Airbnb

Auto Added by WPeMatico

Auto Added by WPeMatico

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

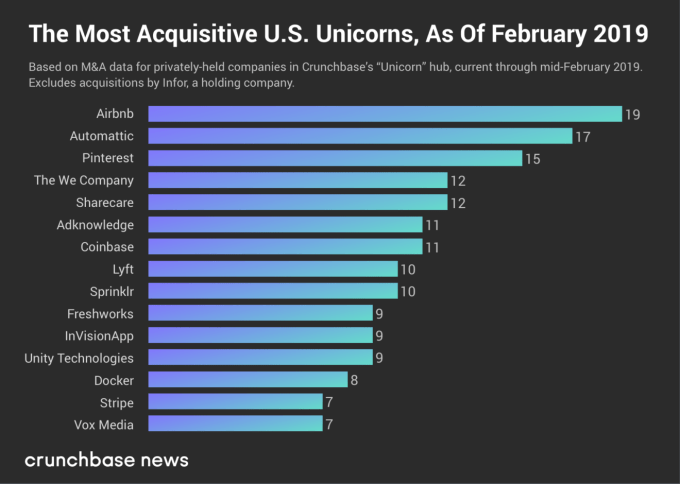

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

The City of Paris first warned Airbnb, and it is now taking action. The mayor of Paris, Anne Hidalgo, told the JDD that the city is suing the company for 1,010 illegal listings. The fine could be worth as much as $14.2 million (€12.625 million).

Based on current legislation, you can’t rent an apartment more than 120 days a year. If you want to rent an apartment on Airbnb in Paris, you first must register your apartment with the city. The city then gives you an ID number so they can track how many nights you’re listing your apartment on Airbnb.

And yet, many listings still don’t have that ID number. The mayor’s office flagged around 1,000 apartments back in December 2017 and said Airbnb was dragging its feet. The company had little incentive to comply, as hosts were responsible for their own listings.

Thanks to a new law, the responsibility is now shared between the hosts and the platform. The City of Paris can now fine Airbnb for all those illegal listings, up to €12,500 per listing.

According to Hidalgo, Airbnb has been putting too much pressure on the housing market. She thinks that 65,000 apartments are now reserved for Airbnb in Paris alone. In some areas, it has become quite hard to find an apartment because of that. Local shops also suffer because tourists have different needs. In addition to better monitoring, Hidalgo is also in favor of restricting listings to 30 nights per year.

Airbnb told the JDD that it has complied with regulations and informed all Airbnb hosts about the new rules. The company also says that regulation in Paris doesn’t comply with European regulation. It’s clear that this fight is not over.

Powered by WPeMatico

I spent the week in Malibu attending Upfront Ventures’ annual Upfront Summit, which brings together the likes of Hollywood, Silicon Valley and Washington, DC’s elite for a two-day networking session of sorts. Cameron Diaz was there for some reason, and Natalie Portman made an appearance. Stacey Abrams had a powerful Q&A session with Lisa Borders, the president and CEO of Time’s Up. Of course, Gwyneth Paltrow was there to talk up Goop, her venture-funded commerce and content engine.

“I had no idea what I was getting into but I am so fulfilled and on fire from this job,” Paltrow said onstage at the summit… “It’s a very different life than I used to have but I feel very lucky that I made this leap.” Speaking with Frederic Court, the founder of Felix Capital, Paltrow shed light on her fundraising process.

“When I set out to raise my Series A, it was very difficult,” she said. “It’s great to be Gwyneth Paltrow when you’re raising money because people take the meeting, but then you get a lot more rejections than you would if they didn’t want to take a selfie … People, understandably, were dubious about [this business]. It becomes easier when you have a thriving business and your unit economics looks good.”

In other news…

The actor stopped by the summit to promote his startup, HitRecord . I talked to him about his $6.4 million round and grand plans for the artist-collaboration platform.

Backed by GV, Sequoia, Floodgate and more, Clover Health confirmed to TechCrunch this week that it’s brought in another round of capital led by Greenoaks. The $500 million round is a vote of confidence for the business, which has experienced its fair share of well-publicized hiccups. More on that here. Plus, Clutter, the startup that provides on-demand moving and storage services, is raising at least $200 million from SoftBank, sources tell TechCrunch. The round is a big deal for the LA tech ecosystem, which, aside from Snap and Bird, has birthed few venture-backed unicorns.

Pinterest, the nine-year-old visual search engine, has hired Goldman Sachs and JPMorgan Chase as lead underwriters for an IPO that’s planned for later this year. With $700 million in 2018 revenue, the company has raised some $1.5 billion at a $12 billion valuation from Goldman Sachs Investment Partners, Valiant Capital Partners, Wellington Management, Andreessen Horowitz, Bessemer Venture Partners and more.

Kleiner Perkins went “back to the future” this week with the announcement of a $600 million fund. The firm’s 18th fund, it will invest at the seed, Series A and Series B stages. TCV, a backer of Peloton and Airbnb, closed a whopping $3 billion vehicle to invest in consumer internet, IT infrastructure and services startups. Partech has doubled its Africa VC fund to $143 million and opened a Nairobi office to complement its Dakar practice. And Sapphire Ventures has set aside $115 million for sports and entertainment bets.

The co-founder of Y Combinator will throw a sort of annual weekend getaway for nerds in picturesque Boulder, Colo. Called the YC 120, it will bring toget her 120 people for a couple of days in April to create connections. Read TechCrunch’s Connie Loizos’ interview with Altman here.

Consumer wellness business Hims has raised $100 million in an ongoing round at a $1 billion pre-money valuation. A growth-stage investor has led the round, with participation from existing investors (which include Forerunner Ventures, Founders Fund, Redpoint Ventures, SV Angel, 8VC and Maverick Capital) . Our sources declined to name the lead investor but said it was a “super big fund” that isn’t SoftBank and that hasn’t previously invested in Hims.

Five years after Andreessen Horowitz backed Oculus, it’s leading a $68 million Series A funding in Sandbox VR. TechCrunch’s Lucas Matney talked to a16z’s Andrew Chen and Floodgate’s Mike Maples about what sets Sandbox apart.

Here’s your weekly reminder to send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

In a new class-action lawsuit, a former Munchery facilities worker is claiming the startup owes him and 250 other employees 60 days’ wages. On top of that, another former employee says the CEO, James Beriker, was largely absent and is to blame for Munchery’s downfall. If you haven’t been keeping up on Munchery’s abrupt shutdown, here’s some good background.

Consolidation in the micromobility space has arrived — in Brazil, at least. Not long after Y Combinator-backed Grin merged its electric scooter business with Brazil-based Ride, it’s completing another merger, this time with Yellow, the bike-share startup based in Brazil that has also expressed its ambitions to get into electric scooters.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm, TechCrunch’s Silicon Valley editor Connie Loizos and Jeff Clavier of Uncork Capital chat about $100 million rounds, Stripe’s mega valuation and Pinterest’s highly anticipated IPO.

Powered by WPeMatico

When considering the structural impact of technology companies on our economy and society, we tend to focus on questions of scale and monopoly.

It’s true that the FAANG companies and more recent winners (Airbnb, Uber) have surfed a combination of network effects, preferential access to capital and classic efficiencies of scale to generate tremendous value for their shareholders — to the detriment of new entrants who attempt to unseat them.

At their high water mark in mid-2018, FAANG alone made up 11 percent of the total market cap of the S&P 500 and 38 percent of the index’s year-to-date gain, representing a doubling in their influence in only five years. The question of regulating technology companies — to the point of instituting anti-trust actions — has even become a rare point of relative concord between Democrats and Republicans in Congress.

But is the narrative of tech companies in the 2010s only a story of economic consolidation and growing inequality? Many of the most successful B2B startups of the last decade are aligned by a theme that paints a different picture. By transforming the nature of the costs required to start a business, these startups are reducing the influence of capital and leveling the playing field for new entrants to share in the surplus generated by the secular shift to a tech-mediated economy.

Source: Getty Images/MIKIEKWOODS

What do AWS, WeWork, Stord, Gusto

But they are alike in the economic purpose they serve for their customers. Each of these services takes a fixed cost — a bank of servers, a lease, a legal retainer — and transforms it into a variable cost. As a refresher, a fixed cost stays constant regardless of output, and variable costs scale with the output of a business.

When my father started his software consulting business in the early 1990s, I remember the giant boxes of AIX servers that arrived at our apartment, and tagging along to office tours in central New Jersey before he decided to run the company out of our spare bedroom. Back then, starting almost any kind of business was hard because of high fixed costs. Without AWS or WeWork, you shelled out upfront for hardware and a lease.

Access to capital, whether in the form of a bank loan, savings or friends and family was a prerequisite for entrepreneurship.

Today, startups make it possible to start and scale almost any kind of business while incurring few fixed costs. Want to found an e-commerce store? Start with a free Shopify account and dropship your inventory. Want to become a freelance designer? Put a shingle up on Fiverr and meet clients at a Breather you rent by the hour.

Whether software or hardware or labor, building a business is way easier when overhead is transformed into a string of flexible microservices that you only pay for as you grow.

Image courtesy of Getty Images

Taken together, startups that turn fixed costs into variable costs make it less capital-intensive to start a business. This decreases the influence of gatekeepers and aggregators of capital — an impact evident in the way entrepreneurs think about starting businesses today.

It’s no coincidence that the rise of B2B startups fitting this theme has coincided with the bootstrap movement, in which tech entrepreneurs with major ambitions demur from raising venture funding because — well, they don’t need the money anymore.

It has also coincided with a renaissance in freelance entrepreneurship: 56.7 million Americans freelanced in 2018. Beyond the economic benefits of working for yourself — the fastest growing segment of freelancers earns more than $75,000 a year — freelancers can access the lifestyle and health benefits of owning their destiny, which aren’t directly captured but play a role in the economic picture. Indeed, 51 percent of freelancers said no amount of money would lure them into a traditional job, and 64 percent reported feeling healthier and happier.

When capital plays a reduced role in new business formation, access to capital plays a smaller role in determining who will succeed. More companies are founded, and the economy becomes more likely to birth new Davids that will unseat the Goliaths. Economics 101: lower barriers to entry create markets that converge on perfect competition instead of oligarchic concentration.

Source: Getty Images/ERHUI1979

Variable costs have their downsides. A startup with a relatively higher proportion of fixed costs — the profile of the classic high-tech software business — can achieve higher profit margins as it scales. Compare Microsoft or Google, which pay high fixed costs in the form of salaries and servers but few costs in delivering their services and achieve operating margins of 25-30 percent, to Costco, which takes in more than $100 billion of annual revenue but earns an operating margin in the single digits.

That’s OK. Neither type of cost is “better” or “worse,” but having the option to decide how to structure costs through a company’s life cycle can meaningfully impact an entrepreneur’s ability to execute a business idea.

Founders investigating startup ideas — and politicians debating the impact of technology — would do well to pay attention to how B2B companies have democratized access to entrepreneurship.

Powered by WPeMatico

If you’re down in ///joins.slides.predict you may want to visit ///history.writing.closets, or if you’ve got a little money to spend, try the Bananas Foster at ///cattle.excuse.luggage. Either way, don’t forget to stop by ///plotting.nest.reshape before you fly out.

If things go what3words’ way, that’s how you’ll be sending out addresses in the future. Founded by musician Chris Sheldrick and Cambridge mathematician Mohan Ganesalingam, the company has cut the world into three meter boxes that are identified by three words. Totonno’s Pizzeria in Brooklyn is at ///cats.lots.dame, while the White House is at ///kicks.mirror.tops. Because there are only three words, you can easily find spots that have no addresses and without using cumbersome latitude and longitude coordinates.

The team created this system after finding that travelers found it almost impossible to find some out-of-the-way places. Tokyo, for example, is notoriously difficult to traverse via address, while other situations — renting a Yurt in Alaska, for example — require constantly updated addresses that do not lend themselves to GPS coordinates. Instead, you can tell your driver to take you to ///else.impulse.broom and be done with it.

The team has raised £40 million and is currently working on systems to add their mapping API to industrial and travel partners. You can browse the map here.

“I organized live music events around the world. Often in rural places. HeIfound equipment, musicians and guests got lost. We tried to give coordinates but they were impossible to remember and communicate accurately,” said Sheldrick. “This is the only address solution designed for voice, and the only system using words and not alphanumeric codes.”

Obviously this will take some getting used to. The three words might get mispronounced, leading to some fun problems, but in general it might be a good to way to get around the world in a post-modern way. After all, some of the spot names sound like poetry, and if you don’t like it you can always just go to ///drills.dandelions.bounds.

Powered by WPeMatico

It was several years ago, at a tech conference in Laguna Beach, Calif., that the venture capitalist Bill Gurley issued one of what would become repeated warnings that startups were staying private too long. Comparing companies that refuse to go public to undergrads whose college careers extend several years past the point that they should, Gurley suggested they should be embarrassed, not proud, for keeping their shares in private hands. “Until you get liquid, you really haven’t accomplished anything,” Gurley said.

Whether Gurley was referring to Uber at the time, only he knows. Though his firm, Benchmark, eventually forced out Travis Kalanick, the co-founder and longtime CEO of Uber, the tipping point was seemingly not Kalanick’s determination to keep Uber privately held as long as possible, but rather an investigation into sexual harassment investigations and the employee misconduct that was discovered in the process.

Either way, it’s looking increasingly like Gurley had a point. As you may have noticed if you care anything about the public markets, they took a nosedive today. In fact, they fell to a new low for the year this afternoon, a reaction in part to the Federal Reserve’s decision earlier today to raise its benchmark overnight lending rate for the fourth time in 2018.

The Fed also signaled minimal rate hikes for next year — forecasting two rate hikes instead of three — but investors were apparently hoping for even better news.

It’s hard to blame them for seeking out more of a silver lining, given everything else that’s going on. Tech stocks are getting battered, with the FANG companies (Facebook, Apple, Netflix and Google) down meaningfully from their share prices of six months ago. (Amazon has held up the best.)

The economy of China — the U.S.’s third largest export partner and its largest import partner — is slowing sharply, which is expected to have an impact on the U.S. and world economies. Add trade tensions into the mix, a sprinkling of uncertainty about regulations, a splash of a possible government shutdown and the growing prospect that Donald Trump will be impeached, and you start to appreciate why the market is finally going off the rails.

Despite so much uncertainty, Uber, Lyft, Slack and now Pinterest, among many others, are racing to become publicly traded at long last. According to Dealogic data quoted in today’s WSJ, 38 unicorn companies went public this year, and more are expected to test the market in 2019. Their venture backers will tell you it’s because the markets recognize a strong growth company when they see it, and that each is finally positioned well to tell their story, aided by some dazzling metrics. Yet it seems just as likely that they see the window, which flew open this year, starting to swing back in the other direction. And if this month is any indicator, it could be hard to pry it open again, at least in the first quarter or two.

“The market is basically closed between now, and the start of a new year is always slow because companies don’t start roadshows [until the markets re-open],” says Kathleen Smith, a principal of Renaissance Capital and the manager of its IPO exchange-traded fund. Pre-IPO companies like Uber are also waiting on their audits to close before they put any numbers in a public document, she notes. But it could be far from smooth sailing after that, suggests Smith. “In normal times, late January and February and March become very active, but we aren’t in a typical market. I can predict from other times that we’ve seen a bear market like this that it will have an impact on IPO activity.”

It’s all part of a vicious cycle, Smith suggests. As public market shareholders begin to feel less affluent and more risk averse, they start redeeming their public market shares. That leaves fund managers who might otherwise gamble on new issuers with less capital to invest, and less flexibility. “Investors are just not going to want to take on any risk positions when market has [taken a turn for the worse],” says Smith.

Put another way, if the markets are as crummy early next year as looks to be the case, it’s too bad, too sad for unicorn companies. “They made the choice to stay private and get capital,” says Smith. “I’ve stated many times that they should be getting while the getting is good. The pain can happen if money dries up, and it will dry up when the public market dries up.”

That doesn’t mean tech’s favorite unicorn companies are doomed, of course, especially those that can show strong fundamentals. For her part, Smith notes that what often happens in a downturn is that offerings get heavily discounted. “Valuations will be chopped if the companies want investors to participate. They’ll have to be sure to make money.”

Even if they don’t get the rich prices that ambitious bankers might pitch them (or that their VCs assigned them before that), they can always grow into the valuations their investors want to see. One need look no further than Facebook to remember why a bumpy offering doesn’t mean all that much longer term.

“Just because a stock crashes below its IPO price isn’t a sign of a bubble,” says Pivotal Research analyst Brian Wieser. “You also have to keep in mind the dynamic of companies going public,” he says. “You expect IPOs to be overvalued. Investors in these companies are necessarily selling to the greatest fool.”

Still, there may be fewer fools willing to buy what they are selling than there might have been this year or last, and if those numbers really change, today’s unicorns will look like tomorrow’s donkeys. They’re certainly going to face more scrutiny than they might have had they moved sooner.

“Maybe we’ll roar into 2019 and all will be well,” says Lise Buyer, the founder of Class V Group, an advisory firm for IPOs. “But to the extent that investors will be more selective, they’ll look at path to profitability, and they’ll look at the valuations these companies took when they were private.” Then they’ll do their own math, suggests Buyer.

If the market is truly shifting, public market shareholders “won’t care what valuations companies achieved when they were private,” says Buyer. “They’ll only be willing to pay what they are willing to pay.”

Powered by WPeMatico

The second wave of Internet-era travel companies has captured the attention of venture capitalists.

In the last five years, travel companies have raised more than $1 billion in venture capital funding. That includes short-term rental startups, travel and tourism apps, marketplaces for “experiences” and other travel or hospitality tech platforms. Airbnb, a $38 billion company and an anomaly in the category, has raised $3 billion in that same time frame, according to PitchBook.

In the last few months alone, aspiring Concur-competitor TripActions and travel activities platform Klook entered the “unicorn” club with large venture rounds that valued both of the businesses at more than $1 billion. Meanwhile, luggage maker Away raised $50 million at a $400 million valuation and smaller startups in the space like Freebirds, IfOnly, KKDay, Duffel and RedDoorz all closed modest funding rounds.

“Something is really happening in the industry; something bigger than us,” TripActions co-founder Ariel Cohen said in a recent conversation with TechCrunch about his company’s $154 million Series C financing. “Different startups are identifying the opportunity here and the fact that companies want to make sure their employees are happy while they are on the go. That’s why you see investments in companies like Brex and like TripActions.”

Brex, though not classified as a travel startup, lets startup employees earn extra points on business travel with its corporate credit card for startups. It recently raised a $125 million Series C at a $1.1 billion valuation.

Global travel and tourism is one of the most valuable industries worth some $7 trillion. The online travel market, in particular, is expected to grow to $817 billion by 2020. VCs are hunting for tech-enabled startups poised to dominate that slice.

“You have a new wave of businesses where all of that digital infrastructure is set up, so the focus can be on things like efficiency, improved customer service, scale and growth — you have a ton of companies popping up catering to those needs,” Defy Partners co-founder Neil Sequeira told TechCrunch. Sequeira was a managing director at General Catalyst when the firm made its first investment in Airbnb.

On the other hand, you have a whole cohort of travel business founded amid the dot-com boom that are looking to technology startups for a much-needed infusion of innovation. Many of those larger companies have become active acquirers, fueling VC interest in the space. SAP Concur, for example, acquired the formerly VC-backed travel-booking startup Hipmunk in 2016. Before that, it bought travel planning company TripIt for $120 million, among others.

Expedia has gobbled up a number of travel brands too, like travel photography community Trover; Airbnb-competitor HomeAway, which it paid a whopping $3.9 billion for in 2015; and most recently, both Pillow and ApartmentJet.

Many of these acquisitions are for peanuts, which is far from ideal for a venture-funded company. And building a travel business is cash intensive, hence the $4.4 billion Airbnb has raised to date or even TripActions’ $236 million in total VC funding. To keep momentum in the space, companies need to be striking larger M&A deals.

It doesn’t help that many in and around the venture capital industry are predicting an imminent turn in the market. Travel companies, which are reliant upon a consumer’s tendency to spend excess cash, will be among the first sectors to be impacted by hostile economic conditions.

“If the market turns, people aren’t going to spend $10,000 on a trip to Zimbabwe,” Sequeira said, referencing companies like IfOnly, which sells curated experiences.

Travel startups should raise now while the market is hot. The conditions may not remain favorable for long.

Powered by WPeMatico

Hotels can be pricey, and travelers are often forced to leave their rooms for basic things, like food that doesn’t come from the minibar. Yet Airbnb accommodations, which have become the go-to alternative for travelers, can be highly inconsistent.

Domio, a two-year-old, New York-based outfit, thinks there’s a third way: apartment hotels, or “apart hotels,” as the company is calling them.

The idea is to build a brand that travelers recognize as upscale yet affordable, more tech friendly than boutique hotels and features plenty of square footage, which it expects will appeal to both families as well as companies that send teams of employees to cities and want to do it more economically.

Domio has a host of competitors, if you’ll forgive the pun. Marriott International earlier this year introduced a branded home-sharing business called Tribute Portfolio Homes wherein it says it vets, outfits and maintains to hotel standards homes of its choosing. And Marriott is among a growing number of hotels to recognize that customers who stay in a hotel for a business trip or a family vacation might prefer a multi-bedroom apartment with hotel-like amenities.

Property management companies have been raising funding left and right for the same reason. Among them: Sonder, a four-year-old, San Francisco-based startup offering “spaces built for travel and life” that, according to Crunchbase, has raised $135 million from investors, much of it this year; TurnKey, a six-year-old, Austin, Tex.-based home rental management company that has raised $72 million from investors, including via a Series D round that closed back in March; and Vacasa, a nine-year-old, Portland, Ore.-based vacation rental management company that manages more than 10,000 properties and which just this week closed on $64 million in fresh financing that brings its total funding to $207.5 million.

That’s saying nothing of Airbnb itself, which has begun opening hotel-like branded apartment complexes that lease units to both long-term renters and short-term visitors in partnership with development partner Niido.

Whether Domio can stand out from competitors remains to be seen, but investors are happy to provide it the financing to try. The company is today announcing it has raised $12 million in Series A equity funding led by Tribeca Venture Partners, with participation from SoftBank Capital NY and Loric Ventures. The round comes on the heels of Domio announcing a $50 million joint venture last month with the private equity firm Upper 90 to exclusively fund the leasing and operations of as many as 25 apartment-style hotels for group travelers.

Indeed, Domio thinks one advantage it may have over other home-share companies is that rather than manage the far-flung properties of different owners, it can shave costs and improve the quality of its offerings by entering five- to 10-year leases with developers and then branding, furnishing and operating entire “apart hotel” properties. (It even has partners in China making its furniture.)

As CEO and former real estate banker Jay Roberts told us earlier this week, the plan is to open 25 of these buildings across the U.S. over the next couple of years. The units will average 1,500 square feet and feature two to three bedrooms, and, if all goes as planned, they’ll cost 10 to 25 percent below hotel prices, too.

And if the go-go property management market turns? Roberts insists that Domio can “slow down growth if necessary.” He also notes that “Airbnb was founded out of the recession, supported by people who were interested in saving money. We’re starting to see companies that want to be more cost-effective, too.”

Domio had earlier raised $5 million in equity and convertible debt from angel investors in the real estate industry; altogether it has now amassed funding of $67 million.

Powered by WPeMatico

Alumni Ventures Group’s (AVG) limited partners aren’t endowment or pension funds. Its typical LP is a heart surgeon in Des Moines, Iowa.

The firm has both an unorthodox model of fundraising and dealmaking. Across 25 micro funds, AVG is raising and investing upwards of $200 million per year for and in tech startups.

Tucked away in Boston, far from the limelight of Silicon Valley, few seem to be paying attention to AVG. There are a few reasons why, and those seem to be working to the firm’s advantage.

Today, AVG is announcing a close of roughly $30 million for three additional funds: Green D Ventures, Chestnut Street Ventures and Purple Arch Ventures, which represent capital committed by Dartmouth, the University of Pennsylvania and Northwestern alums, respectively.

AVG walks and talks like a venture fund, but a peek under the hood reveals its unconventional fundraising mechanisms.

Rather than collecting $5 million minimum investments from institutional LPs, AVG takes $50,000 directly from individual alums of prestigious universities. The firm pools the capital and creates university-specific venture funds for graduates of Duke, Stanford, Harvard, MIT and several other colleges.

“People don’t really know what to make of us because we’re so different,” said Michael Collins, AVG’s founder and chief executive officer.

Collins started AVG to make venture capital more accessible to individual people. He’s been a VC since 1986, formerly of TA Associates, and had grown tired of the hubris that runs rampant in the industry. In 2014, he started a $1.5 million fund for alums of his alma mater, Dartmouth. Since then, AVG has grown into 25 funds, each of which fundraise annually and are seeing substantial growth over their previous raises.

“What we observed is VC is a really good asset class but it’s really designed for institutional investors,” Collins (pictured below) said. “It’s really hard for individual people to put together a smart, simple portfolio unless they do it themselves. That’s why we created AVG.”

AVG and its team of 40 investment professionals make 150 to 200 investments per year of roughly $1 million each in U.S. startups across industries. In the second quarter of 2018, PitchBook listed the firm as the second most active global investor, ranked below only Plug and Play Tech Center and above the likes of Kleiner Perkins, NEA and Accel.

Unlike the Kleiners, NEAs and Accels of the world, AVG never leads investments. Collins says they just “tuck themselves into” a deal with a great lead investor. They don’t take board seats; Collins says he doesn’t see any value in more than one VC on a company board. And they don’t try to negotiate deal terms.

Though unusual, all of this works to their advantage. Founders appreciate the easy capital and access to AVG’s network, and other VC firms don’t view AVG as a threat, making it easier for the firm to get in on great deals.

“We are low friction, we are small and we have a hell of a Rolodex,” Collins said.

Despite a deal flow that’s unmatched by many VC firms, AVG manages to fly under the radar — and the firm is totally OK with that.

“A lot of VC is a bit of a star business where people try to build their own individual brand,” Collins said. “They get out there; they like publicity; they blog; they speak at conferences; they want to be known as the person to bring great deals to. We don’t lead. We work in the background. We just don’t feel the need to put the energy into PR.”

“Most VC returns are really achieved through investing in great companies as opposed to changing the trajectory of a company because you’re on the board,” he added. “If you’re a seed investor in Airbnb or Google, you were really great to be an early investor in that company, not because you sat on the board and you’re brilliance created Google’s success.”

AVG has completed 115 investments in the last 12 months. It’s investing out of 10-year funds, so at just four years in, it has some more waiting to do before it’ll see the full outcomes of its investments. Still, Collins says 65 of their portfolio companies have had liquidity events so far, including Jump, which sold to Uber in April, and Whistle, acquired by Mars Petcare a few years back.

“I hope that we can be a catalyst to bring more people into this asset class,” he concluded.

“I am a big believer that it’s really important that America continues to lead in entrepreneurship and I think the more people that own this asset class the better.”

Powered by WPeMatico

Only six months ago Barcelona-based TravelPerk bagged a $21 million Series B, off the back of strong momentum for a software as a service platform designed to take a Slack-like chunk out of the administrative tedium of arranging and expensing work trips.

Today the founders’ smiles are firmly back in place: TravelPerk has announced a $44 million Series C to keep stoking growth that’s seen it grow from around 20 customers two years ago to approaching 1,500 now. The business itself was only founded at the start of 2015.

Investors in the new round include Sweden’s Kinnevik, Russian billionaire and DST Global founder Yuri Milner and Tom Stafford, also of DST. Prior investors include the likes of Target Global, Felix Capital, Spark Capital, Sunstone, LocalGlobe and Amplo.

Commenting on the Series C in a statement, Kinnevik’s Chris Bischoff, said: “We are excited to invest in TravelPerk, a company that fits perfectly into our investment thesis of using technology to offer customers more and much better choice. Booking corporate travel is unnecessarily time-consuming, expensive and burdensome compared to leisure travel. Avi and team have capitalised on this opportunity to build the leading European challenger by focusing on a product-led solution, and we look forward to supporting their future growth.”

TravelPerk’s total funding to date now stands at almost $75 million. It’s not disclosing the valuation that its latest clutch of investors are stamping on its business but, with a bit of a chuckle, co-founder and CEO Avi Meir dubs it “very high.”

TravelPerk contends that a $1.3 trillion market is ripe for disruption because legacy business travel booking platforms are both lacking in options and roundly hated for being slow and horrible to use. (Hi Concur!)

Helping business save time and money using a slick, consumer-style trip booking platform that both packs in options and makes business travelers feel good about the booking process (i.e. rather than valueless cogs in a soul-destroying corporate ROI machine) is the general idea — an idea that’s seemingly catching on fast.

And not just with the usual suspect, early adopter, startup dog food gobblers but pushing into the smaller end of the enterprise market too.

“We kind of stumbled on the realization that our platform works for bigger companies than we thought initially,” says Meir. “So the users used to be small, fast-growing tech companies, like GetYourGuide, Outfittery, TypeForm etc… They’re early adopters, they’re tech companies, they have no fear of trying out tech — even for such a mission-critical aspect of their business… But then we got pulled into bigger companies. We recently signed FarFetch for example.”

Other smaller-sized enterprises that have signed up include the likes of Adyen, B&W, Uber and Aesop.

Companies small and big are, seemingly, united in their hatred of legacy travel booking platforms — and feeling encouraged to check out TravelPerk’s alternative, thanks to the SaaS being free to use and free from the usual contract lock ins.

TravelPerk’s freemium business model is based on taking affiliate commissions on bookings. Down the road, it also has its eye on generating a data-based revenue stream via paid-tier trip analytics.

Currently it reports booking revenues growing at 700 percent year on year. And Meir previously told us it’s on course to do $100 million GMV this year — which he confirms continues to be the case.

It also says it’s on track to complete bookings for one million travelers by next year. And it claims to be the fastest growing software as a service company in Europe, a region which remains its core market focus — though the new funding will be put toward market expansion.

And there is at least the possibility, according to Meir, that TravelPerk could actively expand outside Europe within the next 12 months.

“We definitely are looking at expansion outside of Europe as well. I don’t know yet if it’s going to be first U.S. — West or East — because there are opportunities in both directions,” he tells TechCrunch. “And we have customers; one of our largest customers is in Singapore. And we do have a growing amount of customers out of the U.S.”

Doubling down on growth within Europe is certainly on the slate, though, with a chunk of the Series C going to establish a number of new offices across the region.

Having more local bases to better serve customers is the idea. Meir notes that, perhaps unusually for a startup, TravelPerk has not outsourced customer support — but kept customer service in-house to try to maintain quality. (Which, in Europe, means having staff who can speak the local language.)

He also quips about the need for a travel business to serve up “human intelligence” — i.e. by using tech tools to slickly connect on-the-road customers with actual people who can quickly and smartly grapple with and solve problems, versus an automated AI response which is — let’s face it — probably the last thing any time-strapped business traveler wants when trying to get orientated fast and/or solve a snafu away from home.

“I wouldn’t use [human intelligence] for everything but definitely if people are on the road, and they need assistance, and they need to make changes, and you need to understand what they said…” argues Meir, going on to say ‘HI’ has been his response when investors asked why TravelPerk’s pitch deck doesn’t include the almost-impossible-to-avoid tech buzzword: “AI.”

“I think we are probably the only startup in the world right now that doesn’t have AI in the pitch deck somewhere,” he adds. “One of the investors asked about it and I said ‘well we have HI; it’s better’… We have human intelligence. Just people, and they’re smart.”

Also on the cards (it therefore follows): More hiring (the team is at ~150 now and Meir says he expects it to push close to 300 within 18 months), as well as continued investment on the product front, including in the mobile app, which was a late addition, only arriving this year.

The TravelPerk mobile app offers handy stuff like a one-stop travel itinerary, flight updates and a chat channel for support. But the desktop web app and core platform were the team’s first focus, with Meir arguing the desktop platform is the natural place for businesses to book trips.

This makes its mobile app more a companion piece — to “how you travel” — housing helpful additions for business travelers, as nice-to-have extras. “That’s what our app does really well,” he adds. “So we’re unusually contrarian and didn’t have a mobile app until this year… It was a pretty crazy bet but we really wanted to have a great web app experience.”

Much of TravelPerk’s early energy has clearly gone into delivering on the core product via nailing down the necessary partnerships and integrations to be able to offer such a large inventory — and thus deliver expanded utility versus legacy rivals.

As well as offering a clean-looking, consumer-style interface intended to do for business travel booking feels what Slack has done for work chat, the platform boasts a larger inventory than traditional players in the space, according to Meir — by plugging into major consumer providers such as Booking.com and Expedia.

The inventory also includes Airbnb accommodation (not just traditional hotels), while other partners on the flight side include Kayak and Skyscanner.

“We have not the largest bookable inventory in the world,” he claims. “We’re way larger than old-school competitors… We went through this licensing process which is almost as difficult as getting a banking license… which gives us the right to sell you the same product as travel agencies… Nobody in the world can sell you Kayak’s flights directly from their platform — so we have a way to do that.”

TravelPerk also recently plugged trains into its directly bookable options. This mode of transport is an important component of the European business travel market, where rail infrastructure is dense, highly developed and often very high-speed. (Which means it can be both the most convenient and environmentally friendly travel option to use.)

“Trains are pretty complex technically so we found a great partner,” notes Meir on that, listing major train companies including in Germany, Spain and Italy as among those it’s now able to offer direct bookings for via its platform.

On the product side, the team is also working on integrating travel and expenses management into the platform — to serve its growing numbers of (small) enterprise customers who need more than just a slick trip booking tool.

Meir says getting pulled to these bigger accounts is steering its European expansion — with part of the Series C going to fund a clutch of new offices around the region near where some of its bigger customers are based. Beginning in London, with Berlin, Amsterdam and Paris slated to follow soon.

What does the team attribute TravelPerk’s momentum to generally? It comes back to the pain, says Meir. Business travelers are being forced to “tolerate” horrible legacy systems. “So I think the pain-point is so visible and so clear [it sells itself],” he argues, also pointing out this is true for investors (which can’t have hurt TravelPerk’s funding pitch).

“In general we just built a great product and a great service, and we focused on this consumer angle — which is something that really connects well with what people want in this day and age,” he adds. “People want to use something that feels like Slack.”

For the Series C, Meir says TravelPerk was looking for investors who would be comfortable supporting the business for the long haul, rather than pushing for a quick sale. So they are now articulating the possibility of a future IPO.

And while he says TravelPerk hadn’t known much about Swedish investment firm Kinnevik prior to the Series C, Meir says he came away impressed with its focus on “global growth and ambition,” and the “deep pockets and the patience that comes with it.”

“We really aligned on this should be a global play, rather than a European play,” he adds. “We really connected on this should be a very, big independent business that goes to the path of IPO rather than a quick exit to one of the big players.

“So with them we buy patience, and also the condition, when offers do come onto the table, to say no to them.”

Given it’s been just a short six months between the Series B and C, is TravelPerk planning to raise again in the next 12 months?

“We’re never fundraising and we’re always fundraising I guess,” Meir responds on that. “We don’t need to fundraise for the next three years or so, so it will not come out of need, hopefully, unless something really unusual is happening, but it will come more out of opportunity and if it presented a way to grow even faster.

“I think the key here is how fast we grow. And how good a product we certify — and if we have an opportunity to make it even faster or better than we’ll go for it. But it’s not something that we’re actively doing it… So to all investors reading this piece don’t call me!” he adds, most likely inviting a tsunami of fresh investor pitches.

Discussing the challenges of building a business that’s so fast growing it’s also changing incredibly rapidly, Meir says nothing is how he imagined it would be — including fondly thinking it would be easier the bigger and better resourced the business got. But he says there’s an upside too.

“The challenges are just much, much bigger on this scale,” he says. “Numbers are bigger, you have more people around the table… I would say it’s very, very difficult and challenging but also extremely fun.

“So now when we release a feature it goes immediately into the hands of hundreds of thousands of travelers that use it every month. And when you fundraise… it’s much more fun because you have more leverage.

“It’s also fun because — and I don’t want to position myself as the cynical guy — the reality is that most startups don’t cure cancer, right. So we’re not saving the world… but in our little niche of business travel, which is still like $1.3 trillion per year, we are definitely making a dent.

“So, yes, it’s more challenging and difficult as you grow, and the problems become much bigger, but you can also deliver the feedback to more people.”

Powered by WPeMatico