Valuations

Auto Added by WPeMatico

Auto Added by WPeMatico

We’re not digging into another IPO filing today. You can read all about AppLovin’s filing here, or ThredUp’s document here.

This morning, instead, we’re talking about an old favorite: software valuations. The folks over at Battery Ventures have compiled a lengthy dive into the 2020 software market that’s worth our time — you can read along here; I’ll provide page numbers as we go — because it helps explain some software valuations.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

There’s little doubt that there is some froth in the software market, but it may not be where you think it is.

The Battery report has a lot of data points that we’ll also work through in this week’s newsletter, but this morning, let’s narrow ourselves to thinking about rising aggregate software multiples, the breakdown of multiples expansion through the lens of relative growth rates, and cap it off with a nibble on the importance, or lack thereof, of cash flow margins for the valuation of high-growth software companies.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

I chatted through pieces of the report with its authors, Battery’s Brandon Gleklen and Neeraj Agrawal. So, we’ll lean on their perspective a little as we go to help us move quickly. This is our Friday treat. Or at least mine. Let’s get into it.

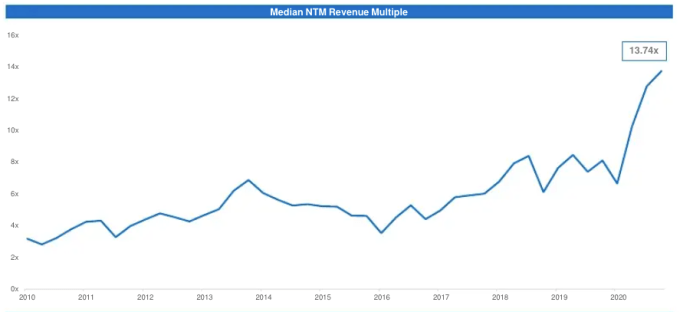

Let’s start with an affirmation. Yes, software valuations have risen to record-high multiples in recent years. Here’s the Battery chart that makes the change clear:

Page 31, Battery report. Image Credits: Battery Ventures

Powered by WPeMatico

This year’s Bessemer Venture Partners’ annual Cloud 100 Benchmark report was published recently and my colleague Alex Wilhelm looked at some broad trends in the report, but digging into the data, I decided to concentrate on the Top 10 companies by valuation. I found that the top company has defied convention for a couple of reasons.

Bessemer looks at private companies. Once they go public, they lose interest, and that’s why certain startups go in and out of this list each year. As an example, Dropbox was the most highly valued company by far with a valuation in the $10 billion range for 2016 and 2017, the earliest data in the report. It went public in 2018 and therefore disappeared.

While that $10 billion benchmark remains a fairly good measure of a solidly valued cloud company, one company in particular blew away the field in terms of valuation, an outlier so huge, its value dwarfs even the mighty Snowflake, which was valued at over $12 billion before it went public earlier this month.

That company is Stripe, which has an other-worldly valuation of $36 billion. Stripe began its ascent to the top of the charts in 2016 and 2017 when it sat behind Dropbox with a $6 billion valuation in 2016 and around $8 billion in 2017. By the time Dropbox left the chart in 2018, Stripe would have likely blown past it when its valuation soared to $20 billion. It zipped up to around $23 billion last year before taking another enormous leap to $36 billion this year.

Stripe remains an outlier not only for its enormous valuation, but also the fact that it hasn’t gone public yet. As TechCrunch’s Ingrid Lunden pointed out in an article earlier this year, the company has remained quiet about its intentions, although there has been some speculation lately that an IPO could be coming.

What Stripe has done to earn that crazy valuation is to be the cloud payment API of choice for some of the largest companies on the internet. Consider that Stripe’s customers include Amazon, Salesforce, Google and Shopify and it’s not hard to see why this company is valued as highly as it is.

Stripe came up with the idea of making it simple to incorporate a payments mechanism into your app or website, something that’s extremely time-consuming to do. Instead of building their own, developers tapped into Stripe’s ready-made variety and Stripe gets a little money every time someone bangs on the payment gateway.

When you’re talking about some of the biggest companies in the world being involved, and many others large and small, all of those payments running through Stripe’s systems add up to a hefty amount of revenue, and that revenue has led to this amazing valuation.

One other company you might want to pay attention to here is UIPath, the robotic process automation company, which was sitting just behind Snowflake with a valuation of over $10 billion. While it’s unclear if RPA, the technology that helps automate legacy workflows, will have the lasting power of a payments API, it certainly has come on strong the last couple of years.

Most of the companies in this report appear for a couple of years as they become unicorns, watch their values soar and eventually go public. Stripe up to this point has chosen not to do that, making it a highly unusual company.

Powered by WPeMatico

Silicon Valley has many dreams. One dream — the Hollywood version anyway — is for a down-and-out founder to begin tinkering and coding in their proverbial garage, eventually building a product that is loved by humans the world over and becoming a startup billionaire in the process.

The more prosaic and common version of that Valley dream though is to join an early-stage company right before its growth kicks into high gear. Sure, those early employees might only have a smidgen of equity, but that equity could be worth a whole heck of a lot if they join the right startup.

Every startup has a window of opportunity, a timeframe in which early employees can join while the stock option strike prices are low and the equity grants are high. Join before the big uptick in valuation, and suddenly what might have been an otherwise nice couple of hundred K dollars in the coming years becomes actually, well, in the Bay Area, a reasonably-sized domicile.

Yet, that opportune window seems to be shrinking in size, making it harder for potential startup employees to nail the timing necessary to garner their own best financial return.

For every Roblox, which as we profiled in-depth this week, took almost two decades to reach its current apotheosis, there is a Brex, which seems to reach unicorn status in no time at all. And such stories — while certainly anecdotal — seem to be more commonplace than ever.

Part of the reason for that fast early valuation growth is that Silicon Valley has simply learned how to grow even faster, even earlier. As venture capitalist Reid Hoffman and Chris Yeh discuss in their book Blitzscaling, there are now frameworks and tried-and-true techniques to not just grow a startup, but to grow it at a dizzying rate. Through better marketing channels, growth strategies, and product development, we have indeed made progress at cutting at least some of the time to better valuations.

That rapid transformation from nothing to everything though gives very little time for early employees to discover a startup through the grapevine when the financial conditions are still interesting.

Half a decade ago, I wrote about the plight of early employees in an article I entitled “The Problem with Founders.” I wrote then that:

The secret of Silicon Valley is that the benefits of working at a startup accrues almost entirely to the founders, and that’s why people repeat the advice to just go start a business. There is a reason it is hard to hire in Silicon Valley today, and it isn’t just that there are a lot of startups. It’s because engineers and other creators are realizing that the cards are stacked against them unless they are the ones in charge.

My reasoning then was simple: early employees take on pretty much just as much risk as their founders do, but for a fraction of the equity. Now, with startups jumping to unicorn status in sometimes as short as a handful of months, that risk-reward ratio seems to be even more off-kilter for those early employees.

And it doesn’t just have to be a Brex -scale transformation either. The rapid increase in the size and valuation of series A rounds of financing the past three years means that engineers and salespeople who might have an employee number in the low double digits are suddenly seeing their options struck at a couple of hundred million in valuation. Exits, meanwhile, aren’t suddenly getting richer to compensate.

I started to notice this pattern over the past few weeks in the course of several conversations with software engineering friends of mine who had gotten excited about very early-stage companies — say, just a handful of employees — but who walked away from their offer letters due to already sky-high company valuations.

Now, there is an argument to be made that joining these sorts of companies is precisely where the best opportunities lie. Sure, the valuations are already high, but these are startups with the financial resources and the backing that might allow them to compete effectively. So maybe the equity is smaller and more expensive, but ultimately, if the startup is more likely to be successful, the expected value function might actually be favorable.

Maybe. Yet it is also hard to see how these startups, which despite their rich valuations have barely laid any foundation for success, are a safer bet than a similarly-valued startup with years of experience under its belt and a growth strategy based upon dependable results. Even worse, early employees are perhaps taking even more financial risk, since the preference stack of the venture capital could mean that smaller exits are particularly unfavorable to them.

Plus, the shrinking opportunity window for leading startups means that the difference in financial outcome between two early employees — what could be millions of dollars upon an exit — could have been decided based on who joined the week before the other. That doesn’t seem fair or right, but is increasingly widespread in our industry.

As with most macroeconomic structural changes, there’s not much for anyone to do. Founders aren’t going to take lower valuations or less money just to make the lives of their early employees a bit more rosy, and certainly venture capitalists aren’t going to lowball their offers in a hyper-competitive investment environment. Indeed, the very excitement of a sudden unicorn may be the best attraction for candidates to hear a startup’s pitch and ultimately join.

But when it comes to that Silicon Valley dream of a nice house from a decent return on exit, it’s getting narrower and less widely-distributed. Blitzscaling is making a lot of people a lot of wealth, but early employees? Not so much.

Powered by WPeMatico

Some very big brands outside the tech space have been stepping in to acquire technology companies as the pressure to keep up with consumer-powered digital trends touches more industries. Add in a deregulating President Trump and the mercury could keep rising for tech company valuations this year, suggests John Stiffler, senior M&A director at business and technology consulting firm West… Read More

Some very big brands outside the tech space have been stepping in to acquire technology companies as the pressure to keep up with consumer-powered digital trends touches more industries. Add in a deregulating President Trump and the mercury could keep rising for tech company valuations this year, suggests John Stiffler, senior M&A director at business and technology consulting firm West… Read More

Powered by WPeMatico

The hot air around young and savvy tech startups is not going anywhere, despite dark prophecies that saw 2016 as the “winter is coming” year. Snapchat and Airbnb are warming up on the sidelines of an IPO, BuzzFeed, Palantir and Uber are snatching hundreds of millions of dollars every couple of months and young startups with no revenues and almost no users raise tens of millions… Read More

The hot air around young and savvy tech startups is not going anywhere, despite dark prophecies that saw 2016 as the “winter is coming” year. Snapchat and Airbnb are warming up on the sidelines of an IPO, BuzzFeed, Palantir and Uber are snatching hundreds of millions of dollars every couple of months and young startups with no revenues and almost no users raise tens of millions… Read More

Powered by WPeMatico

Management and boards at late-stage, or pre-IPO, companies are on notice that the SEC is paying attention to the late-stage financing arena, and should look internally to ensure that corporate governance and financial controls are befitting their scale, and should also ensure the accuracy of the disclosures they make when raising funds. Read More

Management and boards at late-stage, or pre-IPO, companies are on notice that the SEC is paying attention to the late-stage financing arena, and should look internally to ensure that corporate governance and financial controls are befitting their scale, and should also ensure the accuracy of the disclosures they make when raising funds. Read More

Powered by WPeMatico