zero

Auto Added by WPeMatico

Auto Added by WPeMatico

“Whatever your symptom, WebMD says you have cancer.” It’s a long-running joke that underscores the distrust of perhaps the top source of medical advice, stemming from a confusing site clogged with ads that’s been criticized for questionable information and pushing pills from its sponsors.

Health Guide is the new medical handbook for the internet, where 30% of content is written by doctors and 100% is reviewed by them. On a single clean, coherent page for each condition, it lays out a tl;dr summary, what the ailment really is, how to spot the symptoms and what you need for treatment. Rather than pushing you to nervously keep clicking, it just wants to answer the question.

Health Guide officially launches today. It was built by digital pharmacy Ro, which has raised $176 million for medicine brands Roman for men’s health, Rory for women’s health and Zero for smoking cessation. With Ro, patients can get a $15 telemedicine consultation with a doctor, receive an instant prescription and have it filled and sent to you from the startup’s in-house pharmacy operating in all 50 states. A competitor to Hims & Hers, Ro scored a $500 million valuation last year.

Rather than aggressively hawking its own products at the end of articles, Health Guide just lists the medications you could take, insists you ask a doctor what’s right and leaves it up to you to choose where to buy. Ro founder Zachariah Reitano calls Health Guide “a significant investment in trust. There’s not a clear ROI (return on investment) to it but it’s one of those long-term bets . . . Providing education to patients will serve Ro really well in the long-run.” He acknowledges the suspicions of self-dealing, and says “if we don’t do this correctly, it can hurt more than it can help.”

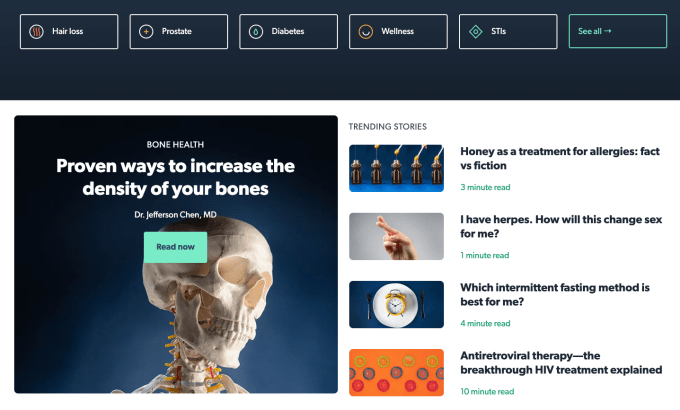

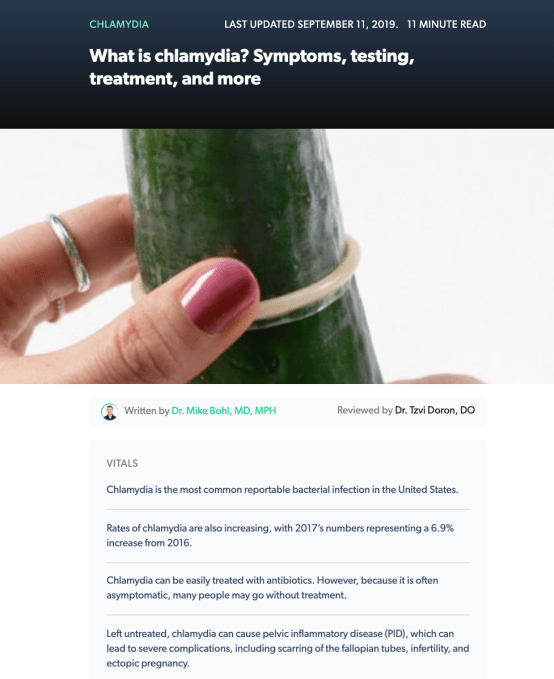

On Health Guide you can search for specific conditions, browse categories like diabetes or hair loss and browse featured articles like “Proven ways to increase the density of your bones” or “How do you test for gonorrhea.” There are no banner ads, so your search about the flu or testosterone won’t immediately lead to you being bombarded with promotions for Mucinex or dicey supplements. “On these other sites . . you have [advertisers] with unregulated supplements and services that are the highest bidder beside medical information, which creates a lot of distrust.”

The simplicity and accuracy of Health Guide has already attracted a sizable audience. It’s on pace to reach 30 million readers this year, with 25% being women despite Roman’s initial focus on aiding men with erectile dysfunction. It already ranks in the top 10 Google results for 300 medical questions. The no-filler entries come signed by the specific doctors that wrote or approved them, and Ro pledges to have them reviewed and updated at least once per year. At the bottom are links to all the original source material, including peer-reviewed medical journals.

Reitano tells me that the idea from Health Guide came after Ro’s physicians and customer service were bombarded with the same patient questions over and over. The easiest move was to put all the answers on an open site they could send patients to. A major goal was to debunk hoaxes other sites often don’t address directly. “For something like vaccines where there is a potential for misinformation, you’ll see us take a strong stance. We won’t let the potential for misinformation spread through Health Guide.”

One thing Health Guide is missing that could keep people coming back to WebMD is a symptom checker. Right now it’s better at research on major conditions or lifestyle choices than figuring out why your throat’s sore. But given it’s day one and Ro has tons of funding, it has plenty of time to improve. There’s sure to be concerns about how it collects data and what treatments Health Guide lists. So as a precaution, it never forcefully makes recommendations besides asking a doctor for personalized advice, and there’s just one button atop the site for visiting its medication marketplace.

Ro is trying to move fast as the ePharmacy space heats up. It plans to launch 10 more products in the next two quarters, with a focus on Rory for women. It just struck an exclusive deal with Pfizer to provide Roman customers with generic Viagra, offering clear supply chain transparency around a drug that’s often counterfeited. And thanks to its licenses across all states, it’s helping new weight loss treatment Plenity launch nationwide atop its diagnosis, prescription and fulfillment technology.

Yet Reitano sees space for multiple startups to succeed in replacing embarrassing and inconvenient in-person trips to the doctor or drug store. “It might be a somewhat cheesy answer but . . . the best thing about competition is it makes everyone build a better experience for patients,” he says, citing NURX and PillClub enhancing birth control access. “I think all this innovation in digital health — it’s an absolutely massive market. No one’s taking market share from someone else. We’re raising the bar for care.”

Powered by WPeMatico

Just ahead of the launch of the Apple Card, a startup that has its own take on modernizing the credit card industry, Zero, is announcing the close of its $20 million Series A. The new round of funding was led by New Enterprise Associates (NEA), and brings Zero’s total raised to date to $35 million, including both equity and debt funding.

Other investors in the round include SignalFire, Eniac Ventures, Nyca Partners and some unnamed school endowments. Zero had previously announced an $8.5 million raise in fall 2017, led by Eniac, and had raised $7 million in venture debt from Silicon Valley Bank.

Zero has a clever idea that targets millennials’ hesitance to sign up for credit cards.

Today, only 33% of millennials have a major credit card, a Bankrate survey found — largely because they’re wary of falling into the vicious debt cycle. Instead, this younger demographic often only carries a debit card. But that also means they’re missing out on credit card benefits — like points, rewards and cash back.

Zero’s idea is to offer a rewards credit card that works like debit.

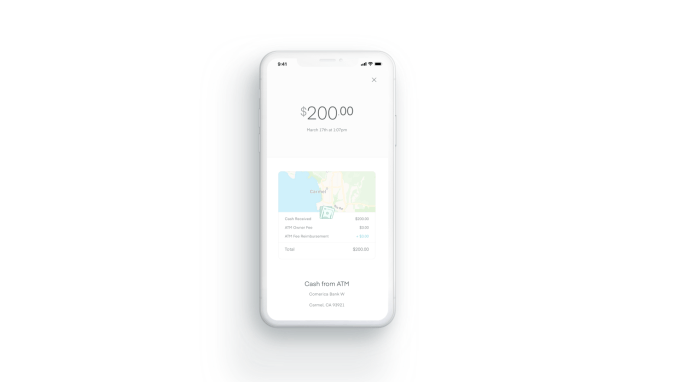

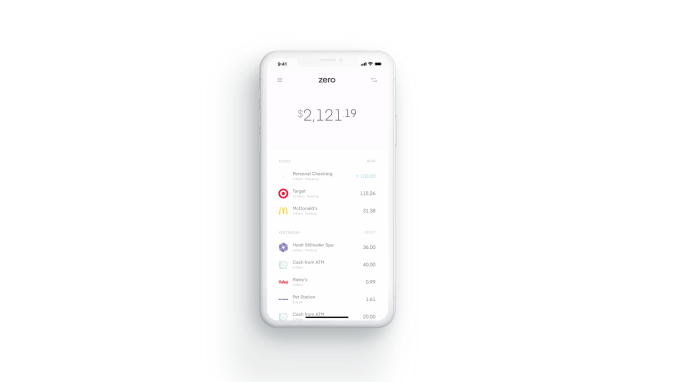

The Zerocard itself is a World Mastercard, so it earns credit card cash back. But unlike a traditional credit card, it’s combined with an FDIC-backed checking account called Zero Checking. That means Zerocard and Zero Checking work together in the app, allowing cardholders to see one net number they can spend from.

That way, they won’t make the mistake of accidentally going over budget, as is often the case with traditional credit cards, which then benefit from charging interest on the unpaid balance.

Zero co-founder and CEO Bryce Galen says he had always liked optimizing his personal finances, but didn’t see the value in overspending to chase rewards.

“People spend 10 to 15% more on average just because they’re putting it on a credit card, and not seeing where they stand all the time,” he says. “Spending 10 to 15% more to chase 1 to 2% in rewards doesn’t make sense.”

Plus, he adds, “half of all credit card points are never even redeemed.”

With Zerocard, the company does away with other credit card annoyances as well.

Zerocard doesn’t charge annual fees like many traditional credit cards do. And Zero Checking doesn’t add any additional ATM fees beyond what the ATM owner charges. It also does away with foreign transaction fees, minimum balance fees and overdraft fees — like many of today’s challenger banks.

Meanwhile, the Zero app is built with an eye toward what makes apps great.

Galen, who led product development for Zynga’s “Words with Friends” has experience in this department, while co-founder and COO Joel Washington previously co-founded car sales marketplace Shift. The executive team, combined, has backgrounds that include time at Affirm, Apple, Capital One, Dropbox, Google, Postmates, Silicon Valley Bank, Upgrade and Wells Fargo.

Overall, Zero’s design feels clean and simple, compared to the cluttered and dated apps from traditional banks. It has smart features, too, like a detailed transaction view that shows the vendor’s logo and location on a map to make it easier to recognize purchases.

“Zero creates an innovative debit-style experience, with an elegant design, and truly compelling rewards. It’s a fabulous banking experience,” said Hans Morris, managing partner of Nyca Partners and former president of Visa, Inc., in a statement. “Few people understand how complex it is to launch either a credit card or a checking account program, and I believe Zero is the first U.S. startup to launch both,” he said.

Zero launched in November 2018, but only to a small number of customers. Though officially open for business, it was functioning more like a public beta — though it didn’t call it that at the time. Meanwhile, its waitlist continued to grow.

Today, there are still 204,000 people waiting to be allowed in — something that Galen says is now going to happen.

“We haven’t launched to everyone on the waitlist yet, but we expect to within the next few weeks,” he says.

Another interesting twist on traditional credit cards is Zero’s path to card upgrades: it encourages but also rewards customers for telling their friends. By doing so, customers gain access to better-looking cards and higher cash-back percentages.

Zero customers start with a “Quartz” card offering 1% back on purchases. When a friend they refer joins, they receive a higher-level card called “Graphite” that offers 1.5% back. Two friends earns you the “Magnesium” card with 2% back and four friends gets you the “Carbon” card with 3% back. The Carbon card is also solid metal, capitalizing on the millennial trend of wanting their cards to look cool. And metal cards are in particular demand.

To receive the full cash-back rates, customers have to pay their balances in full by the due date, Zero says.

The company has partnered with Salt Lake City-based WebBank to issue the card, and deposits are held at Memphis-based Evolve Bank & Trust, an FDIC member. Zero makes money primarily on interchange and interest on deposits.

While some users may leave balances on the card that generate interest, Zero isn’t focused on that aspect of the business for revenue generation.

“Most companies in fintech today are launching undifferentiated debit cards as a feature or extension to their product for an additional engagement and monetization stream,” says Rick Yang, partner at NEA, as to why he invested.

“Zero is completely focused on their card programs and building a differentiated solution that actually provides a value proposition that resonates with consumers. We’ve also been fascinated by the growth of debit outpacing credit, and we think that our solution gives consumers the best of both worlds,” he adds.

Zero is currently iOS-only, but is working on an Android version that is expected to be ready in August.

Powered by WPeMatico

Over the past few years, the Internet of Things (IoT) has been the white-hot center of a flurry of activity. The IoT may well be The Next Big Thing, but maybe the attention around sensors is misplaced… What if we didn’t even need embedded sensors to allow things to gather data about their surrounding environment? What if material could be a sensor in and of itself? Read More

Over the past few years, the Internet of Things (IoT) has been the white-hot center of a flurry of activity. The IoT may well be The Next Big Thing, but maybe the attention around sensors is misplaced… What if we didn’t even need embedded sensors to allow things to gather data about their surrounding environment? What if material could be a sensor in and of itself? Read More

Powered by WPeMatico

A new mobile email application called Zero is launching today to help users power through their inboxes on the go to achieve the often sought-after state of “inbox zero.” Aimed at heavy email users who receive a lot of inbound email, an app that promises to speed up email processing by 30 percent or more sounds too good to be true. But while still far from perfect in its present… Read More

A new mobile email application called Zero is launching today to help users power through their inboxes on the go to achieve the often sought-after state of “inbox zero.” Aimed at heavy email users who receive a lot of inbound email, an app that promises to speed up email processing by 30 percent or more sounds too good to be true. But while still far from perfect in its present… Read More

Powered by WPeMatico