canalys

Auto Added by WPeMatico

Auto Added by WPeMatico

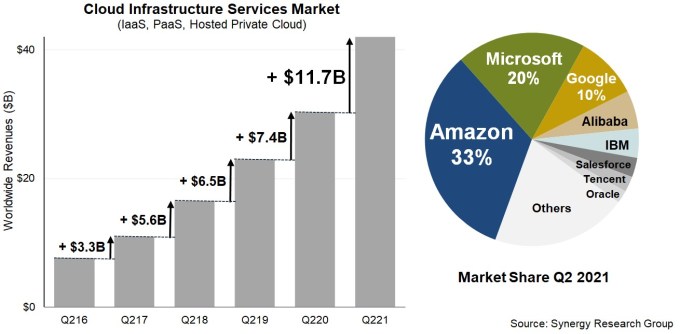

It’s often said in baseball that a prospect has a high ceiling, reflecting the tremendous potential of a young player with plenty of room to get better. The same could be said for the cloud infrastructure market, which just keeps growing, with little sign of slowing down any time soon. The market hit $42 billion in total revenue with all major vendors reporting, up $2 billion from Q1.

Synergy Research reports that the revenue grew at a speedy 39% clip, the fourth consecutive quarter that it has increased. AWS led the way per usual, but Microsoft continued growing at a rapid pace and Google also kept the momentum going.

AWS continues to defy market logic, actually increasing growth by 5% over the previous quarter at 37%, an amazing feat for a company with the market maturity of AWS. That accounted for $14.81 billion in revenue for Amazon’s cloud division, putting it close to a $60 billion run rate, good for a market leading 33% share. While that share has remained fairly steady for a number of years, the revenue continues to grow as the market pie grows ever larger.

Microsoft grew even faster at 51%, and while Microsoft cloud infrastructure data isn’t always easy to nail down, with 20% of market share according to Synergy Research, that puts it at $8.4 billion as it continues to push upward with revenue up from $7.8 billion last quarter.

Google too continued its slow and steady progress under the leadership of Thomas Kurian, leading the growth numbers with a 54% increase in cloud revenue in Q2 on revenue of $4.2 billion, good for 10% market share, the first time Google Cloud has reached double figures in Synergy’s quarterly tracking data. That’s up from $3.5 billion last quarter.

Image Credits: Synergy Research

After the Big 3, Alibaba held steady over Q1 at 6% (but will only report this week), with IBM falling a point from Q1 to 4% as Big Blue continues to struggle in pure infrastructure as it makes the transition to more of a hybrid cloud management player.

John Dinsdale, chief analyst at Synergy, says that the Big 3 are spending big to help fuel this growth. “Amazon, Microsoft and Google in aggregate are typically investing over $25 billion in capex per quarter, much of which is going towards building and equipping their fleet of over 340 hyperscale data centers,” he said in a statement.

Meanwhile, Canalys had similar numbers, but saw the overall market slightly higher at $47 billion. Their market share broke down to Amazon with 31%, Microsoft with 22% and Google with 8% of that total number.

Canalys analyst Blake Murray says that part of the reason companies are shifting workloads to the cloud is to help achieve environmental sustainability goals as the cloud vendors are working toward using more renewable energy to run their massive data centers.

“The best practices and technology utilized by these companies will filter to the rest of the industry, while customers will increasingly use cloud services to relieve some of their environmental responsibilities and meet sustainability goals,” Murray said in a statement.

Regardless of whether companies are moving to the cloud to get out of the data center business or because they hope to piggyback on the sustainability efforts of the Big 3, companies are continuing a steady march to the cloud. With some estimates of worldwide cloud usage at around 25%, the potential for continued growth remains strong, especially with many markets still untapped outside the U.S.

That bodes well for the Big 3 and for other smaller operators who can find a way to tap into slices of market share that add up to big revenue. “There remains a wealth of opportunity for smaller, more focused cloud providers, but it can be hard to look away from the eye-popping numbers coming out of the Big 3,” Dinsdale said.

In fact, it’s hard to see the ceiling for these companies any time in the foreseeable future.

Powered by WPeMatico

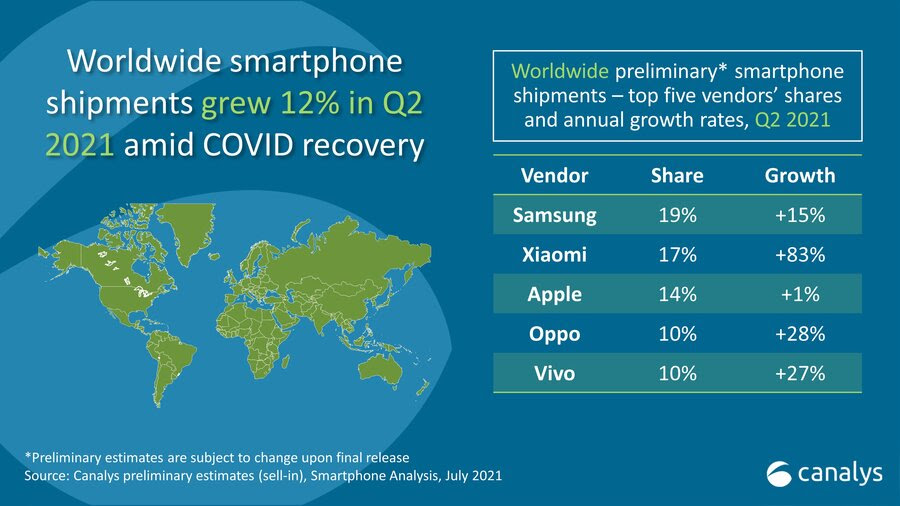

A banner quarter for Xiaomi helped the Chinese mobile company snag the No. 2 spot in global smartphone shipments, according to newly posted Q2 numbers from research firm Canalys. It’s pretty stunning growth for the company, up 83% year-over-year for the quarter and capturing 17% of the global market.

The surge puts Xiaomi at No. 2, globally, behind only Samsung’s 19% by a relatively small margin. Apple is at third with 14% (after its own solid growth has slowed), while fellow Chinese manufacturers Oppo and Vivo round out the top five at 10% a piece.

Huawei, of course, is nowhere to be seen among the top companies. It’s a pretty massive drop, due in no small part to blacklisting that has both barred the company from certain markets (namely, the U.S.) and cut off access to U.S. mobile products, including Google’s Android and various apps.

Image Credits: Canalys

Canalys cites aggressive pricing as a big factor in Xiaomi’s success — particularly contrasted with premium priced offerings from Samsung and Apple.

“It is now transforming its business model from challenger to incumbent, with initiatives such as channel partner consolidation and more careful management of older stock in the open market,” the analyst firm’s Research Manager Ben Stanton said in a release. “It is still largely skewed toward the mass market, however, and compared with Samsung and Apple, its average selling price is around 40% and 75% cheaper respectively. So a major priority for Xiaomi this year is to grow sales of its high-end devices, such as the Mi 11 Ultra.”

The company certainly isn’t a household name in the States (the company has dealt with its own issues here), but of late it has found particular success in Latin America, Africa and Western Europe. It seems that there are still plenty of markets available to continue its expansion as it looks to take on Samsung, even as Oppo and Vivo hope to continue their own respective rapid global growth.

Powered by WPeMatico

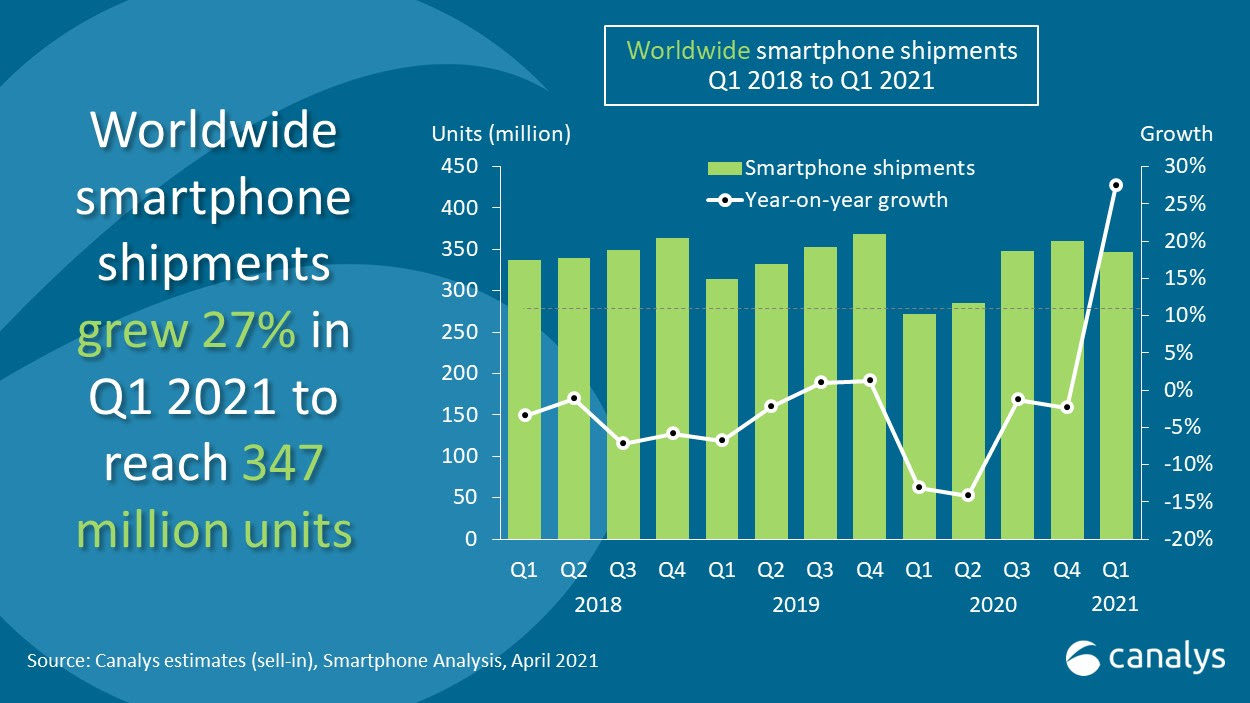

More good news from a smartphone market currently rebounding from the far-reaching impacts of the pandemic. New numbers from Canalys put global shipments for Q1 2021 at 27% above where they were the same time last year.

The industry was hit early and hit hard by COVID-19. The first quarter saw the company running into serious supply chain issues as the pandemic first hit China and parts of Asia where most manufacturing occurs. Following that, demand began to slow, as fewer people were interested in buying mobile devices, coupled with broader economic and job impacts.

Image Credits: Canalys

Samsung continued to lead the way globally, with 76.5 million, up from 59.6 million, representing a 28% jump, year-over-year. In all, the company controls around 22% of global shipments (same as a year prior).

In second place, Apple represented the biggest jump of the quarter, with a 41% increase, from 37.1 million to 52.4 million. That no doubt owes substantially to the big upgrades that arrived toward the end of last year. Huawei’s struggles, meanwhile, have knocked the company out of the top five.

“Xiaomi is in pole position to be the new Huawei,” said Canalys’ Ben Stanton in a release. “Its competitors offer superior channel margin, but Xiaomi’s sheer volume actually gives distributors a better opportunity to make money than rival brands. But the race is not over. Oppo and Vivo are hot on its heels, and are positioning in the mid-range in many regions to box Xiaomi in at the low end.”

The study also notes that LG’s exit from the category should mix things up a bit, as well, particularly in the Americas region, which accounted for 80% of the company’s sales last year.

Powered by WPeMatico

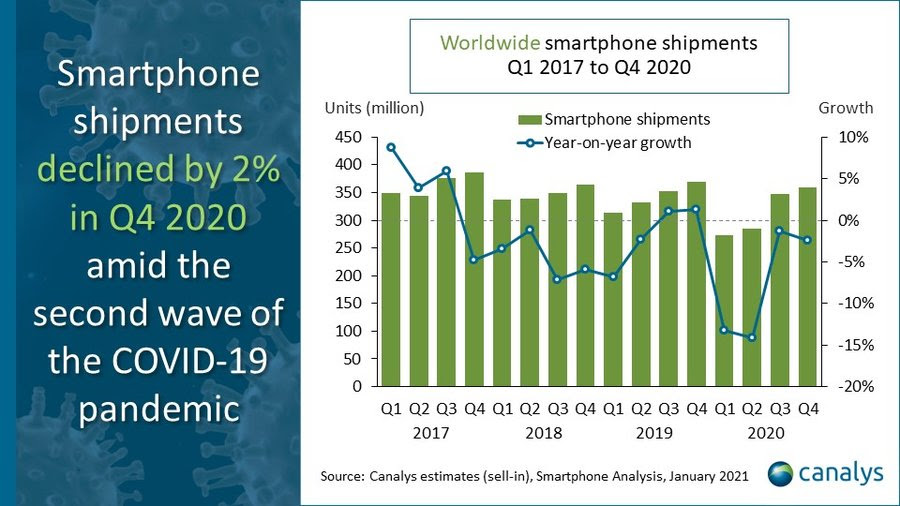

New numbers from Canalys show a slowing in the major smartphone decline we saw for 2020. The past year was, of course, a major blow to an industry already suffering a slide. Hope that the arrival of 5G would right the ship were dashed by Covid-19.

Things are looking up, fueled in large part by a killer quarter for Apple. The company posted its earnings last night, putting much of its success at the feet of the iPhone 12. In spite (or perhaps because) of pandemic-fueled delays, the handset arrived in a perfect storm – the beginnings of a “supercycle” that see customers upgrading devices in a kind of critical mass.

Numbers are still down for the fourth quarter of 2020 – but they’re down by only 2% per the firm. That’s due in no small part to what amounted to the iPhone’s best quarter, as the company introduced four 5G-sporting handsets. Canalys shows a 4% increase for Apple, as the device arrived to a wider 5G rollout just in time for the holiday season.

The company snagged the global number one spot, with Samsung taking number two in spite of a 12% decline. Chinese manufacturers Xiaomi, Oppo and Vivo rounded out the top five, all seeing double digit increases, y-o-y.

Image Credits:

The category is expected to see a rebound this year, after suffering declines due first to supply chain concerns and then larger economic issues, stemming from the pandemic.

“The introduction of COVID-19 vaccines is also boosting business confidence for 2021, allowing them to plan and invest,” analyst Ben Stanton says of the figures. “Going forwards, there will be obvious economic ripple effects as government stimulus fades, and there are ongoing concerns around new virus strains. Overall though, sentiment in the industry is positive, and 2021 will see the smartphone market rebound after a 7% decline in 2020.”

Another report from Canalys notes more positive news for the PC market, showing a 35% y-o-y increase, courtesy of tablet and Chromebook sales.

Powered by WPeMatico

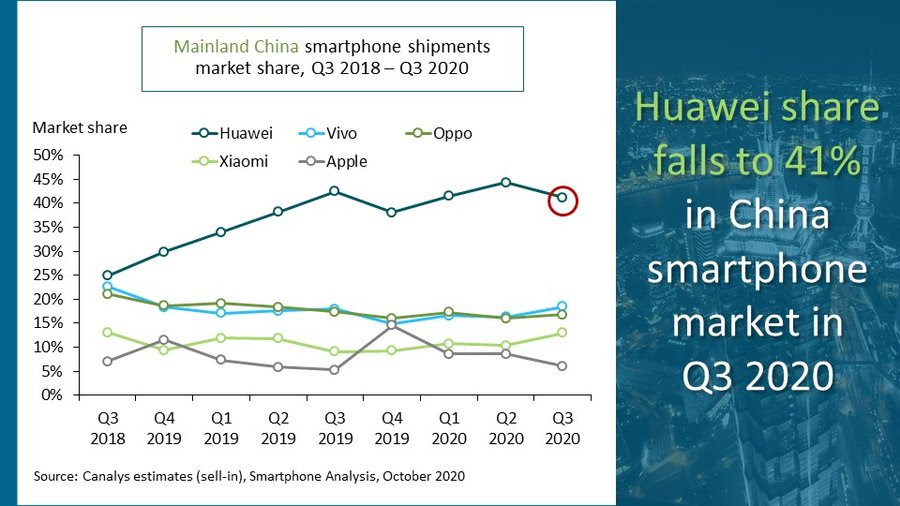

China was the first major global smartphone market to rebound from the early days of the COVID-19 pandemic. Stringent lockdown measures were able to help the country recover from the virus relatively quickly during the first wave, as sales started to return well ahead of other areas.

In Q3, however, things have begun to decline again. New numbers from Canalys point to an 8% drop between quarters — and a 15% drop year-over-year. The firm chalks much of the slowdown to longtime market leader Huawei’s ongoing issues with the U.S. government. The problems had a kind of cascading effect that served to impact the number two companies, Vivo and Oppo.

Image Credits: Canalys

“Huawei was forced to restrict its smartphone shipments following the August 17 US sanctions which caused a void in channels in Q3 that its peers were not equipped to fill. Huawei is facing its most serious challenge since taking the lead in 2016,” analyst Mo Jia said in a release. “If the position of the US administration does not change, Huawei will attempt to pivot its business strategy, to focus on building the [Harmony] OS and software ecosystem, as the Chinese government is eager to nurture home-grown alternatives to global platforms.”

Huawei dropped 18% in Mainland China, year-over-year. Vivo and Oppo posted similar declines at 13% and 18%, respectively. Xiaomi was able to make up ground at third place, gaining 19% y-o-y per the figures. Apple, meanwhile, remained relatively steady, in spite of the delated launch of the iPhone 12. Huawei’s continued struggles could provide a vacuum for the competition to fill.

Analyst Nicole Peng notes that the arrival of the 5G handset put the U.S. company in a strong position, looking forward: “iPhone 12 series will be a game changer for Apple in Mainland China. As most smartphones in China are now 5G-capable, Apple is closing a critical gap, and pent-up demand for its new 5G-enabled family will be strong.”

Powered by WPeMatico

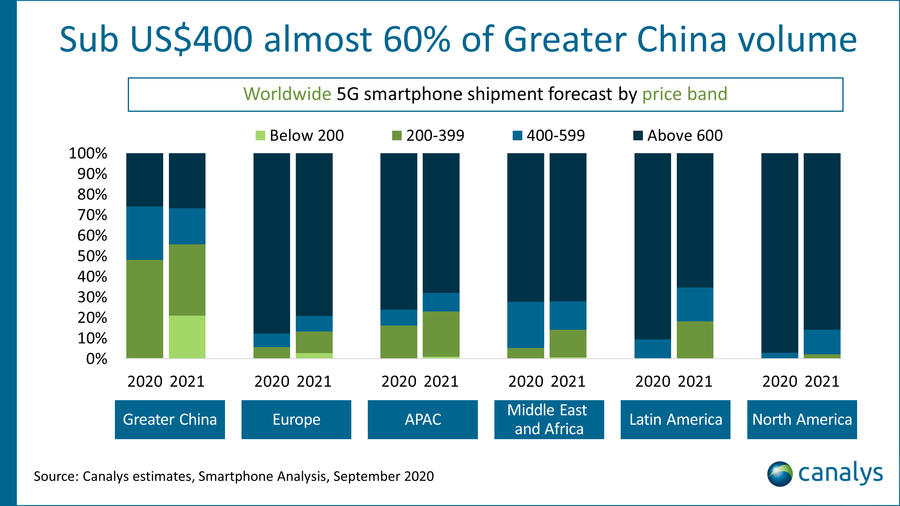

Things have gone from bad to worse for a stumbling smartphone market in 2020. Already plateauing and declining figures have taken a big hit from COVID-19. The pandemic has hampered sales of non-essential items, particularly those best enjoyed outside of the home. According to new figures from Canalys, smartphone shipments are set to experience a 10.7% decline for the year.

There are a couple of silver linings worth noting. For starters, 5G adoption continues to grow. The firm projects that some 280 million units will be shipped in 2020, with the Greater China market making up a majority at 62% of the total figure, thanks in part to lower-cost devices like the Realme V3, which retails for less than $150 U.S. — a remarkable price for a product with next-gen wireless.

Image Credits: Canalys

North America is in second place, with around 15% of shipments, while EMEA and Asia Pacific (sans Greater China) are projected to each make up around 11%. A 5G-enabled iPhone 12 should help speed up adoption as well, when it’s launched in the next month or so.

“Smartphone vendors have relentlessly pushed new product launches, as well as online marketing and sales during the post-lockdown period, generating strong consumer interest for the latest gadgets,” analyst Ben Stanton says in a release. “Gradual reopening of offline stores, improving logistics and production have provided necessary uplift for most markets to move into a more stabilized second half of 2020.”

5G was expected to have a rebounding effect for the industry — though the pandemic quickly hampered those plans. Likely it has gone a ways toward helping prohibit a further slide in sales. And numbers are still expected to rebound somewhat in the 2021, at 9.9% year over year. That’s not quite enough to return things to pre-2020 levels, but would no doubt be a welcome sign for an industry that has shown signs of decline for some time now.

Powered by WPeMatico

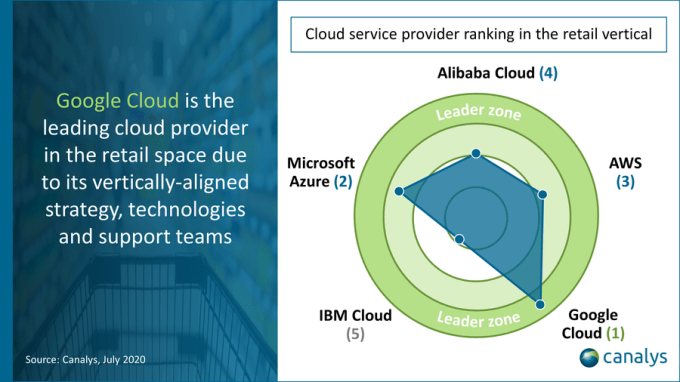

While Google Cloud Platform has shown some momentum in the last year, it remains a distant third behind Amazon and Microsoft in the cloud infrastructure market. But Google got some good news from Canalys today when the firm reported that GCP is the No. 1 cloud platform provider for retailers.

Canalys didn’t provide specific numbers, but it did set overall market positions in the retail sector, with Microsoft coming in second, Amazon third, followed by Alibaba and IBM in fourth and fifth respectively.

Image Credits: Canalys

It’s probably not a coincidence that Google went after retail. Many retailers don’t want to put their cloud presence onto AWS, as Amazon.com competes directly with these retailers. Brent Leary, founder and principal analyst at CRM Essentials, says that as such, the news doesn’t really surprise him.

“Retailers have to compete with Amazon, and I’m guessing the last thing they want to do is use AWS and help Amazon fund all their new initiatives and experiments that in some cases will be used against them,” Leary told TechCrunch. Further, he said that many retailers would also prefer to keep their customer data off of Amazon’s services.

Canalys Senior Director Alex Smith says that this Amazon effect combined with the pandemic and other technological factors has been working in Google’s favor, at least in the retail sector. “Now more than ever, retailers need a digital strategy to win in an omnichannel world, especially with Amazon’s online dominance. Digital is applied everywhere from customer experience to cost optimization, and the overall technological capability of a retailer is what will define its success,” he said.

COVID-19 has forced many retailers to close stores for extended periods of time, and when you combine that with people being more reluctant to go inside stores when they do open, retailers have had to take a crash course in e-commerce if they didn’t have a significant online presence already.

Canalys points out that Google has lured customers with its advertising and search capabilities beyond just pure infrastructure offerings, taking advantage of its other strengths to grow the market segment.

Recognizing this, Google has been making a big retail push, including a big partnership with Salesforce and specific products announced at Google Cloud Next last year. As we wrote at the time of the retail offering:

The company offers eCommerce Hosting, designed specifically for online retailers, and it is offering a special premium program, so retailers get “white glove treatment with technical architecture reviews and peak season operations support…” according to the company. In other words, it wants to help these companies avoid disastrous, money-losing results when a site goes down due to demand.

What’s more, Canalys reports that Google Cloud has also been hiring aggressively and forming partnerships with big systems integrators to help grow the retail business. Retail customers include Home Depot, Kohl’s, Costco and Best Buy.

Powered by WPeMatico

The cloud market is coming into its own during the pandemic as the novel coronavirus forced many companies to accelerate plans to move to the cloud, even while the market was beginning to mature on its own.

This week, the big three cloud infrastructure vendors — Amazon, Microsoft and Google — all reported their earnings, and while the numbers showed that growth was beginning to slow down, revenue continued to increase at an impressive rate, surpassing $30 billion for a quarter for the first time, according to Synergy Research Group numbers.

Powered by WPeMatico

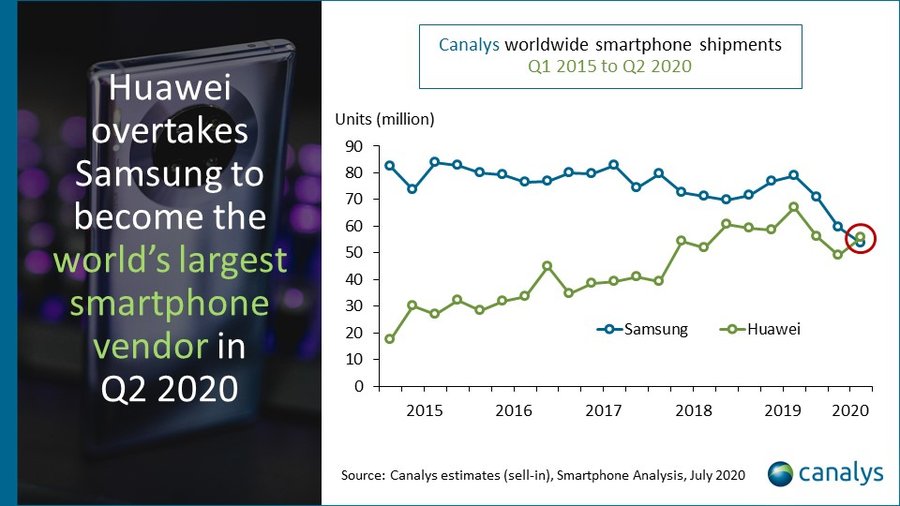

Things haven’t exactly been smooth sailing for Huawei in recent years. The company’s rapid trajectory has been disrupted by on-going battles with the U.S. government that have, among other things, blocked its access to Google apps and services. But a new report from Canalys paints a reasonably rosy picture as the hardware giant overtook Samsung to snag the top spot in global smartphone shipments for the second quarter of 2020.

The news is a milestone for a number of reasons, not the least of which is the fact that this is first time in nine years that neither Apple nor Samsung has been at the top of Canalys’ charts. Huawei’s figures were almost exclusively boosted by sales in its native China, which currently comprises more than 70% of its total figure.

Image Credits: Canalys

It’s important to note here, however, the fact that the company took the top spot by essentially shrinking at a less rapid rate than Samsung. Huawei’s overall figures are down 5% year-over-year. But that figure pales in comparison to Samsung’s 30% drop. The two Goliaths are currently at 55.8 million and 53.7 million, respectively.

Things were bad for the smartphone industry prior to COVID-19, but the pandemic certainly hasn’t helped overall, as people are less inclined toward shelling out hundreds to north of $1,000 for inessential upgrades. And, indeed, Huawei’s numbers dropped by 27% outside of China, but the overall slide was dampened by an 8% growth in China. Samsung, meanwhile, currently controls less than 1% of the Chinese market.

As for what this all means for the future, it seems that it may be difficult for Huawei to maintain its top spot. “Its major channel partners in key regions, such as Europe, are increasingly wary of ranging Huawei devices, taking on fewer models, and bringing in new brands to reduce risk” Canalys’ Mo Jia said of the report. “Strength in China alone will not be enough to sustain Huawei at the top once the global economy starts to recover.”

Powered by WPeMatico

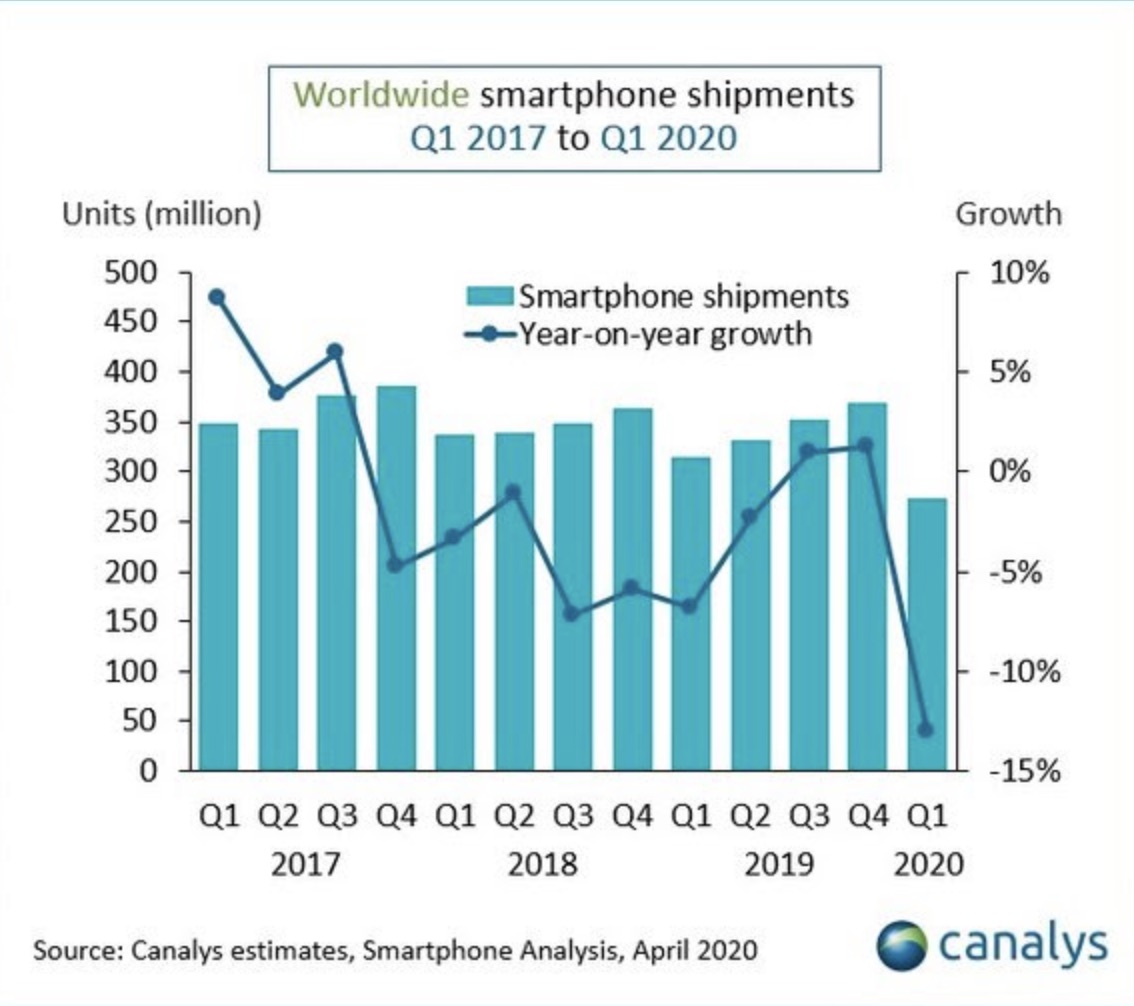

We knew it was going to be bad — but not necessarily “lowest level since 2013” bad. As Apple was busy reporting its earnings, Canalys just dropped some of its own figures — and they’re not pretty. After two quarters of much-needed growing, the global smartphone market just took a big hit. And you no doubt already know who the culprit is.

The mobile industry joins countless others that have taken a massive hit due to the COVID-19 pandemic, with shipments dropping 13% from this time last year. Here’s a graph for those of you who are visual learners:

Analyst Ben Stanton used the word “crushed” to describe the novel coronavirus’s impact on the mobile market. “In February, when the coronavirus was centered on China, vendors were mainly concerned about how to build enough smartphones to meet global demand,” he writes. “But in March, the situation flipped on its head. Smartphone manufacturing has now recovered, but as half the world entered lockdown, sales plummeted.”

First it was impact on the global supply chain, which is centered in Asia, along with a drop in demand among consumers in China. As Europe, the U.S. and other locations continue to live under shelter in place orders, demand in those markets has taken a significant hit. People are stuck inside and many have lost jobs — it’s not really the ideal time to consider shelling out $1,000+ for what still seems a luxury for many.

Samsung regained the top spot, while still losing significant numbers. Both it and the number two company, Huawei, were down 17% for the quarter. Apple, at number three, dropped 8%. Chinese manufacturers Xiaomi and Vivo saw some gains, at 9% and 3%, respectively.

There are bound to be rough times ahead as well. Per Stanton, “Most smartphone companies expect Q2 to represent the peak of the coronavirus’ impact.” Apple noted the uncertainty of its own earnings by opting not to issue guidance for next quarter.

Powered by WPeMatico