Venture Capital

Auto Added by WPeMatico

Auto Added by WPeMatico

China’s technology scene has been in the news for all the wrong reasons in recent months. In the wake of the scuttling of Ant Group’s IPO, the Chinese government has gone on a regulatory offensive against a host of technology companies. Edtech got hit. On-demand companies took incoming fire. Ride-hailing? Check. Gaming? You bet.

The result of the government fusillade against some of the best-known companies in China was falling share prices. The damage topped $1 trillion among just public Chinese companies listed abroad.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

What about startups in sectors that were reformed overnight? If their public comps are any indication, even more wealth was deleted in the recent wave of crackdowns.

The Exchange was curious about the impact of the Chinese government’s actions on the venture capital market. The Chinese startup economy has produced a number of world-leading companies. Tencent and Alibaba, yes, and even Baidu have become well-known for a reason. Could regulatory changes shake up the venture model that helped grow the country’s largest tech concerns?

After we checked in on the same question this Monday, SoftBank provided a partial answer, noting yesterday that it is pausing investments in China. The Japanese teleco, conglomerate and investing powerhouse has been deploying capital at a rapid pace in recent weeks. That will slow, at least in China. Here’s the WSJ:

The regulatory initiative in China has become so unpredictable and widespread that SoftBank and its funds are planning to hold off on investing much more there until the risks become clearer, [SoftBank CEO Masayoshi Son] said at an earnings press conference in Tokyo.

Is SoftBank early to its decision to shake up its investing strategy, missing Chinese deals for some time? Or is it late? We secured data from PitchBook and Traxcn that paints a somewhat surprising picture of venture capital activity at least thus far in Q3 2021.

But first, a reminder of how well China’s venture capital market was performing as 2020 eased its way into 2021.

But first, a reminder of how well China’s venture capital market was performing as 2020 eased its way into 2021.

China had a reasonably good Q2 2021 despite the turmoil.

Sure, funding flowing into Chinese startups was down 18% compared to Q4 2020, per CB Insights, but that quarter had recorded an all-time high of $27.7 billion. With $22.8 billion raised, Q2 2021 still did better than every other quarter since Q2 2016 with the exception of Q2 2018, Q4 2020 and Q1 2021. Indeed, the ecosystem had started to cool down in late 2018 before picking up pace again at the end of 2020.

However, that’s only one way to look at the numbers. If you compare recent Chinese venture results with other regions, it underperformed. During Q2 2021, U.S. funding reached a new high of $70.4 billion, with places like Latin America, Canada and India also establishing new records.

This also means that China lost ground as to its share of global startup deal-making, and the same goes for unicorn creation. According to Tech Buzz China’s summary of CB Insights data, the U.S. accounted for 132 unicorn births between January 1 and June 16, 2021, compared with just three in China.

Slightly falling quarterly venture capital totals and a notable decline in unicorn formation does not a startup winter make. So let’s look at what’s happened more recently.

The thesis that there would be an instantly obvious slowdown in Chinese venture capital activity is not supported by the data we secured.

Powered by WPeMatico

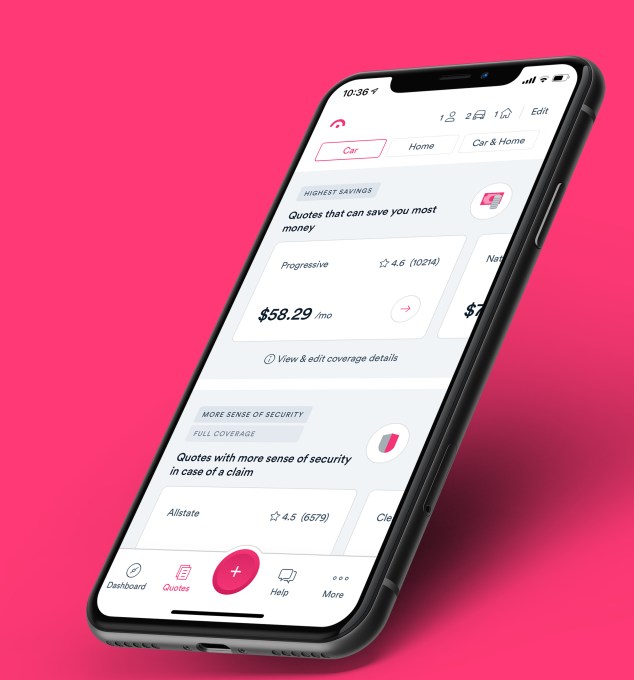

Just months after raising $28 million, Jerry announced today that it has raised $75 million in a Series C round that values the company at $450 million.

Existing backer Goodwater Capital doubled down on its investment in Jerry, leading the “oversubscribed” round. Bow Capital, Kamerra, Highland Capital Partners and Park West Asset Management also participated in the financing, which brings Jerry’s total raised to $132 million since its 2017 inception. Goodwater Capital also led the startup’s Series B earlier this year. Jerry’s new valuation is about “4x” that of the company at its Series B round, according to co-founder and CEO Art Agrawal.

“What factored into the current valuation is our annual recurring revenue, growing customer base and total addressable market,” he told TechCrunch, declining to be more specific about ARR other than to say it is growing “at a very fast rate.” He also said the company “continues to meet and exceed growth and revenue targets” with its first product, a service for comparing and buying car insurance. At the time of the company’s last raise, Agrawal said Jerry saw its revenue surge by “10x” in 2020 compared to 2019.

Jerry, which says it has evolved its model to a mobile-first car ownership “super app,” aims to save its customers time and money on car expenses. The Palo Alto-based startup launched its car insurance comparison service using artificial intelligence and machine learning in January 2019. It has quietly since amassed nearly 1 million customers across the United States as a licensed insurance broker.

“Today as a consumer, you have to go to multiple different places to deal with different things,” Agrawal said at the time of the company’s last raise. “Jerry is out to change that.”

The new funding round fuels the launch of the company’s “compare-and-buy” marketplaces in new verticals, including financing, repair, warranties, parking, maintenance and “additional money-saving services.” Although Jerry also offers a similar product for home insurance, its focus is on car ownership.

Image Credits: Jerry

“Access to reliable and affordable transportation is critical to economic empowerment,” said Rafi Syed, Jerry board member and general partner at Bow Capital, which also doubled down on its investment in the company. “Jerry is helping car owners make the most of every dollar they earn. While we see Jerry as an excellent technology investment showcasing the power of data in financial services, it’s also a high-performing investment in terms of the financial inclusion it supports.”

Goodwater Capital Partner Chi-Hua Chien said the firm’s recurring revenue model makes it stand out from lead generation-based car insurance comparison sites.

CEO Agrawal agrees, noting that Jerry’s high-performing annual recurring revenue model has made the company “attractive to investors” in addition to the fact that the startup “straddles” the auto, e-commerce, fintech and insurtech industries.

“We recognized those investment opportunities could drive our business faster and led to raising the round earlier than expected,” he told TechCrunch. “We’re eager to launch new categories to save customers time and money on auto expenses and the new investment shortens our time to market.”

Agrawal also believes Jerry is different from other auto-related marketplaces out there in that it aims to help consumers with various aspects of car ownership (from repair to maintenance to insurance to warranties), rather than just one. The company also believes it is set apart from competitors in that it doesn’t refer a consumer to an insurance carrier’s site so that they still have to do the work of signing up with them separately, for example. Rather, Jerry uses automation to give consumers customized quotes from more than 45 insurance carriers “in 45 seconds.” The consumers can then sign on to the new carrier via Jerry, which can then cancel former policies on their behalf.

Jerry makes recurring revenue from earning a percentage of the premium when a consumer purchases a policy on its site from carriers such as Progressive.

Powered by WPeMatico

Trendyol, an e-commerce platform based in Turkey, has raised $1.5 billion in a massive funding round that values the company at $16.5 billion. General Atlantic, SoftBank Vision Fund 2, Princeville Capital and sovereign wealth funds, ADQ (UAE) and Qatar Investment Authority co-led the round.

The deal marks SoftBank’s first in the country.

The new financing also makes Trendyol Turkey’s first decacorn, and among the highest-valued private tech companies in Europe. It comes just months after strategic — and majority — backer Alibaba invested $350 million in the company at a $9.4 billion valuation.

Founded in 2010, Trendyol ranks as Turkey’s largest e-commerce company, serving more than 30 million shoppers and delivering more than 1 million packages per day. It claims to have evolved from marketplace to “superapp” by combining its marketplace platform (which is powered by Trendyol Express, its own last-mile delivery solution) with instant grocery and food delivery through its own courier network (Trendyol Go), its digital wallet (Trendyol Pay), consumer-to-consumer channel (Dolap) and other services.

Image Credits: Founder Demet Mutlu / Trendyol

Trendyol founder Demet Suzan Mutlu said the new capital will go toward expansion within Turkey and globally. Specifically, the company plans to continue investing in nationwide infrastructure, technology and logistics and toward accelerating digitalization of Turkish SMEs. She said the company was founded to create positive impact and that it intends to continue on that mission.

Evren Ucok, Trendyol’s chairman, added that part of the company’s goal is to create new export channels for Turkish merchants and manufacturers.

Melis Kahya Akar, managing director and head of consumer for EMEA at General Atlantic, said that Trendyol’s marketplace model — ranging from grocery delivery to mobile wallets — “brings convenience and ease to consumers” in Turkey and internationally.

“Turkey is one of the fastest growing economies in the world and benefits from attractive demographics, with a young population that is very active online,” wrote General Atlantic’s Kahya Akar via e-mail. “We expect its already sizable e-commerce market –$17 billion in 2020 – to continue to grow meaningfully on the back of growing online penetration. We think Trendyol is ideally positioned to meet the needs of consumers in Turkey and around the world as the company expands.”

A 2020 report by JPMorgan found that e-commerce represented only 5.3% of the overall Turkish retail market at the time but that Turkish e-commerce had notched impressive leaps in revenues in recent years: 2018 alone saw the market jump by 42%, followed by 31% in 2019. As of 2020, 67% of the Turkish population were making purchases online.

Powered by WPeMatico

We’ve all been there. (Or at least I have.)

You’re getting ready to vacate a property you’ve rented, only to be told by the landlord that you won’t be getting your security deposit back.

This happened to me the first time I ever rented a place in the late 90s. I was shocked, but more than anything, I was angry at the injustice because I knew that what the landlord claimed was not true. It was her word against mine and my roommate’s. Still, we took her to small claims court, not so much over the $800 she was trying to keep but more to prove her wrong. In the end, we won.

But it was a lot of work, and a lot of time spent. If only there was some kind of technology available to have helped us make our case.

Well, today there is. RentCheck, a startup that is out to help solve the “he said, she said” challenge in these situations with an automated property inspection platform, has recently raised $2.6 million in seed money.

Lydia Winkler and Marco Nelson started the company in mid-2019 after Winkler experienced a similar situation to mine and ended up suing her landlord in small claims court. She was working on getting her JD/MBA at Tulane University at the time.

“It was an injustice for me not to pursue it,” she told TechCrunch. “I took meticulous photos of the move-out condition of my apartment. The process took 18 months. But not everyone has the time or knowledge to fight in court.”

She then met Nelson, who had bought several properties that he ended up renting out. He had issues with security deposits too, but the opposite ones. He had to settle disputes over deposits, and found himself documenting properties’ condition at the time of move-out.

“I met Lydia and we realized we were passionate about the same problem,” Nelson recalled.

And so New Orleans-based RentCheck was born.

Image Credits: RentCheck; Co-founders Marco Nelson and Lydia Winkler

There are an estimated 48 million rental units in the U.S., with an average deposit of $1,000.

“A good chunk of that is being fought after on aggregate,” Winkler said. “And so many need that money to put down a deposit on another unit.”

To address the problem, RentCheck built a web app for property managers that they believe also benefits tenants. The company’s digital platform works by providing a way for property managers to facilitate and conduct remote, guided property inspections. For obvious reasons, the company saw increased demand upon the onset of the COVID-19 pandemic, considering that the platform was automated and contactless. It saw 1,000% — mostly organic — growth in terms of the number of properties on the platform.

“What we do is, using a guided inspection process, prompt users and guide them room by room, telling them exactly what to take photos of so that floors, ceilings, windows and walls are all accounted for,” Winkler said.

Everything is done within the app so that users can’t upload photos that were previously on their camera roll “to ensure the integrity of the inspection” and that everything is time stamped. Once the inspection is complete, whoever does it signs off on it that they completed it accurately and honestly. Then the property manager can also sign off on it so both parties can agree on the move-out condition.

The company operates as a SaaS business, and charges property management companies a subscription fee based on the number of properties that they have on the RentCheck platform. They can then conduct “as many inspections as they want,” Nelson says, “whether the residents are doing them, their internal teams are doing them, or a third-party vendor, or a hybrid of the three.”

Image Credits: RentCheck/Bryce Ell Photography

The startup has attracted some large-name investors since its inception, first catching the attention of James “Jim” Coulter, the founder of TPG Capital, when the company won New Orleans Entrepreneurship Week. Coulter subsequently became one of the company’s first investors in its $1 million pre-seed round.

The company’s seed round included participation from Cox Enterprises, for its operations in the multifamily housing space, and angels such as Jim Payne, who previously sold MoPub to Twitter, and MAX to AppLovin; Ken Goldman, the former CFO of Yahoo, and who currently runs Hillspire, Eric and Wendy Schmidt’s family office; Mark Zaleski and John Kuolt of BCG Digital Ventures, and Brian Long, the founder of Attentive, who previously sold TapCommerce to Twitter. It also included institutional investors such as Irongrey, Context Ventures and Techstars.

“What we love about RentCheck is that it’s using very clever technology to automate and solve arguably the industry’s biggest problem in terms of money and time for both property managers and tenants,” said Kuolt, former managing director at BCG Digital Ventures and an early RentCheck investor. “The deposit deduction issue needs a technology-based solution, and almost everyone, at some time, has felt like they’ve been screwed over on their deposit by a landlord. When you see and use RentCheck’s solution, it makes you think: ‘Why didn’t I think of this?’ ”

Powered by WPeMatico

Assembling a startup team is harder than assembling 10 IKEA dressers, and the stakes are much, much higher.

Starting with the assumption that 90% of startups will fail and the most successful ones take an average of six years to IPO, founders must make careful decisions about whom they invite to join the core team.

Will that stellar engineer become a great CTO? Should your product person be opinionated or a team player? Are you even the best choice for CEO?

ThoughtSpot CEO Sudheesh Nair shared some of his thoughts about building a sturdy leadership team and drafted a thorough checklist for entrepreneurs who are putting a crew together. His initial advice?

“Investors love founder-CEOs, and founders are often fantastic candidates for this role. But not everyone can do it well, and more importantly, not everyone wants to.”

In a related article, Gregg Adkin, VP and managing director at Dell Technologies Capital, shared the framework he’s developed for helping founders set up their board.

Choosing the right mix of people can impact everything from fundraising to hiring: “Investors often ask founders about their board [because] it says a lot about their character, their judgment and their willingness to be challenged,” he writes.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Miranda Halpern spoke to Amsterdam-based coach Ward van Gasteren for our latest growth marketing interview, which is free to read.

In their discussion, van Gasteren addressed misconceptions about growth hacking, the mistakes most startups are likely to make, and the distinctions he draws between growth hacking and growth marketing:

“Growth hacking is great to kickstart growth, test new opportunities and see what tactics work,” he tells us.

“Marketers should be there to continue where the growth hackers left off: Build out those strategies, maintain customer engagement, and keep tactics fresh and relevant.”

Thanks very much for reading Extra Crunch this week; I hope you have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

Image Credits: sureeporn / Getty Images

In his first column since returning to TechCrunch, reporter Ryan Lawler considered the potential ripples Square’s purchase of Afterpay may send across the pond of buy now, pay later startups.

For commentary and perspective, he interviewed:

The investors he spoke to agreed that deferring payments helps drive e-commerce, “but scale matters and long-term margins look slim for BNPL startups,” reports Ryan.

Image Credits: Ivan Bajic (opens in a new window) / Getty Images

Businesses have been deploying AI solutions for 20 years, but few have achieved the outstanding gains in efficiency and profitability promised when the technology first appeared.

But there’s a burgeoning new generation of enterprise AI, Eshwar Belani, an operating partner at Symphony AI, writes in a guest column.

“Companies on the leading edge of AI innovation have advanced to the next generation, which will define the coming decade of big data, analytics and automation — Enterprise AI 2.0.”

Image Credits: Joan Cros Garcia-Corbis (opens in a new window) / Getty Images

Over the next 18 months, one technologist says the increased adoption of embodied artificial intelligence will open a path to superintelligence — incredibly powerful software that dwarfs anything the human mind could produce.

“All the crazy Boston Dynamics videos of robots jumping, dancing, balancing and running are examples of embodied AI,” says Chris Nicholson, founder and CEO of Pathmind, which uses deep reinforcement learning to optimize industrial operations and supply chains.

“The field is moving fast and, in this revolution, you can dance.”

Image Credits: Nigel Sussman (opens in a new window)

The Exchange looks at the valuations of public insurtech companies and considers what that means for startups — but from a slightly different perspective.

“We’d typically riff on the new values of public neoinsurance companies and use that data to work our way into a guess concerning what the price declines might mean for related startups,” Alex Wilhelm writes. “Taking public-market data and using it to better understand private markets is pretty much the national pastime of this column.

“Not today.”

Image Credits: Anastassiia (opens in a new window) / Getty Images

The fact that the globe is awash in venture capital should not be news to readers of this newsletter.

For founders, it means more than just fat checks, Kunal Lunawat, the co-founder and managing partner of Agya Ventures, writes in a guest column.

“Founders would be well served to go back to the basics and focus on the principles of fundraising when determining who sits on their cap table.”

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm checks in on results from Starling Bank and Monzo to see what the neobanks’ most recent financial figures say about the state of neobanks overall.

“Although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black,” he notes.

But among those that are?

“At least a portion of the neobanking world is financially stable enough to consider public offerings.”

Image Credits: MicroStockHub (opens in a new window)/ Getty Images

The red-hot venture capital market may give founders lots of investors to choose from, but the most important thing (if you can be choosy) is being able to trust and rely on your investors, Ripple Ventures’ Matt Cohen and True’s Tony Conrad write in a guest column.

“This … new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table,” they write.

“It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.”

Image Credits: A-Digit (opens in a new window) / Getty Images

Assembling a board of directors is not merely about finding individuals who can aid your early-stage journey, Gregg Adkin, the vice president and managing director at Dell Technologies Capital, writes in a guest column.

The composition of the board can also impact your fundraising.

“Investors often ask founders about their board [because] it says a lot about their character, their judgment and their willingness to be challenged,” he writes.

Adkins offers a framework he calls “SPIFS” — for strategy, people, image, finance and systems for compliance — to aid founders in setting up a board.

Image Credits: Nigel Sussman (opens in a new window)

In the wake of Deliveroo’s plans to abandon the Spanish market after the country passed legislation requiring companies dependent on gig workers to hire employees, Alex Wilhelm wondered about the battle for smaller markets and whether third place is sufficient.

“One company exiting a market is not a big deal, but we were curious about Deliveroo’s comments regarding the need for market leadership — or something close to it — to warrant continued investment,” he writes for The Exchange.

“Is this the common reality for startups battling for market position, no matter if those markets are cities or countries?”

Powered by WPeMatico

Venture capitalists are chatting this week about a recent piece from The Information titled “The End of Venture Capital as We Know It.” As with nearly everything you read, the article in question is a bit more nuanced than its headline. Its author, Sam Lessin, makes some pretty good points. But I don’t fully agree with his conclusions, and want to talk about why.

This will be fun, and, because it’s Friday, both relaxed and cordial. (For fun, here’s a long-ass podcast I participated in with Lessin last year.)

Lessin notes that venture capitalists once made risky wagers on companies that often withered away. Higher-than-average investment risk meant that returns from winning bets had to be very lucrative, or else the venture model would have failed.

Thus, venture capitalists sold their capital dearly to founders. The prices that venture capitalists have historically paid for startup equity in high-growth tech upstarts make IPO pops appear de minimis; it’s the VCs who make out like bandits when a tech company floats, not the bankers. The Wall Street crew just gets a final lap at the milk saucer.

Over time, however, things changed. Founders could lean on AWS instead of having to spend equity capital on server racks and colocation. The process of building software and taking it to market became better understood by more people.

Even more, recurring fees overtook the traditional method of selling software for a one-time price. This made the revenues of software companies less like those of video game companies, driven by episodic releases and dependent on the market’s reception of the next version of any particular product.

As SaaS took over, software revenues kept their lucrative gross margin profile but became both longer-lasting and more dependable. They got better. And easier to forecast to boot.

So, prices went up for software companies — public and private.

Another result of the revolution in both software construction and distribution — higher-level programming languages, smartphones, app stores, SaaS and, today, on-demand pricing coupled to API delivery — was that more money could pile into the companies busy writing code. Lower risk meant that other forms of capital found startup investing — super-late stage to begin with, but increasingly earlier in the startup lifecycle — not just possible, but rather attractive.

With more capital varieties taking interest in private tech companies thanks in part to reduced risk, pricing changed. Or, as Lessin puts it, thanks to better market ability to metricize startup opportunity and risk, “investors across the board [now] price [startups] more or less the same way.”

You can see where this is going: If that’s the case, then the model of selling expensive capital for huge upside becomes a bit soggy. If there is less risk, then venture capitalists can’t charge as much for their capital. Their return profile might change, with cheaper and more plentiful money chasing deals, leading to higher prices and lower returns.

The result of all of the above is Lessin’s lede: “All signs seem to indicate that by 2022, for the first time, nontraditional tech investors — including hedge funds, mutual funds and the like — will invest more in private tech companies than traditional Silicon Valley-style venture capitalists will.”

Capital crowding into the parts of finance once reserved for the high priests of venture means that the VCs of the world are finding themselves often fighting for deals with all sorts of new, and wealthier, players.

The result of this, per Lessin, is that venture “firms that grew up around software and internet investing and consider themselves venture capitalists” must “enter the bigger pond as a fairly small fish, or go find another small pond.”

The obvious critique of Lessin’s argument is one that he makes himself, namely that what he is discussing is not as relevant to seed investing. As Lessin puts it, his argument’s impact on seed investing is “far less clear.”

Agreed. Sure, it’s the end of venture capital as we know it. But it’s not the end of venture capital, because if capitalism is going to continue, there’s always going to need to be risky-ass shit for VCs to bet on at the bottom.

The factors that made later-stage SaaS investing something that even idiots can make a few dollars doing become scarce the earlier one looks in the startup world. Investing in areas other than software compounds this effect; if you try to treat biotech startups as less risky than before simply because public clouds exist, you are going to fuck up.

So the Lessin argument matters less in seed-stage and earlier investing than it does in the later stages of startup backing, and doubly less when it comes to earlier investing in non-software companies.

While it’s a little-known fact, some venture capitalists still invest in startups that are not software-focused. Sure, nearly every startup involves code, but you can make a lot of money in a lot of ways by building startups, especially tech startups. The figuring-out of SaaS investing does not mean that investing in marketplaces, for example, has enjoyed a similar decline in risk.

So, the VCs-are-dead concept is less true for seed and non-software startups.

Is Lessin correct, then, that the game really has changed for middle- and late-stage software investing? Of course it has, but I think that he takes the concept of less risky, private-market software investing in the wrong direction.

First, even if private-market investing in software has a lower risk profile than before, it’s not zero. Many software startups will fail or stall out and sell for a modest sum at best. As many in today’s market as before? Probably not, but still some.

This means that the act of picking still matters; we can vamp as long as we’d like about how venture capitalists are going to have to pay more competitive prices for deals, but VCs could retain an edge in startup selection. This can limit downside, but may also do quite a lot more.

Anshu Sharma of Skyflow — and formerly of Salesforce and Storm Ventures, where I first met him — made an argument about this particular point earlier this week with which I am sympathetic.

Sharma thinks, and I agree, that venture winners are getting bigger. Recall that a billion-dollar private company was once a rare thing. Now they are built daily. And the biggest software companies aren’t worth the few hundred billion dollars that Microsoft was largely valued at between 1998 and 2019. Today they are worth several trillion dollars.

More simply, a more attractive software market in terms of risk and value creation means that outliers are even more outlier-y than before. This means that venture capitalists that pick well, and, yes, go earlier than they once did, can still generate bonkers returns. Perhaps even more so than before.

This is what I am hearing about certain funds regarding their present-day performance. If Lessin’s point held up as strongly as he states it, I reckon that we’d see declining rates of return at top VCs. We’re not, at least based on what I am hearing. (Feel free to tell me if I am wrong.)

So yes, venture capital is changing, and the larger funds really are looking more and more like entirely different sorts of capital managers than the VCs of yore. Capitalism is happening to venture capital, changing it as the world of money itself evolves. Services were one way that VCs tried to differentiate from one another, and probably from non-venture capital sources, though that was discussed less when The Services Wars were taking off.

But even the rapid-fire Tiger can’t invest in every company, and not all its bets will pay out. You might decide that you’d be better off putting capital into a slightly smaller fund with a slightly more measured cadence of dealmaking, allowing selection at the hand of fund managers that you trust to allocate your funds among other pooled capital to bet for you. So that you might earn better-than-average returns.

You know, the venture model.

Powered by WPeMatico

Last summer, in the wake of George Floyd’s murder, Best Buy committed to “do better” when it came to supporting communities of color. As part of the retail giant’s self-proclaimed mission to better address underrepresentation and technology inequities, the company announced today that it is investing up to $10 million in Brown Venture Group.

Minnesota-based Brown Venture Group is a three-year-old venture capital firm that has pledged to exclusively back Black, Latino and Indigenous technology startups in “emerging technologies.” Black and Latin communities were the recipients of just 2.6% of total funding in 2020, according to Crunchbase data.

Brown Venture Group is in the process of fundraising for its targeted inaugural $50 million fund, 75% of which has been committed, according to its principals. This means that Minneapolis-based Best Buy’s pledge to invest “up to $10 million” could represent as much as 20% of the total capital raised, making it a lead LP in the fund.

Brown Venture Group co-founder and managing partner Dr. Paul Campbell said that in the early days of forming the firm, he and co-founder Dr. Chris Brooks were told by “multiple people locally” that they should leave the Twin Cities metro area because “all the capital was on the coasts.”

“We just made a firm decision in the very early stages to stay put in the Twin Cities and that we wanted this to be a Twin City story,” Campbell told TechCrunch. “So when we thought about our Twin Cities ecosystem and who we wanted to be leading partners with, Best Buy was at the top of the list. So we are just more than excited to have Best Buy as a lead LP in our fund.”

For its part, Best Buy — which notched $47 billion in revenue last year — said the move is aimed at helping “break down the systemic barriers often faced by Black, Indigenous and people of color (BIPOC) entrepreneurs — including lack of access to funding — and empowering the next generation within the tech industry.”

The company added: “The partnership with Brown Venture Group will work toward making the technology startup landscape more inclusive and creating a stronger community of diverse suppliers.”

In conjunction with announcing Best Buy’s commitment to the fund, the company and venture firm said they would jointly launch an entrepreneurship program at Best Buy Teen Tech Centers to help develop young entrepreneurs through education, mentorship, networking and funding access.

Brown Venture Group — whose name was chosen to represent an “inclusive” skin color of the groups it represents — has so far invested in five companies, including clean energy startup Ecolution kwh.

Ten million dollars seems like a drop in the bucket for a company that generated sales of $47 billion last year. Best Buy said this initiative is just one of several that it has underway to support BIPOC businesses, including plans to provide $44 million to expand college prep and career opportunities for BIPOC students and a pledge to spend at least $1.2 billion with BIPOC and diverse businesses by 2025. The company has also said that by 2025 it will fill one out of three new non-hourly corporate positions with BIPOC employees and hire 1,000 new employees to its technology team, with 30% of them being diverse, specifically Black, Latinx, Indigenous and women.

“We’re committed to taking meaningful action to address the challenges faced by BIPOC entrepreneurs,” Best Buy CEO Corie Barry said in a written statement. “Through partnerships like this, we believe we can begin to do this by helping to build a stronger, more vibrant community of diverse innovators in the tech industry, some of whom we hope will become partners of Best Buy in the future.”

Powered by WPeMatico

Many VCs tout their mentorship and hands-on approach to founders, especially those who run early-stage startups. But in the recent era of lightning-fast rounds closing at sky-high valuations, the cap tables of early-stage startups are becoming increasingly crowded.

This isn’t to say that the value VCs bring has diminished. If anything, it’s quite the opposite — this new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table. It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.

Founders should definitely pursue big rounds at sky-high valuations, but it’s important that they recognize how important it is to manage who they allow into their mentorship circles. Initially, founders should make sure their first layer consists of the real “doers” — usually angels and early venture investors who founders meet with weekly (or more frequently) to help solve some of the most granular problems.

Everything from hiring to operational hurdles all the way to deeper, more personal challenges like balancing family life with a rapidly growing startup.

This circle is where the real mentorship happens, where founders can be open and vulnerable. For obvious reasons, this circle has to be small, and usually consist of two to six people at most. Anything more simply becomes unwieldy and leaves founders spending more time managing these relationships than actually building their company.

How founders manage their VC circles can mean the difference in success or failure for a thousand different reasons.

The second layer should consist of the “quarterly crowd” of investors. These aren’t necessarily people who are uninterested or unwilling to participate in the nitty gritty of running the company, but this circle tends to consist of VCs who make dozens of investments per year. They, like their founders, aren’t capable of managing 50 relationships on a weekly basis, so their touch points on company issues tend to move slower or less frequently.

Powered by WPeMatico

This morning Allocations, a fintech startup building software to help smaller private equity funds form and operate, announced that it has raised a $4 million round at a $100 million valuation.

The startup also shared a host of performance metrics, including that it reached a $4.6 million revenue run rate in June, and a $6 million bookings run rate in the same month.

Allocations also told TechCrunch that it has posted 28% monthly revenue growth over the last 12 months. With metrics like that, our curiosity was piqued. What is Allocations building that is attracting so much early demand? And how does the company’s thesis regarding the future of private equity funds intersect with microventure funds themselves?

Born from CEO Kingsley Advani’s efforts in building a community of angel investors, and the issues that he ran into spinning up special purpose vehicles (SPVs), Allocations started off as software built to scratch its founder’s itch. SPVs are an increasingly common way to raise capital for a single investment from pooled sources, and in today’s rapid-fire venture capital market, Advani had to race to get capital into deals before they closed.

As with many technology startups, Allocations is software designed to solve a known pain point. The old way of putting together SPVs just didn’t match the expected pace at which private investors are expected to commit to investing.

Today the startup’s software helps its users to create new SPVs and funds more quickly, also helping investors manage capital calls and the like after their fund is formed. The startup charges either one-time (in the case of an SPV, by definition a single-shot investment), or recurring fees (multiasset SPVs and funds). A 30-investment fund will cost its managers $15,000 per year through Allocations.

But how many funds are there for the startup to support? Is there enough market to allow Allocations to become a large enterprise itself? So far, the company has attracted some 300 funds to its roster. Advani thinks that there will be plenty of demand. In an interview with TechCrunch, the founder noted that present-day denizens of major funds locked out of material carry — venture economic upside, more simply — can peel off and start their own fund, allowing them much better economics. That dynamic could spur demand for his startup’s services.

Advani also said that family offices and other major capital pools that once fought for allocation into brand-name venture capital funds and other private equity vehicles — venture capital is a subset of private equity — are increasingly chasing smaller funds that may post better returns than larger investing partnerships can manage. This is the law of large numbers in reverse; it’s easier to 10x a $10 million fund than a $10 billion vehicle.

Advani expects his customers will put together multiple funds. Per the CEO, the goal of new fund managers is to get to their second fund. So, new managers often invest their first fund quickly in hope of reaching their second more quickly — more funds means more fees for Allocations.

In the startup’s view, the market will see many more small-scale private equity funds in time, perhaps smaller than $10 million in capital. This perspective mirrors what TechCrunch has seen in the market lately, with rolling funds rising to prominence in the early-stage startup investing, and solo GPs putting together what feels like more microfunds than ever.

Allocations fits into the larger trend of fintech startups taking antiquated models in the world of money and making them faster, more modern and often lower cost. Sure, there’s miles of distance between Allocations and Robinhood, but as both are about smaller investors, democratization of investing access, and using tech to tear down old walls, they are more brethren than different species.

Update: It’s a $4 million round, not $5 million. Post has been corrected.

Powered by WPeMatico

Cent was founded in 2017 as an ad-free creator network that allows users to offer each other crypto rewards for good posts and comments — it’s like gifting awards on Reddit, but with Ethereum. But in late 2020, Cent’s small, San Francisco-based team created Valuables, an NFT market for tweets, and by March, the small blockchain startup was thrown a serendipitous curveball.

“We just wrapped up for the day, and I was about to go eat dinner, and all these people started texting me,” remembers CEO Cameron Hejazi. Then, he realized that Twitter CEO Jack Dorsey had minted Twitter’s first-ever Tweet through Cent’s Valuables application. “I was basically like, mildly shivering for the rest of the night. The whole team, we were like, ‘Okay, battle stations, prepare to get hacked!’ ”

Dorsey ended up selling his NFT for $2.9 million, and he donated the proceeds to Give Directly’s Africa Response fund for COVID-19 relief. But for Cent, it was as if the small company had just been handed a free marketing campaign. Now, about five months later, Cent is announcing a $3 million round of seed funding with investors like Galaxy Interactive, former Disney chairman Jeffrey Katzenberg, will.i.am and Zynga founder Mark Pincus.

On Valuables, anyone on the internet can place an offer on any tweet, which then makes it possible for someone else to make a counter-offer. If the author of the tweet accepts an offer (logging into Valuables requires you to validate your Twitter account), then Cent will mint the tweet on the blockchain and create a 1-of-1 NFT.

The NFT itself contains the text of the tweet, the username of the creator, the time it was minted and the creator’s digital signature. The NFT also includes a link to the tweet, though the linked content lives outside the blockchain.

Image Credits: Cent (opens in a new window)

There’s nothing proprietary about minting tweets as NFTs — another company could do the same thing that Cent is doing. Even Twitter itself has recently dabbled in giving away free NFT art, though it hasn’t tried to sell actual tweets as NFTs like Cent. Still, Hejazi sees Dorsey’s use of Cent like an endorsement — he thinks it would be difficult for Twitter to shut them down, since Dorsey made $2.9 million on the platform himself. After all, Dorsey chose Cent instead of taking a screenshot of his first tweet, minting the .JPG as an NFT and posting it on a larger NFT platform, like OpenSea.

“We’ve spoken with people at Twitter. I’m positive that we have a healthy relationship going,” Hejazi said (Twitter declined to comment on or confirm whether that’s true). “We thought about applying this approach to other social platforms, like Instagram and TikTok, but we hypothesized that this is particularly suited for Twitter, because it’s a conversation platform, and it’s where all of the crypto people are actually living.”

With Cent’s seed funding Hejazi hopes to continue building the platform. The company’s goal is to enable anyone creative to make an income through the use of NFTs — that means developing tools to make it simpler for its users to mint NFTs, but also, building out its existing creator-focused social network. The content people post on Cent is usually creative work, like art and writing, rather than short posts — it’s closer to DeviantArt than it is to Reddit. These are lofty goals for a $3 million seed funding round, but there are aspects of Cent’s Beta platform that make it promising.

“There’s already value in what we post on social media. It’s just being proxied through ad dollars, and it doesn’t have to be the case that there’s so much wealth concentration in a single entity. We can work toward a system that decentralizes that wealth,” said Hejazi. “These networks as they exist have monopolies on distribution — you can’t take your Twitter audience, download it as a .CSV and send them all an email.”

A screenshot of Cent’s social platform.

In addition to independent distribution lists, Hejazi wants to move away from the ad-supported internet. He references Substack as an example of a company where the creator has control of their list, and at the same time, the platform can remain ad-free, since the money that propels it comes from the users who pay to subscribe to newsletters (and also, venture capital helps).

But Cent does something different by allowing users to essentially invest in creators who they think have the potential to take off on their platform.

Users can “seed” a post, which is how you subscribe to a creator participating on the creatives side of Cent’s platform. As the seeder, you pay a set fee of at least one dollar per month. There’s an incentive to support up-and-coming creators on the platform, because seeders get a portion of the creators’ future profit — it’s like making a bet on them that they will continue to make great content in the future. Five percent of profits go toward Cent, but the remaining 95% is split 50/50 between the creator and all of their past seeders. Participating on this platform would allow creators to network and show support for one another, but doesn’t prevent them from more directly monetizing their work on other creator platforms, like Patreon.

In addition to seeding posts, users can also “spot” other people’s posts — Cent’s version of a “like” button. Each “spot” is the equivalent of one cent from the user’s crypto wallet. Cent’s argument is that getting 1,000 likes on a post on other platforms yields nothing but a vague sensation of social clout. But on Cent, if a user gets 1,000 “spots,” that’s $10. Still, a project like this can only work if enough people use the platform.

“When we started Cent, we chose cryptocurrencies because we loved the idea of someone being able to earn money with nothing more than their creativity and a crypto address,” Hejazi said. “Over time, we’ve found it to be limiting as a payment type — very few people actually own it and have it ready to spend. We’re working on ways to make payments to creators using Cent easier, and are exploring both crypto-native and non-crypto options.”

This mindset echoes other NFT startups like Yat, which allows payments via credit card as part of its “progressive decentralization” model. So much of these companies’ success depends on public buy-in toward an eventual decentralized, blockchain-based internet. But until then, companies like Cent will continue to experiment in reimagining how creatives can get paid online.

Powered by WPeMatico