Wefox

Auto Added by WPeMatico

Auto Added by WPeMatico

The U.S. insurance technology market is hot and has been for years now. Back in early 2020, to pick an example, TechCrunch reported on a wave of funding events among domestic insurtech marketplaces. Those companies have since gone on to raise hundreds of millions of dollars more.

And after a long period of incubation, we’ve seen neoinsurance players from the U.S. like Root and Metromile go public. Hippo is working to join the cohort.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

So from the perspective of venture capital activity, startup growth and exits, insurtech is proving itself in the States. Even if growth remains the name of the game in insurance tech and profits are often scarce.

What about other markets? The recent Wefox round caught The Exchange’s eye. A $650 million insurtech round would have commanded our attention regardless of its location. But to see a European insurance technology startup raise that amount of cash made us wonder if there’s as much money present for the EU market’s insurtech startups as we’ve seen here in the U.S.

After all, with business-focused neoinsurance provider Embroker raising a big round this week in the United States, to pick an example, it seems that attacking the massive and antiquated insurance market is good startup sport. Why wouldn’t that concept apply to Europe?

After all, with business-focused neoinsurance provider Embroker raising a big round this week in the United States, to pick an example, it seems that attacking the massive and antiquated insurance market is good startup sport. Why wouldn’t that concept apply to Europe?

To find out more, we got in touch with a number of VCs from Europe to hear their perspectives on what’s happening on the ground, including folks from Accel, Astorya.vc and Insurtech Gateway. To ground us, we collated the biggest recent rounds from the EU insurance technology market. Let’s go!

Venture capitalists and startup founders get paid when they generate an exit. Lately, exits in the space have featured a number of IPOs.

The older a startup gets, the more it has to deal with public-market investors. Crossover funds and the like make their appearance before unicorns go public. And then former startups have to pitch not the venture capital market, but the public markets. It’s a different game.

That’s the impression that The Exchange got chatting with the CEO of Root, Alex Timm, this earnings cycle. He noted that public tech-focused investors don’t always grok the insurance elements of his business, while insurance investors don’t always grok the tech side of Root.

Powered by WPeMatico

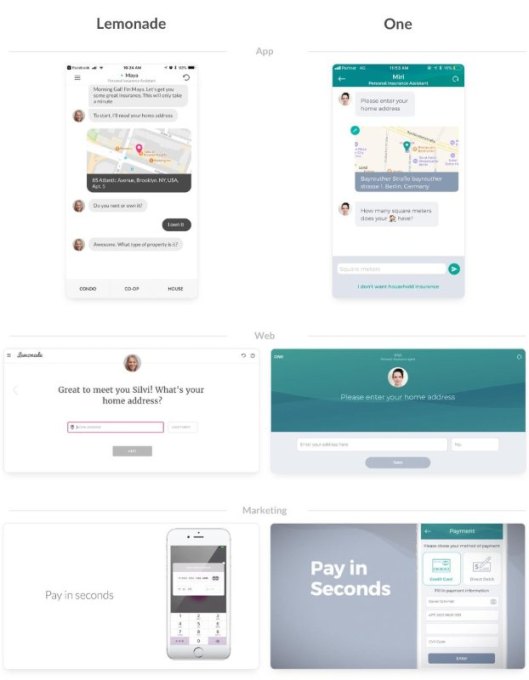

Lemonade, the insurance platform based out of NYC, has filed a lawsuit against German company ONE Insurance, its parent company wefox, and founder Julian Teicke.

The complaint, filed in the U.S. District Court Southern District of NY, alleges that wefox reverse engineered Lemonade to create ONE, infringing Lemonade’s intellectual property, violating the Computer Fraud and Abuse Act, and breaching its contractual obligations to Lemonade not to “copy content… to provide any service that is competitive…or to…create derivative works.”

In the filing (which you can see on Pacer or here), Lemonade alleges that Teicke repeatedly registered for insurance on Lemonade under various names and for various addresses, some of which do not exist. Teicke also allegedly filed claims in what appeared to be an attempt to assess and copy the arrangement of those flows.

Lemonade’s counsel says Teicke started seven claims over the course of 20 days, prompting Lemonade to cancel his policy.

Alongside Teicke, a number of other executives and members of leadership at wefox also filed fake claims, says the complaint, despite having opted in to Lemonade’s user agreement and taking an honesty pledge, which is required of all Lemonade users.

This, according to Lemonade, violates the Computer Fraud and Abuse act. Lemonade also alleges that the ONE app infringes Lemonade’s IP, and that in assessing the Lemonade app and building a competitor, Teicke also violated Lemonade’s TOS.

Lemonade has changed the insurance business in two key ways: First, it made the process of actually buying insurance as easy as a few clicks on your smartphone. Digitizing the process makes the issue of getting home or renters insurance far less daunting and more approachable to consumers. Secondly, Lemonade rethought the business model of insurance.

Normally, insurance providers charge you a certain monthly rate based on the value of the property/items looking to be insured. But at the end of the year, the money remaining in that policy becomes profit, putting the insurance company in direct opposition to the consumer any time a claim is filed.

Lemonade takes its profit directly out of each payment, and if a file isn’t claimed, it sends the rest of the leftover money to the charity of your choice, ensuring that Lemonade and the consumer are on the same page when a claim is filed.

In keeping with that thesis, any proceeds generated from this lawsuit will go directly to Code.org.

“We’re not trying to enrich ourselves by poking another startup,” said Lemonade CEO Daniel Schreiber . “We’re not anti-competition. We’re just saying ‘Play by the rules, play fair and square.’”

Update: A wefox spokesperson offered up the following statement:

At wefox Group, we have 160 talented people whose hard work has created a unique business that is challenging the status quo every day. These allegations have no merit and ultimately appear to be an attempt to disrupt our business rather than a serious dispute. Lemonade actually raised these questions with us nine months ago, and – as we explained at the time – the concerns are meritless and we further received no answer. We have not been served any paper from Lemonade: if we are, we intend to defend ourselves vigorously. This lawsuit appears to be an attempt to bait the media into covering a non-issue.

Powered by WPeMatico

Wefox, the insurance platform that enables customers, insurance brokers and insurance providers to transact and manage insurance products digitally, has acquired One, a fully digital and newly launched insurance provider.

Wefox, the insurance platform that enables customers, insurance brokers and insurance providers to transact and manage insurance products digitally, has acquired One, a fully digital and newly launched insurance provider.