valar ventures

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to This Week in Apps, the weekly TechCrunch series that recaps the latest in mobile OS news, mobile applications and the overall app economy.

The app industry continues to grow, with a record 218 billion downloads and $143 billion in global consumer spend in 2020. Consumers last year also spent 3.5 trillion minutes using apps on Android devices alone. And in the U.S., app usage surged ahead of the time spent watching live TV. Currently, the average American watches 3.7 hours of live TV per day, but now spends four hours per day on their mobile devices.

Apps aren’t just a way to pass idle hours — they’re also a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus. In 2020, investors poured $73 billion in capital into mobile companies — a figure that’s up 27% year-over-year.

Do you want This Week in Apps in your inbox every Saturday? Sign up here: techcrunch.com/newsletters

Apple announced a major initiative to scan devices for CSAM imagery. The company on Thursday announced a new set of features, arriving later this year, that will detect child sexual abuse material (CSAM) in its cloud and report it to law enforcement. Companies like Dropbox, Google and Microsoft already scan for CSAM in their cloud services, but Apple had allowed users to encrypt their data before it reached iCloud. Now, Apple’s new technology, NeuralHash, will run on users’ devices, tatformso detect when a users upload known CSAM imagery — without having to first decrypt the images. It even can detect the imagery if it’s been cropped or edited in an attempt to avoid detection.

Meanwhile, on iPhone and iPad, the company will roll out protections to Messages app users that will filter images and alert children and parents if sexually explicit photos are sent to or from a child’s account. Children will not be shown the images but will instead see a grayed-out image instead. If they try to view the image anyway through the link, they’ll be shown interruptive screens that explain why the material may be harmful and are warned that their parents will be notified.

Some privacy advocates pushed back at the idea of such a system, believing it could expand to end-to-end encrypted photos, lead to false positives, or set the stage for more on-device government surveillance in the future. But many cryptology experts believe the system Apple developed provides a good balance between privacy and utility, and have offered their endorsement of the technology. In addition, Apple said reports are manually reviewed before being sent to the National Center for Missing and Exploited Children (NCMEC).

The changes may also benefit iOS developers who deal in user photos and uploads, as predators will no longer store CSAM imagery on iOS devices in the first place, given the new risk of detection.

Image Credits: Apple

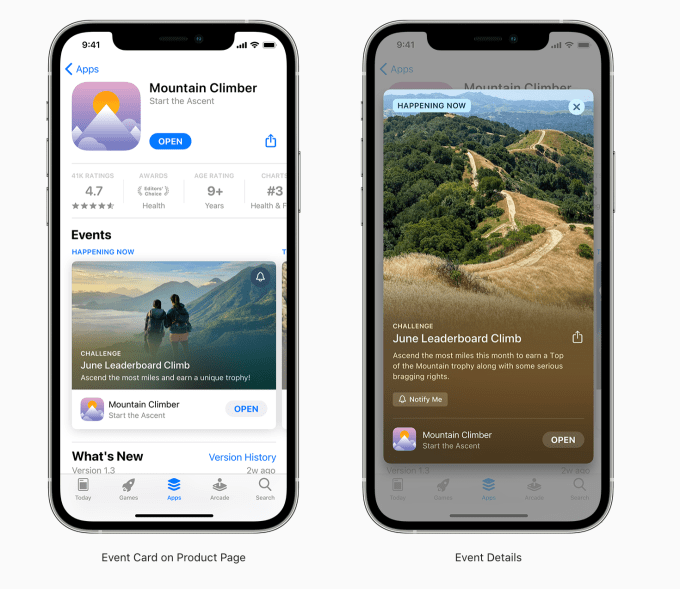

Though not yet publicly available to all users, those testing the new iOS 15 mobile operating system got their first glimpse of a new App Store discovery feature this week: “in-app events.” First announced at this year’s WWDC, the feature will allow developers and Apple editors alike to showcase directly on the App Store upcoming events taking place inside apps.

The events can appear on the App Store homepage, on the app’s product pages or can be discovered through personalized recommendations and search. In some cases, editors will curate events to feature on the App Store. But developers will also be provided tools to submit their own in-app events. TikTok’s “Summer Camp” for creators was one of the first in-app events to be featured, where it received a top spot on the iPadOS 15 App Store.

Apple expands support for student IDs on iPhone and Apple Watch ahead of the fall semester. Tens of thousands more U.S. and Canadian colleges will now support mobile student IDs in the Apple Wallet app, including Auburn University, Northern Arizona University, University of Maine, New Mexico State University and others.

Apple was accused of promoting scam apps in the App Store’s featured section. The company’s failure to properly police its store is one thing, but to curate an editorial list that actually includes the scams is quite another. One of the games rounded up under “Slime Relaxations,” an already iffy category to say the least, was a subscription-based slime simulator that locked users into a $13 AUD per week subscription for its slime simulator. One of the apps on the curated list didn’t even function, implying that Apple’s editors hadn’t even tested the apps they recommend.

Tax changes hit the App Store. Apple announced tax and price changes for apps and IAPs in South Africa, the U.K. and all territories using the Euro currency, all of which will see decreases. Increases will occur in Georgia and Tajikistan, due to new tax changes. Proceeds on the App Store in Italy will be increased to reflect a change to the Digital Services Tax effective rate.

Game Center changes, too. Apple said that on August 4, a new certificate for server-based Game Center verification will be available via the publicKeyUrl.

Robinhood stock jumped more than 24% to $46.80 on Tuesday after initially falling 8% on its first day of trading last week, after which it had continued to trade below its opening price of $38.

Square’s Cash app nearly doubled its gross profit to $546 million in Q2, but also reported a $45 million impairment loss on its bitcoin holdings.

Coinbase’s app now lets you buy your cryptocurrency using Apple Pay. The company previously made its Coinbase Card compatible with Apple Pay in June.

An anonymous app called Sendit, which relies on Snap Kit to function, is climbing the charts of the U.S. App Store after Snap suspended similar apps, YOLO and LMK. Snap was sued by the parent of child who was bullied through those apps, which led to his suicide. Sendit also allows for anonymity, and reviews compare it to YOLO. But some reviews also complained about bullying. This isn’t the first time Snap has been involved in a lawsuit related to a young person’s death related to its app. The company was also sued for its irresponsible “speed filter” that critics said encouraged unsafe driving. Three young men died using the filter, which captured them doing 123 mph.

TikTok is testing Stories. As Twitter’s own Stories integrations, Fleets, shuts down, TikTok confirmed it’s testing its own Stories product. The TikTok Stories appear in a left-hand sidebar and allow users to post ephemeral images or video that disappear in 24 hours. Users can also comment on Stories, which are public to their mutual friends and the creator. Stories on TikTok may make more sense than they did on Twitter, as TikTok is already known as a creative platform and it gives the app a more familiar place to integrate its effects toolset and, eventually, advertisements.

Facebook has again re-arranged its privacy settings. The company continually moves around where its privacy features are located, ostensibly to make them easier to find. But users then have to re-learn where to go to find the tools they need, after they had finally memorized the location. This time, the settings have been grouped into six top-level categories, but “privacy” settings have been unbundled from one location to be scattered among the other categories.

A VICE report details ban-as-a-service operations that allow anyone to harass or censor online creators on Instagram. Assuming you can find it, one operation charged $60 per ban, the listing says.

TikTok merged personal accounts with creator accounts. The change means now all non-business accounts on TikTok will have access to the creator tools under Settings, including Analytics, Creator Portal, Promote and Q&A. TikTok shared the news directly with subscribers of its TikTok Creators newsletter in August, and all users will get a push notification alerting them to the change, the company told us.

Discord now lets users customize their profile on its apps. The company added new features to its iOS and Android apps that let you add a description, links and emojis and select a profile color. Paid subscribers can also choose an image or GIF as their banner.

Twitter Spaces added a co-hosting option that allows up to two co-hosts to be added to the live audio chat rooms. Now Spaces can have one main host, two co-hosts and up to 10 speakers. Co-hosts have all the moderation abilities as hosts, but can’t add or remove others as co-hosts.

Tencent reopened new user sign-ups for its WeChat messaging app, after having suspended registrations last week for unspecified “technical upgrades.” The company, like many other Chinese tech giants, had to address new regulations from Beijing impacting the tech industry. New rules address how companies handle user data collection and storage, antitrust behavior and other checks on capitalist “excess.” The gaming industry is now worried it’s next to be impacted, with regulations that would restrict gaming for minors to fight addiction.

WhatsApp is adding a new feature that will allow users to send photos and videos that disappear after a single viewing. The Snapchat-inspired feature, however, doesn’t alert you if the other person takes a screenshot — as Snap’s app does. So it may not be ideal for sharing your most sensitive content.

Telegram’s update expands group video calls to support up to 1,000 viewers. It also announced video messages can be recorded in higher quality and can be expanded, regular videos can be watched at 0.5 or 2x speed, screen sharing with sound is available for all video calls, including 1-on-1 calls, and more.

American Airlines added free access to TikTok aboard its Viasat-equipped aircraft. Passengers will be able to watch the app’s videos for up to 30 minutes for free and can even download the app if it’s not already installed. After the free time, they can opt to pay for Wi-Fi to keep watching. Considering how easy it is to fall into multi-hour TikTok viewing sessions without knowing it, the addition of the addictive app could make long plane rides feel shorter. Or at least less painful.

Chinese TikTok rival Kuaishou saw stocks fall by more than 15% in Hong Kong, the most since its February IPO. The company is another victim of an ongoing market selloff triggered by increasing investor uncertainty related to China’s recent crackdown on tech companies. Beijing’s campaign to rein in tech has also impacted Tencent, Alibaba, Jack Ma’s Ant Group, food delivery company Meituan and ride-hailing company Didi. Also related, Kuaishou shut down its controversial app Zynn, which had been paying users to watch its short-form videos, including those stolen from other apps.

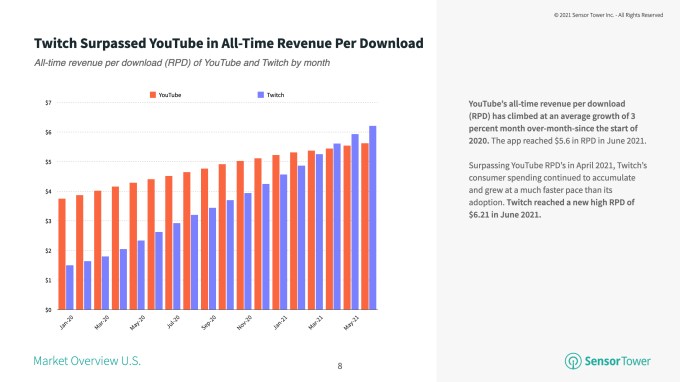

Twitch overtook YouTube in consumer spending per user in April 2021, and now sees $6.20 per download as of June compared with YouTube’s $5.60, Sensor Tower found.

Image Credits: Sensor Tower

Spotify confirmed tests of a new ad-supported tier called Spotify Plus, which is only $0.99 per month and offers unlimited skips (like free users get on the desktop) and the ability to play the songs you want, instead of only being forced to use shuffle mode.

The company also noted in a forum posting that it’s no longer working on AirPlay2 support, due to “audio driver compatibility” issues.

Mark Cuban-backed audio app Fireside asked its users to invest in the company via an email sent to creators which didn’t share deal terms. The app has yet to launch.

YouTube kicks off its $100 million Shorts Fund aimed at taking on TikTok by providing creators with cash incentives for top videos. Creators will get bonuses of $100 to $10,000 based on their videos’ performance.

Match Group announced during its Q2 earnings it plans to add to several of the company’s brands over the next 12 to 24 months audio and video chat, including group live video, and other livestreaming technologies. The developments will be powered by innovations from Hyperconnect, the social networking company that this year became Match’s biggest acquisition to date when it bought the Korean app maker for a sizable $1.73 billion. Since then, Match was spotted testing group live video on Tinder, but says that particular product is not launching in the near-term. At least two brands will see Hyperconnect-powered integrations in 2021.

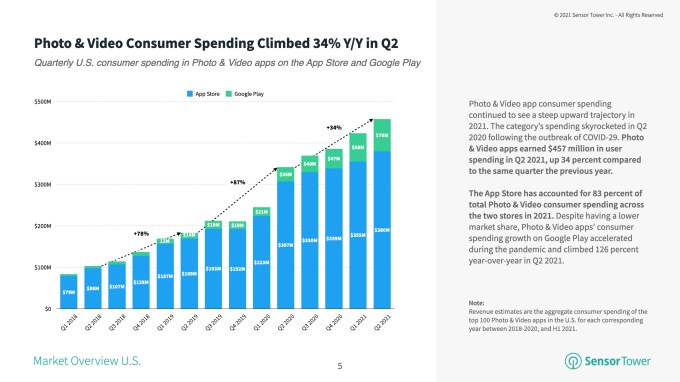

The Photo & Video category on U.S. app stores saw strong growth in the first half of the year, a Sensor Tower report found. Consumer spend among the top 100 apps grew 34% YoY to $457 million in Q2 2021, with the majority of the revenue (83%) taking place on iOS.

Image Credits: Sensor Tower

Epic Games revealed the host of its in-app Rift Tour event is Ariana Grande, in the event that runs August 6-8.

Pokémon GO influencers threatened to boycott the game after Niantic removed the COVID safety measures that had allowed people to more easily play while social distancing. Niantic’s move seemed ill-timed, given the Delta variant is causing a new wave of COVID cases globally.

Apple kicked out an app called Unjected from the App Store. The new social app billed itself as a community for the unvaccinated, allowing like-minded users to connect for dating and friendships. Apple said the app violated its policies for COVID-19 content.

Google Pay expanded support for vaccine cards. In Australia, Google’s payments app now allows users to add their COVID-19 digital certification to their device for easy access. The option is available through Google’s newly updated Passes API which lets government agencies distribute digital versions of vaccine cards.

COVID Tech Connect, a U.S. nonprofit initially dedicated to collecting devices like phones and tablets for COVID ICU patients, has now launched its own app. The app, TeleHome, is a device-agnostic, HIPAA-compliant way for patients to place a video call for free at a time when the Delta variant is again filling ICU wards, this time with the unvaccinated — a condition that sometimes overlaps with being low-income. Some among the working poor have been hesitant to get the shot because they can’t miss a day of work, and are worried about side effects. Which is why the Biden administration offered a tax credit to SMBs who offered paid time off to staff to get vaccinated and recover.

Popular journaling app Day One, which was recently acquired by WordPress.com owner Automattic, rolled out a new “Concealed Journals” feature that lets users hide content from others’ viewing. By tapping the eye icon, the content can be easily concealed on a journal by journal basis, which can be useful for those who write to their journal in public, like coffee shops or public transportation.

Recently IPO’d language learning app Duolingo is developing a math app for kids. The company says it’s still “very early” in the development process, but will announce more details at its annual conference, Duocon, later this month.

Educational publisher Pearson launched an app that offers U.S. students access to its 1,500 titles for a monthly subscription of $14.99. the Pearson+ mobile app (ack, another +), also offers the option of paying $9.99 per month for access to a single textbook for a minimum of four months.

Quora jumps into the subscription economy. Still not profitable from ads alone, Quora announced two new products that allow its expert creators to monetize their content on its service. With Quora+ ($5/mo or $50/yr), subscribers can pay for any content that a creator paywalls. Creators can choose to enable a adaptive paywall that will use an algorithm to determine when to show the paywall. Another product, Spaces, lets creators write paywalled publications on Quora, similar to Substack. But only a 5% cut goes to Quora, instead of 10% on Substack.

Google Maps on iOS added a new live location-sharing feature for iMessage users, allowing them to more easily show your ETA with friends and even how much battery life you have left. The feature competes with iMessage’s built-in location-sharing feature, and offers location sharing of 1 hour up to 3 days. The app also gained a dark mode.

Controversial crime app Citizen launched a $20 per month “Protect” service that includes live agent support (who can refer calls to 911 if need be). The agents can gather your precise location, alert your designated emergency contacts, help you navigate to a safe location and monitor the situation until you feel safe. The system of live agent support is similar to in-car or in-home security and safety systems, like those from ADT or OnStar, but works with users out in the real world. The controversial part, however, is the company behind the product: Citizen has been making headlines for launching private security fleets outside law enforcement, and recently offered a reward in a manhunt for an innocent person based on unsubstantiated tips.

Square announced its acquisition of the “buy now, pay later” giant AfterPay in a $29 billion deal that values the Australian firm at more than 30% higher than the stock’s last closing price of AUS$96.66. AfterPay has served over 16 million customers and nearly 100,000 merchants globally, to date, and comes at a time when the BNPL space is heating up. Apple has also gotten into the market recently with an Affirm partnership in Canada.

Square announced its acquisition of the “buy now, pay later” giant AfterPay in a $29 billion deal that values the Australian firm at more than 30% higher than the stock’s last closing price of AUS$96.66. AfterPay has served over 16 million customers and nearly 100,000 merchants globally, to date, and comes at a time when the BNPL space is heating up. Apple has also gotten into the market recently with an Affirm partnership in Canada.

Gaming giant Zynga acquired Chinese game developer StarLark, the team behind the mobile golf game Golf Rival, from Betta Games for $525 million in both cash and stock. Golf Rival is the second-largest mobile golf game behind Playdemic’s Golf Clash, and EA is in the process of buying that studio for $1.4 billion.

U.K.-based Humanity raised an additional $2.5 million for its app that claims to help slow down aging, bringing the total raise to date to $5 million. Backers include Calm’s co-founders, MyFitness Pal’s co-founder and others in the health space. The app works by benchmarking health advice against real-world data, to help users put better health practices into action.

U.K.-based Humanity raised an additional $2.5 million for its app that claims to help slow down aging, bringing the total raise to date to $5 million. Backers include Calm’s co-founders, MyFitness Pal’s co-founder and others in the health space. The app works by benchmarking health advice against real-world data, to help users put better health practices into action.

YELA, a Cameo-like app for the Middle East and South Asia, raised $2 million led by U.S. investors that include Tinder co-founder Justin Mateen and Sean Rad, general partner of RAD Fund. The app is focusing on signing celebrities in the regions it serves, where smartphone penetration is high and over 6% of the population is under 35.

London-based health and wellness app maker Palta raised a $100 million Series B led by VNV Global. The company’s products include Flo.Health, Simple Fasting, Zing Fitness Coach and others, which reach a combined 2.4 million active, paid subscribers. The funds will be used to create more mobile subscription products.

Emoji database and Wikipedia-like site Emojipedia was acquired by Zedge, the makers of a phone personalization app offering wallpapers, ringtones and more to 35 million MAUs. Deal terms weren’t disclosed. Emojipedia says the deal provides it with more stability and the opportunity for future growth. For Zedge, the deal provides ….um, a popular web resource it thinks it can better monetize, we suspect.

….um, a popular web resource it thinks it can better monetize, we suspect.

Mental health app Revery raised $2 million led by Sequoia Capital India’s Surge program for its app that combines cognitive behavioral therapy for insomnia with mobile gaming concepts. The company will focus on other mental health issues in the future.

London-based Nigerian-operating fintech startup Kuda raised a $55 million Series B, valuing its mobile-first challenger bank at $500 million. The inside round was co-led by Valar Ventures and Target Global.

Vietnamese payments provider VNLife raised $250 million in a round led by U.S.-based General Atlantic and Dragoneer Investment Group. PayPal Ventures and others also participated. The round values the business at over $1 billion.

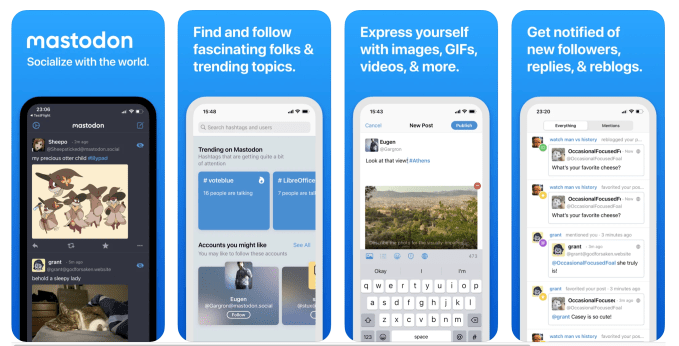

Fans of decentralized social media efforts now have a new app. The nonprofit behind the open source decentralized social network Mastodon released an official iPhone app, aimed at making the network more accessible to newcomers. The app allows you to find and follow people and topics; post text, images, GIFs, polls, and videos; and get notified of new replies and reblogs, much like Twitter.

Xingtu

@_666eveITS SO COOL FRFR do u guys want a tutorial? #fypシ #醒图 #醒图app♬ original sound – Ian Asher

TikTok users are teaching each other how to switch over to the Chinese App Store in order to get ahold of the Xingtu app for iOS. (An Android version is also available.) The app offers advanced editing tools that let users edit their face and body, like FaceTune, apply makeup, add filters and more. While image-editing apps can be controversial for how they can impact body acceptance, Xingtu offers a variety of artistic filters which is what’s primarily driving the demand. It’s interesting to see the lengths people will go to just to get a few new filters for their photos — perhaps making a case for Instagram to finally update its Post filters instead of pretending no one cares about their static photos anymore.

Facebook still dominating top charts, but not the No. 1 spot:

Not cool, Apple:

This user acquisition strategy:

Maybe Stories don’t work everywhere:

Powered by WPeMatico

Small businesses have traditionally been underserved when it comes to IT — they are too big and have too many requirements that can’t be met by consumer products, yet are much too small to afford, implement or thoroughly need apps and other IT build for larger enterprises. But when it comes to neobanks, it feels like there is no shortage of options for the SMB market, nor venture funding being invested to help them grow.

In the latest development, Novo, a neobank that has built a service targeting small businesses, has closed a round of $40.7 million, a Series A that it will be using to continue growing its business, and its platform.

The funding is being led by Valar Ventures with Crosslink Capital, Rainfall Ventures, Red Sea Ventures and BoxGroup all participating. The startup is not disclosing valuation, but Novo — originally founded in New York in 2018 but now based out of Miami — has racked up 100,000 SMB customers — which it defines as businesses that make between $25,000 and $100,000 in annualized revenues — and has seen $1 billion in lifetime transactions, with growth accelerating in the last couple of years.

There are a wide variety of options for small businesses these days when it comes to going for a banking solution. They include staying with traditional banks (which are starting to add an increasing number of services and perks to retain small business customers), as well as a variety of fintechs — other neobanks, like Novo — that are building banking and related financial tools to cater to startups and other small businesses.

Just doing a quick search, some of the others targeting the sector include Rho, NorthOne, Lili, Mercury, Brex, Hatch, Anna, Tide, Viva Wallet, Open and many more (and you could argue also players like Amazon, offering other money management and spending tools similar to what neobanks are providing). Some of these are not in the U.S., and some are geared more at startups, or freelancers, but taken together they speak to the opportunity and also the attention that it is getting from the tech industry right now.

As CEO and co-founder Michael Rangel — who hails from Miami — described it to me, one of the key differentiators with Novo is that it’s approaching SMB banking from the point of view of running a small business. By this, he means that typically SMBs are already using a lot of other finance software — on average seven apps per business — to manage their books, payments and other matters, and so Novo has made it easier by way of a “drag and drop” dashboard where an SMB can integrate and view activity across all of those apps in one place. There are “dozens” of integrations currently, he said, and more are being added.

This is the first step, he said. The plan is to build more technology so that the activity between different apps can also be monitored, and potentially automated

“We’re able to see this is your balance and what you should expect,” he said. “The next frontier is to marry the incoming with outgoing. We’re using the funding to build that, and it’s on the roadmap in the next six months.”

Novo has yet to bring cash advances or other lending products into its platform, although those too are on the roadmap, but it is also listening to its customers and watching what they want to do on the platform — another reason why it’s clever to make it easy to for those customers to integrate other services into Novo: not only does that solve a pain point for the customer, but it becomes a pretty clear indicator of what customers are doing, and how you could better cater to that.

Listening to the customers is in itself becoming a happy challenge, it seems. Novo launched quietly enough — between 2018 and the end of 2019, it had picked up only 5,000 accounts. But all that changed during 2020 and the COVID-19 pandemic, which Rangel describes as “just hockey stick growth. We grew like crazy.”

The reason, he said, is a classic example of why incumbent banks have to catch up with the times. Everyone was locked down at home, and suddenly a lot of people who were either furloughed or laid off were “spinning up businesses,” he said, and that led to many of them needing to open bank accounts. But those who tried to do this with high-street banks were met with a pretty significant barrier: you had to go into the bank in person to authenticate yourself, but either the banks were closed, or people didn’t want to travel to them. That paved the way for Novo (and others) to cater to them.

Its customer numbers shot up to 24,000 in the year.

Then other market forces have also helped it. You might recall that banking app Simple was shut down by BBVA ahead of its merger with PNC; but at the same time, it also shut down Azlo, it’s small business banking service. That led to a significant number of users migrating to other services, and Novo got a huge windfall out of that, too.

In the last six months, Novo grew four-fold, and Rangel attributed a lot of that to ex-Azloans looking for a new home.

The fact that there are so many SMB banking providers out there might mean competition, but it also means fragmentation, and so if a startup emerges that seems to be catching on, it’s going to catch something else, too: the eye of investors.

“The ability of the Novo team to grow the company rapidly during a year where businesses have faced unprecedented challenges is impressive,” said Andrew McCormack, founding partner at Valar Ventures, the firm co-founded by Peter Thiel, another big figure in fintech. “Novo tripled its small business customer base in the first half of 2021! Their custom infrastructure and banking platform put them in prime position to expand their services at an even faster pace as we come out of the health crisis. All of us at Valar Ventures are excited to join this team.”

Powered by WPeMatico

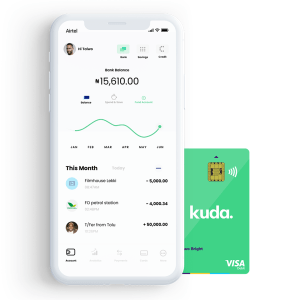

Challenger banks continue to make significant advances in attracting customers away from the big incumbents by providing more modern, user-friendly tools to manage their money. Today, one of the trailblazers in this area, Kuda Technologies, is announcing funding to continue building out its specific ambition: to provide a modern banking service for Africans and the African diaspora, or as co-founder and CEO Babs Ogundeyi describes them, “every African on the planet, wherever you are in the world.”

The company, which currently offers mobile-first banking services in Nigeria, has picked up $25 million in a Series A being led by Valar Ventures, the firm co-founded and backed by Peter Thiel, with Target Global and other unnamed investors participating. This is the first time that Valar — which has invested in a number of fintech startups, including N26, TransferWise, Stash and, just in the last week, BlockFi and BitPanda — has backed an African startup.

Kuda currently provides services for consumers to save and spend money, and it has recently introduced overdrafts (essentially revolving credit for individuals). Ogundeyi said in an interview that the plan is to use these new funds to continue expanding its credit offerings, to build out services for businesses, to add in more integrations and to move into more markets.

The funding is coming on the heels of very strong growth for Kuda, which is co-headquartered in London and Lagos.

When we last wrote about the startup, four months ago, it had just closed a seed round of $10 million led by Target Global. That was, at the time — and I think still is — the largest-ever seed round raised by a startup out of Africa, and thus as much of a milestone for the tech industry there as it was for Kuda itself.

At the time of the seed round, Kuda had registered 300,000 customers: now, that figure has more than doubled to 650,000, and tellingly, that base is spending more money through the Kuda app.

“In November we were doing about $500 million in transactions per month,” Ogundeyi said, for services like bill payments, card transactions and phone top-ups. “We closed February at $2.2 billion.”

Image Credits: Kuda

Kuda, as we described in our profile of the company when covering its seed round, is following in the footsteps of a number of other so-called “neobanks”, building a suite of banking services with a more accessible user interface and a more modern approach: you interact with the bank using a mobile app, and in addition to basic banking services, it provides tools to help people manage their money more intelligently.

But Kuda is also different from many of these, specifically because it taps into some financial practices that are unique to its market.

As Ogundeyi describes it, most people who are employed by companies will have “salary accounts” at banks, where companies pay in a person’s wages on a regular basis. These will typically be at incumbent banks, but they do not offer the same ranges of services to customers. No mobile apps, no facilities to buy mobile top-ups or make other kinds of bill payments, no AI-based calculators to figure out your monthly spend and provide suggestions on how to manage your budget, and so on.

That has opened a gap in the market for others to provide those services in their place. Kuda’s deposits, Ogundeyi said, typically start as basic transfers that people make from those “salary accounts” elsewhere. These start out small, maybe 20% of a person’s wages, but as those users find themselves using Kuda’s payment and other tools more, they are increasing how much they transfer in each payment period.

“As the trust increases you’re naturally more comfortable having money with Kuda,” he said. The next stage from that will be people depositing money directly with Kuda. A small minority already do this, he added, although the startup “has a bit more work to do” to get more companies integrated into its platform. (This is one of the areas that will be developed with this latest round of funding.)

In turn, having more money in Kuda accounts is likely to spur another wave of services being turned on at the startup, such as loans with more competitive interest rates, because they will not just be based on how much money people have but also their spending histories on the platform. “We can offer loans to salaried customers instantly as long as their salary is with Kuda,” he said.

Much of this is being enabled because of how Kuda is built. A lot of challenger banks have tapped into a world of finance and banking APIs built by another wave of fintech startups, partnering with other banks to provide backend deposit and other services: their value-add is in building efficient customer service and tools to help people manage and borrow money in smarter ways.

Kuda, on the other hand, has its own microfinance banking license from the central bank of Nigeria. This means that on top of building those same money management services, Kuda can also issue debit cards (in partnership with Visa and Mastercard), manage payments and transfers, and build all of the services in the stack itself, including those salary account services and loans. (Kuda does have partnerships with incumbent banks, specifically Zenith Bank, Guaranteed Trust and Access Bank, for people to come in for physical deposits and withdrawals when needed.)

While the service is still only live in Nigeria, the “vision is still to serve all Africans in Africa as well as outside of it,” Ogundeyi said.

The first step of that will likely be Nigerians outside of Nigeria — most likely in the U.K., where Kuda already has a headquarters, and where it has a ready market: London alone has been estimated to be home to upwards of 1 million Nigerian immigrants and people of Nigerian descent (the number of U.K. residents actually born in Nigeria is considerably smaller, more like 200,000: that is the diaspora at work).

He added that the startup is also at work on preparing for the next countries on the continent to expand its service, another area where this funding will go: “It will let us fast-track teams, on-the-ground operational teams,” he said.

The bigger picture is that the market for financial services targeting Africans has been on a significant upswing and so we will be seeing a lot more activity coming out of the region, not just from home-grown startups, but also out of other tech companies increasingly doing more business in that part of the world.

Cases in point: In addition to Stripe acquiring Nigerian payments company Paystack last year, just earlier this week, PayPal announced a deal with Flutterwave to bring PayPal services to more merchants in the region — specifically so that PayPal customers can pay merchants in the region using PayPal rails. Square’s CEO, Jack Dorsey, meanwhile, never did make his intended move to the continent — COVID-19 has derailed many plans, as we all know — but it shows that the company is trying not to overlook opportunities there, either.

PayPal, to be clear, has been active in Nigeria since 2014, but partnering with a significant player in the region represents an important step for it: Flutterwave itself earlier this month raised $170 million and became Africa’s latest unicorn, in what is still a pretty small list.

The fact that there is so much more to be done with payments and more financial services leaves the door open wide for Kuda to move in a number of different directions if it chooses. Having customers in two countries, especially with one foot in the developed market and another in an emerging market, for example, gives the company an interesting window into the world of remittances.

Money transfer has been one of the very biggest, and most important financial services for African diasporas — alongside those from many other emerging markets.

Even in cases where people are “unbanked” and have no other financial footprints, they have been turning to remittance services to send money home to their families from abroad. Kuda, with its integrations into people’s salaries, could easily become an efficient, one-stop-shop conduit for that activity too. (That’s one reason, likely, that remittance startup, Remitly, has also moved into starting to offer accounts to its users in originating countries.)

All of this to say that Valar’s making a new kind of bet here, but one laden with possibilities and a differentiated approach compared to the rest of its investment activities.

“Nigeria is at a tipping point in the adoption of digital banking,” noted Andrew McCormack, a general partner and co-founder at Valar, who led its investment here. “With the rapidly growing, youthful population who are open to new financial alternatives, Kuda is well-positioned to benefit and will transform the landscape of African banking. We are excited to lead their Series A and continue on the journey alongside Kuda.”

Powered by WPeMatico

With nearly half a million customers across Mexico and a network of 30,000 retail locations where representatives can take deposits, the challenger bank albo is already on its way to becoming a dominant player in Mexico’s emerging fintech industry.

And the company has recently raised another $45 million to consolidate its position.

“When your mission is to build the biggest bank in Mexico, you will need a ton of money,” said albo founder Angel Sahagún.

The company received its license to operate as a full depository bank in Mexico, and is slowly working toward being the premier internet-based financial services provider for Mexico’s large and growing middle class, Sahagún said.

“We are targeting a similar target market to Chime,” the albo founder and chief executive said. “We are targeting people who are underbanked and don’t have access to all the financial products in the market.”

Sahagún said the money will be used to expand into lending and insurance products the range of services albo offers. That’s a path that has already produced one multi-billion-dollar business in Nubank, Brazil’s wildly successful fintech company, which planted a flag for a new generation of Latin American startups.

While many challenger banks in the region pursued a strategy targeting upper-class and upper-middle-class consumers, Sahagún said his service had chosen a different path.

The company is trying to bring the middle and low-income Mexican consumers into the banking system by making it easy for them to move from a cash-based world to a digital one. “Where 90% of transactions are cash-based you need a value proposition that fits very well on that cash-based society,” Sahagún said.

It’s why the company set up a network of 30,000 locations, including convenience stores and drug stores, so that it can accept deposits at the places where its customers frequent.

That growth, and the company’s 40% share of the digital banking market in Mexico, according to data from Apptopia cited by the company, is why investors like Valar Ventures, Greyhound Capital, Mountain Nazca and Flourish Ventures were willing to invest as part of the $45 million round.

“albo has proven its ability to drive sustainable growth and is leading the market. This is the team that is going to transform banking in the region and we are proud to be supporting them in that,” said James Fitzgerald of Valar Ventures, in a statement.

Powered by WPeMatico

Last year, we told you about a New York-based startup that had begun lending cold, hard, cash to cryptocurrency holders who don’t want to offload their holdings but also don’t necessarily want so much of their assets tied up in cryptocurrencies.

Today, that two-year-old company, BlockFi, is announcing $18.3 million in Series A funding led by Peter Thiel’s Valar Ventures, with participation from Winklevoss Capital, Morgan Creek Digital, Akuna Capital and earlier backers Galaxy Digital Ventures and ConsenSys Ventures.

Apparently, BlockFi is gaining some traction.

Last year, after raising $1.5 million in seed funding from ConsenSys Ventures, SoFi and Kenetic Capital, it secured $50 million led by Galaxy Digital Ventures (the digital currency and blockchain tech firm founded by famed investor Mike Novogratz) that is used to loan out cash to customers who use their bitcoin and ethereum holdings as collateral.

The minimum deposit required: $20,000 worth of cryptocurrency.

According to founder Zac Prince, who talked with Bloomberg about BlockFi’s newest round, enough people are now using those loans that BlockFi has seen its monthly revenue grow more than 10 times since January.

No doubt the uptick in loans correlates with the rebound in Bitcoin’s value, which was priced as low as $3,400 earlier this year but is now valued at roughly $11,400.

Prince also told the outlet that he expects annual revenue to hit eight figures by the end of this year. In startup land, that means it’s time to roll out new money-making services. BlockFi already introduced a savings account product earlier this year that it says enables investors to earn interest on their assets. They are not backed by the FDIC, though the company says it “operates with a focus on compliance with U.S. laws and regulations.” And while it won’t say exactly what’s coming up next, it says in a statement about the new round more products are being added to its existing platform.

Prince previously spent roughly five years in consumer lending and began investing his own money in crypto in early 2016.

He told us last year that his “lightbulb moment” for the company came as he was in the process of getting a loan for an investment property. Instead of using a traditional bank, he decided to list his crypto holdings to see what would happen, and the response was overwhelming. “I realized that there was no debt or credit outside of [person-to-person] margin lending on a few exchanges, and I had the feeling that this was a big opportunity that I was well-suited to go after.”

Other companies providing crypto-backed loans that are issued in fiat currencies include CoinLoan, SALT Lending, Nexo.io and Celsius Network, among others.

Powered by WPeMatico

We’re three weeks into January. We’ve recovered from our CES hangover and, hopefully, from the CES flu. We’ve started writing the correct year, 2019, not 2018.

Venture capitalists have gone full steam ahead with fundraising efforts, several startups have closed multi-hundred million dollar rounds, a virtual influencer raised equity funding and yet, all anyone wants to talk about is Slack’s new logo… As part of its public listing prep, Slack announced some changes to its branding this week, including a vaguely different looking logo. Considering the flack the $7 billion startup received instantaneously and accusations that the negative space in the logo resembled a swastika — Slack would’ve been better off leaving its original logo alone; alas…

On to more important matters.

Rubrik more than doubled its valuation

The data management startup raised a $261 million Series E funding at a $3.3 billion valuation, an increase from the $1.3 billion valuation it garnered with a previous round. In true unicorn form, Rubrik’s CEO told TechCrunch’s Ingrid Lunden it’s intentionally unprofitable: “Our goal is to build a long-term, iconic company, and so we want to become profitable but not at the cost of growth,” he said. “We are leading this market transformation while it continues to grow.”

Deal of the week: Knock gets $400M to take on Opendoor

Will 2019 be a banner year for real estate tech investment? As $4.65 billion was funneled into the space in 2018 across more than 350 deals and with high-flying startups attracting investors (Compass, Opendoor, Knock), the excitement is poised to continue. This week, Knock brought in $400 million at an undisclosed valuation to accelerate its national expansion. “We are trying to make it as easy to trade in your house as it is to trade in your car,” Knock CEO Sean Black told me.

While we’re on the subject of VCs’ favorite industries, TechCrunch cybersecurity reporter Zack Whittaker highlights some new data on venture investment in the industry. Strategic Cyber Ventures says more than $5.3 billion was funneled into companies focused on protecting networks, systems and data across the world, despite fewer deals done during the year. We can thank Tanium, CrowdStrike and Anchorfree’s massive deals for a good chunk of that activity.

Send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I would be remiss not to highlight a slew of venture firms that made public their intent to raise new funds this week. Peter Thiel’s Valar Ventures filed to raise $350 million across two new funds and Redpoint Ventures set a $400 million target for two new China-focused funds. Meanwhile, Resolute Ventures closed on $75 million for its fourth early-stage fund, BlueRun Ventures nabbed $130 million for its sixth effort, Maverick Ventures announced a $382 million evergreen fund, First Round Capital introduced a new pre-seed fund that will target recent graduates, Techstars decided to double down on its corporate connections with the launch of a new venture studio and, last but not least, Lance Armstrong wrote his very first check as a VC out of his new fund, Next Ventures.

More money goes toward scooters

In case you were concerned there wasn’t enough VC investment in electric scooter startups, worry no more! Flash, a Berlin-based micro-mobility company, emerged from stealth this week with a whopping €55 million in Series A funding. Flash is already operating in Switzerland and Portugal, with plans to launch into France, Italy and Spain in 2019. Bird and Lime are in the process of raising $700 million between them, too, indicating the scooter funding extravaganza of 2018 will extend into 2019 — oh boy!

TechCrunch’s Josh Constine introduced readers to Squad this week, a screensharing app for social phone addicts.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I marveled at the dollars going into scooter startups, discussed Slack’s upcoming direct listing and debated how the government shutdown might impact the IPO market.

Powered by WPeMatico

The working class of the United States doesn’t get many breaks these days. It’s not just a function of low pay and long hours, but also the incredible uncertainty of income and expenses that makes surviving week-to-week so challenging. One in five Americans have a negative net wealth, even in an economy where the unemployment rate is the lowest in almost two decades. Banks, meanwhile, are actively dissuading the working class from banking with them, creating a permanent class of unbanked and underbanked citizens.

For Jon Schlossberg, CEO and co-founder of Even.com, improving the plight of ordinary Americans and their finances is a deeply personal and professional mission. And now that mission has a huge new bucket of capital behind it, with Keith Rabois of Khosla Ventures leading a $40 million Series B round into the Oakland-based startup. Rabois is a return investor, having previously backed the company in its late 2014 seed round. With this latest round of capital, Even.com has now raised $50.5 million.

When Even.com first launched its eponymous app, the goal was to offer income smoothing for workers, helping them avoid usurious payday loans to make ends meet. Since that first launch several years ago, Schlossberg and his team learned that the only way to improve the finances for the working class is to help them budget better — ending the need for loans in the first place. “To do anything with your life, unless you are just born to the right family, you need to spend your money wisely, but we never teach you how to do that,” Schlossberg explained to me.

Last year, Even.com announced that it had stopped evening through its Pay Protection product. Instead, Schlossberg said that Even.com has evolved and wanted to “build a new kind of financial institution with products that fit your life.” It still has a feature it brands as Instapay, which allows users to request their earned pay in advance of their payday.

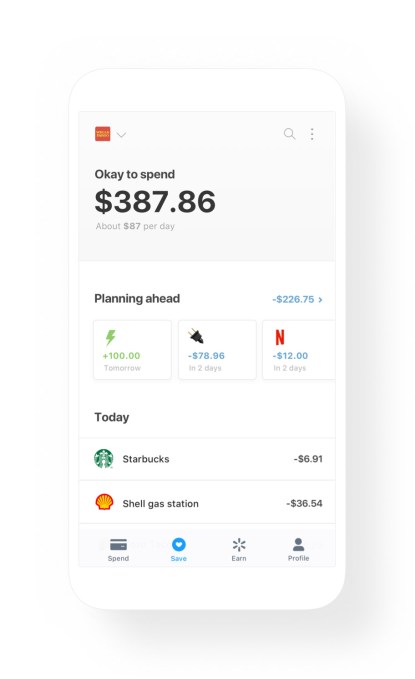

But Even.com is increasingly focused on improving the quality of its intelligent budgeting feature. Using artificial intelligence models honed over the past few years, the company now gives users of its Even app an “Okay to spend” figure that helps them think through their cash flow. By giving a predictive figure rather than a checking account balance, Even can help its users avoid sudden surprise expenses that can trigger the kind of financial death spiral that has become a familiar story in America. The company will also soon launch an automatic savings feature similar to Digit or Acorns that helps people build up regular savings.

Even’s Okay to spend feature gives insight into future cash flows before it is too late

While the company offers an increasingly comprehensive suite of financial tools, it has decided to avoid charging users specific use fees, opting instead for a subscription model. Schlossberg explained that “We are a mission-oriented company, but talk is cheap and where the rubber hits the road, it’s how you make money.” Even is free for users participating through partner employers, or $2.99 a month for individuals without a sponsor.

The company’s highest expense feature is Instapay due to underwriting, and so the company makes higher profits when fewer of its customers need access to payday credit. In other words, the better that its users budget, the fewer loans it will underwrite, and the more money the company makes. We are “directly incentivized to help people with their financial health,” Schlossberg noted.

Even has proven attractive to corporate customers, including Walmart, which partnered with the startup last December to offer its service to all 1.4 million employees at the retailer. Since the launch of that partnership, more than 200,000 Walmart employees regularly use the app, according to Even, and the typical active user checks their Okay to spend balance four times a week. A majority of active users have also taken out an Instapay through Even.

More interestingly, salaried employees at Walmart used the app slightly more than hourly workers, proving that just having a guaranteed income isn’t necessarily a panacea to financial trouble for many American households.

Even.com’s Series B round is all about expansion and growth for the company. Even intends to open an East Coast office this year, and intends to expand its product further into the Fortune 500 with partnerships similar to its Walmart deal. The company currently has 37 employees. In addition to Khosla, the startup raised funding from Valar Ventures, Allen & Company, Harrison Metal, SV Angel, Silicon Valley Bank and others.

Powered by WPeMatico