wework

Auto Added by WPeMatico

Auto Added by WPeMatico

In Silicon Valley, investors don’t expect their portfolio companies to be profitable. “Blitzscaling: The Lightning-Fast Path to Building Massively Valuable Companies,” a bible for founders, instead calls for heavy spending on growth to scale in an Amazon -like fashion.

As for Wall Street, it’s shown an affinity for stock in Jeff Bezos’ business, despite the many years it spent navigating a path to profitability, as well as other money-losing endeavors. Why? Because it too is far less concerned with profitability than market opportunity.

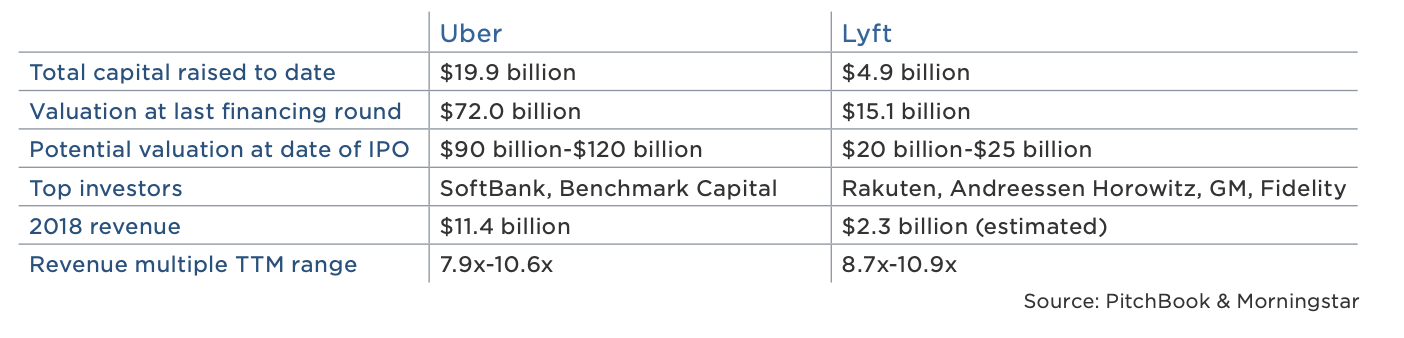

Lyft, a ride-hailing company expected to go public this week, is not profitable. It posted losses of $911 million in 2018, a statistic that will make it the biggest loser amongst U.S. startups to have gone public, according to data collected by The Wall Street Journal. On the other hand, Lyft’s $2.2 billion in 2018 revenue places it atop the list of largest annual revenues for a pre-IPO business, trailing behind only Facebook and Google in that category.

Wall Street, in short, is betting on Lyft’s revenue growth, assuming it will narrow its loses and reach profitability… eventually.

Lyft, losses notwithstanding, is growing rapidly and Wall Street is paying attention. On the second day of its road show, reports emerged that its IPO was already oversubscribed. As a result, Lyft is said to have upped the cost of its stock, with new plans to raise more than $2 billion at a valuation upwards of $25 billion. That represents a revenue multiple of more than 11x, a step up multiple of more than 1.6x from its most recent private valuation of $15.1 billion and, of course, Wall Street’s insatiable desire for unicorns, profitable or not.

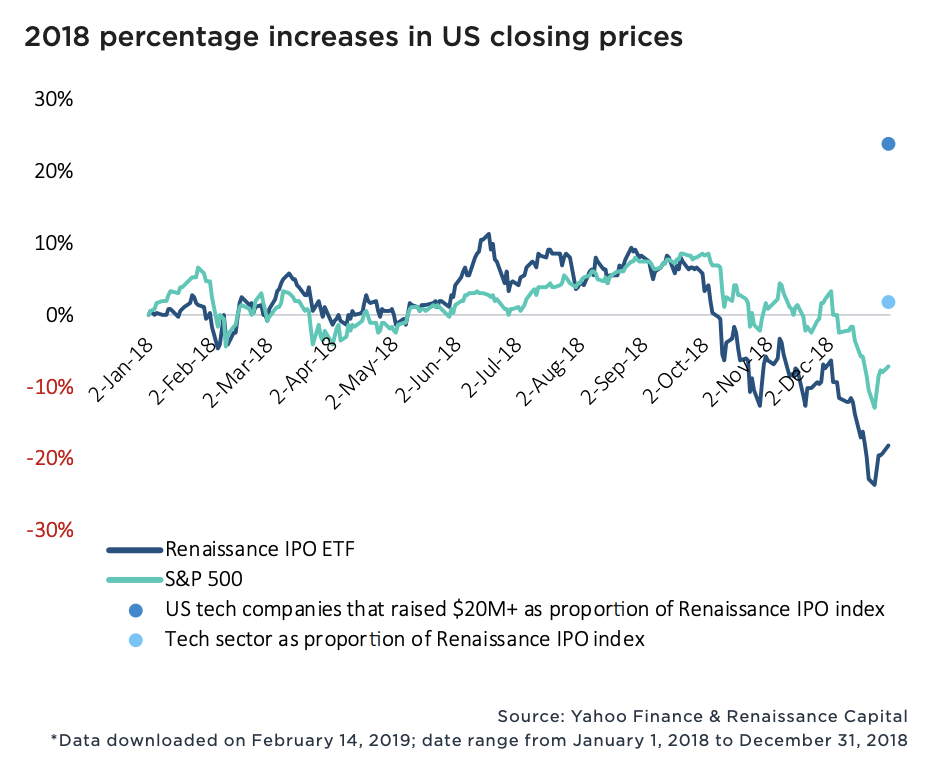

New data from PitchBook exploring the performance of billion-dollar-plus VC exits confirms Wall Street’s leniency toward unprofitable tech companies. Sixty-four percent of the 100+ companies valued at more than $1 billion to complete a VC-backed IPO since 2010 were unprofitable, and in 2018, money-losing startups actually fared better on the stock exchange than money-earning businesses. Moreover, U.S. tech companies that had raised more than $20 million traded up nearly 25 percent of 2018, while the S&P 500 technology sector posted flat returns.

Wall Street is still adapting to the rapid growth of the tech industry; public markets investors, therefore, are willing to deal with negative to minimal cash flows for, well, a very long time.

There’s no doubt Lyft and its much larger competitor, Uber, will go public at monstrous valuations. The two IPOs, set to create a whole bunch of millionaires and return a number of venture capital funds, will provide Silicon Valley a lesson in Wall Street’s tolerance for outsized exits.

Much like a seed-stage investor must bet on a founder’s vision, Wall Street, given a choice of several unprofitable businesses, has to bet on potential market value. Fortunately, this strategy can work quite well. Take Floodgate, for example. The seed fund invested a small amount of capital in Lyft when it was still a quirky idea for ridesharing called Zimride. Now, it boasts shares worth more than $100 million. I’m sure early shareholders in Amazon — which went public as a money-losing company in 1997 — are pretty happy, too.

Ultimately, Wall Street’s appetite for unicorns like Lyft is a result of the shortage of VC-backed IPOs. In 2006, it was the norm for a company to make its stock market debut at 7.9 years old, per PitchBook. In 2018, companies waited until the ripe age of 10.9 years, causing a significant slowdown in big liquidity events and stock sales.

Fund sizes, however, have grown larger and the proliferation of unicorns continues at unforeseen rates. That may mean, eventually, an influx of publicly shared unicorn stock. If that’s the case, might Wall Street start asking more of these startups? At the very least, public market investors, please don’t be swayed by WeWork‘s eventual stock offering and its “community adjusted EBITDA.” Silicon Valley’s pixie dust can’t be that potent.

Powered by WPeMatico

Hello Alfred — the startup that assigns in-home assistants to take care of your recurring chores and tasks — has announced the launch of a new service tier that will provide more properties and residents with access to the company’s underlying technology.

The company, which won the Startup Battlefield competition at our 2014 Disrupt event in San Francisco, looks to unlock valuable time for users by handling the long list of small routine items that add up over the course of a week and still require human oversight.

Hello Alfred partners with building owners to provide residents with dedicated home managers that assist with various errands and on-request services, such as apartment cleaning, grocery delivery, laundry services, prescription refills and more. Users have a direct line of communication with the company’s hospitality team through Hello Alfred’s mobile app, where they can manage tasks and set recurring appointments.

The new platform, “Powered by Alfred,” acts as a fairly similar but more accessible alternative to the company’s current offering. Residents in buildings equipped with “Powered by Alfred” are given access to all of the company’s solutions with the exception of the weekly visits from dedicated home managers currently included in the existing service. By excluding the dedicated in-home service, Hello Alfred is able to offer its new service tier at a lower price point and integrate with more buildings faster.

Property owners using “Powered by Alfred” can customize packages to include the services that best fit the needs of their residents and can upgrade or change service levels at any time. Both residents and building owners using the new platform are also given more control and direct access to Hello Alfred’s proprietary technology, allowing users to control functions that normally fall under the purview of the company’s dedicated home managers.

Additionally, with the launch of the new offering, Hello Alfred will be consolidating its various solutions under one central app, where residents and building managers can handle all inquiries, appointments and payments.

Hello Alfred’s new service tier, “Powered by Alfred,” provides a single, shared access point for resident and property owners to manage inquiries and drive property performance / Hello Alfred Press Kit

The launch of “Powered by Alfred” seems to be a natural evolution for the company, which seeks to make its offering more accessible to all residents of all backgrounds.

Hello Alfred previously employed a consumer-facing business model, in which customers would pay a monthly subscription fee for the array of in-home services and access to the company’s team of hospitality specialists, referred to as Alfreds.

However, around the time of the startup’s Series B round, Hello Alfred adopted the model of partnering directly with property owners to offer its services complimentary to residents. The partnership structure was not only a more conducive model for scaling but also enabled the company to offer the same services to any resident in an Alfred-equipped building, regardless of socioeconomic status.

Hello Alfred quickly built up a sizeable backlog of property owners hoping to integrate the platform into their units, according to the company. However, the task of maintaining dedicated staffing for every unit in every location made it difficult for the Alfred team to satisfy its swelling demand, having to instead focus resources primarily on luxury properties.

With “Powered by Alfred” removing in-home management services, the company has been able to improve accessibility and better satisfy the market’s appetite for its services, now rolling out the offering to non-luxury buildings and properties that previously sat in its pipeline.

Behind the launch of the new platform — which the company has piloted over the course of several months — Hello Alfred has increased its market share by more than 50 percent, with its services now available in more than 150,000 residential properties.

“We want Alfred to be a utility. We want to make “help” a universal utility and make it something anyone can access,” Hello Alfred CEO and co-founder Marcela Sapone told TechCrunch. “We wanted to find a way where we could accelerate growth and get human-focused help into urban buildings to help most urban environments.”

The launch represents the latest step in Hello Alfred’s broader expansion plans, which appear to have ramped up in recent months. Hello Alfred is now active in 16 cities — including Houston, where the company plans to launch next week — with its new offering available across all of its active markets. The startup already boasts an impressive partnership roster that includes more than 20 of the largest property owners in the U.S., and the Alfred team expects its new offering to open up further opportunities for partnerships across different property classes and different stages of a resident’s life cycle.

“As WeWork transformed commercial real estate, Hello Alfred is transforming residential real estate, and redefining what it means to live in a city today,” said Sapone. “This business expansion allows us to not only satisfy increasing demand for our service, but to connect every part of the resident experience — from the moment you sign your lease, until the moment you move to another Hello Alfred building.”

To date, the company has raised just over $63.5 million in venture capital, according to data from PitchBook, from prestigious investment brands that include New Enterprise Associates, Spark Capital, SV Angel, Moderne Ventures, Invesco and others.

Powered by WPeMatico

Finding myself talking at a startup conference in Kosovo three years ago (as one does), I realized how close I was to Albania, a place which held some fascination for me. I managed to grab a lift with a friendly techie to Tirana, where they arranged for me to speak to the local tech community. That meetup was held in a small co-working space called Talent Garden. It gradually transpired that, while WeWork and other such co-working/offices spaces were concentrating on New York and London, Talent Garden had been busily populating southern and eastern Europe with a network of spaces crisscrossing the continent.

That strategy has now paid off with their desire to raise money from investors. Today, it announces that it has raised €44 million ($49.5 million) in a funding round led by Italian private equity firm Tamburi Investment Partners alongside Social Capital, Inadco Ventures and a range of European family offices. Tamburi previously led a €12 million funding round for Talent Garden in 2016.

The company, founded in Brescia, Italy in 2011, now plans to expand its co-working and education to places like Spain, Italy, Denmark, Austria and many more countries around Europe, focusing on second or third-tier cities where tech communities tend to grow fastest because costs are lower than in the major capitals.

Talent Garden’s chief executive and co-founder Davide Dattoli now plans to open 20 new international co-working campuses over the next five years and expand the scope of its “Innovation School” in digital training (as an analogy, think a combination of offices and General Assembly) and generating a “second tech ecosystem” around Europe outside London, Paris and Berlin. It’s also a licensee of the SingularityU Summit brand across Italy, Spain and Switzerland, for instance.

So far, it is now present in eight countries and has 23 active campuses with the Talent Garden Innovation School present in five of those countries.

There will, however, be a particular focus on Spain, with new locations in Madrid and Barcelona; France, with one opening planned in 2019; Italy, where it already has more than 10 campuses; and Austria, where it just recently opened.

In 2018, Talent Garden opened a new campus in Dublin as part of a strategic partnership with Dublin City University and also created a joint venture with Rainmaking Loft in Denmark, and has more than three locations across Copenhagen and is now looking for more locations in the Nordic region. Germany, Israel, Benelux and the CEE region are also within its sights. It won’t be ignoring San Francisco, however, with a kind of the “campus” project planned for next year.

Will things be different as Talent Garden tries to make incursions into bigger cities? For starters, WeWork is building from a very expensive base (major capitals) while TG isn’t. There are fewer revenues in these third-tier cities, sure, but geography has been downgraded for startup teams that are well-used to remote working. So TG could try to lock-in members who only need to “pop in” to the major capitals now and again, where TG has a “landing pad” for them to visit. This potentially creates an incursion into WeWork’s space directly from emerging markets and second/third-tier cities.

Powered by WPeMatico

A Chinese startup that’s taking a dorm-like approach to urban housing just raised $500 million as its valuation jumped over $2 billion. Danke Apartment, whose name means “eggshell” in Chinese, closed the Series C round led by returning investor Tiger Global Management and newcomer Ant Financial, Alibaba’s e-payment and financial affiliate controlled by Jack Ma.

Four years ago, Beijing-based Danke set out with a mission to provide more affordable housing for young Chinese working in large urban centers. It applies the co-working concept to housing by renting apartments that come renovated and fully furnished, a model not unlike that of WeWork’s WeLive. The idea is by slicing up a flat designed for a family of three to four — the more common type of urban housing in China — into smaller units, young professionals can afford to live in nicer neighborhoods as Danke takes care of hassles like housekeeping and maintenance. To date, the startup has set foot in 10 major Chinese cities.

With the new funds, Danke plans to upgrade its data processing system that deals with rental transactions. Housing prices are set by AI-driven algorithms that take into account market forces such as locations rather than rely on the hunches of a real estate agent. The more data it gleans, the smarter the system becomes. That layout is the engine of the startup, which believes an internet platform play is a win-win for both homeowners and tenants because it provides greater transparency and efficiency while allowing the company to scale faster.

“We are focused on business intelligence from day one,” Danke’s angel investor and chairman Derek Shen told TechCrunch in an interview. Shen was the former president of LinkedIn China and was instrumental in helping the professional networking site enter the country. “By doing so we are eliminating the need to set up offline retail outlets and are able to speed up the decision-making process. What landlords normally care is who will be the first to rent out their property. The model is also copyable because it requires less manpower.”

“We’ve proven that the rental housing business can be decentralized and done online,” added Shen.

Photo: Danke Apartment via Weibo

Danke doesn’t just want to digitize the market it’s after. Half of the company’s core members have hailed from Nuomi, the local services startup that Shen founded and was sold to Baidu for $3.2 billion back in 2015. Having worked for a business whose mission was to let users explore and hire offline services from their connected devices, these executives developed a propensity to digitize all business aspects, including Danke’s day-to-day operations, a scheme that will also take up some of the new funds. This will allow Danke to “boost operational efficiency and cut costs” as it “actively works with the government to stabilize rental prices in the housing market,” the company says.

The rest of the proceeds will go toward improving the quality of Danke’s apartment amenities and tenant experiences, a segment that Shen believes will see great revenue potential down the road, akin to how WeWork touts software services to enterprises. The money will also enable Danke, which currently zeroes in on office workers and recent college graduates, to explore the emerging housing market for blue-collar workers.

Other investors from the round include new backer Primavera Capital and existing investors CMC Capital, Gaorong Capital and Joy Capital.

China’s rental housing market has boomed in recent years as Beijing pledges to promote affordable apartments in a country where few have the money to buy property. As President Xi Jinping often stresses, “houses are for living in, not for speculation.” As such, investors and entrepreneurs have been piling into the rental flat market, but that fervor has also created unexpected risks.

One much-criticized byproduct is the development of so-called “rental loans.” It goes like this: Housing operators would obtain loans in tenants’ names from banks or other lending institutions allegedly by obscuring relevant details from contracts. So when a tenant signs an agreement that they think binds them to rents, they have in fact agreed to take on loans and their “rent” payments become monthly loan repayments.

Housing operators are keen to embrace such practices because the loans provide working capital for renovation and their pipeline of properties. On the other hand, the capital allows companies like Danke to lower deposits for cash-strapped young tenants. “There’s nothing wrong with the financial instrument itself,” suggested Shen. “The real issue is when the housing operator struggles to repay, so the key is to make sure the business is well-functioning.”

Danke, alongside competitors Ziroom and 5I5J, has drawn fire for not fully informing tenants when signing contracts. Shen said his company is actively working to increase transparency. “We will make it clear to customers that what they are signing are loans. As long as we give them enough notice, there should be little risk involved.”

Powered by WPeMatico

Co-working juggernaut WeWork (now known as the We Company) has laid off 3 percent of its global workforce, or roughly 300 employees, the company told TechCrunch. The heavily funded business, most recently valued at a whopping $47 billion, employs 10,000 people around the world.

Headquartered in New York, the layoffs were performance-related, part of the company’s routine process of shedding underperformers. Among the departments impacted by the cuts were WeWork’s engineering team, product and user experience design.

“Over the past nine years, WeWork has grown into one of the largest global physical networks thanks to the hard work and dedication of our team,” the company said in a statement provided to TechCrunch. “WeWork recently conducted a standard annual performance review process. Our global workforce is now more than 10,000 strong, and we remain committed to continuing to grow and scale in 2019, including hiring an additional 6,000 employees.”

WeWork has raised more than $8 billion in venture capital funding since it emerged to disrupt office sharing. The business is backed significantly by the SoftBank Vision Fund, which invested $2 billion in WeWork as recently as January.

Powered by WPeMatico

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

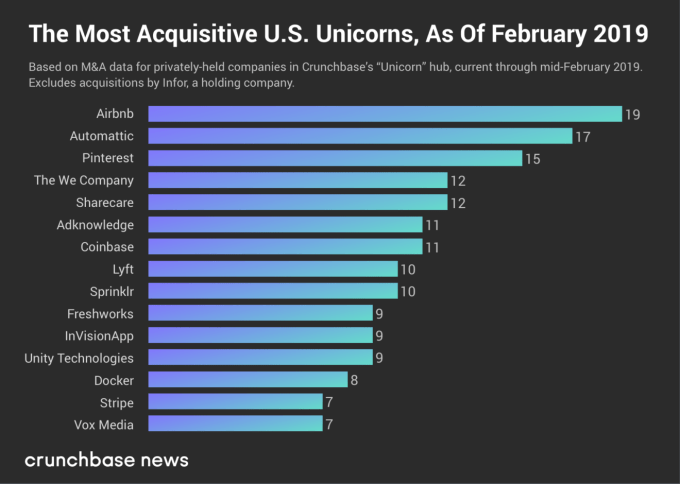

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

It has been just about a year since the relaunch of WeWork Labs, an accelerator-type program operating under the WeWork umbrella. Since then, it has grown to 37 locations in 22 cities. And it’s truly international, operating in 12 countries, including Brazil, China, Germany and India.

These Labs offices are often — but not always — housed within a larger WeWork space, and, like an accelerator, they offer mentorship and programming. However, WeWork doesn’t take any equity; instead, it simply makes money by charging rent. (In New York, a desk costs between $450 and $550 a month, but the price varies by location.)

I spoke to Roee Adler, the program’s global head, about how Labs has evolved over the past year. Adler actually has a long history with startups — in fact, his company Soluto won the very first Startup Battlefield at TechCrunch Disrupt. He’s held a number of positions at WeWork, including chief product officer, and he said that as his role was evolving, he found himself asking, “What is the next startup we can build inside WeWork?”

The answer: “We decided to reevaluate our level of commitment and investment with the earliest of stages for startups.”

WeWork actually had a startup program called WeWork Labs back in 2011, but it languished in the years since. Adler relaunched the program with its first New York space in January of last year, and he’s been opening locations at a furious pace since then.

Roee Adler

Each Labs office is supervised by a Labs manager, who Adler said is usually “a former entrepreneur whose life’s mission is to manage startups.” For example, before Mor Barak joined the program last year to launch Labs in Tel Aviv, she was the general manager of Israel’s oldest accelerator program, The Junction.

“I got to a point where I felt like I finally found what I loved to do, which is to work with startups and to support startups and understand how our connections and our network can help them move forward,” Barak said. “And then I wanted to take that and do that on a bigger scale, as part of a company that can reach new geographies and bring forward local entrepreneurs.”

As a Labs manager, Barak said her main role is to “be that business connector for the startups,” which means meeting with the entrepreneurs on a weekly basis to understand their needs and challenges. At the same time, she emphasized that Labs is a global program: “As a Labs manager in Tel Aviv, I can quite easily connect to my colleagues around the world to find the people that I need to get to in order to help the startup.”

Adler made a similar point about sharing resources between the different locations.

“A lecture that is at our Najing Xi Lu Road space in Shanghai will get captured, summarized, translated and become available to all of the entrepreneurs around the world,” he said. “Does that mean every piece of information is relevant for everyone? No. But truthfully, who knows?”

Adriana Vazquez of Lilu

To celebrate the one-year anniversary, WeWork Labs held a pitch competition at the company’s New York City headquarters last week, with $250,000 in funding distributed among the winners. The $150,000 grand prize went to Lilu, a startup making a compression bra that helps mothers pump milk. (It’s another Startup Battlefield alum.)

CEO and co-founder Adriana Vazquez told me that Lilu has been working out of the WeWork Labs in Dumbo since August. Vazquez has participated in other accelerator programs and worked out of other co-working spaces, and she said Labs is something else — it allows you to “get the community of an accelerator without the prescribed schedule,” and it offers a very different feeling from a co-working space.

“There is that understanding and respect that everyone’s really busy and has fires to put out,” she said. “We had a brief stay at another co-working space with creatives and small businesses, and there wasn’t that camaraderie, where you see someone that’s working on a weekend and you know you’re not here because they want to hang out on a Friday. It’s almost an unspoken understanding: Yeah, I know what you’re going through.”

As for what Adler has planned for Labs’ second year, he said he wants to do more work connecting startups with larger corporations: “WeWork has really become the only natural nexus in the world where you can have a three-month-old startup entrepreneur bumping shoulders with a senior vice president of Microsoft going to get coffee from the same machine and engaging in a conversation about the future.”

WeWork Labs Dumbo

And of course, he plans to open more offices, with the goal of reaching 100 locations by the end of 2019.

“The three of us are sitting in Manhattan right now, one of the wealthiest cities in the world … but it’s not about here,” Adler said. “It’s about the people who aren’t sitting in the big tech hubs or bubbles. That is exciting.”

Powered by WPeMatico

When considering the structural impact of technology companies on our economy and society, we tend to focus on questions of scale and monopoly.

It’s true that the FAANG companies and more recent winners (Airbnb, Uber) have surfed a combination of network effects, preferential access to capital and classic efficiencies of scale to generate tremendous value for their shareholders — to the detriment of new entrants who attempt to unseat them.

At their high water mark in mid-2018, FAANG alone made up 11 percent of the total market cap of the S&P 500 and 38 percent of the index’s year-to-date gain, representing a doubling in their influence in only five years. The question of regulating technology companies — to the point of instituting anti-trust actions — has even become a rare point of relative concord between Democrats and Republicans in Congress.

But is the narrative of tech companies in the 2010s only a story of economic consolidation and growing inequality? Many of the most successful B2B startups of the last decade are aligned by a theme that paints a different picture. By transforming the nature of the costs required to start a business, these startups are reducing the influence of capital and leveling the playing field for new entrants to share in the surplus generated by the secular shift to a tech-mediated economy.

Source: Getty Images/MIKIEKWOODS

What do AWS, WeWork, Stord, Gusto

But they are alike in the economic purpose they serve for their customers. Each of these services takes a fixed cost — a bank of servers, a lease, a legal retainer — and transforms it into a variable cost. As a refresher, a fixed cost stays constant regardless of output, and variable costs scale with the output of a business.

When my father started his software consulting business in the early 1990s, I remember the giant boxes of AIX servers that arrived at our apartment, and tagging along to office tours in central New Jersey before he decided to run the company out of our spare bedroom. Back then, starting almost any kind of business was hard because of high fixed costs. Without AWS or WeWork, you shelled out upfront for hardware and a lease.

Access to capital, whether in the form of a bank loan, savings or friends and family was a prerequisite for entrepreneurship.

Today, startups make it possible to start and scale almost any kind of business while incurring few fixed costs. Want to found an e-commerce store? Start with a free Shopify account and dropship your inventory. Want to become a freelance designer? Put a shingle up on Fiverr and meet clients at a Breather you rent by the hour.

Whether software or hardware or labor, building a business is way easier when overhead is transformed into a string of flexible microservices that you only pay for as you grow.

Image courtesy of Getty Images

Taken together, startups that turn fixed costs into variable costs make it less capital-intensive to start a business. This decreases the influence of gatekeepers and aggregators of capital — an impact evident in the way entrepreneurs think about starting businesses today.

It’s no coincidence that the rise of B2B startups fitting this theme has coincided with the bootstrap movement, in which tech entrepreneurs with major ambitions demur from raising venture funding because — well, they don’t need the money anymore.

It has also coincided with a renaissance in freelance entrepreneurship: 56.7 million Americans freelanced in 2018. Beyond the economic benefits of working for yourself — the fastest growing segment of freelancers earns more than $75,000 a year — freelancers can access the lifestyle and health benefits of owning their destiny, which aren’t directly captured but play a role in the economic picture. Indeed, 51 percent of freelancers said no amount of money would lure them into a traditional job, and 64 percent reported feeling healthier and happier.

When capital plays a reduced role in new business formation, access to capital plays a smaller role in determining who will succeed. More companies are founded, and the economy becomes more likely to birth new Davids that will unseat the Goliaths. Economics 101: lower barriers to entry create markets that converge on perfect competition instead of oligarchic concentration.

Source: Getty Images/ERHUI1979

Variable costs have their downsides. A startup with a relatively higher proportion of fixed costs — the profile of the classic high-tech software business — can achieve higher profit margins as it scales. Compare Microsoft or Google, which pay high fixed costs in the form of salaries and servers but few costs in delivering their services and achieve operating margins of 25-30 percent, to Costco, which takes in more than $100 billion of annual revenue but earns an operating margin in the single digits.

That’s OK. Neither type of cost is “better” or “worse,” but having the option to decide how to structure costs through a company’s life cycle can meaningfully impact an entrepreneur’s ability to execute a business idea.

Founders investigating startup ideas — and politicians debating the impact of technology — would do well to pay attention to how B2B companies have democratized access to entrepreneurship.

Powered by WPeMatico

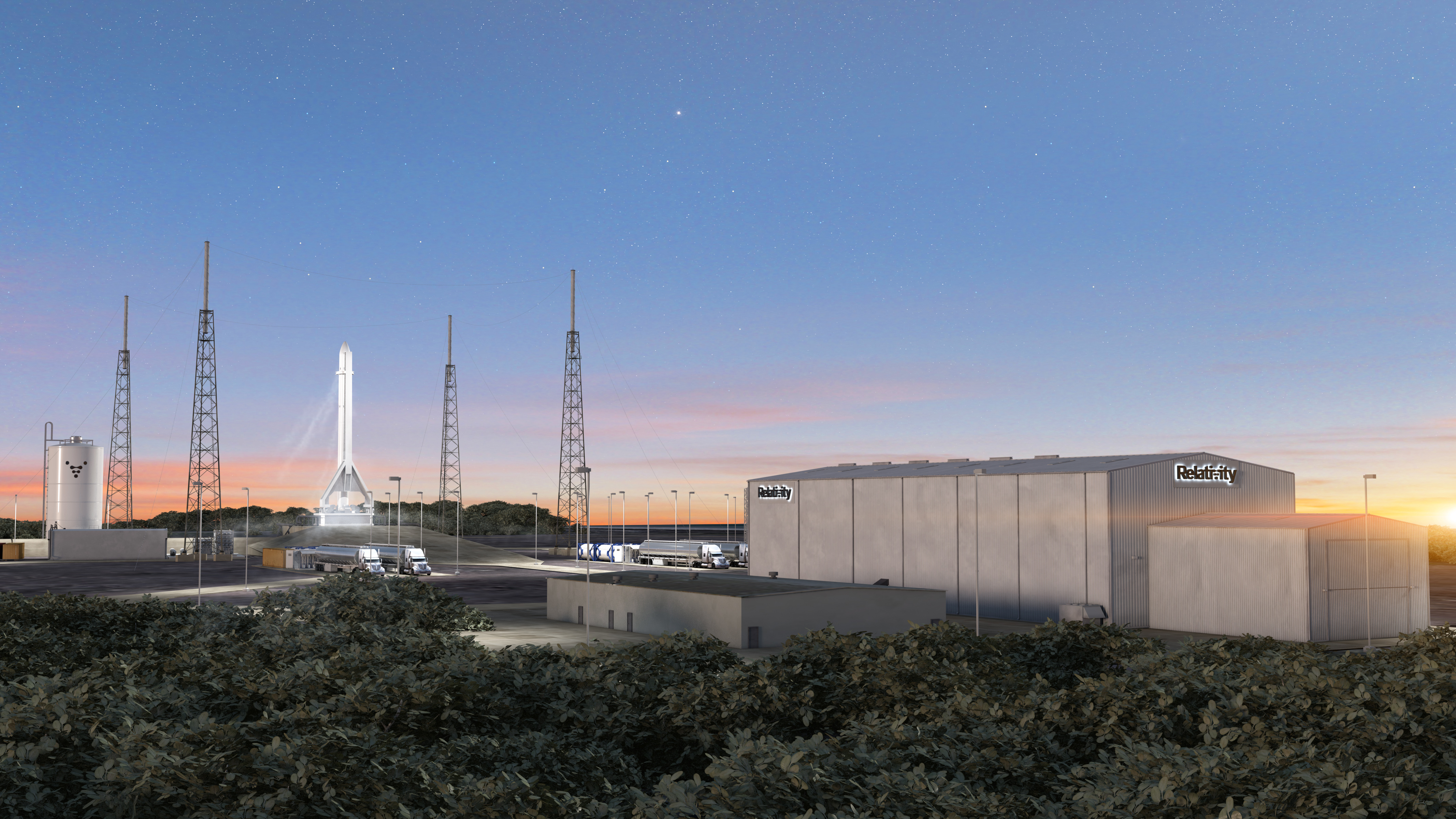

3D-printing the first rocket on Mars.

That’s the goal Tim Ellis and Jordan Noone set for themselves when they founded Los Angeles-based Relativity Space in 2015.

At the time they were working from a WeWork in Seattle, during the darkest winter in Seattle history, where Ellis was wrapping up a stint at Blue Origin . The two had met in college at USC in their jet propulsion lab. Noone had gone on to take a job at SpaceX and Ellis at Blue Origin, but the two remained in touch and had an idea for building rockets quickly and cheaply — with the vision that they wanted to eventually build these rockets on Mars.

Now, more than $35 million dollars later, the company has been awarded a multi-year contract to build and operate its own rocket launch facilities at Cape Canaveral Air Force Station in Florida.

That contract, awarded by The 45th Space Wing of the Air Force, is the first direct agreement the U.S. Air Force has completed with a venture-backed orbital launch company that wasn’t also being subsidized by billionaire owner-operators.

By comparison, Relativity’s neighbors at Cape Canaveral are Blue Origin (which Jeff Bezos has been financing by reportedly selling $1 billion in shares of Amazon stock since 2017); SpaceX (which has raised roughly $2.5 billion since its founding and initial capitalization by Elon Musk); and United Launch Alliance, the joint venture between the defense contracting giants Lockheed Martin Space Systems and Boeing Defense.

Like the other launch sites at Cape Canaveral, Launch Complex 16, where Relativity expects to be launching its first rockets by 2020, has a storied history in the U.S. space and missile defense program. It was used for Titan missile launches, the Apollo and Gemini programs and Pershing missile launches.

From the site, Relativity will be able to launch its first designed rocket, the Terran 1, which is the only fully 3D-printed rocket in the world.

That rocket can carry a maximum payload of 1,250 kilograms to a low earth orbit of 185 kilometers above the Earth. Its nominal payload is 900 kilograms of a Sun-synchronous orbit 500 kilometers out, and it has a 700 kilogram high-altitude payload capacity to 1,200 kilometers in Sun-synchronous orbit. Relativity prices its dedicated missions at $10 million, and $11,000 per kilogram to achieve Sun-synchronous orbit.

If the company’s two founders are right, then all of this launch work Relativity is doing is just a prelude to what the company considers to be its real mission — the advancement of manufacturing rockets quickly and at scale as a test run for building out manufacturing capacity on Mars.

“Rockets are the business model now,” Ellis told me last year at the company’s offices at the time, a few hundred feet from SpaceX. “That’s why we created the printing tech. Rockets are the largest, lightest-weight, highest-cost item that you can make.”

It’s also a way for the company to prove out its technology. “It benefits the long-term mission,” Ellis continued. “Our vision is to create the intelligent automated factory on Mars… We want to help them to iterate and scale the society there.”

Ellis and Noone make some pretty remarkable claims about the proprietary 3D printer they’ve built and housed in their Inglewood offices. Called “Stargate,” the printer is the largest of its kind in the world and aims to go from raw materials to a flight-ready vehicle in just 60 days. The company claims that the speed with which it can manufacture new rockets should pare down launch timelines by somewhere between two and four years.

Another factor accelerating Relativity’s race to market is a long-term contract the company signed last year with NASA for access to testing facilities at the agency’s Stennis Space Center on the Mississippi-Louisiana border. It’s there, deep in the Mississippi delta swampland, that Relativity plans to develop and quality control as many as 36 complete rockets per year on its 25-acre space.

All of this activity helps the company in another segment of its business: licensing and selling the manufacturing technology it has developed.

“The 3D factory and automation is the other product, but really that’s a change in emphasis,” says Ellis. “It’s always been the case that we’re developing our own metal 3D printing technology. Not only can we make rockets. If the long-term mission is 3D printing on Mars, we should think of the factory as its own product tool.”

Not everyone agrees. At least one investor I talked to said that in many cases, the cost of 3D printing certain basic parts outweighs the benefits that printing provides.

Still, Relativity is undaunted.

But first, the company — and its competitors at Blue Origin, SpaceX, United Launch Alliance and the hundreds of other companies working on launching rockets into space again — need to get there. For Relativity, the Canaveral deal is one giant step for the company, and one great leap toward its ultimate goal.

“This is a giant step toward being a launch company,” says Ellis. “And it’s aligned with the long-term vision of one day printing on Mars.”

Powered by WPeMatico

The company formerly known as WeWork has come under scrutiny for potential conflict of interest issues regarding CEO Adam Neumann’s partial ownership of three properties where WeWork is (or will be) a tenant. TechCrunch has seen excerpts of the company’s prospectus for investors that details upwards of $100 million in total future rents WeWork will pay to properties owned, in part, by Adam Neumann.

In March 2018, The Real Deal reported that Neumann had purchased a 50 percent stake in 88 University Place alongside fashion designer Elie Tahari. That property was then leased by WeWork, which then leased space within the building to IBM.

Today, the WSJ is reporting that 88 University Place isn’t alone. Neumann also personally invested in properties in San Jose that are either currently leased to WeWork as a tenant or are earmarked for such a purpose. Unlike 88 University, where Neumann is a 50/50 owner with Tahari, the CEO of the We Company — as WeWork is now known — invested in the two San Jose properties as part of a real estate consortium and owns a smaller stake of an unspecified percentage.

These transactions were all disclosed in the company prospectus documents it filed as part of its $700 million bond sale in April 2018. According to the prospectus, WeWork’s total future rents on these properties (partially owned by Neumann) are $110.8 million, as of December 2017.

That doesn’t include the reported $65 million purchase of a Chelsea property by Neumann and partners, which is said to be earmarked for a new WeLive space built from the ground up. That, too, will be subject to rent payments from the We Company to run WeLive out of it.

This raises questions of whether there is a conflict of interest in Neumann being both the landlord and the tenant of properties through WeWork. The WSJ says that investors of the company are concerned that the CEO could personally benefit on rents or other terms with the company in these deals.

According to WeWork, however, the company has not been made aware of any issues by any of its investors about related party transactions or their disclosures. The company also said that the majority of the Board are independent of Adam and all of these transactions were approved.

A WeWork spokesperson also had this to say: “WeWork has a review process in place for related party transactions. Those transactions are reviewed and approved by the board, and they are disclosed to investors.”

As it stands now, The We Company is privately held and in the midst of a transition as it contemplates how to turn a substantial profit on its more than 400 property assets across the world. The company is taking a broad-stroke approach, serving tiny startups and massive corporate clients alike, while also offering co-living WeLive spaces to renters and building out the Powered By We platform to spread its bets.

The company is valued at a hefty $47 billion, even after a scaled back investment from SoftBank (which went from $16 billion to $2 billion). But as the We Company inches toward an IPO, we may start to see a call for tighter corporate governance and more scrutiny of potential conflicts of interest.

Powered by WPeMatico