wework

Auto Added by WPeMatico

Auto Added by WPeMatico

After WeWork exploded there was — at least supposedly — a change in sentiment among investors and founders alike. Gone were the days of easy nine-figure rounds, expensive growth, negative unit economics and the rest of the excess that Startupland has enjoyed over the past half-decade.

Inside this purported sentiment shift, I presumed, was a decrease in optimism; surely venture capitalists and entrepreneurs would change their behavior inside this new paradigm?

But by some measures, they haven’t. I expected that startups would achieve more conservative proximate valuations in the post-WeWork world, as their leaders would aim to raise a bit less, and a bit more conservatively, and investors would be less starry-eyed in the prices they were willing to pay for startup equity.

That was all wrong, it turns out. A recent report from Fenwick and West, a legal firm that works with technology companies, paints a picture that is the complete opposite of what we might have anticipated.

Perhaps we shouldn’t be surprised; our recent reporting hardly describes a market in slowdown. Boston is having a good start to the year, for example. SaaS is also looking healthy from a venture capital perspective. Cloud stocks are at all-time highs and One Medical is still defying gravity as a public stock. Whatever lesson WeWork was supposed to teach, it doesn’t appear to have made much impact.

Let’s explore the Fenwick data and then ask if we can spot anywhere where the markets are behaving like the chastened children that we were told had taken over.

Powered by WPeMatico

As founding executive director of Tech:NYC, Julie Samuels is one of the state’s most prominent advocates for the tech sector, both in Albany and at City Hall.

Samuels, a lawyer by training, came to New York after serving as executive director of Engine, a San Francisco organization on which Tech:NYC is modeled. In an interview with TechCrunch, Samuels spoke about several issues, including her rationale for why, despite the controversy over Amazon’s decision not to build its second headquarters in Queens, the area is well-positioned for the next wave of tech innovation.

TechCrunch: What is the need for organizations like Tech:NYC and Engine?

Julie Samuels: As the tech industry matures, it is incredibly important that there are organizations [that] represent these companies politically, civically, making sure they have a seat at the table with so many public policy debates. There is no shortage of public policy debates surrounding technology.

It is also incredibly important that there are organizations who are talking from the viewpoint of smaller companies and startups. There are a lot of organizations that represent the biggest and most well-known companies, including Tech:NYC. But [we] also have hundreds of members who are small and growing startups. We think that diversity of the ecosystem is what really sets the technology sector apart and it is something we want to foster and celebrate.

Who are your members, then?

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

As One Medical looks to become the first venture-backed company to price its IPO in 2020 this afternoon and Casper aims to price its own shares next Wednesday, the market is gearing up for a pair of tests.

If you listen to the Nasdaq and the NYSE, IPO volume in 2020 will prove vibrant. A surprise, perhaps, in the wake of the WeWork meltdown that many had expected might reduce IPO cadence. One Medical and Casper, though, are charging ahead, meaning that their debuts will help set the tone for the 2020 IPO market.

If they struggle with weak pricing and slow initial trading, their disappointing offerings could slow the IPO market. If they price well and are welcomed by the street, however, the opposite.

Let’s take a look at how many IPOs are coming, what One Medical and Casper are hoping for and what their results might mean for unicorn liquidity. Don’t forget that we’re still living in the midst of a unicorn liquidity crisis — there are hundreds of private companies worth $1 billion or more around the world that need an exist, and the market is creating them faster than it can get them out the door. If IPOs stumble in 2020, lots just won’t make it out before the market turns.

Yesterday, CNBC reported notes from Nasdaq CEO Adena Friedman and NYSE President Stacey Cunningham, each speaking about their expected IPO cadence in 2020. Friedman said there are “lot of companies looking to tap the public markets in the first half,” implying a strong flow of potential debuts.

Powered by WPeMatico

Los Angeles is one of the most desirable locations for commercial real estate in the United States, so it’s little wonder that there’s something of a boom in investments in technology companies servicing the market coming from the region.

It’s one of the reasons that CREXi, the commercial real estate marketplace, was able to establish a strong presence for its digital marketplace and toolkit for buyers, sellers and investors.

Since the company raised its last institutional round in 2018, it has added more than 300,000 properties for sale or lease across the U.S. and increased its user base to 6 million customers, according to a statement.

It has now raised $30 million in new financing from new investors, including Mitsubishi Estate Company (“MEC”), Industry Ventures and Prudence Holdings . Previous investors Lerer Hippeau Ventures and Jackson Square Ventures also participated in the financing.

CREXi makes money three ways. There’s a subscription service for brokers looking to sell or lease property; an auction service where CREXi will earn a fee upon the close of a transaction; and a data and analytics service that allows users to get a view into the latest trends in commercial real estate based on the vast collection of properties on offer through the company’s services.

The company touts its service as the only technology offering that can take a property from marketing to the close of a sale or lease without having to leave the platform.

According to chief executive Mike DeGiorgio, the company is also recession-proof thanks to its auction services. “As more distressed properties hit the market, the best way to sell them is through an online auction,” DeGiorgio says.

So far, the company has seen $700 billion of transactions flow through the platform, and roughly 40% of those deals were exclusive to the company.

“The CRE industry is evolving, and market players, especially younger, digitally native generations are seeking out platforms that provide free and open access to information,” said Gavin Myers, general partner at Prudence Holdings, in a statement. “CREXi directly addresses this market need, providing fair access to a range of CRE information. As CREXi continues to build out its stable of services, features, and functionality, we’re thrilled to partner with them and support the company’s continued momentum.”

CREXi joins the ranks of startups based in Los Angeles that have raised money to reshape the real estate industry. Estimates from Built in LA count roughly 127 companies, which have raised in excess of $2.4 billion, active in the real estate industry in Los Angeles. These companies range from providers of short-term commercial office space, like Knotel, or co-working companies like WeWork, to companies focused on servicing the real estate industry like Luxury Presence, which raised a $5 million round earlier in the year.

Due to inaccurate information provided by the company, an initial version of this story indicated that CREXi had raised $29 million in its Series B round. The correct number is $30 million.

Powered by WPeMatico

One of the enduring truths of big companies is that they aren’t innovative. They are “innovative” in the marketing sense, but fail to ever execute on new ideas, particularly when those ideas cannibalize existing products and revenues.

So it often takes a real competitor to force these incumbent, legacy businesses to evolve in any meaningful way. Usually that change leads to disruption, in the classic way that Clayton Christensen describes in “The Innovator’s Dilemma.” An upstart company creates a new technology or business model that is better for an under-served segment of a market, and as that company improves, it competes directly with the incumbent and eventually wins over its market with a vastly superior product.

Unfortunately, real life isn’t so easy, as WeWork and MoviePass have shown us over the past few years.

In both cases, there were incumbents. In movie theaters, you had AMC and the like, which built a business model around ticket sales (shared with movie studios) and food/beverage concessions that targeted occasional customers at a high price point. Meanwhile, in commercial real estate, you had large landowners and family holders who demanded extremely long rent terms at high prices, often with personal financial guarantees from the CEO of the tenant firm.

Powered by WPeMatico

This week we’ve covered layoffs at unicorns both inside the Vision Fund and out. This afternoon we add two more to our list: Oyo and Rappi.

The staff reductions are surprising — and not. They are surprising, as Oyo (India-based, low-cost hotels) and Rappi (Latin America-focused e-commerce) were bright lights in the Vision Fund’s crown. And the layoffs are not surprising as other famous unicorns have recently cut staff in a bid to reduce costs, diminish losses and aim closer to profitability.

Our net lack of shock is underscored by the Vision Fund itself, which signaled late last year that it wants portfolio companies to get profitable and get public. The cuts are therefore a little more than unsurprising; we should have anticipated them.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

A million dollars isn’t cool. You know what’s cool? Positive adjusted EBITDA, or something close to it.

That’s the message from scooter unicorn Lime, which announced this week that it was cutting about 14% of its staff and closing a dozen markets. The staff reductions, numbering about 100, come as the company has touted efforts to improve its profitability — going as far as setting targets for when it might reach capital freedom, as well as highlighting the matter in a recent corporate blog post.

(Bird, a Lime competitor, also underwent layoffs this year.)

What’s going on? Unicorns, once hungry for growth, are now hell-bent to show current (and future) investors that their businesses aren’t unprofitable quagmires. Profitability, or movement towards it, is hot, and Lime is a good example of the trend — as is Getaround, which also wrote about its own layoffs this week. Let’s dig in.

Powered by WPeMatico

Welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week I wrote about the startups we lost in 2019. Before that, I noted the defining moments of VC in 2019.

Unfortunately, this will be my last newsletter, as I am leaving TechCrunch for a new opportunity. Don’t worry, Startups Weekly isn’t going anywhere. We’ll have a new writer taking over the weekly update soon enough; in the meantime, TechCrunch editor Henry Pickavet will be at the helm. You can still get in touch with me on Twitter @KateClarkTweets.

If you’re new here, you can subscribe to Startups Weekly here. Lots of good content will be coming your way in 2020.

TechCrunch reporter Manish Singh penned an interesting piece on the state of Indian startups this week: As Indian startups raise record capital, losses are widening (Extra Crunch membership required). In it, he claims the financial performance of India’s largest startups are cause for concern. Gems like Flipkart, BigBasket and Paytm have lost a collective $3 billion in the last year.

“What is especially troublesome for startups is that there is no clear path for how they would ever generate big profits,” he writes. “Silicon Valley companies, for instance, have entered and expanded into India in recent years, investing billions of dollars in local operations, but yet, India has yet to make any substantial contribution to their bottom lines. If that wasn’t challenging enough, many Indian startups compete directly with Silicon Valley giants, which while impressive, is an expensive endeavor.”

Manish’s story came one day after The New York Times published an in-depth report on Oyo, a tech-enabled budget hotel chain and rising star in the Indian tech community. The NYT wrote that Oyo offers unlicensed rooms and has bribed police officials to deter trouble, among other toxic practices.

Whether Oyo, backed by billions from the SoftBank Vision Fund, will become India’s WeWork is the real cause for concern. India’s startup ecosystem is likely to face a number of barriers as it grows to compete with the likes of Silicon Valley.

Follow Manish here or on Twitter for more of TechCrunch’s growing India coverage.

If you’ve still not subscribed to Extra Crunch, now is the time. Longtime TechCrunch reporter and editor Josh Constine is launching a new series to teach you how to pitch your startup. In it he will examine embargoes, exclusives, press kit visuals, interview questions and more. The first of many, How to find the right reporter to pitch your startup, is online now.

Subscribe to Extra Crunch here.

Another week, another new episode of TechCrunch’s venture capital-focused podcast, Equity. This week, we discussed a few of 2019’s largest scandals, Peloton’s strange holiday ad and the controversy over at the luggage startup Away. Listen here and be sure to subscribe, too.

For anyone wondering about changes at Equity following my departure from TechCrunch, the lovely Alex Wilhelm (founding Equity co-host) will keep the show alive and, soon enough, there will be a brand new co-host in my place. Please keep supporting the show and be sure to recommend it to all your podcast-adoring friends.

Powered by WPeMatico

In the wake of WeWork’s embarrassing IPO rout, you might imagine that startups working in similar markets would cool it for a bit. Perhaps they could work on cutting spending, improving their gross margins, and, say, shooting for profitability.

Not so, at least in one case. Instead of doing those things, China-based Ucommune filed to go public in America this month. The WeWork competitor is mostly a co-working business. It’s also a marketing company. And it has some of the worst economics we’ve seen in a company since WeWork.

Why this company is trying to go public isn’t hard to understand. It needs the cash. But at the same time, the chance of it debuting at a price it likes seems slim, given the market’s recent history — as well as Ucommune’s own.

Before we chat about the business fundamentals of Ucommune, a primer on the company itself.

Founded in 2015, according to Crunchbase data, Ucommune has raised over hundreds of millions. In 2018 alone the company raised a venture round and its Series C and its Series D. Prior investors include Gopher Asset Management, Aikang Group, Tianhong Asset Management, All-Stars Investment and Longxi Real Estate.

TechCrunch reported that its final private round valued Ucommune at $3 billion.

All that capital was put to work. According to is F-1 filing, Ucommune operates 197 co-working facilities in 42 cities. The company also claims more than 600,000 members and nearly 73,000 workstations.

The WeWork similarities continue: While discussing itself in its IPO filing, the firm touts an “asset-light model,” which it claims helps property owners “benefit from our professional capabilities and strong brand recognition” as well as allowing its “business to scale at a cost-efficient manner.”

Let’s see.

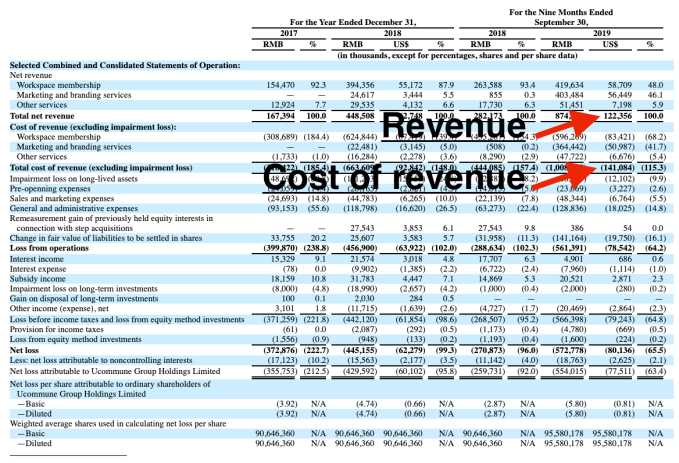

As a primer for all you non-accountants, here’s how you make money as a company: First, generate some revenue. Next, deduct the direct costs that that revenue engendered. What’s left is called “gross profit,” and the relative total of gross profit generated from revenue is called gross margin. From there, subtract your operating costs. If there’s anything left over, that’s operating profit. Now take your operating profit and remove taxes and other costs. What remains is net income.

As you can quickly see, the more gross profit a business generates from its revenue, the more money is has left over to pay for operating expenses. So, revenues that generate lots of gross profit — called high-margin revenue — are better than those that don’t.

Ucommune, our IPO hopeful, is unique in that its revenue doesn’t generate any gross profit at all. Its revenue doesn’t even pay for itself. The company is gross margin negative.

Here’s what that looks like:

If your cost of revenue is higher than your revenue, your gross profit is negative. And that means that you have no gross margin available to fund operating costs. In turn, that means that your company is super unprofitable.

Ucommune is unprofitable, unsurprisingly. (If it feels like we’re overly focused on gross margins, keep in mind that software companies are worth as much as they are in part because they have very high gross margins.)

Things get a bit worse when we look further.

Digging in, Ucommune operates two main businesses. The first enterprise is co-working, which generated just less than half of the company’s total revenue during the first three quarters of 2019. Its second largest business is a marketing effort. Ucommune acquired a company called “Shengguang Zhongshuo” in December of 2018, a deal that lets the company drive revenue by selling “branding services and online targeted marketing services.”

Ucommune is therefore a hybrid co-working and services business. Neither piece of the whole is attractive from a margin perspective. For example, the company’s $58.7 million in co-working revenue earned during the first nine months of 2019 was nearly entirely offset by lease costs ($49.6 million) alone, before the company staffed and otherwise managed the locations in question.

The company’s marketing business is slightly better. Its $56.5 million in revenue from the first three quarters of 2019 was nearly offset by $51.0 million in revenue costs. Ucommune’s services arm, therefore, was more lucrative in terms of generating gross margin for the co-working company than its actual co-working business.

(Bear in mind as we go along that this company wants to go public.)

Wrapping our discussion of yuck, let’s talk about cash. Ucommune had cash and equivalents of $23.4 million and short-term investments worth $11.0 million at the end of Q3 2019. That’s $33.4 million in total that the company can access, presuming that every short-term investment is unwindable into cash inside the window in which Ucommune would need to access it.

A window that is closing, mind. Ucommune’s operations burned through $32.4 million in the first three quarters of 2019. If the company kept consuming cash at its prior pace, we can estimate that it will not have enough cash to make it to the end of Q2 2020. Which is why Ucommune is going public.

The only counterargument to the mess that is Ucommune’s business is that it is growing quickly. That’s true. The company’s revenue grew from ¥282.2 million in the first three quarters of 2018 to ¥874.6 million over the same time period this year. That’s quick!

But instead of demonstrating operating leverage (losing less money as its revenue grew), the company lost more money this year than the last, making its business appear likely to keep burning acres of cash while it grows. And you have to ask yourself if it is a good business, why are its private investors pushing it onto the public markets instead of giving it more of their own money?

They must have known, landing this close to WeWork, how this was going to look. And that’s not confidence-inspiring.

Powered by WPeMatico

Airbnb has well and truly disrupted the world of travel accommodation, changing the conversation not just around how people discover and book places to stay, but what they expect when they get there, and what they expect to pay. Today, one of the startups riding that wave is announcing a significant round of funding to fuel its own contribution to the marketplace.

Domio, a startup that designs and then rents out apart-hotels with kitchens and other full-home experiences, has raised $100 million ($50 million in equity and $50 million in debt) to expand its business in the U.S. and globally to 25 markets by next year, up from 12 today. Its target customers are millennials traveling in groups or families swayed by the size and scope of the accommodation — typically five times bigger than the average hotel room — as well as the price, which is on average 25% cheaper than a hotel room.

The Series B, which actually closed in August of this year, was led by GGV Capital, with participation from Eldridge Industries, 3L Capital, Tribeca Venture Partners, SoftBank NY, Tenaya Capital and Upper90. Upper90 also led the debt round, which will be used to lease and set up new properties.

Domio is not disclosing its valuation, but Jay Roberts, the founder and CEO, said in an interview that it’s a “huge upround” and around 50x the valuation it had in its seed round and that the company has tripled its revenues in the last year. Prior to this, Domio had only raised around $17 million, according to data from PitchBook.

For some comparisons, Sonder — another company that rents out serviced apartments to the kind of travelers who have a taste for boutique hotels — earlier this year raised $225 million at a valuation north of $1 billion. Others like Guesty, which are building platforms for others to list and manage their apartments on platforms like Airbnb, recently raised $35 million with a valuation likely in the range of $180 million to $200 million. Airbnb is estimated to be valued around $31 billion.

Domio plays in an interesting corner of the market. For starters, it focuses its accommodations at many of the same demographics as Airbnb. But where Airbnb offers a veritable hodgepodge of rooms and homes — some are people’s homes, some are vacation places, some never had and never will have a private occupant, and across all those the range of quality varies wildly — Domio offers predictability and consistency with its (possibly more anodyne) inventory.

“We are competing with amateur hosts on Airbnb,” said Roberts, who previously worked in real estate investment banking. “This is the next step, a modern brand, the next Marriott but with a more tech-powered brain and operating model.” These are not to be confused with something like Hilton’s Homewood Suites, Roberts stressed to me. He referred to Homewood as “a soulless hotel chain.”

“Domio is the anti-hotel chain,” he added.

Roberts is also quick to describe how Domio is not a real estate company as much as it is a tech-powered business. For starters, it uses quant-style algorithms that it’s built in-house to identify regions where it wants to build out its business, basing it not just on what consumers are searching for, but also weather patterns, economic indicators and other factors. After identifying a city or other location, it works on securing properties.

It typically sets up its accommodations in newer or completely new buildings, where developers — at least up to now — are not usually constructing with short-term rentals in mind. Instead, they are considering an option like Domio as an alternative to selling as condominiums or apartments, something that might come up if they are sensing that there is a softening in the market. “We typically have 75%-78% occupancy,” Roberts said. He added that hotels on average have occupancy rates in the high 60% nationally.

As Domio lengthens its track record — its 12 U.S. markets include Miami, Los Angeles, Philadelphia and Phoenix — Roberts says that they’re getting a more select seat at the table in conversations.

“Investors are starting to go out to buy properties on our behalf and lease them to us,” he said. This gives the startup a much more favorable rate and terms on those deals. “The next step is that Domio will manage these directly.” The most recent property it signed, he noted, includes a Whole Foods at the ground level, and a gym.

Using technology to identify where to grow is not the only area where tech plays a role. Roberts said that the company is now working on an app — yet to be released — that will be the epicenter of how guests interact to book places and manage their experience once there.

“Everything you can do by speaking to a human in a traditional hotel you will be able to do with the Domio app,” he said. That will include ordering room service, getting more towels, booking experiences and getting restaurant recommendations. “You can book your Uber through the Domio app, or sync your Spotify account to play music in the apartment.

Ans there are plans to extend the retail experience using the app. Roberts says it will be a “shoppable” experience where, if you like a sofa or piece of art in the place where you’re staying, you can order it for your own home. You can even order the same wallpaper that’s been designed to decorate Domio apartments.

Although Airbnb has grown to be nearly as ubiquitous as hotels (and perhaps even more prominent, depending on who you are talking to), the wider travel and accommodation market is still ripe for the taking, estimated to reach $171 billion by 2023 and the highest growth sector in the travel industry.

“Airbnb has taught us that hotels are not the only place to stay,” said Hans Tung, GGV’s managing partner. “Domio is capitalizing on the global shift in short-term travel and the consumer demand for branded experiences. From my travels around the world, there is a large, underserved audience — millennials, families, business teams — who prefer the combined benefits of an apartment and hotel in a single branded experience.”

I mentioned to Roberts that the leasing model reminded me a little of WeWork, which itself does not own the property it curates and turns into office space for its tenants. (The SoftBank investor connection is interesting in that regard.) Roberts was very quick to say that it’s not the same kind of business, even if both are based around leased property re-rented out to tenants.

“One of the things we liked about Domio is that is very capital-efficient,” said Tung, “focusing on the model and payback period. The short-term nature of customer stays and the combination of experience/price required to maintain loyal customers are natural enforcers of efficient unit economics.”

“For GGV, Domio stands out in two ways,” he continued. “First, CEO Jay Roberts and the Domio team’s emphasis on execution is impressive, with expansion into 12 cities in just three years. They have the right combination of vision, speed and agility. Domio’s model can readily tap into the global opportunity as they have ambition to scale to new markets. The global travel and tourism spend is $2.8 trillion with 5 billion annual tourists. Global travelers like having the flexibility and convenience of both an apartment and hotel — with Domio they can have both.”

Powered by WPeMatico