washington DC

Auto Added by WPeMatico

Auto Added by WPeMatico

Micromobility startup Helbiz, which now operates across Europe and the USA, is merging with a special purpose acquisition company (SPAC) to become a publicly listed company, giving it a war chest to potentially roll-up smaller competitors in the space, as well as the resources to expand into “cloud” or “ghost” kitchens as part of a move into food delivery.

Helbiz intends to merge with GreenVision Acquisition Corp. (Nasdaq: GRNV) in the second quarter of 2021. The combined entity will be named Helbiz Inc. and will be listed on the Nasdaq Capital Market under the new ticker symbol, “HLBZ.”

The transaction includes $30 million PIPE anchored by institutional investors and approximately $80 million in net proceeds will be fed into Helbiz’s micromobility and advertising businesses, which have 2.7 million users.

Helbiz says the merged entity will have a valuation of $408 million, and by run Helbiz’s existing management under CEO Salvatore Palella.

Palella said: “Through this transaction, we’re committed to fulfilling our vision in revolutionizing transport by using micromobility to become a seamless last-mile solution.”

He further revealed to me that the company plans to establish “ghost kitchens” in Milan and Washington, DC later this year, with the aim of introducing a five-minute delivery time.

Helbiz has tried to differentiate itself from other players like Lime and Bird by offering e-scooters, e-bicycles and e-mopeds all on one platform.

Key to Helbiz’s offering is an integrated geofencing platform that tends to appeal to city authorities who don’t want scooters left in random places, as well as a swappable battery that enables easier charging of the devices. Its subscription service allows users to take unlimited 30-minute trips on its e-bikes and e-scooters every month.

In Europe the company currently operates a fleet of e-scooters and e-bicycles in Milan, Turin, Verona, Rome, Madrid and Belgrade, and in the U.S. it operates in Washington, DC, Alexandria, Arlington and Miami.

David Fu, chairman, and CEO of GreenVision, commented: “Helbiz has distinguished itself as the only company to offer e-scooters, e-bicycles, and e-mopeds all on one user-friendly platform… Helbiz has a proven and capital-light business model that combines hardware, software, and services with extensive customer relationships.”

Powered by WPeMatico

At the FAA’s 23rd Annual Commercial Commercial Space Transportation Conference in Washington, DC on Wednesday, a panel dedicated to the topic of trends in VC around space startups touched on public vs. private funding, the right kinds of space companies that should even be considering venture funding, and, perhaps most notably, the big L: Liquidity.

Moderator Tess Hatch, Vice President at Bessemer Venture Partners, addressed the topic in response to an audience question that noted while we’ve heard a lot about how much money will flow into space-related startups from the VC community, we haven’t actually et seen much in the way of liquidity events that prove out the validity of these investments.

“In 2008, a company called Skybox was created and a handful of years later Google acquired the company for $500 million,” Hatch said. “Every venture capitalist’s ears perked up and they thought ‘Hey, that’s pretty good ROI in a short amount of time – maybe the space thing is an investable area’ and then a ton of venture capital investments flooded into space startups, and all of these venture capitalists made one, or maybe two investments in the area. Since then, there have not been many — if any – liquidity events: Perhaps Virgin Galactic going public via the SPAC (special uprose vehicle) on the New York Stock Exchange late last year would be the second. So we’re still waiting; we’re still waiting for those exits, we are still waiting for companies to pave the path for the 400+ startups in the ecosystem to return our investment.”

Hatch added that she’s looking at a number of companies who have the potential to break this somewhat prolonged exit drought in 2020, including five who are either quite mature in terms of their development, naming SpaceX, Rocket Lab, Planet and Spire as all likely candidates to have some kind of liquidity event in 2020, with the mostly likely being an IPO.

Space as an industry was described to me recently as a ‘maturing’ startup market by Space Angels CEO Chad Anderson, by virtue of the distribution of activity in terms of the overall investment rounds in the sector. There is indeed a lot of activity with early stage companies and seed rounds, but the fact remains that there hasn’t been much in the way of exits, and it’s also worth pointing out that corporate VCs haven’t been as acquisitive in space as some of their consumer and enterprise technology counterparts.

The panel touched on a lot more apart from liquidity, which actually only came up towards the end of the discussion, which included panelists Astranis CEO and co-founder John Gedmark; Capella Space CEO and founder Payam Banazadeh and Rocket Lab VP of Global Commercial Launch Services Shane Fleming. Both Gedmark and Banazadeh addressed aspects of the risks and benefits of seeking VC as a space technology company.

“Not every space business is a venture-backable business,” said Banazadeh earlier in the conversation. “But there are a lot of space businesses that are specifically going after raising venture money, and that’s dangerous for everyone – because at the end of the day venture is looking at high risk, high return. The ‘high return’ comes from being able to get substantial amount of revenue in a market that’s big

enough for those revenues to be coming from. But if your idea is to go build, maybe, some very specific part in a satellite, then you have to make the case of why you’ll be able to make those returns for the investors, and in a lot of cases, that’s just not possible.”

Banazadeh also concedes that doing any kind of space technology development is expensive, and the money has to come from somewhere. Gedmark talked about one popular source, government funding and grants, and why that often isn’t as obviously a positive thing for startups as it might seem.

“Small government grants can be great, and obviously a fantastic source of non dilutive capital,” Gedmark said. “But there is a little bit of a trick there, or something to be aware of: I think people are often surprised how much time is spent in the early days of a startup refining the exact idea and the product, and if you’re not certain that you have the that product market fit […] then, the government grant can be extremely dangerous, because they will fund you to do something that is sort of similar to what to what you’re doing, but it really prevents you changing your approach later; you’re going to end up spending time executing on the specific project of the program manager on the government side and you’re executing on what they want.”

VC funds, on the other hand, come with the built-in expectation that you’re going to refine and potentially even change direction altogether, Gedmark says. Depending on the terms of the public funding you’re seeking, that flexibility may not be part of the arrangement, which ultimately could be more important than a bit of equity dilution.

Powered by WPeMatico

By the end of 2019, the global gaming market is estimated to be worth $152 billion, with 45% of that, $68.5 billion, coming directly from mobile games. With this tremendous growth (10.2% YoY to be precise) has come a flurry of investments and acquisitions, everyone wanting a cut of the pie. In fact, over the last 18 months, the global gaming industry has seen $9.6 billion in investments and if investments continue at this current pace, the amount of investment generated in 2018-19 will be higher than the eight previous years combined.

What’s interesting is why everyone is talking about games, and who in the market is responding to this — and how.

Today, mobile games account for 33% of all app downloads, 74% of consumer spend and 10% of all time spent in-app. It’s predicted that in 2019, 2.4 billion people will play mobile games around the world — that’s almost one-third of the global population. In fact, 50% of mobile app users play games, making this app category as popular as music apps like Spotify and Apple Music, and second only to social media and communications apps in terms of time spent.

In the U.S., time spent on mobile devices has also officially outpaced that of television — with users spending eight more minutes per day on their mobile devices. By 2021, this number is predicted to increase to more than 30 minutes. Apps are the new prime time, and games have grabbed the lion’s share.

Accessibility is the highest it’s ever been as barriers to entry are virtually non-existent. From casual games to the recent rise of the wildly popular hyper-casual genre of games that are quick to download, easy to play and lend themselves to being played in short sessions throughout the day, games are played by almost every demographic stratum of society. Today, the average age of a mobile gamer is 36.3 (compared with 27.7 in 2014), the gender split is 51% female, 49% male, and one-third of all gamers are between the ages of 36-50 — a far cry from the traditional stereotype of a “gamer.”

With these demographic, geographic and consumption sea-changes in the mobile ecosystem and entertainment landscape, it’s no surprise that the game space is getting increased attention and investment, not just from within the industry, but more recently from traditional financial markets and even governments. Let’s look at how the markets have responded to the rise of gaming.

Image courtesy of David Maung/Bloomberg via Getty Images

The first substantial investments in mobile gaming came from those who already had a stake in the industry. Tencent invested $90 million in Pocket Gems and$126 million in Glu Mobile (for a 14.6% stake), gaming powerhouse Supercell invested $5 million in mobile game studio Redemption Games, Boom Fantasy raised $2M million from ESPN and the MLB and Gamelynx raised $1.2 million from several investors — one of which was Riot Games. Most recently, Ubisoft acquired a 70% stake in Green Panda Games to bolster its foot in the hyper-casual gaming market.

Additionally, bigger gaming studios began to acquire smaller ones. Zynga bought Gram Games, Ubisoft acquired Ketchapp, Niantic purchased Seismic Games and Tencent bought Supercell (as well as a 40% stake in Epic Games). And the list goes on.

Beyond the flurry of investments and acquisitions from within the game industry, games are also generating huge amounts of revenue. Since launch, Pokémon GO has generated $2.3 billion in revenue and Fortnite has amassed some 250 million players. This is catching the attention of more traditional financial institutions, like private equity firms and VCs, which are now looking at a variety of investment options in gaming — not just of gaming studios, but all those who have a stake in or support the industry.

In May 2018, hyper-casual mobile gaming studio Voodoo announced a $200 million investment from Goldman Sachs’ private equity investment arm. For the first time ever, a mobile gaming studio attracted the attention of a venerable old financial institution. The explosion of the hyper-casual genre and the scale its titles are capable of achieving, together with the intensely iterative, data-driven business model afforded by the low production costs of games like this, were catching the attention of investors outside of the gaming world, looking for the next big growth opportunity.

The trend continued. In July 2018, private equity firm KKR bought a $400 million minority stake in AppLovin and now, exactly one year later, Blackstone announced their plan to acquire mobile ad-network Vungle for a reported $750 million. Not only is money going into gaming studios, but investments are being made into companies whose technology supports the mobile gaming space. Traditional investors are finally taking notice of the mobile gaming ecosystem as a whole and the explosive growth it has produced in recent years. This year alone mobile games are expected to generate $55 billion in revenue, so this new wave of investment interest should really come as no surprise.

A woman holds up her cell phone as she plays the Pokemon GO game in Lafayette Park in front of the White House in Washington, DC, July 12, 2016. (Photo: JIM WATSON/AFP/Getty Images)

Most recently, governments are realizing the potential and reach of the gaming industry and making their own investment moves. We’re seeing governments establish funds that support local gaming businesses — providing incentives for gaming studios to develop and retain their creatives, technology and employees locally — as well as programs that aim to attract foreign talent.

As uncertainty looms in England surrounding Brexit, France has jumped on the opportunity with “Join the Game.” They’re painting France as an international hub that is already home to many successful gaming studios, and they’re offering tax breaks and plenty of funding options — for everything from R&D to the production of community events. Their website even has an entire page dedicated to “getting settled in France,” in English, with a step-by-step guide on how game developers should prepare for their arrival.

The U.K. Department for International Trade used this year’s Game Developers Conference as a backdrop for the promotion of their games fund — calling the U.K. “one of the most flourishing game developing ecosystems in the world.” The U.K. Games Fund allows for both local and foreign-owned gaming companies with a presence in the U.K. to apply for tax breaks. And ever since France announced their fund, more and more people have begun encouraging the British government to expand their program, saying that the U.K. gaming ecosystem should be “retained and enhanced.” But, not only does the government take gaming seriously, the Queen does as well. In 2008, David Darling, the CEO of hyper-casual game studio Kwalee, was made a Commander of the Order of the British Empire (CBE) for his services to the games industry. CBE is the third-highest honor the Queen can bestow on a British citizen.

Over in Germany, and the government has allocated €50 million of its 2019 budget for the creation of a games fund. In Sweden, the Sweden Game Arena is a public-private partnership that helps students develop games using government-funded offices and equipment. It also links students and startups with established companies and investors. While these numbers dwarf the investment of more commercial or financial players, the sudden uptick in interest governments are paying to the game space indicate just how exciting and lucrative gaming has become.

The evolution of investment in the gaming space is indicative of the stratospheric growth, massive revenue, strong user engagement and extensive demographic and geographic reach of mobile gaming. With the global games industry projected to be worth a quarter of a trillion dollars by 2023, it comes as no surprise that the diverse players globally have finally realized its true potential and have embraced the gaming ecosystem as a whole.

Powered by WPeMatico

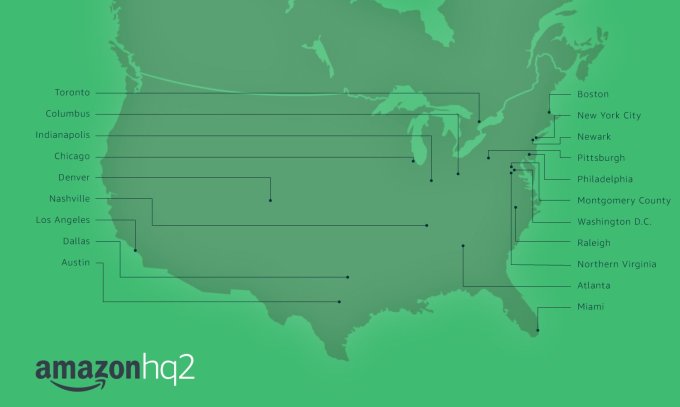

The big news today is that — finally — we have Amazon’s selection of cities for its dual second headquarters (Northern Virginia and NYC). Then some notes on China. But first, semiconductors and open sourcing analysis.

We are experimenting with new content forms at TechCrunch. This is a rough draft of something new — provide your feedback directly to the authors: Danny at danny@techcrunch.com or Arman at Arman.Tabatabai@techcrunch.com if you like or hate something here.

Last week, I focused on SoftBank’s debt and Form D filings by startups. On Friday, I asked what I should start to analyze next. There were several feedback hotspots, but the one that popped out to me was around next-generation chips and the battle for dominance at the hardware layer.

As a software engineer, I know almost nothing about silicon (the beauty of abstraction). But it is clear that the future of all kinds of workflows will increasingly be driven by capabilities at the hardware/silicon level, particularly in future applications like artificial intelligence, machine learning, AR/VR, autonomous driving and more. Furthermore, China and other countries are spending billions to go after the leaders in this space, such as Nvidia and Intel. Startups, funding, competition, geopolitics — we’ve got it all here.

Arman and I are now diving deeper into this space. We will start to post once we have some interesting things to share, but if you have ideas, opinions, companies or investments in this space: tell us about them, as we are all ears: danny@techcrunch.com and Arman.tabatabai@techcrunch.com.

Since I launched this daily “column” last week, I have included the text near the top that “We are experimenting with new content forms at TechCrunch.” One of those forms is what might be called open-source journalism. Definitions are fuzzy, but I take it to mean working “in the open” — allowing you, the audience of this column, to engage in not just feedback around finalized and published posts, but to actually affect the entire process of analysis, from sourcing and ideation to data science and writing.

I am thankful to work at a publication like TechCrunch where my readers are often working in the exact sectors that I am writing about. When I wrote about Form Ds last week, a number of startup attorneys reached out with their own thoughts and analysis, and also explained key aspects of how the law is changing around SEC disclosure for startups. That’s really powerful, and I want to apply it to as many fields as possible.

This thesis is ultimately intentional — now I have to operationalize it. There aren’t good tools (yet!) that I know of that allow for easy sharing of data and notes that don’t rely on a hacked-together set of Google Docs and GitHub. But I’m exploring the stack, and will publish more things publicly as we have them.

Amazon’s long process for selecting an HQ2 is finally over, and the official answer is two: Northern Virginia and NYC. Tons of words have been spilled about the search, and I am sure even more analysis will strike today about what put those two locations over the top.

To me, the key for mayors is to start using these reverse searches (where a company seeks a city and not vice versa) as leverage to actually get resources to fund infrastructure and other critical services.

This is a theme that I discussed about a year ago:

Take Boston’s bid for GE’s new headquarters. Yes, the city offered property tax rebates of about $25 million , but GE’s move also pushed the state to fund a variety of infrastructure improvements, including the Northern Avenue bridge and new bike lanes. That bridge adds a critical path for vehicles and pedestrians in Boston’s central business district, yet has gone unfunded for years.

Ideally, governments could debate, vote, and then fund these sorts of infrastructure projects and community improvements. The reality is that without a time-sensitive forcing function like a reverse RFP process, there is little hope that cities and states will make progress on these sorts of projects. The debates can literally go on forever in American democracy.

So if you are a mayor or economic planning official, use these processes as tools to get stuff done. Use the allure of new jobs and tax revenues to spur infrastructure spending and get a rezoning through a recalcitrant city council. Use that “prosperity bomb” to upgrade old parts of the urban landscape and prepare the city for the future. A healthier, more humane city can be just around the corner.

Take DC. The city has seen one of the best-run Metro systems deteriorate to abysmal levels over the past few years due to a complete dumpster fire of organizational design (the DC transit agency WMATA is funded by inconsistent revenue sources that ensure it will never be sustainable). Here is an opportunity to use Amazon’s announcement to get the tax framework and operations figured out to ensure that real estate, transportation and other critical urban infrastructure are designed effectively.

Timothy Allen/Getty Images

Talking about second headquarters, the technology industry clearly has separated into poles, one based around the United States and the other based around China. Two articles I read recently gave good insights of the benefits and challenges for China in this world.

The first is from Sam Byford writing at The Verge, who investigates the native OS options that Chinese consumers receive from companies like Xiaomi, Huawei, Oppo and others. The headline is much more shrill than the text, so don’t let that frighten you.

Byford provides an overview of the lineage of Chinese mobile OSes, and also notes that what might look like design gaffes in Western consumer eyes might be critical needs for Chinese buyers:

But what is true today is that not all Chinese phone software is bad. And when it is bad from a Western perspective, it’s often bad for very different reasons than the bad Android skins of the past. Yes, many of these phones make similar mistakes with overbearing UI decisions — hello, Huawei — and yes, it’s easy to mock some designs for their obvious thrall to iOS. But these are phones created in a very different context to Android devices as we’ve previously understood them.

The article is perhaps a tad long for what it is, but Byford’s key viewpoint should be repeated as a mantra by any person connected to the technology sector today: “The Chinese phone market is a spiraling behemoth of innovation and audacity, unlike anything we’ve ever seen. If you want to be on board with the already exciting hardware, it’s worth trying to understand the software.”

Of course, while China may be a huge country, its leading technology companies do want to globalize and expand their user bases outside of the Middle Kingdom’s borders. That may well be a challenging proposition.

Writing at Factor Daily, Shadma Shaikh dives into the failure of WeChat to break into the Indian market. The product lessons learned by WeChat’s owner Tencent could be applied to any Silicon Valley company — cultural knowledge and appropriate product design are key to entering overseas markets.

Shaikh gives a couple of examples:

Another design feature in the app allowed users to look up and send add-friend requests to WeChat users nearby. During initial onboarding when users were just checking app’s features, many would tap the “people nearby” feature, which would switch on location sharing by default – including with strangers. Once location sharing with strangers was switched on, it wasn’t very intuitive to turn it off.

“Women used to get a lot of unwarranted messages from men, which was a major turn off and many of them left the platform,” Gupta says. “China probably didn’t have this stalking problem.”

And

In China, where the internet was cheaper than in India in 2012, sending video files of, say, 4 MB was not a challenge. WhatsApp compresses a 5 MB photo to 40 kilobytes. WeChat did not compress the files and took many minutes and data to send and receive media files.

Internationalization will never be easy, but the lessons that Silicon Valley has slowly learned over the past two decades will need to be learned again by Chinese companies if they want to export their software to other countries.

Powered by WPeMatico

Women-focused co-working space The Wing has made its way to California, opening its first of two planned locations in the state this morning.

On Sansome Street in San Francisco’s Financial District, The Wing hopes to attract professional women able to shell out $215 per month for access to its 8,000-square-foot workspace, which is complete with conference rooms, a cafe, a library stocked with books on feminist theory, a lactation room and more.

In addition to its chic decor and feminist messaging, The Wing is also known for its programming. Headquartered in New York City, where the company operates three of its four existing spaces, The Wing has hosted events with former Secretary of State Hillary Clinton, actress Jennifer Lawrence and New York Senator Kirsten Gillibrand, to name a few. The San Francisco location will be no different.

A spokesperson for The Wing tells me they have a fully booked calendar of politics, tech, entertainment and lifestyle-focused events prepped for members. In the first month, San Francisco Mayor London Breed will stop by, as will Democratic House Minority Leader Nancy Pelosi and Oakland Mayor Libby Schaaf.

As a brand founded by women — Audrey Gelman and Lauren Kassan — and inspired by the women’s club movement of the 19th century, The Wing and its majority female staff very carefully and skillfully practice what they preach. In building their spaces, for example, they hire female architects to design and perfect the location. Their conference rooms are named for notable women. One, in particular, named for Dr. Christine Blasey Ford, stands out.

The dozens of art pieces scattered throughout The Wing are by female artists. The menu at The Wing’s cafe, which has a sign above it that reads “I’ll have what she’s having,” showcases women of the Bay Area’s food and beverage industries. Even the wines served at The Wing are made by female wine makers in California.

If there’s on thing about The Wing that stands out, it’s the startup’s attention to detail.

Founded in 2016, The Wing plans to open its next location, in West Hollywood, in early 2019.

The Wing is backed by venture capital firms NEA, Kleiner Perkins and BBG Ventures, as well as co-working unicorn WeWork. It has raised just over $40 million to date to expand its co-working spaces throughout the U.S. and beyond.

“The Wing answers a desire by women to connect with each other in an environment that aims to promote learning and camaraderie,” Forerunner Ventures’ Kirsten Green told TechCrunch. “It’s both a timely and timeless need. With so much focus on entrepreneurship and start-ups here in the Bay Area, The Wing offers the community that many independent women are looking for and can benefit from.”

Powered by WPeMatico