boston

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today, the last day of 2019, we’re taking a second look at Boston. Regular readers of this column will recall that we recently took a peek at Boston’s startup ecosystem, and that we compiled a short countdown of the largest rounds that took place this year in Utah. Today we’re doing the latter with the former.

What follows is a countdown of Boston’s seven largest venture rounds from the year, including details concerning what the company does and who backed it. We’re also taking a shot after each entry at where we think the companies are on the path to going public.

As before, we’re using Crunchbase data for this project (here). And we’re only looking at venture rounds, so no post-IPO action, no grants, no secondaries, no debt, and no private equity-style buyouts.

Ready? Let’s have some fun.

Boston has produced a number of big exits in recent years, like Carbon Black’s IPO, DraftKings’ impending kinda-IPO, Cayan’s billion-dollar exit, and SimpliVity’s huge sale to HP. Despite that, however, Boston is often pigeon-holed as a biotech hotbed with little technology that folks from San Francisco can understand. That’s not really fair, it turns out. There’s plenty of SaaS in Boston.

As you read the list, keep tabs on what percent of the companies included you were already familiar with. These are startups that will to take up more and more media attention as they march towards the public markets. It’s better to know them now than later.

Following the pattern set with Utah, we’ll start at the smallest round of our group and then count up to the largest.

We could actually call the Motif FoodWorks‘ Series A a $117.5 million round as it came in two parts. However, the first tranche was $90 million total and landed in 2019 so that’s our selection for the uses of this post. The company is backed by Fonterra Ventures, Louis Dreyfus Corp, and General Atlantic.

Motif works in the alternative food space, creating things like fake meat and alt-dairy. Given the meteoric rise of Beyond Meat and Impossible Food’s big year, the space is hot. Lots of folks want to eat less meat for ethical or ecological reasons (often the two intertwine). That demand is powering a number of companies forward. Motif is riding a powerful wave.

The company’s known raised capital is encompassed in a large, early-stage round. That means that we won’t see an S-1 from this company for a long, long time.

An email marketing and analytics company, Klaviyo gets point for having a pricing page that actually makes sense — a rarity in the enterprise software world.

The Boston-based company was founded in 2012 and, according to Crunchbase data, has raised a total of $158.5 million. It raised just $8.5 million in total (across a small Seed round and a modest Series A) before its mega-round. How did it manage to raise such an enormous infusion in one go? As TechCrunch reported when the round was announced in April of this year:

The company is growing in leaps and bounds. It currently has 12,000 customers. To put that into perspective, it had just 1,000 at the end of 2016 and 5,000 at the end of 2017.

That will get the attention of anyone with a checkbook. The Summit Partners and Astral Capital-backed company has huge capital reserves for what we presume is the first time in its life. That means it’s not going public any time soon, even if our back-of-the-napkin math puts it comfortably over the $100 million ARR mark (warning: estimates were used in the creation of that number).

ezCater is an online catering marketplace. That’s an attractive business, it turns out, as evinced by the Boston company’s funding history. The startup has raised over $300 million to date according to Crunchbase, including capital from Insight Partners, ICONIQ Capital, Wellington Management, GIC, and Lightspeed.

The company’s 2019 $150 million Series D-1 that valued the company at $1.25 billion wasn’t its only nine-figure round; ezCater’s 2018 Series D was also over the mark, weighing in at $100 million.

When might the Northeast unicorn go public? An interview earlier this year put 2021 on the map as a target for the startup. That’s ages away from now, sadly, as I’d love to know how the company’s gross margin have changed since it started raising venture capital in huge gulps.

Cybereason competes with CrowdStrike. That’s a good space to play in as CrowStrike went public earlier this year, and it went pretty well. That fact makes the Boston’s endpoint security shop’s $200 million investment pretty easy to understand. Indeed, CrowdStrike went public to great effect in June of 2019; Cybereason announced its huge round two months later in August. Surprise.

As far as backing goes, Cybereason has friends at SoftBank, with the Japanese conglomerate leading its Series C, D, and E rounds. Prior leads include CRV and Spark Capital.

The market is hot for SaaS-y security companies, meaning that there is natural pressure on Cybereason to go public. The firm, worth a flat $1.0 billion post-money after its latest round, is therefore an obvious IPO candidate for 2020. If it has the guts, that is. With SoftBank in your corner, there’s probably always another $100 million lying around you can snap up to avoid filing. (More from CrowdStrike’s CEO coming later this week on the 2019 and 2020 IPO markets, by the way. Stay tuned.)

DataRobot does enterprise AI, allowing companies to use computer intelligence to help their flesh-and-blood staffers do more, more quickly. That’s the gist I got from learning what I could this morning, but as with all things AI I cannot tell you what’s real and what’s not.

Given its investor list, though, I’d bet that DataRobot is onto something. New Enterprise Associates led its 2014, 2016, and 2017 Series A, B, and C rounds. Meritech and Sapphire took over at the Series D, with Sapphire heroing DataRobot’s $206 million Series E. That round creatively valued the firm at, you guessed it, $1.0 billion according to Crunchbase.

DataRobot is hiring like mad (343 open positions as of this morning) and buying other companies (three in 2019). Flush with its largest round ever, I don’t see the company in a hurry to go public. That means no 2020 debut unless it’s monetizing faster than expected.

Powered by WPeMatico

Venture capital investment exploded across a number of geographies in 2019 despite the constant threat of an economic downturn.

San Francisco, of course, remains the startup epicenter of the world, shutting out all other geographies when it comes to capital invested. Still, other regions continue to grow, raking in more capital this year than ever.

In Utah, a new hotbed for startups, companies like Weave, Divvy and MX Technology raised a collective $370 million from private market investors. In the Northeast, New York City experienced record-breaking deal volume with median deal sizes climbing steadily. Boston is closing out the decade with at least 10 deals larger than $100 million announced this year alone. And in the lovely Pacific Northwest, home to tech heavyweights Amazon and Microsoft, Seattle is experiencing an uptick in VC interest in what could be a sign the town is finally reaching its full potential.

Seattle startups raised a total of $3.5 billion in VC funding across roughly 375 deals this year, according to data collected by PitchBook. That’s up from $3 billion in 2018 across 346 deals and a meager $1.7 billion in 2017 across 348 deals. Much of Seattle’s recent growth can be attributed to a few fast-growing businesses.

Convoy, the digital freight network that connects truckers with shippers, closed a $400 million round last month bringing its valuation to $2.75 billion. The deal was remarkable for a number of reasons. Firstly, it was the largest venture round for a Seattle-based company in a decade, PitchBook claims. And it pushed Convoy to the top of the list of the most valuable companies in the city, surpassing OfferUp, which raised a sizable Series D in 2018 at a $1.4 billion valuation.

Convoy has managed to attract a slew of high-profile investors, including Amazon’s Jeff Bezos, Salesforce CEO Marc Benioff and even U2’s Bono and the Edge. Since it was founded in 2015, the business has raised a total of more than $668 million.

Remitly, another Seattle-headquartered business, has helped bolster Seattle’s startup ecosystem. The fintech company focused on international money transfer raised a $135 million Series E led by Generation Investment Management, and $85 million in debt from Barclays, Bridge Bank, Goldman Sachs and Silicon Valley Bank earlier this year. Owl Rock Capital, Princeville Global, Prudential Financial, Schroder & Co Bank AG and Top Tier Capital Partners, and previous investors DN Capital, Naspers’ PayU and Stripes Group also participated in the equity round, which valued Remitly at nearly $1 billion.

Up-and-coming startups, including co-working space provider The Riveter, real estate business Modus and same-day delivery service Dolly, have recently attracted investment too.

A number of other factors have contributed to Seattle’s long-awaited rise in venture activity. Top-performing companies like Stripe, Airbnb and Dropbox have established engineering offices in Seattle, as has Uber, Twitter, Facebook, Disney and many others. This, of course, has attracted copious engineers, a key ingredient to building a successful tech hub. Plus, the pipeline of engineers provided by the nearby University of Washington (shout-out to my alma mater) means there’s no shortage of brainiacs.

There’s long been plenty of smart people in Seattle, mostly working at Microsoft and Amazon, however. The issue has been a shortage of entrepreneurs, or those willing to exit a well-paying gig in favor of a risky venture. Fortunately for Seattle venture capitalists, new efforts have been made to entice corporate workers to the startup universe. Pioneer Square Labs, which I profiled earlier this year, is a prime example of this movement. On a mission to champion Seattle’s unique entrepreneurial DNA, Pioneer Square Labs cropped up in 2015 to create, launch and fund technology companies headquartered in the Pacific Northwest.

Boundless CEO Xiao Wang at TechCrunch Disrupt 2017

Operating under the startup studio model, PSL’s team of former founders and venture capitalists, including Rover and Mighty AI founder Greg Gottesman, collaborate to craft and incubate startup ideas, then recruit a founding CEO from their network of entrepreneurs to lead the business. Seattle is home to two of the most valuable businesses in the world, but it has not created as many founders as anticipated. PSL hopes that by removing some of the risk, it can encourage prospective founders, like Boundless CEO Xiao Wang, a former senior product manager at Amazon, to build.

“The studio model lends itself really well to people who are 99% there, thinking ‘damn, I want to start a company,’ ” PSL co-founder Ben Gilbert said in March. “These are people that are incredible entrepreneurs but if not for the studio as a catalyst, they may not have [left].”

Boundless is one of several successful PSL spin-outs. The business, which helps families navigate the convoluted green card process, raised a $7.8 million Series A led by Foundry Group earlier this year, with participation from existing investors Trilogy Equity Partners, PSL, Two Sigma Ventures and Founders’ Co-Op.

Years-old institutional funds like Seattle’s Madrona Venture Group have done their part to bolster the Seattle startup community too. Madrona raised a $100 million Acceleration Fund earlier this year, and although it plans to look beyond its backyard for its newest deals, the firm continues to be one of the largest supporters of Pacific Northwest upstarts. Founded in 1995, Madrona’s portfolio includes Amazon, Mighty AI, UiPath, Branch and more.

Voyager Capital, another Seattle-based VC, also raised another $100 million this year to invest in the PNW. Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, closed on another $180 million to invest in early-stage consumer startups in May. And new efforts like Flying Fish Partners have been busy deploying capital to promising local companies.

There’s a lot more to say about all this. Like the growing role of deep-pocketed angel investors in Seattle have in expanding the startup ecosystem, or the non-local investors, like Silicon Valley’s best, who’ve funneled cash into Seattle’s talent. In short, Seattle deal activity is finally climbing thanks to top talent, new accelerator models and several refueled venture funds. Now we wait to see how the Seattle startup community leverages this growth period and what startups emerge on top.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today, we’re digging into a host of data concerning the East Coast venture capital scene, specifically looking into the performance of its two key startup markets.

It’s 12 degrees Fahrenheit as I write this in my office situated between Boston and New York City — a perfect vantage point for studying these vibrant tech ecosystems. Let’s see what the data tells us.

The information we’re examining today comes from White Star Capital (often via CBInsights), a venture capital firm that describes itself as “transatlantic” and takes part in seed, Series A and Series B rounds around the globe. The group last raised a $180 million fund that TechCrunch covered here, noting at the time that capital pool was “oversubscribed from an initial target of $140 million” and would be invested into “around 20 new companies from the new fund, writing opening cheques of between $1 million and $6 million.”

With boots on the ground in New York, White Star cares about the East Coast, so the fund’s put dossier on the region isn’t unexpected. What it includes, however, is.

We’ll start with NYC and its surprising 2019 before turning to Boston, digging into its super-giant venture totals and hearing from Founder Collective’s Eric Paley on the state of things in urban Massachusetts.

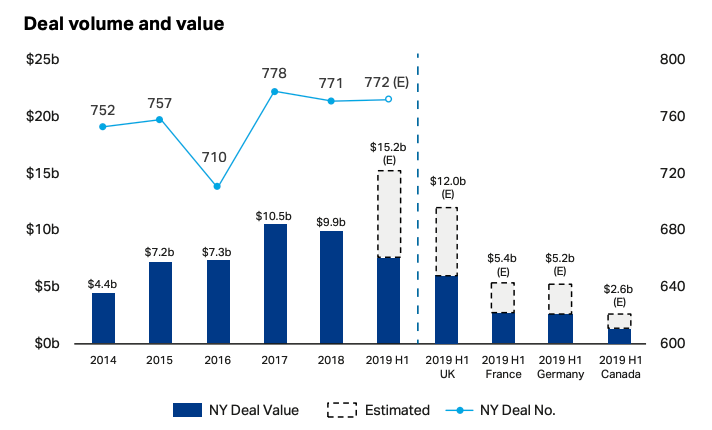

White Star’s report details record-breaking figures for NYC’s current year. Off of effectively flat deal volume (New York City sees around 775 venture deals per year at the moment, or a little more than two per day), the overgrown town should set record venture dollar volume in 2019.

Observe the following, astounding chart detailing the abnormality of 2019 from a comparative venture dollar perspective:

By smashing 2017’s local maximum, 2019 appears set to crush the city’s record — and rich — venture investment totals. The graphic also manages to point out (somewhat embarrassingly) that Gotham will manage to best a number of European countries’ aggregate venture dollar investments by itself this year.

That’s is a useful bit of context as in the United States, New York City is always Number Two to Silicon Valley. But, this chart argues, being number two in the number-one market is still a hell of a lot of capital.

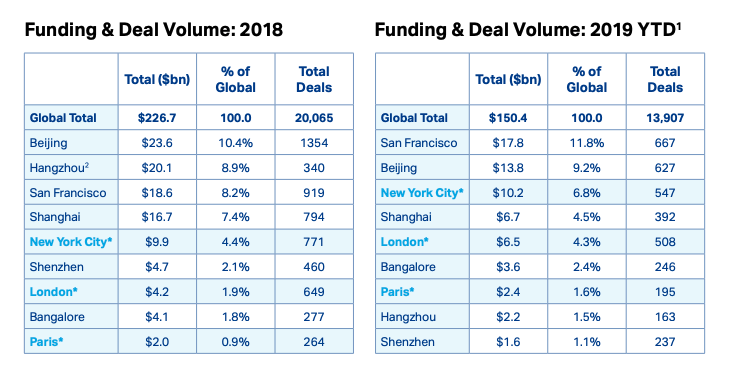

Putting New York City’s venture into even sharper comparative perspective, observe the following table:

Powered by WPeMatico

Raysecur says at least ten times a day someone sends a suspicious package containing powder, liquid, or some other kind of hazard.

The Boston, Mass.-based startup says its desktop-sized 3D real-time scanning technology, dubbed MailSecur, can intercept and detect threats in the mailroom before they ever make it onto the office floor.

Mailroom security may not seem fancy or interesting, but they’re a common gateway into a corporate environment. They’re a huge attack vector for attackers — both physical and cyber. Earlier this year we wrote about warshipping, a “Trojan horse”-type attack that can be used as a way for hackers to ship hardware exploits into a business, break the Wi-Fi, and pivot onto the corporate network to steal data.

Now, the company has raised $3 million in seed-round funding led by One Way Ventures, with participation from Junson Capital, Launchpad Venture Group, and also Dreamit Ventures, a Philadelphia-based early stage investor and accelerator, which last year announced it would move into the early-stage security space.

Raysecur’s proprietary millimeter-wave scanner, MailSecur. (Image: supplied)

Raysecur uses millimeter-wave technology — similar to the scanners you find at airport security — to examine suspicious letters, flat envelopes, and small parcels. Its technology can detect powders as small as 2% of a teaspoon or a single drop of liquid, the company claims.

The startup said the funding will help expand its customer base. Although still in its infancy, the company has about ten Fortune 500 customers using its MailSecur scanner.

Since it was founded in 2018, the company has scanned more than 9.2 million packages.

Semyon Dukach, managing partner at One Way Ventures, said the funding will help “bring this compelling technology to an even broader market.”

Powered by WPeMatico

Vendr has developed an enterprise SaaS solution for managing enterprise SaaS.

The new startup, founded by InVision’s former head of enterprise sales Ryan Neu, is another standout from Y Combinator’s latest batch. Contrary to the majority of those businesses, however, Vendr is already profitable.

In classic YC fashion, the company has created software to sell to other startups, and, as such, it was quick to gain the confidence of top venture capital investors. Headquartered in Boston, Vendr has raised a $2 million round led by F-Prime Capital, with participation from Ashton Kutcher’s Sound Ventures, Joe Montana’s Liquid2 Ventures, Garage VC and angel investors including Canva co-founder and chief operating officer Cliff Obrecht and HubSpot COO JD Sherman.

The company offers subscription-based software, priced depending on company headcount, that helps fast-growing businesses buy and manage enterprise SaaS. In short, the product cuts the human out of the sales process, allowing companies to purchase or upgrade software using software. The goal isn’t to eliminate the sales profession, rather to put an end to “persuasion driven” sales, Neu explains, and to make enterprise software purchases as easy as consumer product purchases.

Boston-based Vendr graduated from the Y Combinator startup accelerator earlier this year

“We see software sales actually going away because most people are tired of being sold to, they are tired of being persuaded, they want to transact,” Neu, who previously led sales at HubSpot, tells TechCruch. “Vendr was created to allow people to transact software without actually having to talk to people.”

Founded 14 months ago, Vendr has reached $1 million in annual recurring revenue, which, for context, has historically been amongst the benchmarks necessary for a SaaS startup to raise its Series A. Neu says the company is growing 15% month-over-month with monthly recurring revenue currently sitting at $96,500. Already profitable, Neu says they want to put themselves in a position in which they don’t have to raise any additional outside capital.

“I can’t imagine looking at the bank account every month and watching it deplete,” Neu said. “We want to be in a position where we can control our own destiny.”

Vendr currently operates with a team of six employees and 19 customers, including Canva, Grammarly, GitLab, Brex, HubSpot and InVision. The company is also backed by Okta’s general counsel Jon Runyan, AppDynamics’ COO Dan Wright and YC partner Aaron Epstein.

Powered by WPeMatico

Ginkgo Bioworks is now worth $4 billion after a $290 million capital infusion that will give the company the cash to dramatically expand its developer shop for genetic programming.

The Boston-based company is one of a handful of U.S.-based early-stage companies that are on the forefront of developing the tools to modify genetic material for everyday applications.

“Cells are programmable similar to computers because they run on digital code in the form of DNA,” said Jason Kelly, CEO and co-founder of Ginkgo Bioworks, in a statement. “Ginkgo has the best compiler and debugger for writing genetic code and we use it to program cells for customers in a range of industries. Today’s fundraise will allow us to expand our technology and continue our drive to bring biology into every physical goods industry — materials, clothing, electronics, food, pharmaceuticals and more. They are all biotech industries but just don’t know it yet.”

Ginkgo makes money in two ways. The company sells its development services to anyone who comes in with an idea. Kelly said that it’d be like any agreement with an entrepreneur who hires a coding shop to develop an application.

For example, if an entrepreneur wanted to develop houseplants that smelled like roses or lilies, they could approach Ginkgo, pay a (not-insignificant) fee and Ginkgo would do the research into designing something like a lily-scented fern. (Kelly puts the sticker price on that kind of development somewhere in the neighborhood of $10 million, so a founder best believe their product can sell.)

“You don’t need to come in with deep biological know-how,” Kelly says. “The question is, is capital interested in the problem?”

The other way that Ginkgo is approaching the market is by taking equity stakes in businesses that rely on its technology.

Those take the form of joint ventures with companies like Bayer (the first joint venture partner for Ginkgo) and the launch of Joyn, a $100 million spin-out that was created in the summer of 2018.

The two companies are collaborating on the development of seeds that require less fertilizer for growth — something that could save the industry millions and decrease pollution associated with traditional chemical fertilizers.

Since that first spin-out, Ginkgo has created three other companies and joint ventures. There’s the $122 million deal to produce rare cannabinoids with the Canadian cannabis company, Cronos; a partnership with Roche that was born out of Ginkgo’s acquisition of Warp Drive Bio; and Motif Foodworks, which is working on manufacturing alternative proteins with a $120 million in financing.*

Alongside these large-scale initiatives, Ginkgo has signed partnerships with the West Coast powerhouse accelerator program from Y Combinator and a new Boston-based life sciences-focused group called Petri to conduct development work for startups from those programs in exchange for an equity stake.

“We’re not going to have all the good ideas,” says Kelly. “We want to tap the much larger pool of smart people and really have them building on our platform. Of all of the people we can give value to, we can give the most to startups. If we can offer them to do their biowork without all of the fixed costs of building a lab,” that’s valuable, he says.

Investors in the company include Y Combinator, DCVC, MassChallenge, Felicis Ventures, General Atlantic, Baillie Gifford, Bill Gates and Viking Global.

Powered by WPeMatico

As biotechnology becomes more central to new innovations in healthcare, material science and manufacturing, one of the nation’s research hubs is getting a new accelerator called Petri to launch companies focused on the commercialization of new technologies.

Backed by the Boston-based venture capital firm Pillar, Petri has a three-year $15 million commitment to back companies developing new biotech applications in food, healthcare, industrial chemicals and new materials — along with the enabling technologies to bring these products to market.

“We’re at the inflection point where these technologies will impact and continue to impact health but will also impact food, agriculture, chemicals and materials,” says Petri co-founder, Tony Kulesa. “Everything we touch has some element of biology.”

Pillar has already invested in a couple of companies that show the potential promise of new biotech research coming from Boston-based universities, like Boston University, Harvard and the Massachusetts Institute of Technology.

Asimov,io, a company that has set an ultimate goal of designing new genomes for industrial applications, was co-founded by graduates from Boston University and MIT, and is a part of the Pillar portfolio. PathAi, a company working on enabling technologies for computational biology, also counts an MIT grad as a co-founder. Meanwhile, Harvard’s George Church has been instrumental in the development of a number of biotech companies working at the frontier of genetic applications for healthcare and manufacturing.

As an instructor at MIT, Kulesa spent seven years at MIT watching, in his words, how engineering has transformed biology. “It became clear to me that these technologies need to get out in the world,” he said.

Joining Kulesa as a managing director is Brian Baynes, a serial entrepreneur who founded Midori Health, an animal nutrition startup; Kaleido Biosciences, a microbiome control focused company; Celexion, a protein engineering and synthetic biology company; and Codon Devices, a synthetic biology toolkit company which was sold to Ginkgo Bioworks .

Over time, Kulesa and Baynes expect to have 10 to 20 companies in each cohort as the program expands. In addition to checks of at least $250,000 the Petri accelerator has lab and office space available for each company.

The companies also could benefit from potential partnerships with companies like Ginkgo Bioworks, which happens to share office space in the same building, and with the accelerator’s clutch of big-name advisors and “co-founders” recruited from across the life sciences industry.

These co-founders, who collectively hold a double-digit equity stake in Petri’s accelerator, include Reshma Shetty, from Ginkgo Bioworks; Emily Leproust of Twist Bioscience; Stan Lapidus, who was at Exact Sciences and Cytyc; Daphne Koller, the co-founder and chief executive of Insitro; Alec Nielsen, the founder Asimov; and researchers Chris Voigt of MIT and Pam Silver and George Church from Harvard’s Wyss Institute.

Genetically engineered organisms are finding their way into everything from food to fuel to chemistry. Companies like Impossible Foods, which uses genetically modified soy product, has raised hundreds of millions for its protein replacement, while Solugen, a manufacturer of chemicals using genetically modified organisms, has raised tens of millions to commercialize its technology. And Ginkgo Bioworks has raised nearly half a billion dollars to pursue applications for industrial biology.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week was a bit special. Instead of meeting up at the TechCrunch HQ to record the episode, Kate and Alex met up in muggy Boston at Drift’s office, where we linked up with Axios’s Dan Primack. And because we were feeling chatty, we went a bit long.

After checking in with Primack (he has a newsletter and a podcast), we first dealt with the latest from Tumblr. In short, Verizon Media is selling Tumblr to Automattic for a few dollars. How did Verizon wind up owning Tumblr? Ah. Well, Yahoo bought it. Later, after Verizon bought AOL, it bought Yahoo. Then it smushed them together and called it Oath. Then Verizon decided that it didn’t like that much and renamed the group Verizon Media. But Verizon doesn’t want to own media (besides TechCrunch, of course), so it sold Tumblr to Automattic, a venture-backed company best known for operating WordPress.

That’s a lot, I know. What matters is that Yahoo bought Tumblr for more than $1 billion. Verizon sold it for around $3 million. Now, Automattic has a few hundred new employees and a shot at juicing its user base before it goes public.

After that, we lamented that the WeWork S-1 had yet to appear. This was a tragedy, frankly. We had expected to spend half the show riffing on WeWork’s financials, alas…

So we turned to some normal material, like Ramp’s recent $7 million raise to take on Brex, and, SmartNews’s recent round, which gave it an eye-popping $1.1 billion valuation.

We ran a bit long because we were having fun, fitting in some conversation surrounding the notes from the SEC regarding the now-dead and then-fraudulent Rothenberg Ventures. More on that here if you want to get angry.

And finally, Vision Fund 2. It’s been a big source of interest for everyone on the show, and we expect whatever the second-act Vision Fund winds up becoming to be a big damn deal. The fund will invest in more than just consumer marketplaces; in fact, it’s eyeing more AI businesses and even biotech. That should be interesting.

All that and we have a lot more good stuff coming. Thanks for listening to the show, and we’ll be right back.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Cybereason, which uses machine learning to increase the number of endpoints a single analyst can manage across a network of distributed resources, has raised $200 million in new financing from SoftBank Group and its affiliates.

It’s a sign of the belief that SoftBank has in the technology, since the Japanese investment firm is basically doubling down on commitments it made to the Boston-based company four years ago.

The company first came to our attention five years ago when it raised a $25 million financing from investors, including CRV, Spark Capital and Lockheed Martin.

Cybereason’s technology processes and analyzes data in real time across an organization’s daily operations and relationships. It looks for anomalies in behavior across nodes on networks and uses those anomalies to flag suspicious activity.

The company also provides reporting tools to inform customers of the root cause, the timeline, the person involved in the breach or breaches, which tools they use and what information was being disseminated within and outside of the organization.

For co-founder Lior Div, Cybereason’s work is the continuation of the six years of training and service he spent working with the Israeli army’s 8200 Unit, the military incubator for half of the security startups pitching their wares today. After his time in the military, Div worked for the Israeli government as a private contractor reverse-engineering hacking operations.

Over the last two years, Cybereason has expanded the scope of its service to a network that spans 6 million endpoints tracked by 500 employees, with offices in Boston, Tel Aviv, Tokyo and London.

“Cybereason’s big data analytics approach to mitigating cyber risk has fueled explosive expansion at the leading edge of the EDR domain, disrupting the EPP market. We are leading the wave, becoming the world’s most reliable and effective endpoint prevention and detection solution because of our technology, our people and our partners,” said Div, in a statement. “We help all security teams prevent more attacks, sooner, in ways that enable understanding and taking decisive action faster.”

The company said it will use the new funding to accelerate its sales and marketing efforts across all geographies and push further ahead with research and development to make more of its security operations autonomous.

“Today, there is a shortage of more than three million level 1-3 analysts,” said Yonatan Striem-Amit, chief technology officer and co-founder, Cybereason, in a statement. “The new autonomous SOC enables SOC teams of the future to harness technology where manual work is being relied on today and it will elevate L1 analysts to spend time on higher value tasks and accelerate the advanced analysis L3 analysts do.”

Most recently the company was behind the discovery of Operation SoftCell, the largest nation-state cyber espionage attack on telecommunications companies.

That attack, which was either conducted by Chinese-backed actors or made to look like it was conducted by Chinese-backed actors, according to Cybereason, targeted a select group of users in an effort to acquire cell phone records.

As we wrote at the time:

… hackers have systematically broken in to more than 10 cell networks around the world to date over the past seven years to obtain massive amounts of call records — including times and dates of calls, and their cell-based locations — on at least 20 individuals.

Researchers at Boston-based Cybereason, who discovered the operation and shared their findings with TechCrunch, said the hackers could track the physical location of any customer of the hacked telcos — including spies and politicians — using the call records.

Lior Div, Cybereason’s co-founder and chief executive, told TechCrunch it’s “massive-scale” espionage.

Call detail records — or CDRs — are the crown jewels of any intelligence agency’s collection efforts. These call records are highly detailed metadata logs generated by a phone provider to connect calls and messages from one person to another. Although they don’t include the recordings of calls or the contents of messages, they can offer detailed insight into a person’s life. The National Security Agency has for years controversially collected the call records of Americans from cell providers like AT&T and Verizon (which owns TechCrunch), despite the questionable legality.

It’s not the first time that Cybereason has uncovered major security threats.

Back when it had just raised capital from CRV and Spark, Cybereason’s chief executive was touting its work with a defense contractor who’d been hacked. Again, the suspected culprit was the Chinese government.

As we reported, during one of the early product demos for a private defense contractor, Cybereason identified a full-blown attack by the Chinese — 10,000 thousand usernames and passwords were leaked, and the attackers had access to nearly half of the organization on a daily basis.

The security breach was too sensitive to be shared with the press, but Div says that the FBI was involved and that the company had no indication that they were being hacked until Cybereason detected it.

Powered by WPeMatico

There comes a time for many startup companies where they either realize they need to do a nationwide rollout, or they need to actively target buyers in the middle of the country. If you are a startup on either the East or the West Coasts, it’s worth thinking about how this market might present its own set of unique challenges, and how you plan to overcome them.

There are a lot of misconceptions about what some people call “flyover country,” and as a San Francisco native who spent two decades in New York, Washington DC, and Boston before moving to Pittsburgh, I can assure you they are almost all wrong. Without getting into specifics, the reality of “middle America” is that it’s the same as anywhere else.

Income, education, world view, and waistlines are all varied. It’s pretty accurate that San Francisco possesses a culture obsessed with fitness and entrepreneurship, but California isn’t necessarily all like that, and if you think it is, I encourage you to go to Bakersfield, the Central Valley, or Eureka sometime.

In addition, just because the stereotypes are wrong doesn’t mean there’s nothing different about doing business here. As you think about how to conduct your rollout, here are some things you should consider:

As with any market, research is key since it informs every other aspect of the rollout. Start by looking into who your competition is.

Since there are fewer VC-backed startups in middle America, and smaller companies tend to get less press, the research may be harder. However, there are some major universities that are actively putting money into their own Entrepreneurship programs and those spinoffs often do very well.

Powered by WPeMatico