vroom

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here — and be sure to check out last week’s main ep that dug into Robinhood, Miami and a host of other topics.

This morning we had a pile of news to get through. Here’s the rundown:

Equity drops every Monday at 7:00 a.m. PST and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Today Jamf, a software company that helps other firms manage their Apple devices, raised its IPO price range.

The company had previously targeted a $17 to $19 per-share range. A new SEC filing from the firm today details a far higher $21 to $23 per-share IPO price interval.

Jamf still intends to sell up to 18.4 million shares in its debut, including 13.5 million in primary stock, 2.5 million shares from existing shareholders and an underwriter option worth 2.4 million shares. The whole whack at $21 to $23 per share would tally between $386.4 million and $423.2 million, though not all those funds would flow to the company.

At the low and high-end of its new IPO range, Jamf is worth between $2.44 billion and $2.68 billion, steep upgrades from its prior valuation range of $1.98 billion to $2.21 billion.

Jamf follows in the footsteps of recent IPOs like nCino, Vroom and others in seeing demand for its public offering allow its pricing to track higher the closer it gets to its public offering. Such demand from public-market investors indicates there is ample demand for debut shares in mid-2020, a fact that could spur other companies to the exit market.

Coinbase, Airbnb and DoorDash are three such companies that are expected to debut in the next year’s time, give or take a quarter or two.

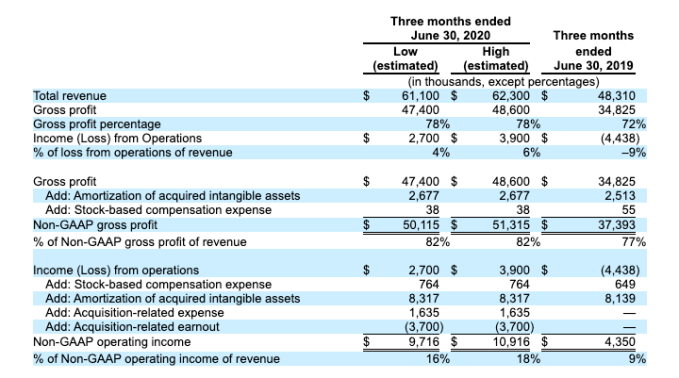

In anticipation of the Jamf debut that should come this week, let’s chat about the company’s recent performance.

Observe the following table from the most-recent Jamf S-1/A:

From even a quick glance we can learn much from this data. We can see that Jamf is growing, has improving gross margins and has managed to swing from an operating loss to operating profit in Q2 2020, compared to Q2 2019. And, for you fans out there of adjusted metrics, that Jamf managed to generate more non-GAAP operating income in its most recent period than the year-ago quarter.

In more precise terms:

Profits! Growth! Software! Improving margins! It’s not a huge surprise that Jamf managed to bolster its IPO price range.

Finally, for the SaaS-heads out there, the following:

This data lets us have a little fun. Recall that we have seen possible valuations for Jamf at IPO that started at $1.98 billion to $2.21 billion, and now include $2.44 billion and $2.68 billion? With our two ARR ranges for the end of Q2, we can now come up with eight ARR multiples for Jamf, from the low-end of its initial IPO price estimate, to the top-end of its new range.

Here they are:

From that perspective, the pricing changes feel a bit more modest, even if they work out to a huge spread on a valuation basis.

Regardless, this is the current state of the Jamf IPO. Rackspace also filed a new S-1/A today, but we can’t find anything useful in it. A bit like the Jamf S-1/A from Friday. Perhaps we’ll get a new Rackspace document soon with pricing notes.

And, of course, like the rest of the world we await the Palantir S-1 with bated breath. Consider that our white whale.

Powered by WPeMatico

In a move that highlights how open the American IPO window may be at the moment, China-based Agora priced its public offering at $20 per share last night, ahead of its $16 to $18 proposed price range. (Update: As noted here, the company has a second HQ in California.)

At $20 per share, the 17.5 million shares sold in its debut raised $350 million, a huge haul for a company that reported around 10% of that figure in Q1 2020 revenue. Provided that your humble servant is doing his Class A to ADS share conversion calculations correctly, Agora is worth about $2 billion at its IPO price.

Agora raised well over $100 million while a private company, backed by GGV Capital, Coatue and others, according to Crunchbase data.

The Exchange is a daily look at startups and the private markets for Extra Crunch subscribers; use code EXCHANGE to get full access and take 25% off your subscription.

Agora is an API-powered company that allows customers to embed real-time video and voice abilities in their applications; appropriately, the company’s ticker symbol in America will be “API.”

With an annual run rate of $142.2 million, a $2 billion valuation gives Agora a run-rate multiple of around 14x. That’s rich, but not stratospheric. Perhaps Agora wasn’t able to command a higher multiple due to its sub-70% margins (68.8% in Q1)?

With an annual run rate of $142.2 million, a $2 billion valuation gives Agora a run-rate multiple of around 14x. That’s rich, but not stratospheric. Perhaps Agora wasn’t able to command a higher multiple due to its sub-70% margins (68.8% in Q1)?

Agora’s financials make its IPO pricing a neat puzzle, so let’s pull apart the good and the bad to better understand why the market was willing to pay more than the company anticipated.

After that short exercise, we’ll make note of the current IPO climate, inclusive of what we learn from Agora. (Spoiler for unicorns out there: Things look good.)

We can’t calculate Agora’s enterprise value with confidence until we get updated filings. But taking into account the company’s pre-IPO cash and liabilities, its implied enterprise value/run rate is something around 13x. (That figure will dip if the company’s shares don’t rise after its debut, as its cash position rises from its share sale; more on enterprise values here.)

Powered by WPeMatico

Earlier today we took a look at two companies that have filed to go public, nCino and GoHealth. The pair join Lemonade in a march toward the public markets.

But those three firms are hardly alone. We know that DoorDash filed privately earlier this year (it also raised a pile of cash lately, so its IPO may not be in a hurry), and Postmates filed privately last year.

Even more, there are a number of companies whose IPOs we anticipate in short order. So, what follows is our incredibly scientific survey of impending IPOs, starting with those closest to the gate. This list is focused on companies that were at one point venture-backed startups, even if they have become behemoths in the intervening years.

We’ll start with companies that have filed and are moving toward debuts in the next few weeks:

And, next, companies that have filed privately but are still hanging back:

And here are companies that are making the sort of noise that one might make before finally going public:

All of the above is a jam, and I am stoked to dig through the S-1 trenches with you.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This time around we’re recording what we call an Equity Shot, a single-topic show that we pull together whenever there’s a news item of sufficient weight that it demands we break our regular cadence and record a little more.

So Danny and Tash and Alex got together to discuss the recent Vroom IPO and Lemonade filing to go public. These are topics that TechCrunch has covered quite a lot lately, so here’s a chronology to help you keep it all straight:

So you can catch up as you need to. What matters is that public investors have swooned over the Vroom IPO, pushing its pricing and, today, more than doubling its value as a public company. It’s a huge debut, and that bodes well for other gross-margin-light businesses — unicorns, even — that might want to go public.

The IPO window is pretty open, it appears. And best of all, we three disagreed quite a bit this week. It’s a fun show.

OK, that’s enough from us. We are back on Friday. Take care, and keep up the good fight.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Yesterday evening, Vroom, a digital used car retailer, priced its IPO at $22 per share, a figure that was a full $7 above the low end of its first proposed IPO price range. The venture-backed firm first proposed a $15 to $17 per-share IPO price range, which it later raised to $18 to $20 per share.

Pricing at $22 per share meant that there was strong demand for the company’s equity during its IPO process. Pricing strength doesn’t guarantee performance as a public company, but it does provide a proxy for investor interest.

TechCrunch has covered a few IPOs lately, noting along the way that some recent offerings have featured heavy financial backing and incredibly slim margins. Not profit margins, mind, those don’t exist for the firms we’re talking about — we’re discussing gross margins, the most basic element of corporate profitability.

Gross margins are part of why software companies are so valuable. Their incredibly strong gross margins make their revenues, and therefore their operations, attractive to investors; higher gross margins mean more money left over to cover expenses and redistribute to shareholders via dividends and buybacks. Lower gross margin businesses, in contrast, have less money once they are done paying for revenue costs, making it harder for those companies to cover operating costs, let alone give away leftover funds to their owners.

So it has been to our surprise that Kingsoft Cloud, Vroom, and, soon, Lemonade are seeing such strong responses. It’s perhaps even more surprising that these companies managed to raise as much private capital as they did in their youth, despite not sporting gross margins that track with what we expect from venture-backed, tech and tech-ish companies.

With markets at all-time highs — and thus comparable valuations contentedly stretched — it’s probably a great time to take low-margin, growth-y companies public. But that doesn’t mean the situation makes perfect financial sense.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

ZoomInfo went public yesterday. After pricing its IPO $1 ahead of its proposed range at $21 per share, the company closed its first day’s trading worth $34.00, up 61.9%, according to Yahoo Finance. Then the company gained another 5.2% in after-hours trading.

Whether you feel that this SaaS player was worth the revenue multiple its original, $8 billion valuation dictated — let alone that same multiple times 1.6x — the message from the offering was clear: the IPO window is open.

This is not news to a few companies looking to take advantage of today’s strong equity prices.

Used-car marketplace Vroom is looking to get its shares public before its Q2 numbers come out, despite a history of slim gross profit generation. The company hopes to go public for as much as $1.9 billion, a modest uptick from its final private valuations.

We’ll get another dose of data when Vroom does price — how much investors are willing to pay for slim-margin revenue will tell us a bit more than what we learned from ZoomInfo, which has far superior gross margins. Investors have already signaled that they are content to value high-margin software-ish revenues richly. Vroom is more of a question, but if it does price strongly we’ll know public investors are looking for any piece of growth they can find.

This brings us to the latest news: Amwell has confidentially filed to go public. Formerly known as American Well, CNBC reports that the venture-backed telehealth company has dramatically expanded its customer base:

Telemedicine has seen an uptick in recent months, as people in need of health services turned to phone calls and video chats so they could avoid exposure to COVID-19. The company told CNBC last month that it’s seen a 1,000% increase in visits due to coronavirus, and closer to 3,000% to 4,000% in some places.

Powered by WPeMatico