Accel

Auto Added by WPeMatico

Auto Added by WPeMatico

CleverTap, an India-based startup that lets companies track and improve engagement with users across the web, has pulled in $26 million in new funding thanks to a round led by Sequoia India.

Existing investor Accel and new backer Tiger Global also took part in the deal, which values CleverTap at $150-$160 million, the startup disclosed. The deal takes CleverTap to around $40 million from investors to date.

Founded in 2015 and based in Mumbai, CleverTap competes with a range of customer experience services, including Oracle Cloud. Its service covers a range of touchpoints with consumers, including email, in-app activity, push notifications, Facebook, WhatsApp (for business) and Viber. Its service helps companies map out how their users are engaging across those vectors, and develop “re-engagement” programs to help reactive dormant users or increase engagement among others.

The company says its SDK is installed in more than 8,000 apps and its customers include Southeast Asia-based startups Go-Jek and Zilingo, Hotstar in India and U.S.-based Fandango . With a considerable customer base in Asia, CleverTap puts a particular focus on mobile because many of these markets are all about personal devices.

“Asia is mobile-first and massively growing,” CleverTap CEO and co-founder Sunil Thomas told TechCrunch in an interview. “A lot of engagement in this [part of the] world is timely… we were sort of born physically on the east side of the world, so we got to scale with all these diverse set of devices.”

That stands to benefit CleverTap as it seeks to grow market share outside of Asia, and in markets like the U.S. and Europe where mobile is — right now — just one part of the marketing and customer engagement process. The company believes that engagement by mobile has a long way to develop there.

“Engagement [in the West] is still email-heavy and not really timely,” Thomas said. “Whereas the East thinks of it as ‘Hey, let’s be proactive… instead of a user coming in to hunt for information, can I provide it when I think he or she will need it?’ ”

Of course, mobile push and in-app notifications can be easily abused.

Most people will know of an app on their phone that falls into that category. So, how does a company know what is too much or what isn’t enough?

“As long as you use push or in-app as an extension of your brand, then I think it’s extremely useful,” explained Thomas. “After all, this is a really competitive world; it isn’t just your app out there — if you can make your brand count when this person isn’t in your app, that’ll help you.”

More broadly, Thomas argued that CleverTap brings data to the table which, ultimately, “changes the whole context in real time.” So a customer can really look holistically at their online presence and figure out what is working, and with which users. In real terms, when used to acquire new users online, he said he believes that CleverTap typically doubles registration conversions and triples the buying rate.

“The cost of acquisition to first purchase is what we really effect,” said Thomas. “It’s that moment you get a new person into your house.”

CleverTap has an office in Sunnyvale and it has just landed in Singapore. Now it plans to add a location in Indonesia before the end of the year. Those expansions are centered around business development, with some customer support, since tech and other teams are in India. Already, according to Thomas, the company is looking to grow in Europe while it is weighing the potential to enter Latin America in a move that could include a local partnership.

The CleverTap CEO is also considering raising more money toward the end of the year, when he believes that the company can push its valuation as high as $400 million.

“That’s very doable based on revenue growth,” he said. “We think that the revenue will demand that valuation.”

Powered by WPeMatico

Business customers continue to be a huge target for the travel industry, and today a startup has raised a tidy sum to help it double down on the $1.7 trillion opportunity. Lola.com — a platform for business users to book and manage trips — has raised $37 million to continue building out its technology and hire more talent as it takes on incumbents like SAP targeting the corporate sector.

The Series C is led by General Catalyst and Accel, with participation from CRV, Tenaya Capital and GV. All are previous investors. We are asking about the valuation but it looks like prior to this, the company had raised just under $65 million, and its last post-money valuation, in 2017, was $100 million, according to PitchBook.

“We’re happy with our valuation and think it provides a good balance between recognizing our progress growing the business and protecting employees equity by keeping a reasonable valuation,” said Mike Volpe, who took over last year as CEO, in an email to us. “We prioritize our team over everything else and we’re not going to raise too much money at overly high valuations that make it hard for employees to make money on their equity.”

There are signs that the valuation will have had a bump in this round. The company said in 2018, its bookings have gone up by 423 percent, with revenues up 786 percent, although it’s not disclosing what the actual figures are for either.

“As business travelers have become increasingly mobile, Lola.com’s mission is to completely transform the landscape of corporate travel management,” said Volpe. “The continued support of our investors underscores the market potential, which is leading us to expand our partner ecosystem and double our headcount across engineering, sales and marketing. At the core, we continue to invest in building the best, simplest corporate travel management platform in the industry.”

Co-founded by Paul English and Bill O’Donnell — respectively, the former CTO/co-founder and chief architect of the wildly successful consumer travel booking platform Kayak — Lola originally tried to fix the very thing that Kayak and others like it had disrupted: it was designed as a platform for people to connect to live agents to help them organise their travel. That larger cruise ship might have already said, however (so to speak), and so the company later made a pivot to cater to a more specific demographic in the market that often needs and expects the human touch when arranging logistics: the business user.

Its unique selling point has not been just to provide a pain-free “agile” platform to make bookings, but for the platform’s human agents to be proactively pinging business users when there are modifications to a booking (for example because of flight delays), and offering help when needed to sort out the many aspects of modern travel that can be painful and time consuming for busy working people, such as technical issues around a frequent flyer program.

Lola.com is not the only one to spot the opportunity there. To further diversify its business and to move into higher-margin, bigger-ticket offerings, Airbnb has also been slowly building out its own travel platform targeting business customers by adding in hotels and room bookings.

There are others that are either hoping to bypass or complement existing services with their own takes on how to improve business travel such as TravelPerk (most recent raise: $44 million), Travelstop (an Asia-focused spin), and TripActions (most recently valued at $1 billion), to name a few. That speaks to an increasingly crowded market of players that are competing against incumbents like SAP, which owns Concur, Hipmunk and a plethora of other older services.

Lola.com has made some interesting headway in its own approach to the market, by partnering with one of the names most synonymous with corporate spending, American Express, and specifically a JV it is involved in called American Express Global Business Travel.

“Lola.com offers an incredibly simple solution to corporate travel management, which enables American Express Global Business Travel to take our value proposition to even more companies across the middle market,” said Evan Konwiser, VP of Product Strategy and Marketing for American Express GBT, in a statement.

Powered by WPeMatico

Hundreds gathered this week at San Francisco’s Pier 48 to see the more than 200 companies in Y Combinator’s Winter 2019 cohort present their two-minute pitches. The audience of venture capitalists, who collectively manage hundreds of billions of dollars, noted their favorites. The very best investors, however, had already had their pick of the litter.

What many don’t realize about the Demo Day tradition is that pitching isn’t a requirement; in fact, some YC graduates skip out on their stage opportunity altogether. Why? Because they’ve already raised capital or are in the final stages of closing a deal.

ZeroDown, Overview.AI and Catch are among the startups in YC’s W19 batch that forwent Demo Day this week, having already pocketed venture capital. ZeroDown, a financing solution for real estate purchases in the Bay Area, raised a round upwards of $10 million at a $75 million valuation, sources tell TechCrunch. ZeroDown hasn’t responded to requests for comment, nor has its rumored lead investor: Goodwater Capital.

Without requiring a down payment, ZeroDown purchases homes outright for customers and helps them work toward ownership with monthly payments determined by their income. The business was founded by Zenefits co-founder and former chief technology officer Laks Srini, former Zenefits chief operating officer Abhijeet Dwivedi and Hari Viswanathan, a former Zenefits staff engineer.

The founders’ experience building Zenefits, despite its shortcomings, helped ZeroDown garner significant buzz ahead of Demo Day. Sources tell TechCrunch the startup had actually raised a small seed round ahead of YC from former YC president Sam Altman, who recently stepped down from the role to focus on OpenAI, an AI research organization. Altman is said to have encouraged ZeroDown to complete the respected Silicon Valley accelerator program, which, if nothing else, grants its companies a priceless network with which no other incubator or accelerator can compete.

Overview .AI’s founders’ resumes are impressive, too. Russell Nibbelink and Christopher Van Dyke were previously engineers at Salesforce and Tesla, respectively. An industrial automation startup, Overview is developing a smart camera capable of learning a machine’s routine to detect deviations, crashes or anomalies. TechCrunch hasn’t been able to get in touch with Overview’s team or pinpoint the size of its seed round, though sources confirm it skipped Demo Day because of a deal.

Catch, for its part, closed a $5.1 million seed round co-led by Khosla Ventures, NYCA Partners and Steve Jang prior to Demo Day. Instead of pitching their health insurance platform at the big event, Catch published a blog post announcing its first feature, The Catch Health Explorer.

“This is only the first glimpse of what we’re building this year,” Catch wrote in the blog post. “In a few months, we’ll be bringing end-to-end health insurance enrollment for individual plans into Catch to provide the best health insurance enrollment experience in the country.”

TechCrunch has more details on the healthtech startup’s funding, which included participation from Kleiner Perkins, the Urban Innovation Fund and the Graduate Fund.

Four more startups, Truora, Middesk, Glide and FlockJay had deals in the final stages when they walked onto the Demo Day stage, deciding to make their pitches rather than skip the big finale. Sources tell TechCrunch that renowned venture capital firm Accel invested in both Truora and Middesk, among other YC W19 graduates. Truora offers fast, reliable and affordable background checks for the Latin America market, while Middesk does due diligence for businesses to help them conduct risk and compliance assessments on customers.

Finally, Glide, which allows users to quickly and easily create well-designed mobile apps from Google Sheets pages, landed support from First Round Capital, and FlockJay, the operator an online sales academy that teaches job seekers from underrepresented backgrounds the skills and training they need to pursue a career in tech sales, secured investment from Lightspeed Venture Partners, according to sources familiar with the deal.

Raising ahead of Demo Day isn’t a new phenomenon. Companies, thanks to the invaluable YC network, increase their chances at raising, as well as their valuation, the moment they enroll in the accelerator. They can begin chatting with VCs when they see fit, and they’re encouraged to mingle with YC alumni, a process that can result in pre-Demo Day acquisitions.

This year, Elph, a blockchain infrastructure startup, was bought by Brex, a buzzworthy fintech unicorn that itself graduated from YC only two years ago. The deal closed just one week before Demo Day. Brex’s head of engineering, Cosmin Nicolaescu, tells TechCrunch the Elph five-person team — including co-founders Ritik Malhotra and Tanooj Luthra, who previously founded the Box-acquired startup Steem — were being eyed by several larger companies as Brex negotiated the deal.

“For me, it was important to get them before batch day because that opens the floodgates,” Nicolaescu told TechCrunch. “The reason why I really liked them is they are very entrepreneurial, which aligns with what we want to do. Each of our products is really like its own business.”

Of course, Brex offers a credit card for startups and has no plans to dabble with blockchain or cryptocurrency. The Elph team, rather, will bring their infrastructure security know-how to Brex, helping the $1.1 billion company build its next product, a credit card for large enterprises. Brex declined to disclose the terms of its acquisition.

Y Combinator partners Michael Seibel and Dalton Caldwell, and moderator Josh Constine, speak onstage during TechCrunch Disrupt SF 2018. (Photo by Kimberly White/Getty Images)

Ultimately, it’s up to startups to determine the cost at which they’ll give up equity. YC companies raise capital under the SAFE model, or a simple agreement for future equity, a form of fundraising invented by YC. Basically, an investor makes a cash investment in a YC startup, then receives company stock at a later date, typically upon a Series A or post-seed deal. YC made the switch from investing in startups on a pre-money safe basis to a post-money safe in 2018 to make cap table math easier for founders.

Michael Seibel, the chief executive officer of YC, says the accelerator works with each startup to develop a personalized fundraising plan. The businesses that raise at valuations north of $10 million, he explained, do so because of high demand.

“Each company decides on the amount of money they want to raise, the valuation they want to raise at, and when they want to start fundraising,” Seibel told TechCrunch via email. “YC is only an advisor and does not dictate how our companies operate. The vast majority of companies complete fundraising in the 1 to 2 months after Demo Day. According to our data, there is little correlation between the companies who are most in demand on Demo Day and ones who go on to become extremely successful. Our advice to founders is not to over optimize the fundraising process.”

Though Seibel says the majority raise in the months following Demo Day, it seems the very best investors know to be proactive about reviewing and investing in the batch before the big event.

Khosla Ventures, like other top VC firms, meets with YC companies as early as possible, partner Kristina Simmons tells TechCrunch, even scheduling interviews with companies in the period between when a startup is accepted to YC to before they actually begin the program. Another Khosla partner, Evan Moore, echoed Seibel’s statement, claiming there isn’t a correlation between the future unicorns and those that raise capital ahead of Demo Day. Moore is a co-founder of DoorDash, a YC graduate now worth $7.1 billion. DoorDash closed its first round of capital in the weeks following Demo Day.

“I think a lot of the activity before demo day is driven by investor FOMO,” Moore wrote in an email to TechCrunch. “I’ve had investors ask me how to get into a company without even knowing what the company does! I mostly see this as a side effect of a good thing: YC has helped tip the scale toward founders by creating an environment where investors compete. This dynamic isn’t what many investors are used to, so every batch some complain about valuations and how easy the founders have it, but making it easier for ambitious entrepreneurs to get funding and pursue their vision is a good thing for the economy.”

This year, given the number of recent changes at YC — namely the size of its latest batch — there was added pressure on the accelerator to showcase its best group yet. And while some did tell TechCrunch they were especially impressed with the lineup, others indeed expressed frustration with valuations.

Many YC startups are fundraising at valuations at or higher than $10 million. For context, that’s actually perfectly in line with the median seed-stage valuation in 2018. According to PitchBook, U.S. startups raised seed rounds at a median post-valuation of $10 million last year; so far this year, companies are raising seed rounds at a slightly higher post-valuation of $11 million. With that said, many of the startups in YC’s cohorts are not as mature as the average seed-stage company. Per PitchBook, a company can be several years of age before it secures its seed round.

I did not talk to a single company in this batch raising under $10M post (admittedly I only was able to speak with a fraction of the 205).

— Peter Rojas (@peterrojas) March 20, 2019

Nonetheless, pricey deals can come as a disappointment to the seed investors who find themselves at YC every year but because their reputations aren’t as lofty as say, Accel, aren’t able to book pre-Demo Day meetings with YC’s top of class.

The question is who is Y Combinator serving? And the answer is founders, not investors. YC is under no obligation to serve up deals of a certain valuation nor is it responsible for which investors gain access to its best companies at what time. After all, startups are raking in larger and larger rounds, earlier in their lifespans; shouldn’t YC, a microcosm for the Silicon Valley startup ecosystem, advise their startups to charge the best investors the going rate?

Powered by WPeMatico

For a long time, it was the norm for founders to haul their hardware to the 3000 block of Sand Hill Road, where the venture capitalists of “Silicon Valley” would be awaiting their pitches. Today, many of the investors that touted the exclusivity of “The Valley” have moved north to San Francisco, where they have better access to top entrepreneurs.

Y Combinator, a Silicon Valley institution and to many the lifeblood of the startups and venture capital ecosystem, is the latest to pack up shop. YC, which invests $150,000 for 7 percent equity in a few hundred startups per year, is currently searching for a space in SF to operate its accelerator program, sources close to YC confirm to TechCrunch, because the majority of YC’s employees and its portfolio founders reside in the city.

Founded in 2005, YC’s roots are in Mountain View, California. In its first four years, YC offered programs in Cambridge, Massachusetts and Mountain View before opting in 2009 to focus exclusively on The Valley. In late 2013, as more and more of its partners and portfolio companies were establishing themselves in SF, YC opened a satellite office in the city in what would be the beginning of its journey northbound.

The small satellite office, used to support SF-based staff and provide portfolio companies resources and workspace, is located in Union Square. The fate of YC’s Mountain View office is unclear.

YC’s move north will be the latest in a series of small changes that, together, point to a new era for the accelerator. Approaching its 15th birthday, YC announced in September it was changing up the way it invests. No longer would it seed startups with $120,000 for 7 percent equity, it would give startups an additional 30,000 to cover the expenses of getting a business off the ground and it would admit a whole lot more companies.

YC began mentoring its largest cohort of companies to date in late 2018. The astonishing 200-plus group in its winter 2019 batch is more than 50 percent larger than the 132-team cohort that graduated in spring 2018. To accommodate the truly gigantic group at YC Demo Days later this month (March 18 and 19), YC has moved to a new venue, SF’s Pier 48. Historically, YC Demo Days were hosted at the Computer History Museum near its home in Mountain View.

YC has also ditched “Investor Day,” which is typically an opportunity for investors to schedule meetings with startups that just completed the accelerator program. YC writes that the decision came “after analyzing its effectiveness.” On top of that, rumors suggest YC is planning to put an end to Demo Days. Other accelerators, AngelPad for example, put a stop to the tradition last year after realizing demo day was more of a stress to startup founders than a resource. Sources close to YC, however, tell TechCrunch these rumors are categorically false.

YC isn’t the first accelerator to ditch its Silicon Valley digs. 500 Startups, a smaller yet still prolific accelerator, opened an SF satellite office the same year as YC, and in 2018, the nine-year-old program made the decision to permanently relocate to SF. Venture capital firms, too, have realized the opportunities are larger in SF than on Sand Hill Road.

The transition from the peninsula to the city began around 2012, when VC heavyweights like Uber and Twitter-backer Benchmark opened an office in SF’s mid-market neighborhood. Months later, 47-year-old Kleiner Perkins, an investor in Stripe and DoorDash, opened the doors to its new workplace in SF’s South Park neighborhood.

Around that same time a whole bunch of firms followed suit: Shasta Ventures, Norwest Venture Partners, Accel, GV, General Catalyst and NEA opened SF shops, to name a few. Many of these firms, Benchmark, Kleiner and Accel, for example, held onto their Silicon Valley locations. Firms like True Ventures and Peter Thiel’s Founders Fund planted stakes in SF years prior. Both firms have operated SF offices since 2005; True Ventures, for its part, has managed a Palo Alto office from the get-go, as well.

“When we first started, it was [expected] that it would be maybe 60-40 Peninsula to the city; it’s actually turned out to be 80-20 SF to The Valley,” True Ventures co-founder Phil Black told TechCrunch. “For us, it was important to be near our customer: the founder. It’s important for us to be in and around where founders are doing their things.”

The transition out of The Valley is ongoing. Other VC funds are still in the process of opening their first SF offices as more partners beg for shorter commutes. Khosla Ventures, for example, is currently searching for an SF headquarters.

Silicon Valley real estate will likely remain a hot — or warm, at least — commodity, however. Why? Because long-time investors have lives established in that part of the bay, where they’ve built homes in well-kept, affluent cities like Woodside, Atherton and Los Altos.

Still, Y Combinator’s move highlights an increasingly adopted mantra: Silicon Valley isn’t the goldmine it used to be. For the best deals and greatest access to entrepreneurs, SF takes the cake — for now, that is. But with rising rents and a changing attitude toward geographically diverse founders, how long SF will remain the destination for top talent is an entirely different question.

Powered by WPeMatico

Young founders who want to start companies while still in school have an increasing number of resources to tap into that exist just for them. Students that want to learn how to build companies can apply to an increasing number of fast-track programs that allow them to gain valuable early stage operating experience. The energy around student entrepreneurship today is incredible. I’ve been immersed in this community as an investor and adviser for some time now, and to say the least, I’m continually blown away by what the next generation of innovators are dreaming up (from Analytical Space’s global data relay service for satellites to Brooklinen’s reinvention of the luxury bed).

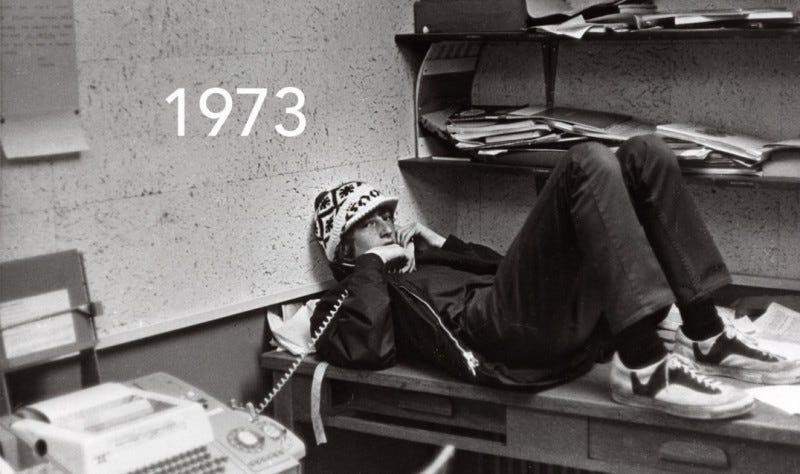

Bill Gates in 1973

First, let’s look at student founders and why they’re important. Student entrepreneurs have long been an important foundation of the startup ecosystem. Many students wrestle with how best to learn while in school —some students learn best through lectures, while more entrepreneurial students like author Julian Docks find it best to leave the classroom altogether and build a business instead.

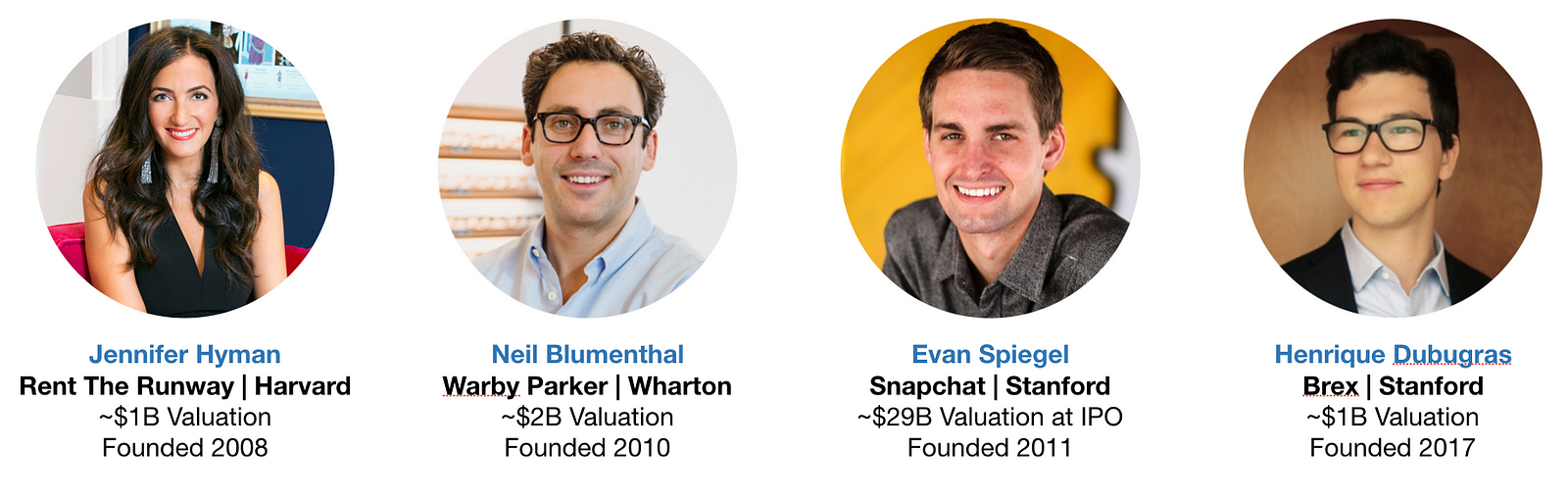

Indeed, some of our most iconic founders are Microsoft’s Bill Gates and Facebook’s Mark Zuckerberg, both student entrepreneurs who launched their startups at Harvard and then dropped out to build their companies into major tech giants. A sample of the current generation of marquee companies founded on college campuses include Snap at Stanford ($29B valuation at IPO), Warby Parker at Wharton (~$2B valuation), Rent The Runway at HBS (~$1B valuation), and Brex at Stanford (~$1B valuation).

Some of today’s most celebrated tech leaders built their first ventures while in school — even if some student startups fail, the critical first-time founder experience is an invaluable education in how to build great companies. Perhaps the best example of this that I could find is Drew Houston at Dropbox (~$9B valuation at IPO), who previously founded an edtech startup at MIT that, in his words, provided a: “great introduction to the wild world of starting companies.”

Student founders are everywhere, but the highest concentration of venture-backed student founders can be found at just 5 universities. Based on venture fund portfolio data from the last six years, Harvard, Stanford, MIT, UPenn, and UC Berkeley have produced the highest number of student-founded companies that went on to raise $1 million or more in seed capital. Some prospective students will even enroll in a university specifically for its reputation of churning out great entrepreneurs. This is not to say that great companies are not being built out of other universities, nor does it mean students can’t find resources outside a select number of schools. As you can see later in this essay, there are a number of new ways students all around the country can tap into the startup ecosystem. For further reading, PitchBook produces an excellent report each year that tracks where all entrepreneurs earned their undergraduate degrees.

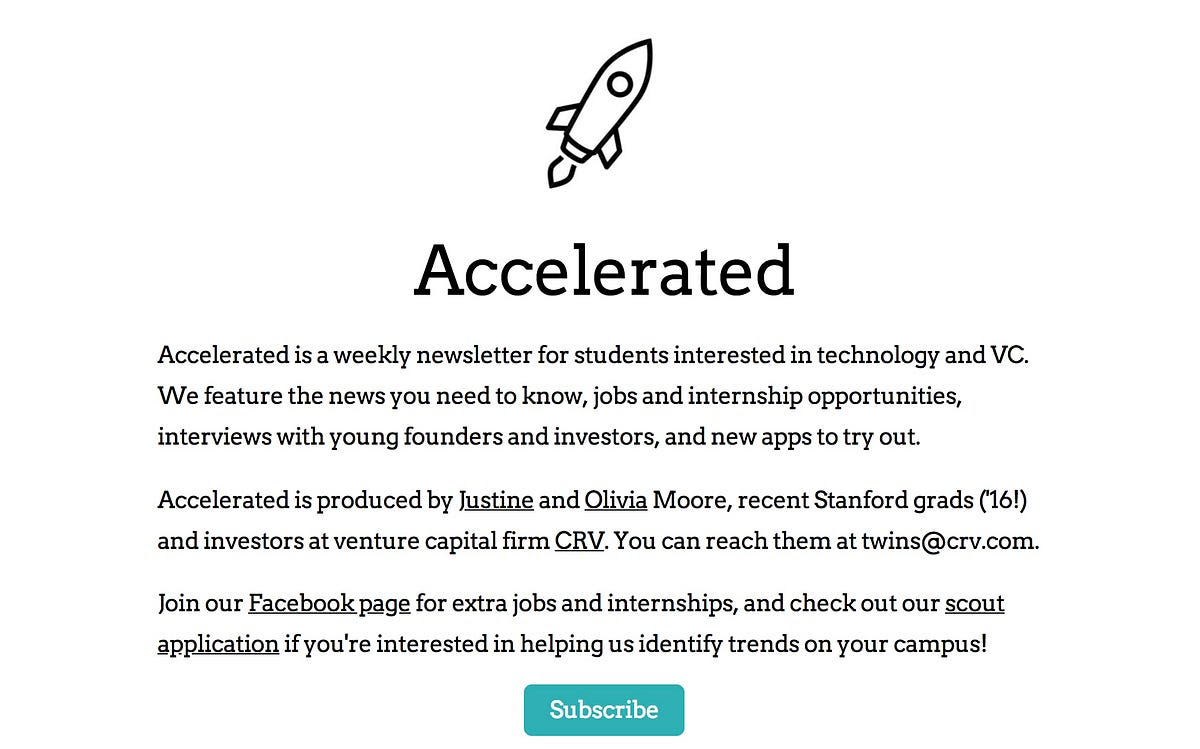

Student founders have a number of new media resources to turn to. New email newsletters focused on student entrepreneurship like Justine and Olivia Moore’s Accelerated and Kyle Robertson’s StartU offer new channels for young founders to reach large audiences. Justine and Olivia, the minds behind Accelerated, have a lot of street cred— they launched Stanford’s on-campus incubator Cardinal Ventures before landing as investors at CRV.

StartU goes above and beyond to be a resource to founders they profile by helping to connect them with investors (they’re active at 12 universities), and run a podcast hosted by their Editor-in-Chief Johnny Hammond that is top notch. My bet is that traditional media will point a larger spotlight at student entrepreneurship going forward.

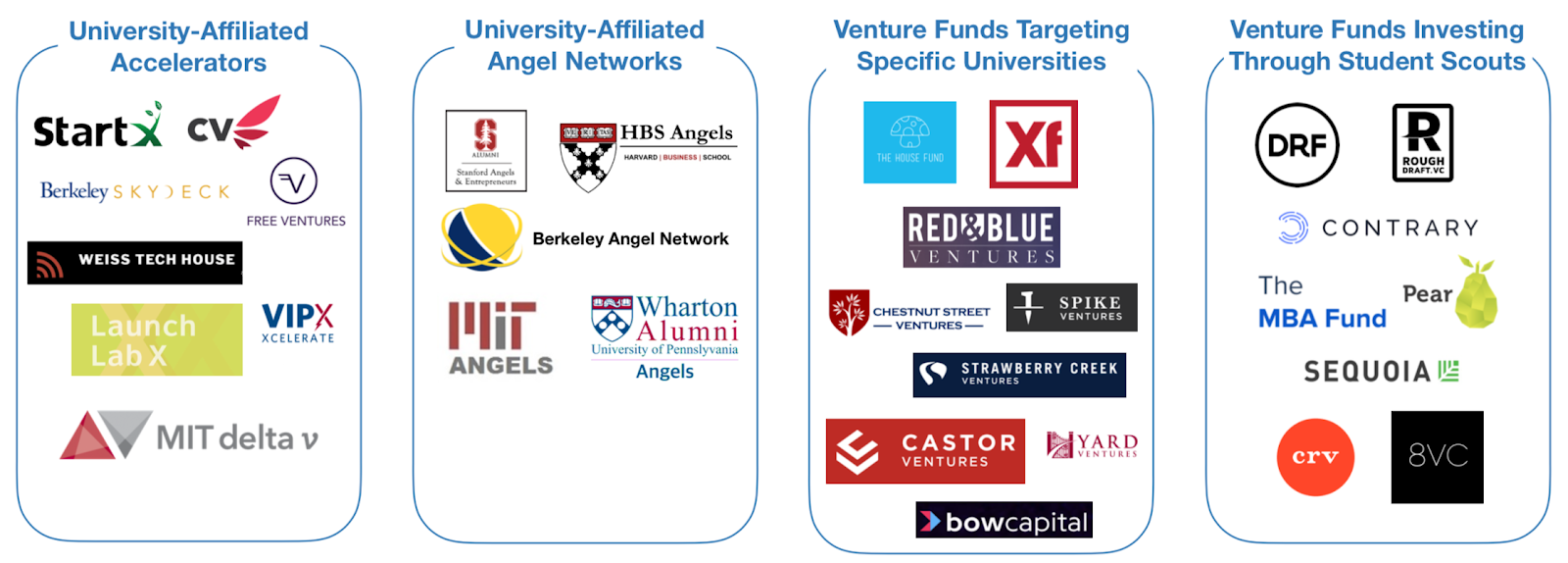

New pools of capital are also available that are specifically for student founders. There are four categories that I call special attention to:

While it is difficult to estimate exactly how much capital has been deployed by each, there is no denying that there has been an explosion in the number of programs that address the pre-seed phase. A sample of the programs available at the Top 5 universities listed above are in the graphic below — listing every resource at every university would be difficult as there are so many.

One alumni-centric fund to highlight is the Alumni Ventures Group, which pools LP capital from alumni at specific universities, then launches individual venture funds that invest in founders connected to those universities (e.g. students, alumni, professors, etc.). Through this model, they’ve deployed more than $200M per year! Another highlight has been student scout programs — which vary in the degree of autonomy and capital invested — but essentially empower students to identify and fund high-potential student-founded companies for their parent venture funds. On campuses with a large concentration of student founders, it is not uncommon to find student scouts from as many as 12 different venture funds actively sourcing deals (as is made clear from David Tao’s analysis at UC Berkeley).

Investment Team at Rough Draft Ventures

In my opinion, the two institutions that have the most expansive line of sight into the student entrepreneurship landscape are First Round’s Dorm Room Fund and General Catalyst’s Rough Draft Ventures. Since 2012, these two funds have operated a nationwide network of student scouts that have invested $20K — $25K checks into companies founded by student entrepreneurs at 40+ universities. “Scout” is a loose term and doesn’t do it justice — the student investors at these two funds are almost entirely autonomous, have built their own platform services to support portfolio companies, and have launched programs to incubate companies built by female founders and founders of color. Another student-run fund worth noting that has reach beyond a single region is Contrary Capital, which raised $2.2M last year. They do a particularly great job of reaching founders at a diverse set of schools — their network of student scouts are active at 45 universities and have spoken with 3,000 founders per year since getting started. Contrary is also testing out what they describe as a “YC for university-based founders”. In their first cohort, 100% of their companies raised a pre-seed round after Contrary’s demo day. Another even more recently launched organization is The MBA Fund, which caters to founders from the business schools at Harvard, Wharton, and Stanford. While super exciting, these two funds only launched very recently and manage portfolios that are not large enough for analysis just yet.

Over the last few months, I’ve collected and cross-referenced publicly available data from both Dorm Room Fund and Rough Draft Ventures to assess the state of student entrepreneurship in the United States. Companies were pulled from each fund’s portfolio page, then checked against Crunchbase for amount raised, accelerator participation, and other metrics. If you’d like to sift through the data yourself, feel free to ping me — my email can be found at the end of this article. To be clear, this does not represent the full scope of investment activity at either fund — many companies in the portfolios of both funds remain confidential and unlisted for good reasons (e.g. startups working in stealth). In fact, the In addition, data for early stage companies is notoriously variable in quality, even with Crunchbase. You should read these insights as directional only, given the debatable confidence interval. Still, the data is still interesting and give good indicators for the health of student entrepreneurship today.

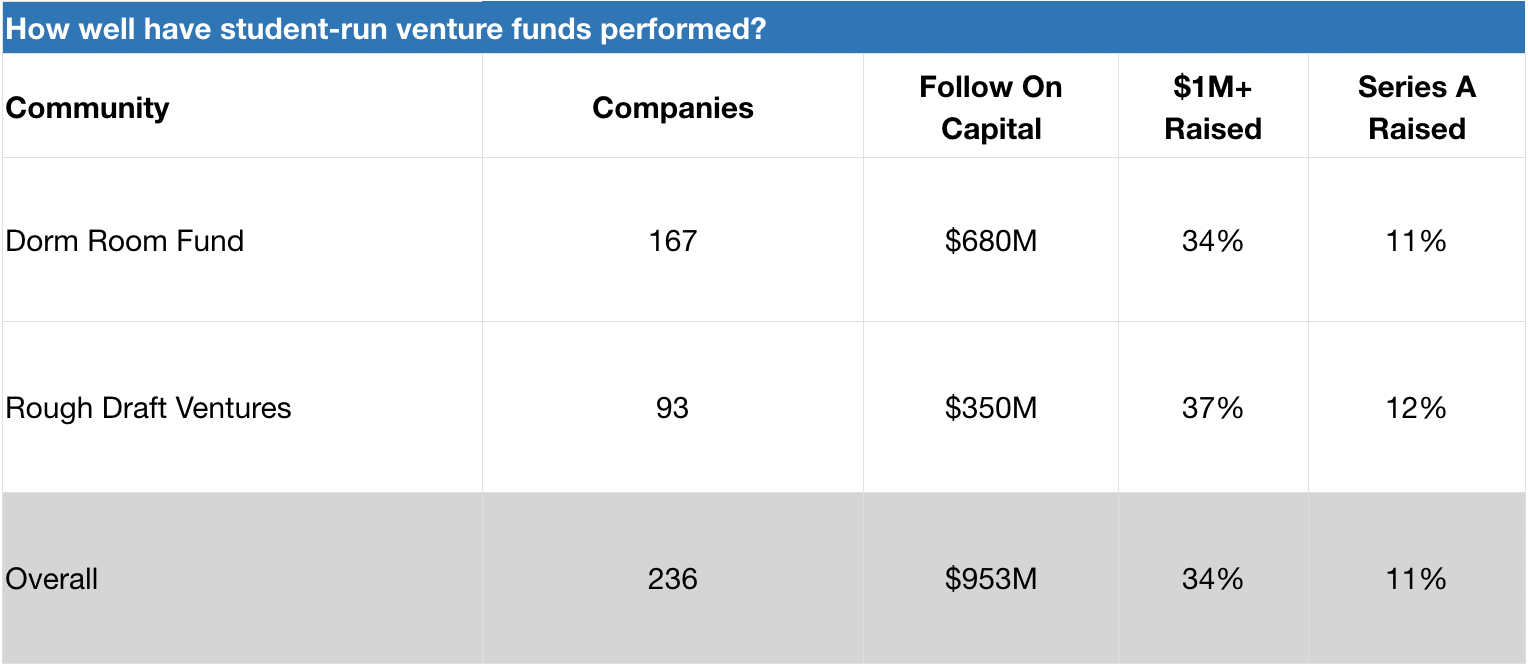

Dorm Room Fund and Rough Draft Ventures have invested in 230+ student-founded companies that have gone on to raise nearly $1 billion in follow on capital. These funds have invested in a diverse range of companies, from govtech (e.g. mark43, raised $77M+ and FiscalNote, raised $50M+) to space tech (e.g. Capella Space, raised ~$34M). Several portfolio companies have had successful exits, such as crypto startup Distributed Systems (acquired by Coinbase) and social networking startup tbh (acquired by Facebook). While it is too early to evaluate the success of these funds on a returns basis (both were launched just 6 years ago), we can get a sense of success by evaluating the rates by which portfolio companies raise additional capital. Taken together, 34% of DRF and RDV companies in our data set have raised $1 million or more in seed capital. For a rough comparison, CB Insights cites that 40% of YC companies and 48% of Techstars companies successfully raise follow on capital (defined as anything above $750K). Certainly within the ballpark!

Dorm Room Fund and Rough Draft Ventures companies in our data set have an 11–12% rate of survivorship to Series A. As a benchmark, a previous partner at Y Combinator shared that 20% of their accelerator companies raise Series A capital (YC declined to share the official figure, but it’s likely a stat that is increasing given their new Series A support programs. For further reading, check out YC’s reflection on what they’ve learned about helping their companies raise Series A funding). In any case, DRF and RDV’s numbers should be taken with a grain of salt, as the average age of their portfolio companies is very low and raising Series A rounds generally takes time. Ultimately, it is clear that DRF and RDV are active in the earlier (and riskier) phases of the startup journey.

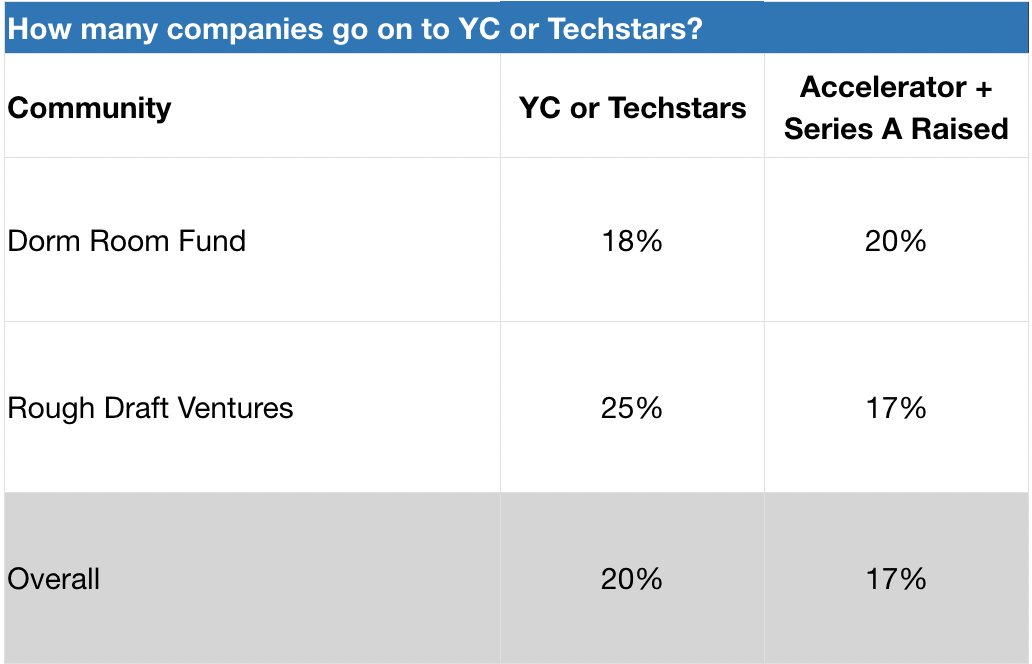

Dorm Room Fund and Rough Draft Ventures send 18–25% of their portfolio companies to Y Combinator or Techstars. Given YC’s 1.5% acceptance rate as reported in Fortune, this is quite significant! Internally, these two funds offer founders an opportunity to participate in mock interviews with YC and Techstars alumni, as well as tap into their communities for peer support (e.g. advice on pitch decks and application content). As a result, Dorm Room Fund and Rough Draft Ventures regularly send cohorts of founders to these prestigious accelerator programs. Based on our data set, 17–20% of DRF and RDV companies that attend one of these accelerators end up raising Series A venture financing.

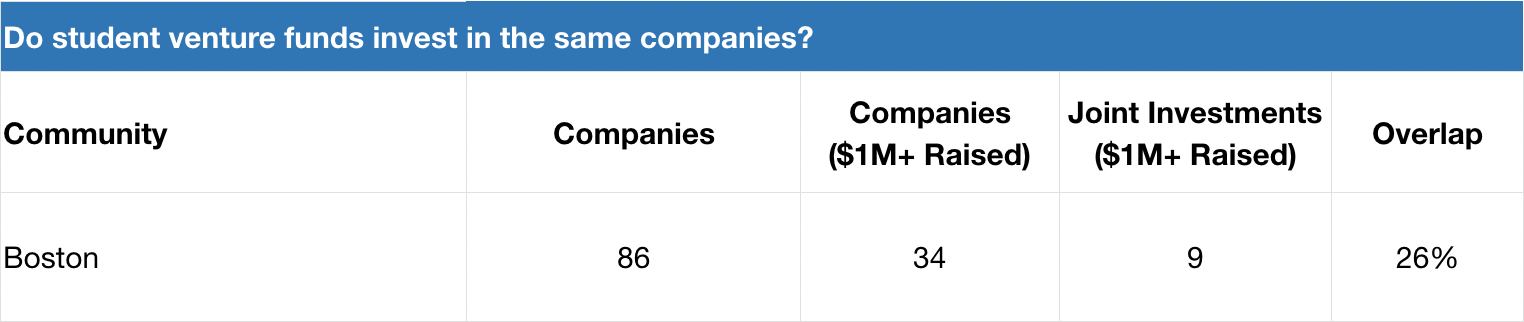

Dorm Room Fund and Rough Draft Ventures don’t invest in the same companies. When we take a deeper look at one specific ecosystem where these two funds have been equally active over the last several years — Boston — we actually see that the degree of investment overlap for companies that have raised $1M+ seed rounds sits at 26%. This suggests that these funds are either a) seeing different dealflow or b) have widely different investment decision-making.

Dorm Room Fund and Rough Draft Ventures should not just be measured by a returns-basis today, as it’s too early. I hypothesize that DRF and RDV are actually encouraging more entrepreneurial activity in the ecosystem (more students decide to start companies while in school) as well as improving long-term founder outcomes amongst students they touch (portfolio founders build bigger and more successful companies later in their careers). As more students start companies, there’s likely a positive feedback loop where there’s increasing peer pressure to start a company or lean on friends for founder support (e.g. feedback, advice, etc).Both of these subjects warrant additional study, but it’s likely too early to conduct these analyses today.

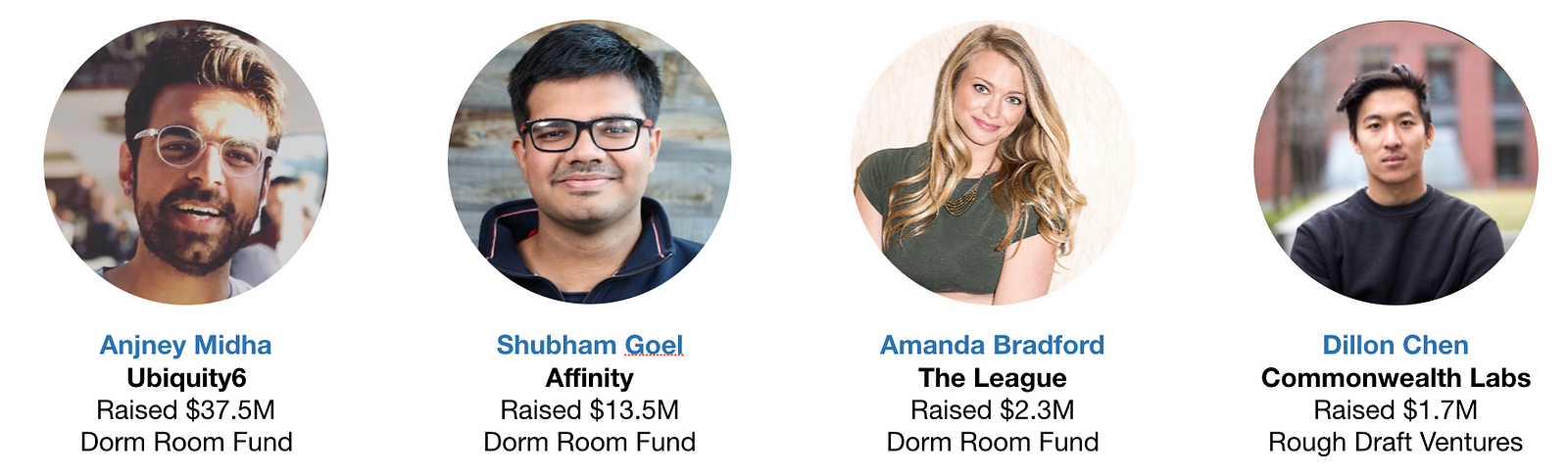

Dorm Room Fund and Rough Draft Ventures have impressive alumni that you will want to track. 1 in 4 alumni partners are founders, and 29% of these founder alumni have raised $1M+ seed rounds for their companies. These include Anjney Midha’s augmented reality startup Ubiquity6 (raised $37M+), Shubham Goel’s investor-focused CRM startup Affinity (raised $13M+), Bruno Faviero’s AI security software startup Synapse (raised $6M+), Amanda Bradford’s dating app The League (raised $2M+), and Dillon Chen’s blockchain startup Commonwealth Labs (raised $1.7M). It makes sense to me that alumni from these communities that decide to start companies have an advantage over their peers — they know what good companies look like and they can tap into powerful networks of young talent / experienced investors.

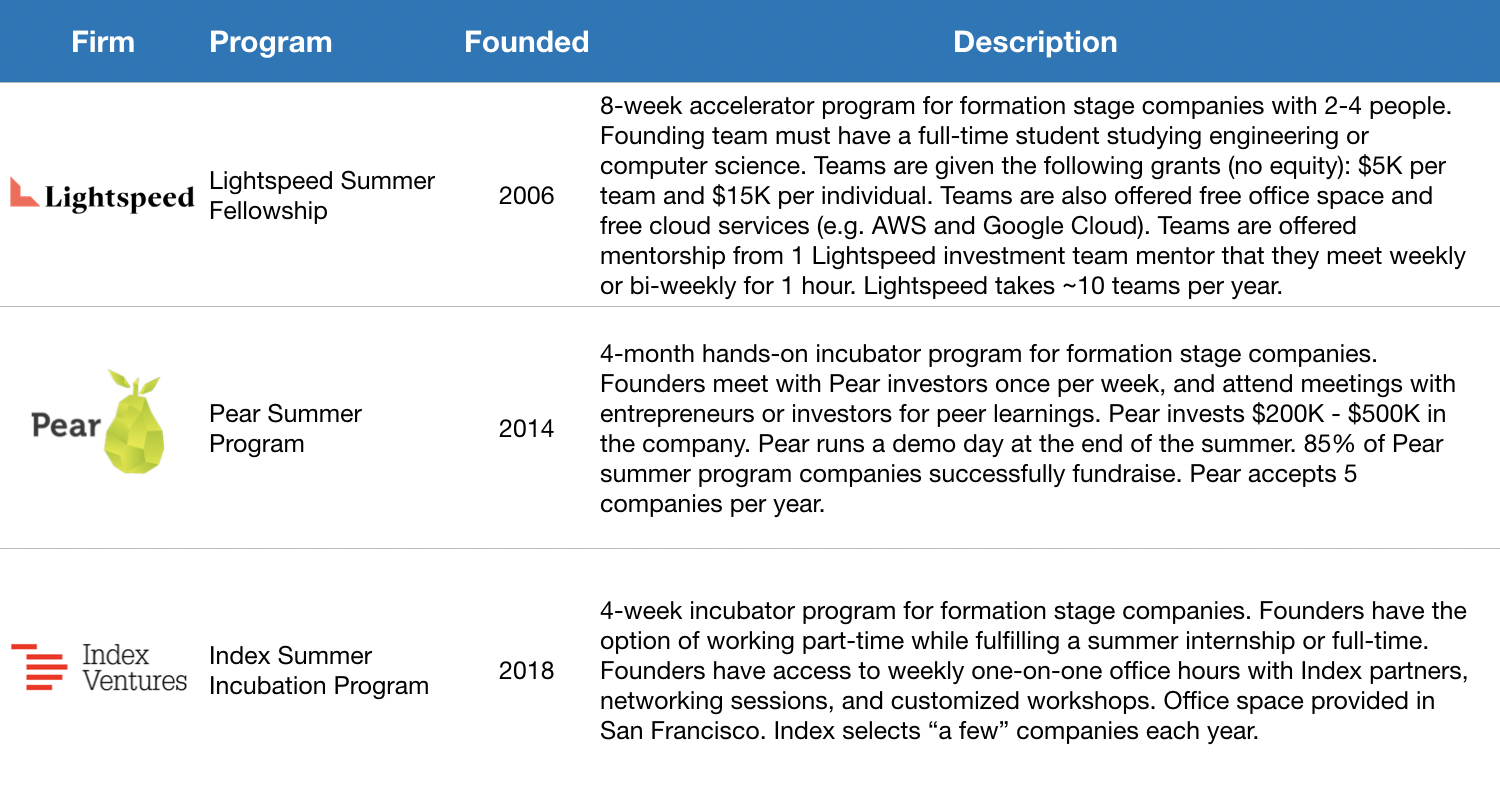

Beyond Dorm Room Fund and Rough Draft Ventures, some venture capital firms focus on incubation for student-founded startups. Credit should first be given to Lightspeed for producing the amazing Summer Fellows bootcamp experience for promising student founders — after all, Pinterest was built there! Jeremy Liew gives a good overview of the program through his sit-down interview with Afterbox’s Zack Banack. Based on a study they conducted last year, 40% of Lightspeed Summer Fellows alumni are currently active founders. Pear Ventures also has an impressive summer incubator program where 85% of its companies successfully complete a fundraise. Index Ventures is the latest to build an incubator program for student founders, and even accepts founders who want to work on an idea part-time while completing a summer internship.

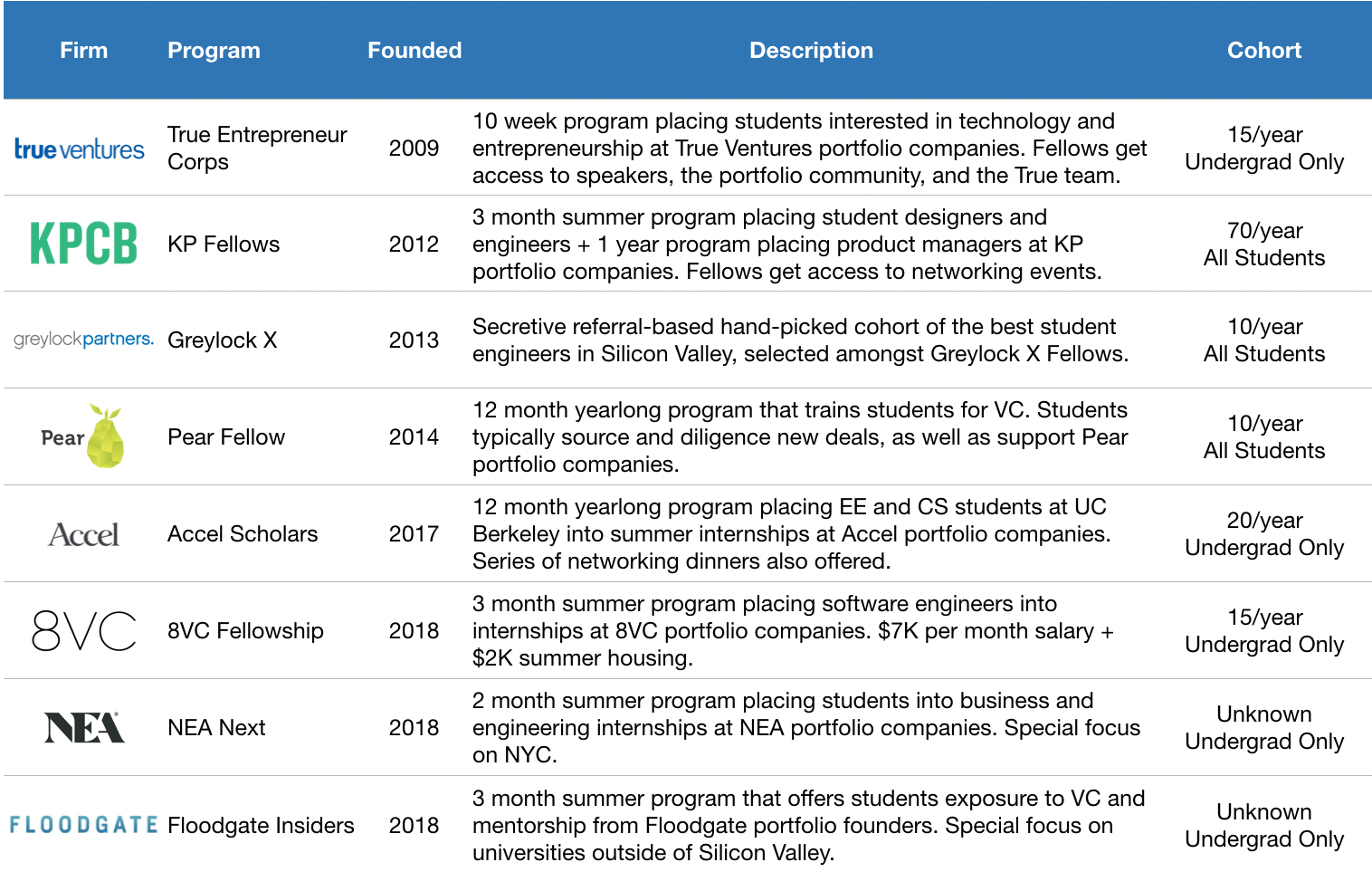

Let’s now look at students who want to join a startup before founding one. Venture funds have historically looked to tap students for talent, and are expanding the engagement lifecycle. The longest running programs include Kleiner Perkins’ class=”m_1196721721246259147gmail-markup–strong m_1196721721246259147gmail-markup–p-strong”> KP Fellows and True Ventures’ TEC Fellows, which focus on placing the next generation’s most promising product managers, engineers, and designers into the portfolio companies of their parent venture funds.

There’s also the secretive Greylock X, a referral-based hand-picked group of the best student engineers in Silicon Valley (among their impressive alumni are founders like Yasyf Mohamedali and Joe Kahn, the folks behind First Round-backed Karuna Health). As these programs have matured, these firms have recognized the long-run value of engaging the alumni of their programs.

More and more alumni are “coming back” to the parent funds as entrepreneurs, like KP Fellow Dylan Field of Figma (and is also hosting a KP Fellow, closing a full circle loop!). Based on their latest data, 10% of KP Fellows alumni are founders — that’s a lot given the fact that their community has grown to 500! This helps explain why Kleiner Perkins has created a structured path to receive $100K in seed funding to companies founded by KP Fellow alumni. It looks like venture funds are beginning to invest in student programs as part of their larger platform strategy, which can have a real impact over the long term (for further reading, see this analysis of platform strategy outcomes by USV’s Bethany Crystal).

KP Fellows in San Francisco

Venture funds are doubling down on student talent engagement — in just the last 18 months, 4 funds have launched student programs. It’s encouraging to see new funds follow in the footsteps of First Round, General Catalyst, Kleiner Perkins, Greylock, and Lightspeed. In 2017, Accel launched their Accel Scholars program to engage top talent at UC Berkeley and Stanford. In 2018, we saw 8VC Fellows, NEA Next, and Floodgate Insiders all launch, targeting elite universities outside of Silicon Valley. Y Combinator implemented Early Decision, which allows student founders to apply one batch early to help with academic scheduling. Most recently, at the start of 2019, First Round launched the Graduate Fund (staffed by Dorm Room Fund alumni) to invest in founders who are recent graduates or young alumni.

Given more time, I’d love to study the rates by which student founders start another company following investments from student scout funds, as well as whether or not they’re more successful in those ventures. In any case, this is an escalation in the number of venture funds that have started to get serious about engaging students — both for talent and dealflow.

Student entrepreneurship 2.0 is here. There are more structured paths to success for students interested in starting or joining a startup. Founders have more opportunities to garner press, seek advice, raise capital, and more. Venture funds are increasingly leveraging students to help improve the three F’s — finding, funding, and fixing. In my personal view, I believe it is becoming more and more important for venture funds to gain mindshare amongst the next generation of founders and operators early, while still in school.

I can’t wait to see what’s next for student entrepreneurship in 2019. If you’re interested in digging in deeper (I’m human — I’m sure I haven’t covered everything related to student entrepreneurship here) or learning more about how you can start or join a startup while still in school, shoot me a note at sxu@dormroomfund.com. A massive thanks to Phin Barnes, Rei Wang, Chauncey Hamilton, Peter Boyce, Natalie Bartlett, Denali Tietjen, Eric Tarczynski, Will Robbins, Jasmine Kriston, Alicia Lau, Johnny Hammond, Bruno Faviero, Athena Kan, Shohini Gupta, Alex Immerman, Albert Dong, Phillip Hua-Bon-Hoa, and Trevor Sookraj for your incredible encouragement, support, and insight during the writing of this essay.

Powered by WPeMatico

Humio, a startup that provides a real-time log analysis platform for on-premises and cloud infrastructures, today announced that it has raised a $9 million Series A round led by Accel. It previously raised its seed round from WestHill and Trifork.

The company, which has offices in San Francisco, the U.K. and Denmark, tells me that it saw a 13x increase in its annual revenue in 2018. Current customers include Bloomberg, Microsoft and Netlify .

“We are experiencing a fundamental shift in how companies build, manage and run their systems,” said Humio CEO Geeta Schmidt. “This shift is driven by the urgency to adopt cloud-based and microservice-driven application architectures for faster development cycles, and dealing with sophisticated security threats. These customer requirements demand a next-generation logging solution that can provide live system observability and efficiently store the massive amounts of log data they are generating.”

To offer them this solution, Humio raised this round with an eye toward fulfilling the demand for its service, expanding its research and development teams and moving into more markets across the globe.

As Schmidt also noted, many organizations are rather frustrated by the log management and analytics solutions they currently have in place. “Common frustrations we hear are that legacy tools are too slow — on ingestion, searches and visualizations — with complex and costly licensing models,” she said. “Ops teams want to focus on operations — not building, running and maintaining their log management platform.”

To build this next-generation analysis tool, Humio built its own time series database engine to ingest the data, with open-source tools like Scala, Elm and Kafka in the backend. As data enters the pipeline, it’s pushed through live searches and then stored for later queries. As Humio VP of Engineering Christian Hvitved tells me, though, running ad-hoc queries is the exception, and most users only do so when they encounter bugs or a DDoS attack.

The query language used for the live filters is also pretty straightforward. That was a conscious decision, Hvitved said. “If it’s too hard, then users don’t ask the question,” he said. “We’re inspired by the Unix philosophy of using pipes, so in Humio, larger searches are built by combining smaller searches with pipes. This is very familiar to developers and operations people since it is how they are used to using their terminal.”

Humio charges its customers based on how much data they want to ingest and for how long they want to store it. Pricing starts at $200 per month for 30 days of data retention and 2 GB of ingested data.

Powered by WPeMatico

Electric scooter startup Bird is said to be nearing a deal to extend its Series C funding with an additional $300 million led by cross-over investor Fidelity, according to an Axios report. Bird declined to comment.

Fidelity has not previously invested in Bird and is reportedly doing so at a flat pre-money valuation of $2 billion, which Bird earned with a $300 million Sequoia-led financing in June. Santa Monica-based Bird has raised more than $400 million in venture capital funding to date from investors, including Accel, CRV, Greycroft, Index Ventures, Upfront Ventures, Craft Ventures and Tusk Ventures.

The investment comes at a time when many investors are losing faith in scooter startups’ claims to be the solution to the problem of last-mile transportation, as companies in the space display poor unit economics, faulty batteries and a general air of undependability. Lime, Bird’s biggest e-scooter competitor, has at least expanded its suite of micro-mobility offerings from bikes and scooters to LimePods, a line of shareable vehicles available in Seattle, to peak investor interest. San Francisco-based Lime has been seen pitching to investors in Silicon Valley recently, too, with reports indicating it’s looking for a $400 million investment at a $3 billion valuation — more than three times the valuation it garnered with a $335 million round in July.

Powered by WPeMatico

The lines between streetwear and luxury fashion have blurred in recent years, especially as excitement around sneaker brands like Yeezy and Off-White has soared.

A marriage between a luxury fashion marketplace and a sneaker and streetwear reseller seems like a natural way to wrap up M&A in 2018. With that said, Farfetch has acquired New York-based Stadium Goods, opting to pay $250 million for the sneaker startup in a combination of cash and Farfetch stock. Headquartered in London, Farfetch went public on the New York Stock Exchange in September, pricing its shares at $20 apiece and raising $885 million in the process.

What’s more impressive is Stadium Goods’ journey to exit. The company, which sells new and deadstock products online and in a brick-and-mortar store in New York’s Soho neighborhood, was founded in 2015 by John McPheters and Jed Stiller and had only raised $4.6 million in venture capital funding from Forerunner Ventures, The Chernin Group and Mark Cuban, who is an advisor to the startup.

“There was a time not that long ago when you couldn’t wear sneakers and streetwear to nightclubs and restaurants,” McPheters, Stadium Goods’ chief executive officer, told TechCrunch. “But adoption of the stuff we are selling has continued to grow at a very large clip.”

The sale to Farfetch not only provides a major boost to the sneaker tech ecosystem, which is surprisingly much larger than those who aren’t familiar with it might have guessed, but it’s yet another successful e-commerce exit for Kirsten Green, the founding partner of Forerunner Ventures, who’s also backed Dollar Shave Club and Bonobos — direct-to-consumer retailers that sold for $1 billion and $310 million, respectively.

Stadium Goods founders John McPheters (left) and Jed Stiller

Farfetch boarded the sneaker and streetwear hype train a while ago when it incorporated brands like Nike’s Jordan, pairs of which sell for more than $1,000 on the site. The company doubled down on sneakers earlier this year when it began integrating Stadium Goods products. After noticing high-demand, Farfetch founder and CEO José Neves tells TechCrunch, they began acquisition talks with the startup. Stadium Goods will remain independent as part of the deal, with McPheters and Stiller staying on to lead the brand forward. The company’s portfolio of shoes and apparel will be fully available on Farfetch’s e-commerce platform in the coming months.

“Luxury streetwear is a significant part of our business,” Neves said. “For many years now, we have had the largest collection of Off-White, for example, on the internet … What we did not have was the resale, secondary market. It was clear this was an interesting opportunity.”

Together, Farfetch and Stadium Goods will focus on international growth. McPheters tells TechCrunch Stadium Goods already had a significant international base of customers, but a partnership with Farfetch gives them the tools to go places they’ve never been.

“In my mind, we are only just beginning,” McPheters said. “As more and more customers get comfortable with purchasing aftermarket items, we are going to continue to grow.”

The global athletic footwear industry is expected to be worth $95 billion by 2025. Meanwhile, sneaker resale is a $1 billion market and growing, fueled by a cohort of startups making it easier than ever for sneakerheads to locate rare shoes online and have them delivered to their doorsteps. That includes Stadium Goods, Flight Club, GOAT and StockX.

All four of these resellers, which ensure authentication of their products, are backed by VCs. Flight Club merged with GOAT earlier this year and together the pair raised a $60 million Series C. Before that, GOAT had brought in $30 million for its secondary market for collectible shoes from Accel, Upfront Ventures, Matrix Partners and more. StockX, for its part, has raised just over $50 million from Mark Wahlberg, Scooter Braun, Wale, Eminem, SV Angel and others.

According to Crunchbase data, VCs have funneled more than $200 million into sneaker startups in the past two years. Now, given the size of Stadium Goods’ exit, investment in the space will likely pick up significantly as other VCs hope to land an exit multiple that substantial.

Whether the reselling market will continue to expand is in question. Some have called it a bubble poised to burst, claiming it’s at its “height in popularity.” Why? Because corporate shoe brands like Nike and Adidas are keenly aware of the secondary market for their products and how they, too, can profit from it. If they decide to increase the supply of particular shoe models hot on the secondary market, they can radically disrupt the reseller economy. McPheters, however, says this doesn’t concern him.

“Brands need to strangle the demand to keep driving excitement in the space,” McPheters said. “They count on that hype to really move the needle.”

Powered by WPeMatico

Transit, a company that built a mobile app designed to help people in cities live without cars, has raised $17.5 million from two automakers in a Series B round.

The round was led by RenaultNissan-Mitsubishi’s joint investment arm Alliance Ventures. InMotion Ventures, Jaguar Land Rover’s venture capital fund, also joined the round, as well as two past investors, Accel and Real Ventures.

RenaultNissan-Mitsubishi and Jaguar Land Rover’s investment would have seemed counterintuitive five years ago. But this is 2018. It’s the year of the scooter wars and micro-mobility; it’s also a time of transition for automakers that are looking to diversify their traditional business of building and selling cars.

Founded in 2012, Transit started as an app to help people check departure times for buses and trains. It’s grown into a mobile app platform that enables multi-modal transportation, integrating public transit, ride hailing, bike sharing and scooter sharing. The mobile app, which provides real-time data from transit agencies with user crowdsourcing, gives users notifications from their ride. The app then tracks the real-time location of the vehicle and notifies the user when to leave for their stop, when to disembark. and sends adjusted ETAs. Transit is now used by transit agencies, including Boston’s MBTA, Baltimore’s MDOT MTA, Silicon Valley’s VTA, Tampa Bay’s PSTA and Montreal’s STM.

The company wants to be transit and company agnostic, so, it’s a big proponent of open APIs. Montreal, where the company is based, is a model of what Transit wants to be everywhere. In Montreal, people can use the app for car sharing, bike sharing, to order an Uber or use public transit, COO Jake Sion explained.

Transit, which operates in 175 cities globally, will use the injection of capital to scale operations and improve the platform by integrating various services and payment methods on the app.

“This investment, which will advance Transit’s efforts to make mobility seamless and accessible in cities, fits with the Alliance 2022 strategy to become a leader in robo-vehicle ride-hailing mobility services and a provider of vehicles for public transit use and car-sharing,” François Dossa, Alliance Global vice president of ventures and open innovation, said in a statement.

Powered by WPeMatico

Instana, an application performance monitoring (APM) service with a focus on modern containerized services, today announced that it has raised a $30 million Series C funding round. The round was led by Meritech Capital, with participation from existing investor Accel. This brings Instana’s total funding to $57 million.

The company, which counts the likes of Audi, Edmunds.com, Yahoo Japan and Franklin American Mortgage as its customers, considers itself an APM 3.0 player. It argues that its solution is far lighter than those of older players like New Relic and AppDynamics (which sold to Cisco hours before it was supposed to go public). Those solutions, the company says, weren’t built for modern software organizations (though I’m sure they would dispute that).

What really makes Instana stand out is its ability to automatically discover and monitor the ever-changing infrastructure that makes up a modern application, especially when it comes to running containerized microservices. The service automatically catalogs all of the endpoints that make up a service’s infrastructure, and then monitors them. It’s also worth noting that the company says that it can offer far more granular metrics that its competitors.

Instana says that its annual sales grew 600 percent over the course of the last year, something that surely attracted this new investment.

“Monitoring containerized microservice applications has become a critical requirement for today’s digital enterprises,” said Meritech Capital’s Alex Kurland. “Instana is packed with industry veterans who understand the APM industry, as well as the paradigm shifts now occurring in agile software development. Meritech is excited to partner with Instana as they continue to disrupt one of the largest and most important markets with their automated APM experience.”

The company plans to use the new funding to fulfill the demand for its service and expand its product line.

Powered by WPeMatico