Accel

Auto Added by WPeMatico

Auto Added by WPeMatico

Risk and compliance management platform VComply announced today that it has picked up a $2.5 million seed round led by Accel Partners for its international growth plan. The funding will be used to acquire more customers in the United States, open a new office in the United Kingdom to support customers in Europe and expand its presence in New Zealand and Australia.

The company was founded in 2016 by CEO Harshvardhan Kariwala and has customers in a wide range of industries, including Acreage Holdings, Ace Energy Solutions, CHD, the United Kingdom’s Department of International Trade and Burger King. It currently claims about 4,000 users in more than 100 countries. VComply is meant to be used by all departments in a company, with compliance information organized into a central dashboard.

While there are already a roster of governance, risk and compliance management solutions on the market (including ones from Oracle, HPE, Thomson Reuters, IBM and other established enterprise software companies), VComply’s competitive edge may be its flexibility, simple user interface and easy deployment (the company claims customers can on-board and start using the solution for compliance tasks in about 30 minutes). It also seeks out smaller companies whose needs have not been met by compliance solutions meant for large enterprises.

Kariwala told TechCrunch in an email that he began thinking of creating a new risk and compliance solution while working at his first startup, LIME Learning Systems, an education management platform, after being hit with a $4,000 penalty due to a non-compliance issue.

“Believe me, $4,000 really hurts when you’re bootstrapped and trying to save every single cent you can. In this case, I had asked our outsourced accounting partners to manage this compliance and they forgot!,” he said. After talking to other entrepreneurs, he realized compliance posed a challenge for most of them. LIME’s team built an internal compliance tracking tool for their own use, but also shared it with other people. After getting good feedback, Kariwala realized that despite the many governance, risk and compliance management solutions already on the market, there was still a gap in the market, especially for smaller businesses.

VComply is designed so organizations can customize it for their industry’s regulations and standards, as well as their own workflow and data needs, with competitive pricing for small to medium-sized organizations (a subscription starts at $3,999 a year).

“Most of the traditional GRC solutions that exist today are expensive, have a steep learning curve and entail a prolonged deployment. Not only are they expensive, they are also rigid, which means that organizations have little to no control or flexibility,” Kariwala said. “A GRC tool is often looked at as an expense, while it should really be treated as an investment. It is particularly the SMB sector that suffers the most. With the current solutions costing thousands of dollars (and sometimes millions), it becomes the least of their priorities to invest in a GRC platform, and as a result they fall prey to heightened risks and hefty penalties for non-compliance.”

In a press statement, Accel partner Dinesh Katiyar said, “The first generation of GRC solutions primarily allowed companies to comply with industry-mandated regulations. However, the modern enterprise needs to govern its operations to maintain integrity and trust, and monitor internal and external risks to stay successful. That is where VComply shines, and we’re delighted to be partnering with a company that can redefine the future of enterprise risk management.”

Powered by WPeMatico

Sam Lessin, a former product management executive at Facebook and old friend to Mark Zuckerberg, incorporated his latest startup under the name “Fin Exploration Company.”

Why? Well, because he wanted to explore. The company — co-founded alongside Andrew Kortina, best known for launching the successful payments app Venmo — was conceived as a consumer voice assistant in 2015 after the two entrepreneurs realized the impact 24/7 access to a virtual assistant would have on their digital to-do lists.

The thing is, developing an AI assistant capable of booking flights, arranging trips, teaching users how to play poker, identifying places to purchase specific items for a birthday party and answering wide-ranging zany questions like “can you look up a place where I can milk a goat?” requires a whole lot more human power than one might think. Capital-intensive and hard-to-scale, an app for “instantly offloading” chores wasn’t the best business. Neither Lessin nor Kortina will admit to failure, but Fin‘s excursion into B2B enterprise software eight months ago suggests the assistant technology wasn’t a billion-dollar idea.

Staying true to its name, the Fin Exploration Company is exploring again.

Powered by WPeMatico

Slack, the popular workplace messaging company, is expected to list on the New York Stock Exchange on Thursday in the second major direct listing in the U.S. after Spotify introduced the concept to investors in April of last year.

At this point, plenty of industry observers think it makes sound sense for Slack to embrace the direct listing approach, wherein a company places its stock on a public exchange without raising any money or using underwriters. Though the company warned last week that its operating losses are widening as it chases new customers, it has $800 million on its balance sheet, meaning it doesn’t need to raise more right now.

Slack also doesn’t need underwriters who typically discount a company’s shares in order to ensure that they appreciate in value when they begin trading. It’s a known brand in the tech world, and that universe is broadening by the day. Put another way, Slack doesn’t need to be “sold” for investors to want to snap up its shares.

Still, we wondered about some of the thinking that has gone into preparing Slack for its move into the world of publicly traded companies, so we talked with a couple of people who are familiar with what’s happening behind the scenes to find out more. They asked not to be named, but here’s what we learned:

1) Unlike with the popular streaming music platform Spotify, which has more than 100 million premium subscribers and roughly twice as many active monthly users, Slack wasn’t as well-known to Wall Street as Silicon Valley might imagine. In fact, we’re told the bankers that were selected to advise Slack on its offering — Morgan Stanley, Goldman Sachs and Allen & Co., which are the same three that advised Spotify — had to provide more education to analysts and institutional investors this time around.

2) There will (hopefully) be enough shares to go around, while also not a glut of them. The big concern in a direct offering — which does not feature a lock-up period — is that too many people will dump their shares on the market, crushing the company’s share price, or else that too few will part with their holdings, turning the buying and selling of the company’s shares into a financial game of chicken. We’ll see what happens here, but we’re told the banks have spent the last six months trying to ensure that many — but not all — of the company’s institutional shareholders will be selling some of their stakes at the offering, Also worth noting is that unlike with Spotify, some Slack employees have restricted stock units that will vest upon its public listing and so be part of the supply of shares on its first day.

3) In establishing guidance around how Spotify’s shares should be valued, the banks advising the company looked almost entirely to its private market trades, of which there were many. There has been less secondary activity with Slack’s shares, so the banks are likely to rely on these sales but also to use other inputs. We’ll learn soon enough what they settle on, but based on the latest prices at which its shares have traded in the private market, Slack’s presumed valued right now is at $16.7 billion, or 36 times trailing 12-month sales.

4) You might imagine that banks hate direct listings because of the rich underwriting fees they aren’t collecting, and they probably do. Still, even with a direct listing, they get paid pretty well, thanks to both advisory fees and also because investors often trade through the banks named as advisers in the prospectus. There are also fewer mouths to feed on a deal with a direct listing. In Slack’s case — as happened with Spotify — Morgan Stanley, Goldman Sachs and Allen & Co. will reportedly reap almost all of the spoils — or a reported 90% of the $22 million in fees earmarked for all the advisers involved in the deal. In a traditional IPO, a longer number of banks that promise research coverage are given shares to sell, which eats into lead underwriters’ allotment.

5) One risk that Slack shouldn’t necessarily run into but that may have adversely impacted Uber’s IPO is its investor base. According to Slack’s S-1, its biggest outside shareholders include Accel (it owns 24% sailing into the offering), Andreessen Horowitz (13.3%), Social Capital (10.2%) and SoftBank (7.3 %). Why it matters: Slack doesn’t have to worry about less traditional private company backers like mutual funds not wanting to buy up its shares because they’re too busy trying to offload some.

6) Direct listings may well become a more popular product for consumer companies because companies can avoid further dilution, and there’s no lock-up on their shares, creating a shorter path to liquidity for the company and its employees and its investors. Still, Slack is probably anomalous as an enterprise company with a high enough profile to pull one off. The listings are really for companies that don’t need money any time soon and whose shares are already of interest to investors, who don’t need inducements to pay attention.

7) This is the second direct listing of a highly valued privately held company and, for the second time, it’s happening on the NYSE, with the same market maker, Citadel Securities, charged with ensuring orderly trading; the same bank, Morgan Stanley, selected to advise Citadel; and even the same law firms that worked on Spotify’s direct listing pulled back into service.

It’s nice if you’re part of this particular club, and no one can blame Slack for not wanting to reinvent the wheel. But one wonders how nervous it makes Nasdaq, as well as other banks and law firms, to be shut out of this process a second time.

Powered by WPeMatico

Almost every organization, regardless of size, is inundated with meetings, so much so it’s often hard to find dedicated time to do actual work. Clockwise wants to change that by bringing machine learning to the calendar to help employees free up time. Today, it announced an $11 million Series A investment, and made the product, which had been in beta, generally available.

The round was co-led led by Greylock and Accel . Other investors included Slack Fund, Michael Ovitz, Ellen Levy, George Hu, Soraya Darabi, SV Angel and Jay Simons. The company has raised a total of $13 million.

Matt Martin, CEO and co-founder at Clockwise, says the company’s mission is to help employees make time for what matters, and they are doing that by applying machine learning to the calendar to free up blocks of time to concentrate on work. Calendars have tended to be pretty static, and this provides a way to bring a level of intelligence to automatically shift meetings to a better time when it makes sense.

After you download Clockwise you can set parameters for which meetings can be moved and which are set in stone, and other preferences. As Martin wrote in a blog post announcing the new tool, this gives employees “uninterrupted blocks of time to focus, think and innovate.” For now, it’s available for G Suite users.

Gif: Clockwise

You may think this is a one-trick pony that will be hard to scale, but Martin says in the past few months, Clockwise has recovered thousands of hours, and as they gain more data, the tool will get even more intelligent about meeting shifting.

Certainly his investors see the potential. John Lilly, who is leading the investment at Greylock, believes Clockwise is filling a huge unfilled need inside organizations. “Clockwise is focused on helping individuals and teams retake ownership of their time. This is not an easy feat — building the Clockwise product requires a sophisticated understanding of machine learning, user interaction and systems design breakthrough,” Lilly said.

Clockwise founders were part of the team at RelateIQ, a company Salesforce bought for $390 million in 2014. Since leaving RelateIQ they decided to put that experience to work on making the calendar more efficient.

Powered by WPeMatico

Slack wants to be the new operating system for teams, something it has made clear on more than one occasion, including in its recent S-1 filing. To accomplish that goal, it put together an in-house $80 million venture fund in 2015 to invest in third-party developers building on top of its platform.

Weeks ahead of its direct listing on The New York Stock Exchange, it continues to put that money to work.

Troops is the latest to land additional capital from the enterprise giant. The New York-based startup helps sales teams communicate with a customer relationship management tool plugged directly into Slack. In short, it automates routine sales management activities and creates visibility into important deals through integrations with employee emails and Salesforce.

Troops founder and chief executive officer Dan Reich, who previously co-founded TULA Skincare, told TechCrunch he opted to build a Slackbot rather than create an independent platform because Slack is a rocket ship and he wanted a seat on board: “When you think about where Slack will go in the future, it’s obvious to us that companies all over the world will be using it,” he said.

Troops has raised $12 million in Series B funding in a round led by Aspect Ventures, with participation from the Slack Fund, First Round Capital, Felicis Ventures, Susa Ventures, Chicago Ventures, Hone Capital, InVision founder Clark Valberg and others. The round brings Troops’ total raised to $22 million.

Launched in 2015 by New York tech veterans Reich, Scott Britton and Greg Ratner, the trio weren’t initially sure of Slack’s growth trajectory. It wasn’t until Slack confirmed its intent to support the developer ecosystem with a suite of developer tools and a fund that the team focused its efforts on building a Slackbot.

“People sometimes thought of us, at least in the early days, as a little bit crazy,” Reich said. “But now Slack is the fastest-growing SaaS company ever.”

“We think the biggest opportunity in the [enterprise SaaS] category is going to be tools oriented around the customer-facing employee (CRM), and that’s where we are innovating,” he added.

Troops’ tools are helpful for any customer-facing team, Reich explains. Envoy, WeWork, HubSpot and a few hundred others are monthly paying subscribers of the tool, using it to interact with their CRM in a messaging interface and to receive notifications when a deal has closed. Troops integrates with Salesforce, so employees can use it to search records, schedule automatic reports and celebrate company wins.

Slack, in partnership with a number of venture capital funds, including Accel, Kleiner Perkins and Index, has also deployed capital to a number of other startups, like Lattice, Drafted and Loom.

With Slack’s direct listing afoot, the Troops team is counting on the imminent and long-term growth of the company’s platform.

“We think it’s still early days,” Reich said. “In the future, we see every company using something like Troops to manage their day-to-day.”

Powered by WPeMatico

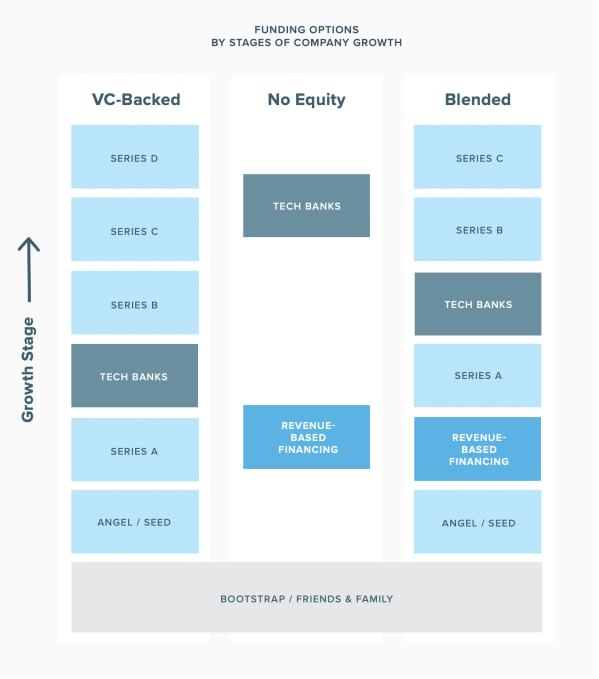

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

Slack, the ubiquitous workplace messaging tool, will make its pitch to prospective shareholders on Monday at an invite-only event in New York City, the company confirmed in a blog post on Wednesday. Slack stock is expected to begin trading on the New York Stock Exchange as soon as next month.

Slack, which is pursuing a direct listing, will live stream Monday’s Investor Day on its website.

An alternative to an initial public offering, direct listings allow businesses to forgo issuing new shares and instead sell directly to the market existing shares held by insiders, employees and investors. Slack, like Spotify, has been able to bypass the traditional roadshow process expected of an IPO-ready business, as well as some of the exorbitant Wall Street fees.

Spotify, if you remember, similarly live streamed an event that is typically for investors eyes only. If Slack’s event is anything like the music streaming giant’s, Slack co-founder and chief executive officer Stewart Butterfield will speak to the company’s greater mission alongside several other executives.

Slack unveiled documents for a public listing two weeks ago. In its SEC filing, the company disclosed a net loss of $138.9 million and revenue of $400.6 million in the fiscal year ending January 31, 2019. That’s compared to a loss of $140.1 million on revenue of $220.5 million for the year before.

Additionally, the company said it reached 10 million daily active users earlier this year across more than 600,000 organizations.

Slack has previously raised a total of $1.2 billion in funding from investors, including Accel, Andreessen Horowitz, Social Capital, SoftBank, Google Ventures and Kleiner Perkins.

Powered by WPeMatico

Airbnb has completed its acquisition of the last-minute hotel booking application, HotelTonight, the company announced on Monday. The deal is Airbnb’s largest M&A transaction yet, and will accelerate the home-sharing giant’s growth as it gears up for an initial public offering.

Airbnb reportedly began talks to acquire HotelTonight months ago, and finally confirmed its intent to acquire the business in early March. Reports indicated a price tag of more than $400 million; Airbnb declined to comment on the size of the deal.

As part of the deal, HotelTonight co-founder and chief executive officer Sam Shank will lead the boutique hotel category at Airbnb, one of the company’s newer units meant to help it scale beyond treehouses and quirky homes.

“When we founded HotelTonight, we sought to reimagine the hotel booking experience to be more simple, fast and fun, and to better connect travelers with the world’s best boutique and independent hotels,” Shank said in a statement. “We are delighted to take this vision to new heights as part of Airbnb.”

Shank launched the San Francisco-based company in 2010. Most recently, it was valued at $463 million with a $37 million Series E funding in 2017, according to PitchBook. HotelTonight raised a total of $131 million in equity funding from venture capital firms including Accel, Battery Ventures, Forerunner Ventures and First Round Capital.

Powered by WPeMatico

PagerDuty debuted on the New York Stock Exchange today, and as we type, shares of the nine-year-old, San Francisco-based incident response software company are trading at nearly $39.

That’s up more than 60 percent above their IPO range of $24 per share, which was itself adjusted from the range of $21 to $23 that had been expected earlier and gives the company a valuation of close to $3 billion. That’s an awful lot for a company whose software helps technical teams at 11,000 companies spot problems with applications and respond to incidents. Though it’s growing quickly — revenue was up 48 percent last year — it still pulled in just $117.8 million in 2018. Meanwhile, its net loss widened last year, to $40.7 million from $38.1 million in 2017.

Certainly, its performance has to make the company’s investors — who last assigned the company a valuation of $1.3 billion back in September — very happy. Some of the VCs poised to win big if PagerDuty’s shares continue flying high include Andreessen Horowitz, which owned 18.4 percent of PagerDuty’s shares sailing into the IPO; Accel, which owned 12.3 percent; and Bessemer, which owned 12.2 percent. Other winners include Baseline Ventures (6.7 percent) and Harrison Metal (5.3 percent).

It’s also exciting for CEO Jennifer Tejada, a proven operator who was brought in to lead PagerDuty in 2016 and now becomes part of a small — but growing — club of women CEOs to take their tech companies public, including Katrina Lake of Stitch Fix and Julia Hartz of Eventbrite.

We talked with Tejada earlier today about the company’s big day. In addition to crediting company co-founders (and shareholders) Andrew Miklas and Baskar Puvanathasan, both of whom have since left the company, Tejada thanked PagerDuty co-founder Alex Solomon, who remains the company’s CTO. She also told us a little bit about what today has been like, and how the IPO changes things — and doesn’t. Our chat has been edited for length.

TC: First and foremost, how are you feeling?

JT: It’s been an incredible day. It’s been an incredible several months. You have to enjoy it when it’s going well.

TC: How does the vision for the company change now that it’s public? Have you been thinking ahead to possible acquisitions?

JT: The vision doesn’t change. We intend to do exactly what we’ve been doing, which is to provide the best real-time operations platform available to companies as they undergo digital transformation to meet the growing demands of their customers. We think we’re [facing] an early and very large opportunity that will be available to us for a long time. So our job continues to be to build great products, stay close to our customers, expand regionally and continue doing what has allowed us to be a successful private company.

TC: You and I had talked about the challenges of retaining employees in San Francisco when we sat down together in November. It’s a battle for every local company. How do you keep employees beyond the lock-up period? How do you ensure they stay focused on performance and not your share price?

JT: I think that mindset of, ‘It’s all over when you go public,’ is kind of a Silicon Valley fable. If you look at the most successful SaaS companies on the planet, they’ve gained 10x, 20x, 30x their value post their IPO. I also think what employees look for ahead of their financial success is career success. Am I being developed and recognized and can I build my career at this company? And we’ve worked really hard to create those career opportunities for our employees who [I think see, as I do] the IPO like a racing boat pushing off the dock, across the starting line, and into the open ocean, where the next adventure awaits.

In the meantime, we’ve already lessened our reliance on [overheated job markets] by opening offices in Toronto and Atlanta and Seattle and London and Sydney, even while we’re still hiring in San Francisco and Seattle.

TC: Obviously, Lyft’s shares have been up and down, owing to short sellers. Have you been monitoring short interest? Are you at all concerned about investors driving the price sky high, then selling it on the way down?

JT: I haven’t even looked at the stock price in the last several hours . . . There are a lot of things outside of my control, and the free market is one of them.

TC: PagerDuty is rare in that is doesn’t have a dual-class structure, which can greatly empower leaders over everyone else associated with a company. Presumably, this is a great relief to your investors; I just wonder whether it was ever a consideration?

JT: I’m a little bit of a traditionalist. I’ve been around long enough to know how checks and balances work, and a single-class structure made sense for PagerDuty. Also, dual-class structures tend to emerge more when you have deeply involved founders, and though Alex is still very much a part of the business, PagerDuty’s other two founders have worked outside of the business for some time.

TC: You have plenty of operating experience, including previously running Keynote Systems, but you’ve never taken a company public. Were there ways in which you found the roadshow experience surprising?

JT: I was surprised by how fun it was! [Laughs.] When you have a great story, and a great partner helping you tell it — in my case that’s [PagerDuty CFO] Howard Wilson, who I’ve worked with for 10 years — it’s great. We had a great reception from investors. I loved our IPO team; our Top were both led by women and whenever I had a question, they [had the answer]. I also had this cocoon of experience surrounding me thanks to our board. If anyone tells you that [in this position] they are super comfortable, they’re either lying or [clueless] but I was very lucky. I also have a whole bunch of buddies who are CEOs [and other executives] in SaaS and I’ve been shaking them down for advice for months, so I felt well-prepared.

TC: What was some of the advice you received from those friends about how your life is about to change?

JT: Some of it was about the need to keep people focused and not get distracted, to remind everyone that this is a milestone, not the goal. [Some centered on] surrounding yourself with a great team and the importance of great investor relations, a function you don’t have as a private company but that can create huge value and provide support and understanding of the market.

One CEO said to just make sure you keep having fun, to try and stay “you,” to find joy in the same things as before. There will be stressful moments and tough questions — that’s true of any company that’s scaling — but I heard a lot of advice about just taking care of myself, including on the roadshow. In fact, there were a lot of really supportive notes and private tweets that, in a job that can feel lonely, made me feel not alone, and I’m very appreciative of that.

TC: People call IPOs just another funding event, but that’s kind of baloney, isn’t it? If you had to list the most meaningful moments in your life on a scale from 1 to 10, 1 being the most important, where might today fall? Would today be up there on that list?

JT: When I think of most meaningful moments, I think of the day my daughter was born, and my wedding. Another day that was very meaningful to me was when I approved our pledge to donate one percent [of PagerDuty’s equity, one percent of its product and one percent of employees’ time] to social impact. We did it a lot later in the game than some companies; our equity was already valuable. But we knew that it was going to create meaningful impact over time.

But yes, it is a gratifying day, especially for the co-founders who were pulling the idea together for PagerDuty a couple of years before they even launched it, and for employees who’ve been with the company for nearly as long and who turned down safer and higher-paying jobs along the way. Seeing their joy today — that is a memory that will be in my top 10 for sure.

Powered by WPeMatico

Conversational AI and the use of chatbots have been through multiple cycles of hype and disillusionment in the tech world. You know the story: first you get a launch from the likes of Apple, Facebook, Microsoft, Amazon, Google or any number of other companies, and then you get the many examples of how their services don’t work as intended at the slightest challenge. But time brings improvements and more focused expectations, and today a startup that has been harnessing all those learnings is announcing funding to take to the next level its own approach to conversational AI.

Rasa, which has built an open-source platform for third parties to design and manage their own conversational (text or voice) AI chatbots, is today announcing that it has raised $13 million in a Series A round of funding led by Accel, with participation from Basis Set Ventures, Greg Brockman (co-founder & CTO OpenAI), Daniel Dines (founder & CEO UiPath) and Mitchell Hashimoto (co-founder & CTO Hashicorp).

Rasa was founded in Berlin, but with this round, it will be moving its headquarters to San Francisco, with a plan to hire more people there in sales, marketing and business development; and to continue its tech development with its roadmap including plans to expand the platform to cover images, too.

The company was founded 2.5 years ago, by co-founder/CEO Alex Weidauer’s own admission “when chatbot hype was at its peak.”

Rasa itself was not immune to it, too: “Everyone wanted to automate conversations, and so we set out to build something, too,” he said. “But we quickly realised it was extremely hard to do and that the developer tools were just not there yet.”

Rather than posing an insurmountable roadblock, the shortcomings of chatbots became the problem that Rasa set out to fix.

Alan Nichols, the co-founder who is now the CTO, is an AI PhD, not in natural language as you might expect, but in machine learning.

“What we do is more is address this as a mathematical, machine learning problem rather than one of language,” Weidauer said. Specifically, that means building a model that can be used by any company to tap its own resources to train their bots, in particular with unstructured information, which has been one of the trickier problems to solve in conversational AI.

At a time when many have raised concerns about who might “own” the progress of artificial intelligence, and specifically the data that goes into building these systems, Rasa’s approach is a refreshing one.

Typically, when an organization wants to build an AI chatbot either to interact with customers or to run something in the back end of their business, their developers most commonly opt for third-party cloud APIs that have restrictions on how they can be customized, or they build their own from scratch — but if the organization is not already a large tech company, it will be challenged to have the human or other resources to execute this.

Rasa underscores an emerging trend for a strong third contender. The company has built a stack of tools that it has open-sourced, meaning that anyone can (and thousands of developers do) use it for free, with a paid enterprise version that includes extra tools, including customer support, testing and training tools, and production container deployment. (It’s priced depending on size of organization and usage.)

Importantly, whichever package is used, the tools run on a company’s own training data; and the company can ultimately host their bots wherever they choose, which have been some of the unique selling points for those using Rasa’s platform, when they are less interested in working with organizations that might also be competitors.

Adobe’s new AI assistant for searching on Adobe Stock, which has some 100 million images, was built on Rasa.

“We wanted to give our users an AI assistant that lets them search with natural language commands,” said Brett Butterfield, director of software development at Adobe, in a statement. “We looked at several online services, and, in the end, Rasa was the clear choice because we were able to host our own servers and protect our user’s data privacy. Being able to automate full conversations and the fact it is open source were key elements for us.”

Other customers include Parallon and TalkSpace, Zurich and Allianz, Telekom and UBS.

Open source has become big business in the last several years, and so a startup that’s built an AI platform that has a very direct application in the enterprise built on it presents an obvious attraction for VCs.

“Automation is the next battleground for the enterprise, and while this is a very difficult space to win, especially for unstructured information like text and voice, we are confident Rasa has what it takes given their impressive adoption by developers,” said Andrei Brasoveanu, partner at Accel, in a statement.

“Existing solutions don’t let in-house developer teams control their own automation destiny. Rasa is applying commercial open source software solutions for AI environments similarly to what open source leaders such as Cloudera, Mulesoft, and Hashicorp have done for others.”

Powered by WPeMatico