battery ventures

Auto Added by WPeMatico

Auto Added by WPeMatico

Amid a recent tear in residential real estate investment, venture capitalists are looking to get a piece of homebuying startup Flyhomes.

The five-year-old startup announced today that they’ve closed a $150 million Series C round co-led by Norwest Venture Partners and Battery Ventures. Fifth Wall, Camber Creek, Balyasny Asset Management, Zillow’s Spencer Rascoff and existing investors Andreessen Horowitz and Canvas Partners also participated in the round. Norwest’s Lisa Wu and Battery’s Roger Lee are joining Flyhomes’ board as part of the deal.

The end-to-end residential real estate startup says they handle “every step of the homebuying process, from brokerage to mortgage,” building financial tools that customers need throughout the process. The company has now raised some $310 million in total.

The startup is well-positioned during a historic run-up of home prices in the U.S. that has made deals more competitive than ever for prospective buyers. A recent report by Redfin notes that more than half of U.S. homes are selling above their asking price right now, up from one in four a year ago. A Zillow report notes that nearly half of U.S. homes are selling within one week of going on the market.

Flyhomes’s Cash Offer lending product allows consumers purchasing homes to make more attractive all-cash offers to sellers, with the company noting that even if a buyer ends up backing out of the deal, Flyhomes will still buy the home themselves. Central to the startup’s business is sellers being more amenable to all-cash offers, allowing consumers making them to win deals even when they aren’t the highest bidders.

The company says it has bought and sold more than $2.6 billion worth of homes since launching in 2016.

Powered by WPeMatico

Every branch of science is increasingly reliant on big data sets and analysis, which means a growing confusion of formats and platforms — more than inconvenient, this can hinder the process of peer review and replication of research. Code Ocean hopes to make it easier for scientists to collaborate by making a flexible, shareable format and platform for any and all data sets and methods, and it has raised a total of $21 million to build it out.

Certainly there’s an air of “Too many options? Try this one!” to this (and here’s the requisite relevant XKCD). But Code Ocean isn’t creating a competitor to successful tools like Jupyter or GitLab or Docker — it’s more of a small-scale container platform that lets you wrap up all the necessary components of your data and analysis in an easily shared format, whatever platform they live on natively.

The trouble appears when you need to share what you’re doing with another researcher, whether they’re on the bench next to you or at a university across the country. It’s important for replication purposes that data analysis — just like any other scientific technique — be done exactly the same way. But there’s no guarantee that your colleague will use the same structures, formats, notation, labels and so on.

That doesn’t mean it’s impossible to share your work, but it does add a lot of extra steps as would-be replicators or iterators check and double check that all the methods are the same, that the same versions of the same tools are being used in the same order, with the same settings, and so on. A tiny inconsistency can have major repercussions down the road.

Turns out this problem is similar in a way to how many cloud services are spun up. Software deployments can be as finicky as scientific experiments, and one solution to this is containers, which like tiny virtual machines include everything needed to accomplish a computing task, in a portable format compatible with many different setups. The idea is a natural one to transfer to the research world, where you can tie up all in one tidy package the data, the software used and the specific techniques and processes used to reach a given result. That, at least, is the pitch Code Ocean offers for its platform and “Compute Capsules.”

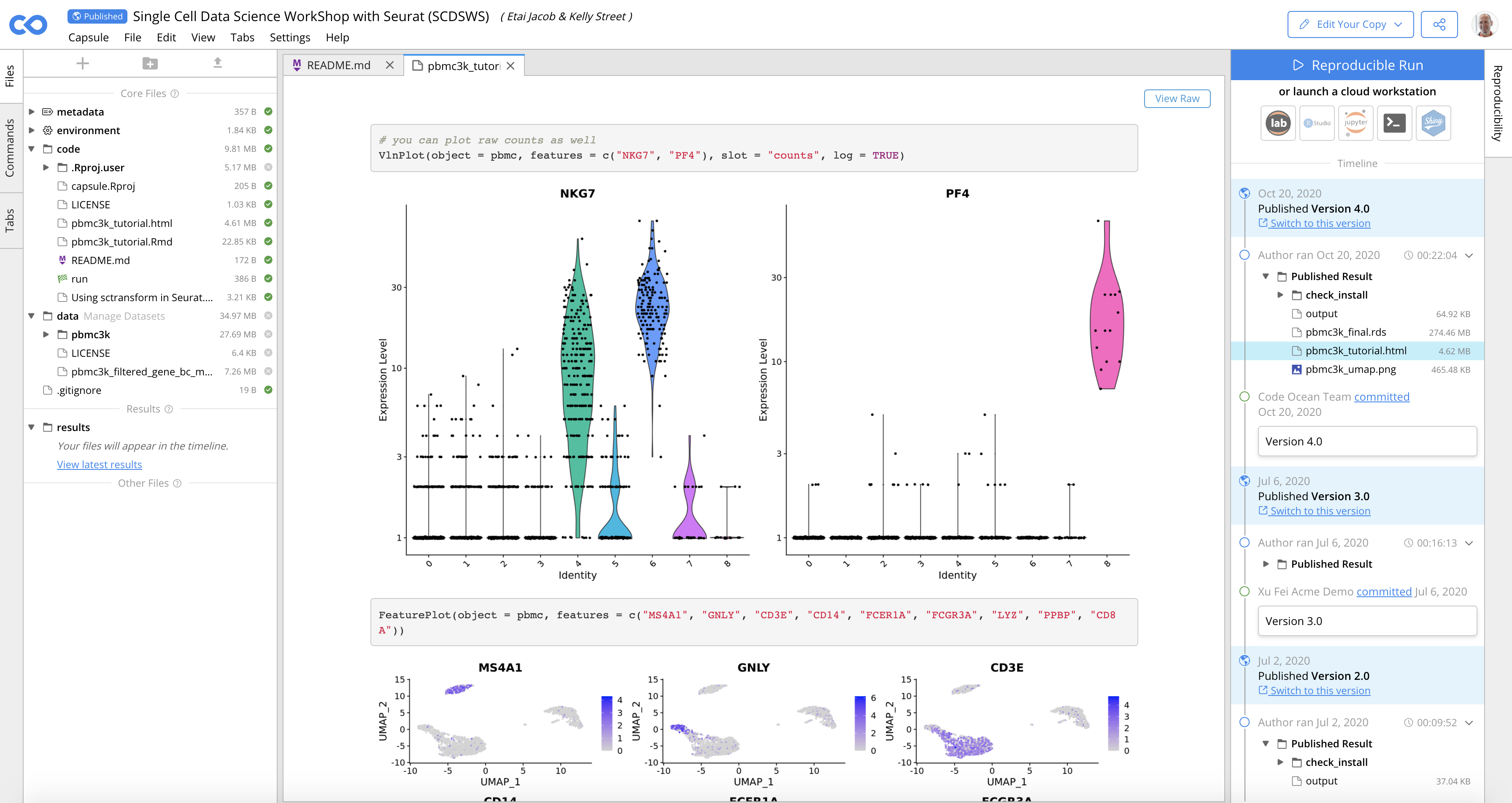

Image Credits: Code Ocean

Say you’re a microbiologist looking at the effectiveness of a promising compound on certain muscle cells. You’re working in R, writing in RStudio on an Ubuntu machine, and your data are such and such collected during an in vitro observation. While you would naturally declare all this when you publish, there’s no guarantee anyone has an Ubuntu laptop with a working RStudio setup around, so even if you provide all the code, it might be for nothing.

If, however, you put it on Code Ocean, like this, it makes all the relevant code available, and capable of being inspected and run unmodified with a click, or being fiddled with if a colleague is wondering about a certain piece. It works through a single link and web app, cross platform, and can even be embedded on a webpage like a document or video. (I’m going to try to do that below, but our backend is a little finicky. The capsule itself is here.)

More than that, though, the Compute Capsule can be repurposed by others with new data and modifications. Maybe the technique you put online is a general purpose RNA sequence analysis tool that works as long as you feed it properly formatted data, and that’s something others would have had to code from scratch in order to take advantage of some platforms.

Well, they can just clone your capsule, run it with their own data and get their own results in addition to verifying your own. This can be done via the Code Ocean website or just by downloading a zip file of the whole thing and getting it running on their own computer, if they happen to have a compatible setup. A few more example capsules can be found here.

Image Credits: Code Ocean

This sort of cross-pollination of research techniques is as old as science, but modern data-heavy experimentation often ends up siloed because it can’t easily be shared and verified even though the code is technically available. That means other researchers move on, build their own thing and further reinforce the silo system.

Right now there are about 2,000 public compute capsules on Code Ocean, most of which are associated with a published paper. Most have also been used by others, either to replicate or try something new, and some, like ultra-specific open source code libraries, have been used by thousands.

Naturally there are security concerns when working with proprietary or medically sensitive data, and the enterprise product allows the whole system to run on a private cloud platform. That way it would be more of an internal tool, and at major research institutions that in itself could be quite useful.

Code Ocean hopes that by being as inclusive as possible in terms of codebases, platforms, compute services and so on will make for a more collaborative environment at the cutting edge.

Clearly that ambition is shared by others, as the the company has raised $21 million so far, $6 million of which was in previously undisclosed investments and $15 million in an A round announced today. The A round was led by Battery Ventures, with Digitalis Ventures, EBSCO and Vaal Partners participating as well as numerous others.

The money will allow the company to further develop, scale and promote its platform. With luck they’ll soon find themselves among the rarefied air often breathed by this sort of savvy SaaS — necessary, deeply integrated and profitable.

Powered by WPeMatico

HoneyBook, which has built out a client experience and financial management platform for service-based small businesses and freelancers, announced today that it has raised $155 million in a Series D round led by Durable Capital Partners LP.

Tiger Global Management, Battery Ventures, Zeev Ventures, 01 Advisors as well as existing backers Norwest Venture Partners and Citi Ventures also participated in the financing, which brings the San Francisco-based company’s valuation to over $1 billion. With the latest round, HoneyBook has now raised $248 million since its 2013 inception. The Series D is a big jump from the $28 million that HoneyBook raised in March 2019.

When the COVID-19 pandemic hit last year, HoneyBook’s leadership team was concerned about the potential impact on their business and braced themselves for a drop in revenue.

Rather than lay off people, they instead asked everyone to take a pay cut, and that included the executive team, who cut theirs “by double” the rest of the staff.

“I remember it was terrifying. We knew that our customers’ businesses were going to be impacted dramatically, and would impact ours at the same time dramatically,” recalls CEO Oz Alon. “We had to make some hard decisions.”

But the resilience of HoneyBook’s customer base surprised even the company, who ended up reinstating those salaries just a few months later. And, as corporate layoffs driven by the COVID-19 pandemic led to more people deciding to start their own businesses, HoneyBook saw a big surge in demand.

“Our members who saw a hit in demand went out and found demand in another thing,” Oz said. As a result, HoneyBook ended up doubling its number of members on its SaaS platform and tripling its annual recurring revenue (ARR) over the past 12 months. Members booked more than $1 billion in business on the platform in the past nine months alone.

HoneyBook combines on its platform tools like billing, contracts and client communication, with the goal of helping business owners stay organized. Since its inception, service providers across the U.S. and Canada such as graphic designers, event planners, digital marketers and photographers have booked more than $3 billion in business on its platform. And as the pandemic had more people shift to doing more things online, HoneyBook prepared to help its members adapt by being armed with digital tools.

Image Credits: HoneyBook

“Clients now expect streamlined communication, seamless payments, and the same level of exceptional service online that they were used to receiving from business owners in person,” Alon said.

Oz co-founded HoneyBook with wife Naama and longtime friend Dror Shimoni. Oz and Naama were both small business owners themselves at one time, so they had firsthand insight on the pain points of running a service-based business.

HoneyBook’s software not only helps SMBs do more business, but helps them “convert potentials to actual clients,” Oz said.

“We help them communicate with potential clients so they can win their business, and then help them manage the relationship so they can keep them,” Naama said.

The company plans to use its new capital toward continued product development and to “dramatically” boost its 103-person headcount across its New York and Tel Aviv offices.

“We’re seeing so much demand for additional services and products, so we definitely want to invest and create better ways for our members to present themselves online,” Alon told TechCrunch. “We’re also seeing demand for financial products and the ability to access capital faster. So that’s just a few of the things we plan to invest in.”

The company also wants to make its platform “more customizable” for different categories and verticals.

Chelsea Stoner, general partner at Battery Ventures, said her firm recognized that the expansive market of productivity tools to serve small businesses and entrepreneurs was “a market of discrete and separate productivity tools.”

HoneyBook, she said, is a true platform for SMBs, “providing a huge array of functionality in one cohesive UX.”

“It unites and connects every task for the solopreneurs, from creating and distributing marketing collateral, to organizing and executing proposals, to sending invoices and collecting payments,” Stoner said. “The company is constantly innovating and iterating in response to its members; we also see a lot of opportunity with payments going forward…And, due to COVID-19 and other factors, the company is sitting on pent-up demand that will accelerate growth even more.”

Powered by WPeMatico

More than half a decade ago, my Battery Ventures partner Neeraj Agrawal penned a widely read post offering advice for enterprise-software companies hoping to reach $100 million in annual recurring revenue.

His playbook, dubbed “T2D3” — for “triple, triple, double, double, double,” referring to the stages at which a software company’s revenue should multiply — helped many high-growth startups index their growth. It also highlighted the broader explosion in industry value creation stemming from the transition of on-premise software to the cloud.

Fast forward to today, and many of T2D3’s insights are still relevant. But now it’s time to update T2D3 to account for some of the tectonic changes shaping a broader universe of B2B tech — and pushing companies to grow at rates we’ve never seen before.

One of the biggest factors driving billion-dollar B2Bs is a simple but important shift in how organizations buy enterprise technology today.

I call this new paradigm “billion-dollar B2B.” It refers to the forces shaping a new class of cloud-first, enterprise-tech behemoths with the potential to reach $1 billion in ARR — and achieve market capitalizations in excess of $50 billion or even $100 billion.

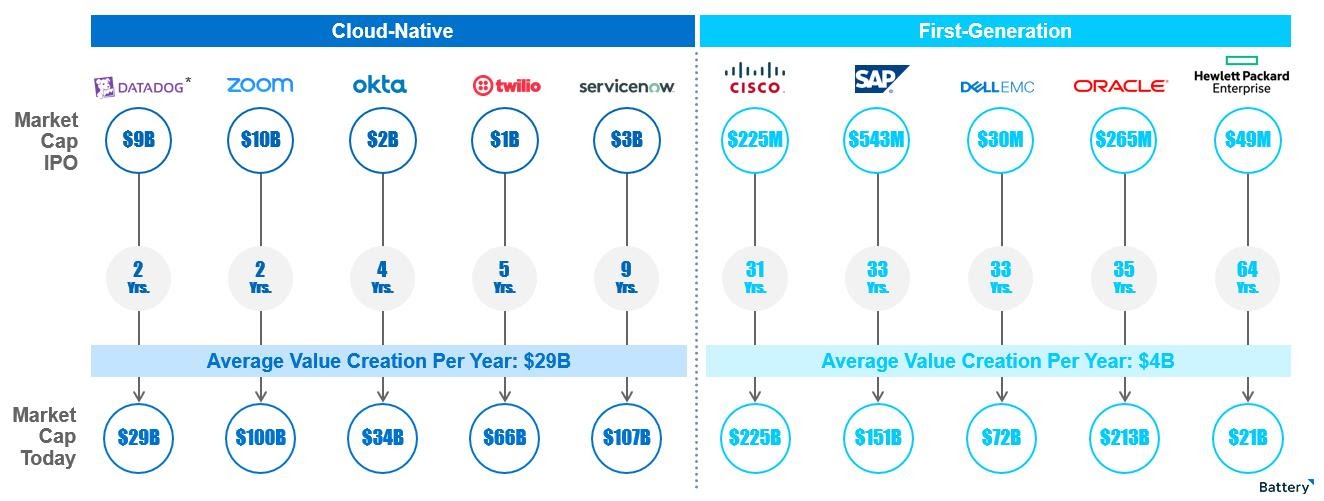

In the past several years, we’ve seen a pioneering group of B2B standouts — Twilio, Shopify, Atlassian, Okta, Coupa*, MongoDB and Zscaler, for example — approach or exceed the $1 billion revenue mark and see their market capitalizations surge 10 times or more from their IPOs to the present day (as of March 31), according to CapIQ data.

More recently, iconic companies like data giant Snowflake and video-conferencing mainstay Zoom came out of the IPO gate at even higher valuations. Zoom, with 2020 revenue of just under $883 million, is now worth close to $100 billion, per CapIQ data.

Image Credits: Battery Ventures via FactSet. Note that market data is current as of April 3, 2021.

In the wings are other B2B super-unicorns like Databricks* and UiPath, which have each raised private financing rounds at valuations of more than $20 billion, per public reports, which is unprecedented in the software industry.

Powered by WPeMatico

Teamflow, founded by ex-Uber manager Flo Crivello, has raised an $11 million Series A just three months after raising a $3.9 million seed for its virtual HQ platform. The latest round in the startup was led by Battery Ventures, with Menlo Ventures leading its previous financing event.

Teamflow’s raise comes just days after competitor Gather announced a $26 million Series A round led by Sequoia Capital. Another company, Branch, has raised a $1.5 million seed round from investors such as Homebrew and Gumroad’s Sahil Lavingia and is currently raising its Series A.

All these startups want to bring into the mainstream a game-like interface for people to toggle through during their work day. The reality is, all three companies (and dozens of others) likely can’t win. The winning difference lies in strategy, Teamflow’s Crivello tells me.

“I think in the early days, the biggest differentiator is going to be UX and our aesthetic,” he said. “A lot of the other players have a very gamified approach, and we’re big fans of that, but we think that people don’t want to have their [work] meetings in a Pokémon game.”

A tour through Teamflow’s office shows that the company is more focused on productivity than gamification. Integrations include a Slack-like chat feature as well as file and image sharing. It is working on an in-platform app store so users can download the integrations that work best with their team, Crivello said. There are games too.

Teamflow’s virtual HQ platform.

This focus has helped Teamflow gain traction with employers instead of event organizers, a more stable source of revenue per the founder. The company currently hosts thousands of teams within startups on its platform, wracking in “hundreds of thousands of dollars in revenue.” Gather, a competitor, recently told TechCrunch that it gets the majority of its revenue from one-off events. Gather’s monthly revenue is currently $400,000, according to founder Philip Wang.

Gather, alternatively, looks and feels very different from Teamflow in that it is closer to the feel of Sims.

Gather’s virtual HQ platform.

Branch’s Dayton Mills said that it has been able to stay competitive through becoming “much more gamified.” It has added levels, in-game currencies and XP to encourage employees to customize their office space.

“Productivity isn’t broken, but culture, fun and social interaction is,” Mills told TechCrunch. “So when it comes to work and play we’re aiming to fix the play part, not the work. Work comes as a side effect.” Branch has not made revenue yet.

The next ambition for Teamflow is expanding its customer base beyond the hip experimental team at startups. Crivello noted that Zoom brings in about 40% of its revenue through enterprise sales, and Teamflow is resultedly “doubling down on enterprise readiness.”

The company will work on being compliant and upholding privacy standards so it can onboard healthcare and biotech companies, what it views as “buttoned up verticals” that might not want the other gamified approaches.

Crivello is clear about his vision for the startup: He wants to make it harder to move out of a virtual office than a physical office. If Teamflow can become an operating system of sorts long-term, adding on applications and bringing in a high quality of standards, it might be able to bring on a broader set of clients.

Powered by WPeMatico

We’re not digging into another IPO filing today. You can read all about AppLovin’s filing here, or ThredUp’s document here.

This morning, instead, we’re talking about an old favorite: software valuations. The folks over at Battery Ventures have compiled a lengthy dive into the 2020 software market that’s worth our time — you can read along here; I’ll provide page numbers as we go — because it helps explain some software valuations.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

There’s little doubt that there is some froth in the software market, but it may not be where you think it is.

The Battery report has a lot of data points that we’ll also work through in this week’s newsletter, but this morning, let’s narrow ourselves to thinking about rising aggregate software multiples, the breakdown of multiples expansion through the lens of relative growth rates, and cap it off with a nibble on the importance, or lack thereof, of cash flow margins for the valuation of high-growth software companies.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

I chatted through pieces of the report with its authors, Battery’s Brandon Gleklen and Neeraj Agrawal. So, we’ll lean on their perspective a little as we go to help us move quickly. This is our Friday treat. Or at least mine. Let’s get into it.

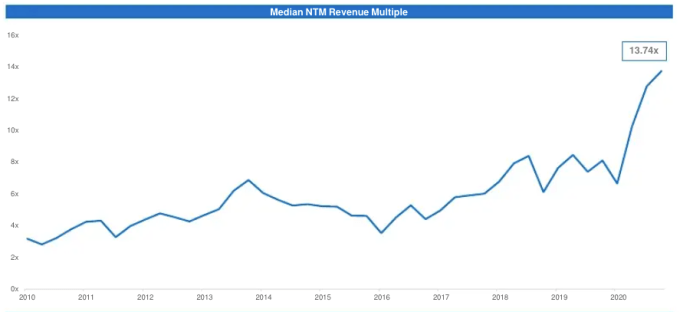

Let’s start with an affirmation. Yes, software valuations have risen to record-high multiples in recent years. Here’s the Battery chart that makes the change clear:

Page 31, Battery report. Image Credits: Battery Ventures

Powered by WPeMatico

EquityBee, a stock option marketplace startup, has raised $20 million in a Series A round of funding.

Group 11 led the financing, which also included participation from Oren Zeev Ventures, Battery Ventures and ICON Continuity Fund. It brings the company’s total raised to over $28 million since its 2018 inception.

EquityBee CEO and co-founder Oren Barzilai says his company’s mission is to help educate startup employees on the meaning of their stock options, as well as provide them with funds to be able to purchase them.

“I have seen many of my friends and colleagues negotiate a $500 salary increase, but completely disregard their stock options package, from lack of knowledge due to the whole field of startup stock options being opaque,” said Barzilai, who also founded Tapingo, which was acquired by Grubhub in 2018 for $150 million. “As a founder I saw my team members who helped build the company not take part in our success because they left prematurely and didn’t exercise their stock options.”

The way it works is fairly straightforward. EquityBee provides capital to startup employees so they can purchase stock options. The employees get money to cover the cost of exercising their stock options and the taxes. The investors who helped provide the funding so they could do that get a return, or a share of the profit, if there’s “a liquidity event.” EquityBee makes money by charging an upfront fee from the investor on the investment day, as well as any carried interest upon a successful exit or IPO.

Barzilai said that many employees don’t realize they have about 90 days to exercise options before they expire once they leave a company. And even if they do, they may not always have the money to exercise them. That’s where EquityBee wants to help.

The company was originally founded in Israel before launching in the U.S. market, and moved its headquarters to Silicon Valley in February 2020. Since then, it’s funded employees from “hundreds” of companies, including Airbnb, Palantir, DoorDash and Unity, with capital provided by family offices, funds and high-net individuals. Its investor community is made up of 8,000 funds, family offices and high-net worth individuals.

2020 was a good year for EquityBee, according to Barzilai, who says it grew by more than 560% the amount of money it raised to fund employee stock options. It also saw a 360% increase in the number of individual employees funded through its platform.

Looking ahead, the 33-person company plans to use the money toward hiring and expanding product offerings.

Dovi Frances, founding partner of Group 11, said it doubled down on EquityBee after backing the company in its $6.6 million funding round in February 2020 because it’s impressed by what it described as the company’s “perfect product market fit” and triple-digit growth.

WeWork co-founder Adam Neumann led the company’s $1.5 million seed round in September of 2018.

Powered by WPeMatico

SLAs, SLOs, SLIs. If there’s one thing everybody in the business of managing software development loves, it’s acronyms. And while everyone probably knows what a Service Level Agreement (SLA) is, Service Level Objectives (SLOs) and Service Level Indicators (SLIs) may not be quite as well known. The idea, though, is straightforward, with SLOs being the overall goals a team must hit to meet the promises of its SLA agreements, and SLIs being the actual measurements that back up those other two numbers. With the advent of DevOps, these ideas, which are typically part of a company’s overall Site Reliability Engineering (SRE) efforts, are becoming more mainstream, but putting them into practice isn’t always straightforward.

Nobl9 aims to provide enterprises with the tools they need to build SLO-centric operations and the right feedback loops inside an organization to help it hit its SLOs without making too many trade-offs between the cost of engineering, feature development and reliability.

The company today announced that it has raised a $21 million Series B round led by its Series A investors Battery Ventures and CRV. In addition, Series A investors Bonfire Ventures and Resolute Ventures also participated, together with new investors Harmony Partners and Sorenson Ventures.

Before starting Nobl9, co-founders Marcin Kurc (CEO) and Brian Singer (CPO) spent time together at Orbitera, where Singer was the co-founder and COO and Kurc the CEO, and then at Google Cloud, after it acquired Orbitera in 2016. In the process, the team got to work with and appreciate Google’s site reliability engineering frameworks.

As they started looking into what to do next, that experience led them to look into productizing these ideas. “We came to this conclusion that if you’re going into Kubernetes, into service-based applications and modern architectures, there’s really no better way to run that than SRE,” Kurc told me. “And when we started looking at this, naturally SRE is a complete framework, there are processes. We started looking at elements of SRE and we agreed that SLO — service level objectives — is really the foundational part. You can’t do SRE without SLOs.”

As Singer noted, in order to adopt SLOs, businesses have to know how to turn the data they have about the reliability of their services, which could be measured in uptime or latency, for example, into the right objectives. That’s complicated by the fact that this data could live in a variety of databases and logs, but the real question is how to define the right SLOs for any given organization based on this data.

“When you go into the conversation with an organization about what their goals are with respect to reliability and how they start to think about understanding if there’s risks to that, they very quickly get bogged down in how are we going to get this data or that data and instrument this or instrument that,” Singer said. “What we’ve done is we’ve built a platform that essentially takes that as the problem that we’re solving. So no matter where the data lives and in what format it lives, we want to be able to reduce it to very simply an error budget and an objective that can be tracked and measured and reported on.”

The company’s platform launched into general availability last week, after a beta that started last year. Early customers include Brex and Adobe.

As Kurc told me, the team actually thinks of this new funding round as a Series A round, but because its $7.5 million Series A was pretty sizable, they decided to call it a Series A instead of a seed round. “It’s hard to define it. If you define it based on a revenue milestone, we’re pre-revenue, we just launched the GA product,” Singer told me. “But I think just in terms of the maturity of the product and the company, I would put us at the [Series] B.”

The team told me that it closed the round at the end of last November, and while it considered pitching new VCs, its existing investors were already interested in putting more money into the company and since its previous round had been oversubscribed, they decided to add to this new round some of the investors that didn’t make the cut for the Series A.

The company plans to use the new funding to advance its roadmap and expand its team, especially across sales, marketing and customer success.

Powered by WPeMatico

The recent Databricks funding round, a $1 billion investment at a $28 billion valuation, was one of the year’s most notable private investments so far.

For Databricks signaled its IPO readiness by disclosing to TechCrunch last year that it had scaled its revenue run rate from $200 million to $350 million in a year, so the new capital looked like the capstone on its private fundraising before an eventual public debut.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But I did have a few questions, starting with the price of the round.

At a $28 billion valuation and ARR of $425 million, Databricks is valued at around 66x top line. That’s steep, if not the highest number we can dredge up on the public markets. Of course, for Databricks shareholders, seeing the value of their stock rise so quickly is hardly a bad thing. They are hardly going to complain about having more paper wealth.

But what about the investor perspective? Does the price really make sense? The Exchange caught up with Battery Ventures’ Dharmesh Thakker earlier this week to discuss a number of things, one of which was Databricks’ round and pricing. Thakker is named in the Databricks Series D funding announcement, which brought Battery into the company.

What was surprising about our conversation was not that Thakker was bullish on Databricks — a company that he and his firm have backed since its $140 million, 2017 round when the company was worth just under $1 billion. What surprised me was that he thinks its new $28 billion valuation might be a little low.

What was surprising about our conversation was not that Thakker was bullish on Databricks — a company that he and his firm have backed since its $140 million, 2017 round when the company was worth just under $1 billion. What surprised me was that he thinks its new $28 billion valuation might be a little low.

Intriguing, yeah? So this morning for both of us, I’ve pulled out quotes from our chat to help explain how Thakker views the market for Databricks, unicorns at scale more broadly through the lens of risk-adjusted investing, and the scale of the market some unicorns are playing in.

At the close, we’ll remind ourselves what Databricks CEO Ali Ghodsi told TechCrunch when we asked him the same question. Let’s go!

Here’s how the valuation part of my chat with the Battery Ventures’ investor went down:

The Exchange: I want to talk about Databricks, because I spoke to [CEO] Ali [Ghodsi] yesterday about this round, and hot damn, it’s a lot of money at a valuation that is roughly 64x ARR, give or take. I don’t understand the price, and I know it’s a boring thing to talk about. [It’s a] great company, I get their market, I’ve talked to them a bunch, I know their revenue numbers. [But] I don’t understand the price, and I was hoping you could tell me why I’m being too conservative.

Dharmesh Thakker: I, for what it’s worth, think [the price] fair. If anything, I think it is on the lower end — he could have done better, frankly. But I think it comes down to three major things, right?

One is the addressable market. Just think about the addressable market of data. If there’s a trillion dollars spent in software or technology, I think you and I would be both hard pressed to say, almost all of that [isn’t] influenced by some data-oriented decisioning. Whether it’s digital transformation, whether it’s analytics, data is everywhere. So the TAM is massive … I think you and I both agree on that, whether it is $20 billion or $80 billion — it’s massive.

Powered by WPeMatico

Productivity software has been getting a major re-examination this year, and human resources platforms — used for hiring, firing, paying and managing employees — have been no exception. Today, one of the startups that’s built what it believes is the next generation of how HR should and will work is announcing a big fundraise, underscoring its own growth and the focus on the category.

Hibob, the startup behind the HR platform that goes by the name of “bob” (the company name is pronounced, “Hi, Bob!”), has picked up $70 million in funding at a valuation that reliable sources close to the company tell us is around $500 million.

“Our mission is to modernize HR technology,” said Ronni Zehavi, Hibob’s CEO, who co-founded the company with Israel David. “We are a people management platform for how people work today. Whether that’s remotely or physically collaborative, our customers face challenges with work. We believe that the HR platforms of the future will not be clunky systems, annoying, giant platforms. We believe it should be different. We are a system of engagement rather than record.”

The Series B is being led by SEEK and Israel Growth Partners, with participation also from Bessemer Venture Partners, Battery Ventures, Eight Roads Ventures, Arbor Ventures, Presidio Ventures, Entree Capital, Cerca Partners and Perpetual Partners, the same group that also backed Hibob in its last round (a Series A extension) in 2019. It has raised $124 million to date.

The company has its roots in Israel but these days describes its headquarters as London and New York, and the funding comes on the back of strong growth in multiple markets. In an interview, Zehavi said that Hibob specialises in the mid-market customers and says that it has more than 1,000 of them currently on its books across the U.S., Europe and Asia, including Monzo, Revolut, Happy Socks, ironSource, Receipt Bank, Fiverr, Gong and VaynerMedia. In the last year Hibob has had “triple-digit” year-on-year growth (it didn’t specify what those digits are).

Human resources has never been at the more glamorous end of how a company works, and it can sometimes even be looked on with some disdain. However, HR has found itself in a new spotlight in 2020, the year when every company — whether one based around people sitting at desks or in more interactive and active environments — had to change how it worked.

That might have involved sending everyone home to sign in from offices possibly made out of corners of bedrooms or kitchens, or that might have involved a vastly different set of practices in terms of when and where workers showed up and how they interacted with people once they did. But regardless of the implementations, they all involved a team of people who needed to be linked together, still feeling connected and managed; and sometimes hired, furloughed, or let go.

That focus has started to reveal the strains of how some legacy systems worked, with older systems built to consider little more than creating an employee identity number that could then be tracked for payroll and other purposes.

Hibob — Zehavi said they chose the name after the person who owned the bob.com domain wanted too much to sell it, but they liked “bob” for the actual product — takes an approach from the ground up that is in line with how many people work today, balancing different software and apps depending on what they are doing, and linking them up by way of integrations: its own includes Slack, Microsoft Teams and Mercer, and other packages that are popular with HR departments.

While it covers all of the necessary HR bases like payroll and further compensation, onboarding, managing time off and benefits, it further brings in a variety of other features that help build out bigger profiles of users, such as performance and culture, with the ability for peers, managers and workers themselves to provide feedback to enhance their own engagement with the company, and for the company to have a better idea of how they are fitting into the organization, and what might need more attention in the future.

That then links into a bigger organizational chart and conceptual charts that highlight strong performers, those who are possible flight risks, those who are leaders and so on. While there have been a number of others in the HR world that have built standalone apps that cover some of these features (for example, 15five was early to spot the value of a platform that made it much easier to set goals and provide feedback), what’s notable here is how they are all folded into one system together.

The end effect, as you can see here, looks less like word salad and more interactive, graphic interfaces that are presumably a lot more enjoyable and at least easier to use for HR people themselves.

The importance for investors has been that the product and the startup has identified the opportunity, but has delivered not just more engagement, but a strong piece of software that still provides the essentials.

“This is certainly not a Workday,” said Adam Fisher, a partner at Bessemer, in an interview. “Our overall thesis has been that HR is only growing in importance. And while engagement is super important, that opportunity is not enough to create the market.”

The end result is a platform that has a significant shot at building in even more over time. For example, another large area that has been seeing traction in the world of enterprise and B2B software is employee training. Specifically, enterprise learning systems are creating another way to help keep people not only up to speed on important aspects of how they work, but also engaged at a time when connections are under strain.

“Training, a SuccessFactors -style offering, is definitely in our road map,” said Zehavi, who noted they are adding new features all the time. The latest has been compensation, sometimes known as merit increase cycles. “That is a very complex issue and requires deeper integrations finance and the CFO’s office. We streamlined it and made it easy to use. We launched two months ago and it’s on fire. After learning and development there are other modules also down the road.”

Powered by WPeMatico