Airbnb

Auto Added by WPeMatico

Auto Added by WPeMatico

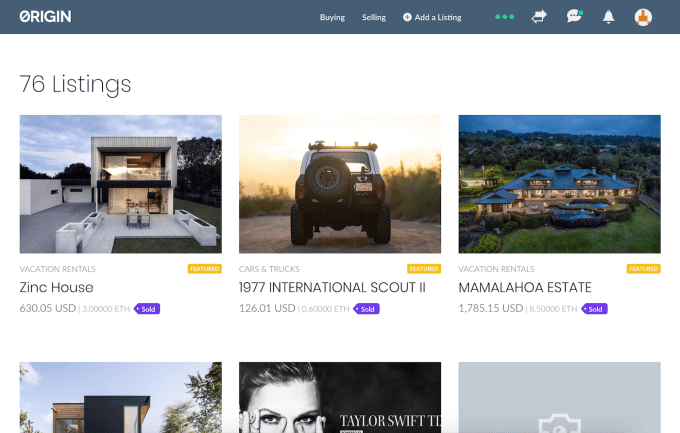

The sharing economy ends up sharing a ton of labor’s earnings with middlemen like Uber and Airbnb, and $38 million-funded Origin wants the next great two-sided marketplace to be decentralized on the blockchain so drivers and riders or hosts and guests can connect directly and avoid paying steep fees that can range up to 20 percent or higher. So today Origin launches its decentralized marketplace protocol on the ethereum mainnet that replaces a central business that connects users and vendors with a smart contract.

“Marketplaces don’t redistribute the profits they make to members. They accrue to founders and venture capitalists,” said Origin co-founder Matt Liu, who was the third product manager at YouTube. “Building these decentralized marketplaces, we want to make them peer-to-peer, not peer-to-corporate-monopoly-to-peer.” When people transact through Origin, it plans to issue them tokens that will let them participate in the governance of the protocol, and could incentivize them to get on these marketplaces early as well as convince others to use them.

Origin’s in-house marketplace DApp

Today’s mainnet beta sees Origin offering its own basic decentralized app that operates like a Craigslist on the blockchain. Users can create a profile, connect their ethereum wallet through services like MetaMask, browse product and service listings, message each other to arrange transactions through smart contracts with no extra fees, leave reviews and appeal disputes to Origin’s in-house arbitrators.

Eventually, with the Origin protocol, developers will be able to quickly build their own sub-marketplaces for specific services like dog walking, house cleaning, ridesharing and more. These developers can opt to charge fees, though Origin hopes the cost-savings from its blockchain platform will let them undercut non-blockchain services. And vendors can offer a commission to any marketplace that gets their listing matched/sold.

It might be years before the necessary infrastructure like login systems and simple wallets make it easy for developers and mainstream users to build and adopt DApps built on Origin. But it has plenty of runway thanks to $3 million in seed token sale funding from Pantera Capital, $6.6 million raised through a Coinlist token sale, plus $26.4 million in traditional venture funding from Pantera Capital, Foundation Capital, Garry Tan, Alexis Ohanian, Gil Penchina, Kamal Ravikant, Steve Jang and Randall Kaplan.

“Marketplaces are at the core of what makes the internet so valuable and useful and the Origin team has one of the most promising blockchain platforms for the new sharing economy — with currency baked in — this could be really disruptive (and one of the best utilizations of the ethereum blockchain),” says Ohanian, the Reddit and Initialized Capital co-founder.

Liu and co-founder Josh Fraser came up with the idea after trying to imagine the downstream effects of ethereum. Liu recalls thinking, “What if we could replace dozens of multi-million and multi-billion-dollar companies with open-source protocols that aren’t owned or controlled by anyone?”

Origin co-founders (from left): Matthew Liu and Josh Fraser

So why would marketplaces want to build on Origin instead of creating their own blockchain or traditional proprietary system? Fraser tells me smart contracts can save money, but that “these individual pieces are incredibly difficult to build,” so he sees Origin as “analogous to Stripe — able to abstract away all the friction of building on the blockchain.” Indeed, 40 marketplaces have already signed letters of intent to build on the protocol.

If Origin reaches critical mass, it could also benefit from the concept of shared network effect. Users only have to sign up once, and can then interact with any marketplace built on Origin. That means new marketplaces that builds on the protocol instantly has a registered user base.

Origin will face some stiff challenges, though. There’ll be a chicken-and-egg problem of getting the first marketplaces signed up before there are users on its self-sovereign identity platform, or getting those users aboard when there’s little for them to do. Liu admits that timing is the startup’s biggest threat. “We believe that decentralized marketplaces are inevitable, but a lot of smart people seem to think we’re too early and that we should be focused on building lower-level infrastructure instead,” the co-founder says. For us, we’d rather be too early than too late.”

There’s also the trouble of leaving actors in a capitalist system to treat each other properly without a centralized authority. If an Uber driver treats you terribly, you can complain and get them kicked off the platform. Even with Origin’s review system, abusers of the system may be able to continue operating. It’s easy to imagine its arbitration service becoming completely overwhelmed with disputes. Luckily, Origin has made some strong hires to tackle these challenges, including Yu Pan, who it says was a PayPal co-founder, former head of Dropbox’s NYC engineering team Cuong Du, and Franck Chastagnol who previously led engineering teams at PayPal, YouTube, Google and Dropbox.

There’s also the trouble of leaving actors in a capitalist system to treat each other properly without a centralized authority. If an Uber driver treats you terribly, you can complain and get them kicked off the platform. Even with Origin’s review system, abusers of the system may be able to continue operating. It’s easy to imagine its arbitration service becoming completely overwhelmed with disputes. Luckily, Origin has made some strong hires to tackle these challenges, including Yu Pan, who it says was a PayPal co-founder, former head of Dropbox’s NYC engineering team Cuong Du, and Franck Chastagnol who previously led engineering teams at PayPal, YouTube, Google and Dropbox.

Origin’s success will all come down to usability. Your average Uber driver or Airbnb host is no blockchain expert. They vend through those apps because it’s easy. Those centralized organizations are also highly incentivized to fulfill transactions quickly and smoothly in ways prohibited by eliminating fees. Origin will have to effectively make the blockchain aspects of its service disappear so all users and vendors know is that they’re paying less or earning more.

Powered by WPeMatico

Dressed in a Naruto t-shirt and a hat emblazoned with the phrase “lone wolf,” Ne-Yo slouches over in a chair inside a Holberton School classroom. The Grammy-winning recording artist is struggling to remember the name of “that actor,” the one who’s had a successful career in both the entertainment industry and tech investing.

“I learned about all the things he was doing and I thought it was great for him,” Ne-Yo told TechCrunch. “But I didn’t really know what my place in tech would be.”

It turns out “that actor” is Ashton Kutcher, widely known in Hollywood and beyond for his role in several blockbusters and the TV sitcom That ’70s Show, and respected in Silicon Valley for his investments via Sound Ventures and A-Grade in Uber, Airbnb, Spotify, Bird and several others.

Ne-Yo, for his part, is known for a string of R&B hits including So Sick, One in a Million and Because of You. His latest album, Good Man, came out in June.

Ne-Yo, like Kutcher, is interested in pursuing a side gig in investing but he doesn’t want to waste time chasing down the next big thing. His goal, he explained, is to use his wealth to encourage people like him to view software engineering and other technical careers as viable options.

“Little black kids growing up don’t say things like ‘I want to be a coder when I grow up,’ because it’s not real to them, they don’t see people that look like me doing it,” Ne-Yo said. “But tech is changing the world, like literally by the day, by the second, so I feel like it just makes the most sense to have it accessible to everyone.”

Last year, Ne-Yo finally made the leap into venture capital investing: his first deal, an investment in Holberton School, a two-year coding academy founded by Julien Barbier and Sylvain Kalache that trains full-stack engineers. The singer returned to San Francisco earlier this month for the grand opening of Holberton’s remodeled headquarters on Mission Street in the city’s SoMa neighborhood.

Holberton, a proposed alternative to a computer science degree, is free to students until they graduate and land a job, at which point they are asked to pay 17 percent of their salaries during their first three years in the workforce.

It has a different teaching philosophy than your average coding academy or four-year university. It relies on project-based and peer learning, i.e. students helping and teaching each other; there are no formal teachers or lecturers. The concept appears to be working. Holberton says their former students are now employed at Apple, NASA, LinkedIn, Facebook, Dropbox and Tesla.

Ne-Yo participated in Holberton’s $2.3 million round in February 2017 alongside Reach Capital and Insight Venture Partners, as well as Trinity Ventures, the VC firm that introduced Ne-Yo to the edtech startup. Holberton has since raised an additional $8 million from existing and new investors like daphni, Omidyar Network, Yahoo! co-founder Jerry Yang and Slideshare co-founder Jonathan Boutelle.

Holberton has used that capital to expand beyond the Bay Area. A school in New Haven, Conn., where the company hopes to reach students who can’t afford to live in tech’s hubs, is in development.

The startup’s emphasis on diversity is what attracted Ne-Yo to the project and why he signed on as a member of the board of trustees. More than half of Holberton’s students are people of color and 35 percent are women. Since Ne-Yo got involved, the number of African American applicants has doubled from roughly 5 percent to 11.5 percent.

“I didn’t really know what my place in tech would be.”

Before Ne-Yo’s preliminary meetings with Holberton’s founders, he says he wasn’t aware of the racial and gender diversity problem in tech.

“When it was brought to my attention, I was like ‘ok, this is definitely a problem that needs to be addressed,’” he said. “It makes no sense that this thing that affects us all isn’t available to us all. If you don’t have the money or you don’t have the schooling, it’s not available to you, however, it’s affecting their lives the same way it’s affecting the rich guys’ lives.”

Holberton’s founders joked with TechCrunch that Ne-Yo has actually been more supportive and helpful in the last year than many of the venture capitalists who back Holberton. He’s very “hands-on,” they said. Despite the fact that he’s balancing a successful music career and doesn’t exactly have a lot of free time, he’s made sure to attend events at Holberton, like the recent grand opening, and will Skype with students occasionally.

“I wanted it to be grassroots and authentic.”

Ne-Yo was very careful to explain that he didn’t put money in Holberton for the good optics.

“This isn’t something I just wanted to put my name on,” he said. “I wanted to make sure [the founders] knew this was something I was going to be serious about and not just do the celebrity thing. I wanted it to be grassroots and authentic so we dropped whatever we were doing and came down, met these guys, hung out with the students and hung out at the school to see what it’s really about.”

What’s next for Ne-Yo? A career in venture capital, perhaps? He’s definitely interested and will be making more investments soon, but a full pivot into VC is unlikely.

At the end of the day, Silicon Valley doesn’t need more people with fat wallets and a hankering for the billionaire lifestyle. What it needs are people who have the money and resources necessary to bolster the right businesses and who care enough to prioritize diversity and inclusivity over yet another payday.

“Not to toot the horn or brag, but I’m not missing any meals,” Ne-Yo said. “So, if I’m going to do it, let it mean something.”

Powered by WPeMatico

To keep up with the growing sizes of early-stage funding rounds, Y Combinator announced this morning that it will increase the size of its investments to $150,000 for 7 percent equity starting with its winter 2019 batch.

Based in Mountain View, Calif., YC funds and mentors hundreds of startups per year through its 12-week program that culminates in a demo day, where founders pitch their companies to an audience of Silicon Valley’s top investors. Airbnb, Dropbox and Instacart are among its greatest successes.

Since 2014, YC has invested $120,000 for 7 percent equity in its companies. It has increased the size of its investment before — in 2007, a YC “standard deal” was just $20,000 — but the amount of equity the accelerator takes in exchange for the capital has been consistent.

“We thought a $30K increase was necessary to help companies stay focused on building their product without worrying about fundraising too soon,” Y Combinator chief executive officer Michael Seibel wrote in a blog post this morning. “Capital for startups has never been more abundant, and we’ll continue to focus on the things that remain hard to come by — community, simplicity, advice that’s systematic and personal, and above all, a great founder experience.”

Seibel was named CEO in 2016. Co-founder Sam Altman serves as YC’s president.

YC is also changing the way it crafts its investments. It will now invest in startups on a post-money safe basis rather than on a pre-money safe. YC invented the fundraising mechanism, safe, in 2013. A safe, or a simple agreement for future equity, means an investor makes an investment in a company and receives the company stock at a later date — an alternative to a convertible note. A safe is a quicker and simpler way to get early money into a company and the idea was, according to YC, that holders of those safes would be early investors in the startup’s Series A or later priced equity rounds.

In recent years, YC noticed that startups were raising much larger seed rounds than before and those safes were “really better considered as wholly separate financings, rather than ‘bridges’ into later priced rounds.” Founders, in the meantime, were struggling to determine how much they were being diluted.

YC’s latest change, in short, will make it easier for founders to know exactly how much of their company they are selling off and will make capitalization table math, which can be extremely grueling for founders, a whole lot easier.

The pre-money safe has been criticized by founders and investors alike.

Last year, a pair of venture capitalists who’d worked with YC companies, Dolby Family Partners’ Pascal Levensohn and Andrew Krowne, wrote that the safe method was screwing over founders.

“Entrepreneurs who don’t do the capitalization table math end up owning less of their company’s equity than they thought they did. And when an equity round is inevitably priced, entrepreneurs don’t like the founder dilution numbers at all. But they can’t blame the VC, they can’t blame the angels, so that means they can only blame… oops!”

A transition to a post-money safe will eliminate that cap table math headache while still being simple and efficient. The trade-off, YC says, “is that each incremental dollar raised on post-money safes dilutes just the current stockholders, which is often the founders and early employees.” So it’s not perfect, but it’s an improvement.

Recent YC grad Deepak Chhugani, the founder of The Lobby, which announced a $1.2 million investment this week, had a positive response to the changes and said either way, most of the resources provided by YC are priceless to a first-time founder, like himself.

YC is also tweaking its policy around pro-rata follow-ons. You can read about that here.

Powered by WPeMatico

Watching the current price madness is scary. Bitcoin is falling and rising in $500 increments with regularity and Ethereum and its attendant ICOs are in a seeming freefall with a few “dead cat bounces” to keep things lively. What this signals is not that crypto is dead, however. It signals that the early, elated period of trading whose milestones including the launch of Coinbase and the growth of a vibrant (if often shady) professional ecosystem is over.

Crypto still runs on hype. Gemini announcing a stablecoin, the World Economic Forum saying something hopeful, someone else saying something less hopeful – all of these things and more are helping define the current market. However, something else is happening behind the scenes that is far more important.

As I’ve written before, the socialization and general acceptance of entrepreneurs and entrepreneurial pursuits is a very recent thing. In the old days – circa 2000 – building your own business was considered somehow sordid. Chancers who gave it a go were considered get-rich-quick schemers and worth of little more than derision.

As the dot-com market exploded, however, building your own business wasn’t so wacky. But to do it required the imprimaturs and resources of major corporations – Microsoft, Sun, HP, Sybase, etc. – or a connection to academia – Google, Netscape, Yahoo, etc. You didn’t just quit school, buy a laptop, and start Snapchat.

It took a full decade of steady change to make the revolutionary thought that school wasn’t so great and that money was available for all good ideas to take hold. And take hold it did. We owe the success of TechCrunch and Disrupt to that idea and I’ve always said that TC was career pornography for the cubicle dweller, a guilty pleasure for folks who knew there was something better out there and, with the right prodding, they knew they could achieve it.

So in looking at the crypto markets currently we must look at the dot-com markets circa 1999. Massive infrastructure changes, some brought about by Y2K, had computerized nearly every industry. GenXers born in the late 70s and early 80s were in the marketplace of ideas with an understanding of the Internet the oldsters at the helm of media, research, and banking didn’t have. It was a massive wealth transfer from the middle managers who pushed paper since 1950 to the dot-com CEOs who pushed bits with native ease.

Fast forward to today and we see much of the same thing. Blockchain natives boast about having been interest in bitcoin since 2014. Oldsters at banks realize they should get in on things sooner than later and price manipulation is rampant simply because it is easy. The projects we see now are the Kozmo.com of the blockchain era, pie-in-the-sky dream projects that are sucking up millions in funding and will produce little in real terms. But for every hundred Kozmos there is one Amazon .

And that’s what you have to look for.

Will nearly every ICO launched in the last few years fail? Yes. Does it matter?

Not much.

The market is currently eating its young. Early investors made (and probably lost) millions on early ICOs but the resulting noise has created an environment where the best and brightest technical minds are faced with not only creating a technical product but also maintaining a monetary system. There is no need for a smart founder to have to worry about token price but here we are. Most technical CEOs step aside or call for outside help after their IPO, a fact that points to the complexity of managing shareholder expectations. But what happens when your shareholders are 16-year-olds with a lot of Ethereum in a Discord channel? What happens when little Malta becomes the de facto launching spot for token sales and you’re based in Nebraska? What happens when the SEC, FINRA, and Attorneys General from here to Beijing start investigating your hobby?

Basically your hobby stops becoming a hobby. Crypto and blockchain has weaponized nerds in an unprecedented way. In the past if you were a Linux developer or knew a few things about hardware you could build a business and make a little money. Now you can build an empire and make a lot of money.

Crypto is falling because the people in it for the short term are leaving. Long term players – the Amazons of the space – have yet to be identified. Ultimately we are going to face a compression in the ICO and, for a while, it’s going to be a lot harder to build an ICO. But give it a few years – once the various financial authorities get around to reading the Satoshi white paper – and you’ll see a sea change. Coverage will change. Services will change. And the way you raise money will change.

VC used to be about a team and a dream. Now it’s about a team, $1 million in monthly revenue, and a dream. The risk takers are gone. The dentists from Omaha who once visited accelerator demo days and wrote $25,000 checks for new apps are too shy to leave their offices. The flashy VCs from Sand Hill have to keep Uber and Airbnb’s plates spinning until they can cash out. VC is dead for the small entrepreneur.

Which is why the ICO is so important and this is why the ICO is such a mess right now. Because everybody sees the value but nobody – not the SEC, not the investors, not the founders – can understand how to do it right. There is no SAFE note for crypto. There are no serious accelerators. And all of the big names in crypto are either goldbugs, weirdos, or Redditors. No one has tamed the Wild West.

They will.

And when they do expect a whole new crop of Amazons, Ubers, and Oracles. Because the technology changes quickly when there’s money, talent, and a way to marry the two in which everyone wins.

Powered by WPeMatico

Business travelers have become an increasingly important part of Airbnb’s business, according to a new blog post. The company says that Airbnb for Work, which launched in 2014, has seen bookings triple from 2015 to 2016, and triple again from 2016 to 2017. In fact, Airbnb says that almost 700,000 companies have signed up for and booked with Airbnb for Work.

Interestingly, the breakdown of companies working with Airbnb for traveler lodging are pretty diverse — employees from large enterprise companies (5,000+ employees) and employees from startups and SMBs (one to 250 employees) take a 40-40 split, with the final 20 percent of Airbnb for Work bookings going to mid-sized companies.

In July of 2017, Airbnb started making its listings available via SAP Concur, a tool used by a large number of business travelers. Airbnb says that this integration has been a huge help to growing Airbnb for Work, with Concur seeing a 42 percent increase in employees expensing Airbnb stays from 2016 to 2017. Moreover, 63 percent of Concur’s Fortune 500 clients have booked a business trip on Airbnb.

One interesting trend that Airbnb has noticed is that nearly 60 percent of Airbnb for Work trips had more than one guest.

“We can offer big open areas for collaborations, while still giving employees their own private space,” said David Holyoke, global head of business travel at Airbnb. “We think this offers a more meaningful business trip and it saves the company a lot of money.”

Given the tremendous growth of the business segment, as well as the opportunity it represents, Airbnb is working on new features for business travelers. In fact, in the next week, Airbnb will be launching a new feature that lets employees search for Airbnb listings on a company-specific landing page.

So, for example, a Google employee might search for their lodging on Google.Airbnb.com, and the site would be refined to cater to Google’s preferences, including locations close to the office, budget, and other factors.

While the growth has picked up, Holyoke still sees Airbnb for Work as an opportunity to grow. He said that Airbnb for Work listings only represent 15 percent of all Airbnb trips.

But, the introduction of boutique hotels and other amenity-driven listings such as those on Airbnb Plus are paving the way for business travelers to lean toward Airbnb instead of a business hotel.

Plus, as mobility and relocation become even more important to how a business operates, Airbnb believes it can be a useful tool to help employees get started in a new town before they purchase a home.

Powered by WPeMatico

Airbnb is testing a new payments feature for hosts, letting them get partially paid out at the time of booking.

This feature isn’t rolling out to everyone just yet, as Airbnb says that this is just a preliminary test to gauge interest. Invited hosts simply opt in to payout splitting to check out the feature.

Here’s how it works:

Normally, Airbnb hosts are paid 24 hours after their guest’s scheduled check-in time. With the new payouts test, hosts who have been invited and opt in will receive 50 percent of their cash three days after the guest has booked their stay, and the other half will be received 24 hours after check-in time.

For their trouble, Airbnb is taking a 1 percent fee of the booking subtotal for early payouts.

As per usual, hosts can opt out of early payouts at any time by making the change in their Payout Preferences.

If a booking is cancelled after an early payout has been received, the amount will be deducted from the host’s next booking.

This comes on the heels of Airbnb’s announcement in February to add new tiers and types of lodging to the platform, including boutique hotels and B&Bs. Airbnb classifies hosts with more than six listings on the platform as Professional Hosts, and early payouts are one way that Airbnb can help these hosts grow their business.

However, in certain housing-constrained markets like NYC, professional hosts aren’t necessarily welcome. In May, NYC Comptroller Scott Stringer released a report saying that Airbnb’s presence in NYC is driving up the cost of rent for full-time residents. The company and the Comptroller’s office went back and forth over the veracity of the report, but NYC isn’t the only market worried about the folks who make Airbnb their full-time job.

In 2017, the WSJ reported on a study surveying 100 of the largest metro areas in the U.S. that found that a 10 percent increase in Airbnb listings leads to a 0.39 percent increase in rent and a 0.64 percent increase in housing prices. That may sound small, but rental prices typically climbed by 2.2 percent per year without Airbnb, according to one of the survey’s authors. So Airbnb is accelerating the rate at which rental prices rise.

This very argument and the ensuing spats have led Airbnb to cut SF listings (almost in half) following the city’s kick-off of new short-term rental laws. And new, stricter laws may be coming to NYC.

Airbnb says that it works with its communities to stay on the right side of the law, but that professionally managed properties are integral in markets where tourism is a huge part of the economy.

“For decades, vacation rentals and professionally managed properties have been the backbone of the economy in vacation destinations like beach and ski towns and we welcome these types of listings in these types of communities,” said an Airbnb spokesperson. “Trials like these are one way we work to support our community. In some places, usually urban destinations, there can be rules around hosting multiple listings. We always want Airbnb to be a positive force in local communities and we make it clear to hosts that they need to follow these rules.”

The payouts test is geared toward professional hosts, but is being spread via an invite basis to both pro hosts and regular hosts.

Powered by WPeMatico

Airbnb brings in billions of dollars of revenue annually and is profitable on an EBITDA basis, so many wonder if and when the home-sharing company will go public. At the Code Conference today, Airbnb CEO Brian Chesky said the company will “be ready to IPO next year, but I don’t know if we will.”

He added that he wants to make sure it’s a major benefit to the company when Airbnb does go public. Following some more probing, Chesky said he has “no issues with [going public] at all. It could happen.”

Meanwhile, Airbnb has been struggling from a regulatory standpoint since at least 2010. Specifically, San Francisco and New York are two of the most difficult cities from a regulatory standpoint, Chesky said.

In New York, for example, there has been a standstill since 2010. At this point, Chesky said he expects it to take a few more years to overcome the challenge in New York.

“It doesn’t seem like the end is in sight with that challenge,” Chesky said. That challenge, Chesky said, involves the hotel industry and unions that “have galvanized people in these perpetual battles.”

Another general critique of Airbnb is its effect on rising rent costs and displacement. Chesky added that if it was simply a business decision, “it probably wouldn’t be worth it to stay there” in New York. But Chesky said there are hosts who have come to rely on Airbnb to earn income.

At Code, Chesky also touted Airbnb’s experiences product and how it’s growing 10x faster than its homes product. Airbnb Experiences sees 1.5 million bookings a year, Chesky said. Experiences, which Airbnb started testing in 2014 and officially launched in 2016, is Airbnb’s product that helps travelers find things to do in cities throughout the world.

When it first launched, Airbnb didn’t verify the experiences, but after some bad experiences, Airbnb has started verifying them.

“They’re doing incredibly well,” Chesky said. He added that the “experience economy” is growing and “there will probably be a massive economy around experiences.”

Powered by WPeMatico

Why has San Francisco’s startup scene generated so many hugely valuable companies over the past decade?

That’s the question we asked over the past few weeks while analyzing San Francisco startup funding, exit, and unicorn creation data. After all, it’s not as if founders of Uber, Airbnb, Lyft, Dropbox and Twitter had to get office space within a couple of miles of each other.

We hadn’t thought our data-centric approach would yield a clear recipe for success. San Francisco private and newly public unicorns are a diverse bunch, numbering more than 30, in areas ranging from ridesharing to online lending. Surely the path to billion-plus valuations would be equally varied.

But surprisingly, many of their secrets to success seem formulaic. The most valuable San Francisco companies to arise in the era of the smartphone have a number of shared traits, including a willingness and ability to post massive, sustained losses; high-powered investors; and a preponderance of easy-to-explain business models.

No, it’s not a recipe that’s likely replicable without talent, drive, connections and timing. But if you’ve got those ingredients, following the principles below might provide a good shot at unicorn status.

First, lose money until you’ve left your rivals in the dust. This is the most important rule. It is the collective glue that holds the narratives of San Francisco startup success stories together. And while companies in other places have thrived with the same practice, arguably San Franciscans do it best.

It’s no secret that a majority of the most valuable internet and technology companies citywide lose gobs of money or post tiny profits relative to valuations. Uber, called the world’s most valuable startup, reportedly lost $4.5 billion last year. Dropbox lost more than $100 million after losing more than $200 million the year before and more than $300 million the year before that. Even Airbnb, whose model of taking a share of homestay revenues sounds like an easy recipe for returns, took nine years to post its first annual profit.

Not making money can be the ultimate competitive advantage, if you can afford it.

Industry stalwarts lose money, too. Salesforce, with a market cap of $88 billion, has posted losses for the vast majority of its operating history. Square, valued at nearly $20 billion, has never been profitable on a GAAP basis. DocuSign, the 15-year-old newly public company that dominates the e-signature space, lost more than $50 million in its last fiscal year (and more than $100 million in each of the two preceding years). Of course, these companies, like their unicorn brethren, invest heavily in growing revenues, attracting investors who value this approach.

We could go on. But the basic takeaway is this: Losing money is not a bug. It’s a feature. One might even argue that entrepreneurs in metro areas with a more fiscally restrained investment culture are missing out.

What’s also noteworthy is the propensity of so many city startups to wreak havoc on existing, profitable industries without generating big profits themselves. Craigslist, a San Francisco nonprofit, may have started the trend in the 1990s by blowing up the newspaper classified business. Today, Uber and Lyft have decimated the value of taxi medallions.

Not making money can be the ultimate competitive advantage, if you can afford it, as it prevents others from entering the space or catching up as your startup gobbles up greater and greater market share. Then, when rivals are out of the picture, it’s possible to raise prices and start focusing on operating in the black.

You can’t lose money on your own. And you can’t lose any old money, either. To succeed as a San Francisco unicorn, it helps to lose money provided by one of a short list of prestigious investors who have previously backed valuable, unprofitable Northern California startups.

It’s not a mysterious list. Most of the names are well-known venture and seed investors who’ve been actively investing in local startups for many years and commonly feature on rankings like the Midas List. We’ve put together a few names here.

You might wonder why it’s so much better to lose money provided by Sequoia Capital than, say, a lower-profile but still wealthy investor. We could speculate that the following factors are at play: a firm’s reputation for selecting winning startups, a willingness of later investors to follow these VCs at higher valuations and these firms’ skill in shepherding portfolio companies through rapid growth cycles to an eventual exit.

Whatever the exact connection, the data speaks for itself. The vast majority of San Francisco’s most valuable private and recently public internet and technology companies have backing from investors on the short list, commonly beginning with early-stage rounds.

Generally speaking, you don’t need to know a lot about semiconductor technology or networking infrastructure to explain what a high-valuation San Francisco company does. Instead, it’s more along the lines of: “They have an app for getting rides from strangers,” or “They have an app for renting rooms in your house to strangers.” It may sound strange at first, but pretty soon it’s something everyone seems to be doing.

It’s not a recipe that’s likely replicable without talent, drive, connections and timing.

A list of 32 San Francisco-based unicorns and near-unicorns is populated mostly with companies that have widely understood brands, including Pinterest, Instacart and Slack, along with Uber, Lyft and Airbnb. While there are some lesser-known enterprise software names, they’re not among the largest investment recipients.

Part of the consumer-facing, high brand recognition qualities of San Francisco startups may be tied to the decision to locate in an urban center. If you were planning to manufacture semiconductor components, for instance, you would probably set up headquarters in a less space-constrained suburban setting.

While it can be frustrating to watch a company lurch from quarter to quarter without a profit in sight, there is ample evidence the approach can be wildly successful over time.

Seattle’s Amazon is probably the poster child for this strategy. Jeff Bezos, recently declared the world’s richest man, led the company for more than a decade before reporting the first annual profit.

These days, San Francisco seems to be ground central for this company-building technique. While it’s certainly not necessary to locate here, it does seem to be the single urban location most closely associated with massively scalable, money-losing consumer-facing startups.

Perhaps it’s just one of those things that after a while becomes status quo. If you want to be a movie star, you go to Hollywood. And if you want to make it on Wall Street, you go to Wall Street. Likewise, if you want to make it by launching an industry-altering business with a good shot at a multi-billion-dollar valuation, all while losing eye-popping sums of money, then you go to San Francisco.

Powered by WPeMatico

As the vacation rental sector heats up — with Airbnb making even more moves to expand its portfolio of services to include multiple tiers of rentals — there’s going to be more and more of a need for people who manage a large number of properties.

Guesty is one service that aims to do that, and today a filing with the Securities and Exchange Commission notes that it’s raised $19.75 million in a new Series B round of financing. While Airbnb may be the dominant home vacation rental service, there are others like VRBO, and managing those properties across multiple different platforms could require handling all of that information in something more analog like an Excel sheet. It’s a kind of CRM tool for property management, ranging from tracking guest check-ins to the amount of revenue a property owner. Guesty also helps property owners by providing tools to manage operations beyond just the tracking.

Airbnb earlier this year started rolling out more tiers of home categories that are geared toward different kinds of travelers. That included high-end tiers called Airbnb Plus and Beyond by Airbnb. While these new categories potentially offer a more granular set of choices for consumers, it might make managing those properties a little more difficult — especially if it’s across multiple different services like Airbnb and VRBO, or even more analog channels. Tools like Guesty can help owners of multiple different properties (that might span multiple tiers) turn those homes into an actual business.

There are also plenty of platforms that are looking for additional services for people managing multiple properties on vacation rental sites. There are startups like Beyond Pricing, which look to help property managers figure out how to best price their homes. Airbnb has its own pricing algorithms, but there’s clear demand for tools that cross multiple platforms. Guesty was party of Y Combinator’s winter 2014 class, and raised $3 million in May last year.

While Airbnb continues to try to expand into new categories and offer home owners a way to rent out their homes — or for owners of multiple properties to run a side business — it’s not the only approach to vacation rentals. One startup, Selina, is looking to convert existing properties into kinds of campuses that cater to different tiers of travelers, ranging from travelers looking to stay in a hostel to ones that are willing to pay for their own rooms. Selina earlier this month said it raised $95 million. Selina is more of a hotel-ish model as it expands from geography to geography, but it also shows that there’s demand for an experience that can cater to a wide variety of guests.

Powered by WPeMatico

If you’ve ever gone camping and found yourself thinking it kind of sucks, likely because you’re too close to other campers, you might be interested to learn about Tentrr, a three-year-old, 47-person company that’s promising to make it “dirt simple” to enjoy the great outdoors. How: by striking deals with private landowners who are willing to host semi-permanent campsites on their property.

What do these look like? Picture elevated decks with Adirondack chairs, canvas expedition tents, wood picnic tables and sun showers, not to mention a fire pit, lanterns, dry food storage, cookware, a camping toilet and air mattresses that, courtesy of most hosts, will come with fresh linens.

Venture capitalists certainly appreciate the startup’s pitch. Tentrr — founded by one-time investment banker turned former NYSE managing director Michael D’Agostino — has raised $13 million to date, including a newly closed $8 million Series A round led by West, a San Francisco-based venture studio that both funds startups and helps them market their goods and services.

No doubt the investors are looking at the overall market, whose numbers are compelling. According to one trade association, the outdoor recreation industry represents an $887 billion opportunity, with Americans shelling out $24 billion annually on campsites alone.

Still, it’s easy to wonder how scalable the company will be. Tentrr had 100 campsites up and running in the Northeastern U.S. as of the end of last year. D’Agostino expects it will have 1,000 sites by year-end, including on the West Coast, where it will begin installing camps this summer. But this assumes that Tentrr can convince enough families with sufficiently large properties that partnering with the company is worthwhile.

D’Agostino says its landowner partners need to have 15 acres at least and that the average property on the platform currently is much larger than that. He also says these property owners keep 80 percent of whatever they decide to charge campers to stay on their grounds.

For what it’s worth, Tentrr doesn’t seem to have much in the way of direct competition if you exclude state campgrounds. Venture-backed Hipcamp, for example, which raised a small amount of seed funding back in 2014, partners with private landowners to help arrange camping experiences, but it mostly acts as a search engine. A growing number of RV-focused startups have also sprung up, including Outdoorsy. But their customers are largely looking for adventure on the road, not in a secluded field.

There’s always industry giant Airbnb to worry about. But Airbnb, whose offerings include campsites, emphasizes unique experiences. Tentrr is largely about standardizing its process in order to leave fewer questions — and less doubt — about what to expect. (D’Agostino says that roughly 40 percent of Tentrr customers are first-time campers.)

We know that if the service makes it way to California, we’re likely to try it, having suffered through some fairly crummy camping experiences. If you’re also interested in learning more, you might check out our conversation with D’Agostino, edited for length. We chatted yesterday.

TC: You were a banker, then you traveled around the country and world, trying to convince companies that they should list on the NYSE instead of Nasdaq. How did this company come to pass?

MD: When I was a little kid, we’d sometimes stay at a family friend’s farm in Litchfield, Connecticut. I assumed that every kid had a Litchfield farm where they could camp, which isn’t the case obviously. Meanwhile, working 100 hours a week as an investment banker, it just became harder and harder to get out of the city and have great experiences.

After a couple of disastrous camping trips at noisy, dirty campgrounds with my girlfriend and now wife, Eloise, we just realized the idea [of camping as it’s known today] is stupid. It’s taking a bunch of people who are living on top of each other in a city and moving them to a campground where they’re living on top of each other in flimsy tents.

The legacy campground industry hasn’t changed since the Civil War. It’s run by the government — which I’m happy to compete with all day long. And these are just terrible businesspeople. We want to wipe away this infrastructure by distributing it among rural landowners.

TC: So you’re building these semi-permanent camping sites. How standardized is the pricing?

MD: Pricing is variable and set by the landowner who keeps 80 percent of that fee. We keep 20 percent; we also charge a 15 percent fee on top of that nightly rate. Right now, the average price per night is $140, but we’re introducing more features for [hosts], including minimum-night stays, and [surge] pricing if they have demand for a bunch of bookings at the same time.

They can also offer extra amenities and experiences that will allow you to have a personalized experience. For example, landowners, or “camp keepers” as we call them, can offer extra bundles of wood or luxury bedding or horseback riding or skeet shooting. It’s really only limited by the imagination. We’ll also soon allow third parties to provide curated activities so that when you log on to our app, you can book a whitewater rafting trip or reservations at the best farm-to-table restaurant nearby.

TC: What happens if something goes wrong? Who insures what?

MD: Every campsite is covered by a $2 million commercial insurance policy. It’s a benefit not just in terms of liability but in making people feel more comfortable during these stays — both the hosts and guests.

TC: Where are you building these sites, exactly, and how long do you estimate that they will last?

MD: We build them ourselves, right now in places from southern Maine to eastern Pennsylvania.

We get our tents from a family company in Colorado that’s been around for 90 years and that still receives requests to repair tents they’d built 30 years ago [meaning they’re durable]. We also use pressure-treated lumber and marine-grade plywood, so we expect they’ll last for 10 to 20 years.

TC: You’re having to convince people to let strangers onto their properties, sprawling as they may be. What does that sales process look like?

MD: It used to look like me putting 45,000 miles on my Jeep Cherokee and explaining to families why they should have a Tentrr campsite in their hayfields. [Laughs.] Today, direct mail campaigns work beautifully. [Hosts] are also hearing about us from other [hosts] and we make it easier for them to [apply] to join the platform. You click on a link that says “List my property” and you’re walked through a 20-point checklist, including about accessibility and how secluded a property is. Using that feedback, we know with 90 percent accuracy whether or not a property is appropriate. If we think it is, we’ll send out a scout.

TC: Are there sometimes more than one campsite on a property?

MD: No, and we ensure the sites are secluded from neighbors, as well as the landowners, as well as other possible distractions.

TC: What does the clean-up process involve?

MD: It’s relatively maintenance free. There’s no maid service. No keys. No worries about someone stealing silverware. Homeowners have to make sure there are no beer cans left behind, but we place a high priority on land stewardship and emphasize a leave-no-trace approach when it comes to our guests.

Powered by WPeMatico