venture capital Firms

Auto Added by WPeMatico

Auto Added by WPeMatico

While retail investors grew more comfortable buying cryptocurrencies like Bitcoin and Ethereum in 2021, the decentralized application world still has a lot of work to do when it comes to onboarding a mainstream user base.

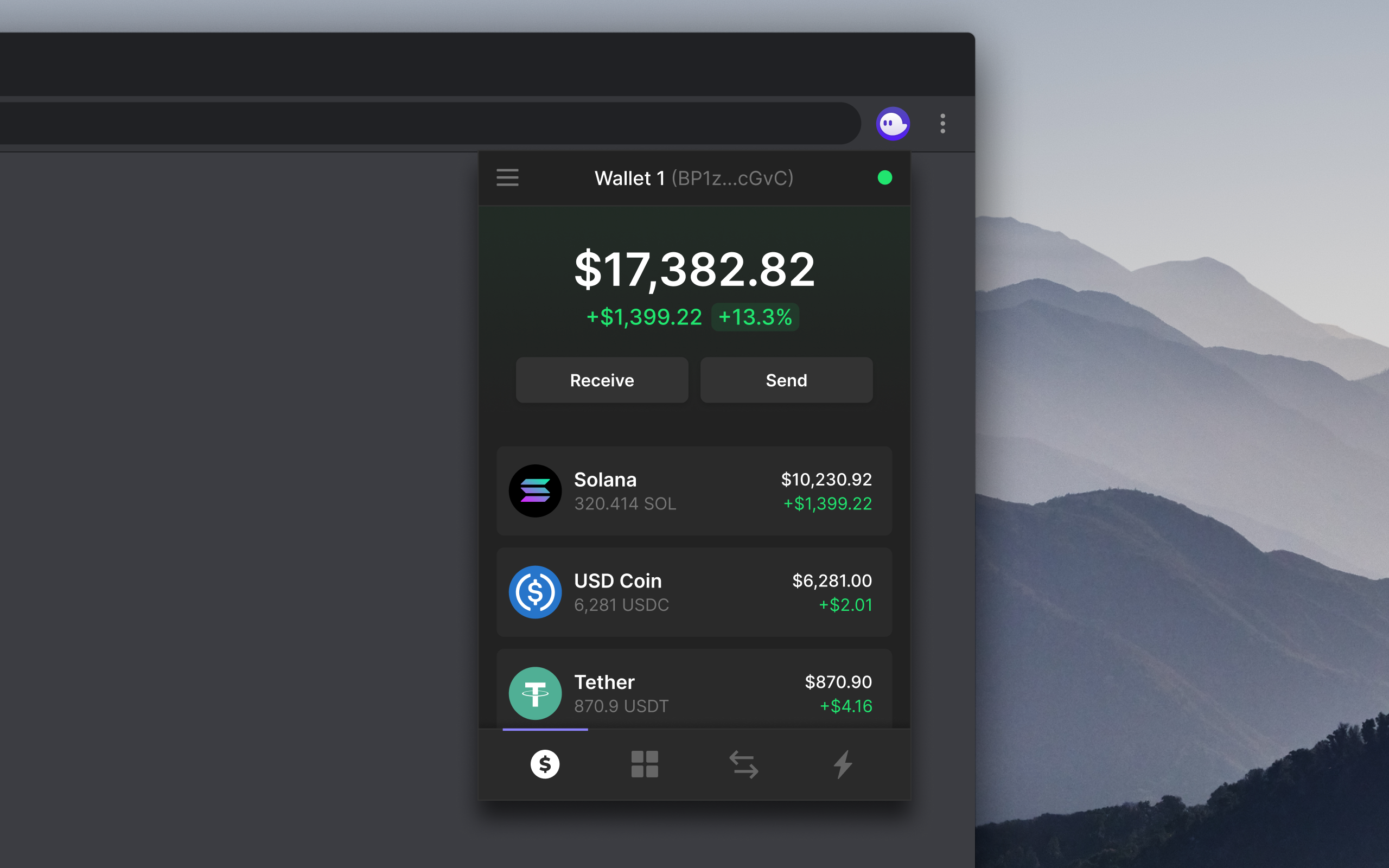

Phantom is part of a new class of crypto startups looking to build infrastructure that streamlines blockchain-based applications and provides a more user-friendly UX for navigating the crypto world, something that can make the entire space more approachable to a non-developer audience. Users can download the Phantom wallet to their browsers to interact with applications, swap tokens and collect NFTs.

The crypto wallet startup has banked a $9 million Series A round led by Andreessen Horowitz (a16z), with Variant Fund, Jump Capital, DeFi Alliance, Solana Foundation and Garry Tan also participating. The round, which closed earlier this summer, comes as some venture capital firms embrace a crypto future even as volatility continues to envelop the broader market. Last month, a16z announced a whopping 2.2 billion crypto fund, the firm’s largest vertical-specific investment vehicle ever.

Image via Phantom

The co-founding team of CEO Brandon Millman, CPO Chris Kalani and CTO Francesco Agosti all come aboard from crypto infrastructure startup 0x.

At the moment, Phantom is best-known among the Solana community, where it has become the go-to wallet for applications on that blockchain. The startup’s ambition is to interface with more and more networks, currently building out compatibility with Ethereum and looking to embrace other blockchains, aiming to be a product built for a “multichain world,” Millman tells TechCrunch.

Alongside building out support for other networks, Phantom wants to build more sophisticated DeFi mechanisms right into their wallet, allowing users to stake cryptocurrencies and swap more tokens inside the wallet.

The startup says they have some 40,000 users of their existing wallet product.

Building out a presence on the popular Ethereum blockchain, which already has a handful of popular wallet providers, will be a challenge, but Phantom’s broadest challenge is helping a new breed of crypto-curious users interface with a network of apps that still have a long way to go when it comes to being mainstream-friendly.

“The entire space is kind of stuck in this ‘built by developers for other developers mode,’ ” Millman says. “This bar has been kind of stuck there, and no one is really stepping up to push the bar up higher.”

Powered by WPeMatico

Digital House, a Buenos Aires-based edtech focused on developing tech talent through immersive remote courses, announced today it has raised more than $50 million in new funding.

Notably, two of the main investors are not venture capital firms but instead are two large tech companies: Latin American e-commerce giant Mercado Libre and San Francisco-based software developer Globant. Riverwood Capital, a Menlo Park-based private equity firm, and existing backer early-stage Latin American venture firm Kaszek also participated in the financing.

The raise brings Digital House’s total funding raised to more than $80 million since its 2016 inception. The Rise Fund led a $20 million Series B for Digital House in December 2017, marking the San Francisco-based firm’s investment in Latin America.

Nelson Duboscq, CEO and co-founder of Digital House, said that accelerating demand for tech talent in Latin America has fueled demand for the startup’s online courses. Since it first launched its classes in March 2016, the company has seen a 118% CAGR in revenues and a 145% CAGR in students. The 350-person company expects “and is on track” to be profitable this year, according to Duboscq.

Digital House CEO and co-founder Nelson Duboscq. Image Credits: Digital House

In 2020, 28,000 students across Latin America used its platform. The company projects that more than 43,000 will take courses via its platform in 2021. Fifty percent of its business comes out of Brazil, 30% from Argentina and the remaining 20% in the rest of Latin America.

Specifically, Digital House offers courses aimed at teaching “the most in-demand digital skills” to people who either want to work in the digital industry or for companies that need to train their employees on digital skills. Emphasizing practice, Digital House offers courses — that range from six months to two years — teaching skills such as web and mobile development, data analytics, user experience design, digital marketing and product development.

The courses are fully accessible online and combine live online classes led by in-house professors, with content delivered through Digital House’s platform via videos, quizzes and exercises “that can be consumed at any time.”

Digital House also links its graduates to company jobs, claiming an employability rate of over 95%.

Looking ahead, Digital House says it will use its new capital toward continuing to evolve its digital training platforms, as well as launching a two-year tech training program — dubbed the the “Certified Tech Developer” initiative — jointly designed with Mercado Libre and Globant. The program aims to train thousands of students through full-time two-year courses and connect them with tech companies globally.

Specifically, the company says it will also continue to expand its portfolio of careers beyond software development and include specialization in e-commerce, digital marketing, data science and cybersecurity. Digital House also plans to expand its partnerships with technology employers and companies in Brazil and the rest of Latin America. It also is planning some “strategic M&A,” according to Duboscq.

Francisco Alvarez-Demalde, co-founder & co-managing partner of Riverwood Capital, noted that his firm has observed an accelerating digitization of the economy across all sectors in Latin America, which naturally creates demand for tech-savvy talent. (Riverwood has an office in São Paulo).

For example, in addition to web developers, there’s been increased demand for data scientists, digital marketing and cybersecurity specialists.

“In Brazil alone, over 70,000 new IT professionals are needed each year and only about 45,000 are trained annually,” Alvarez-Demalde said. “As a result of such a talent crunch, salaries for IT professionals in the region increased 20% to 30% last year. In this context, Digital House has a large opportunity ahead of them and is positioned strategically as the gatekeeper of new digital talent in Latin America, preparing workers for the jobs of the future.”

André Chaves, senior VP of Strategy at Mercado Libre, said the company saw in Digital House a track record of “understanding closely” what Mercado Libre and other tech companies need.

“They move as fast as we do and adapt quickly to what the job market needs,” he said. “A very important asset for us is their presence and understanding of Latin America, its risks and entrepreneurial environment. Global players have succeeded for many years in our region. But things are shifting gradually, and local knowledge of risks and opportunities can make a great difference.”

Powered by WPeMatico

Demetrius Curry has spent the last couple years chasing a dream.

His startup, College Cash, allows brands to petition users to create photo and video marketing content highlighting their product or service, with the wrinkle being that content creators are paid by the brands in the form of credits that go directly toward paying down their student loan debt. This model awards the brands involved a level of social good will and tax benefits.

The Dallas-area founder was inspired to tackle the student loan debt crisis after talking with his daughter about the prospect of eventually paying down her own loan debt. Curry has spent the past two years building out the nascent platform, tracking down brand partners, navigating accelerator programs, enticing users and pounding the pavement to find investors willing to bet on his vision.

College Cash has raised $105,000 to date, and is hoping to eventually wrap the funding into a $1 million seed round.

Filling out the round has been its own challenge for Curry, who has struggled at times to find opportunity, even among historic levels of capital flowing into the startup ecosystem, a distinction that has been less noticeable for black founders that still make up just a small percentage of VC allocation. In the aftermath of last summer’s protests against police brutality, a number of venture capital firms issued statements decrying institutional racism and pledging to back more underserved founders, spinning up new programs for diverse founders.

Demetrius Curry, CEO of College Cash

While Curry says he appreciates the scope of the problem and the good intentions of those making the statements, he believes that venture capital networks still have a lot to learn about what being an “underserved” founder means, and that plenty of the existing efforts feel like “lip service.” He says that even as Silicon Valley continues to idolize dropouts from prestigious universities, stakeholders have less interest in recognizing the accomplishments of founders who fought their way through poverty or found opportunity in geographies where opportunities are harder to come by.

“You can’t look for something different if you’re looking in the same places,” Curry tells TechCrunch. “When you look at the topic of ‘underserved founders,’ it’s not only a skin color thing, it’s also about where they came from and what they’ve been through.”

Curry says that it can be frustrating to compete for early-stage opportunities when investors aren’t willing to meaningfully adjust their parameters. Of particular frustration to Curry has been navigating the world of “warm introductions” to even get a foot in the door for programs meant for diverse founders, or applying for early-stage programs geared toward the “underserved” only to be told that they weren’t far enough along to qualify.

“Think about how much we had to go through to even get in the room with you,” Curry says. “I’ve sold plasma to pay a web hosting fee, nothing is going to stop me.”

College Cash’s mission of expanding opportunities for people struggling to manage their student loan debt is personal to Curry, who saw his life turn around after going back to school.

Decades ago, fresh out of the military, Curry said he had a random conversation with a stranger while eating at a Hardee’s — the discussion about what more he wanted from life ended up pushing him to to go back and get his GED and later a business degree. What followed was a career in finance that eventually led toward his recent entrepreneurial pursuits with College Cash.

The platform is firmly an early-stage venture at the moment, but Curry has big ambitions he’s building toward. His next effort is building out a College Cash tipping integration with gig economy platforms, with the aim that users of those platforms could ultimately opt to tip a worker and route that money directly toward paying down that person’s student loan debt.

Curry says the team at College Cash has been working with a “national gig economy platform” to run a pilot of the integration and has run focus groups showing that users are more likely to tip when they know that money goes toward erasing loan debt.

Powered by WPeMatico

It’s a special day; we’re hosting the year’s final episode of Extra Crunch Live with General Catalyst’s Peter Boyce and Katherine Boyle at 4 p.m. EST/1 p.m. PST.

Extra Crunch members can join the live conversation (details below) or catch it on demand. Questions from the audience are not just allowed, they’re highly encouraged, so if you’re not yet an Extra Crunch member, sign up here and join the fun!

General Catalyst is widely recognized as one of the top venture capital firms, with portfolio companies that include Snap, Kayak, Airbnb, Stripe, HubSpot and GitLab.

Boyce has been with General Catalyst since 2013, leading investments in companies like Ro, Macro, towerIQ and Atom. He also supported some big deals, including investments in Giphy, Jet.com and Circle. He also co-founded Rough Draft Ventures, an investment arm of General Catalyst focused on funding first-time CEOs out of university.

Boyle was previously a business reporter at The Washington Post before joining General Catalyst, which gives her a unique perspective on the entrepreneurial landscape. She’s invested in several companies, including AirMap, Origin and Nova Credit and has joined us for previous events to lay out some advice for startups navigating governmental rules.

We’re amped to discuss which opportunities are exciting them these days, how tech, innovation and venture has changed amid the pandemic, what they look for in a pitch, and much, much more.

You really won’t want to miss it.

Oh, and if this is of interest, I highly suggest you check out our library of ECL episodes right here. We’ve spoken to big names like Roelof Botha, Jason Green, Alexa von Tobel, Aileen Lee, Charles Hudson and many others.

Catch the details for today’s call below.

Powered by WPeMatico

When you’re running your own venture — especially if it’s your first — it’s unlikely you will find the time to deep dive into how venture capital firms work. Fundraising is distracting for founders and can even hurt their company in the early days. But if you only start learning about VCs when you’re already down the fundraising path, you’ll already be too late.

Founders tend to make a series of classic mistakes when raising funding. Error number one (and two) is to raise the wrong amount of money and to do it at the wrong time. This double whammy results in founders being very diluted too early or not raising enough money to reach the next funding stage.

They can also put all their eggs in one basket too early. I made that mistake. I had signed a term-sheet (a nonbinding agreement) for a €2.5 million Series A round, passed the due diligence process, and the investment committee had approved the deal. But at the very last minute, a claim from one of the angels on my cap table made the prospect investor change his mind. In a Point Nine Capital survey, founders said that the two most stressful elements of raising venture capital are not knowing where in the fundraising process they are and not understanding why VCs have rejected their proposal.

On the other hand, if you know what VCs all about, you’ll be geared up for the ride, know the kind of investor personality you’re aiming for, and crucially — you’ll optimize the value of your equity in the long run. Founders who manage to raise more VC funds end up having a greater value stake in their company when the time comes to IPO, according to statistical research. The learning curve is steep; you’re not just studying VC as an industry, but the individual investors themselves. So, I’ve decided to share the main lessons about VC that I wish I’d known when I was a startup founder chasing venture capital.

Startups are all about reaching two milestones: (a) product/market fit and (b) a profitable, repeatable and scalable growth model. Once those two corners are turned, the risk of a startup decreases enormously, which is normally reflected in the valuation. As an early-stage founder, if you want to protect your ownership, make sure you’re raising small amounts of money while your valuations are low.

Save your cash until you de-risk your early-stage startup. Then, raise aggressively when you finally have hard evidence that you have a strong product/market fit and a clear growth model. Be sure you understand when your company reaches that stage and becomes a scaleup. You don’t want to be a founder that has successfully raised a Series A round but has very little ownership and a very long road ahead.

Sometimes, the timing is out of your hands. The price of equity in startups is governed by the supply and demand of capital. Investors themselves have to raise money from another type of investor called Limited Partners (LPs), who may hold stakes in a variety of assets. If LPs have a strong interest in VC assets, there is more supply of capital and the price of startup equity will rise. But the opposite is also true. If you take a look at the last two recessions in the United States (2000 and 2008), you will see that the stock market crash coincided with corrections to valuations in the VC market.

So, be strategic and raise when “the market” has a strong appetite for your equity; otherwise, stretch your runway and wait for the right time. Right now, it’s common to see startups postponing their next raise to 2021, looking for stronger winds.

I see two conditions for startups to raise a large round: (a) a large market that can justify a sizable exit, and (b) a large VC fund (small funds don’t need super sizable exits to be successful).

Assuming the first condition is met, where can we find those large VC funds? Typically, they’ll be in locations close to large markets, with a track record of sizable exits.

Powered by WPeMatico

Only a few weeks after the successful public offering of Array Technologies proved that there’s a market for technologies aimed at improving efficiencies across the solar manufacturing and installation chain, Leading Edge Equipment has raised capital for its novel silicon wafer manufacturing equipment.

The $7.6 million financing came from Prime Impact Fund, Clean Energy Ventures and DSM Venturing, and the company said it would use the technology to ramp up its sales and marketing efforts.

For the last few years researchers have been talking up the potential of so-called kerfless, single-crystal silicon wafers. For industry watchers, the single-crystal versus poly-crystalline wafers may sound familiar, but as with many things with the resurgence of climate technology investment, maybe this time will be different.

Silicon wafer production today is a seven-step process in which large silicon ingots created in heavily energy-intensive furnaces are sawed into wafers by wires. The process wastes large amounts of silicon, requires an incredible amount of energy and produces low-quality wafers that reduce the efficiency of solar panels.

Using ribbons to produce its wafers, Leading Edge’s manufacturing equipment uses the floating silicon method to reduce production to a single step, consuming less energy and producing almost no waste, according to the company.

Leading Edge Equipment was founded by longtime experts in the silicon foundry industry — Alison Greenlee, a quadruple-degreed graduate of the Massachusetts Institute of Technology who worked on floating silicon method that reduces waste in the manufacturing of silicon for solar cells; and Peter Kellerman, the progenitor of floating silicon method technologies.

The two founded Leading Edge Equipment to rejuvenate a project that had been mothballed by Applied Materials after years of research.

The two won $5 million in federal grants and raised an initial $6 million from venture capital firms in 2018 to kick off the technology.

Leading Edge expects that its equipment could become the standard for silicon substrate manufacturing.

Kellerman, now the emeritus chief technology officer, was replaced by Nathan Stoddard, a seasoned silicon manufacturing technology expert who has worked on teams that have brought three different solar wafer technologies from concept to pilot production. Stoddard, a former colleague of Greenlee’s at 1366 — one of the early companies devoted to new silicon production technologies — was won over by Greenlee and Kellerman’s belief in the old Applied Materials technology.

The company claims that its technology can reduce wafer costs by 50%, increase commercial solar panel power by up to 7% and reduce manufacturing emissions by more than 50%.

To commercialize the project, earlier this year the team brought in Rick Schwerdtfeger, a longtime innovator in solar technology who began working with CIGS crystals back in 1995. In the 2000s Schwerdtfeger spent his time in building out ARC Energy to scale next-generation furnace technologies.

“After critical technology demonstrations and the development of a new commercial tool, we are now ready to launch this technology into market in 2021,” said Schwerdtfeger in a statement. “Having recently secured a 31,000 square foot facility and doubled the size of our team, we will use this new funding to prepare for our 2021 commercial pilots.”

Powered by WPeMatico

For many investors, the coronavirus has effectively taken geography out of the equation when it comes to vetting new opportunities.

While this dynamic opens up startups to more investment opportunities, venture capital firms that focus on a specific region are in a thornier spot. The competitive advantage they once had when raising — the notion that they’re focused on an area no one else is — is potentially threatened.

Natasha Mascarenhas, Danny Crichton and Alex Wilhelm of the TechCrunch Equity crew discussed the future of geographic-focused funds given the uptick of remote investing:

Since 2014, Steve Case and his team have made an annual bus trip across the country to meet startups in emerging startup hubs. Five days, five cities and at least $500,000 of investment dollars given to startups. Case would even offer to fly out promising and hard-to-reach startups to have them join the trip.

The Rise of the Rest fund, with more than $300 million in assets under management, has invested in over 130 startups across 70 cities, including Austin, Chicago, Detroit, Los Angeles, New Orleans and Washington, D.C.

Powered by WPeMatico

We won’t sit here as we have for so many years with strong faces and encouraging words and pretend that we’re not tired.

We’re tired because we’ve spent yet another week mourning our Black brothers and sisters who died unjust deaths. We’re tired because we spent half of that week holding the hands of White allies as they were reminded that racism still exists and that it is, indeed, sad. We’re tired because we’re a broken record, telling firms and companies what they can do to fight racism and rarely getting the action they so emotionally promise they care about. We’re tired of holding back anger and sadness as we talk about these issues, knowing our industry isn’t even doing the bare minimum to support Black investors. On top of advising allies, mourning lives lost and working full time jobs, we also raised over $100,000. And we’re tired of racism.

Last week, BLCK VC hosted We Won’t Wait, a day of action where we called on venture firms to discuss, donate and diversify. We asked these firms to discuss Venture’s role in combating institutional racism, to donate to nonprofits that promote racial equity and to release their data on the diversity of their investment teams and portfolio founders. These are the first steps. If you haven’t done these, you’re likely not ready for “Office Hours.” So before we get ahead of ourselves, let’s address why these steps aren’t straightforward or sufficient.

Discuss. It took nationwide uprisings for many VC firms to discuss how they could combat institutional racism. Yet, 80% of firms don’t have one Black investment professional who can identify with what we go through in both our professional and personal lives. BLCK VC held its own discussion to share that perspective, centered on the experiences of Black investors and entrepreneurs.

During this discussion, Terri Burns of GV said, “when a Black person is murdered yet again by police, it is not correct to say that the system has failed, because the system was designed that way.” It is clear that systemic racism leads to the maltreatment, dehumanization and unjustified deaths of Black people across the country. Van Jones of Drive Capital drew a fitting analogy: “Being Black is like being in lane eight with a weight vest and cement boots.” Sounds uncomfortable. But that’s how every Black person in America feels stepping out of bed everyday. For Black founders, discrimination by VCs is par for the course. Elise Smith is not alone when she puts on her daily armor to allow herself to show up in the White-dominated industries of venture capital and Silicon Valley tech.

But we’re not going to repeat what they said. Because you can watch the video, and you can do the research, and you can understand the problem on your own. Truthfully, we have no interest in explaining the problem to White VCs again and again when so many of my brothers and sisters have already spoken on it. If you’d like to know why institutional racism made venture capital so homogeneous and exclusive and racist, please see here, here, here, here and here.

What we are interested in explaining is that these are just examples of what Black investors and entrepreneurs deal with everyday. For almost every Black person in tech, these examples are not only relatable, they are commonplace. These are not the stories that shock and surprise the Black community, these are the stories of the everyday. We didn’t talk about the times we heard the N-word from your colleagues or the times they said our natural hair and beards were unprofessional. We talked about the systems.

There are so many more stories and experiences out there besides what was shared by those seven voices, so please think about what perspectives are missing when you have your discussions. Not just your discussion about racism, but your discussions about the future of venture capital, and about aerospace investing, and about COVID-19 and D2C businesses, and about hiring, and about mentoring and about golf. Black voices are so often left out of the conversations where relationships are built and investment decisions are made, but discussions that lack a Black perspective are incomplete.

Donate. Many VC firms and investors spoke last week about donating their time and resources to Black entrepreneurs and investors — what an interesting way to talk about your job. Please do not donate your time or your money to Black investors or entrepreneurs.

Invest in Black founders because they’re some of the best entrepreneurs. Invest in them because they understand an issue that you do not. Invest in them for the same reason you invest in all of your entrepreneurs — because they’re good. When you frame what you’re doing as a donation, it not only demeans what these entrepreneurs are doing and perpetuates some of the most racist aspects of venture capital, but it also prevents you from understanding that you’re bad at your job. Yes, if you don’t have a diverse pipeline or a diverse portfolio you are bad at your job. Making a separate space and separate fund for Black entrepreneurs removes firms from the responsibility they have to search for, invest in and support Black founders.

If you would like to donate money, donate money to nonprofits that fight institutional racism. If you would like to donate time, volunteer. If you would like to become a better investor, figure out why your pipeline is so homogeneous and fix it.

Diversify. Let’s circle back to an important statistic: More than 80% of venture capital firms don’t have a single Black investor. This statistic is interesting because, as much as it’s about industry trends, it’s really about the failings of individual firms. Most firms don’t have a diverse investing staff. They don’t have a diverse investing staff because they don’t understand the value of racial diversity. They don’t understand the value of racial diversity because there are no diverse investors to force them to think about diversity. Rinse. Repeat.

The single most important part of diversifying a VC firm and diversifying VC broadly is tracking the lack of diversity. Most firms do not routinely track data on their investor, deal pipeline, event or investment diversity. As a result, they rarely think about racial diversity. This is where we ask firms to start. Yes, mentorship can be helpful, office hours can be helpful, but if you’re not tracking your firm’s diversity metrics, they will not improve.

What now? Okay, you’ve discussed racism with your partners, you’ve donated money to nonprofits and you (hopefully) started tracking the diversity of your firm. Now what? Racism resolved? Probably not.

Hopefully these conversations made you realize where your firm’s specific shortcomings are, and you have to address those. Most firms will realize they have a pipeline problem, so start there. Do all of your events, dinners and programs have Black representation? When you’re trying to fill an investor role, did you post the job on your website and in different Black online communities? Did your final round of candidates reflect the diversity of our country? Did you support the diverse investors you already employ so they don’t feel disadvantaged, under-advocated and left out? When you’re trying to write new checks, did you utilize Black scouts and consider businesses that don’t address you directly?

When you’ve done all of that, ask yourself this: When the protests quiet down, and articles about racial oppression aren’t at the top of your timeline, what will you be doing? Don’t let it just be office hours. Don’t let the enormity of the work ahead paralyze you against taking action now. Your actions matter. Your inaction matters.

The resilience of the Black community is unparalleled. That resilience means that no matter how tired we are, we will still fight to change this country and to change this industry. It means that no matter how many times we don’t want to advise allies, we will. And it means that no matter how many times we face oppression and mourn for our brothers and sisters, we will still rise to the challenges. And while the stories of overt racism and microaggressions will continue, so too will our drive to move forward and our action to break down barriers. We will continue to build a home for ourselves in this industry. We will continue to work to ensure that Black Lives Matter.

Powered by WPeMatico

In the past few weeks, several venture capital firms have published different variations of the same pledge: we’ll do a better job supporting the Black community.

My timeline, and I’m assuming yours too, has been filled with statements from non-Black venture capitalists saying that they will rethink how to be more inclusive with their hiring and wiring.

There is no need to applaud firms for taking long overdue steps to treat others equally. What is more important is how we’re going to hold these firms accountable going forward, after a history of inaction.

In a memo published on Friday, Matchstick Ventures outlined a series of commitments to fight racism and underrepresentation. The firm, which manages nearly $37 million dollars and is led by Ryan Broshar and Natty Zola, turned to Black entrepreneur Clarence Bethea for advice on how to proceed.

The pledge stood out for two firm reasons: It is more robust than most promises we have seen by high-profile firms, and it has actual numbers and a deadline, which are key to benchmarking progress.

Matchstick says 7% of the companies it has invested in have Black founders or founding team members, which is seven times the industry average. Portfolio diversity data needs to be more largely released by the VC community because it’s the only way to determine if progress is being made. So far, beyond Matchstick, we’ve only seen Initialized Capital release diversity metrics. Union Square Ventures said that of moe than 100 investments, only a few have been in self-identified Black founders.

Powered by WPeMatico

With commercial launch services expected to reach $7 billion by 2024, there’s increasing demand for an array of new technologies that can offer advantages to companies looking to get communications infrastructure in orbit.

That’s one of the reasons behind the new $25.5 million financing for Momentus, which sells in-space shuttle services to move satellites between orbits.

The company joins other satellite and telecommunications technology vendors like Akash Systems, which raised $14.5 million for its advanced telecommunications chipsets used in satellites, that have raised money from investors looking beyond basic launch services.

A motley assortment of venture capital firms, hedge funds, family offices and other institutional investors came in to finance the new round of funding for Momentus including: Y Combinator, the Lerner Family, the University of Wyoming Foundation, Quiet Capital, Mountain Nazca, ACE & Co., Liquid 2 Ventures and Drake Management. The financing was led by Prime Movers Lab.

With $34 million in funding to date, Momentus said it will use its new cash to continue the development of its two shuttles designed to move payloads between different orbits. As the space in space fills up, the ability to maneuver payloads once they reach low Earth orbit will become more important.

“In the past 18 months, Momentus has rapidly matured their water plasma propulsion system to deliver the world’s safest and most affordable in-space transportation services. They recently launched their first demonstration and are on track to radically reshape the landscape of the space economy,” said Dakin Sloss, founder and general partner at Prime Movers Lab, in a statement. “I look forward to Momentus delivering on their massive backlog of contracts and partnerships with NASA, SpaceX and other top players in the space ecosystem.”

A backlog of contracts is impressive, but the down payment on a potential flight is minimal compared to the ability to get on a vehicle, so companies tend to spread the wealth.

The money will also pay for building in-house research and development for the company’s technology and additional flight demonstrations throughout 2020, according to Momentus chief executive Mikhail Kokorich. The company expects to generate its first revenue next year, as well, Kokorich said.

The company has three flights scheduled for 2020.

Powered by WPeMatico

{kind=link}