boston

Auto Added by WPeMatico

Auto Added by WPeMatico

Many of the stories in our EC-1 series tell tales of startups in the wilderness hacking out green field opportunities. Klaviyo is a different breed of company: One that went into an established market and challenged powerful incumbents, ultimately finding success with a new, more data-oriented generation of email marketers.

As such, the lessons that it offers are, perhaps, more subtle; its insights bordering on common sense.

But as the saying goes, common sense to an uncommon degree becomes wisdom. Here are four pieces of wisdom I’ve gleaned from Klaviyo’s story:

Drama and sizzle help companies stand out, undoubtedly. But are they necessary for success? Klaviyo’s story suggests otherwise.

Silicon Valley has become a showcase for oddity. Ironically, we all enjoy “Silicon Valley” (the show) or “The Social Network.” Unironically, we toss around phrases like “the hustle” and “sweat equity.” Hot companies often stand out with stories of intense struggle and failure, a larger-than-life founder or a chaotic (and often toxic) management structure.

Drama and sizzle help companies stand out, undoubtedly. But are they necessary for success? Klaviyo’s story suggests otherwise.

Powered by WPeMatico

When the world shifted toward virtual one year ago, one service in particular saw heated demand: remote online notarization.

The ability to get a document notarized without leaving one’s home suddenly became more of a necessity than a luxury. Pat Kinsel, founder and CEO of Boston-based Notarize, worked to get appropriate legislation passed across the country to make it possible for more people in more states to get documents notarized digitally.

That hard work has paid off. Today, Notarize has announced $130 million in Series D funding led by fintech-focused VC firm Canapi Ventures after experiencing 600% year over year revenue growth. The round values Notarize at $760 million, which is triple its valuation at the time of its $35 million Series C in March of 2020. This latest round is larger than the sum of all of the company’s previous rounds to date, and brings Notarize’s total raised to $213 million since its 2015 inception.

A slew of other investors participated in the round, including Alphabet’s independent growth fund CapitalG, Citi Ventures, Wells Fargo, True Bridge Capital Partners and existing backers Camber Creek, Ludlow Ventures, NAR’s Second Century Ventures and Fifth Wall Ventures.

Notarize insists that it “isn’t just a notary company.” Rather, Canapi Ventures partner Neil Underwood described it as the “last mile” of businesses (such as iBuyers, for example).

The company has also evolved to “also bring trust and identity verification” into those businesses’ processes.

Over the past year, Notarize has seen a massive increase in transactions and inked new partnerships with companies such as Adobe, Dropbox, Stripe and Zillow Group, among others. It’s seen big spikes in demand from the real estate, financial services, retail and automotive sectors.

“In 2020, the world rushed to digitize. Online commerce ballooned, and businesses in almost every industry needed to transition to digital basically overnight so they could continue uninterrupted,” Kinsel said. “Notarize was there to help them safely close these deals with trust and convenience.”

The company plans to use its new capital to expand its platform and product and scale “to serve enterprises of all sizes.” It also plans to double down on hiring in the next year.

“Notarize is disrupting outdated business models and technologies, and there’s massive potential, particularly in the financial services space, as more companies will need to offer secure digital alternatives to in-person transactions,” Canapi’s Underwood said.

Notarize’s success comes after a difficult 2019, when the company saw “critical financing” fall through and had to lay off staff, according to Kinsel. Talk about a turnaround story.

Powered by WPeMatico

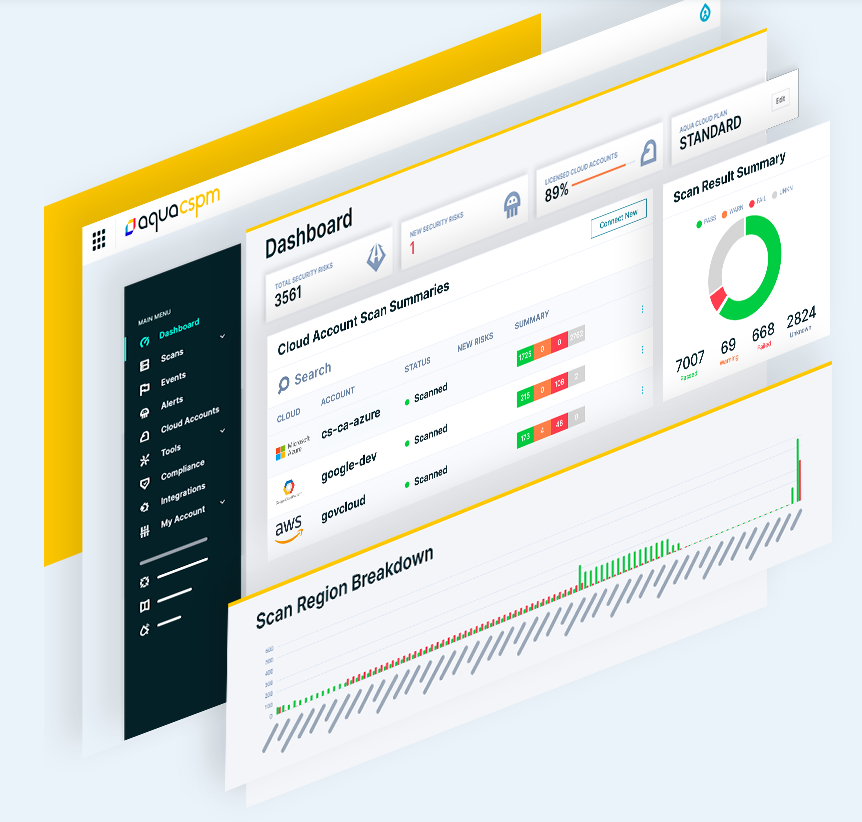

Aqua Security, a Boston- and Tel Aviv-based security startup that focuses squarely on securing cloud-native services, today announced that it has raised a $135 million Series E funding round at a $1 billion valuation. The round was led by ION Crossover Partners. Existing investors M12 Ventures, Lightspeed Venture Partners, Insight Partners, TLV Partners, Greenspring Associates and Acrew Capital also participated. In total, Aqua Security has now raised $265 million since it was founded in 2015.

The company was one of the earliest to focus on securing container deployments. And while many of its competitors were acquired over the years, Aqua remains independent and is now likely on a path to an IPO. When it launched, the industry focus was still very much on Docker and Docker containers. To the detriment of Docker, that quickly shifted to Kubernetes, which is now the de facto standard. But enterprises are also now looking at serverless and other new technologies on top of this new stack.

“Enterprises that five years ago were experimenting with different types of technologies are now facing a completely different technology stack, a completely different ecosystem and a completely new set of security requirements,” Aqua CEO Dror Davidoff told me. And with these new security requirements came a plethora of startups, all focusing on specific parts of the stack.

Image Credits: Aqua Security

What set Aqua apart, Dror argues, is that it managed to 1) become the best solution for container security and 2) realized that to succeed in the long run, it had to become a platform that would secure the entire cloud-native environment. About two years ago, the company made this switch from a product to a platform, as Davidoff describes it.

“There was a spree of acquisitions by CheckPoint and Palo Alto [Networks] and Trend [Micro],” Davidoff said. “They all started to acquire pieces and tried to build a more complete offering. The big advantage for Aqua was that we had everything natively built on one platform. […] Five years later, everyone is talking about cloud-native security. No one says ‘container security’ or ‘serverless security’ anymore. And Aqua is practically the broadest cloud-native security [platform].”

One interesting aspect of Aqua’s strategy is that it continues to bet on open source, too. Trivy, its open-source vulnerability scanner, is the default scanner for GitLab’s Harbor Registry and the CNCF’s Artifact Hub, for example.

“We are probably the best security open-source player there is because not only do we secure from vulnerable open source, we are also very active in the open-source community,” Davidoff said (with maybe a bit of hyperbole). “We provide tools to the community that are open source. To keep evolving, we have a whole open-source team. It’s part of the philosophy here that we want to be part of the community and it really helps us to understand it better and provide the right tools.”

In 2020, Aqua, which mostly focuses on mid-size and larger companies, doubled the number of paying customers and it now has more than half a dozen customers with an ARR of over $1 million each.

Davidoff tells me the company wasn’t actively looking for new funding. Its last funding round came together only a year ago, after all. But the team decided that it wanted to be able to double down on its current strategy and raise sooner than originally planned. ION had been interested in working with Aqua for a while, Davidoff told me, and while the company received other offers, the team decided to go ahead with ION as the lead investor (with all of Aqua’s existing investors also participating in this round).

“We want to grow from a product perspective, we want to grow from a go-to-market [perspective] and expand our geographical coverage — and we also want to be a little more acquisitive. That’s another direction we’re looking at because now we have the platform that allows us to do that. […] I feel we can take the company to great heights. That’s the plan. The market opportunity allows us to dream big.”

Powered by WPeMatico

As President-elect Joe Biden readies his transition team and sets the agenda for his first 100 days in office, startups can expect to see some movement on long-stalled infrastructure initiatives that could mean big boosts to their business.

Infrastructure is high on the list of priorities of the incoming Biden Administration as the former vice president hopes to make good on his campaign promise to “build back better.”

American infrastructure has been crumbling for decades without significant investment from the federal government, and much of what will be replaced will also be upgraded with new technology, according to people familiar with the Biden plan.

That means tech companies focused on next-generation telecommunications and utility infrastructure, transportation, housing and construction tech around energy efficiency could see new dollars pour in over the next four years.

“Infrastructure and build out of the clean energy economy … doesn’t necessarily mean large wind or large solar projects. It could mean advanced metering … it can be new engine technologies,” said Dan Goldman, a managing partner at Clean Energy Ventures. “We think that that can be a huge opportunity for job creation … not only putting people back to work but putting people back to work in high quality jobs.”

And there’s a willingness to encourage these infrastructure projects in less partisan ways in states like Massachusetts, Virginia and Florida, which are actively building out electric vehicle infrastructure and renewable energy projects, Goldman said.

While the federal government will ultimately be distributing the cash, startups can expect to see the spending actually come from municipalities and state governments, which often have a better understanding of local needs and where the money should go.

The electrification of everything — a component of any zero-carbon movement — requires significant upgrades to existing power infrastructure. That means everything from systems management technologies to distribution facilities to ways to store power that can be moved on to the grid.

“Without that infrastructure investment it gets quite challenging,” said Abe Yokell, a co-founder and managing partner of Congruent Ventures.

He pointed to large-scale energy storage technologies as one solution, but management systems for utilities will be another area of interest.

Those infrastructure initiatives will likely mean good things for battery companies like Form Energy, which signed its first major contract with Great River Energy earlier this year; or Antora and Malta, which store energy as heat; or Quidnet, which has a pumped hydroelectric play for large-scale energy storage by pumping water into the gaps between rocks underground that creates pressure and can force water back up through a generator.

Other large-scale energy storage companies working on developing and installing batteries could benefit as well. That means good things for Tesla, which has a few major battery installs under its belt, and Fluence, which manages and operates big install projects.

Natel Energy, another startup working on energy storage (and generation) using hydropower, could also find its technology in the mix, according to company founder, Gia Schneider.

Schneider sees three potential pitches for her company’s technologies. “Climate change is water change,” she said. “We have a bucket in energy, a bucket of stuff in environmental and a bucket of stuff in working lands.”

Powered by WPeMatico

NextView Ventures, a Boston-based venture capital fund, has raised an $89.6 million fund, according to SEC filings. The firm’s fourth fund, its largest to date, is oversubscribed, with early documents indicating a $70 million goal. The NextView Ventures team did not immediately respond to request for comment.

NextView Ventures was launched in 2010 by Rob Go, a former partner at Spark Capital; Dave Beisel, who clocked time at Venrock and Masthead Venture Partners; and Lee Hower, a former investor at Point Judith Capital. Melody Koh joined as a partner three years ago, and most recently, the fund brought on former journalist Leah Fessler as an investor.

The fund, which has offices in New York as well as Boston, invests in consumer and software-as-a-service enterprise startups at the pre-seed and seed stage. Its portfolio includes Ellevest, an investing platform for women; Grove Collaborative, a sustainable goods subscription platform; and ThredUp, which has confidentially filed for IPO. In April, NextView launched a virtual accelerator for startups to build a more robust pipeline for deal flow. The firm invested $200,000 for an 8% equity stake in a number of pre-seed and seed startups focused on “the everyday economy.”

Despite the pandemic, Boston’s startup scene has continued to attract record numbers in venture capital volume. In fact, according to PitchBook data, Boston-area startups raised more private capital during summer 2020 than they did in summer 2019, suggesting that the pandemic has been a boon to startups in aggregate.

More recently, my colleague Alex Wilhelm and I wrote about how the Boston area is growing its demographic footprint in venture capital. In Q3 2019, New England drove 9.3% of U.S. venture deals, and 10.3% of U.S. venture dollars. In Q3 2020, those numbers were 9.3% of U.S. venture deals, and 12.7% of U.S. venture dollars. The percentage change is notable, especially amid volatile times.

NextView’s new fund is yet another signal of the city’s ability to attract institutional investment. Its previous fund was raised in 2017 at a $50 million close.

Powered by WPeMatico

Deep tech. Hard tech. Or, as The Engine dubs it, Tough Tech.

Venture investing today is essentially identical to what happens on Wall Street, focused on data rooms, spreadsheets, SaaS churn models and cohort analysis. Yet, the history of venture capital firms is heavily interwoven with universities and their research. Some of the most famous VC funds like Kleiner Perkins got their start funding compelling research projects out of laboratories and financing their commercialization toward scale.

Technical risk is something many VCs like to avoid, but The Engine has built an entire brand and thesis around it. Centered around Kendall Square and the broader MIT ecosystem, The Engine debuted a couple of years ago with a focus on “tough tech” problems that are perhaps a touch too early for other VCs. That’s led to investments in companies like Boston Metal, which builds environmentally-friendly steel alloys, WoHo, which is rethinking modular building construction that we profiled last week, and Commonwealth Fusion Systems, which is developing fusion power.

Indeed, the firm’s portfolio page has to be one of the most interesting in the industry today.

The good news is that the firm’s ambitious funding strategy looks set to continue. It announced this morning that it has raised $230 million toward the firm’s second fund, which on top of the firm’s first fund brings it to a total of $435 million under management. In a press statement, the firm said that it has funded 27 portfolio companies out of its first fund. While MIT continues to be the anchor LP, Harvard joined for Fund 2, creating a cross-Cambridge, MA venture platform.

Katie Rae remains CEO and managing partner of the fund, and her team has expanded over the past few years as the firm has scaled up.

The Engine’s Reed Sturtevant, Katie Rae, and Ann DeWitt prepare for the Tough Tech Summit today. Photo via The Engine.

One interesting point that we haven’t noted previously is that MIT is building The Engine a 200,000 square foot building near its campus that will offer massive space for startups and portfolio companies to start and grow over time. That building is expected to open in 2022, hopefully when this whole pandemic situation allows for in-office collaboration again.

Boston has become something of a hub for deeper technical projects. Local startup Desktop Metal, which builds 3D printers that can print metal, is going through a SPAC process that values the company at roughly $2.5 billion. With this latest news from The Engine, it seems clear that Boston’s tough tech ecosystem will continue to have a pipeline of interesting and compelling companies.

Powered by WPeMatico

This year has shaken up venture capital, turning a hot early start to 2020 into a glacial period permeated with fear during the early days of COVID-19. That ice quickly melted as venture capitalists discovered that demand for software and other services that startups provide was accelerating, pushing many young tech companies back into growth mode, and investors back into the check-writing arena.

Boston has been an exemplar of the trend, with early pandemic caution dissolving into rapid-fire dealmaking as summer rolled into fall.

We collated new data that underscores the trend, showing that Boston’s third quarter looks very solid compared to its peer groups, and leads greater New England’s share of American venture capital higher during the three-month period.

For our October look at Boston and its startup scene, let’s get into the data and then understand how a new cohort of founders is cropping up among the city’s educational network.

For our October look at Boston and its startup scene, let’s get into the data and then understand how a new cohort of founders is cropping up among the city’s educational network.

Boston’s third quarter was strong, effectively matching the capital raised in New York City during the three-month period. As we head into the fourth quarter, it appears that the silver medal in American startup ecosystems is up for grabs based on what happens in Q4.

Boston could start 2021 as the number-two place to raise venture capital in the country. Or New York City could pip it at the finish line. Let’s check the numbers.

According to PitchBook data shared with TechCrunch, the metro Boston area raised $4.34 billion in venture capital during the third quarter. New York City and its metro area managed $4.45 billion during the same time period, an effective tie. Los Angeles and its own metro area managed just $3.90 billion.

In 2020 the numbers tilt in Boston’s favor, with the city and surrounding area collecting $12.83 billion in venture capital. New York City came in second through Q3, with $12.30 billion in venture capital. Los Angeles was a distant third at $8.66 billion for the year through Q3.

Powered by WPeMatico

Companies that have leveraged technology to make the procurement and delivery of food more accessible to more people have been seeing a big surge of business this year, as millions of consumers are encouraged (or outright mandated, due to COVID-19) to socially distance or want to avoid the crowds of physical shopping and eating excursions.

Today, one of the companies that is supplying produce and other items both to consumers and other services that are in turn selling food and groceries to them, is announcing a new round of funding as it gears up to take its next step, an IPO.

GrubMarket, which provides a B2C platform for consumers to order produce and other food and home items for delivery, and a B2B service where it supplies grocery stores, meal-kit companies and other food tech startups with products that they resell, is today announcing that it has raised $60 million in a Series D round of funding.

Sources close to the company confirmed to TechCrunch that GrubMarket — which is profitable, and originally hadn’t planned to raise more than $20 million — has now doubled its valuation compared to its last round — sources tell us it is now between $400 million and $500 million.

The funding is coming from funds and accounts managed by BlackRock, Reimagined Ventures, Trinity Capital Investment, Celtic House Venture Partners, Marubeni Ventures, Sixty Degree Capital and Mojo Partners, alongside previous investors GGV Capital, WI Harper Group, Digital Garage, CentreGold Capital, Scrum Ventures and other unnamed participants. Past investors also included Y Combinator, where GrubMarket was part of the Winter 2015 cohort. For some context, GrubMarket last raised money in April 2019 — $28 million at a $228 million valuation, a source says.

Mike Xu, the founder and CEO, said that the plan remains for the company to go public (he’s talked about it before), but given that it’s not having trouble raising from private markets and is currently growing at 100% over last year, and the IPO market is less certain at the moment, he declined to put an exact timeline on when this might actually happen, although he was clear that this is where his focus is in the near future.

“The only success criteria of my startup career is whether GrubMarket can eventually make $100 billion of annual sales,” he said to me over both email and in a phone conversation. “To achieve this goal, I am willing to stay heads-down and hardworking every day until it is done, and it does not matter whether it will take me 15 years or 50 years.”

I don’t doubt that he means it. I’ll note that we had this call in the middle of the night his time in California, even after I asked multiple times if there wasn’t a more reasonable hour in the daytime for him to talk. (He insisted that he got his best work done at 4:30 a.m., a result of how a lot of the grocery business works.) Xu on the one hand is very gentle with a calm demeanor, but don’t let his quiet manner fool you. He also is focused and relentless in his work ethic.

When people talk today about buying food, alongside traditional grocery stores and other physical food markets, they increasingly talk about grocery delivery companies, restaurant delivery platforms, meal kit services and more that make or provide food to people by way of apps. GrubMarket has built itself as a profitable but quiet giant that underpins the fuel that helps companies in all of these categories by becoming one of the critical companies building bridges between food producers and those that interact with customers.

Its opportunity comes in the form of disruption and a gap in the market. Food production is not unlike shipping and other older, non-tech industries, with a lot of transactions couched in legacy processes: GrubMarket has built software that connects the different segments of the food supply chain in a faster and more efficient way, and then provides the logistics to help it run.

To be sure, it’s an area that would have evolved regardless of the world health situation, but the rise and growth of the coronavirus has definitely “helped” GrubMarket not just by creating more demand for delivered food, but by providing a way for those in the food supply chain to interact with less contact and more tech-fueled efficiency.

Sales of WholesaleWare, as the platform is called, Xu said, have seen more than 800% growth over the last year, now managing “several hundreds of millions of dollars of food wholesale activities” annually.

Underpinning its tech is the sheer size of the operation: economies of scale in action. The company is active in the San Francisco Bay Area, Los Angeles, San Diego, Seattle, Texas, Michigan, Boston and New York (and many places in between) and says that it currently operates some 21 warehouses nationwide. Xu describes GrubMarket as a “major food provider” in the Bay Area and the rest of California, with (as one example) more than 5 million pounds of frozen meat in its east San Francisco Bay warehouse.

Its customers include more than 500 grocery stores, 8,000 restaurants and 2,000 corporate offices, with familiar names like Whole Foods, Kroger, Albertson, Safeway, Sprouts Farmers Market, Raley’s Market, 99 Ranch Market, Blue Apron, Hello Fresh, Fresh Direct, Imperfect Foods, Misfit Market, Sun Basket and GoodEggs all on the list, with GrubMarket supplying them items that they resell directly, or use in creating their own products (like meal kits).

While much of GrubMarket’s growth has been — like a lot of its produce — organic, its profitability has helped it also grow inorganically. It has made some 15 acquisitions in the last two years, including Boston Organics and EJ Food Distributor this year.

It’s not to say that GrubMarket has not had growing pains. The company, Xu said, was like many others in the food delivery business — “overwhelmed” at the start of the pandemic in March and April of this year. “We had to limit our daily delivery volume in some regions, and put new customers on waiting lists.” Even so, the B2C business grew between 300% and 500% depending on the market. Xu said things calmed down by May and even as some B2B customers never came back after cities were locked down, as a category, B2B has largely recovered, he said.

Interestingly, the startup itself has taken a very proactive approach in order to limit its own workers’ and customers’ exposure to COVID-19, doing as much testing as it could — tests have been, as we all know, in very short supply — as well as a lot of social distancing and cleaning operations.

“There have been no mandates about masks, but we supplied them extensively,” he said.

So far it seems to have worked. Xu said the company has only found “a couple of employees” that were positive this year. In one case in April, a case was found not through a test (which it didn’t have, this happened in Michigan) but through a routine check and finding an employee showing symptoms, and its response was swift: the facilities were locked down for two weeks and sanitized, despite this happening in one of the busiest months in the history of the company (and the food supply sector overall).

That’s notable leadership at a time when it feels like a lot of leaders have failed us, which only helps to bolster the company’s strong growth.

Powered by WPeMatico

Most venture capital firms are based in hubs like Silicon Valley, New York City and Boston. These firms nurture those ecosystems and they’ve done well, but SaaS Ventures decided to go a different route: it went to cities like Chicago, Green Bay, Wisconsin and Lincoln, Nebraska.

The firm looks for enterprise-focused entrepreneurs who are trying to solve a different set of problems than you might find in these other centers of capital, issues that require digital solutions but might fall outside a typical computer science graduate’s experience.

Saas Ventures looks at four main investment areas: trucking and logistics, manufacturing, e-commerce enablement for industries that have not typically gone online and cybersecurity, the latter being the most mainstream of the areas SaaS Ventures covers.

The company’s first fund, which launched in 2017, was worth $20 million, but SaaS Ventures launched a second fund of equal amount earlier this month. It tends to stick to small-dollar-amount investments, while partnering with larger firms when it contributes funds to a deal.

We talked to Collin Gutman, founder and managing partner at SaaS Ventures, to learn about his investment philosophy, and why he decided to take the road less traveled for his investment thesis.

Gutman’s journey to find enterprise startups in out of the way places began in 2012 when he worked at an early enterprise startup accelerator called Acceleprise. “We were really the first ones who said enterprise tech companies are wired differently, and need a different set of early-stage resources,” Gutman told TechCrunch.

Through that experience, he decided to launch SaaS Ventures in 2017, with several key ideas underpinning the firm’s investment thesis: after his experience at Acceleprise, he decided to concentrate on the enterprise from a slightly different angle than most early-stage VC establishments.

Collin Gutman, founder and managing partner at SaaS Ventures (Image Credits: SaaS Ventures)

The second part of his thesis was to concentrate on secondary markets, which meant looking beyond the popular startup ecosystem centers and investing in areas that didn’t typically get much attention. To date, SaaS Ventures has made investments in 23 states and Toronto, seeking startups that others might have overlooked.

“We have really phenomenal coverage in terms of not just geography, but in terms of what’s happening with the underlying businesses, as well as their customers,” Gutman said. He believes that broad second-tier market data gives his firm an upper hand when selecting startups to invest in. More on that later.

Powered by WPeMatico

For many investors, the coronavirus has effectively taken geography out of the equation when it comes to vetting new opportunities.

While this dynamic opens up startups to more investment opportunities, venture capital firms that focus on a specific region are in a thornier spot. The competitive advantage they once had when raising — the notion that they’re focused on an area no one else is — is potentially threatened.

Natasha Mascarenhas, Danny Crichton and Alex Wilhelm of the TechCrunch Equity crew discussed the future of geographic-focused funds given the uptick of remote investing:

Since 2014, Steve Case and his team have made an annual bus trip across the country to meet startups in emerging startup hubs. Five days, five cities and at least $500,000 of investment dollars given to startups. Case would even offer to fly out promising and hard-to-reach startups to have them join the trip.

The Rise of the Rest fund, with more than $300 million in assets under management, has invested in over 130 startups across 70 cities, including Austin, Chicago, Detroit, Los Angeles, New Orleans and Washington, D.C.

Powered by WPeMatico