vista equity partners

Auto Added by WPeMatico

Auto Added by WPeMatico

Jamf, the Apple device management company, filed to go public today. Jamf might not be a household name, but the Minnesota company has been around since 2002 helping companies manage their Apple equipment.

In the early days, that was Apple computers. Later it expanded to also manage iPhones and iPads. The company launched at a time when most IT pros had few choices for managing Macs in a business setting.

Jamf changed that, and as Macs and other Apple devices grew in popularity inside organizations in the 2010s, the company’s offerings grew in demand. Notably, over the years Apple has helped Jamf and its rivals considerably, by building more sophisticated tooling at the operating system level to help manage Macs and other Apple devices inside organizations.

Jamf raised approximately $50 million of disclosed funding before being acquired by Vista Equity Partners in 2017 for $733.8 million, according to the S-1 filing. Today, the company kicks off the high-profile portion of its journey toward going public.

In a case of interesting timing, Jamf is filing to go public less than a week after Apple bought mobile device management startup Fleetsmith. At the time, Apple indicated that it would continue to partner with Jamf as before, but with its own growing set of internal tooling, which could at some point begin to compete more rigorously with the market leader.

Other companies in the space managing Apple devices besides Jamf and Fleetsmith include Addigy and Kandji. Other more general offerings in the mobile device management (MDM) space include MobileIron and VMware Airwatch among others.

Vista is a private equity shop with a specific thesis around buying out SaaS and other enterprise companies, growing them, and then exiting them onto the public markets or getting them acquired by strategic buyers. Examples include Ping Identity, which the firm bought in 2016 before taking it public last year, and Marketo, which Vista bought in 2016 for $1.8 billion and sold to Adobe last year for $4.8 billion, turning a tidy profit.

Now that we know where Jamf sits in the market, let’s talk about it from a purely financial perspective.

Jamf is a modern software company, meaning that it sells its digital services on a recurring basis. In the first quarter of 2020, for example, about 83% of its revenue came from subscription software. The rest was generated by services and software licenses.

Now that we know what type of company Jamf is, let’s explore its growth, profitability and cash generation. Once we understand those facets of its results, we’ll be able to understand what it might be worth and if its IPO appears to be on solid footing.

We’ll start with growth. In 2018 Jamf recorded $146.6 million in revenue, which grew to $204.0 million in 2019. That works out to an annual growth rate of 39.2%, a more than reasonable pace of growth for a company going public. It’s not super quick, mind, but it’s not slow either. More recently, the company grew 36.9% from $44.1 million in Q1 2019 to $60.4 million in revenue in Q1 2020. That’s a bit slower, but not too much slower.

Turning to profitability, we need to start with the company’s gross margins. Then we’ll talk about its net margins. And, finally, adjusted profits.

Gross margins help us understand how valuable a company’s revenue is. The higher the gross margins, the better. SaaS companies like Jamf tend to have gross margins of 70% or above. In Jamf’s own case, it posted gross margins of 75.1% in Q1 2020, and 72.5% in 2019. Jamf’s gross margins sit comfortably in the realm of SaaS results, and, perhaps even more importantly, are improving over time.

When all its expenses are accounted for, the picture is less rosy, and Jamf is unprofitable. The company’s net losses for 2018 and 2019 were similar, totaling $36.3 million and $32.6 million, respectively. Jamf’s net loss improved a little in Q1, falling from $9.0 million in 2019 to $8.3 million this year.

The company remains weighed down by debt, however, which cost it nearly $5 million in Q1 2020, and $21.4 million for all of 2019. According to the S-1, Jamf is sporting a debt-to-equity ratio of roughly 0.8, which may be a bit higher than your average public SaaS company, and is almost certainly a function of the company’s buyout by a private equity firm.

But the company’s adjusted profit metrics strip out debt costs, and under the heavily massaged adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) metric, Jamf’s history is only one of rising profitability. From $6.6 million in 2018 to $20.8 million in 2019, and from $4.3 million in Q1 2019 to $5.6 million in Q1 2020, with close to 10% adjusted operating profit margins through YE 2019.

It will be interesting to see how the company’s margins will be affected by COVID-19, with financials during the period still left blank in this initial version of the S-1. The Enterprise market in general has been reasonably resilient to the recent economic shock, and device management may actually perform above expectations, given the growing push for remote work.

Something notable about Jamf is that it has positive cash generation, even if in Q1 it tends to consume cash that is made up for in other quarters. In 2019, the firm posted $11.2 million in operational cash flow. That’s a good result, and better than 2018’s $9.4 million of operating cash generation. (The company’s investing cash flows have often run negative due to Jamf acquiring other companies, like ZuluDesk and Digita.)

With Jamf, we have a SaaS company that is growing reasonably well, has solid, improving margins, non-terrifying losses, growing adjusted profits and what looks like a reasonable cash flow perspective. But Jamf is cash poor, with just $22.7 million in cash and equivalents as of the end of Q1 2020 — some months ago now. At that time, the firm also had debts of $201.6 million.

Given the company’s worth, that debt figure is not terrifying. But the company’s thin cash balance makes it a good IPO candidate; going public will raise a chunk of change for the company, giving it more operating latitude and also possibly a chance to lower its debt load. Indeed Jamf notes that it intends to use part of its IPO raise to “to repay outstanding borrowings under our term loan facility…” Paying back debt at IPO is common in private equity buyouts.

Jamf’s march to the public markets adds its name to a growing list of companies. The market is already preparing to ingest Lemonade and Accolade this week, and there are rumors of more SaaS companies in the wings, just waiting to go public.

There’s a reasonable chance that as COVID-19 continues to run roughshod over the United States, the public markets eventually lose some momentum. But that isn’t stopping companies like Jamf from rolling the dice and taking a chance going public.

Powered by WPeMatico

As cybercrime continues to evolve and expand, a startup that is building a business focused on endpoint security has raised a big round of funding. SentinelOne — which provides a machine learning-based solution for monitoring and securing laptops, phones, containerised applications and the many other devices and services connected to a network — has picked up $200 million, a Series E round of funding that it says catapults its valuation to $1.1 billion.

The funding is notable not just for its size but for its velocity: it comes just eight months after SentinelOne announced a Series D of $120 million, which at the time valued the company around $500 million. In other words, the company has more than doubled its valuation in less than a year — a sign of the cybersecurity times.

This latest round is being led by Insight Partners, with Tiger Global Management, Qualcomm Ventures LLC, Vista Public Strategies of Vista Equity Partners, Third Point Ventures and other undisclosed previous investors all participating.

Tomer Weingarten, CEO and co-founder of the company, said in an interview that while this round gives SentinelOne the flexibility to remain in “startup” mode (privately funded) for some time — especially since it came so quickly on the heels of the previous large round — an IPO “would be the next logical step” for the company. “But we’re not in any rush,” he added. “We have one to two years of growth left as a private company.”

While cybercrime is proving to be a very expensive business (or very lucrative, I guess, depending on which side of the equation you sit on), it has also meant that the market for cybersecurity has significantly expanded.

Endpoint security, the area where SentinelOne concentrates its efforts, last year was estimated to be around an $8 billion market, and analysts project that it could be worth as much as $18.4 billion by 2024.

Driving it is the single biggest trend that has changed the world of work in the last decade. Everyone — whether a road warrior or a desk-based administrator or strategist, a contractor or full-time employee, a front-line sales assistant or back-end engineer or executive — is now connected to the company network, often with more than one device. And that’s before you consider the various other “endpoints” that might be connected to a network, including machines, containers and more. The result is a spaghetti of a problem. One survey from LogMeIn, disconcertingly, even found that some 30% of IT managers couldn’t identify just how many endpoints they managed.

“The proliferation of devices and the expanding network are the biggest issues today,” said Weingarten. “The landscape is expanding and it is getting very hard to monitor not just what your network looks like but what your attackers are looking for.”

This is where an AI-based solution like SentinelOne’s comes into play. The company has roots in the Israeli cyberintelligence community but is based out of Mountain View, and its platform is built around the idea of working automatically not just to detect endpoints and their vulnerabilities, but to apply behavioral models, and various modes of protection, detection and response in one go — in a product that it calls its Singularity Platform that works across the entire edge of the network.

“We are seeing more automated and real-time attacks that themselves are using more machine learning,” Weingarten said. “That translates to the fact that you need defence that moves in real time as with as much automation as possible.”

SentinelOne is by no means the only company working in the space of endpoint protection. Others in the space include Microsoft, CrowdStrike, Kaspersky, McAfee, Symantec and many others.

But nonetheless, its product has seen strong uptake to date. It currently has some 3,500 customers, including three of the biggest companies in the world, and “hundreds” from the global 2,000 enterprises, with what it says has been 113% year-on-year new bookings growth, revenue growth of 104% year-on-year and 150% growth year-on-year in transactions over $2 million. It has 500 employees today and plans to hire up to 700 by the end of this year.

One of the key differentiators is the focus on using AI, and using it at scale to help mitigate an increasingly complex threat landscape, to take endpoint security to the next level.

“Competition in the endpoint market has cleared with a select few exhibiting the necessary vision and technology to flourish in an increasingly volatile threat landscape,” said Teddie Wardi, managing director of Insight Partners, in a statement. “As evidenced by our ongoing financial commitment to SentinelOne along with the resources of Insight Onsite, our business strategy and ScaleUp division, we are confident that SentinelOne has an enormous opportunity to be a market leader in the cybersecurity space.”

Weingarten said that SentinelOne “gets approached every year” to be acquired, although he didn’t name any names. Nevertheless, that also points to the bigger consolidation trend that will be interesting to watch as the company grows. SentinelOne has never made an acquisition to date, but it’s hard to ignore that, as the company to expand its products and features, that it might tap into the wider market to bring in other kinds of technology into its stack.

“There are definitely a lot of security companies out there,” Weingarten noted. “Those that serve a very specific market are the targets for consolidation.”

Powered by WPeMatico

Acquia announced it has acquired customer data platform (CDP) startup AgilOne today. The companies did not disclose the purchase price.

CDPs are all the rage among customer experience vendors, as they provide a way to pull data from a variety of channels to build a more complete picture of the customer. The goal here is to deliver meaningful content to the customer based on what you know about them. Having a platform like this to draw upon makes it more likely that you will hit the target more accurately.

Acquia co-founder and CTO Dries Buytaert says he has been watching this space for the last year, and wanted to add this piece to the Acquia tool chest. “Adding a CDP like AgilOne to our existing platform will help our customers unify their data across various tools in their technology stack to drive better, more personal customer experiences,” he said.

In particular, he says he liked AgilOne because it used an intelligence layer while building the customer record. “What sets AgilOne apart from other CDPs are its machine learning capabilities, which intelligently segment customers and predict customer behaviors (such as when a customer is likely to purchase something). This allows for the creation and optimization of next-best action models to optimize offers and messages to customers on a 1:1 basis.”

Like most startup founders, AgilOne CEO Omer Artun sees this as an opportunity to grow his company, probably faster than he could have on his own. “Since AgilOne’s inception, our vision has been to give marketers the direct power to understand who their customers are and engage with them in a genuine way in order to boost profitability and create the omnichannel experiences that customers crave. Through this acquisition, Acquia will enable us to continue to deliver, and build upon, this vision,” he wrote in a blog post announcing the acquisition.

Tony Byrne, founder and principal analyst at the Real Story Group, has been watching the marketing automation space for some time, as well as the burgeoning CDP market. He sees this move as good for Acquia, but wonders how it will fit with other pieces in the Acquia stack. “This in theory allows them to support the unification of customer data across their suite,” Byrne told TechCrunch.

But he cautions that the company could struggle incorporating AgilOne into its platform. “The Marketing Automation platform they purchased targets mostly B2B. AgilOne is dialed in on B2C use cases and a fairly narrow set of vertical segments. It will take a lot of work to make it into a CDP that could adequately serve Acquia’s diverse customer base,” he said.

Acquia was acquired by Vista Equity Partners for $1 billion in September, and it tends to encourage its companies to be more acquisitive than they might have been on their own. “Vista has been supportive of our M&A strategy and believes strongly in AgilOne as a part of Acquia’s vision to redefine the customer experience stack,” Buytaert said.

AgilOne raised over $41 million, according to PitchBook data. Investors included Tenaya Capital, Sequoia Capital and Mayfield Fund. It had a post valuation of just over $115 million and was pegged as likely acquisition target by Pitchbook.

AgilOne customers will be happy to hear that Acquia plans to continue to sell it as a stand-alone product in addition to making it part of the Acquia Open Marketing Cloud.

Powered by WPeMatico

Acquia announced yesterday that Vista Equity Partners was going to buy a majority stake in the company worth a $1 billion. That would seem to be reason enough to sell the company. That’s a good amount a dough, but as co-founder and CTO Dries Buytaert told Extra Crunch, he’s also happy to be taking care of his early investors and his long-time, loyal employees who stuck by him all these years.

Vista is actually buying out early investors as part of the deal, while providing some liquidity for employee equity holders. “I feel proud that we are able to reward our employees, especially those that have been so loyal to the company and worked so hard for so many years. It makes me feel good that we can do that for our employees,” he said.

Powered by WPeMatico

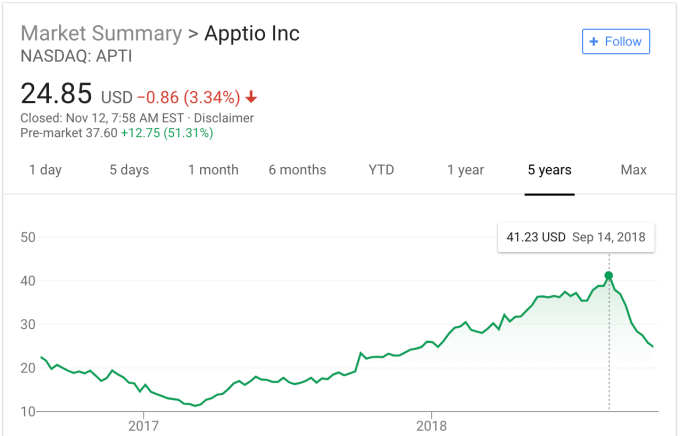

It seems that Sunday has become a popular day to announce large deals involving enterprise companies. IBM announced the $34 billion Red Hat deal two weeks ago. SAP announced its intent to buy Qualtrics for $8 billion last night, and Vista Equity Partners got into the act too, announcing a deal to buy Apptio for $1.94 billion, representing a 53 percent premium for stockholders.

Vista paid $38 per share for Apptio, a Seattle company that helps companies manage and understand their cloud spending inside a hybrid IT environment that has assets on-prem and in the cloud. The company was founded in 2007 right as the cloud was beginning to take off, and grew as the cloud did. It recognized that companies would have trouble understanding their cloud assets alongside on-prem ones. It turned out to be a company in the right place at the right time with the right idea.

Investors like Andreessen Horowitz, Greylock and Madrona certainly liked the concept, showering the company with $261 million before it went public in 2016. The stock price has been up and down since, peaking in August at $41.23 a share before dropping down to $24.85 on Friday. The $38 a share Vista paid comes close to the high-water mark for the stock.

Stock Chart: Google

Sunny Gupta, co-founder and CEO at Apptio, liked the idea of giving his shareholders a good return while providing a good landing spot to take his company private. Vista has a reputation for continuing to invest in the companies it acquires and that prospect clearly excited him. “Vista’s investment and deep expertise in growing world-class SaaS businesses and the flexibility we will have as a private company will help us accelerate our growth…,” Gupta said in a statement.

The deal was approved by Apptio’s board of directors, which will recommend shareholders accept it. With such a high premium, it’s hard to imagine them turning it down. If it passes all of the regulatory hurdles, the acquisition is expected to close in Q1 2019.

It’s worth noting that the company has a 30-day “go shop” provision, which would allow it to look for a better price. Given how hot the enterprise market is right now and how popular hybrid cloud tools are, it is possible it could find another buyer, but it could be hard to find one willing to pay such a high premium.

Vista clearly likes to buy enterprise tech companies, having snagged Ping Identity for $600 million and Marketo for $1.8 billion in 2016. It grabbed Jamf, an Apple enterprise device management company and Datto, a disaster recovery company last year. It turned Marketo around for $4.75 billion in a deal with Adobe just two months ago.

Powered by WPeMatico

A week ago rumors were flying that Adobe would be buying Marketo, and lo and behold it announced today that it was acquiring the marketing automation company for $4.75 billion.

It was a pretty nice return for Vista Equity partners, which purchased Marketo in May 2016 for $1.8 billion in cash. They held onto it for two years and hauled in a hefty $2.95 billion in profit.

We published a story last week, speculating that such a deal would make sense for Adobe, which just bought Magento in May for $1.6 billion. The deal gives Adobe a strong position in enterprise marketing as it competes with Salesforce, Microsoft, Oracle and SAP. Put together with Magento, it gives them marketing and ecommerce, and all it cost was over $6 billion to get there.

“The acquisition of Marketo widens Adobe’s lead in customer experience across B2C and B2B and puts Adobe Experience Cloud at the heart of all marketing,” Brad Rencher, executive vice president and general manager, Digital Experience at Adobe said in a statement.

Ray Wang, principal analyst and founder at Constellation Research sees it as a way for Adobe to compete harder with Salesforce in this space. “If Adobe takes a stand on Marketo, it means they are serious about B2B and furthering the Microsoft-Adobe vs Salesforce-Google battle ahead,” he told TechCrunch. He’s referring to the deepening relationships between these companies.

Brent Leary, senior analyst and founder at CRM Essentials agrees, seeing Microsoft as also getting positive results from this deal. “This is not only a big deal for Adobe, but another potential winner with this one is Microsoft due to the two companies growing partnership,” he said.

Adobe reported its earnings last Thursday announcing $2.29 billion for the third quarter, which represented a 24 percent year over year increase and a new record for the company. While Adobe is well on its way to being a $10 billion company, the majority of its income continues to come from Creative Cloud, which includes Photoshop, InDesign and Illustrator, among other Adobe software stalwarts.

But for a long time, the company has wanted to be much more than a creative software company. It’s wanted a piece of the enterprise marketing pie. Up until now, that part of the company, which includes marketing and analytics software, has lagged well behind the Creative Cloud business. In its last report, Digital Experience revenue, which is where Adobe counts this revenue represented $614 million of total revenue. While it continues to grow, up 21 percent year over year, there is much greater potential here for more.

Adobe had less than $5 billion in cash after the Magento acquisition, but it has seen its stock price rise dramatically in the last year rising from $149.96 last year at this time to $266.05 as of publication.

The acquisition comes as there is a lot of maneuvering going on this space and the various giant companies vie for market share. Today’s acquisition gives Adobe a huge boost and provides them with not only a missing piece, but Marketo’s base of 5000 customers and the opportunity to increase revenue in this part of their catalogue, while allowing them to compete harder inside the enterprise.

The deal is expected to close in Adobe’s 4th quarter. Marketo CEO Steve Lucas will join Adobe’s senior leadership team and report to Rencher.

It’s also worth noting that the announcement comes just days before Dreamforce, Salesforce’s massive customer conference will be taking place in San Francisco, and Microsoft will be holding its Ignite conference in Orlando. While the timing may be coincidental, it does end up stealing some of their competitors’ thunder.

Powered by WPeMatico

Adobe could be shopping for another piece of the digital marketing puzzle, as reports surfaced today that the company might be in talks with Vista Equity Partners to buy Marketo, a company the private equity firm purchased in May 2016 for $1.8 billion in cash. Reuters was first to report the rumor.

While the report states the talks are early, and nothing is imminent, and none of the companies involved would comment (understandably), it is a deal that makes sense for Adobe. The company has been trying to build out its digital marketing business for some time, including buying Magento in May for $1.8 billion to help beef up the ecommerce piece.

Assuming that Vista wants to flip Marketo for a profit, a good bet, it would likely need to come in at $2 billion at a minimum and probably more. There are only a few companies out there that could afford the price tag, who would be interested in a property like Marketo: Adobe, Salesforce, Microsoft, SAP and Oracle.

If Adobe really wanted to go for the digital marketing jugular, it could fork over the cash and buy Marketo. Brent Leary, who covers this industry as the principle at CRM Essentials, says this would be a way for Adobe to grab a chunk of enterprise marketing automation business at a time when the market is getting highly competitive.

“Marketo would give Adobe a leader in the marketing automation space at the enterprise customer level, particularly in the B2B space.” Leary explained.

While nothing is clear yet, Adobe has the resources if it wants to do it. The company currently has $6.3 billion in cash on hand, according to data on Yahoo finance, and has seen its stock price rise significantly in the last year from $156.24 to $269.58 (as of publication today).

Adobe Creative Cloud has always been the primary money maker for Adobe over the years, generating $1.3 billion in the last report (pdf) in June out of $2.2 billion in total revenue. Digital Experience, which includes marketing products, generated $586 million, and although it’s trending up, it has so much more potential.

We have been seeing more M&A action in this space as companies try to fill in various parts of the sale-service-marketing triumvirate. Just last week, we saw Zendesk, the company that concentrates on cloud customer service, enter the sales automation and CRM part of the space with the purchase of Base. Earlier this month, Thoma Bravo bought Apttus, a company which covers the quote-to-cash part of the sales cycle.

Adobe finds itself competing with other giant organizations with the previously mentioned companies all lining up for a piece of the digital marketing business. Getting Marketo certainly has the potential to help push that Digital Experience revenue line up further as the fight for marketshare gets ever more intense. Whether that happens remains to be seen, but Marketo is certainly a company that would match up well with Adobe if it wanted to make such a move.

It’s worth mentioning that Adobe will be reporting its latest earnings this afternoon.

Powered by WPeMatico

Ping Identity announced its first acquisition since being acquired by Vista Equity Partners in June for $600 million, grabbing Austin-based UnboundID for an undisclosed purchase price. The purchase, which Ping CEO Andre Durand says wouldn’t have been possible before the acquisition, expands his company’s mission beyond protecting pure business identity to customer identity and… Read More

Ping Identity announced its first acquisition since being acquired by Vista Equity Partners in June for $600 million, grabbing Austin-based UnboundID for an undisclosed purchase price. The purchase, which Ping CEO Andre Durand says wouldn’t have been possible before the acquisition, expands his company’s mission beyond protecting pure business identity to customer identity and… Read More

Powered by WPeMatico

When I walked into a conference room last Tuesday at the Cloud Identity Summit in New Orleans to interview Ping Identity CEO Andre Durand, it was my first chat with him since the company had been sold the week before for $600 million (as reported by The Information), a tidy exit for the 14 year old company.

When I walked into a conference room last Tuesday at the Cloud Identity Summit in New Orleans to interview Ping Identity CEO Andre Durand, it was my first chat with him since the company had been sold the week before for $600 million (as reported by The Information), a tidy exit for the 14 year old company.

I had questions, lots of questions. After all, in conversations with Durand and CFO… Read More

Powered by WPeMatico