VC

Auto Added by WPeMatico

Auto Added by WPeMatico

Singapore is home to fewer than six million people, making it one of the smallest ASEAN countries, in terms of population. It is a young country as well — having gained independence in 1963 — and resides in a neighborhood with far larger economies, including China, Indonesia, and Vietnam. When the country first became independent, its mandate was to simply survive rather than thrive.

So how does a country evolve from a position of relative uncertainty, with comparatively few resources, to one that leads the ASEAN region in venture capital investment and has been home to 10 unicorns?

Countries around the world examine Singapore’s ecosystem from a distance, hoping to learn from, and emulate, its story. The World Bank Group recently published a report, The Evolution and State of Singapore’s Start-up Ecosystem, documenting the country’s experience in building its startup ecosystem and the challenges facing it.

This article presents an overview of the report’s key findings and offers a few key recommendations on what other countries can learn from Singapore’s experience, as well as what Singapore itself can do to maintain progress.

As of 2019, Singapore had over $19 billion in PE and VC assets under management, more than twice that of neighboring Indonesia, Philippines, Vietnam, Malaysia, and Thailand combined. In that same year, the country was home to an estimated 3,600 tech startups and nearly 200 different intermediary and supporting organizations (accelerators, co-working spaces, coding academies, etc.) – some which have a multinational presence, such as Blk71, whose Singapore headquarters has been referred to as “the world’s most tightly packed entrepreneurial ecosystem.”

While assessing the size and strength of startup ecosystems is an evolving method, Start-up Genome priced Singapore’s ecosystem at over $25 billion, five times the global median.

Arguably, the most eye-catching hallmark of this ecosystem is its population of current and former unicorns. Collectively, Singapore has been home to ten unicorns, three of which have offered an IPO (Nanofilm, Razer and Sea) and two of which have been acquired – one by giant Alibaba (Lazada) and one by Chinese streaming powerhouse YY (Bigo Live). The remaining five are Trax, Acronis, JustCo, PatSnap, and Grab – the ASEAN region’s largest unicorn to date.

The education sector is also prominent in Singapore’s ecosystem. Universities like the National University of Singapore (NUS) and Nanyang Technological University (NTU) are deeply embedded into this ecosystem, helping with R&D commercialization linkages, incubation, talent/knowledge transfer, and other areas.

Numerous factors have contributed to building Singapore’s startup ecosystem, with government intervention and leadership being the dominant driving forces. The government has spent more than USD60 billion over the past several decades to enhance the country’s R&D infrastructure, create VC funds, and launch accelerators and other support organizations.

Powered by WPeMatico

When a founder has a work history that includes the name of the parent company of one of their key investors, you probably assume that was one of the first deals to come together. Not so with May Mobility and Toyota AI Ventures, which connected for the company’s second seed round, after May went out and raised its original seed purely on the strength of its own ideas and proposed solutions.

That’s one of the many interesting things we learned from speaking to May Mobility co-founder and CEO Edwin Olson, as well as Chief Product Officer Nina Grooms Lee and Toyota AI Ventures founding partner Jim Adler on an episode of Extra Crunch Live.

Extra Crunch Live goes down every Wednesday at 3 p.m. EDT/noon PDT. Our next episode is with Sequoia’s Shaun Maguire and Vise’s Samir Vasavada, and you can check out the upcoming schedule right here.

Meanwhile, read on for highlights from our chat with Olson, Grooms Lee and Adler, and then stay tuned at the end for a recording of the full session, including our live pitch-off.

One thing Adler brought up early in the chat is that Toyota AI Ventures likely takes a different approach than most traditional corporate VCs, which are often thought of as being more incentivized by strategic alignment than by venture-scale returns. Adler says the firm he founded within the automaker’s corporate umbrella actually does behave much more like a traditional VC in some ways than many would assume.

Powered by WPeMatico

OMERS Ventures, the venture capital arm of the Ontario Municipal Employees Retirement System (OMERS), has put together a new, $750 million fund to invest in both Europe and North America.

The capital vehicle is larger than the group’s preceding European and North American funds combined. In 2019 OMERS Ventures announced a €300 million fund Europe-focused fund (TechCrunch covered its launch here), and the venture group’s last North American fund was worth $300 million back in 2017. The new $750 million is a hybrid, acting as both the firm’s Europe-focused capital pool and the source of funds from which it can invest in North American startups.

According to Damien Steel, a managing partner at OMERS Ventures, the firm invested about CAD$100 million from the original Europe fund, with the rest now reserved for follow-on investments; Steel told TechCrunch that he doesn’t anticipate that the full amount will be used for that purpose.

But the remaining differential is somewhat immaterial as the venture collective has a new, three-quarters-of-a-billion-dollars capital pool to put to work. According to Steel, OMERS Ventures has “consolidated [its] efforts and made a new transatlantic fund.” The firm’s hope is that the shared capital will lead to a more cohesive investing group than having two funds for different teams engendered.

OMERS Ventures expects to deploy around $200 million a year across Europe and North America, a pace that Steel says will be similar to preceding efforts.

I wanted to chase down what Steel and company are doing that’s different in the new era. Something new is a slightly different mindset concerning runway. Instead of the usual 18-month expectation between rounds, Steel told TechCrunch that expectations and planning are lengthening to 24 months or longer between capital events — enough cash to get through whatever the current downturn winds up becoming.

Happily for Steel and his firm, some OMERS portfolio companies are well capitalized, with the venture capitalist telling TechCrunch during a call that “that the companies [his firm has] invested in a have really benefited from the exceptional amount of liquidity that’s been available in the market over the last two years,” with some of their startups winding up “sitting on quite a lot of cash because arguably they raised too much in 2019 and 2018.”

The capital was cheap, Steel notes, so lots of companies took what was on offer. The result? Many startups heading into 2020’s recession have well-stocked bank accounts. Not all, of course, raised right before things got worse. The firms that didn’t may struggle.

Given that the new OMERS Ventures fund intends to invest both in North America and Europe, I wanted to know what’s different between the two regions today as the COVID-19 pandemic continues to drive economic havoc. Notable to me was the fact that Europe is doing as well as it is, with Steel noting that “the funding environment has remained more active in Europe than it has in the US.”

He’s seeing “healthy” activity in Europe around the Series A and B stages. It’s perhaps unsurprising, then, that Steel told TechCrunch that the startup valuation pressure it’s easy to find in the North America venture scene isn’t quite as tough in Europe. Steel noted that 20% and 30% drops in valuation multiples in American and Canada from prior levels are common, while in Europe “it’s definitely less than that.”

For founders that there’s new funds of scale coming together at all is likely welcome. OMERS Ventures expects to have closed eight deals from its new fund “within a month,” a quick pace given its age.

Disclosure: OMERS Ventures invested in Crunchbase, my former employer.

Powered by WPeMatico

For pre-seed startups, precarious times are baseline until they secure their first customer, first hire and first check. But no matter how built-in turbulence might be for a pre-seed founder, we’re entering a period where stresses are amplified and outlooks are unpredictable.

In light of the new market conditions, a harder fundraising market and slower expected growth, Charles Hudson (founder and general partner of Precursor Ventures) is urging his portfolio companies to reassess their futures with a refreshingly human question: “Are you excited and prepared to run this company for the next two years?

If not, you might want to do something else. Why? Because if a super early-stage company manages to survive the COVID-19 era, making it out the other end, it’s not clear that they’ll be venture-ready when markets recover. As Hudson put it, “there’s never been a better time to maybe fold.” That’s because, he explained, startups that merely survive won’t be judged merely against their peers that also survived; they will also compete with brand-new startups for capital and companies that didn’t need to hunker down during lean times.

It’s possible to make it through, but it won’t be an easy path.

TechCrunch spoke with Hudson earlier this week as part of our ongoing Extra Crunch Live series that brings leading founders and investors to our (virtual) stage. Between our editors and journalists and the best questions from the audience, we’re working with guests to understand the new world that we find ourselves in. That we’re hosting these events virtually instead of in-person is testament to our changed reality.

But the chat was far from all gloom; Hudson is bullish on a number of things. Niche publications with subscription economics? Yes. Social services targeting particular audiences? Yep! Precursor is still cutting checks into net-new deals, and while it’s wrapping up its second main fund and first opportunity fund, the firm is also raising a new, larger capital pool.

The conversation ran the full hour we had set aside for it, meaning we had to condense some later discussions about fintech and the new trade-off between growth and profit, but we did get to diversity in venture and startups in the future, and what impact a recession might have on both (it’s a bigger possible impact than you’re considering).

Hit the jump for the best Hudson takeaways and the full audio recording from the session. Head here if you need Extra Crunch access; there are some trials for just a few bucks, so everyone can access the chat. Let’s go!

Powered by WPeMatico

Today’s your last day to score early-bird pricing on tickets to TC Sessions: Robotics + AI 2020, which takes place on March 3. If you want to keep $150 in your wallet, beat the deadline and buy your ticket here before the clock strikes 11:59 p.m. (PT) tonight!

Our one-day conference dedicated to robotics and AI — the good, the bad and the challenging — features interviews, panel discussions, Q&As, workshops and demos. Join roughly 1,500 experts, visionaries, creators, founders, investors, researchers and engineers. Rub elbows, network and engage with current and aspiring leaders, as well as students poised to drive future innovation.

We have a stellar line up, and just because we’re biased doesn’t mean we’re wrong. I mean come on — assistive robots, ethics and AI, the state of VC investment and robot demos. And that’s just for starters. Here are a couple of specific examples (peruse the full agenda right here):

And in case you haven’t heard, we’ve added Pitch Night, a mini pitch-off, into the mix this year. We’re accepting applications until tomorrow, February 1. This is no time for fence-sitting! Apply to compete in Pitch Night now. TechCrunch editors will review the applications and choose 10 startups to pitch at a private event the night before the conference. A panel of VC judges will select five teams as finalists. Those founders will pitch again the next day — live from the Main Stage. It’s awesome exposure that could take your startup to the next level.

If you love robots, you need to be at TC Sessions: Robotics + AI 2020 on March 3. And there’s no point paying more than necessary. Today’s the last day to buy an early-bird ticket. Buy yours before the deadline expires at 11:59 p.m. (PT) and save $150.

Is your company interested in sponsoring or exhibiting at TC Sessions: Robotics + AI 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

November 2019 could mark when Nigeria (arguably) became Africa’s unofficial capital for fintech investment and digital finance startups.

The month saw $360 million invested in Nigerian-focused payment ventures. That is equivalent to roughly one-third of all the startup VC raised for the entire continent in 2018, according to Partech stats.

A notable trend-within-the-trend is that more than half — or $170 million — of the funding to Nigerian fintech ventures in November came from Chinese investors. This marks a pivot (to tech) in China’s engagement with Africa. We’ll get to that.

Before the big Chinese-backed rounds, one of Nigeria’s earliest fintech companies, Interswitch, confirmed its $1 billion valuation after Visa took a minority stake in the company. Interswitch would not disclose the amount to TechCrunch, but Sky News reporting pegged it at $200 million for 20%.

Founded in 2002 by Mitchell Elegbe, Interswitch pioneered the infrastructure to digitize Nigeria’s then predominantly paper-ledger and cash-based economy.

The company now provides much of the tech-wiring for Nigeria’s online banking system that serves Africa’s largest economy and population. Interswitch offers a number of personal and business finance products, including its Verve payment cards and Quickteller payment app.

The financial services firm has expanded its physical presence to Uganda, Gambia and Kenya . The Nigerian company also sells its products in 23 African countries and launched a partnership in August for Verve cardholders to make payments on Discover’s global network.

Visa and Interswitch touted the equity investment as a strategic collaboration between the two companies, without a lot of detail on what that will mean.

One point TechCrunch did lock down is Interswitch’s (long-awaited) and imminent IPO. A source close to the matter said the company will list on a major exchange by mid-2020.

For the near to medium-term, Interswitch could stand as Africa’s sole tech-unicorn, as e-commerce venture Jumia’s volatile share-price and declining market-cap — since an April IPO — have dropped the company’s valuation below $1 billion.

Circling back to China, November was the month that signaled Chinese actors are all in on African tech.

In two separate rounds, Chinese investors put $220 million into OPay and PalmPay — two fledgling startups with plans to scale in Nigeria and the broader continent.

PalmPay, a consumer-oriented payments product, went live last month with a $40 million seed round (one of the largest in Africa in 2019) led by Africa’s biggest mobile-phone seller — China’s Transsion.

The startup was upfront about its ambitions, stating in a company release its goals to become “Africa’s largest financial services platform.”

To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones.

PalmPay also launched in Ghana in November and its U.K. and Africa-based CEO, Greg Reeve, confirmed plans to expand to additional African countries in 2020.

![]()

OPay’s $120 million Series B was announced several days after the PalmPay news and came only months after the mobile-based fintech venture raised $50 million.

Founded by Chinese-owned consumer internet company Opera — and backed by nine Chinese investors — OPay is the payment utility for a suite of Opera -developed internet-based commercial products in Nigeria. These include ride-hail apps ORide and OCar and food delivery service OFood.

With its latest Series A, OPay announced it would expand in Kenya, South Africa and Ghana.

Though it wasn’t fintech, Chinese investors also backed a (reported) $30 million Series B for East African trucking logistics company Lori Systems in November.

With OPay, PalmPay and Lori Systems, startups in Africa have raised a combined $240 million from 15 Chinese investors in a span of months.

There are a number of things to note and watch out for here, as TechCrunch reporting has illuminated (and will continue to do in follow-on coverage).

These moves mark a next chapter in China’s engagement in Africa and could raise some new issues. Hereto, the country’s interaction with Africa’s tech ecosystem has been relatively light compared to China’s deal-making on infrastructure and commodities.

There continues to be plenty of debate (and critique) of China’s role in Africa. This new digital phase will certainly add a fresh component to all that. One thing to track will be data-privacy and national-security concerns that may emerge around Chinese actors investing heavily in African mobile consumer platforms.

We’ve seen lines (allegedly) blur on these matters between Chinese state and private-sector actors with companies such as Huawei.

As OPay and PalmPay expand, they may need to do some reassuring of African regulators as countries (such as Kenya) establish more formal consumer protection protocols for digital platforms.

One more thing to follow on OPay’s funding and planned expansion is the extent to which it puts Opera (and its entire suite of consumer internet products) in competition with multiple actors in Africa’s startup ecosystem. Opera’s Africa ventures could go head to head with Uber, Jumia and M-Pesa — the mobile money-product that put Kenya out front on digital finance in Africa before Nigeria.

Shifting back to American engagement in African tech, Twitter and Square CEO Jack Dorsey was on the continent in November. No sooner than he’d finished his first trip, Dorsey announced plans to move to Africa in 2020, for three to six months, saying on Twitter, “Africa will define the future (especially the bitcoin one!).”

We still don’t know much about what this last trip — or his future foray — mean in terms of concrete partnerships, investment or market moves in Africa from Dorsey and his companies.

He visited Nigeria, Ghana, South Africa and Ethiopia and met with leaders at Nigeria’s CcHub (Bosun Tijani), Ethiopia’s Ice Addis (Markos Lemma) and did some meetings with fintech founders in Lagos (Paga’s Tayo Oviosu).

He visited Nigeria, Ghana, South Africa and Ethiopia and met with leaders at Nigeria’s CcHub (Bosun Tijani), Ethiopia’s Ice Addis (Markos Lemma) and did some meetings with fintech founders in Lagos (Paga’s Tayo Oviosu).

I know pretty well most of the organizations and people Dorsey talked to and nothing has shaken out yet in terms of partnership or investment news from his recent trip.

On what could come out of Dorsey’s 2020 move to Africa, per his tweet and news highlighted in this roundup, a good bet would be it will have something to do with fintech and Square.

More Africa-related stories @TechCrunch

African tech around the ‘net

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about Airbnb’s issues. Before that, I noted Uber’s new “money” team.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you’re new, you can subscribe to Startups Weekly here.

Three African fintech startups; OPay, PalmPay and East African trucking logistics company Lori Systems, closed large fundraises this year. On their own, the deals aren’t particularly notable, but together, they expose a new trend within the African startup ecosystem.

This year, those three companies brought in a total of $240 million in venture capital funding from 15 different Chinese investors, who’ve become increasingly active in Africa’s tech scene. TechCrunch reporter Jake Bright, who covers African tech, writes that 2019 marks “the year Chinese investors went all in on the continent’s startup scene” — particularly its fintech projects. Why?

“The continent’s 1.2 billion people represent the largest share of the world’s unbanked and underbanked population — which makes fintech Africa’s most promising digital sector,” Bright notes. “In previous years, the country’s interactions with African startups were relatively light compared to deal-making on infrastructure and commodities. Chinese actors investing heavily in African mobile consumer platforms lends to looking at new data-privacy and security issues for the continent.”

Active Chinese investors in Africa include Hillhouse Capital, Meituan-Dianping, GaoRong, Source Code Capital, SoftBank Ventures Asia, BAI, Redpoint, IDG Capital, Sequoia China, Crystal Stream Capital, GSR Ventures, Chinese mobile-phone maker Transsion and NetEase .

Here’s more of TechCrunch’s recent coverage of Africa startup activity:

It was a short week (Happy Thanksgiving, by the way). But here’s a quick look at the top deals of the last few days.

Last week, Facebook announced it was buying Beat Games, the game studio behind Beat Saber, a rhythm game that’s equal parts Fruit Ninja and Guitar Hero. Heard of the company? Maybe if you’re a gamer, but if you’re readying this newsletter because of your interest in VC, this company may not have come across your radar.

Why? It’s one of virtual reality’s biggest successes today, but it’s just an eight-person team with no funding.

“I’m really proud that we were able to build the company with this mindset of making decisions based on what is good for the game and not what is the most profitable thing,” Beat Games CEO told TechCrunch earlier this year. Read about Facebook’s acquisition here and an in-depth profile of the small team here.

If you like this newsletter, you will definitely enjoy Equity, which brings the content of this newsletter to life — in podcast form! Join myself and Equity co-host Alex Wilhelm every Friday for a quick breakdown of the week’s biggest news in venture capital and startups.

This week, we discussed Weekend Fund’s new vehicle, Cocoon’s new friend-tracking app and the unfortunate demise of a startup called Omni. You can listen here.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

VC firm Target Global has just announced it’s expanding its European network by adding a local office in Barcelona, Spain — building on its existing presence in Berlin and London, plus Tel Aviv and Moscow.

The firm has €700 million under management and a broad investment range that covers SaaS, marketplaces, fintech and insurtech, as well as a big focus on mobility.

TechCrunch sat down with general partner Shmuel Chafets and investor director Lina Chong, who will be heading the firm’s push into Spain, to talk about its decision to set up shop in Barcelona — discussing how they see the local and national ecosystem, as well as picking their brains on wider investments trends and regulation in Europe.

Want to know what it takes to get a meeting with Target Global and factors they weigh when they’re deciding whether to cut a check or not? Read on…

The interview has been lightly edited for clarity.

TechCrunch: Why choose Barcelona and why now? Why not Spain’s capital, Madrid — or even a city like Paris?

Shmuel Chafets: First of all have you been outside!?

I started coming to Barcelona four or five years ago just to see things and we had some angel investments here and it feels to me today — or when Lina and I started getting more serious about Barcelona it seemed to us that Barcelona has the attributes of Berlin eight or nine years ago. When I at least started coming to Berlin and Lina moved to Berlin, it has the same attributes. It looks like it’s just about to happen

I think it has a few factors. The first one is that it’s a great place to live and you can’t ignore that. In Europe, if you’re a team and you’re an international team there are very few places that you can live in. So London is the original ex-pat city of Europe and it still is amazing but very, very expensive. Berlin is the second one. And I think a lot of Berlin’s early success was fuelled by people who were not necessary German and definitely not Berliners coming and starting a company there.

It’s a good place to live, it’s also a cheap place to live, and it’s a cheap place to do business. Salaries here are quite low but the quality of living is quite high and that makes it very good for startups. Particularly when you need young people, developers, creative people to move. It’s an easy place to convince people to move to.

It doesn’t have a dominant industry. And that is very similar to Berlin — Berlin is not where Germany economically is, and that means that the smartest people around want to go in for startups. That’s the best employment option. There is no banking industry sucking people in with high salaries. And also driving costs up. It is in its culture a very creative city, a very open, very creative city and that I think is also very important.

And lastly, there are these early success stories that fuel the idea of entrepreneurship and also fuel financial entrepreneurship. So one of the interesting things about entrepreneurship is that people who start need to know where it ends or where it’s going to. And the early success stories — first of all they make the smartest kid graduating — who has a McKinsey job offer and a Goldman Sachs job offer and a startup idea — he needs to know that the startup idea has a future. That there’s a future in being an entrepreneur and he needs to look up to people around him. It’s not enough to know that Mark Zuckerberg dropped out — that’s fine but that’s very far and very large.

Image via Getty Images / Pol Albarrán

But to look at Carlos [Pierre, founder and CEO] from Badi and say okay there’s a guy, he’s a few years older than me, he started a company, he’s doing very well — this is the path that I want to take.

Also, there are more and more mentors. People who’ve done it before. And they can help you figure things out. You have to be able to call someone up and say hey let’s have breakfast and explain how they do it.

And there’s more money — for seed. Because you look at a lot of people starting funds, and we were just talking on the way about the Ticketbis guys. They’re starting a fund. And that’s a great example of one of these early success stories and now they’re putting it back into the ecosystem and helping it grow.

Rocket Internet did a lot of that in Germany. They had early exits and then they went and plowed it all back into the ecosystem in their own particular way. People like [serial entrepreneur] Lukasz Gadowski — who we work with a lot. He built Spreadshirts… [then later] he founded Delivery Hero. So through Team Europe. So people who were early, early entrepreneurs — and then in the second wave helped build an ecosystem. So I think there are more and more people like that that we see here.

That usually fuels the ecosystem. Also as companies here start to scale and as more of these European startups start to build hubs here there’s more experience. You can find people who’ve been through a couple of rounds.

And the last thing which is not about Barcelona it’s about Spain in general. There’s a decent local domestic market and there is a natural second market in South America. And actually in the US too — because Spanish is the second most commonly spoken language in America so when you start a company here you have that second market built-in. Which is very important — you can scale it.

Latin America is a fascinating market right now, a fascinating time. So in a way, it’s a way for us to make a side bet on Latin America in a way without going out of Europe and insetting far. My first boss told me never to do business in a place where there’s no direct flight from where I live and I adhere to that. If things go belly up you don’t want to be stuck in transfer in some airport sitting there waiting for a transfer.

TechCrunch: So in a way being in a second city — this isn’t Madrid, Spain’s capital — is a more interesting proposition for startups because there’s less competition for talent?

Chong: It’s a bit of an underdog here. There are not these big dominant industries. It’s not cosmopolitan like how Madrid is perceived. There’s a lot of creativity, a lot of people who are more entrepreneurial in spirit.

Powered by WPeMatico

Activision Blizzard said it has lined up five franchises for a new, city-based Call of Duty esports league.

Atlanta, Dallas, New York, Paris and Toronto will all play host to franchise teams that will compete in a professional league based on what is perhaps Activision Blizzard’s most successful title, the company announced after its earnings call earlier today.

Each city is partnering with existing Overwatch League team owners to leverage the existing framework that Activision has labored over for the past few years to lay the groundwork for a global, city-based Call of Duty league, the company said.

The first teams are Atlanta Esports Ventures, the joint venture owned by Cox Enterprises and Province Inc.; the Envy Gaming esports team, which has been active in Call of Duty competitive play since 2007 and with the Dallas Fuel Overwatch league team; New York’s Sterling.VC, a sports media company backed by Sterling Equities (owners of the New York Mets); c0ntact Gaming, which owns the Overwatch League team Paris Eternal and the Paris-based Call of Duty team; and Toronto’s OverActive Media.

“The upcoming launch of our new Call of Duty esports league reaffirms our leadership role in the development of professional esports. We have already sold Call of Duty teams in Atlanta, Dallas, New York, Paris and Toronto to existing Overwatch League team owners, and we will announce additional owners and markets later this year,” said Bobby Kotick, chief executive of Activision Blizzard. “Our owners value our professional, global city-based model, the success we have had with broadcast partners, sponsors and licensees, and the passion with which our players have responded to our events.”

The announcement came on the heels of an earnings announcement that saw the company report earnings of $1.825 billion for the quarter, beating its outlook of $1.715 billion but down slightly from the year ago period when the company brought in almost $2 billion.

The company credited esports and its Overwatch League and the newly announced Call of Duty city-based league (including selling its first five teams to cities) for contributing to the better-than-expected numbers.

Powered by WPeMatico

Silicon Valley is in the midst of a health craze, and it is being driven by “Eastern” medicine.

It’s been a record year for US medical investing, but investors in Beijing and Shanghai are now increasingly leading the largest deals for US life science and biotech companies. In fact, Chinese venture firms have invested more this year into life science and biotech in the US than they have back home, providing financing for over 300 US-based companies, per Pitchbook. That’s the story at Viela Bio, a Maryland-based company exploring treatments for inflammation and autoimmune diseases, which raised a $250 million Series A led by three Chinese firms.

Chinese capital’s newfound appetite also flows into the mainland. Business is booming for Chinese medical startups, who are also seeing the strongest year of venture investment ever, with over one hundred companies receiving $4 billion in investment.

As Chinese investors continue to shift their strategies towards life science and biotech, China is emphatically positioning itself to be a leader in medical investing with a growing influence on the world’s future major health institutions.

We like to talk about things we can interact with or be entertained by. And so as nine-figure checks flow in and out of China with stunning regularity, we fixate on the internet giants, the gaming leaders or the latest media platform backed by Tencent or Alibaba.

However, if we follow the money, it’s clear that the top venture firms in China have actually been turning their focus towards the country’s deficient health system.

A clear leader in China’s strategy shift has been Sequoia Capital China, one of the country’s most heralded venture firms tied to multiple billion-dollar IPOs just this year.

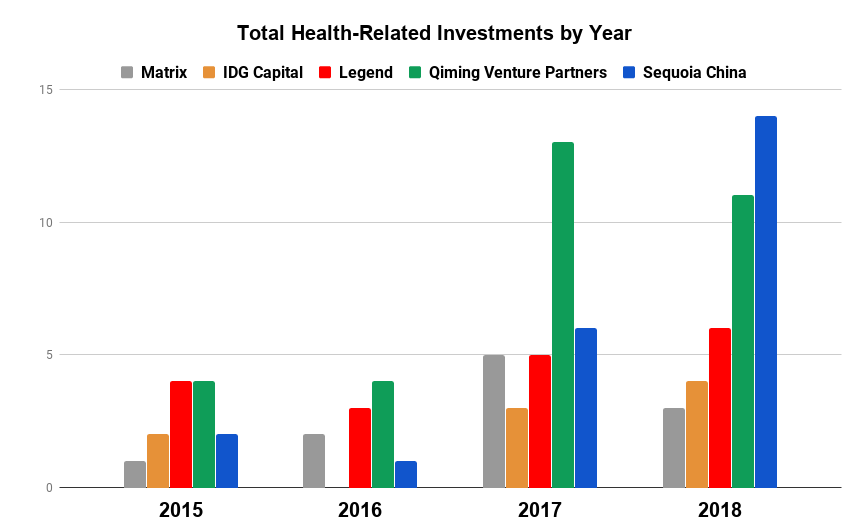

Historically, Sequoia didn’t have much interest in the medical sector. Health was one of the firm’s smallest investment categories, and it participated in only three health-related deals from 2015-16, making up just 4% of its total investing activity.

Recently, however, life sciences have piqued Sequoia’s fascination, confirms a spokesperson with the firm. Sequoia dove into six health-related deals in 2017 and has already participated in 14 in 2018 so far. The firm now sits among the most active health investors in China and the medical sector has become its second biggest investment area, with life science and biotech companies accounting for nearly 30% of its investing activity in recent years.

Health-related investment data for 2015-18 compiled from Pitchbook, Crunchbase, and SEC Edgar

There’s no shortage of areas in need of transformation within Chinese medical care, and a wide range of strategies are being employed by China’s VCs. While some investors hope to address influenza, others are focused on innovative treatments for hypertension, diabetes and other chronic diseases.

For instance, according to the Chinese Journal of Cancer, in 2015, 36% of world’s lung cancer diagnoses came from China, yet the country’s cancer survival rate was 17% below the global average. Sequoia has set its sights on tackling China’s high rate of cancer and its low survival rate, with roughly 70% of its deals in the past two years focusing on cancer detection and treatment.

That is driven in part by investments like the firm’s $90 million Series A investment into Shanghai-based JW Therapeutics, a company developing innovative immunotherapy cancer treatments. The company is a quintessential example of how Chinese VCs are building the country’s next set of health startups using their international footprints and learnings from across the globe.

Founded as a joint-venture offshoot between US-based Juno Therapeutics and China’s WuXi AppTec, JW benefits from Juno’s experience as a top developer of cancer immunotherapy drugs, as well as WuXi’s expertise as one of the world’s leading contract research organizations, focusing on all aspects of the drug R&D and development cycle.

Specifically, JW is focused on the next-generation of cell-based immunotherapy cancer treatments using chimeric antigen receptor T-cell (CAR-T) technologies. (Yeah…I know…) For the WebMD warriors and the rest of us with a medical background that stopped at tenth-grade chemistry, CAR-T essentially looks to attack cancer cells by utilizing the body’s own immune system.

Past waves of biotech startups often focused on other immunologic treatments that used genetically-modified antibodies created in animals. The antibodies would effectively act as “police,” identifying and attaching to “bad guy” targets in order to turn off or quiet down malignant cells. CAR-T looks instead to modify the body’s native immune cells to attack and kill the bad guys directly.

Chinese VCs are investing in a wide range of innovative life science and biotech startups. (Photo by Eugeneonline via Getty Images)

The international and interdisciplinary pedigree of China’s new medical leaders not only applies to the organizations themselves but also to those running the show.

At the helm of JW sits James Li. In a past life, the co-founder and CEO held stints as an executive heading up operations in China for the world’s biggest biopharmaceutical companies including Amgen and Merck. Li was also once a partner at the Silicon Valley brand-name investor, Kleiner Perkins.

JW embodies the benefits that can come from importing insights and expertise, a practice that will come to define the companies leading the medical future as the country’s smartest capital increasingly finds its way overseas.

Despite heavy investment by China’s leading VCs, Silicon Valley is doubling down in the US health sector. (AFP PHOTO / POOL / JASON LEE)

Innovation in medicine transcends borders. Sickness and death are unfortunately universal, and groundbreaking discoveries in one country can save lives in the rest.

The boom in China’s life science industry has left valuations lofty and cross-border investment and import regulations in China have improved.

As such, Chinese venture firms are now increasingly searching for innovation abroad, looking to capitalize on expanding opportunities in the more mature US medical industry that can offer innovative technologies and advanced processes that can be brought back to the East.

In April, Qiming Venture Partners, another Chinese venture titan, closed a $120 million fund focused on early-stage US healthcare. Qiming has been ramping up its participation in the medical space, investing in 24 companies over the 2017-18 period.

New firms diving into the space hasn’t frightened the Bay Area’s notable investors, who have doubled down in the US medical space alongside their Chinese counterparts.

Partner directories for America’s most influential firms are increasingly populated with former doctors and medically-versed VCs who can find the best medical startups and have a growing influence on the flow of venture dollars in the US.

At the top of the list is Krishna Yeshwant, the GV (formerly Google Ventures) general partner leading the firm’s aggressive push into the medical industry.

Krishna Yeshwant (GV) at TechCrunch Disrupt NY 2017

A doctor by trade, Yeshwant’s interest runs the gamut of the medical spectrum, leading investments focusing on anything from real-time patient care insights to antibody and therapeutic technologies for cancer and neurodegenerative disorders.

Per data from Pitchbook and Crunchbase, Krishna has been GV’s most active partner over the past two years, participating in deals that total over a billion dollars in aggregate funding.

Backed by the efforts of Yeshwant and select others, the medical industry has become one of the most prominent investment areas for Google’s venture capital arm, driving roughly 30% of its investments in 2017 compared to just under 15% in 2015.

GV’s affinity for medical-investing has found renewed life, but life science is also part of the firm’s DNA. Like many brand-name Valley investors, GV founder Bill Maris has long held a passion for the health startups. After leaving GV in 2016, Maris launched his own fund, Section 32, focused specifically on biotech, healthcare and life sciences.

In the same vein, life science and health investing has been part of the lifeblood for some major US funds including Founders Fund, which has consistently dedicated over 25% of its deployed capital to the space since at least 2015.

The tides may be changing, however, as the recent expansion of oversight for the Committee on Foreign Investment in the United States (CFIUS) may severely impact the flow of Chinese capital into areas of the US health sector.

Under its extended purview, CFIUS will review – and possibly block – any investment or transaction involving a foreign entity related to the production, design or testing of technology that falls under a list of 27 critical industries, including biotech research and development.

The true implications of the expanded rules will depend on how aggressively and how often CFIUS exercises its power. But a lengthy review process and the threat of regulatory blocks may significantly increase the burden on Chinese investors, effectively shutting off the Chinese money spigot.

Regardless of CFIUS, while China’s active presence in the US health markets hasn’t deterred Valley mainstays, with a severely broken health system and an improved investment environment backed by government support, China’s commitment to medical innovation is only getting stronger.

Deficiencies in China’s health sector has historically led to troublesome outcomes. Now the government is jump-starting investment through supportive policy. (Photo by Alexander Tessmer / EyeEm via Getty Images)

They say successful startups identify real problems that need solving. Marred with inefficiencies, poor results, and compounding consumer frustration, China’s health industry has many.

Outside of a wealthy few, citizens are forced to make often lengthy treks to overcrowded and understaffed hospitals in urban centers. Reception areas exist only in concept, as any open space is quickly filled by hordes of the concerned, sick, and fearful settling in for wait times that can last multiple days.

If and when patients are finally seen, they are frequently met by overworked or inexperienced medical staff, rushing to get people in and out in hopes of servicing the endless line behind them.

Historically, when patients were diagnosed, treatment options were limited and ineffective, as import laws and affordability issues made many globally approved drugs unavailable.

As one would assume, poor detection and treatment have led to problematic outcomes. Heart disease, stroke, diabetes and chronic lung disease accounts for 80% of deaths in China, according to a recent report from the World Bank.

Recurring issues of misconduct, deception and dishonesty have amplified the population’s mounting frustration.

After past cases of widespread sickness caused by improperly handled vaccinations, China’s vaccine crisis reached a breaking point earlier this year. It was revealed that 250,000 children had been given defective and fallacious rabies vaccinations, a fact that inspectors had discovered months prior and swept under the rug.

Fracturing public trust around medical treatment has serious, potentially destabilizing effects. And with deficiencies permeating nearly all aspects of China’s health and medical infrastructure, there is a gaping set of opportunities for disruptive change.

In response to these issues, China’s government placed more emphasis on the search for medical innovation by rolling out policies that improve the chances of success for health startups, while reducing costs and risk for investors.

Billions of public investment flooded into the life science sector, and easier approval processes for patents, research grants, and generic drugs, suddenly made the prospect of building a life science or biotech company in China less daunting.

For Chinese venture capitalists, on top of financial incentives and a higher-growth local medical sector, loosening of drug import laws opened up opportunities to improve China’s medical system through innovation abroad.

Liquidity has also improved due to swelling global interest in healthcare. Plus, the Hong Kong Stock Exchange recently announced changes to allow the listing of pre-revenue biotech companies.

The changes implemented across China’s major institutions have effectively provided Chinese health investors with a much broader opportunity set, faster growth companies, faster liquidity, and increased certainty, all at lower cost.

However, while the structural and regulatory changes in China’s healthcare system has led to more medical startups with more growth, it hasn’t necessarily driven quality.

US and Western investors haven’t taken the same cross-border approach as their peers in Beijing. From talking with those in the industry, the laxity of the Chinese system, and others, have made many US investors weary of investing in life science companies overseas.

And with the Valley similarly stepping up its focus on startups that sprout from the strong American university system, bubbling valuations have started to raise concern.

But with China dedicating more and more billions across the globe, the country is determined to patch the massive holes in its medical system and establish itself as the next leader in international health innovation.

Powered by WPeMatico