Column

Auto Added by WPeMatico

Auto Added by WPeMatico

I’m a Black man in America — that’s hard. Black founders, and uniquely Black founders in tech, are facing insurmountable odds.

As the recipients of less than 1% of venture capital raise, institutionalized systems are visibly at play. Within almost 10 years of my entrepreneurial journey, I have encountered just as many setbacks and failures as I have successes.

However, I have pressed forward despite the disparities that often plague the Black entrepreneurial community. From imbalances in fundraising to minimal capital and access, Black brilliance and its cloak of resilience continues to rise.

Now, as a CEO who has ambitiously raised nearly $13 million for my current venture, against the odds, I posit that it is not the Black founders who are missing out the most — it is the investors who are at a loss, not comprehending that they have underestimated the power of these founders’ Black brilliance.

Black founders need to own their resiliency and leverage the power that has resulted from their unique experiences.

When you think about the intersection of venture capital and technology, and specifically how it works — it is being led from an engineering perspective. Developers and coders historically go to specific schools and colleges, entering a funnel that guides them to success.

Historically, many Black students (more so Black male students), are influenced by sports as a vehicle to higher education and not necessarily the institutions recognized for technological prowess.

Their parents and community encourage athleticism because that is the only thing they know — as an institutionalized mindset reinforced over time. Unless they are guided into the accepted foundations for technology, or get into a Cal Berkeley, Stanford or Harvard, where many of the technology companies are built, they are immediately funneled outside of the “circle,” which sets the first of many ongoing obstacles for a Black tech founder.

I offer, however, that these “obstacles” are not in fact barriers but the crucial catalyst for these founders’ superpowers.

Admittedly, there were no entrepreneurs in my family. I did not have access to information about the best colleges. Despite having great grades and graduating with honors, I was completely unaware of how valuable an Ivy League education could be.

As a star basketball player, with my skills and grades, I could have played and graduated from somewhere like Yale, Brown, Columbia or even a school like Southern Methodist University where I was offered a full scholarship. But because of the lack of knowledge that I could actually do so and benefit from being inside the Ivy League “circle,” I didn’t.

I was in college from 2000 to 2004. A lot of great companies were started at elite schools during that period. It is this institutional blocking of information from myself and many other Black students that molded our overall perspective and created our glass ceilings.

Breaking through that glass ceiling, overcoming these odds to press forward relentlessly, with unyielding focus, and to hold conversations with the types of investors I have had to sit in front of, with the type of company that I have built, takes a different level of brilliance that only the Black experience can provide. For 2021 and beyond, Black founders need to not only recognize, but unlock that power as they look to fundraise and catapult their tech companies to success. It would be smart, and incredibly beneficial for investors, venture capitalists and the entire entrepreneurial ecosystem to take heed.

For Black founders, a paradigm shift is evident, but it can only manifest if implemented in these five ways.

Black founders and specifically Black tech founders are fed a monotonous script of how to raise money “the right way,” in light of disparaging statistics highlighting a lack of funding — so much that there is a robotic approach to the process. They try to become this cookie-cutter entrepreneur that is designed to raise money from investors, with their playbook and by their rules.

Black founders capitulate and conform to what society has dictated as appropriate fundraising, often glorifying the investor with the fate of their startup in their hands, without realizing that they hold the negotiating power. Their playbook hasn’t won us any games. As of today, own your power.

Set the playbook aside and lean more into your expertise and uniqueness.

Years ago, Mark Cuban delivered a keynote address at Dallas Startup Week that chronicled his road to success. One of his main points was to “Know your business, and know your business cold.” It was so simple, yet so impactful.

Early on in my career, I learned about venture capital from my experiences working for a startup. While I did not know the area in depth, I referenced what little knowledge I had as I raised for my own company years later. Although I was limited in my dealings with venture capitalists, I was confident in my background and expertise (at that time as a payroll technology sales professional) to truly stake my claim and seat at the table.

So while they may have sold a company for $7 billion or have $35 billion AUM (assets under management), I knew that they were not as well-versed in payroll or payroll technology than I was. It was this tenacious mindset that made me look at investors, rather than up to them, thereby positioning us on equal footing.

As a Black founder in tech, I have encountered many injustices — from networking to fundraising to the game of business as a whole. Even among those sitting at the table, there is a plethora of worldviews, political preferences, religious propensities and more that create a melting pot of divisiveness. However, recognizing that the common thread between all of the players in the game is the desire to be part of the brilliant business opportunity at hand is what will ultimately prevail.

It served me well not to overindex whether the venture capitalists liked me or on our differences. Locking in on the ambition of my entrepreneurial spirit and focusing on my brilliance — my Black brilliance — made them want to invest in me. Simplistically, investors want to give their money to founders who will make them money — passionately and ambitiously. Be you and find the investor that appreciates you.

Black founders are not getting in front of enough investors. Systemically, the venture capital landscape has marginalized this community and has failed to expand their network for inclusiveness. Currently, ethnic minorities are severely underrepresented in the venture capital industry. Eighty percent of investment partners are white, with only a staggering 3% being Black or African-American.

Regardless, Black entrepreneurs must press forward and still show up. The sheer number of people that entrepreneurs must face during the fundraising process is astronomical, so one must not be swayed by the disillusionment of opportunity.

Realistically speaking, it takes a long time to raise money. Period. I have talked to thousands of potential investors to raise nearly $13 million for my current company. If you are a Black founder, it is going to take you longer to fundraise and you are going to have to get in front of more people. So I ask, “Do you have enough oxygen in the tank to withstand the obstacles, for a long enough period of time, to attract the venture capital that you need?” The wealth gap says no.

When I first started Gig Wage, the number one question I received from investors is, “How much runway do you have?” I would answer, “Until I get to where I need to get.” They would then rephrase, “How much money do you have in the bank? How long is your wife going to let you do this?” I would reply, “It does not matter how much money I have in the bank because I’m going to keep going until this happens.”

Discriminatively, there was this unspoken expectation that I lacked the financial wherewithal and stamina to withstand the fundraising process, and at times it was extremely discouraging — because to be honest, when I looked in the bank account, I realistically had about nine to 12 months of runway.

The reason Black people raise less than 1% of venture capital is because the racism weaved into the fabric of American society bleeds over into the entrepreneurial ecosystem. Despite it all, I took thousands of meetings. I was willing to endure with an ambitious conviction that I was going to win. Again, this is Black brilliance.

As a Black man, I have personally endured challenges to build resiliency — mirroring similar realities of other Black men in America. Whether it was dealing with the police or witnessing men in my family struggle with drugs, violence, poverty or the like — I often think, “Why would I be intimidated by an investor meeting or a term sheet?” The construct of America has dealt me much worse.

Black founders need to own their resiliency and leverage the power that has resulted from their unique experiences. The victory mentality that ensues thereafter is the type of mindset that venture capitalists should want to invest in, and if they do not, they are undoubtedly missing out.

The unyielding focus of “The world is stacked against me but I’m not going to quit. I’m going to pivot. I’m going to be resourceful. I’m going to figure it out — even if I’m scared,” is a person you need to invest in. It is not necessarily that they have a groundbreaking business idea, but culturally, Black people have a passion and a perspective that is unmatched, with limitless possibilities that venture capitalists are overlooking.

So for 2021 and well beyond, Black founders, and those especially in tech, need to shift their respective paradigms, own their place within the entrepreneurial space, take back their power and continue to operate at the utmost in Black brilliance. It is the investors, not the founders, that are missing out. Be bold. Be courageous. Be audacious.

As for me, the best thing that I can do right now is to continue to drive the conversation, illuminate the disparities and be as successful for Black entrepreneurs, Black professionals and the world at large as possible. I am owning my power and I’m committed to epitomizing and evangelizing Black brilliance.

Powered by WPeMatico

In an earlier article, I wrote about how and when to build go-to-market teams at deep tech companies. There, I noted that it is more important for growth hires at deep tech companies to have functional expertise than industry expertise.

But how do deep tech companies connect and cultivate strong relationships with talented nontechnical growth people outside of their industry? In this article, I answer this question, articulating exactly how to:

Incredible growth people are independent and creative and are drawn to environments that explicitly value these traits.

Underscore the autonomy. Incredible growth people are independent and creative and are drawn to environments that explicitly value these traits. Growth talent wants to know that they have room to experiment, fail and iterate with the support and trust of their company. Highlight the creative agency you give to your growth team. Paint the role as one of managing a subset of the startup and its initiatives.

Show you are ready for a growth marketer. Do not expect your growth person to be a panacea for the company. Growth people work cross-functionally, but there are boundaries where the growth role starts and ends. Growth people cannot sell a product that is not ready. Growth people cannot fix product bugs. Growth people cannot replace excellent customer service. Ensure your role description is clear on what the growth person would do and what they would lean on other teams for. Demonstrate that you have a team structure in place where a growth marketer could fit in and thrive.

Articulate your talent needs. Growth is a broad category. Some growth marketers are more creative. Others are more quantitative. Some have more industry experience. Others have more functional experience. Be clear on what type of growth marketer you need and how this person’s talents would complement those of the existing team.

Generate excitement and establish credibility. People can naturally be skeptical about new technologies and younger companies. Do anything you can to ameliorate these concerns. Link to relevant news articles from well-known publications and thought leaders in your industry. Incorporate customer testimonials that speak to the transformative impact your product creates. Name drop well-known advisors, investors and team members.

Powered by WPeMatico

Five years ago I landed the Solar Impulse 2 in Abu Dhabi after flying around the globe powered solely by solar energy, a first in aviation history.

It was also a milestone in energy and technology history. Solar Impulse was an experimental plane, weighing as little as a family car and using 17,248 solar cells. It was a flying laboratory, full of groundbreaking technologies that made it possible to produce renewable energy, store it and use it when necessary in the most efficient manner.

The time has come to use technology again to address the climate crisis affecting us all. As we enter the most crucial decade of climate action — and most likely our last chance to limit global warming to 1.5°C — we need to ensure that clean technologies become the only acceptable norm. These technologies exist now and they can be profitably implemented at this crucial moment.

Hundreds of clean tech solutions exist that protect the environment in a profitable way,

Here are just four innovations from our solar-powered plane that the market can start using now before it’s too late.

The building sector is one of the largest energy consumers in the world. Next to a reliance on carbon-heavy fuels for heating and cooling, poor insulation and associated energy loss are among the main reasons.

Inside Solar Impulse’s cockpit, insulation was crucial for the plane to fly at very high altitudes. Covestro, one of our official partners, developed an ultra-lightweight and insulating material. The cockpit insulation performance was 10% higher than the standards at the time because the pores in the insulating foam were 40% smaller, reaching a micrometer scale. Thanks to its very low density of fewer than 40 kilograms per cubic meter, the cockpit was ultra-lightweight.

This technology and many others exist. We now need to ensure that all market players are motivated to make hyperefficient building insulation their standard operating procedure.

Solar Impulse was first and foremost an electric airplane when it flew 43,000 km without a single drop of fuel. Its four electric motors had a record-beating efficiency of 97%, far ahead of the miserable 27% of standard thermal engines. This means that they only lost 3% of the energy they used versus 73% for combustion propulsion. Today, electric vehicle sales are soaring. According to the International Energy Agency, when Solar Impulse landed in 2016, there were approximately 1.2 million electric cars on the road; the figure has now risen to over 5 million.

Nevertheless, this acceleration is far from enough. Power sockets are still far from replacing petrol pumps. The transport sector still accounts for one-quarter of global energy-related CO2 emissions. Electrification must happen much more quickly to reduce CO2 emissions from our tailpipes. To do so, governments need to boost the adoption of electric vehicles through clear tax incentives, diesel and petrol engine bans, and major infrastructure investments. 2021 should be the year that puts us on a one-way road to zero-emission vehicles and puts thermal engines in a dead end.

To fly for several days and nights, reaching a theoretically endless flight potential, Solar Impulse relied on batteries that stored the energy collected during the day and used it to power its engines during the night.

What was made possible with Si2 on a small scale should guide the way to future-proofing power-generation systems that are made up entirely of renewable energy. In the meantime, microgrids, like those used in Si2, could benefit off-grid systems in remote communities or energy islands, allowing them to abolish diesel or other carbon-heavy fuels already today.

On a larger scale, we are looking at smart grids. If all “stupid grids” were replaced by smart grids, it would allow cities, for example, to manage production, storage, distribution and consumption of energy and to cut peaks in energy demand that would reduce CO2 emissions dramatically.

Solar Impulse’s philosophy was to save energy instead of trying to produce more of it. This is why the relatively small amount of solar energy we collected became enough to fly day and night. All the airplane parameters, including wingspan, aerodynamics, speed, flight profile and energy systems, had therefore been designed to minimize energy loss.

Unfortunately, this approach still stands out against the inefficiency of most of our energy use today. Even though the IEA found energy efficiency improved by an estimated 13% between 2000 and 2017, it is not enough. We need bolder action by policymakers to encourage investors. One of the best ways to do so is to put strict energy efficiency standards in place.

For example, California has set efficiency standards on buildings and appliances, such as consumer electronics and household appliances, estimated to have saved consumers more than $100 billion in utility bills. These measures are as good for the environment as they are for the economy.

When we used all these different innovations to build Solar Impulse, they were groundbreaking and futuristic. Today, they should define the present; they should be the norm. Next to the technologies mentioned above, hundreds of clean tech solutions exist that protect the environment in a profitable way, many of which have received the Solar Impulse Efficient Solution Label.

Just as for the Si2 technologies, we must now ensure that they enter the mainstream market. The faster we scale them, the faster we will set our economy on track to achieve the Paris Agreement goals and attain sustainable economic growth.

Powered by WPeMatico

The world has spent most of 2020 adapting to ever-changing guidelines and restrictions (with no end in sight, even as the vaccines start to roll out). Board meetings are quickly increasing in their significance to foster consistent and vital interactions as an organization. It’s essential for companies to capitalize on the essential time together during these uncertain times.

While we might look like the Brady Bunch while sharing a Zoom window, are you actually communicating more like the family from “Succession?”

Are your meetings organized? Do people talk over one another? Do you usually run over time? Are you giving people time to digest information?

As we move into 2021 and Q1 meetings are being put onto calendars, take some time to modernize how you conduct your board meetings.

Board meetings are quickly increasing in their significance to foster consistent and vital interactions as an organization.

Having served on public company boards, growth-stage businesses and Series A startups, an observation I have made in boards that are later stage are more about financial analysis and governance. Whereas earlier-stage board discussions hinge more on product strategy, key partnerships, sharing best practices to help develop founders as executives and important hiring decisions.

Since the nature of the discussions is more, let’s call it … creative in earlier-stage businesses, where the focus is on where they’ve been particularly impacted by reduced bandwidth for collaboration while meeting remotely.

As said best by Mike Maples and paraphrased by Jeff Bonforte — there are only four things a board really needs to consider:

Collecting data around those points is the job. In the meeting, the team can add color.

Remember the board works for you, so be sure to put them to work. Sharing materials with participants about three days ahead of time tends to be the best. Any later and they may not get enough time to digest, send earlier and the information might be out of date by the time you meet. It’s most common to format as a deck, but lately I’m seeing more written format and even magazine-style.

The number one request I get from early-stage companies is “help find me more customers.”

Other common requests are “help me find or land this type of talent, help me with industry benchmarks for this type of business deal or compensation structure, connect me to people that have experience with X so I can learn ways we could structure our process.” It’s helpful to put these asks in the materials you send ahead because sometimes board members might not be able to react quickly and now “homework” comes up spontaneously in the discussions.

Another purpose of these meetings is to build working relationships so when strategic decisions need to be made, board members are used to working together. Sometimes it is a forum for executives to gain exposure to board members and for board members to have the opportunity to evaluate and provide input on executives. For that reason execs are often invited to participate in certain discussions.

Like the product person who presents a roadmap or a market analysis, the head of sales should give color on pipeline and competitive deals, the marketing person may lead a discussion on ABM or channel marketing tactics, the engineering lead might ask for feedback on their metrics versus other companies, etc. Generally, CEOs also bring forth an interesting topic to have a discussion, such as channel strategy, market mapping/sizing, hiring plan and related issues.

As far as logistics, we reserve two hours in calendars but we try to hit 90 minutes. I suggest something like this for a 90-minute session:

Powered by WPeMatico

Fundraising is challenging, especially for deep tech founders who need to get investors excited about a complex technology, a complex sales cycle and a complex risk profile.

As a former investor and current angel investor, I have met thousands of founders, many in the deep tech space.

Based on my experience, here’s how to avoid making the most common mistakes deep tech founders make when pitching investors:

Early-stage investors are in the business of funding dreams. They chose to be early-stage investors because they love hearing about new ideas and enthralling futures. They deliberately are not investment bankers or accountants because they do not want to constantly pour over endless spreadsheets or dive deep into financial models. Similarly, they are not operators because they do not want to spend time figuring out the intricacies of a supply chain or a marketing campaign or the configuration of a product component.

Make your pitch tailored to what excites venture capital investors and avoid what does not.

So make your pitch tailored to what excites venture capital investors and avoid what does not. Keep the financial model details and the warehouse system logistics information to your Appendix. You have it in case anyone wants to dive in deeper, but your core presentation should be focused on your biggest, most bullish hopes for the company seven to 10 years from now. Dedicate multiple slides to painting the picture of what society would look like should you meet all your intended milestones as a company.

As a deep tech company, your differentiation is in your intellectual property. However, investors care less about the “what” and much more about the “so what.” Investors are less interested in the intricacies of your technology and more interested in what impact it can create.

Formulate your slides to focus on answering questions like, “What can people or companies do as a result of your technology?” and “How will people save time, money and lives with your product?”

Put your presentation to the “grandma” test. Would your grandmother be able to understand and be excited about everything you share? Investor pitch meetings are not dissertation defenses. You are being evaluated on your potential for impact rather than the intricate details of your research. The best way to succeed in this evaluation framework is to ensure that everything you share is relevant and exciting to a diverse audience of even nontechnical folks.

Five million people are a statistic, but one person is a story. When people read data on massive populations of people, they conceptually understand the implications but only on a logical level, not an emotional one. When pitching, you want to reach the hearts of investors.

Powered by WPeMatico

The wave of venture capital interest in geographies other than Silicon Valley has been building momentum over the past 5+ years. If you measure capital flow by Twitter chatter alone, you may assume the tidal wave is about to break and checks are being doled out via T-shirt launchers repurposed from hockey games.

Meanwhile, VCs will approach founders saying, “We are now looking into markets beyond Silicon Valley.”

When Mucker launched back in 2011, our founding partners, who had left Silicon Valley for LA, set out to prove that high-growth companies can be built anywhere. Our portfolio from this past decade is a testament to this very narrative. With offices in LA, Austin and Nashville — and investments all over North America, we are seeing a marked increase in receptivity to an idea we had over a decade ago to invest across the U.S. and into Canada.

As of late, I’m receiving more and more outreach from VCs based in San Francisco, New York and beyond interested in deal flow here in Nashville and the Southeast.

When we think about the opportunity beyond Silicon Valley, we are really speaking of America.

In reality, there will be some lag time before the checks being written by these same VCs are consistent with both the outward hype and existing market opportunity. The broadened geographic focus of VCs for marketing purposes and FOMO is not adequately capturing the real narrative.

In short: When we think about the opportunity beyond Silicon Valley, we are really speaking of America.

“We” is a loaded declaration. I write this as a venture capitalist and also as the biracial daughter of a first-generation immigrant, with both of my parents growing up poor by most people’s standards. One branch of my family immigrated to the U.S. from Mexico during the Mexican Revolution, the other harkens back to rural Oklahoma. The founders I meet day in and day out in the Southeast oftentimes tell a similar story.

My story is that of the average American, and yet feels light years apart from what people perceive as the “innovation economy.” Many of the people I’ve met in venture capital this past decade come from prestigious lineages with parents and grandparents who may have never associated with mine. And yet, here we are. This is America.

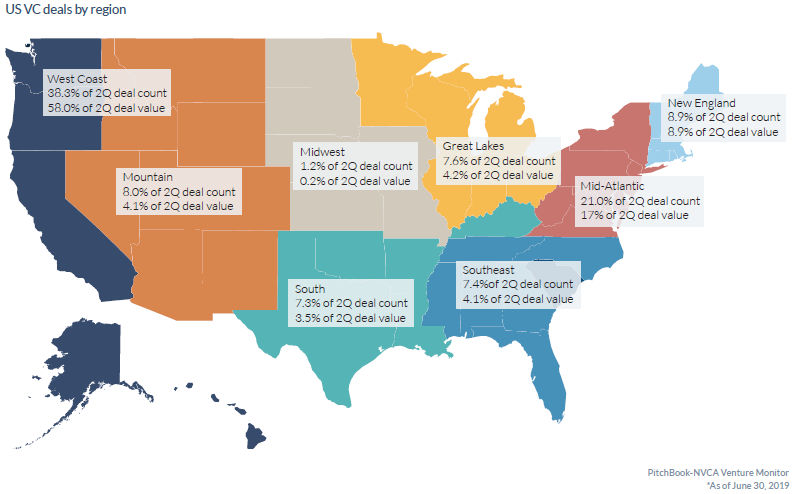

While Silicon Valley’s origins and climb to international stardom center around a collection of innovators, attracting more innovators and capital as the decades passed, one critical element arguably fell by the wayside — America as an expansive and diverse collection of states and people. Annual reporting on where venture capital dollars flow supports this discrepancy, with the majority of funds being funneled into companies based in and around Silicon Valley.

U.S. VC deals by region, as of June 2019. Image Credits: PitchBook/NVCA Venture Monitor

We find ourselves at the threshold of a decade where America will be rightfully recast as the land of opportunity for VC dollars to flow into the products and services fueling America’s future. And, at the helm of such innovations needs to be the people closest to these market opportunities, in full alignment with their customers and the nuances to best serve them.

In a post-COVID world, customers have never demanded more transparency into supply chains, workplace culture and equity ownership. Customers are more informed than ever before, with a 24/7 info line on brands and a growing scrutiny on where to place their hard-earned dollars. In short, they demand to be seen, and the founders who recognize this are the ones thriving in this new climate.

Where do the customers live? I’ll give you a hint: They are largely not in Silicon Valley.

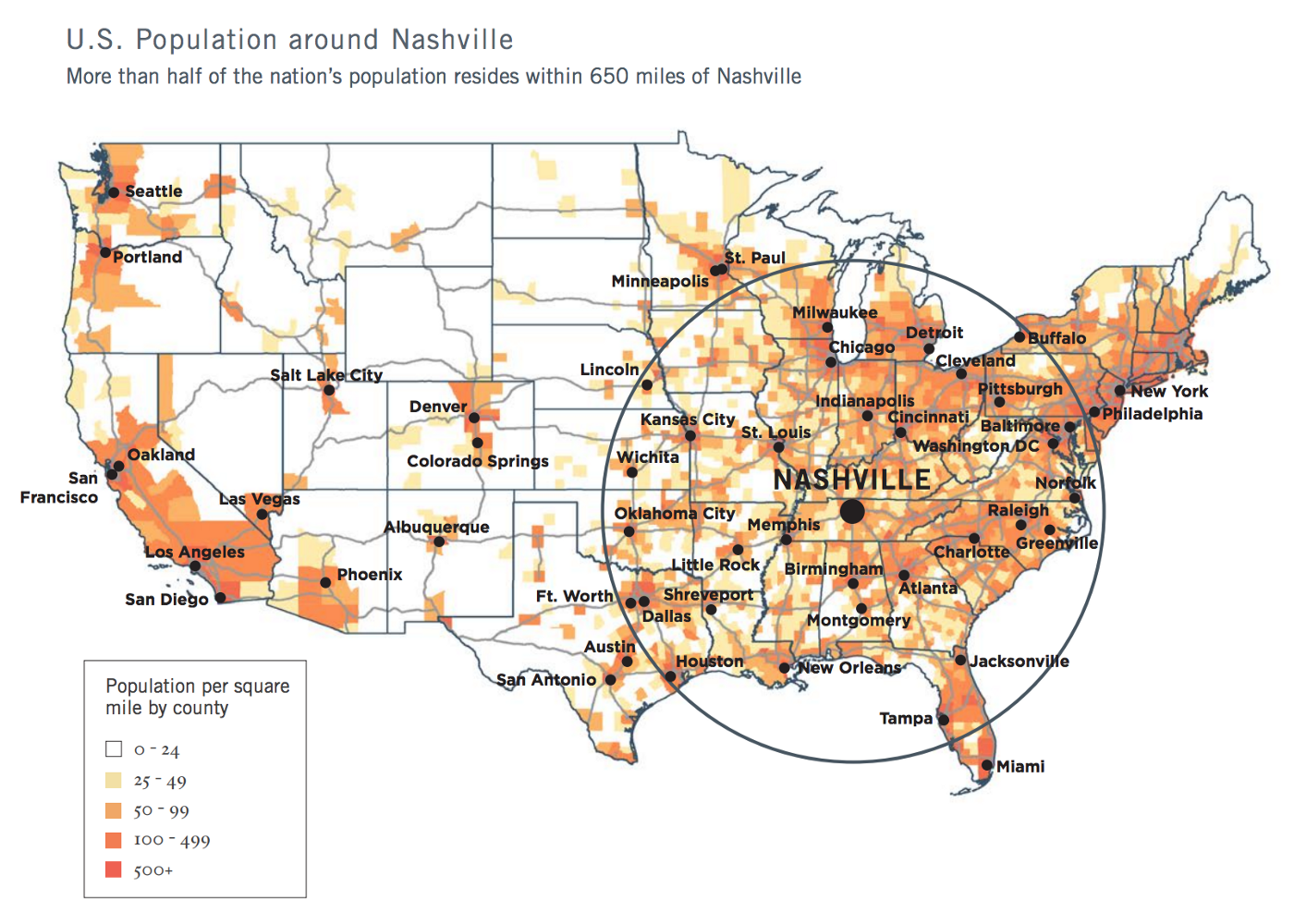

U.S. population around Nashville, TN. Image Credits: Nashville 2018 Regional Economic Development Guide

I wrote about the unfair advantage of Nashville back in 2018 when I announced the launch of Build In SE, a community I co-founded to support founders choosing to build their companies in the Southeast. Nashville is at the center of over half of the United States population within a radius of 650 miles, and within a two-hour flight of 75% of the U.S. market.

Customers come in all shapes and sizes, and founders with boots on the ground in these markets, wearing the same brand of proverbial boots as these customers, carry an unfair advantage. These same founders historically bootstrapped their companies out of need, as access to early-stage, high-risk capital can be scarce and vary widely city by city, state by state, industry by industry.

These same founders still built household name companies in the tech and innovation economy, including the likes of Mailchimp, Calendly, Lynda.com, and GoFundMe (their Series A valued them at $600 million pre-money). All of these companies have another thing in common — they were founded “beyond Silicon Valley.”

Another macrotrend at play is that of the increasing distribution of talent beyond traditional metropolitan strongholds like San Francisco and New York. Entrepreneurs, technologists and operational talent are lifestyle-seeking at a time in history when life feels all the more precious. Moving to cities like Nashville, Austin, Atlanta, Denver, Durham, Miami, et. al. means proximity to aging family members, affordable childcare and outdoor activities.

These simple pleasures were the tradeoffs people made when “pursuing their dreams” in coastal cities, picking up to move in pursuit of money (sometimes better weather). Seemingly overnight, capital abounds in the private markets just as talent becomes increasingly scarce and therefore valuable. The pendulum swung, and capital became the weaker of the two magnets; Wall Street began moving up Manhattan island toward coffee shops and dog parks when talent began to pose the question, “How long do I want my commute to be?” and “How much time do I want to reclaim for my family, and myself?”

2020 was the match to ignite this dry hillside. People trapped inside of cramped quarters with resources left to invest in a new life (or in other cases, left with nothing to lose) packed their bags for a new, up-and-coming metro.

For some, this comes with a newfound sense of community and belonging, as I experienced in 2017 when I moved from my lifelong home of Los Angeles to Nashville. In LA, my local neighborhood hardly knew one another due to the transient nature of the town. In Nashville, I became part of something greater than myself.

One of the big frustrations expressed by founders I know in markets like Nashville, Atlanta, the Research Triangle, Cincinnati and Toronto, is, “I keep hearing there is more capital available, but I’m not seeing it.” They will meet with investors, then be told they are too early, raising too little money, or too much, or not going after a “big enough market.”

Sometimes, one or more of these may be true. However, there are instances where these investor responses may be thinly veiled criticism of the perceived ability of the founders who might not sound, look or behave like Silicon Valley entrepreneurs.

Closing this gap of understanding between pattern-matching VCs of varying skill and startup CEOs across the country will require hard work in the coming decade. A big piece of this will require breaking bread as neighbors, with kids in the same schools, a shared affinity for the local greasy spoon and a mutual trust. This will be step one. Though really, it will require much more alignment and rigor around the very definition of America.

It is up to investors to capture this opportunity in the next decade. In fact, it is our job.

Powered by WPeMatico

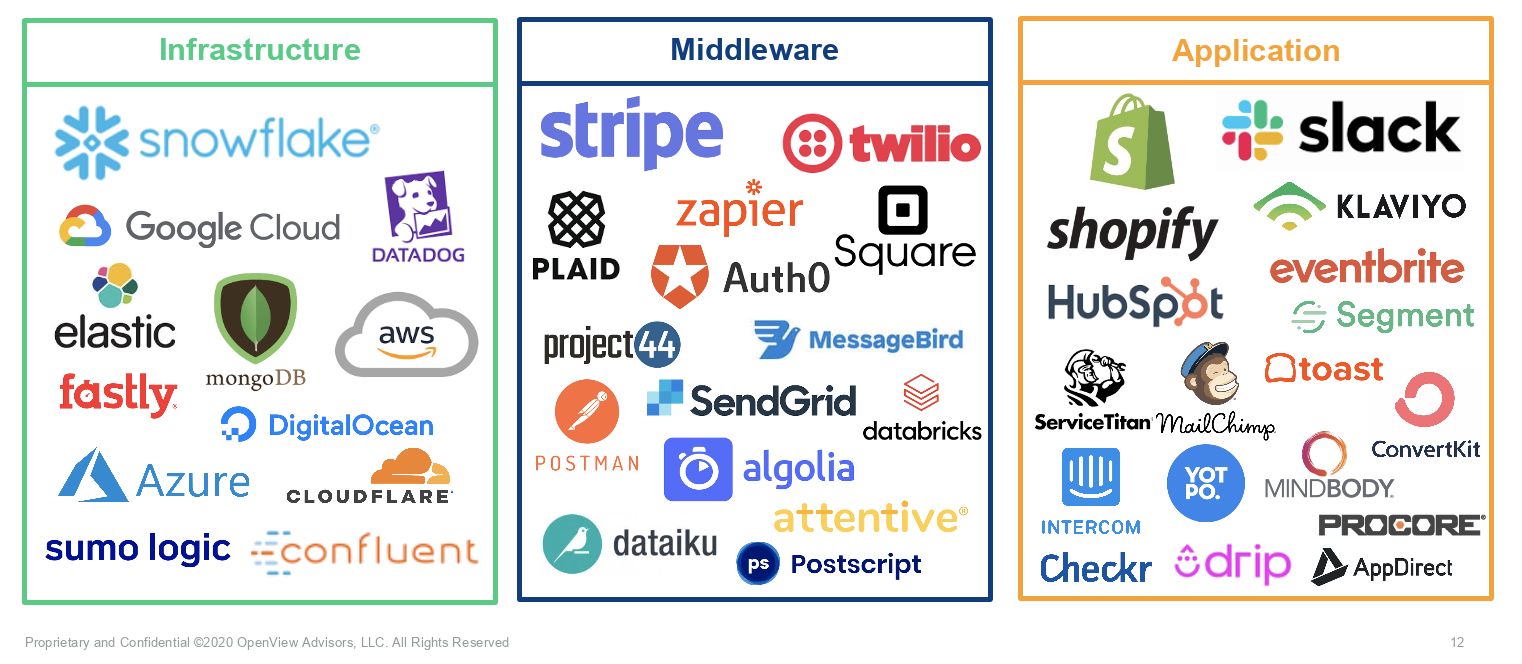

Software buying has evolved. The days of executives choosing software for their employees based on IT compatibility or KPIs are gone. Employees now tell their boss what to buy. This is why we’re seeing more and more SaaS companies — Datadog, Twilio, AWS, Snowflake and Stripe, to name a few — find success with a usage-based pricing model.

The usage-based model allows a customer to start at a low cost, while still preserving the ability to monetize a customer over time.

The usage-based model allows a customer to start at a low cost, minimizing friction to getting started while still preserving the ability to monetize a customer over time because the price is directly tied with the value a customer receives. Not limiting the number of users who can access the software, customers are able to find new use cases — which leads to more long-term success and higher lifetime value.

While we aren’t going 100% usage-based overnight, looking at some of the megatrends in software — automation, AI and APIs — the value of a product normally doesn’t scale with more logins. Usage-based pricing will be the key to successful monetization in the future. Here are four top tips to help companies scale to $100+ million ARR with this model.

Usage-based pricing is in all layers of the tech stack. Though it was pioneered in the infrastructure layer (think: AWS and Azure), it’s becoming increasingly popular for API-based products and application software — across infrastructure, middleware and applications.

Image Credits: Kyle Povar / OpenView

Some fear that investors will hate usage-based pricing because customers aren’t locked into a subscription. But, investors actually see it as a sign that customers are seeing value from a product and there’s no shelf-ware.

In fact, investors are increasingly rewarding usage-based companies in the market. Usage-based companies are trading at a 50% revenue multiple premium over their peers.

Investors especially love how the usage-based pricing model pairs with the land-and-expand business model. And of the IPOs over the last three years, seven of the nine that had the best net dollar retention all have a usage-based model. Snowflake in particular is off the charts with a 158% net dollar retention.

Powered by WPeMatico

In light of climate change and escalating global energy demand, more emphasis is being placed on emerging clean technologies — ranging from renewables and energy storage to nuclear power. Although these technologies have tremendous potential, they require lots of innovation, and innovation needs abundant capital.

The issue: early-stage financing for clean tech hasn’t been plentiful, and it’s stifling the growth of new energy companies. Why is this? In general, clean tech companies lack the startup advantages of agility and flexibility.

“Moving fast” works for products such as consumer mobile apps and SaaS solutions. The clean tech sector, on the other hand, tends to involve highly regulated, capital-intensive, mission-critical infrastructure.

That has hurt both returns and well-intentioned impact. According to Cambridge Associates, venture-backed companies have returned, on average, -15% internal rate of return (IRR) since 2000. Contrast that to venture-backed companies in healthcare, which returned 24% in IRR over the same time period.

While noble in its aims to make the world a better, cleaner, safer, healthier place through technology, clean tech venture capital has suffered simply because clean tech does not fit the traditional venture capital model. Central to the venture capital model is the ability to de-risk new ideas and significantly capitalize the most promising ones, allowing for liquidity via M&A or initial public offering (IPO).

Early-stage financing for clean tech hasn’t been plentiful, and it’s stifling the growth of new energy companies.

This construct allows for the return of venture capital dollars, plus appreciation that enables VC firms to raise new funds. These capitalization events also allow the venture-backed company to accelerate growth and maximize market impact.

How this construct works is evident when comparing healthcare and clean tech. In healthcare, new innovations are de-risked by VCs. More mature innovations are acquired or reach IPO every year. As a result, the average annual ratio of dollars raised via an exit to VC-invested dollars since 2012 is 1.8. This ratio is only 0.2 for clean tech, an 800-plus percent difference in the wrong direction. This has resulted in poor returns and limited capitalization of clean tech companies.

Given the state of the world’s environment and lack of abundant energy in emerging economies, we need to collectively fix this issue. Special purpose acquisition companies (SPACs) are significantly improving clean tech’s venture capital construct. According to Investopedia:

SPACs are companies with no commercial operations that are formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.

Also known as “blank-check companies,” SPACs have been around for decades. In recent years, they’ve become more popular, attracting big-name underwriters and investors and raising a record amount of IPO money in 2019.

In 2020, more than 110 SPACs completed transactions in the U.S., capitalizing these companies with more than $29 billion.

In 2020, SPACs capitalized clean tech companies with almost $4 billion of capital, including Fisker, Lordstown Motors, QuantumScape, Hyliion, XL Fleet and others. This helped push the ratio of funds raised at exit to venture capital invested in 2020 from the previous 0.2 average to a much healthier 0.6, a 200% improvement.

In 2021, we will likely see even further improvement. Why? Because there are 43 active SPACs looking toward or finalizing merger targets with a clean tech focus, potentially providing $12 billion in growth capital. Even if there are no more new SPACs in 2021 and a historically low average of M&As and IPOs, 2021 promises continued improvement for clean tech investment.

One of the most high-profile clean tech SPACs was Nikola Corporation. The battery-electric and hydrogen-powered truck maker has attracted much fanfare since going public last June through a reverse merger with special purpose acquisition company VectoIQ. The company’s market capitalization soared and things seemed to be going well, but things became controversial later in the year when the company was accused of making false statements about its technology and other things.

Although examples such as Nikola have the potential to tarnish the emergence of SPACs as a way to spur clean tech investing, they shouldn’t. There are plenty of examples of emerging companies that scream quality and integrity. For example, Stem*, a leader in the energy storage optimization space, is now going public, pending SEC approval, via the Star Peak SPAC.

Public markets are receiving the SPAC with enthusiasm. Assuming the merger happens, Stem will be capitalized with greater than $450 million of cash to accelerate growth and drive impact. It’s an illustration of SPACs as a positive venture capital construct that is needed to make clean tech work and become a thriving sector.

As a long-time clean tech venture capitalist myself, it is interesting that public investment via the SPAC may be the correcting element for the clean tech VC construct. For years, I assumed that corporates would step up their M&A activity at premium valuations to solve this issue, but I’ve spent a long time waiting.

Judging by activity, corporates seem content to continue playing the still very important investor/nurturer role, versus the “owning” role. Regardless, capitalizing promising clean tech companies can only mean one thing: clean-tech-related impact is coming like never before as these companies require and use capital to scale.

New and more diverse approaches to finding and funding new, great clean tech companies are sorely needed. SPACs are going to be the tool needed to bring clean tech up to par with sectors such as healthcare. It’s a development that will benefit all of us.

*Stem is a Wind Ventures portfolio company.

Powered by WPeMatico

June 4, 2019 should have been one of the happiest days of my life.

At 11:30 a.m., a press release hit the wire announcing that the cybersecurity company I had spent more than eight years building was being acquired by a larger cybersecurity player.

What’s not to love about a successful exit? I’d be set financially, the investors who had given us $70 million would make money, and the technology we created would get new legs in an organization with broader reach and resources.

Still, I had regrets. For one thing, I initially hadn’t wanted to sell. (More on that later.) For another, I was nagged by the feeling that our company had fallen short of its true potential, and that the reason was me — specifically, several rookie mistakes I made as a first-time entrepreneur.

I don’t stew about those errors any longer. In fact, I believe my miscues at my first startup will help define my career from here on out. That’s why, as I grow my next company, I’m thinking about not only the things I want to do but those I’d never do again.

Here are five of them.

In management theory terms, I was a “pacesetter.” I’d be the first to jump into any project or task, I’d execute it as quickly as possible and I expected everyone else to keep up. I thought that was how a startup leader acted — super helpful and scrappy.

But it came at a big price: disempowerment of the team. I was hoarding not only control — nobody felt like they personally owned anything — but also the institutional knowledge that needs to be spread around as a company grows. I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.

I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.

After a few years, I had a frustrating sense that I had all the answers and no one else did. Well, no wonder.

I’m now leaving the pacesetting to NASCAR and marathons.

I believed all I had to do was say something once and everyone would get it. I became irritated when that didn’t happen. “We talked about this three months ago,” I’d bark. Intimidated team members would say to themselves, “Yeah, but we really only got 50% of it.”

Powered by WPeMatico

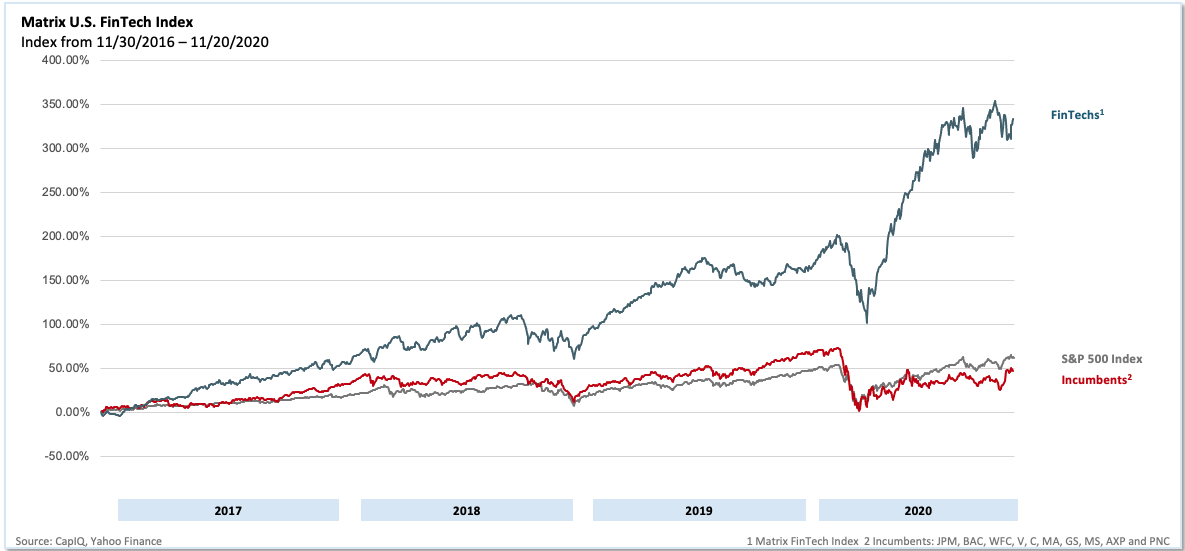

Three years ago, we released the first edition of the Matrix Fintech Index. We believed then, as we do now, that fintech represents one of the most exciting major innovation cycles of this decade. In 2020, all the long-term trends forcing change in this sector continued and even accelerated.

The broad movement away from credit toward debit, particularly among younger consumers, represents one such macro shift. However, the pandemic also created new, unforeseen drivers. Among them, millennials decamped from their rentals in crowded cities to accelerate their first home purchases to the benefit of proptech companies and challenger mortgage players alike.

E-commerce saw an enormous acceleration in growth rates, furthering adoption of online payments platforms. Lastly, low interest rates and looming inflation helped pave the way for the price of Bitcoin to charge toward $30,000. In short, multiple tailwinds combined to produce a blockbuster year for the category.

In this year’s refresh of the Matrix Fintech Index, we’ll divide our attention into three parts. First, a look at the public stocks’ performance. Second, liquidity. Third, we highlight one major trend in the sector: Buy Now Pay Later, or BNPL.

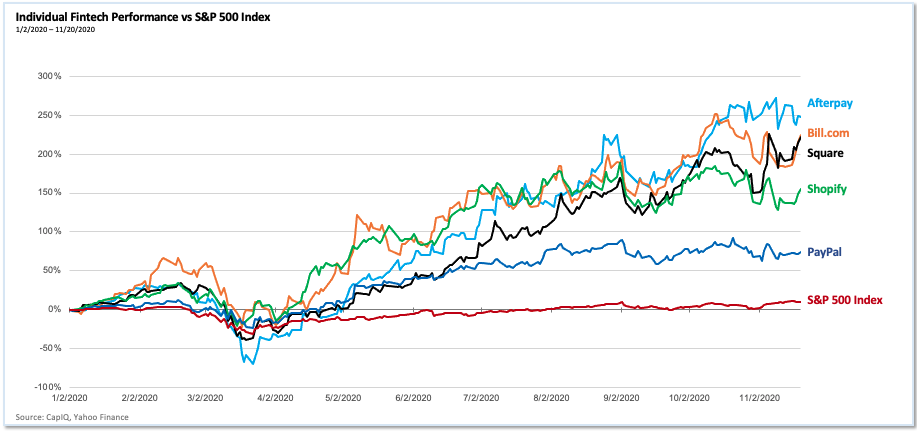

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index. While the underlying performance of these companies was strong, the pandemic further bolstered results as consumers avoided appearing in-person for both shopping and banking. Instead, they sought — and found — digital alternatives.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index.

Our own representation of the public fintechs’ performance is the Matrix Fintech Index — a market cap-weighted index that tracks the progress of a portfolio of 25 leading public fintech companies. The Matrix fintech Index rose 97% in 2020, compared to a 14% rise in the S&P 500 and a 10% drop for the incumbent financial service companies over the same time period.

2020 performance of individual fintech companies vs. SPX Image Credits: CapiQ, Yahoo Finance

Matrix U.S. Fintech Index, 2016 -2020 Image Credits: CapiQ, Yahoo Finance

E-commerce undoubtedly stood out as a major driver. As a category, retail e-commerce grew 35% YoY as of Q3, propelling PayPal and Shopify to add over $160 billion of market capitalization over the year. For its part, PayPal in the third quarter signed up 15 million net new active accounts (its highest ever).

Powered by WPeMatico