canalys

Auto Added by WPeMatico

Auto Added by WPeMatico

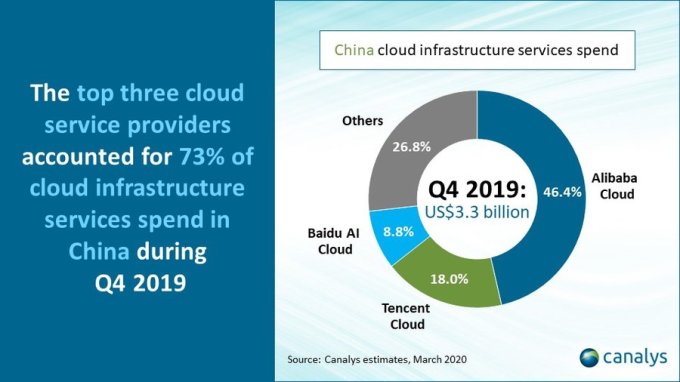

Research firm Canalys reports that the Chinese cloud infrastructure market grew 66.9% to $3.3 billion in the last quarter of 2019, right before the COVID-19 virus hit the country. China is the second largest cloud infrastructure market in the world, with 10.8% share.

The quarter puts the Chinese market on a $13.2 billion run rate. Canalys pegged the U.S. market at $14 billion for the same time period, with a 47% worldwide market share.

Alibaba led the way in China, with more than 46% market share. Like its American e-commerce giant counterpart, Amazon, Alibaba has a cloud arm, and it dominates in its country much the same way AWS does in the U.S.

Tencent was in second, with 18%, roughly the equivalent of Microsoft Azure’s share in the U.S., and Baidu AI Cloud came in third, with 8.8%, roughly the equivalent of Google’s U.S. market share.

Slide: Canalys

Matthew Ball, an analyst at Canalys, says the fourth quarter numbers predate the medical crisis due to the COVID-19 outbreak in China. “In terms of growth drivers for Q4, we have seen the ongoing demand for on-demand compute and storage accelerate throughout 2019, as private and public organizations embark on digital transformation projects and start building platforms and applications to develop new services.”

Ball says gaming was a big cloud customer, as was healthcare, finance, transport and industry. He also pointed to growth in facial recognition technology as part of the smart city sector.

As for next year, Ball says the firm still sees big growth in the market despite the virus impact in Q12020. “In addition to the continuation of digital projects once business returns to normality, we anticipate many businesses new to using cloud services during the crisis will continue use and become paying customers,” he said. The cloud companies have been offering a number of free options to businesses during the crisis.

“The overall outcome of current events around the world will be that companies will assess their business continuity measures and make sure they can continue to operate if events are ever repeated,” he said.

Powered by WPeMatico

We all know the cloud infrastructure market is extremely lucrative; analyst firm Canalys reports that the sector reached $30.2 billion in revenue for Q4 2019.

Cloud numbers are hard to parse because companies often lump cloud revenue into a single bucket regardless of whether it’s generated by infrastructure or software. What’s interesting about Canalys’s numbers is that it attempts to measure the pure infrastructure results themselves without other cloud incomes mixed in:

As an example, Microsoft reported $12.5 billion in total combined cloud revenue for the quarter, but Canalys estimates that just $5.3 billion comes from infrastructure (Azure). Amazon has the purest number with $9.8 billion of a reported $9.95 billion attributed to its infrastructure business. This helps you understand why in spite of the fact that Microsoft reported bigger overall cloud earnings numbers and a higher growth rate, Amazon still has just less than double Microsoft’s market share in terms of IaaS spend.

That’s not to say Microsoft didn’t still have a good quarter — it garnered 17.6% of revenue for the period. That’s up from 14.5% in the same quarter a year ago. What’s more, Amazon lost a bit of ground, according to Canalys, dropping from 33.4% in Q4 2018 to 32.4% in the most recent quarter.

Part of the reason for that is because Microsoft is growing at close to twice the rate as Amazon — 62.3% versus Amazon’s 33.2%.

Meanwhile, number-three vendor Google came in at $1.8 billion for pure infrastructure revenue, good for 6% of the market, up from 4.9% a year ago on growth rate 67.6%. Google reported $2.61 billion in overall cloud revenue, but that included software. Despite the smaller results, it was a good quarter for the Mountain View-based company.

Powered by WPeMatico

In some corners, the smartphone market is showing its first signs of life in some time.

Recent figures from Canalys indicate a small but notable uptick in the European market as shipments grew 3%, year-over-year in Q3.

The analyst firm put global growth at 1% globally in another recent report. Generally, such numbers wouldn’t warrant much celebration, but the way the market has been going, most manufacturers will take what they can get.

New numbers out this morning from Gartner paint a less rosy picture, with sales numbers declining 0.4%. It’s not a huge discrepancy between shipping and sales figures, but it’s the difference between being in the red and being in the black for the quarter.

Powered by WPeMatico

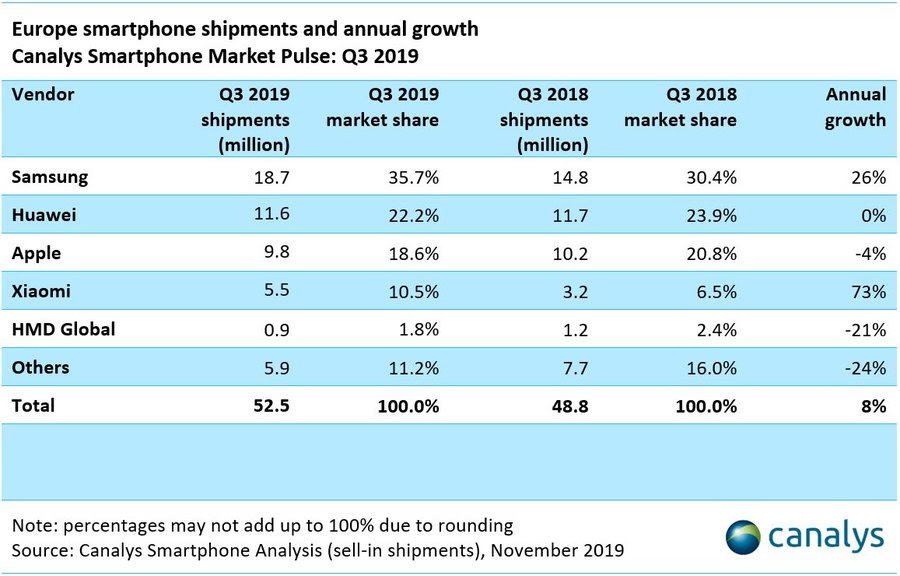

Europe bucked global smartphone stagnation in the third quarter, marking an 8% year over year growth in device shipments. That number, provided by Canalys, puts the region at the top of smartphone growth figures, beating out Asia/Pacific’s six percent.

Once again, Samsung was the biggest winner here. The Korean manufacturer saw a healthy 26%, year over year growth. As noted back in Q2, Samsung’s growth comes as the company floods the market with a variety of different devices. Its mid-tier A Series accounted for all four of its top spots during that time period.

Huawei held steady in second place, as the company refocuses on Europe amid US/China trade tensions. Huawei accounted for 22.2 % of units shipped, versus Samsung’s 35.7%. Fellow Chinese manufacturer Xiaomi saw an extremely healthy boost for the quarter, jumping 73 percent for the year, to nab fourth place behind Apple.

While the numbers are positive in the face of larger negative trends, politics are still having a marked impact on figures.

“On the negative side, Brexit has already had an impact,” analyst Ben Stanton said in a release. “In the UK, shipments of premium devices from Samsung and Apple accelerated before each Brexit deadline this year, in March and recently October, followed by a large dip, as distributors were forced to stockpile product and hedge against impending tariff risk. This shot-term artificial boost distorts the market and the accompanying risk, costs and uncertainty, is a drain on the industry.”

Like much of the rest of the world, the European market is looking forward to a 5G rollout to help further juice shipments moving forward.

Powered by WPeMatico

All is not lost for smartphone manufacturers. On the heels of two years’ of global stagnation, the category is finally showing some signs of life. Much of the bounce back comes as manufacturers are working to correct for dulled consumer interest.

I wouldn’t put too much weight in the numbers right now, as they’re little more than an uptick. Numbers from Canalys put shipment growth at 1% from Q3 2018 to Q3 2019. In most cases, that would be a modest gain, at best, but this is notably the first time in two years that the numbers have been heading in the right direction.

Samsung saw the biggest gains — a phenomenon the analyst firm chalks up to a shift in strategy to eat some of its profits. The move has paid off for the quarter, with an 11% growth in device shipments, to 78.9 million devices shipped. That gives the company the largest global market share, at 22.4%.

Huawei, too, saw impressive growth, year-over-year, commanding second place with 66.8 million units shipped. Much of its growth came from China, which has ramped up spending on the company’s products as it has run into regulatory scrutiny overseas. Resumption of sales in some international markets helped juice growth as well. Of the top three, Apple continued to struggle the most, with a 7% loss from 2018.

For now, at least, none of the these numbers qualify as full turnaround for a stagnant category, though the upcoming roll out of 5G coverage could help move numbers in the right direction in the coming year.

Powered by WPeMatico

The media has largely bought into Huawei’s “strong” half-year results today, but there’s a major catch in the report: the company’s quarter-by-quarter smartphone growth was zero.

The telecom equipment and smartphone giant announced on Tuesday that its revenue grew 23.2% to reach 401.3 billion yuan ($58.31 million) in the first half of 2019 despite all the trade restrictions the U.S. slapped on it. Huawei’s smartphone shipments recorded 118 million units in H1, up 24% year-over-year.

What about quarterly growth? Huawei didn’t say, but some quick math can uncover what it’s hiding. The company clocked a strong 39% in revenue growth in the first quarter, implying that its overall H1 momentum was dragged down by Q2 performance.

Huawei said its H1 revenue is up 23.2% year-on-year — but when you consider that Q1 revenue rose by 39%, Q2 must have been a real struggle…https://t.co/dFQo4gxEVbhttps://t.co/HABAQ6fmfK

— Jon Russell (@jonrussell) July 30, 2019

The firm shipped 59 million smartphones in the first quarter, which means the figure was also 59 million units in the second quarter. As tech journalist Alex Barredo pointed out in a tweet, Huawei’s Q2 smartphone shipments were historically stronger than Q1.

Huawei smartphones Q2 sales were traditionally much more stronger than on Q1 (32.5% more on average).

This year after Trump’s veto it is 0%. That’s quite the effect pic.twitter.com/x3dQlOePDA

— Alex B

(@somospostpc) July 30, 2019

And although Huawei sold more handset units in China during Q2 (37.3 million) than Q1 (29.9 million) according to data from market research firm Canalys, the domestic increase was apparently not large enough to offset the decline in international markets. Indeed, Huawei’s founder and chief executive Ren Zhengfei himself predicted in June that the company’s overseas smartphone shipments would drop as much as 40%.

The causes are multi-layered, as the Chinese tech firm has been forced to extract a raft of core technologies developed by its American partners. Google stopped providing to Huawei certain portions of Android services, such as software updates, in compliance with U.S. trade rules. Chip designer ARM also severed business ties with Huawei. To mitigate the effect of trade bans, Huawei said it’s developing its own operating system (although it later claimed the OS is primarily for industrial use) and core chips, but these backup promises may take some time to materialize.

Consumer products are just one slice of the behemoth’s business. Huawei’s enterprise segment is under attack, too, as small-town U.S. carriers look to cut ties with Huawei. The Trump administration has also been lobbying its western allies to stop purchasing Huawei’s 5G networking equipment.

In other words, being on the U.S.’s entity list — a ban that prevents American companies from doing business with Huawei — is putting a real squeeze on the Chinese firm. Washington has given Huawei a reprieve that allows American entities to resume buying from and selling to Huawei, but the damage has been done. Ren said last month that all told, the U.S. ban would cost his company a staggering $30 billion loss in revenue.

Huawei chairman Liang Hua (pictured above) acknowledged the firm faces “difficulties ahead” but said the company is “fully confident in what the future holds,” he said today in a statement. “We will continue investing as planned – including a total of CNY120 billion in R&D this year. We’ll get through these challenges, and we’re confident that Huawei will enter a new stage of growth after the worst of this is behind us.”

Powered by WPeMatico

When Microsoft reported its FY19, Q4 earnings last week, the numbers were mostly positive, but as we pointed out, Azure earnings growth has stalled. Productivity and business, which includes Office 365, has also mostly flattened out. But slowing growth is not always as bad as it may seem. In fact, it’s an inevitability that once you start to reach Microsoft’s market maturity, it gets harder to maintain large growth numbers.

That said, AWS launched the first cloud infrastructure service, Amazon Elastic Compute Cloud in August, 2006. Microsoft came much later to the cloud, launching Azure in February, 2010, but so were other established companies in Microsoft’s market share rearview. What did it do differently to achieve this success that the companies chasing it — Google, IBM and Oracle — failed to do? It’s a key question.

For starters, let’s look at the most numbers for Productivity & Business Processes this year. This category includes all of its commercial and consumer SaaS products including Office 365 commercial and consumer, Dynamics 365, LinkedIn and others. The percentage growth started FY19 at 19% but ended at 14%

When you look at just Office365 commercial earnings growth, it started at 36% and dropped down to 31% by Q4.

Powered by WPeMatico

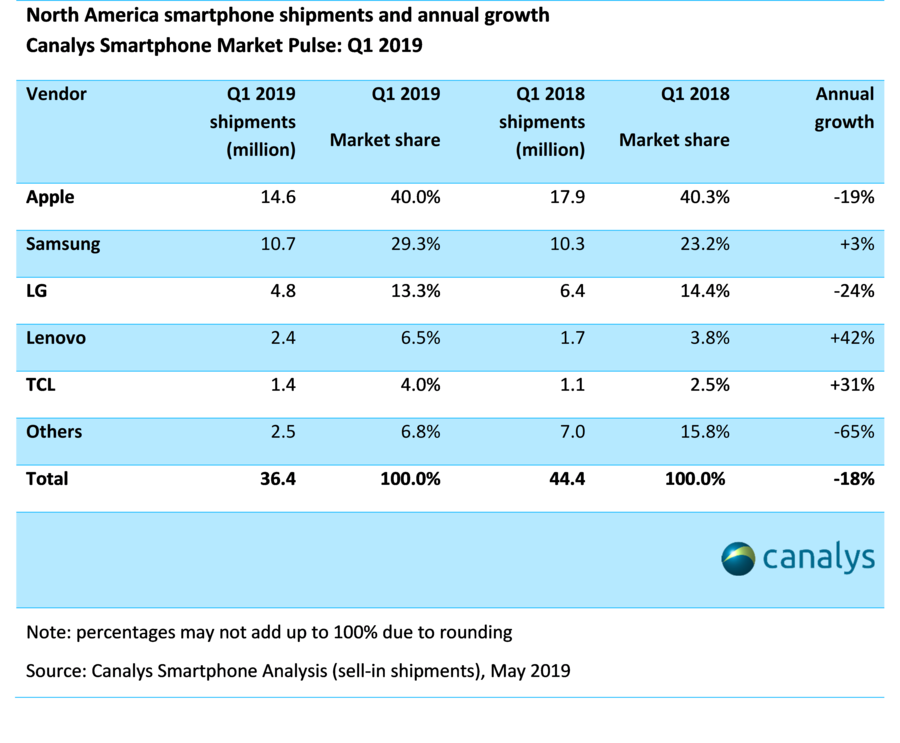

More dismal news from the smartphone number crunchers. New figures out of Canalys put the North American smartphone market at five-year low for the first quarter of 2019. That’s…bad. But also, pretty inline with what we’ve been seeing globally. The market has stagnated, and while manufacturers aren’t in full-on panic mode, there’s certainly cause for concern.

Shipments dropped from 44.4 million down to 36.4 million, marking an 18% drop year over year for the first quarter. Canalys says it’s the steepest drop it’s recorded for the category, chalking up some of the issues to “a lackluster performance by Apple and the absence of ZTE.”

Apple is still the top of the heap, commanding 40% of the North American market with help from the sale of older discounted units. But Samsung managed to tighten the gap on the back of a successful Galaxy S10 launch. The company grew by 3% for the year, up to 29.3% of the market.

Apple is still the top of the heap, commanding 40% of the North American market with help from the sale of older discounted units. But Samsung managed to tighten the gap on the back of a successful Galaxy S10 launch. The company grew by 3% for the year, up to 29.3% of the market.

LG, Lenovo and TCL rounded out the top five, with the latter two making pretty solid market-share strides. The remainder of the market took a massive hit, however, with a 65% drop in shipments. Analysts seem confident that 5G’s imminent arrival will help give the market a boost in coming quarters, but it’s going to be hard for manufacturers to maintain that momentum.

Powered by WPeMatico

The smartphone industry is in rough shape. Sundar Pichai used the word “headwinds” to discuss the company’s difficulties moving Pixel 3 units, but Canalys’ latest report is far more blunt, describing the situation as a “freefall.”

Things are pretty ugly in the Q1 report, as smartphone shipments declined for the sixth quarter in a row. The combined global units hit 313.9 million, marking their lowest point in almost half a decade, according to the firm.

Of the big players, Apple seems to be particularly hard hit, falling 23.2% year on year. Once again, China played a big role here, but as usual, the full story is much more complex.

“This is the largest single-quarter decline in the history of the iPhone,” said analyst Ben Stanton in a release tied to the news. “Apple’s second largest market, China, again proved tough. But this was far from its only problem. Shipments fell in the US as trade-in initiatives failed to offset longer consumer refresh cycles. In markets such as Europe, Apple is increasingly using discounts to prop up demand, but this is causing additional complexity for distributors, and blurring the value proposition of these ‘premium’ devices in the eyes of consumers.”

A lot to unpack there, but what we’re looking at are some larger issues within the industry, including global economic issues and slowed upgrade cycles for users. The XS was also notably much less dramatic of an upgrade than its predecessor. Stanton did add that the iPhone, “show[ed] signs of recovery towards the back-end of the quarter,” which is promising for Q2.

A lot to unpack there, but what we’re looking at are some larger issues within the industry, including global economic issues and slowed upgrade cycles for users. The XS was also notably much less dramatic of an upgrade than its predecessor. Stanton did add that the iPhone, “show[ed] signs of recovery towards the back-end of the quarter,” which is promising for Q2.

It also remains to be seen what this year will hold in terms of iPhone upgrades, though most signs point to 2020 as the year the company makes the jump to 5G. Tim Cook was noncommittal on the topic during the company’s earnings call last night, instead pointing to positive numbers on the iPad side and, of course, Apple’s continued push into services.

Analysts are somewhat bullish about the potential of innovations like 5G and even foldables in shaking up the stagnant market, but big players like Apple are clearly hedging their bets, should the free-falling headwinds continue.

Huawei, meanwhile, continues to be a bright spot, with a 50.2% year over year growth and an 18.8% global market share, according to the firm. That growth could be hampered, however, by increased competition from Samsung and fellow Chinese handset companies like Xiaomi and Oppo.

Powered by WPeMatico

When it comes to the cloud market, there are few known knowns. For instance, we know that AWS is the market leader with around 32 percent of market share. We know Microsoft is far back in second place with around 14 percent, the only other company in double digits. We also know that IBM and Google are wallowing in third or fourth place, depending on whose numbers you look at, stuck in single digits. The market keeps expanding, but these two major companies never seem to get a much bigger piece of the pie.

Neither company is satisfied with that, of course. Google so much so that it moved on from Diane Greene at the end of last year, bringing in Oracle veteran Thomas Kurian to lead the division out of the doldrums. Meanwhile, IBM made an even bigger splash, plucking Red Hat from the market for $34 billion in October.

This week, the two companies made some more noise, letting the cloud market know that they are not ceding the market to anyone. For IBM, which is holding its big IBM Think conference this week in San Francisco, it involved opening up Watson to competitor clouds. For a company like IBM, this was a huge move, akin to when Microsoft started building apps for iOS. It was an acknowledgement that working across platforms matters, and that if you want to gain market share, you had better start thinking outside the box.

While becoming cross-platform compatible isn’t exactly a radical notion in general, it most certainly is for a company like IBM, which if it had its druthers and a bit more market share, would probably have been content to maintain the status quo. But if the majority of your customers are pursuing a multi-cloud strategy, it might be a good idea for you to jump on the bandwagon — and that’s precisely what IBM has done by opening up access to Watson across clouds in this fashion.

Clearly buying Red Hat was about a hybrid cloud play, and if IBM is serious about that approach, and for $34 billion, it had better be — it would have to walk the walk, not just talk the talk. As IBM Watson CTO and chief architect Ruchir Puri told my colleague Frederic Lardinois about the move, “It’s in these hybrid environments, they’ve got multiple cloud implementations, they have data in their private cloud as well. They have been struggling because the providers of AI have been trying to lock them into a particular implementation that is not suitable to this hybrid cloud environment.” This plays right into the Red Hat strategy, and I’m betting you’ll see more of this approach in other parts of the product line from IBM this year. (Google also acknowledged this when it announced a hybrid strategy of its own last year.)

Meanwhile, Thomas Kurian had his coming-out party at the Goldman Sachs Technology and Internet Conference in San Francisco earlier today. Bloomberg reports that he announced a plan to increase the number of salespeople and train them to understand specific verticals, ripping a page straight from the playbook of his former employer, Oracle.

He suggested that his company would be more aggressive in pursuing traditional enterprise customers, although I’m sure his predecessor, Diane Greene, wasn’t exactly sitting around counting on inbound marketing interest to grow sales. In fact, rumor had it that she wanted to pursue government contracts much more aggressively than the company was willing to do. Now it’s up to Kurian to grow sales. Of course, given that Google doesn’t report cloud revenue it’s hard to know what growth would look like, but perhaps if it has more success it will be more forthcoming.

As Bloomberg’s Shira Ovide tweeted today, it’s one thing to turn to the tried and true enterprise playbook, but that doesn’t mean that executing on that approach is going to be simple, or that Google will be successful in the end.

To be honest, all of these suggestions for broadening Google Cloud are from the obvious enterprise sales playbook, but it doesn’t mean they are easy.

— Shira Ovide (@ShiraOvide) February 12, 2019

These two companies obviously desperately want to alter their cloud fortunes, which have been fairly dismal to this point. The moves announced today are clearly part of a broader strategy to move the market share needle, but whether they can or the market positions have long ago hardened remains to be seen.

Powered by WPeMatico