Venture Capital

Auto Added by WPeMatico

Auto Added by WPeMatico

For kids of a certain age — think 9 to 15 — options for enrichment are somewhat limited to school, sports, and camps, while the ability to make money is largely non-existent.

A new startup called Mighty wants to provide them with a new alternative through a platform it’s building that, like a kind of Shopify for kids, enables younger kids to open their own store online and hopefully learn a bit in the process. In fact, Mighty — led by founders Ben Goldhirsh, who previously founded GOOD magazine, and Dana Mauriello, who spent nearly five years with Etsy and was most recently an advisor to Sidewalk Labs — sees itself as smack dab in the center of fintech, ed tech, and entertainment.

As often happens, the concept derived from the founders’ own experience. In this case, Goldhirsh, who has been living in Costa Rica, began worrying about his two daughters, who attend a small school and he feared might fall behind their stateside peers so began tutoring them after school. He says he was using Khan Academy among other software platforms, but their reaction wasn’t exactly positive.

“They were like, “F*ck you, dad. We just finished school and now you’re going to make us do more school?’”

Unsure of what to do, he encouraged them to sell the bracelets they’d been making online, figuring it would teach them needed math skills, as well as teach them about startup capital, business plans (he made them write one), and marketing. It worked, he says, and as he told friends about this successful “project-based learning effort,” they began to ask if he could help their kids get up and running.

Fast forward and Goldhirsh and Mauriello — who ran a crowdfunding platform that Goldhirsh invested in before she joined Etsy — say they’re now steering a still-in-beta startup that has become home to 3,000 “CEOs” as Mighty calls them.

The interest isn’t surprising. Kids are spending more of their time online than at any point in history. Many of the real-world type businesses that might have once employed young kids are shrinking in size. Aside from babysitting or selling cookies on the corner, it’s also challenging to find a job before high school, given the Department of Labor’s Fair Labor Standards Act, which sets 14 years old as the minimum age for employment. (Even then, many employers worry that their young employees might be more work than is worth it.)

Investor think it’s a pretty solid idea, too. Mighty recently closed on $6.5 million in seed funding led by Animo Ventures, with participation from Maveron, Humbition, Sesame Workshop, Collaborative Fund and NaHCO3, a family office.

Still, building out a platform for kids is tricky. For starters, not a lot of 11-year-olds have the tenacity required to sustain their own business over time. While Goldhirsh likens the business to a “21st century lemonade stand,” running a business that doesn’t dissolve at the end of the afternoon is a very different proposition.

Goldhirsh acknowledges that no kid wants to hear they have to “grind” on their business or to follow a certain trajectory, and he says that Mighty is certainly seeing kids who show up for a weekend to make some money. Still, he insists, many others have an undeniably entrepreneurial spirit and says they tend to stick around. In fact, says Goldhirsh, the company — aided by its new seed funding — has much to do in order to keep its hungriest young CEOs happy.

Many are frustrated, for example, that they currently can’t sell their own homemade items through Mighty. Instead, they are invited to sell items like hats, totes, and stickers that they customize and which are made by Mighty’s current manufacturing partner, Printful, which then ships out the item to the end customer. (The Mighty CEO gets a percentage of the sale, as does Mighty.)

They can also sell items made by global artisans through a partnership that Mighty has struck with Novica, an impact marketplace that also sells through National Geographic.

The idea was to introduce as little friction into the process as possible at the outset, but “our customers are pissed — they want more from us,” says Goldhirsh, explaining that Mighty fully intends to one day enable its smaller entrepreneurs to sell their own items, as well as services (think lawn care), which the platform also does not support currently.

As for how it makes money, Mighty plans to layer in subscription services eventually, as well as collect transaction-based revenue.

It’s intriguing, on the whole, though the startup could need to fend off established players like Shopify to should it begin to gain traction.

It’s also conceivable that parents — if not children’s advocates — could push back on what Mighty is trying to do. Entrepreneurship can be alternately exhilarating and demoralizing, after all; it’s a roller coaster some might not want kids to ride from such a young age.

Mauriello insists they haven’t had that kind of feedback to date. For one thing, she says, Mighty recently launched an online community where its young CEOs can encourage one another and trade sales tips, and she says they are actively engaging there.

She also argues that, like sports or learning a musical instrument, there are lessons to be learned by creating a store on Mighty. Storytelling and how to sell are among them, but as critically, she says, the company’s young customers are learning that “you can fail and pick yourself back up and try again.”

Adds Goldhirsch, “There are definitely kids who are like, ‘Oh, this is harder than I thought it was going to be. I can’t just launch the site and watch money roll in.’ But I think they like the fact that the success they are seeing they are earning, because we’re not doing it for them.”

Powered by WPeMatico

Yesterday, China ordered ride-hailing company Didi to stop signing up new customers after regulators announced a cybersecurity review of the company’s operations.

As of this writing, Didi’s stock price is down 5.3%. In today’s edition of The Exchange, Alex Wilhelm suggested that the move wasn’t a complete surprise, but it still “puts a bad taste in our mouths,” since the company went public days ago.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

When Didi filed to go public, it listed several potential pitfalls facing Chinese companies that go public in the U.S., including “numerous legal and regulatory risks” and “extensive government regulation and oversight in its F-1.”

What does this news signify for other Chinese companies that are hoping for stateside IPOs?

We’ll be off on Monday, July 5 in observance of Independence Day. Thanks very much for reading, and I hope you have an excellent weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: NeONBRAND/Unsplash (opens in a new window)

Did you hear about the CEO who made misleading claims about a funding round and got sued? How about that pharmaceutical executive whose taunts to a former Secretary of State led to a 4.4% decline in the Nasdaq Biotechnology Index?

In case it isn’t clear: Startup executives are held to a higher standard when it comes to what they post on social media.

“Reputation and goodwill take a long time to build and are difficult to maintain, but it only takes one tweet to destroy it all,” says Lisa W. Liu, a senior partner at The Mitzel Group, a San Francisco-based law practice that serves many startups.

To help her clients (and Extra Crunch readers) Liu has six basic questions for tech execs with itchy Twitter fingers.

And if the answer to any of them is “I don’t know,” don’t post.

Image Credits: Kari Shea/Unsplash (opens in a new window)

A report from Brighteye Ventures on Europe’s edtech scene shows that this year’s deal flow is on pace to meet or surpass 2020, when remote instruction exploded.

According to Brighteye’s head of Research, Rhys Spence, the average deal size is now $9.4 million, a threefold increase from last year. Still, “It’s interesting that we are not seeing enormous increases in deal count,” he noted.

Image Credits: TechCrunch

Trading platform Robinhood has attracted enough users and activity to change the conversation around retail investing — economists will likely be discussing the 2021 GameStop saga for years to come.

After the company filed to go public yesterday, Alex Wilhelm sorted through Robinhood’s main income statement to better understand how it scaled year-ago revenue from $127.6 million to $522.2 million in Q1.

“Those are numbers that we frankly do not see often amongst companies going public,” says Alex. “300% growth is a pre-Series A metric, usually.”

So: where is all that revenue coming from?

Image Credits: Nigel Sussman (opens in a new window)

Given the valuation gap between U.S. tech markets and those overseas, it’s easy to see why some foreign startups would head to our shores when it’s time to go public.

But Anna Heim and Alex Wilhelm found that a record increase in European venture capital activity is picking up the pace of IPOs this year, and many of these companies are content to go public in their native markets.

To gain some insight into where European investors believe they have an advantage, Anna and Alex interviewed:

Image Credits: Diana Ilieva (opens in a new window) / Getty Images

In a recent private equity survey, 80% of respondents said their co-investments with people outside traditional VC firms outperformed their PE fund investments.

Alternative investors are highly motivated, and because they’re seeking higher returns than are generally available in public markets, they are less daunted by risk. In return, they benefit from less expensive fee structures and develop close ties with VCs, enlarging the talent pool as they build investment skills.

These relationships have direct benefits for VCs as well, such as more flexibility with diversification and consolidated decision-making power.

“With the right deal structure, deal selection and deal investigation, co-investors can significantly increase their returns,” says C5 Capital Managing Partner William Kilmer, who wrote an Extra Crunch post for VCs considering an alternative path.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

My husband and I are both U.S. permanent residents.

Given what we’ve gone through this past year being isolated from loved ones during the pandemic, we’d like to bring my parents and my sister to the U.S. to be close to our family and help out with our children.

Is that possible?

— Symbiotic in Sunnyvale

Image Credits: Andreus (opens in a new window) / Getty Images

Smart-building products include everything from connecting landlords with tenants to managing construction sites.

Given their widespread impact on the enterprise — and the novel nature of much of this new technology, selecting the right digital building platform (DBP) is a challenge for most organizations.

Brian Turner, LEED-AP BD&C, has created a matrix intended to help decision-makers identify the fundamental functions and desired outcomes for stakeholders.

“When it comes to the built environment, creating those comfortable, healthy and enjoyable places requires new tools,” says Turner. “Selecting a solid DBP is one of the most important decisions to be made.”

Image Credits: Octavian Iolu / EyeEm (opens in a new window)/ Getty Images

One perennial problem inside startups: Because no one on the founding team has significant marketing experience, growth-related efforts are pro forma and generally unlikely to move the needle.

Everyone wants higher click-through rates, but creating ads that “stand out” is a risky strategy, especially when you don’t know what you’re doing. This guest post by Demand Curve offers seven strategies for boosting CTR that you can clone and deploy today inside your own startup.

Here’s one: If customers are talking about you online, reach out to ask if you can add a screenshot of their reviews to your advertising. Testimonials are a form of social proof that boost conversions, and they’re particularly effective when used in retargeting ads.

Earlier this week, we ran another post about optimizing email marketing for early-stage startups.

We’ll have more expert growth advice coming soon, so stay tuned.

Image Credits: Jose Fontano/Unsplash (opens in a new window)

Locking down data centers and networks against intruders is just one aspect of an organization’s security responsibilities; cloud services, collaboration tools and APIs extend security perimeters even farther. What’s more, the systems created to prevent the misuse and mishandling of sensitive data often depend heavily on someone’s better angels.

According to Sid Trivedi, a partner at Foundation Capital, and seven-time CIO Mark Settle, IT managers need to replace existing DLP frameworks with a new one that centers on DMP — data misuse protection.

These solutions “will provide data assets with more sophisticated self-defense mechanisms instead of relying on the surveillance of traditional security perimeters,” and many startups are already competing in this space.

Powered by WPeMatico

Let’s play out this scenario. Your deck is ready and you’re just about to start reaching out. What does conventional wisdom say that you should send? A three-paragraph overview, four bullet points outlining the problem, and three bullet points on how you solve it and why you’re the best. You went through all that work … but who is going to read it? A junior person. Not even a senior VC.

Even if you do end up with a meeting, odds are that your deck didn’t even get read. The biggest lie in venture capital is: “Yes, I read through your deck.” Because those words are immediately followed by, “ … but why don’t you run us through it from the beginning?”

At that point, it’s safe to assume that no one has actually taken the time to read through what you sent, the junior guy thought it would be an interesting meeting considering the fund’s current themes of interest, and no one objected to taking the meeting. But no one has really taken the time to read through your deck.

Even if the only benefit was that other investment committee members heard the story direct from the founder, that alone would make your video pitch worth it.

According to DocSend, the average pitch deck review time over the last 20 weeks is less than three minutes. Let’s break down how much time you’ll be given for a 12-page deck (a very concise deck):

That also includes time for that critical-to-understand diagram that illustrates and distills your unique system or view of the world. Do you think 25 seconds is long enough to fully comprehend that diagram and connect the dots with your value prop? Not likely.

Don’t send cold decks, ever. Instead, you should be video pitching — this is a video walkthrough of your deck, with your face in a camera bubble talking through it and giving added color in a video no longer than six-and-a-half minutes. Your objective for this video: Get in, provide a basis of understanding, and get out with a punchy CTA. Nothing flashy, nothing fancy.

More investors are embracing video pitches (prime example: Ashton Kutcher’s Sound Ventures), and in the age of the Zoom-based pitch meeting, it’s quickly becoming the standard.

The rapid but notable shift is because in video pitching, founders get to showcase the preparedness, commitment and passion VCs are looking for, all while telling their story. None of that is effectively transmitted in a cold pitch deck. Further, it allows you to create a deeper connection even before a meeting ever takes place. In a sense, it allows you and the investor to skip a step in the relationship-building process.

Cold decks get blown out of the water when compared with the benefits of the video pitch:

Powered by WPeMatico

Last week was a good one for edtech in Europe.

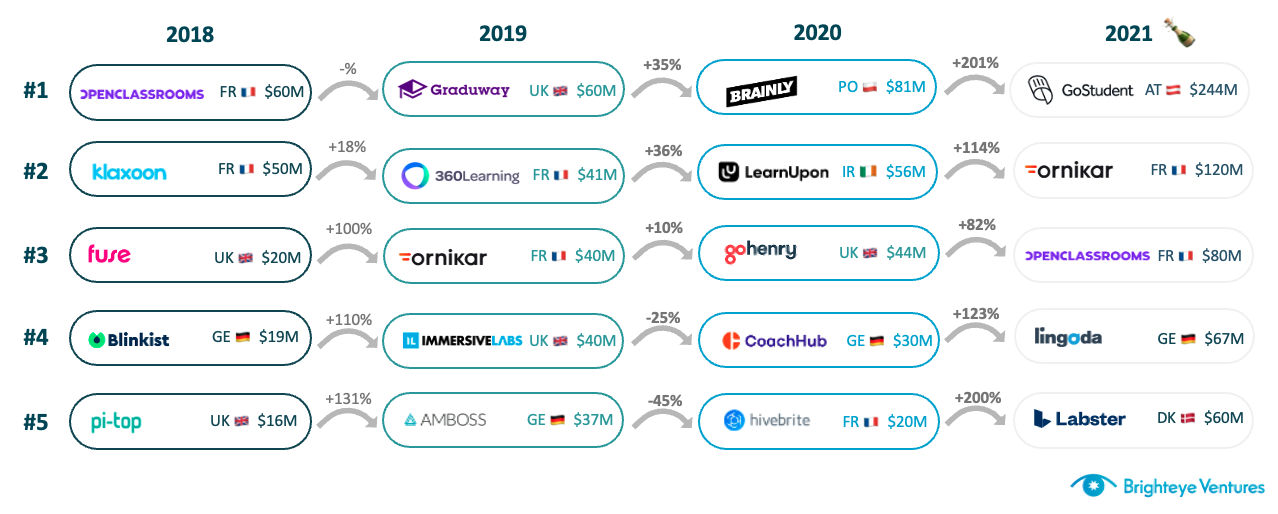

GoStudent became Europe’s first edtech unicorn (IPO’d companies aside), raising its third round in 12 months and the biggest ever in the sector in Europe. Brighteye Ventures’ analysis showed that VC investments in European edtech had breached $1 billion in a calendar year for the first time, even without GoStudent’s mega-round, with six months left to go.

Edtech deal flow in 2021 looks set to match or even outpace 2020 levels, per the report: At $9.4 million, average deal size is triple 2020 levels; seven companies have raised $50 million in five different markets; and the U.K. has more than three times as many deals as the next individual market.

Deal-size progression in edtech over the years. Image Credits: Brighteye Ventures

It’s interesting that we are not seeing enormous increases in deal count. The $1.05-billion mark in the report is spread across 111 transactions — there were 237 in 2020, so we could expect a similar total this year. More funding and stable deal count of course means that we are seeing significant increases in deal size.

It seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

We can draw a few conclusions from this. We can construe that companies created last year and in previous years matured significantly during the pandemic due to increased demand. Moreover, this rapid natural selection process provided insights on verticals and possible winners.

Lastly, it seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

This is contributing to larger early rounds than we have seen in previous years — investors can’t pick the winner, but they can slant the playing field instead. We therefore expect to see a surge in the number of pre-seed, seed and Series A rounds in the second half of 2021, as companies founded during the pandemic begin to raise meaningful funding.

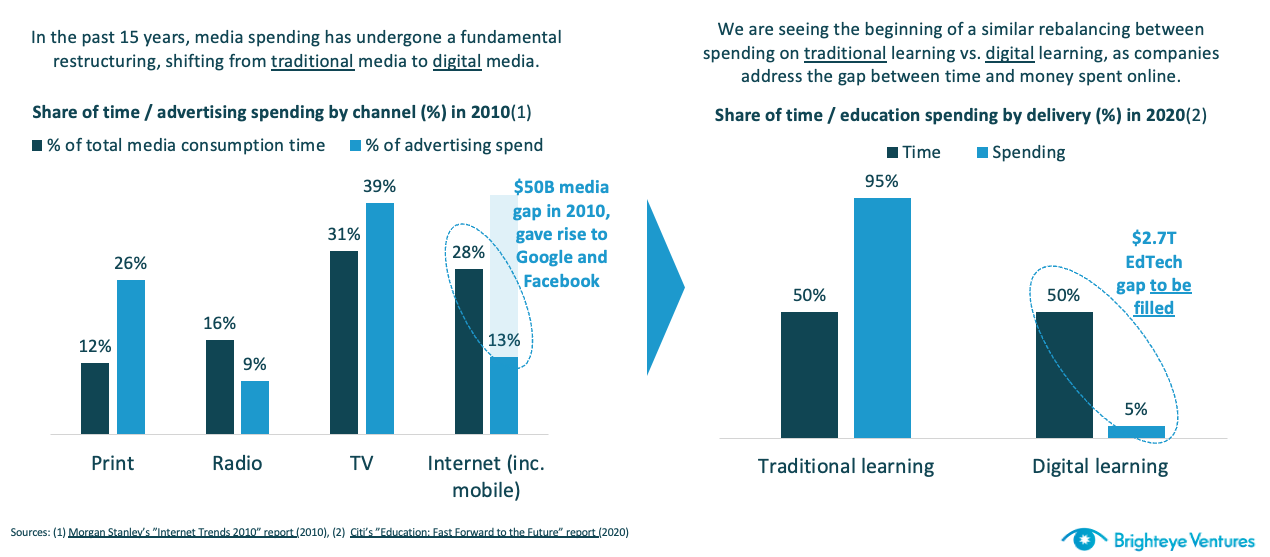

Another reason that edtech is being taken seriously by generalist investors is that the true size of the market (and the extent of digitization to come) is becoming more conceivable.

Edtech spending is growing like media spending did in the 2010s. Image Credits: Brighteye Ventures

Powered by WPeMatico

Jeff Bussgang, a co-founder and general partner at Flybridge Capital, recently wrote an Extra Crunch guest post that argued it is time for a refresh when it comes to the technology adoption life cycle and the chasm. His argument went as follows:

Now, I agree with Jeff that we are seeing remarkable growth in technology adoption at levels that would have astonished investors from prior decades. In particular, I agree with him when he says:

The pandemic helped accelerate a global appreciation that digital innovation was no longer a luxury but a necessity. As such, companies could no longer wait around for new innovations to cross the chasm. Instead, everyone had to embrace change or be exposed to an existential competitive disadvantage.

But this is crossing the chasm! Pragmatic customers are being forced to adopt because they are under duress. It is not that they buy into the vision of software eating the world. It is because their very own lunches are being eaten. The pandemic created a flotilla of chasm-crossings because it unleashed a very real set of existential threats.

The key here is to understand the difference between two buying decision processes, one governed by visionaries and technology enthusiasts (the early adopters and innovators), the other by pragmatists (the early majority).

The key here is to understand the difference between two buying decision processes, one governed by visionaries and technology enthusiasts (the early adopters and innovators), the other by pragmatists (the early majority). The early group makes their decisions based on their own analyses. They do not look to others for corroborative support. Pragmatists do. Indeed, word-of-mouth endorsements are by far the most impactful input not only about what to buy and when but also from whom.

Powered by WPeMatico

Toca Football, a nine-year-old, Costa Mesa, Ca.-based company that operates 14 sports centers across the U.S. that are focused on soccer training, has raised $40 million in Series E funding to roughly double the number of facilities that are now up and running in the U.S., as well as to open a site in the U.K. that CEO Yoshi Maruyama describes as a “highly themed game-experiences-based dining and entertainment facility focused on soccer training.”

Maruyama knows a thing or two about building destinations to which people gravitate. Before joining Toca — which was founded by the American former soccer player Eddie Lewis (“toca” refers to the first touch of the ball in soccer) — Maruyama spent six years as the global head of location-based entertainment for Dreamworks. He spent 14 years before that as an SVP with Universal Parks & Resorts.

Indeed, he was brought into Toca in 2019 to transform it from a manufacturing business that sells Major League Soccer teams a ball-tossing machine that Lewis had developed, to the services business it has become.

On its face, its new model seems like a pretty smart one, given soccer’s growing popularity in the U.S. According to Statista, the number of participants in U.S. high school soccer programs recorded an all-time high in the 2018/19 season, with more than 850,000 playing the sport across the country.

But Toca isn’t built just for kids, even if kids — and their parents –are its primary customers. According to Maruyama, there are several populations that are coming to its various centers throughout the day. In the morning, the centers feature a curriculum for children up to age six to introduce them to soccer; the afternoons feature largely one-on-one soccer training programs where Toca is able to employ its touch trainer; and during the evenings, Toca operates a leagues business for both children and adults.

Some of the centers are huge, by the way. Among Toca’s newest sites, for example, in Naperville, Illinois, outside of Chicago, it has built a 95,000-square-foot facility that features four indoor, full-size soccer fields, as well as one-on-one individual training spaces. (Maruyama suggests the company has been able to take advantage of a depressed commercial real estate market over the last year or so.)

Little wonder that investors see a big opportunity potentially.

The newest round of funding for Toca comes from earlier investors WestRiver Group, RNS TOCA Partners, and D2 Futbol Investors; they were joined by new investors, including angel investor Jared Smith, the co-founder and former COO of Qualtrics.

The company — which plans to expand into Asia as quickly as possible (China has been mandated by the country’s leadership to become “a first-class football superpower” by 2050) — has now raised $105 million in total funding.

Powered by WPeMatico

The number of startups acquiring e-commerce businesses, especially those operating on Amazon, to grow and scale is increasing as more people than ever are shopping online.

The latest such startup to raise capital is Forum Brands, which today announced it has raised $27 million in equity funding for its technology-driven e-commerce acquisition platform.

Norwest Venture Partners led the round, which also included participation from existing backers NFX and Concrete Rose.

Brenton Howland, Ruben Amar and Alex Kopco founded New York-based Forum Brands last summer during the height of the COVID-19 pandemic. Its self-proclaimed goal was to use data to innovate through acquisition.

“We’re buying what we think are A+ high-growth e-commerce businesses that sell predominantly on Amazon and are looking to build a portfolio of standalone businesses that are category leaders, on and off Amazon,” Howland said. “A source of inspiration for us is that we saw how consumer goods and services changed fundamentally for what we think is going to be for decades and decades to come, accelerating the shift toward digital.”

Forum Brands founding team. Image Credits: Forum Brands

Forum’s technology employs “advanced” algorithms and over 60 million data points to populate brand information into a central platform in real time, instantly scoring brands and generating accurate financial metrics.

The M&A team also uses data to contact brand owners “in just three clicks.” But Forum says it already knows which brands meet its acquisition criteria before ever making contact with brand owners.

“The decision to acquire comes within 48 hours and once terms are agreed upon, entrepreneurs get paid in 30 days or less for their brand, with additional income benefits through post-acquisition partnerships,” according to the company.

Its apps leverage analytics to push recommendations to drive growth and financial performance for brands. Then, its multichannel approaches aimed at positioning the brands for “long-term category leadership.”

“We are using a lot of data science and machine learning techniques to build technology that allows us to eventually operate efficiently a large portfolio of digital brands at scale,” Kopco said.

The company is undeterred by the increasingly crowded space based on the belief that the market opportunity is so huge, there’s plenty of room for multiple players.

“We are very much in the day zero consolidation of the e-commerce space, and the market is very, very large,” Amar told TechCrunch. “And based on our data, 98% or 99% of all sellers are still operating independently. So, this is not a winner-takes-all market. There will be multiple winners, and we’ve built a strategy to be one of these winners.”

Norwest Venture Partners’ Stew Campbell believes that the number of sellers who reach a point where they have trouble scaling either due to the lack of resources or time is only going to grow. And Forum Brands intends to capitalize on that.

“There’s a continued need for more liquidity options for the entrepreneurs behind many Amazon-first brands. Forum helps entrepreneurs recognize value, which can be significant too many,” he said. ”After acquisition, the Forum team drives operational efficiencies and scale to create better customer experiences for shoppers on Amazon.”

Campbell emphasizes that his firm was drawn to Forum Brands’ team, which the company also touts as a differentiator.

Co-founder and COO Kopco worked in a variety of product roles for several years at Amazon and Jon Derkits, Forum’s VP of brand growth, is also ex-Amazon. Overall, three-fourths of its operating team are former Amazonians. Co-CEO and co-founder Howland was an investor for two years at Cove Hill Partners and is a former McKinsey consultant. Prior to founding Forum, Co-CEO and co-founder Amar was a growth equity investor at TA Associates.

Campbell says his firm has seen many other models in this market, “but the Forum team blends long-term mindsets and focus on technology, while bringing operational and M&A expertise.”

If this all sounds familiar, it’s because TechCrunch also recently covered the raise of Acquco, which has a similar business model to that of Forum Brands and also involves former Amazon employees. In May, that startup raised $160 million in debt and equity to scale its business. Thrasio is another high-profile player in the space, and has raised $850 million in funding this year. Other startups that have recently attracted venture capital include Branded, which recently launched its own roll-up business on $150 million in funding, as well as Berlin Brands Group, SellerX, Heyday, Heroes and Perch. And, Valoreo, a Mexico City-based acquirer of e-commerce businesses, raised $50 million of equity and debt financing in a seed funding round announced in February.

Also, earlier this month, Moonshot Brands announced a $160 million debt and equity raise to “acquire high-performing Amazon third-party sellers and direct-to-consumer businesses on Shopify and WooCommerce with established brand equity.” That company says that since its founding in 2020, it has achieved a $30 million revenue run rate. Among its investors are Y Combinator, Joe Montana’s Liquid 2 Ventures and the founders of Hippo, Lambda School and Shift.

Powered by WPeMatico

Capping off our dig into the early-stage venture capital market, we’re taking a quick look at Europe this morning. Previously, The Exchange tucked into the United States’ early-stage market for startup capital, uncovering startups using abundant seed capital to get more done before raising a Series A, while others were using pedigree, team and market size to accelerate their first lettered raise.

For both cohorts, it appeared that a rapid-fire Series B could be in the offing, with VCs looking to get capital into winners early.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Latin American venture capital market for early-stage startups had a number of similar hallmarks. That shouldn’t have been surprising. According to Seth Pierrepont, a partner at London-based Accel, “fundraising dynamics are now no longer U.S.- or European-specific — they’re global.” Fundraising over videoconferencing services like Zoom has done more than make geographical distances less impactful inside of countries — it’s even made national borders and even oceans less meaningful.

Is the European startup market similar to what we’ve seen in Latin America and the United States — a cognate for the North American venture capital scene, given its outsized global weight by round count and amount invested?

Largely, yes, a trend that appears to be shaking up prices and the talent wars. This morning, we’re taking a final look at the early-stage venture capital market, this time through a European lens, with an assist from a few investors from the continent.

Broadly, early-stage venture capital rounds in Europe are happening “earlier and are larger in size,” according to Draper Esprit’s Vinoth Jayakumar, an investor based in London. The correlate of larger rounds being raised while startups are younger is valuation expansion, according to Jayakumar, who said that prices are going up “because larger rounds are very dilutive to founders if done at normal — or in this case too low — valuations.”

Powered by WPeMatico

Orum, which aims to speed up the amount of time it takes to transfer money between banks, announced today it has raised $56 million in a Series B round of funding.

Accel and Canapi Ventures co-led the round, which also included participation from existing backers Bain Capital Ventures, Inspired Capital, Homebrew, Acrew, Primary, Clocktower and Box Group. The financing comes barely three months after Orum announced a $21 million Series A, and brings its total raised to over $82 million.

Orum CEO Stephany Kirkpatrick launched the company in 2019 after working for several years at LearnVest, a personal finance site founded by Alexa von Tobel that was acquired by Northwestern Mutual in 2015 for an estimated $375 million. Tobel went on to form Inspired Capital, a venture capital firm that put money in Orum’s $5.2 million seed round last August. Prior to that, the firm also provided Orum with an “inspiration check” that was the first money into the business.

“Most Americans are not familiar with the intricacies of ACH [automated clearing house) or why it takes multiple business days to move money between accounts,” Kirkpatrick said. “But none of us can allow money to wait 5-7 days to hit our accounts. It needs to be instant.”

Her mission with Orum is straightforward even if the technology behind it is complex. Put simply, Orum aims to use machine learning-backed APIs to “move money smartly across all payment rails, and in doing so, provide universal financial access.”

Orum’s first embeddable product, Foresight, launched in September of 2020. It’s an automated programming interface designed to give financial institutions a way to move money in real time. The platform uses machine learning and data science to predict when funds are available and to identify any potential risks. Its Momentum product “intelligently” routes funds across payments rails and is powered by banking providers JPMorgan Chase and Silicon Valley Bank.

“They power the back end of our Momentum platform that allows the money to move on a multirail basis,” Kirkpatrick told TechCrunch. “They power our access to real-time payments.”

Orum says it serves a range of enterprise partners, including Alloy, HM Bradley, First Horizon Bank and Zero Financial (which was recently acquired by Avant).

The volume of transactions being conducted with Orum is growing 100% month over month, Kirkpatrick said. Most of its early growth has come from word of mouth.

The remote-first company prides itself on diversity — in both its employee and investor base. For one, 48% of its 55-person headcount are female, and 48% are “nonwhite,” according to Kirkpatrick. Orum also recently joined the Cap Table Coalition — a partnership between high-growth startups and emerging investors who want to work to close the racial wealth gap — to allocate over 10% of its Series B round to underrepresented founders. For example, the financing includes investors such as the Neythri Features Fund, a group of South Asian women investing in the next generation of female founders and diverse teams.

Jeffrey Reitman, partner at Canapi Ventures (a firm whose LPs mostly consist of banks), told TechCrunch that those bank LPs conduct hundreds of millions of ACH transactions annually,

“They need a path to achieving a state where funds can be transferred instantly,” he said. “Orum’s product paves the path for many players in financial services and fintech — and beyond — to partake in faster money movement without compromising key risk principles.”

To Reitman, the company’s major differentiators are its team, which he describes as consisting of “the best group of data scientists and engineers in the space.”

“Many of their customers consider the team to be instrumental in helping to set the risk dials on how they fund transactions by teasing out key data and insights from historical transaction data,” he said. “Second, Orum is building one of the densest and most comprehensive data sets around the risks of money movement. Better data means better risk models, and it will be hard for other offerings to match Orum’s approach to building this rich data set.”

Accel Partner Sameer Gandhi, who joined Orum’s board as part of the latest financing, agrees. He believes that in an 18-month period, Orum has built “game-changing technology and an exceptional team.”

“Orum is tackling financial infrastructure from its foundation,” he said.

The headline was updated post-publication to reflect the correct funding amount.

Powered by WPeMatico

Accel announced Tuesday the close of three new funds totaling $3.05 billion, money that it will be using to back early-stage startups, as well as growth rounds for more mature companies. Notably, the 38-year-old Silicon Valley-based venture firm is doubling down on global investing.

The announcement underscores both the robust confidence investors continue to have for backing startups in the tech sector and the amount of money available to startups these days.

Specifically, today Accel is announcing its 15th early-stage U.S. fund at $650 million; its seventh early-stage European and Israeli fund also at $650 million and its sixth global growth stage fund at $1.75 billion. The latter fund is in addition, and designed to complement, a previously unannounced $2.3 billion global “Leaders” fund that is focused on later-stage investing that Accel closed in December.

Accel expects to invest in about 20 to 30 companies per fund on average, according to Partner Rich Wong. Its average investment in its growth fund will be in the $50 million to $75 million range, and $75 million and $100 million out of its global Leaders fund.

But the firm is also still eager and “excited” to incubate companies, Wong said.

“We’ll still write $500,000 to $1 million seed checks,” he told TechCrunch. “It’s important to us to work with companies from the very beginning and support them through their entire journey.”

Indeed, as TechCrunch recently reported, Accel has a history of backing companies that were previously bootstrapped (and often profitable) -– the latest example being Lower, a Columbus, Ohio-based fintech, which just raised a $100 million Series A.

Interestingly, Accel is often referred to some of these companies by existing portfolio companies (also in the case of Lower, whose CEO was referred to Accel by Galileo Clay Wilkes). More often than not, companies that Accel backs out of its early-stage and growth funds are bootstrapped and located outside of Silicon Valley.

The venture firm has long looked outside of Silicon Valley for opportunities, and has had offices not only in the Bay Area, but in London and Bangalore for years. Part of its investment thesis is to “invest early and locally,” according to Wong. Examples of this philosophy include investments in companies based all over the world — from Mexico to Stockholm to Tel Aviv to Munich.

Since the time of its last fund closure in 2019, the firm has seen 10 portfolio companies go public, including Slack, Austin-based Bumble, Bucharest-based UiPath, CrowdStrike, PagerDuty, Deliveroo and Squarespace, among others.

It also had 40 companies experience an M&A, including Utah-based Qualtrics’s $8 billion acquisition by SAP and Segment’s $3.2 billion acquisition by Twilio. Also, just last week, Rockwell Automation announced it was buying Michigan-based Plex Systems for $2.22 billion in cash. Accel first invested in Plex, which has developed a subscription-based smart manufacturing platform, in 2012.

Recent investments include a number of fintech companies such as LatAm’s Flink, Berlin-based Trade Republic, Unit and Robinhood rival Public. Accel has also backed as existing portfolio companies such as Webflow, a software company that helps businesses build no-code websites and events startup Hopin.

Wong says Accel is “open-minded but thematic” in its investment approach.

Accel Partner Sonali de Rycker, who is based out of London, agrees.

“For example, we’ll look at automation companies, consumer businesses and security companies, but at a global scale. Our goal is to find the best entrepreneurs regardless of where they are,” she said.

That has only been intensified by the recent rise of the smartphone and cloud, Wong said.

“Before, companies were mostly selling to the consumer in their own country,” he added. “But now the size of the market is so dramatically bigger, allowing them to become even larger, which is one of the reasons why I believe we’re seeing investment pace at this speed.”

To support this, it’s notable that Accel’s global Leaders fund is “dramatically” larger than the $500 million Leaders fund the firm closed in 2019.

Also, de Rycker points out, companies are staying private longer so the opportunity to invest in them until they sell or go public is greater.

Accel is also patient. In some cases, the firm’s investors will develop “years-long” relationships with companies they are courting.

“1Password is an example of this approach,” Wong said. “Arun [Mathew] had that relationship for at least six years before that investment was made. Finally, 1Password called and said ‘We’re ready, and we want you to do it.’ ”

And so Accel led the Canadian company’s first external round of funding in its 14-year history — a $200 million Series A — in 2019.

While the firm is open-minded, there are still some industries it has not yet embraced as much as others. For example, Wong said, “We’re not announcing a $2.2 billion crypto fund, but we have done crypto investments, and see some very interesting trends there. We’ll look at where crypto takes us.”

Powered by WPeMatico