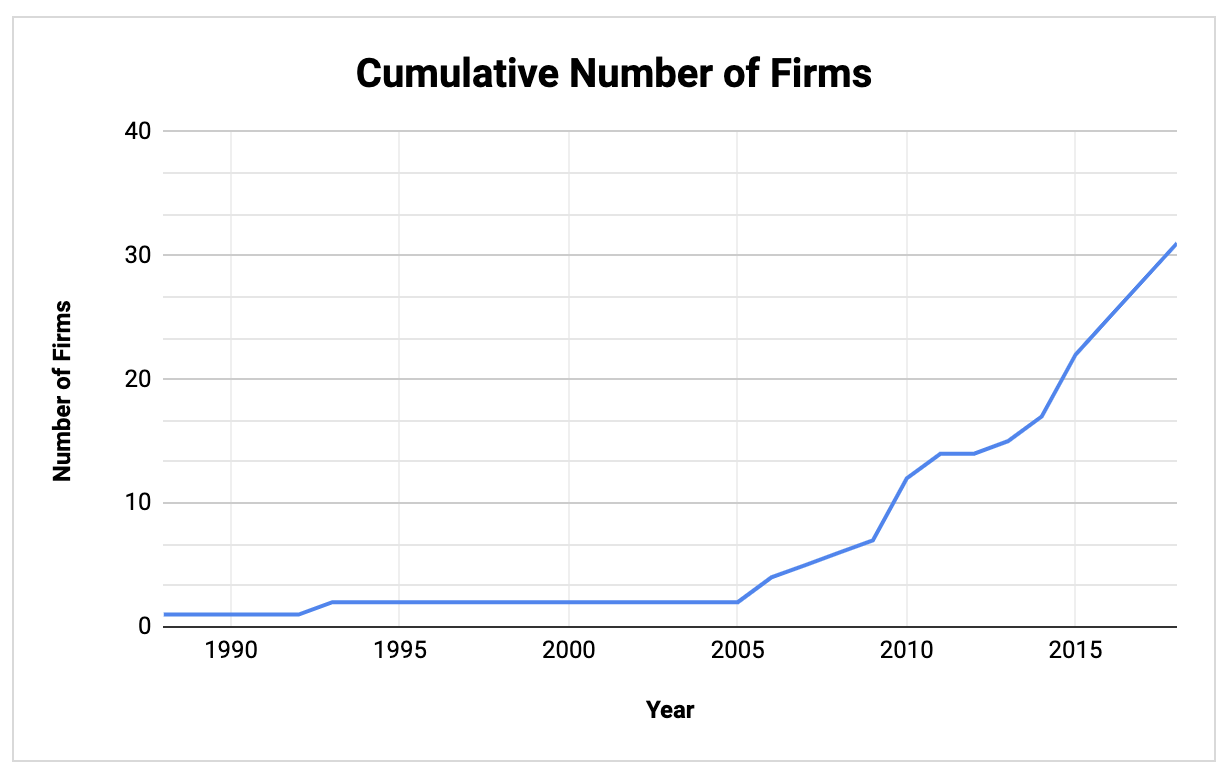

New RBI firms have been founded every year since 2013. In 2010, five firms were founded and in 2015 four additional firms were founded, then from 2014-2019, two or more firms were founded each year.

Image Credits: Bootstrapp (opens in a new window)

Clearly, there has been a major uptick in RBI firms being founded since 2005, with a relatively consistent number of new firms being founded over the 15 years since then. In the last 10 years alone, 25 RBI firms have been founded.

Powered by WPeMatico

In 2020, venture capitalists unceremoniously broke up with D2C brands and product-based businesses.

Many watched as the consumer brands in their portfolios rushed to make hefty layoffs and eke out more runway and grew more concerned with their business models.

Some simply monitored the “lackluster” Casper IPO or skimmed articles about Brandless and others “imploding” and started pulling a slow fade on D2C brands — not taking pitches, not following up.

Many product-based brands, as it turns out, are no longer interested in chasing venture capital.

Last year, investors adopted a wait-and-see approach to all new investments and prayed portfolio brands could cut their burn significantly enough, stay relevant and ride things out.

Product-based businesses fell out of favor and venture capitalists, if they did invest last year, mainly focused on AI startups, or companies focused on data collaboration, data privacy and healthcare (mostly founded by men, might I add).

From a distance, it sounds like direct-to-consumer founders were left destitute and desperate for financing, wounded by every slow fade or hard pass, beholden as ever to the whims of Silicon Valley.

But as Hal Koss so eloquently shared in his “DTC playbook” post-mortem, this wasn’t a one-way breakup; this parting of ways is actually mutual. Many product-based brands, as it turns out, are no longer interested in chasing venture capital, playing the “grow-at-all-costs” game and relinquishing partial control to investors, despite the pandemic and the uncertain circumstances many founders find themselves facing.

Through my work running and scaling Bulletin, I’ve followed thousands of product-based businesses ranging from indie beauty brands selling clean serums and cleansers to sex tech companies making couples’ vibrators and foreplay accessories. I’ve followed them on Instagram, in the press and across various platforms, and in many cases, I’ve spoken to their founders directly.

Over the past two years, I interviewed executives at more than 30 women-owned businesses for my upcoming book, “How to Build a Goddamn Empire,” and had long phone calls with dozens of independent brands and makers as Bulletin got a handle on how the pandemic was impacting customers. And I noticed something new and remarkable about what founders want now, in 2021, compared to what they wanted in years past.

Back then, I’d get dozens of cold emails and DMs asking how I successfully raised VC and what the unspoken rules might be. I’d hear from business owners who were considering a raise or gearing up for one. Product-based entrepreneurs approached me at panels or Bulletin events and say they wanted to be the “Glossier for X” or the “Away for Y.” Many younger founders didn’t even know what venture capital really was, but they saw it as symbolic validation for the business, or the only way to get “big.”

Now, brands would rather scrape by than pursue an injection of funding on someone else’s terms; just ask the Gorjana founders or Scott Sternberg. Many brands that saw astronomical growth in 2020, like Rosen, Golde, Entireworld and others that spurred similar growth for Etsy and Shopify are fully bootstrapped businesses, and proudly so.

Some founders I’ve spoken to have even outright rejected offers for investment. A lot of D2C brands are interested in learning about alternative forms of financing like bank loans, lines of credit and crowdfunding, and ask about iFundWomen or Kickstarter, observing the success of other fully crowdfunded brands like Dame and Pepper.

Venture capital, from my vantage point, has lost its sheen for a lot of product-based brands. They’re not destitute and desperate for financing. They’re actually scoffing at the prospect and trusting they can succeed, scale and maintain long-term profitability without swapping equity for cash. They’re tripped up by what they’ve been reading in the media, or they’ve survived or even thrived during COVID, as a fully bootstrapped company, and feel more conviction than ever that the “grow slow” approach is the right move.

They’re reading the same stories about layoffs and tenuous unit economics at massive D2C companies and agreeing with Sam Kaplan that the old playbook — pricey customer acquisition practices, rapid scale, endless rounds of funding — is out of date. It’s 2021 and we’re midpandemic. These brands want to turn a profit.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie:

Now that the U.S. has a new president coming in whose policies are more welcoming to immigrants, I am considering coming to the U.S. to expand my company after COVID-19. However, I’m struggling with the morass of information online that has bits and pieces of visa types and processes.

Can you please share an overview of the U.S. immigration system and how it works so I can get the big picture and understand what I’m navigating?

— Resilient in Romania

Dear Resilient:

We welcome you to the U.S.! Our country greatly benefits from international entrepreneurs like you who expand here to innovate, create jobs and bolster the global economy.

I followed in my father’s footsteps to become an immigration attorney to fulfill my personal mission of helping people live the life of their dreams in the United States. A big part of making that happen is to give individuals the information and the tools they need to clearly set their immigration goals and to reach them quickly.

Check out my recent podcast where I provide a brief, high-level overview of the U.S. immigration system. The United States is a nation founded by immigrants. The immigration system is based on many of the same values and principles enshrined in our Constitution.

In 1965, the U.S. Congress passed the Immigration and Nationality Act, the foundation of all of our immigration laws today. Although some amendments to the act have been made over more than 50 years since then, the immigration system still operates under the same framework created back then. One of the things I appreciate about this framework is that there are so many legal routes to immigrate to the U.S. that are available.

There are many visa and green card categories you can use to chart your course. As a creative lawyer with plenty of lead time before somebody moves to the U.S., it provides many options to work with. Law doesn’t just place restrictions on people; it can be used as a tool for creation.

So, even though the system has its challenges and can be greatly improved, successfully navigating the system is doable. Everyone from individuals to founders, CEOs at startups and HR and Global Mobility at giant companies, families and couples in love — you just need to know the right questions to ask and the information to empower you to find the right immigration path.

My father used to always say there are five main areas of immigration law:

I have worked on cases in each of these areas, but my firm focuses primarily on business and family immigration. Business immigration encompasses both visas and green cards, whereas family immigration only involves green cards that are based on an individual’s relationship to a U.S. citizen or permanent resident (green card holders), including fiance visa and different pathways to green cards.

At a high level, the U.S. offers two types of visas: nonimmigrant visas and immigrant visas. Immigrant visas are also called green cards.

Nonimmigrant visas allow for a temporary stay in the U.S. Each nonimmigrant visa that allows its holder to work in the U.S. requires an employer to sponsor the individual and hire them after approval and arrival. Each nonimmigrant is designed to allow an individual with certain skills, education or expertise that will benefit the employer, the employer’s industry or the U.S in general, such as a multinational executive (L-1) an individual in a specialty occupation (H-1B) or with extraordinary ability (O-1).

Some nonimmigrant visas are based on the candidate’s home country or whether the individual’s home country has a trade agreement with the U.S. Each work visa has different requirements for renewals. I discuss these and other startup-friendly visas and green cards in more detail in a podcast on the most startup-friendly visas and green cards.

A green card allows its holder to live and work permanently in the U.S. and is the first step to obtaining U.S. citizenship. Some nonimmigrant visas lead directly to a green card. However, many do not. So it’s important to be creative and strategic from the beginning of your U.S. immigration journey.

Most employment-based green cards require an employer sponsor. The two exceptions are the EB-1A green card for extraordinary ability and the EB-2 NIW (National Interest Waiver) for exceptional ability. Individuals can apply for these green cards on their own without an employer sponsor or job offer. We cover both of these green cards, as well as the O-1 nonimmigrant visa in Extraordinary Ability Bootcamp, an online course that takes a deep dive into the O-1A nonimmigrant visa, and the EB-1A and EB-2 NIW green cards, for which you may be eligible to apply.

Most international founders and entrepreneurs typically qualify for an E-2, L-1 or O-1 visa, or an EB-1A, EB-1C or EB-2 NIW green card. Take a look at the immigration options chart we created that outlines the most common visa and green card categories that apply to founders, investors and talent.

In addition to the various visa and green card options, you should know that you can apply for a visa or green card while living outside the U.S. or while living inside the U.S. Living outside the U.S., you can apply for a visa or green card at a U.S. embassy or consulate, which is called consular processing. Once living in the U.S., you can apply for change of status to another visa or adjustment of status to a green card. For more information about specific visas and green cards and how to navigate the U.S. immigration system, check out my weekly podcast.

Even during COVID, I’m confident you’ll find your way to the U.S. to begin your journey of expanding your company. I wish you good health and much success in 2021!

Best regards,

Sophie

Have a question? Ask it here. We reserve the right to edit your submission for clarity and/or space. The information provided in “Dear Sophie” is general information and not legal advice. For more information on the limitations of “Dear Sophie,” please view our full disclaimer here. You can contact Sophie directly at Alcorn Immigration Law.

Sophie’s podcast, Immigration Law for Tech Startups, is available on all major podcast platforms. If you’d like to be a guest, she’s accepting applications!

Powered by WPeMatico

The lure of subscription pricing is the guarantee of recurring revenue for your business. Once a customer flips the switch to turn on your subscription, it’s easy money:

While that’s true, converting a subscription customer isn’t as simple as flipping a switch. You can build a platform, launch with fanfare, offer all sorts of incentives and trials to attract potential customers — and watch as they disengage and lapse into limbo.

Contrary to popular belief, subscription pricing doesn’t work because of the lower price point that a monthly installment allows.

That’s the actual guarantee that comes with subscription pricing, which will happen unless you cultivate a funnel that catches potential subscribers as soon as they learn about your product and follows them until their very last sign-in.

I built my first subscription-model product in 1999. I’m currently in early-access on my latest, and I’ve launched a bunch more along the way.

While the customer dynamic has changed over the last 20 years, the conversion process has not. In fact, it’s actually gotten easier to convert and retain customers through the subscription funnel.

Here’s what I’ve learned.

Subscription pricing is a hot trend in just about every business in every industry. Pay-as-you-go is the new normal from software to retail to service.

In my mind, the major shift occurred when mobile phones started pricing unlimited usage per period instead of fixed or cost per minute. Once usage limits were removed, use cases exploded and the promise of a truly mobile computer was finally realized.

Makers of all stripes learned that lesson: From razors to video streaming to accounting software, pricing models have emerged that focus on time periods instead of units.

But contrary to popular belief, subscription pricing doesn’t work because of the lower price point that a monthly installment allows. It’s effective because a subscription reorients each customer’s mind from product function to value proposition.

I don’t care what kind of German engineering went into my razor blades, as long as I have working blades when I need them.

As an entrepreneur, you probably use at least one digital subscription service to build your own product and company, if not several. In fact, just to get to the MVP of my new project, I subscribed to AWS, MailChimp, Zapier and Bubble. I’m still on the free tier of a few more services for some lower-priority features. There’s a few more I quit or never tried.

Thus, you know that value prop plays a big part of whether the customer will pay and stay. So reinforcing your value proposition should play a big part in every level of your customer funnel.

A subscription-pricing model without an ability to track the steps in the conversion funnel will result in all the headaches of subscription pricing without any of the benefits.

Powered by WPeMatico

From COVID-19’s curve to election polls, public temperature checks to stimulus checks, 2020 was dominated by numbers — the guiding compass of any self-respecting venture capital investor.

As a VC exclusively focused on investments in Israeli cybersecurity, the numbers that guide us have become some of the most interesting to watch over the course of the past year.

The start of a new year presents the perfect opportunity to reflect on the annual performance of Israel’s cybersecurity ecosystem and prepare for what the next twelve months of innovation will bring. With the global cybersecurity market outperforming this year’s panic-stricken expectations, we carefully combed through the figures to see how Israel’s market, its strongest performer, compared — and predict what it has in store.

The cybersecurity market continues to draw the confidence of investors, who appear to recognize its heightened importance during times of crisis.

The “cyber nation” not only remained strong throughout the pandemic, but even saw a rise in fundraising, especially around application and cloud security, following the emergence of remote workflow security gaps brought on by social distancing. Encouraged by this, investors have demonstrated committed enthusiasm to its growth and M&A landscape.

Emboldened by the sector’s overall strength and new opportunities, today’s Israeli visionaries are developing stronger convictions to build larger companies; many of them, already successful entrepreneurs, are making their own bets in the industry as serial entrepreneurs and angel investors.

Image Credits: YL Ventures (opens in a new window)

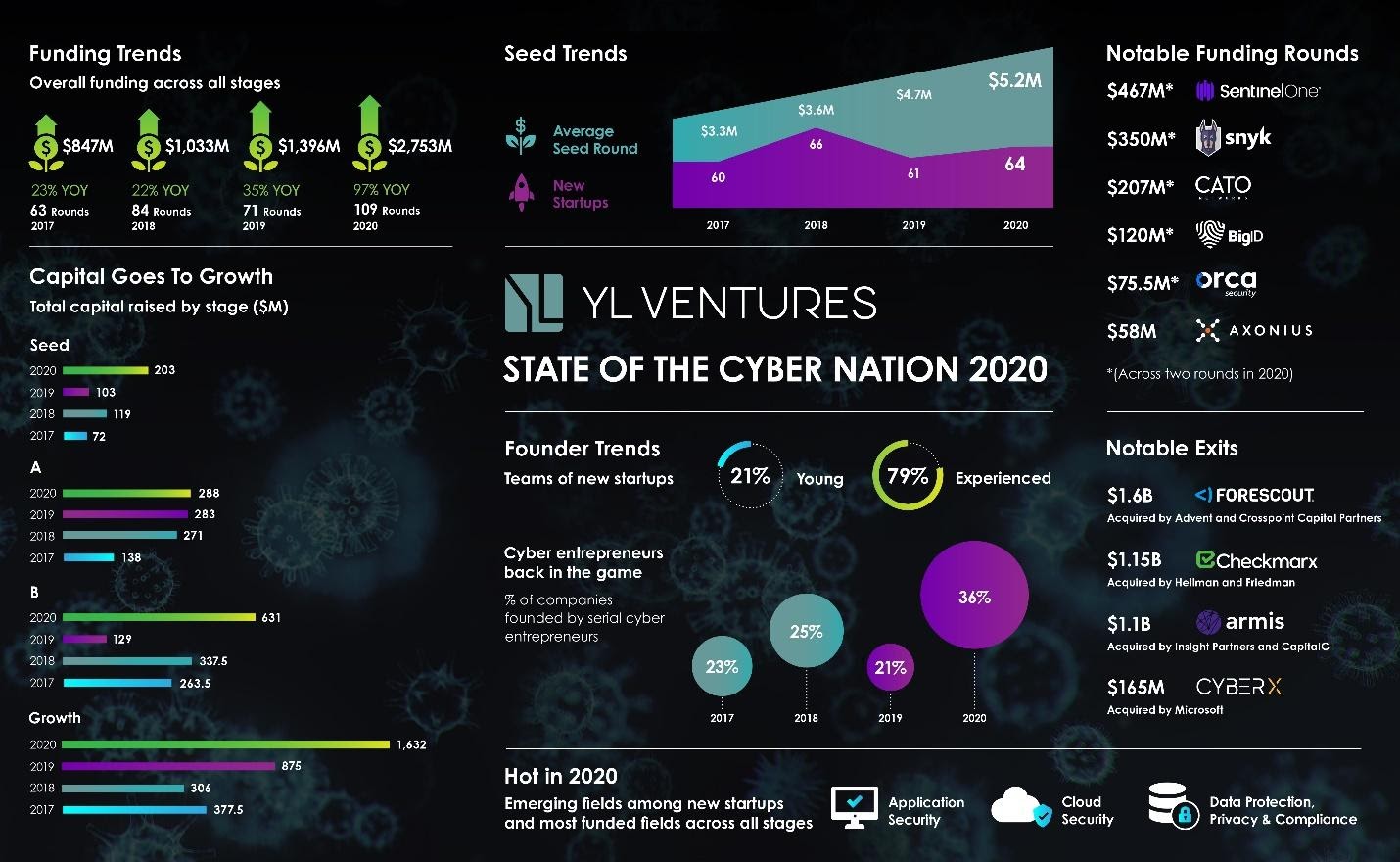

The numbers also reveal how investors are increasingly concentrating their funds on larger seed rounds for serial entrepreneurs and the foremost industry trends. More than $2.75 billion was poured into the industry this year to back companies across all stages, a 97% increase from last year’s $1.39 billion. If its long-term slope is any indication, we can only expect it to continue to grow.

However, though they clearly indicate progress, the numbers still make the need for a demographic reset clear. Like the rest of the industry, Israel’s cybersecurity ecosystem must adapt to the pace of change set out by this year’s social movements, and the time has long passed for true diversity and gender representation in cybersecurity leadership.

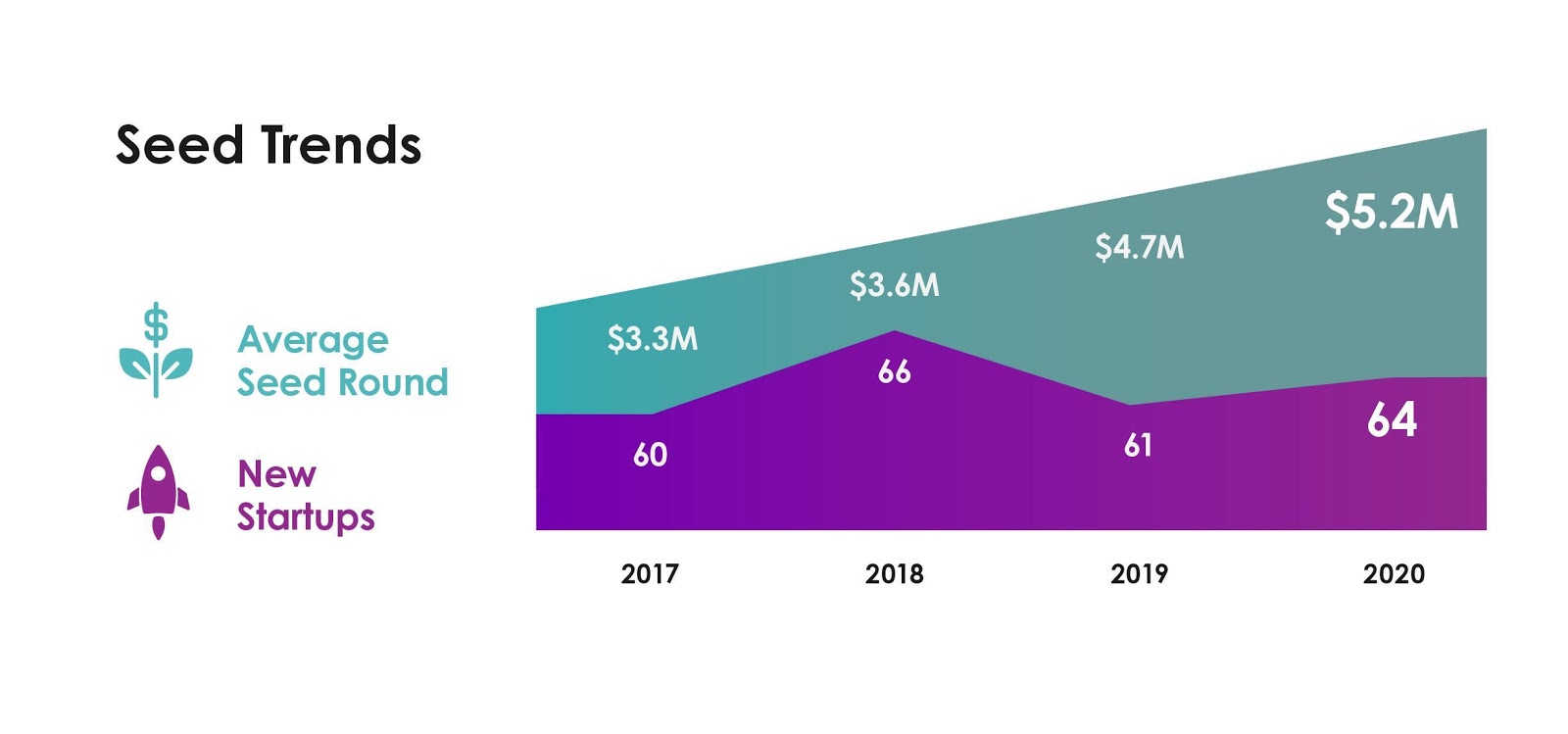

As the market’s biggest leaders garner experience and expertise, the bar for entry to Israel’s cybersecurity startup ecosystem has gradually risen over the years. However, this did not appear to impact this year’s entrepreneurial breakthroughs. 58% of Israel’s newly founded cybersecurity companies received seed rounds this year, totaling 64 seeded companies in 2020 compared with last year’s 61. The total number of newly founded companies increased by 5%, reversing last year’s downward trend.

The amount invested at seed hit an all-time high as average deal size in 2020 increased by 11%, amounting to an average of $5.2 million per deal. This continues an upward trend in average seed rounds, which have surged over the last four years due to sizable year-on-year increases. It also provides further support for a shift toward higher caliber seed rounds with a strategically focused and “all-in” approach. In other words, founders that meet the new bar for entry are raising bigger rounds for more ambitious visions.

Image Credits: YL Ventures

2020 proved an exceptional year for application security and cloud security startups. Perhaps the runaway successes of Snyk and Checkmarx left strong impressions. This year saw an explosive 140% increase in application security company seed investments (such as Enso Security, build.security and CloudEssence), as well as a whopping 200% increase in cloud security seed investments (like Solvo and DoControl), from last year.

Powered by WPeMatico