Zenefits

Auto Added by WPeMatico

Auto Added by WPeMatico

Factorial, a startup out of Barcelona that has built a platform that lets SMBs run human resources functions with the same kind of tools that typically are used by much bigger companies, is today announcing some funding to bulk up its own position: the company has raised $80 million, funding that it will be using to expand its operations geographically — specifically deeper into Latin American markets — and to continue to augment its product with more features.

CEO Jordi Romero, who co-founded the startup with Pau Ramon and Bernat Farrero — said in an interview that Factorial has seen a huge boom of growth in the last 18 months and counts more than anything 75,000 customers across 65 countries, with the average size of each customer in the range of 100 employees, although they can be significantly (single-digit) smaller or potentially up to 1,000 (the “M” of SMB, or SME as it’s often called in Europe).

“We have a generous definition of SME,” Romero said of how the company first started with a target of 10-15 employees but is now working in the size bracket that it is. “But that is the limit. This is the segment that needs the most help. We see other competitors of ours are trying to move into SME and they are screwing up their product by making it too complex. SMEs want solutions that have as much data as possible in one single place. That is unique to the SME.” Customers can include smaller franchises of much larger organizations, too: KFC, Booking.com, and Whisbi are among those that fall into this category for Factorial.

Factorial offers a one-stop shop to manage hiring, onboarding, payroll management, time off, performance management, internal communications and more. Other services such as the actual process of payroll or sourcing candidates, it partners and integrates closely with more localized third parties.

The Series B is being led by Tiger Global, and past investors CRV, Creandum, Point Nine and K Fund also participating, at a valuation we understand from sources close to the deal to be around $530 million post-money. Factorial has raised $100 million to date, including a $16 million Series A round in early 2020, just ahead of the Covid-19 pandemic really taking hold of the world.

That timing turned out to be significant: Factorial, as you might expect of an HR startup, was shaped by Covid-19 in a pretty powerful way.

The pandemic, as we have seen, massively changed how — and where — many of us work. In the world of desk jobs, offices largely disappeared overnight, with people shifting to working at home in compliance with shelter-in-place orders to curb the spread of the virus, and then in many cases staying there even after those were lifted as companies grappled both with balancing the best (and least infectious) way forward and their own employees’ demands for safety and productivity. Front-line workers, meanwhile, faced a completely new set of challenges in doing their jobs, whether it was to minimize exposure to the coronavirus, or dealing with giant volumes of demand for their services. Across both, organizations were facing economics-based contractions, furloughs, and in other cases, hiring pushes, despite being office-less to carry all that out.

All of this had an impact on HR. People who needed to manage others, and those working for organizations, suddenly needed — and were willing to pay for — new kinds of tools to carry out their roles.

But it wasn’t always like this. In the early days, Romero said the company had to quickly adjust to what the market was doing.

“We target HR leaders and they are currently very distracted with furloughs and layoffs right now, so we turned around and focused on how we could provide the best value to them,” Romero said to me during the Series A back in early 2020. Then, Factorial made its product free to use and found new interest from businesses that had never used cloud-based services before but needed to get something quickly up and running to use while working from home (and that cloud migration turned out to be a much bigger trend played out across a number of sectors). Those turning to Factorial had previously kept all their records in local files or at best a “Dropbox folder, but nothing else,” Romero said.

It also provided tools specifically to address the most pressing needs HR people had at the time, such as guidance on how to implement furloughs and layoffs, best practices for communication policies and more. “We had to get creative,” Romero said.

But it wasn’t all simple. “We did suffer at the beginning,” Romero now says. “People were doing furloughs and [frankly] less attention was being paid to software purchasing. People were just surviving. Then gradually, people realized they needed to improve their systems in the cloud, to manage remote people better, and so on.” So after a couple of very slow months, things started to take off, he said.

Factorial’s rise is part of a much, longer-term bigger trend in which the enterprise technology world has at long last started to turn its attention to how to take the tools that originally were built for larger organizations, and right size them for smaller customers.

The metrics are completely different: large enterprises are harder to win as customers, but represent a giant payoff when they do sign up; smaller enterprises represent genuine scale since there are so many of them globally — 400 million, accounting for 95% of all firms worldwide. But so are the product demands, as Romero pointed out previously: SMBs also want powerful tools, but they need to work in a more efficient, and out-of-the-box way.

Factorial is not the only HR startup that has been honing in on this, of course. Among the wider field are PeopleHR, Workday, Infor, ADP, Zenefits, Gusto, IBM, Oracle, SAP and Rippling; and a very close competitor out of Europe, Germany’s Personio, raised $125 million on a $1.7 billion valuation earlier this year, speaking not just to the opportunity but the success it is seeing in it.

But the major fragmentation in the market, the fact that there are so many potential customers, and Factorial’s own rapid traction are three reasons why investors approached the startup, which was not proactively seeking funding when it decided to go ahead with this Series B.

“The HR software market opportunity is very large in Europe, and Factorial is incredibly well positioned to capitalize on it,” said John Curtius, Partner at Tiger Global, in a statement. “Our diligence found a product that delighted customers and a world-class team well-positioned to achieve Factorial’s potential.”

“It is now clear that labor markets around the world have shifted over the past 18 months,” added Reid Christian, general partner at CRV, which led its previous round, which had been CRV’s first investment in Spain. “This has strained employers who need to manage their HR processes and properly serve their employees. Factorial was always architected to support employers across geographies with their HR and payroll needs, and this has only accelerated the demand for their platform. We are excited to continue to support the company through this funding round and the next phase of growth for the business.”

Notably, Romero told me that the fundraising process really evolved between the two rounds, with the first needing him flying around the world to meet people, and the second happening over video links, while he was recovering himself from Covid-19. Given that it was not too long ago that the most ambitious startups in Europe were encouraged to relocate to the U.S. if they wanted to succeed, it seems that it’s not just the world of HR that is rapidly shifting in line with new global conditions.

Powered by WPeMatico

It’s possible to raise VC funding even if you haven’t built a real product, according to Charles Hudson, founder and managing partner at seed-stage firm Precursor Ventures. It’s just very, very difficult.

I interviewed Hudson during TechCrunch Early Stage, our virtual event for startup founders. He gave a short talk titled “How to sell an idea when you don’t have a product,” then answered questions from me and from attendees watching at home.

Hudson said Precursor invests in about 25 startups every year and that a majority are pre-launch and pre-traction. So when he’s considering startups where there “isn’t any evidence or traction,” he and other investors are basically considering two things: How well the founder knows the industry, and how well the investors know the founder.

Of course, if you’ve already had success and you know everyone on Sand Hill Road, it might not be that hard to get that first check. But what about everyone else?

Below, I’ve quoted some highlights from Hudson’s thoughts about how to raise money pre-product. You can also watch the full presentation/conversation at the end of this post.

You need to have a unique and durable insight that will still be true in 12 to 18 months … The unique part is important because you still haven’t launched your product yet. And so whatever it is that you’re doing, if it’s not unique, if it’s a really obvious insight, you’ll probably have 10 or 12 competitors that are launched in the market by the time you get your product out.

Powered by WPeMatico

Remember when Zenefits imploded, and kicked out CEO Parker Conrad. Well, Conrad launched a new employee onboarding startup called Rippling, and now he’s going after another HR company called Gusto with a new billboard, “Outgrowing Gusto? Presto change-o.”

The problem is, Gusto got it taken down by issuing a cease & desist order to Rippling and the billboard operator Clear Channel Outdoor. That’s despite the law typically allowing comparative advertising as long as it’s accurate. Gusto sells HR, benefits and payroll software, while Rippling does the same but adds in IT management to tie together an employee identity platform.

Rippling tells me that outgrowing Gusto is the top reasons customers say they’re switching to Rippling. Gusto’s customer stories page lists no customers larger than 61 customers, and Enlyft research says the company is most often used by 10 to 50-person staffs. “We were one of Gusto’s largest customers when we left the platform last year. They were very open about the fact that the product didn’t work for businesses of our size. We moved to Rippling last fall and have been extremely happy with it,” says Compass Coffee co-founder Michael Haft.

That all suggests the Rippling ad’s claim is reasonable. But the C&D claims that “Gusto counts as customers multiple companies with 100 or more employees and does not state the businesses will ‘outgrow’ their platfrom at a certain size.”

In an email to staff provided to TechCrunch, Rippling CMO Matt Epstein wrote, “We take legal claims seriously, but this one doesn’t pass the laugh test. As Gusto says all over their website, they focus on small businesses.”

So rather than taking Gusto to court or trying to change Clear Channel’s mind, Conrad and Rippling did something cheeky. They responded to the cease & desist order in Shakespeare-style iambic pentameter.

Our billboard struck a nerve, it seems. And so you phoned your legal teams,

who started shouting, “Cease!” “Desist!” and other threats too long to list.Your brand is known for being chill. So this just seems like overkill.

But since you think we’ve been unfair, we’d really like to clear the air.

Rippling’s general counsel Vanessa Wu wrote the letter, which goes on to claim that “When Gusto tried to scale itself, we saw what you took off the shelf. Your software fell a little short. You needed Workday for support,” asserting that Gusto’s own HR tool couldn’t handle its 1,000-plus employees and needed to turn to a bigger enterprise vendor. The letter concludes with the implication that Gusto should drop the cease-and-desist, and instead compete on merit:

So Gusto, do not fear our sign. Our mission and our goals align.

Let’s keep this conflict dignified—and let the customers decide.

Rippling CMO Matt Epstein tells me that “While the folks across the street may find competition upsetting, customers win when companies push each other to do better. We hope our lighthearted poem gets this debate back down to earth, and we look forward to competing in the marketplace.”

Rippling might think this whole thing was slick or funny, but it comes off a bit lame and try-hard. These are far from 8 Mile-worthy battle rhymes. If it really wanted to let customers decide, it could have just accepted the C&D and moved on…or not run the billboard at all. It still has four others that don’t slam competitors running. That said, Gusto does look petty trying to block the billboard and hide that it’s unequipped to support massive teams.

We reached out to Gusto over the weekend and again today asking for comment, whether it will drop the C&D, if it’s trying to get Rippling’s bus ads dropped too and if it does in fact use Workday internally.

[Update 2pm Pacific: Gusto’s PR representative Paul Loeffler claims that “This is common business practice in maintaining a brand”, says that for Gusto “A core, but not exclusive focus, are small businesses”, and admits that “as Gusto itself has grown to become a large-scale company, we have different needs than many of our customers and transitioned to Workday.”

Finally, he declares that “We’re excited to see more companies create new solutions that make it easier for businesses to take care of and support their teams” despite theatening to sue one that was. If Gusto itself grew out of Gusto, an ad asking if its customers are too seems wholly accurate.]

Given Gusto has raised $516 million — 10X what Rippling has — you’d think it could just outspend Rippling on advertising or invest in building the enterprise HR tools so customers really couldn’t outgrow it. They’re both Y Combinator companies with Kleiner Perkins as a major investor (conflict of interest?), so perhaps they can still bury the hatchet.

At least they found a way to make the HR industry interesting for an afternoon.

Powered by WPeMatico

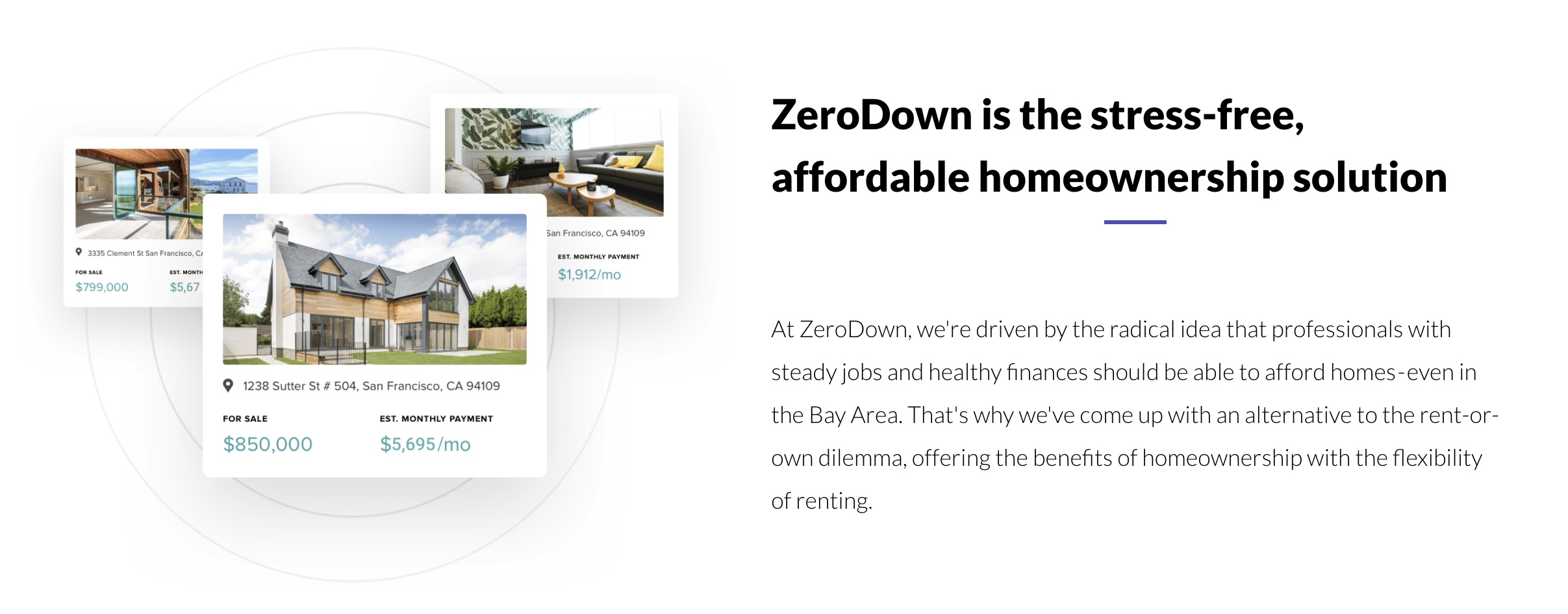

Days out of Y Combinator, venture capitalists valued ZeroDown, a financial and real estate technology startup, at $150 million, the company has confirmed. The startup had the perfect match of experienced founders and eye-popping ambitions to carve a new path to home ownership.

“I think we will be known as a company that makes it easier to buy a home in every single aspect,” ZeroDown co-founder and chief executive officer Abhijeet Dwivedi tells TechCrunch.

The startup, which has raised $30 million in total equity funding and more than $110 million in debt financing to help Bay Area residents make down payments on homes, now plans to take on Zillow and Redfin with its new home search engine.

The business, founded by former Zenefits chief operating officer Dwivedi, Laks Srini, Zenefits’ former chief technology officer, and Hari Viswanathan, a former Zenefits staff engineer, was founded last year and quickly landed backing from Sam Altman, followed by consumer technology venture capital fund Goodwater Capital. Targeting those in the Bay Area, where costs of home ownership are amongst the highest in the country, ZeroDown charges $10,000 to purchase your home outright and front your entire down payment.

That is, however, if your home is priced between approximately $550,000 and $1,750,000 and you have an individual or combined salary of more than $200,000, stock options and some money put away (or some variation of this). If you meet these criteria, ZeroDown will purchase your home and lease it to you. The goal is to eliminate one of the largest pain points of home-buying, the down payment, and facilitate more real estate purchases.

The company says it intends to expand the service outside the greater San Francisco area to cities like Denver, Seattle and Austin, but given the $10,000 price tag and large population of wealthy tech workers in the Bay, the business could flourish in this area without expanding.

With the launch of its home search engine, Dwivedi says users will be able to learn about more than just the square footage of a home. The tool tells users whether a potential home is naturally lit, if it has a large backyard, if it has a decent commute to your work and to various schools and, most importantly, whether it’s dog friendly.

ZeroDown has also partnered with a number of San Francisco-based tech companies, including Pinterest, Postmates and Square, to provide their employees a rebate if they choose to purchase a home using ZeroDown.

“We know first-hand what companies need to support a great quality of life and keep their employees in the Bay Area,” Dwivedi said. “A part of that is loving where you live — feeling part of a local community.”

Powered by WPeMatico

While the software revolution started out slowly, over the past few years it’s exploded and the fastest-growing segment to-date has been the shift towards software as a service or SaaS.

SaaS has dramatically lowered the intrinsic total cost of ownership for adopting software, solved scaling challenges and taken away the burden of issues with local hardware. In short, it has allowed a business to focus primarily on just that — its business — while simultaneously reducing the burden of IT operations.

Today, SaaS adoption is increasingly ubiquitous. According to IDG’s 2018 Cloud Computing Survey, 73% of organizations have at least one application or a portion of their computing infrastructure already in the cloud. While this software explosion has created a whole range of downstream impacts, it has also caused software developers to become more and more valuable.

The increasing value of developers has meant that, like traditional SaaS buyers before them, they also better intuit the value of their time and increasingly prefer businesses that can help alleviate the hassles of procurement, integration, management, and operations. Developer needs to address those hassles are specialized.

They are looking to deeply integrate products into their own applications and to do so, they need access to an Application Programming Interface, or API. Best practices for API onboarding include technical documentation, examples, and sandbox environments to test.

APIs tend to also offer metered billing upfront. For these and other reasons, APIs are a distinct subset of SaaS.

For fast-moving developers building on a global-scale, APIs are no longer a stop-gap to the future—they’re a critical part of their strategy. Why would you dedicate precious resources to recreating something in-house that’s done better elsewhere when you can instead focus your efforts on creating a differentiated product?

Thanks to this mindset shift, APIs are on track to create another SaaS-sized impact across all industries and at a much faster pace. By exposing often complex services as simplified code, API-first products are far more extensible, easier for customers to integrate into, and have the ability to foster a greater community around potential use cases.

Graphics courtesy of Accel

Whether you realize it or not, chances are that your favorite consumer and enterprise apps—Uber, Airbnb, PayPal, and countless more—have a number of third-party APIs and developer services running in the background. Just like most modern enterprises have invested in SaaS technologies for all the above reasons, many of today’s multi-billion dollar companies have built their businesses on the backs of these scalable developer services that let them abstract everything from SMS and email to payments, location-based data, search and more.

Simultaneously, the entrepreneurs behind these API-first companies like Twilio, Segment, Scale and many others are building sustainable, independent—and big—businesses.

Valued today at over $22 billion, Stripe is the biggest independent API-first company. Stripe took off because of its initial laser-focus on the developer experience setting up and taking payments. It was even initially known as /dev/payments!

Stripe spent extra time building the right, idiomatic SDKs for each language platform and beautiful documentation. But it wasn’t just those things, they rebuilt an entire business process around being API-first.

Companies using Stripe didn’t need to fill out a PDF and set up a separate merchant account before getting started. Once sign-up was complete, users could immediately test the API with a sandbox and integrate it directly into their application. Even pricing was different.

Stripe chose to simplify pricing dramatically by starting with a single, simple price for all cards and not breaking out cards by type even though the costs for AmEx cards versus Visa can differ. Stripe also did away with a monthly minimum fee that competitors had.

Many competitors used the monthly minimum to offset the high cost of support for new customers who weren’t necessarily processing payments yet. Stripe flipped that on its head. Developers integrate Stripe earlier than they integrated payments before, and while it costs Stripe a lot in setup and support costs, it pays off in brand and loyalty.

Checkr is another excellent example of an API-first company vastly simplifying a massive yet slow-moving industry. Very little had changed over the last few decades in how businesses ran background checks on their employees and contractors, involving manual paperwork and the help of 3rd party services that spent days verifying an individual.

Checkr’s API gives companies immediate access to a variety of disparate verification sources and allows these companies to plug Checkr into their existing on-boarding and HR workflows. It’s used today by more than 10,000 businesses including Uber, Instacart, Zenefits and more.

Like Checkr and Stripe, Plaid provides a similar value prop to applications in need of banking data and connections, abstracting away banking relationships and complexities brought upon by a lack of tech in a category dominated by hundred-year-old banks. Plaid has shown an incredible ramp these past three years, from closing a $12 million Series A in 2015 to reaching a valuation over $2.5 billion this year.

Today the company is fueling an entire generation of financial applications, all on the back of their well-built API.

Graphics courtesy of Accel

Accel’s first API investment was in Braintree, a mobile and web payment systems for e-commerce companies, in 2011. Braintree eventually sold to, and became an integral part of, PayPal as it spun out from eBay and grew to be worth more than $100 billion. Unsurprisingly, it was shortly thereafter that our team decided to it was time to go big on the category. By the end of 2014 we had led the Series As in Segment and Checkr and followed those investments with our first APX conference in 2015.

Plaid, Segment, Auth0, and Checkr had only raised Seed or Series A financings! And we are even more excited and bullish on the space. To convey just how much API-first businesses have grown in such a short period of time, we thought it would be useful perspective to share some metrics over the past five years, which we’ve broken out in the two visuals included above in this article.

While SaaS may have pioneered the idea that the best way to do business isn’t to actually build everything in-house, today we’re seeing APIs amplify this theme. At Accel, we firmly believe that APIs are the next big SaaS wave — having as much if not more impact as its predecessor thanks to developers at today’s fastest-growing startups and their preference for API-first products. We’ve actively continued to invest in the space (in companies like, Scale, mentioned above).

And much like how a robust ecosystem developed around SaaS, we believe that one will continue to develop around APIs. Given the amount of progress that has happened in just a few short years, Accel is hosting our second APX conference to once again bring together this remarkable community and continue to facilitate discussion and innovation.

Graphics courtesy of Accel

Powered by WPeMatico

Tandem, one of the most sought after companies to graduate from Y Combinator’s summer batch, will emerge from the accelerator program with a supersized seed round and an uncharacteristically high valuation.

The months-old business, which is developing communication software for remote teams after pivoting from crypto, is raising a $7.5 million seed financing at a valuation north of $30 million, sources tell TechCrunch. Airbnb investor Andreessen Horowitz is leading the round.

Tandem and a16z declined to comment for this story. The round has yet to close, which means the deal size is subject to change. Y Combinator startups raise capital using SAFE agreements, or simple agreements for future equity, which allow investors to buy shares in a future priced round at a previously agreed-upon valuation.

We’re told several top venture capital firms were vying for a stake in Tandem. One firm even gifted the founders a tandem bike, sources tell TechCrunch, resorting to amusing measures to sway the Tandem team. But it was A16z — which has an established interest in the growing future of work sector, evidenced by its recent investment in the popular email app Superhuman — that ultimately won the coveted lead investor spot.

Tandem provides a virtual office for remote teams, complete with video-chatting and messaging capabilities, as well as integrations with top enterprise tools including Notion, GitHub and Trello. The service launched one month ago and has signed contracts with Airbnb, Dropbox and others. The company claims to be growing 50% week-over-week.

“Every company is a remote company,” Tandem chief executive officer Rajiv Ayyangar said during his pitch to investors on day two of Y Combinator Demo Days this week. “You have salespeople in the field, [companies with] multiple offices, people working from home. Tandem isn’t just building the future of remote work, it’s building the future of work.”

Ayyangar was previously a data scientist at Yahoo before joining Yakit, a startup seeking to simplify ecommerce delivery, as the director of product. Co-founders Bernat Fortet Unanue and Tim Su are also Yahoo alums.

We’re told Tandem’s fundraise was nearly complete before it pitched to investors Tuesday afternoon. Startups that participate in YC are often flooded with offers from VCs throughout the three-month program. Firms are hungry for the batch’s Airbnb, Dropbox or Stripe — graduates of the program — and will pay premiums on startup equity for their chance to invest in a future ‘unicorn.’

As a result, the median seed deal for U.S. startups in 2018 was roughly $2 million — a record high — with typical pre-money valuations hovering north of $10 million. Tandem’s seed financing represents both a trend of swelling seed deals and valuations, as well as a tendency for VCs to dole out more cash to fresh-from-YC companies amid heightened competition amongst their peers.

The previous YC batch, which wrapped up in March, included ZeroDown, Overview.AI and Catch, a trio of companies that pocketed venture capital ahead of demo day. ZeroDown, a financing solution for real estate purchases in the Bay Area, raised upwards of $10 million at a $75 million valuation before demo day, sources told TechCrunch at the time (months after demo day, Zero Down announced a whopping $30 million financing). ZeroDown was an outlier, of course, as the company’s founders had previously co-founded the billion-dollar HR software company Zenefits.

As for the summer batch, we’re told Actiondesk, Taskade and Tandem are amongst the startups to garner the most hype from investors. Some even forwent the demo day pitch altogether. BraveCare, which is creating urgent care clinics intended just for kids, raised $4.1 million ahead of demo day, we’re told. The company opted not to pitch to additional investors this week.

You can read about all the company’s that pitched during demo day one here and demo day two here.

Powered by WPeMatico

Over the years, we’ve seen a lot of B2B companies apply ineffective demand generation strategies to their startup. If you’re a B2B founder trying to grow your business, this guide is for you.

Rule #1: B2B is not B2C. We are often dealing with considered purchases, multiple stakeholders, long decision cycles, and massive LTVs. These unique attributes matter when developing a growth strategy. We’ll share B2B best practices we’ve employed while working with awesome B2B companies like Zenefits, Crunchbase, Segment, OnDeck, Yelp, Kabbage, Farmers Business Network, and many more. Topics covered include:

We often crack growth for companies that didn’t think it was possible, based on their prior experience with agencies and/or internal resources. There are many misconceptions out there about B2B growth, rooted in the misapplication of B2C strategies and leading to poor performance. Study the differences and you’ll develop a filter for all the advice you get that’s good for one context (ex: B2C) but bad for another (ex: B2B). This guide will get you off on the right foot.

The best growth strategy for your company ultimately depends on whether you’re in an incubation, iteration, or scale stage. One of the most common mistakes we see is a company acting like they’re in the scale phase when they’re actually in the iteration phase. As a result, many of them end up developing inefficient growth strategies that lead to exorbitant monthly ad spends, extraneous acquisition channels, hiring (and later firing) ineffective team members, and de-emphasizing critical customer feedback. There is often an intense pressure to grow, but believing your own hype before it’s real can kill early-stage ventures. Here’s a breakdown of each stage:

")

Incubation is when you are building your minimum viable product (MVP). This should be done in close partnership with potential customers to ensure you are solving a real problem with a credible solution. Typically a founder is a voice of the customer, as someone who experienced the problem and sought out the solution s/he is now building. Other times, founders enter a new space and build a panel of prospective buyers to participate in the product development process. The endpoint of this phase is a working MVP.

Iteration is when you have customers using your MVP and you are rapidly improving the product. Success at this stage is rooted in customer insights – both qualitative and quantitative – not marketing excellence. It’s valuable to include in this iterative process customers with whom the founder(s) have no prior relationship. You want to test the product’s appeal, not friends’ willingness to help you out. We want a customer set that is an accurate sample of a much larger population you will later sell to. The endpoint of the iteration phase is product/market fit.

Scale is when you have product/market fit and are trying to grow your customer base. The goal of this phase is to build a portfolio of tactics that maximize market penetration with minimal – or at least profitable – cost. Success is rooted in growing lifetime value through retention and margin, maximizing funnel conversion to efficiently convert leads to customers, and finding repeatable tactics to drive prospective buyers’ awareness and consideration of your product. The endpoint of this phase is ultimately market saturation, leading to the incubation and iteration of new features, customer segments, and geographies.

Here’s a list of B2B customer acquisition tactics we commonly employ and recommend. Later in this article, we’ll connect each channel to the growth stage it’s best used in. This list is generally sorted by early stage to later stage:

1. Leverage your network. This is particularly valuable for founders who are building a product based on their own past experience.

Powered by WPeMatico

Hundreds gathered this week at San Francisco’s Pier 48 to see the more than 200 companies in Y Combinator’s Winter 2019 cohort present their two-minute pitches. The audience of venture capitalists, who collectively manage hundreds of billions of dollars, noted their favorites. The very best investors, however, had already had their pick of the litter.

What many don’t realize about the Demo Day tradition is that pitching isn’t a requirement; in fact, some YC graduates skip out on their stage opportunity altogether. Why? Because they’ve already raised capital or are in the final stages of closing a deal.

ZeroDown, Overview.AI and Catch are among the startups in YC’s W19 batch that forwent Demo Day this week, having already pocketed venture capital. ZeroDown, a financing solution for real estate purchases in the Bay Area, raised a round upwards of $10 million at a $75 million valuation, sources tell TechCrunch. ZeroDown hasn’t responded to requests for comment, nor has its rumored lead investor: Goodwater Capital.

Without requiring a down payment, ZeroDown purchases homes outright for customers and helps them work toward ownership with monthly payments determined by their income. The business was founded by Zenefits co-founder and former chief technology officer Laks Srini, former Zenefits chief operating officer Abhijeet Dwivedi and Hari Viswanathan, a former Zenefits staff engineer.

The founders’ experience building Zenefits, despite its shortcomings, helped ZeroDown garner significant buzz ahead of Demo Day. Sources tell TechCrunch the startup had actually raised a small seed round ahead of YC from former YC president Sam Altman, who recently stepped down from the role to focus on OpenAI, an AI research organization. Altman is said to have encouraged ZeroDown to complete the respected Silicon Valley accelerator program, which, if nothing else, grants its companies a priceless network with which no other incubator or accelerator can compete.

Overview .AI’s founders’ resumes are impressive, too. Russell Nibbelink and Christopher Van Dyke were previously engineers at Salesforce and Tesla, respectively. An industrial automation startup, Overview is developing a smart camera capable of learning a machine’s routine to detect deviations, crashes or anomalies. TechCrunch hasn’t been able to get in touch with Overview’s team or pinpoint the size of its seed round, though sources confirm it skipped Demo Day because of a deal.

Catch, for its part, closed a $5.1 million seed round co-led by Khosla Ventures, NYCA Partners and Steve Jang prior to Demo Day. Instead of pitching their health insurance platform at the big event, Catch published a blog post announcing its first feature, The Catch Health Explorer.

“This is only the first glimpse of what we’re building this year,” Catch wrote in the blog post. “In a few months, we’ll be bringing end-to-end health insurance enrollment for individual plans into Catch to provide the best health insurance enrollment experience in the country.”

TechCrunch has more details on the healthtech startup’s funding, which included participation from Kleiner Perkins, the Urban Innovation Fund and the Graduate Fund.

Four more startups, Truora, Middesk, Glide and FlockJay had deals in the final stages when they walked onto the Demo Day stage, deciding to make their pitches rather than skip the big finale. Sources tell TechCrunch that renowned venture capital firm Accel invested in both Truora and Middesk, among other YC W19 graduates. Truora offers fast, reliable and affordable background checks for the Latin America market, while Middesk does due diligence for businesses to help them conduct risk and compliance assessments on customers.

Finally, Glide, which allows users to quickly and easily create well-designed mobile apps from Google Sheets pages, landed support from First Round Capital, and FlockJay, the operator an online sales academy that teaches job seekers from underrepresented backgrounds the skills and training they need to pursue a career in tech sales, secured investment from Lightspeed Venture Partners, according to sources familiar with the deal.

Raising ahead of Demo Day isn’t a new phenomenon. Companies, thanks to the invaluable YC network, increase their chances at raising, as well as their valuation, the moment they enroll in the accelerator. They can begin chatting with VCs when they see fit, and they’re encouraged to mingle with YC alumni, a process that can result in pre-Demo Day acquisitions.

This year, Elph, a blockchain infrastructure startup, was bought by Brex, a buzzworthy fintech unicorn that itself graduated from YC only two years ago. The deal closed just one week before Demo Day. Brex’s head of engineering, Cosmin Nicolaescu, tells TechCrunch the Elph five-person team — including co-founders Ritik Malhotra and Tanooj Luthra, who previously founded the Box-acquired startup Steem — were being eyed by several larger companies as Brex negotiated the deal.

“For me, it was important to get them before batch day because that opens the floodgates,” Nicolaescu told TechCrunch. “The reason why I really liked them is they are very entrepreneurial, which aligns with what we want to do. Each of our products is really like its own business.”

Of course, Brex offers a credit card for startups and has no plans to dabble with blockchain or cryptocurrency. The Elph team, rather, will bring their infrastructure security know-how to Brex, helping the $1.1 billion company build its next product, a credit card for large enterprises. Brex declined to disclose the terms of its acquisition.

Y Combinator partners Michael Seibel and Dalton Caldwell, and moderator Josh Constine, speak onstage during TechCrunch Disrupt SF 2018. (Photo by Kimberly White/Getty Images)

Ultimately, it’s up to startups to determine the cost at which they’ll give up equity. YC companies raise capital under the SAFE model, or a simple agreement for future equity, a form of fundraising invented by YC. Basically, an investor makes a cash investment in a YC startup, then receives company stock at a later date, typically upon a Series A or post-seed deal. YC made the switch from investing in startups on a pre-money safe basis to a post-money safe in 2018 to make cap table math easier for founders.

Michael Seibel, the chief executive officer of YC, says the accelerator works with each startup to develop a personalized fundraising plan. The businesses that raise at valuations north of $10 million, he explained, do so because of high demand.

“Each company decides on the amount of money they want to raise, the valuation they want to raise at, and when they want to start fundraising,” Seibel told TechCrunch via email. “YC is only an advisor and does not dictate how our companies operate. The vast majority of companies complete fundraising in the 1 to 2 months after Demo Day. According to our data, there is little correlation between the companies who are most in demand on Demo Day and ones who go on to become extremely successful. Our advice to founders is not to over optimize the fundraising process.”

Though Seibel says the majority raise in the months following Demo Day, it seems the very best investors know to be proactive about reviewing and investing in the batch before the big event.

Khosla Ventures, like other top VC firms, meets with YC companies as early as possible, partner Kristina Simmons tells TechCrunch, even scheduling interviews with companies in the period between when a startup is accepted to YC to before they actually begin the program. Another Khosla partner, Evan Moore, echoed Seibel’s statement, claiming there isn’t a correlation between the future unicorns and those that raise capital ahead of Demo Day. Moore is a co-founder of DoorDash, a YC graduate now worth $7.1 billion. DoorDash closed its first round of capital in the weeks following Demo Day.

“I think a lot of the activity before demo day is driven by investor FOMO,” Moore wrote in an email to TechCrunch. “I’ve had investors ask me how to get into a company without even knowing what the company does! I mostly see this as a side effect of a good thing: YC has helped tip the scale toward founders by creating an environment where investors compete. This dynamic isn’t what many investors are used to, so every batch some complain about valuations and how easy the founders have it, but making it easier for ambitious entrepreneurs to get funding and pursue their vision is a good thing for the economy.”

This year, given the number of recent changes at YC — namely the size of its latest batch — there was added pressure on the accelerator to showcase its best group yet. And while some did tell TechCrunch they were especially impressed with the lineup, others indeed expressed frustration with valuations.

Many YC startups are fundraising at valuations at or higher than $10 million. For context, that’s actually perfectly in line with the median seed-stage valuation in 2018. According to PitchBook, U.S. startups raised seed rounds at a median post-valuation of $10 million last year; so far this year, companies are raising seed rounds at a slightly higher post-valuation of $11 million. With that said, many of the startups in YC’s cohorts are not as mature as the average seed-stage company. Per PitchBook, a company can be several years of age before it secures its seed round.

I did not talk to a single company in this batch raising under $10M post (admittedly I only was able to speak with a fraction of the 205).

— Peter Rojas (@peterrojas) March 20, 2019

Nonetheless, pricey deals can come as a disappointment to the seed investors who find themselves at YC every year but because their reputations aren’t as lofty as say, Accel, aren’t able to book pre-Demo Day meetings with YC’s top of class.

The question is who is Y Combinator serving? And the answer is founders, not investors. YC is under no obligation to serve up deals of a certain valuation nor is it responsible for which investors gain access to its best companies at what time. After all, startups are raking in larger and larger rounds, earlier in their lifespans; shouldn’t YC, a microcosm for the Silicon Valley startup ecosystem, advise their startups to charge the best investors the going rate?

Powered by WPeMatico

The only sure things in this life, according to Ben Franklin, are death and taxes. And a new startup called Visor has just raised $9 million in financing to make one of them as painless as possible.

Unlike Nectome, Visor won’t kill anyone, but it may ring the death knell for the high-end tax advisors that most Americans can’t even access to get help filing and paying their taxes. It’s like having a personalized accountant for the cost of a high-end do-it-yourself tax-prep service.

The $9 million Visor raised came from the venture capital firm Defy, with participation from Unusual Ventures, SVB Capital and existing investors like Obvious Ventures, Fika Ventures and Boxgroup, which had put a previous $6.5 million into the company.

The idea for the company had been percolating for co-founder and chief executive Gernot Zacke since he settled in the U.S.

Growing up in Sweden, Zacke was exposed to a much different process for paying taxes. “The experience of filing taxes in Sweden is that you receive a message from the government that stated how much you made and how much you were withholding. That’s it,” said Zacke. “Taxes should be as easy as ordering a cab.”

That’s the service that Visor aims to provide.

“If you think about the market there are two ways to get your taxes done. There’s the DIY space and then there are other online services but it requires the tax payer to fill out the forms and it leaves the tax payer with a little bit of anxiety,” said Zacke. “We’re delivering the CPA experience through the convenience of a web app and a mobile app.”

On average, Americans spend about 13 hours each year dealing with taxes, and the average American doesn’t have the benefits of a professional advisor who can help optimize the process. That’s what Visor wants to provide.

“You provide the same amount of information you provide to a CPA or TurboTax… we make sure that that information is filed securely on AWS and shared between the docs and the backend,” said Zacke.

The target customers for Zacke’s services are folks who have had a change to their tax situation — whether moving, buying a home or any other life event; or folks who have had a CPA and don’t want to pay the higher fees, he said.

Visor currently has an operations team of around 34 people split between San Francisco and Atlanta.

For Zacke, the pain point he’s solving with the Visor service is very real. A former employee of the European investment firm Atomico, Zacke bounced between the U.S. and Europe — eventually running U.S. investments for the firm before leaving to launch Visor.

Other co-founders and senior executives hail from the tax advisory world, and from employee benefits outsourcing services company Zenefits, along with former Venmo and Square developers.

“Taxpayers spend $20 billion a year to get their taxes prepared and are stuck between spending hours filling out DIY tax software and hiring an expensive CPA,” said Zacke, in a statement. “

Powered by WPeMatico

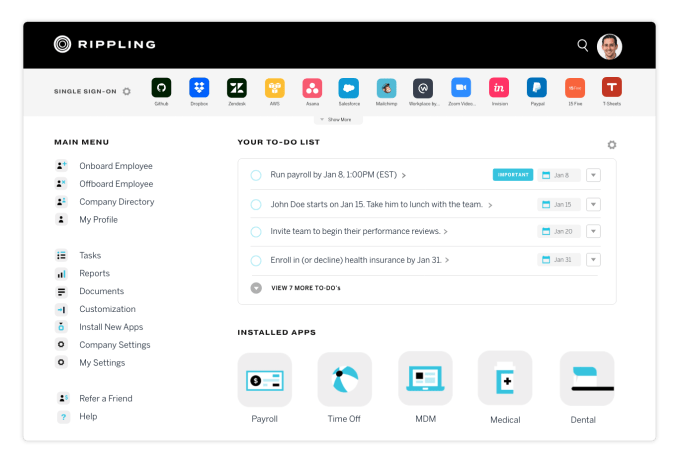

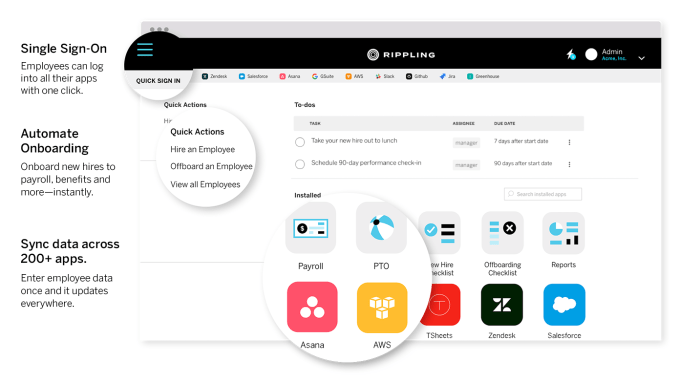

Parker Conrad likes to save time, even though it’s gotten him in trouble. The former CEO of Zenefits was pushed out of the $4.5 billion human resources startup because he built a hack that let him and employees get faster insurance certifications. But 2.5 years later, he’s back to take the busy work out of staff onboarding as well as clumsy IT services like single sign-on to enterprise apps. Today his startup Rippling launches its combined employee management system, which Conrad calls a much larger endeavor than the minimum viable product it announced while in Y Combinator’s accelerator 18 months ago.

“It’s not an HR system. It’s a level below that,” Conrad tells me. “It’s this unholy, crazy mashup of three different things.” First, it handles payroll, benefits, taxes and PTO across all 50 states. “Except Syria and North Korea, you can pay anyone in the world with Rippling,” Conrad claims. That makes it a competitor with Gusto… and Zenefits.

Second, it’s a replacement for Okta, Duo and other enterprise single-sign on security apps that authenticate staffers across partnered apps. Rippling bookmarklets make it easy to auth into over 250 workplace apps, like Gmail, Slack, Dropbox, Asana, Trello, AWS, Salesforce, GitHub and more. When an employee is hired or changes teams, a single modification to their role in Rippling automatically changes all the permissions of what they can access.

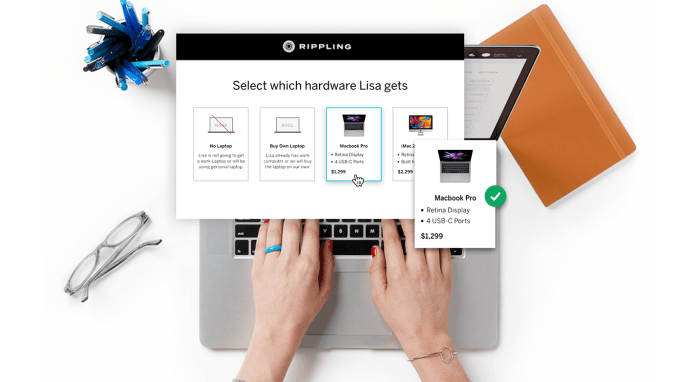

And third, it handles computer endpoint security like Jamf. When an employee is hired, Rippling can instantly ship them a computer with all the right software installed and the hard drive encrypted, or have staffers add the Rippling agent that enforces the company’s security standards. The system is designed so there’s no need for an expert IT department to manage it.

“Distributed, fragmented systems of record for employee data are secretly the cause of almost all the annoying administrative work of running a company,” Conrad explains. “If you could build this system that ties all of it together, you could eliminate all this crap work.” That’s Rippling. It’s opening up to all potential clients today, charging them a combined subscription or à la carte fees for any of the three wings of the product.

Conrad refused to say how much Rippling has raised total, citing the enhanced scrutiny Zenefits’ raises drew. But he says a Wall Street Journal report that Rippling had raised $7 million was inaccurate. “We haven’t raised any priced VC rounds. Just a bunch of seed money. We raised from Initialized Capital, almost all the early seed investors at Zenefits and a lot of individuals.” He cited Y Combinator, YC Growth Fund, YC’s founder Jessica Livingston and president Sam Altman, other YC partners, as well as DFJ and SV Angel.

“Because we were able to raise a bunch of money and court great engineers . . . we were able to spend a lot of time building this fundamental technology,” Conrad tells me. Rippling has about 50 team members now, with about 40 of them being engineers, highlighting just how thoroughly Conrad wants to eradicate manual work about work, starting with his own startup.

The CEO refused to discuss details of exactly what went down at Zenefits and whether he thought his ejection was fair. He was accused of allowing Zenefits’ insurance brokers to sell in states where they weren’t licensed, and giving some employees a macro that let them more quickly pass the online insurance certification exam. Conrad ended up paying about $534,000 in SEC fines. Zenefits laid off 430 employees, or 45 percent of its staff, and moved to selling software to small-to-medium sized businesses through a network of insurance brokers.

But when asked what he’d learned from Zenefits, Conrad looked past those troubles and instead recalled that “one of the mistakes that we made was that we did a lot stuff manually behind the scenes. When you scale up, there are these manual processes, and it’s really hard to come back later when it’s a big hard complicated thing and replace it with technology. You get upside down on margins. If you start at the beginning and never let the manual processes creep in . . . it sort of works.”

Perhaps it was trying to cut corners that got Conrad into the Zenefits mess, but now that same intention has inspired Rippling’s goal of eliminating HR and IT drudgery with an all-in-one tool.

“I think I’m someone who feels the pain of that kind of stuff particularly strongly. So that’s always been a real irritant to me, and I saw this problem. The conventional wisdom is ‘don’t build something like this, start with something much smaller,’ ” Conrad concludes. “But I knew if I didn’t do this, that no one else was gong to do it and I really wanted this system to exist. This is a company that’s all about annoying stuff and making that fucking annoying stuff go away.”

Powered by WPeMatico