cloudflare

Auto Added by WPeMatico

Auto Added by WPeMatico

Facebook is a monopoly. Right?

Mark Zuckerberg appeared on national TV today to make a “special announcement.” The timing could not be more curious: Today is the day Lina Khan’s FTC refiled its case to dismantle Facebook’s monopoly.

To the average person, Facebook’s monopoly seems obvious. “After all,” as James E. Boasberg of the U.S. District Court for the District of Columbia put it in his recent decision, “No one who hears the title of the 2010 film ‘The Social Network’ wonders which company it is about.” But obviousness is not an antitrust standard. Monopoly has a clear legal meaning, and thus far Lina Khan’s FTC has failed to meet it. Today’s refiling is much more substantive than the FTC’s first foray. But it’s still lacking some critical arguments. Here are some ideas from the front lines.

To the average person, Facebook’s monopoly seems obvious. But obviousness is not an antitrust standard.

First, the FTC must define the market correctly: personal social networking, which includes messaging. Second, the FTC must establish that Facebook controls over 60% of the market — the correct metric to establish this is revenue.

Though consumer harm is a well-known test of monopoly determination, our courts do not require the FTC to prove that Facebook harms consumers to win the case. As an alternative pleading, though, the government can present a compelling case that Facebook harms consumers by suppressing wages in the creator economy. If the creator economy is real, then the value of ads on Facebook’s services is generated through the fruits of creators’ labor; no one would watch the ads before videos or in between posts if the user-generated content was not there. Facebook has harmed consumers by suppressing creator wages.

A note: This is the first of a series on the Facebook monopoly. I am inspired by Cloudflare’s recent post explaining the impact of Amazon’s monopoly in their industry. Perhaps it was a competitive tactic, but I genuinely believe it more a patriotic duty: guideposts for legislators and regulators on a complex issue. My generation has watched with a combination of sadness and trepidation as legislators who barely use email question the leading technologists of our time about products that have long pervaded our lives in ways we don’t yet understand. I, personally, and my company both stand to gain little from this — but as a participant in the latest generation of social media upstarts, and as an American concerned for the future of our democracy, I feel a duty to try.

According to the court, the FTC must meet a two-part test: First, the FTC must define the market in which Facebook has monopoly power, established by the D.C. Circuit in Neumann v. Reinforced Earth Co. (1986). This is the market for personal social networking services, which includes messaging.

Second, the FTC must establish that Facebook controls a dominant share of that market, which courts have defined as 60% or above, established by the 3rd U.S. Circuit Court of Appeals in FTC v. AbbVie (2020). The right metric for this market share analysis is unequivocally revenue — daily active users (DAU) x average revenue per user (ARPU). And Facebook controls over 90%.

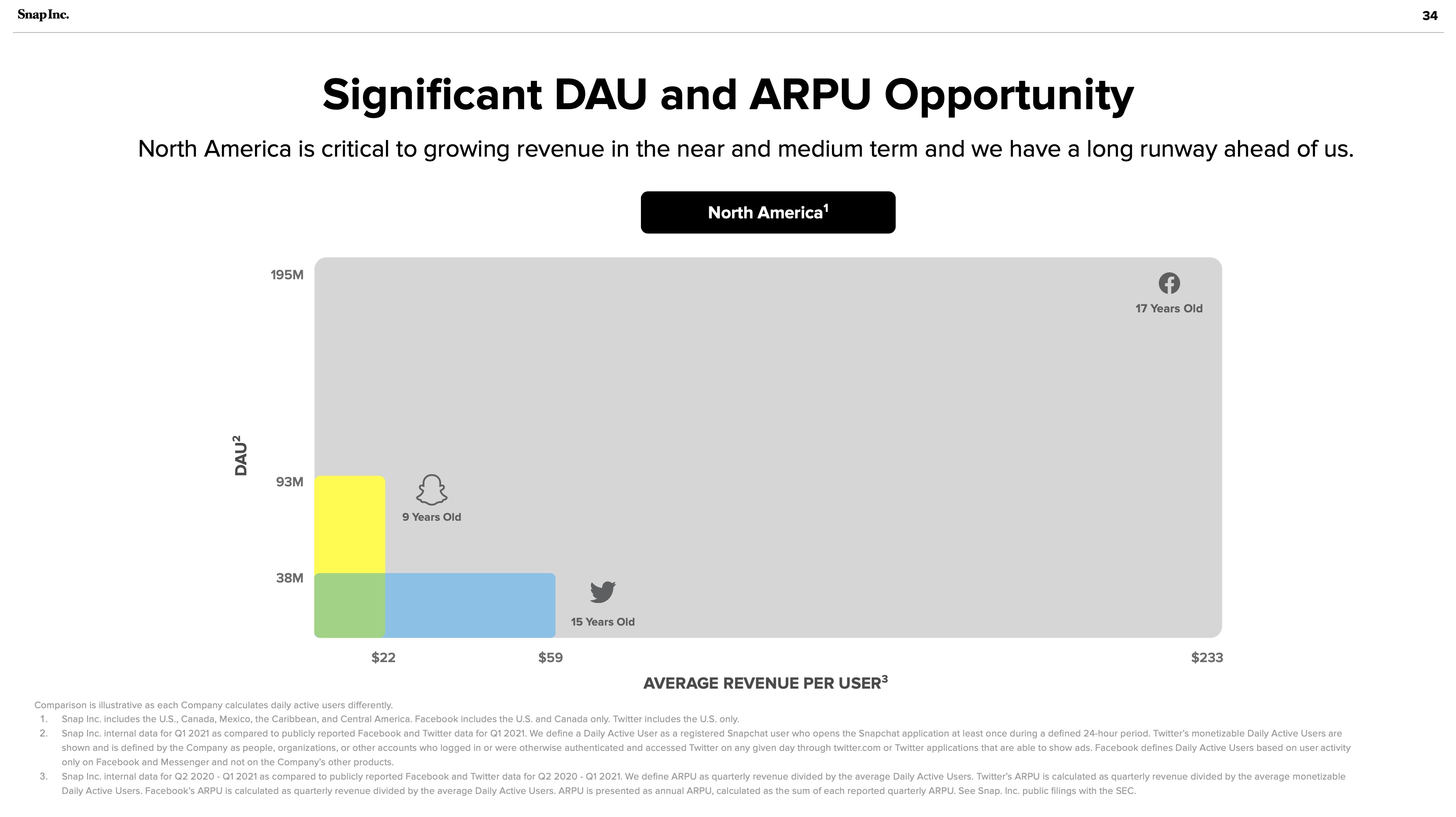

The answer to the FTC’s problem is hiding in plain sight: Snapchat’s investor presentations:

Snapchat July 2021 investor presentation: Significant DAU and ARPU Opportunity. Image Credits: Snapchat

This is a chart of Facebook’s monopoly — 91% of the personal social networking market. The gray blob looks awfully like a vast oil deposit, successfully drilled by Facebook’s Standard Oil operations. Snapchat and Twitter are the small wildcatters, nearly irrelevant compared to Facebook’s scale. It should not be lost on any market observers that Facebook once tried to acquire both companies.

The FTC initially claimed that Facebook has a monopoly of the “personal social networking services” market. The complaint excluded “mobile messaging” from Facebook’s market “because [messaging apps] (i) lack a ‘shared social space’ for interaction and (ii) do not employ a social graph to facilitate users’ finding and ‘friending’ other users they may know.”

This is incorrect because messaging is inextricable from Facebook’s power. Facebook demonstrated this with its WhatsApp acquisition, promotion of Messenger and prior attempts to buy Snapchat and Twitter. Any personal social networking service can expand its features — and Facebook’s moat is contingent on its control of messaging.

The more time in an ecosystem the more valuable it becomes. Value in social networks is calculated, depending on whom you ask, algorithmically (Metcalfe’s law) or logarithmically (Zipf’s law). Either way, in social networks, 1+1 is much more than 2.

Social networks become valuable based on the ever-increasing number of nodes, upon which companies can build more features. Zuckerberg coined the “social graph” to describe this relationship. The monopolies of Line, Kakao and WeChat in Japan, Korea and China prove this clearly. They began with messaging and expanded outward to become dominant personal social networking behemoths.

In today’s refiling, the FTC explains that Facebook, Instagram and Snapchat are all personal social networking services built on three key features:

Unfortunately, this is only partially right. In social media’s treacherous waters, as the FTC has struggled to articulate, feature sets are routinely copied and cross-promoted. How can we forget Instagram’s copying of Snapchat’s stories? Facebook has ruthlessly copied features from the most successful apps on the market from inception. Its launch of a Clubhouse competitor called Live Audio Rooms is only the most recent example. Twitter and Snapchat are absolutely competitors to Facebook.

Messaging must be included to demonstrate Facebook’s breadth and voracious appetite to copy and destroy. WhatsApp and Messenger have over 2 billion and 1.3 billion users respectively. Given the ease of feature copying, a messaging service of WhatsApp’s scale could become a full-scale social network in a matter of months. This is precisely why Facebook acquired the company. Facebook’s breadth in social media services is remarkable. But the FTC needs to understand that messaging is a part of the market. And this acknowledgement would not hurt their case.

Boasberg believes revenue is not an apt metric to calculate personal networking: “The overall revenues earned by PSN services cannot be the right metric for measuring market share here, as those revenues are all earned in a separate market — viz., the market for advertising.” He is confusing business model with market. Not all advertising is cut from the same cloth. In today’s refiling, the FTC correctly identifies “social advertising” as distinct from the “display advertising.”

But it goes off the deep end trying to avoid naming revenue as the distinguishing market share metric. Instead the FTC cites “time spent, daily active users (DAU), and monthly active users (MAU).” In a world where Facebook Blue and Instagram compete only with Snapchat, these metrics might bring Facebook Blue and Instagram combined over the 60% monopoly hurdle. But the FTC does not make a sufficiently convincing market definition argument to justify the choice of these metrics. Facebook should be compared to other personal social networking services such as Discord and Twitter — and their correct inclusion in the market would undermine the FTC’s choice of time spent or DAU/MAU.

Ultimately, cash is king. Revenue is what counts and what the FTC should emphasize. As Snapchat shows above, revenue in the personal social media industry is calculated by ARPU x DAU. The personal social media market is a different market from the entertainment social media market (where Facebook competes with YouTube, TikTok and Pinterest, among others). And this too is a separate market from the display search advertising market (Google). Not all advertising-based consumer technology is built the same. Again, advertising is a business model, not a market.

In the media world, for example, Netflix’s subscription revenue clearly competes in the same market as CBS’ advertising model. News Corp.’s acquisition of Facebook’s early competitor MySpace spoke volumes on the internet’s potential to disrupt and destroy traditional media advertising markets. Snapchat has chosen to pursue advertising, but incipient competitors like Discord are successfully growing using subscriptions. But their market share remains a pittance compared to Facebook.

The FTC has correctly argued for the smallest possible market for their monopoly definition. Personal social networking, of which Facebook controls at least 80%, should not (in their strongest argument) include entertainment. This is the narrowest argument to make with the highest chance of success.

But they could choose to make a broader argument in the alternative, one that takes a bigger swing. As Lina Khan famously noted about Amazon in her 2017 note that began the New Brandeis movement, the traditional economic consumer harm test does not adequately address the harms posed by Big Tech. The harms are too abstract. As White House advisor Tim Wu argues in “The Curse of Bigness,” and Judge Boasberg acknowledges in his opinion, antitrust law does not hinge solely upon price effects. Facebook can be broken up without proving the negative impact of price effects.

However, Facebook has hurt consumers. Consumers are the workers whose labor constitutes Facebook’s value, and they’ve been underpaid. If you define personal networking to include entertainment, then YouTube is an instructive example. On both YouTube and Facebook properties, influencers can capture value by charging brands directly. That’s not what we’re talking about here; what matters is the percent of advertising revenue that is paid out to creators.

YouTube’s traditional percentage is 55%. YouTube announced it has paid $30 billion to creators and rights holders over the last three years. Let’s conservatively say that half of the money goes to rights holders; that means creators on average have earned $15 billion, which would mean $5 billion annually, a meaningful slice of YouTube’s $46 billion in revenue over that time. So in other words, YouTube paid creators a third of its revenue (this admittedly ignores YouTube’s non-advertising revenue).

Facebook, by comparison, announced just weeks ago a paltry $1 billion program over a year and change. Sure, creators may make some money from interstitial ads, but Facebook does not announce the percentage of revenue they hand to creators because it would be insulting. Over the equivalent three-year period of YouTube’s declaration, Facebook has generated $210 billion in revenue. one-third of this revenue paid to creators would represent $70 billion, or $23 billion a year.

Why hasn’t Facebook paid creators before? Because it hasn’t needed to do so. Facebook’s social graph is so large that creators must post there anyway — the scale afforded by success on Facebook Blue and Instagram allows creators to monetize through directly selling to brands. Facebooks ads have value because of creators’ labor; if the users did not generate content, the social graph would not exist. Creators deserve more than the scraps they generate on their own. Facebook suppresses creators’ wages because it can. This is what monopolies do.

Facebook has long been the Standard Oil of social media, using its core monopoly to begin its march upstream and down. Zuckerberg announced in July and renewed his focus today on the metaverse, a market Roblox has pioneered. After achieving a monopoly in personal social media and competing ably in entertainment social media and virtual reality, Facebook’s drilling continues. Yes, Facebook may be free, but its monopoly harms Americans by stifling creator wages. The antitrust laws dictate that consumer harm is not a necessary condition for proving a monopoly under the Sherman Act; monopolies in and of themselves are illegal. By refiling the correct market definition and marketshare, the FTC stands more than a chance. It should win.

A prior version of this article originally appeared on Substack.

Powered by WPeMatico

Vantage, a service that helps businesses analyze and reduce their AWS costs, today announced that it has raised a $4 million seed round led by Andreessen Horowitz. A number of angel investors, including Brianne Kimmel, Julia Lipton, Stephanie Friedman, Calvin French Owen, Ben and Moisey Uretsky, Mitch Wainer and Justin Gage, also participated in this round.

Vantage started out with a focus on making the AWS console a bit easier to use — and helping businesses figure out what they are spending their cloud infrastructure budgets on in the process. But as Vantage co-founder and CEO Ben Schaechter told me, it was the cost transparency features that really caught on with users.

“We were advertising ourselves as being an alternative AWS console with a focus on developer experience and cost transparency,” he said. “What was interesting is — even in the early days of early access before the formal GA launch in January — I would say more than 95% of the feedback that we were getting from customers was entirely around the cost features that we had in Vantage.”

Image Credits: Vantage

Like any good startup, the Vantage team looked at this and decided to double down on these features and highlight them in its marketing, though it kept the existing AWS Console-related tools as well. The reason the other tools didn’t quite take off, Schaechter believes, is because more and more, AWS users have become accustomed to infrastructure-as-code to do their own automatic provisioning. And with that, they spend a lot less time in the AWS Console anyway.

“But one consistent thing — across the board — was that people were having a really, really hard time 12 times a year, where they would get a shocking AWS bill and had to figure out what happened. What Vantage is doing today is providing a lot of value on the transparency front there,” he said.

Over the course of the last few months, the team added a number of new features to its cost transparency tools, including machine learning-driven predictions (both on the overall account level and service level) and the ability to share reports across teams.

Image Credits: Vantage

While Vantage expects to add support for other clouds in the future, likely starting with Azure and then GCP, that’s actually not what the team is focused on right now. Instead, Schaechter noted, the team plans to add support for bringing in data from third-party cloud services instead.

“The number one line item for companies tends to be AWS, GCP, Azure,” he said. “But then, after that, it’s Datadog, Cloudflare, Sumo Logic, things along those lines. Right now, there’s no way to see, P&L or an ROI from a cloud usage-based perspective. Vantage can be the tool where that’s showing you essentially, all of your cloud costs in one space.”

That is likely the vision the investors bought into, as well, and even though Vantage is now going up against enterprise tools like Apptio’s Cloudability and VMware’s CloudHealth, Schaechter doesn’t seem to be all that worried about the competition. He argues that these are tools that were born in a time when AWS had only a handful of services and only a few ways of interacting with those. He believes that Vantage, as a modern self-service platform, will have quite a few advantages over these older services.

“You can get up and running in a few clicks. You don’t have to talk to a sales team. We’re helping a large number of startups at this stage all the way up to the enterprise, whereas Cloudability and CloudHealth are, in my mind, kind of antiquated enterprise offerings. No startup is choosing to use those at this point, as far as I know,” he said.

The team, which until now mostly consisted of Schaechter and his co-founder and CTO Brooke McKim, bootstrapped the company up to this point. Now they plan to use the new capital to build out its team (and the company is actively hiring right now), both on the development and go-to-market side.

The company offers a free starter plan for businesses that track up to $2,500 in monthly AWS cost, with paid plans starting at $30 per month for those who need to track larger accounts.

Powered by WPeMatico

Merge, a startup that helps its users build customer-facing integrations with third-party tools, today announced that it has raised a $4.5 million seed round led by NEA. Additional angel investors include former MuleSoft CEO Greg Schott, Cloudflare CEO Matthew Prince, Expanse co-founders Tim Junio and Matt Kraning, and Jumpstart CEO Ben Herman.

Launched in 2020, the core focus of Merge is to give B2B companies a unified API to access data from what is currently about 40 HR, payroll, recruiting and accounting platforms, with plans for expanding to additional areas soon. But Merge co-founders Shensi Ding and Gil Feig, who have been lifelong friends and previously worked at companies like Expanse and Jumpstart, stress that the service isn’t aiming to replace workflow tools Workato or Zapier.

Image Credits: Merge

“What we built is more similar to Plaid than MuleSoft or other things,” Feig said. “We built a unified API, so we’re fully embedded in a customer’s product and they build one integration with us and can automatically offer all these integrations to their customers. On top of that, we offer what we call integrations management, which is a suite of tools to automatically detect issues where the customer would have to get involved — automatically detect that stuff and handle it without ever having to involve engineering again.”

When Merge’s systems detect issues with an integration, maybe because a data schema in an API response has changed without notice (which happens with some regularity), Merge’s engineers can fix that within minutes, in part because the teams also built an internal no-code tool for building and managing these integrations.

Image Credits: Merge

As Ding also noted, B2B buyers today also simply expect their tools to feature integrations with the service they use. “Companies, when they purchase a vendor, they expect that vendor to have integrations with all the other vendors that they own,” she said. “They don’t want to have to purchase a vendor and then purchase a workflow product and then connect those products.”

And while Merge’s focus right now is squarely on a few verticals, the plan is to expand this to far more areas shortly, likely starting with CRM. “Salesforce has a pretty large market share, so we thought that it wasn’t going to be as interesting of a market,” Ding said. “But it turns out that their API is so complex that customers would still prefer to integrate with us instead if we simplify it for them.”

Ding and Feig tell me the company, which came out of stealth about two months ago, already has about 100 organizations on its platform, varying from seed-stage companies to publicly listed enterprises. The team credits its focus on security and reliability (and its SOC II compliance) with being able to bring on some of these larger companies despite being a seed-stage company itself.

To monetize the service, Merge offers a free tier (up to 10,000 API requests per month) and charges $0.01 per API request for additional usage. Unsurprisingly, the company also offers customized enterprise plans for its larger customers.

“The time and expense associated with building and maintaining myriad API integrations is a pain point we hear about consistently from our portfolio companies across all industries,” said NEA managing general partner Scott Sandell, who will join the company’s board. “Merge is tackling this ubiquitous problem head-on via their easy-to-use, unified API platform. Their platform has broad applicability and is a massive upgrade for any software company that needs to build, manage, and maintain multiple API integrations.”

Powered by WPeMatico

As the first sales hire at Cloudflare, I learned firsthand from both our high growth and my own mistakes how to build a world-class sales team. Early hires are the cultural cornerstones of an organization. As Vinod Khosla described the initial hires at Sun Microsystems, “Initial hiring is way more important than you think because of its multiplicative effect. So, it’s worth taking a little longer when you hire those people.”

The first sales hire will set the best practices, cultural tone and is responsible for making sure each subsequent new sales hire succeeds. For this reason, it is important that startups look to hire missionaries, not mercenaries, when they bring on their first sales team member. If the first sales hire is a “coin-operated” mercenary whose priority is to overachieve quota and is a great solo player, they may be more competitive than collaborative. In contrast, if the first hire is a missionary who cares more about evangelizing the product and is a team player, they will naturally enable the next set of hires to succeed.

There is an overwhelming amount of declarative advice on how to make your first sales hire: They should have experience selling at an early-stage company, tenure in that company to a much larger team (five to 50 employees, or $100,000 to $10 million ARR), they’ve sold at your price point, overachieved quota consistently (beware of this one. Quota overachievement can be a false positive and may be the result of a fruitful territory, a comp plan where quotas were too low or selfish “me-first” behavior.), etc. What you should look for are missionaries, and they exhibit two key qualities: resourceful ingenuity and team-based behavior.

At early-stage startups, there is more work to do than people to do it. These are resource-constrained environments where roles go beyond job descriptions and are “jack-of-all-trades” positions. This first sales hire is not an ordinary sales gig. It requires a missionary with a deep interest in the technology who wants to evangelize the product. The resourceful missionary must have an enterprising mindset to build their own sales collateral, a clever approach for testing pricing, a passion for the product technology and an ability to navigate the organization so engineering and product teams can hear the voice of the customer.

While resourceful skills are needed to test out different sales motions, the most important quality the missionary must have is a team-first attitude to share those learnings with colleagues. As the missionary, and the subsequent missionary hires, are developing a repeatable process they are engaging in novel intellectual work; this is not routine execution. When someone develops better messaging, or discovers a new use case, the goal is to spread that expertise so overall collective intelligence and team performance increases. If that operational know-how becomes siloed and an individual optimizes for themselves, instead of the team, the organization loses.

Powered by WPeMatico

When you start a company, it can be tempting to keep it simple. You want something that investors and customers can easily understand. While it might be easier to go that route, that is not something that Cloudflare did when it launched a decade ago at TechCrunch Disrupt. Instead, the company decided to go big or go home, and went with the wild idea of building a faster and safer internet. Not too much pressure.

It launched in 2010 with a free product and a paid tier and grew that original notion of delivering speed and security into a suite of products and services. Today, a decade later, Cloudflare is a public company with a market cap of nearly $12 billion.

We are going to talk to company co-founder and chief operating officer Michelle Zatlyn in a one-on-one interview at TechCrunch Disrupt 2020 about what it took to build off that vision as an early stage company. They were going after established giants like Akamai at the time. They needed to build a network of data centers around the world, starting with five on three continents at launch.

None of this could have been easy from an operations perspective. They were offering the bold assertion that they could make the world’s websites faster and safer and do it in a way that didn’t require any additional hardware and software. As an early adherent to the notion of cloud computing, they were giving customers the ability to do things that up until that point were only in reach of the largest internet properties, selling a value proposition that is common today, but was pretty unusual at the time.

We’re going to ask Zatlyn how they built this early product, how they grew the product set and expanded their data center coverage to over 200 around the world and what it took do all that and eventually become a public company.

You can see this session on the Disrupt stage along with all the programming on the Extra Crunch stage, network with CrunchMatch and discover hundreds of early-stage companies in Digital Startup Alley with your Digital Pro Pass purchase for just $345. There are discounts available for students, government and nonprofit employees as well as a great offer for early-stage founders who want to exhibit in Digital Startup Alley. Get your pass today before prices increase!

Powered by WPeMatico

How and when should startup founders think about the “exit”? It’s the perennial question in tech entrepreneurialism, but the hows and whens are questions to which there are a multitude of answers. For one thing, new founders often forget that the terms of the exit may not eventually be entirely in their control. There’s the board to think of, the strategic direction of the company, the first-in investors, the last-in. You name it. We’ll be chatting about this at Disrupt 2020.

Exits normally happen in only one of two ways: Either the startup gets acquired for enough money to give the investors a return or it grows big enough to list on the public markets. And it just so happens we have two perfect founders who will be able to unpack their own journeys on those two roads.

When Cloudflare went public last year it certainly wasn’t the end of its 10-year journey, and nor was it PlanGrid’s when it was acquired by Autodesk in 2018.

Cloudflare’s Michelle Zatlyn saw every nook and cranny of the company’s journey toward its IPO, which received a warm reception, even if there were a few bumps along the road leading up to it. What comes after an IPO and how do you even get there in the first place? Zatlyn will be laying it all out for us.

PlanGrid’s journey to acquisition by Autodesk was equally fascinating, and Tracy Young — who, as CEO and co-founder, shepherded the company to an $875 million exit — will be able to give us insight into what it’s like to dance with a potential acquirer, go through that (often fraught) process and come out the other side.

We’re excited to host this conversation at Disrupt 2020 and expect it to fill up quickly. Grab your pass before this Friday to save up to $300 on this session and more.

Powered by WPeMatico

Stanford’s success in spinning out startup founders is a well-known adage in Silicon Valley, with alumni founding companies like Google, Cisco, LinkedIn, YouTube, Snapchat, Instagram and, yes, even TechCrunch. And venture capitalists routinely back more founders coming out of the Stanford business program than any other university in the country.

One group of Stanford graduate students is well-aware of their favorable odds, and think that they should be able to cash in their classmates, too — not just accredited investors and the super-wealthy.

They have put together Stanford 2020, a new fund created entirely by Stanford classmates to invest in their fellow students’ ventures.

The idea was spurred by six students, who after a year of working with Fenwick & West law firm to find a suitable legal structure landed on creating an investment club — multiple parties can invest together as long as they have some form of shared ties.

Steph Mui, a founding member of Stanford 2020 and former venture capital associate at VC firm NEA, formed the club in defiance of the inaccessibility of angel investing, which she described as an elite Silicon Valley status symbol.

“Especially in Silicon Valley where it seems kind of a status symbol and only accredited people can do it, it feels very elite” she said. “We started thinking more about if we can actually make this something that the whole class could participate in, or at least make it more accessible to more than just like these small pockets of people that do it behind closed doors.”

Stanford 2020 club members must put up a minimum of $3,000 to join the investment club, and any eventual returns will be distributed proportionally to the investment each makes. So far, Mui tells TechCrunch that $1.5 million has been raised across 175 investors, with 50 investors willing to give $500,000 on the waitlist. In fact, the club is so “oversubscribed” that it is working to give money back.

Mui estimates that roughly 40% of the class is participating in the club. The founding members are being defined as “board members” who were recruited for passion and for diversity in background, professional interests and past leadership experience.

The group plans to invest $50,000 to $100,000 in startups depending on round size and valuation.

Mui thinks that Stanford 2020’s competitive advantage is largely the personal relationship it has with the companies it will invest in. After all, success might be just an arm’s reach away. Indeed, Cloudflare, Rent the Runway and ThredUp were all born in the same HBS classroom after being assigned a class project, according to Cloudflare CEO Matthew Prince.

“We have such strong pre-existing relationships, we know what people are working on way before they even raise,” Mui said.

Anyone who has been part of a club or team knows that loyalty runs deep, but we’ll see if that closeness is enough for a founder to dole out a stake in their company. While Stanford 2020 doesn’t take any management fee or carry, equity isn’t casual; in that vein, a famed Silicon Valley firm might be of better utility than your classmates.

Stanford 2020’s set up sounds similar to StartX, the university’s attempt at investing in its own, leafy backyard, which shut down in 2019. Launched in 2013, StartX offered to invest money in exchange for equity in any startup that went through its auxiliary accelerator and has $500,000 from professional investors.

Looking at Stanford 2020’s set up, the rules are almost exactly the same. Mui tells TechCrunch that startups must fulfill two criteria in order to automatically invest: first, the co-founder must be a member of the class, and second, they must raise a round of $750,000 or more from a reputable institutional investor. They define reputable as a list of 80 investors they got guidance on from advisors in the industry.

The concept of a rule-based automatic investment strategy comes with a big red flag: what if the founder has a bad idea or is a bad person, and still meets the criteria?

“I actually literally can’t think of a single person and I’m like, that person is so bad or so immoral, that we wouldn’t invest in them,” Mui said. “That’s part of the benefit of investing only in your classmates.”

But in case a Stanford-born class does have a problematic founder, Stanford 2020 has a veto voting mechanism.

In the grand scheme of things, Stanford-born startups are in a better spot than most when it comes to securing cash. They don’t desperately need another fund to invest in them. Mui’s ambition for Stanford 2020 is that other schools can copy and paste the legal structure they took a year (and a lot of hard work) to figure out.

She says they’re already getting inbound from incoming Stanford classes, other Stanford Schools and undergraduates. Now that it’s closed, she hopes they hear from other business schools, too.

Powered by WPeMatico

This week saw protests spread across the world sparked by the murder of George Floyd, an unarmed Black man, killed by a white police officer in Minneapolis last month.

The U.S. hasn’t seen protests like this in a generation, with millions taking to the streets each day to lend their voice and support. But they were met with heavily armored police, drones watching from above, and “covert” surveillance by the federal government.

That’s exactly why cybersecurity and privacy is more important than ever, not least to protect law-abiding protesters demonstrating against police brutality and institutionalized, systemic racism. It’s also prompted those working in cybersecurity — many of which are former law enforcement themselves — to check their own privilege and confront the racism from within their ranks and lend their knowledge to their fellow citizens.

The Justice Department has granted the Drug Enforcement Administration, typically tasked with enforcing federal drug-related laws, the authority to conduct “covert surveillance” on protesters across the U.S., effectively turning the civilian law enforcement division into a domestic intelligence agency.

The DEA is one of the most tech-savvy government agencies in the federal government, with access to “stingray” cell site simulators to track and locate phones, a secret program that allows the agency access to billions of domestic phone records, and facial recognition technology.

Lawmakers decried the Justice Department’s move to allow the DEA to spy on protesters, calling on the government to “immediately rescind” the order, describing it as “antithetical” to Americans’ right to peacefully assembly.

Powered by WPeMatico

Early-stage founders: Don’t miss your chance to follow in the footsteps of tech giants. We know COVID-19 has created challenges for startup founders, but fear not. Disrupt SF is still proceeding as scheduled, with a Disrupt Digital Pass Virtual option. Launch your startup in the world’s most famous pitch competition, Startup Battlefield. The smackdown goes down live on the Main Stage at Disrupt San Francisco 2020 on September 14-16. Want a shot at $100,000 and the Disrupt Cup? Fill out your application to compete right here.

Companies such as Fitbit, Cloudflare, Mint.com, Dropbox, Vurb, Yammer and Getaround — to name but a few — trace their origins to the Battlefield competition. The Startup Battlefield Alumni Community — 902 companies strong and counting — has collectively raised $9 billion and produced more than 115 successful exits (IPOs or acquisitions). That’s some impressive company to keep. Why not join their ranks?

Here’s how Startup Battlefield works. First, you apply. (Pro tip: Applying and competing in the Battlefield is free and TechCrunch does not take any equity). Next, TechCrunch’s Battlefield-savvy editorial team pours over every application looking for approximately 20 startups to pitch on the Main Stage.

The TechCrunch team will put all participants through rigorous, weeks-long training to hone pitches, business models, presentation skills and any other startup issues that require tightening. You’ll be in fighting trim and ready to step out onto the Main Stage.

Teams have just six minutes to pitch and present a live demo to a panel of expert judges. After each pitch, the judges (we’re talking folks like Cyan Banister, Kirsten Green, Aileen Lee, Alfred Lin and Roelof Botha) will put each team through a Q&A. No flop-sweat here, thanks to all those weeks of pitch coaching.

The judges will select anywhere from four to six teams to advance to the finals. And that means another pitch and Q&A in front of a fresh set of judges. The winning team takes home $100,000, the coveted Disrupt Cup and they bask in a spotlight of media and investor attention. Startup Battlefield can be a life-changing experience for all competitors — not just the ultimate winner.

The action takes place in front of an enthusiastic audience of thousands. Plus, we live-stream the entire event on TechCrunch.com, once you sign up for the digital pass. If all that’s not enough, consider this. Startup Battlefield competitors receive a VIP Disrupt experience.

You’ll have access to private VIP events like the Startup Battlefield Reception, and each team receives four complimentary event tickets. You get to exhibit at the show for all three days, and you’ll have access to CrunchMatch, TC’s investor-founder networking platform. And you also get a complimentary ticket to all future TC events and free subscriptions to Extra Crunch.

Whew. That’s a whole lot of opportunity and exposure. So, what are you waiting for? Disrupt San Francisco 2020 takes place on September 14-16. Apply to compete in Startup Battlefield for a shot at launching your dream to the world.

TechCrunch is mindful of the COVID-19 issue and its impact on live events. You can follow our updates here.

Is your company interested in sponsoring or exhibiting at Disrupt San Francisco 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

There was a lot of moving and shaking in the cybersecurity unicorn world in 2019.

It was a year that saw two of the biggest exits in cybersecurity history: CrowdStrike went public valued at $3.35 billion and Cloudflare rocketed 20% in its first day on the stock market.

Clearly, the cybersecurity market is booming. Recent data suggests that cybersecurity investing could reach $250 billion by 2023, and spending rose in 2019 more than any other industry. If that pace keeps up, there’s little to suggest that the cybersecurity “bubble” will burst any time soon.

A number of cybersecurity companies are firmly in the club of private companies worth $1 billion or more. These unicorns represent some of the best talent, technologies and offerings in cybersecurity, but the club is getting crowded. Now that CrowdStrike and Cloudflare have graduated to the public market, there are a number of cybersecurity companies that could make the leap.

Powered by WPeMatico