upsie

Auto Added by WPeMatico

Auto Added by WPeMatico

Four years ago, Brandon Gell was an architecture student who spent most of his time working on 3D printing modular housing. Now, he’s the founder of Clyde, an extended warranty startup that wants to help small e-commerce businesses offer product protection.

Today, the company announced it has raised a $14 million Series A led by Spark Capital with participation from Crosslink, RRE, Rea Sea Ventures and others.

How do you go from being a product person to the founder of an insurance startup? According to Gell: a stint at a four-person 3D scanner startup in Columbus, Ohio.

Because the team and resources were small, Gell was put in charge of finding an insurance company to work with to protect their expensive end product of scanners.

“I spent six months trying to find a company,” he said. After seeing how seamless it was to work with fintech customer support tools from companies like Stripe, Shopify, Affirm and others, he said it was clear that insurance, and especially the extended warranty space, wasn’t as mature. So he set up an office in his grandma’s New York apartment.

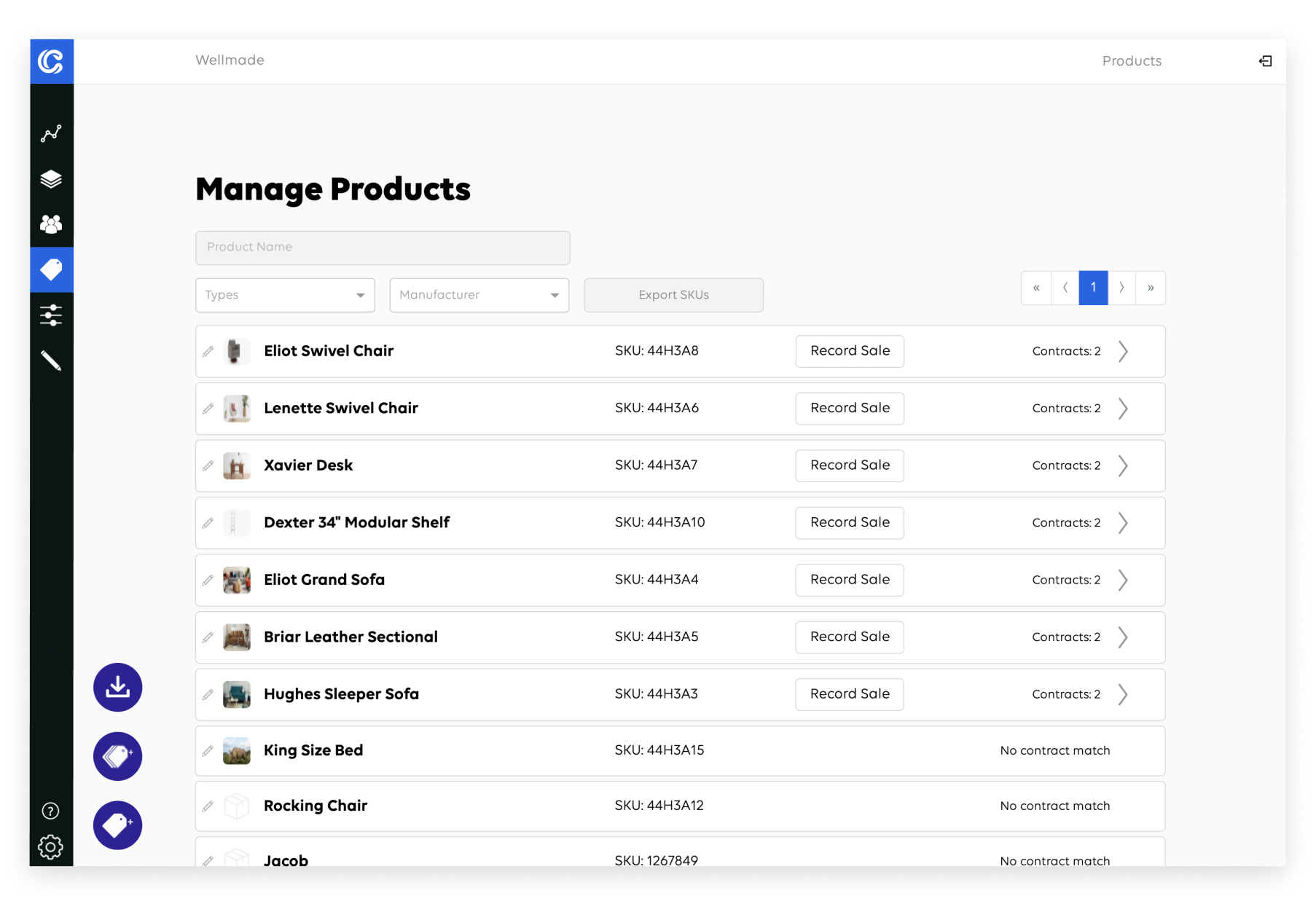

Clyde is a platform that connects small retailers to insurance companies to launch and manage product protection programs.

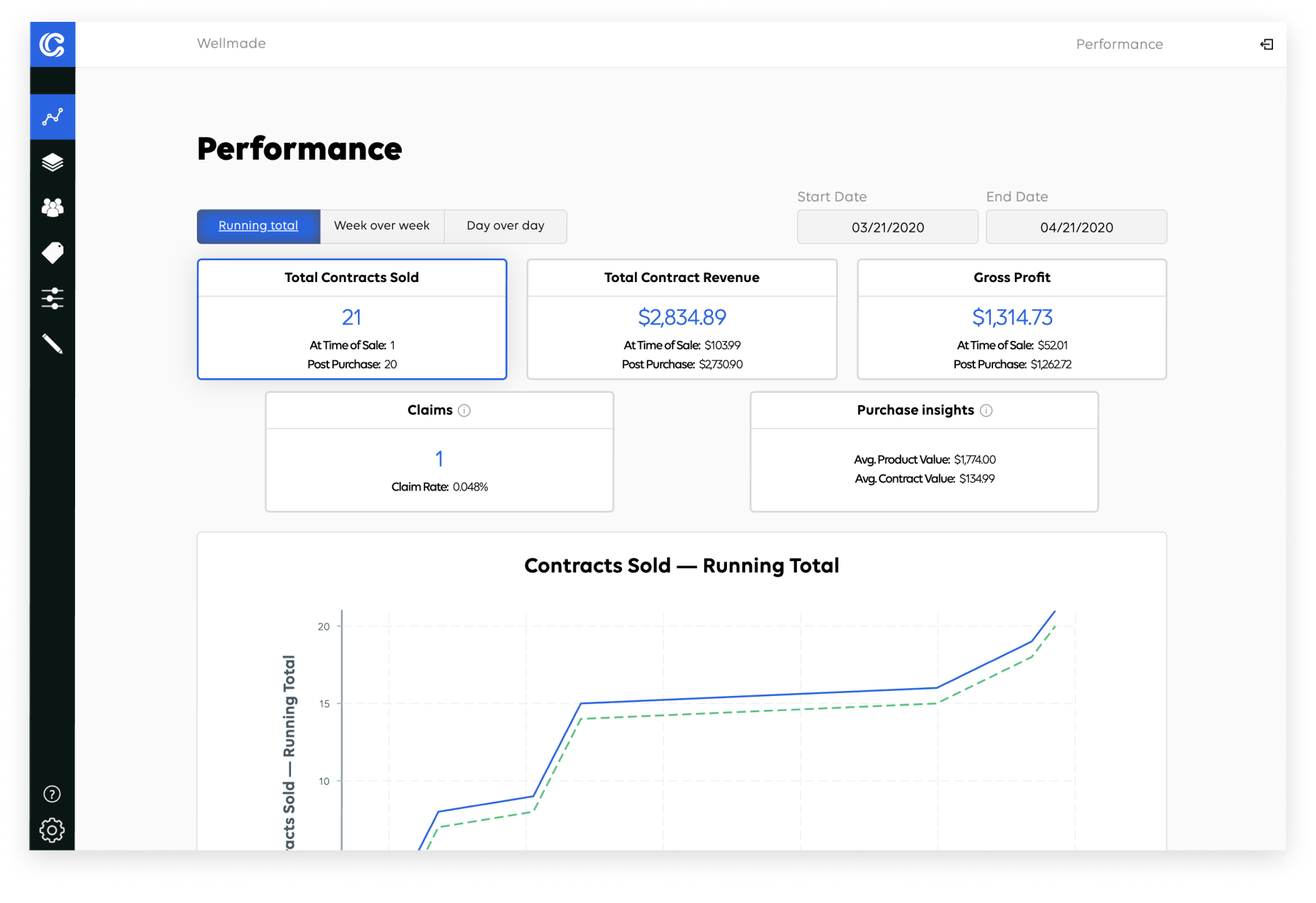

Using Clyde, customers can access a dashboard and e-commerce apps to manage their protection programs. For example, a user can see how many contracts were sold, how much revenue total those bring and gross profit in real time. It also can see which products are most often purchased with an extended warranty contract.

“It’s a similar type of offering as Affirm or Stripe,” he said. “We give you access to large insurance companies and we enable you to launch the program live on your website or physical point of sale and store wherever you sell.” It has plugins with Shopify, BigCommerce, Salesforce, Magento, Woocommerce, and more so store owners on the site can add Clyde to their small businesses.

Clyde’s most critical metric is that it has an 18% attachment rate on average, which means that 18% of people that go through a Clyde-powered purchasing path end up purchasing extended warranties or protection plans.

The reason businesses care about extended warranty is two-fold. First, insurance benefits the customer experience. Second, insurance purchases are often the highest-margin product that companies sell to their customers. Product protection alone is a $50 billion market. Gell said that Best Buy drives about 2% of its annual revenue from the sale of extended warranties, but that generates more than half of its profit.

Clyde helps small businesses, like a four-person startup in Columbus Ohio, get a bite of this profitable pie. Most e-commerce businesses have to work with Amazon, thus giving a lot of that cash to the big company versus putting it in their own pocket, per Gell. He says that when Amazon sells an extended warranty on a seller’s product, it doesn’t share any revenue with the seller on how the product performs, which prevents a seller from both a stream of revenue and data analytics.

“Our sort of mantra is that the retailers that we work with are basically everybody that’s not Amazon and Walmart,” he said.

Clyde’s goal is different from Upsie, another venture-backed startup focusing on warranties. Upsie is looking to be a direct-to-consumer warranty replacement, while Clyde works on behalf of the retailer and insurance company to connect the two parties.

Closer competitors to the startup include Mulberry and Extend, which were both founded after Clyde and have raised less in venture capital funding. Gell thinks his competitive advantage is partnerships with top insurance companies, and a strong product-focused platform. Clyde’s entire founding team is made up of product people.

Startups right now need to prove that they are viable in both a pre-coronavirus and post-coronavirus world. And Clyde might be exactly in that sweet spot, as it focuses on e-commerce businesses.

The Series A round closed a few weeks ago, before the COVID-19 craziness began, but he said that the pandemic has led to more inbounds and interest than ever before. Gell says it’s a mix of e-commerce being more important than ever, and customer behavior.

“It’s a shift of customers that want to buy online more, but also protect their purchases more than ever,” he said. “Companies are realizing how important it is.”

New cash in hand, Clyde’s growing while its customer-base is looking for new ways to bring in revenue and take care of customers. If the startup can handle the influx of attention and importance right, sticky harmony will follow.

Powered by WPeMatico

Warranties for purchased products is a $40 billion annual market. But in their current form, they are considered by some to be one of the bigger scams in the world of retail because they cost so much and often return too little.

Now there is an alternative emerging. A startup out of Minneapolis, Minn. called Upsie has decided to wage war on the old warranty, with more reasonable pricing (typically 70% lower than what the retailer offers) and a much more modern approach to selling and managing the warranty.

Its bet is that lower prices, and more flexible options for ordering, tracking and claiming against warranties, will drive more users to its service and take some business away from the retailers that largely dominate the market today. Today it’s announcing that it has raised $5 million led by True Ventures to build out that business in the U.S. Techstars Ventures, Matchstick Ventures, Syndicate Fund, M25 and angel investor Marc Belton also participated.

If you’ve ever purchased an expensive consumer electronics product, you know the problem that Upsie is tackling: warranties can cost a lot, and in many cases you’re not sure what you might even be getting out of it. And if you do find yourself in the unfortunate predicament of needing to file a claim, you may find the process a little less than efficient, but hopefully not as bad as this:

“If you buy a product worth $900, a warranty might cost an extra $130, but that warranty might cost only $10 from the insurance company,” said Clarence Bethea, the CEO and founder of Upsie.

When an expensive purchase like a consumer electronics product breaks down, the buyer needs to pay out big money for repairs or replacements, and that worry drives many of those customers to pay a big sum for the guarantee that someone else will cover those liabilities.

When an expensive purchase like a consumer electronics product breaks down, the buyer needs to pay out big money for repairs or replacements, and that worry drives many of those customers to pay a big sum for the guarantee that someone else will cover those liabilities.

The operative words in that last paragraph are “big sum”: a warranty can represent peace of mind, and sometimes actually help in those cases where something relatively new does break down, but one of the big issues is the mark-up that providers put on a service that preys on the fear of needing it — in some cases a warranty can cost as much as 900% more than the policy would cost if it were purchased directly from an insurance provider.

Bethea used to be a consultant to big-box retailers and in the work he did, he realised quickly that the retailers were taking advantage of consumers when they were selling warranties on top of products. “Consumers don’t know what the warranties actually cost,” he said. “That’s what pushed me into this.”

Upsie gives consumers the option to purchase warranties up to 60 days after the sale (or 45 for smartphones). The product itself needs a minimum 90-day warranty from the manufacturers themselves, and the Upsie warranty does not kick in until 30 days after it’s purchased — the idea being that it picks up right after the manufacturer warranty ends.

The warranties can be purchased online or through an app and they apply currently to around 15 categories and hundreds of electric goods covering areas like computers, wearables, phones, TVs, small and large appliances and outdoor tools. The Upsie app in itself is like your warranty file in your filing cabinet, except much simpler and lighter and less cluttered: it stores receipts, lets you scan SKUs to register the goods and more to make it easier. Then after a user purchases the warranty, it can be managed and claims can be filed by way of Upsie’s app.

The basic idea behind Upsie is reminiscent of the direct-to-consumer brands that have grown in popularity over the last several years.

Just as these have leveraged the web, mobile apps and more recently social media to build direct relationships with consumers, Upsie is also bypassing retailers and hoping that consumers will consider their cheaper alternatives, which in actuality have been negotiated with the same warranty service providers that the retailers use. It currently works with Centricity, and the plan is to expand it to a wider range over time.

Other companies have built businesses in the area of providing warranty services outside of what retailers offer, such as SquareTrade, which was acquired by AllState, and Asurion. Puneet Agarwal, a partner at True Ventures, believes that it stands out.

“Upsie is the only consumer-facing brand in the space, whereas everyone else is more of a back-end provider,” he said. “Their subscriber growth and engagement are tremendous and the end consumer identifies with them. Because of their direct consumer focus, they also offer a level of pricing, convenience and customer service the industry has not seen.” He added that the “big ambition” is “to make the idea of ‘upsie-ing’ a product as part of the the everyday lexicon of the consumer.”

Bethea said that one of the big early challenges was convincing insurance companies that D2C was a viable idea — which dissipated as insurance companies, like all brands and B2B2C businesses, began to consider the plethora of ways that people are buying goods today, which increasingly extend well outside the realm of just retailers.

The other challenge that is still one that Upsie will continue to work to surmount as it continues growing is convincing consumers to change their behavior. “Initially it was about convincing the industry that this is a market,” he said. “Today it’s awareness and giving consumers another option. ‘I didn’t know I could leave the register and purchase a plan afterwards’ is what we want people to be thinking.”

So far, the results have been pretty positive. Since exiting beta in 2016, Bethea said the company has grown 300% each year. Services are live only in the U.S., and while it works toward expanding to international markets, it will also be adding auto warranties to its plans next.

Living outside of Silicon Valley as I do, companies that are outliers from the normal pattern that often list the same litany of credentials (including but not limited to grads from Stanford or MIT, possible stint at YC, office in San Francisco, past history at other tech companies), but are still thriving, do tend to catch my eye. Upsie, with its roots in the Midwest and an African American founder (also not very common at the typical SV startup), and tackling something that is fundamentally broken but not flashy, ticks some of those boxes.

Turns out that True sees and wants to seek out more of this, too.

“Great companies are being built everywhere,” said Agarwal. “More and more of the companies we invest in are outside of the Valley or are building teams outside of the Valley and we encourage it. It can be a tremendous competitive advantage both from a talent and cost perspective. We have had great success investing in places like Michigan, Montana, Oregon, Wisconsin, Washington, even recently in Africa, and now in Minnesota with Upsie. I still do see a lot of bias from investors not wanting to invest outside of the Valley. There is no question they will miss out not because of high prices in the Valley but because of the opportunity.”

Powered by WPeMatico