United States

Auto Added by WPeMatico

Auto Added by WPeMatico

As renewable energy continues to gobble up more and more of the new energy capacity coming online, the solar project lending company Wunder Capital has raised $112 million in primarily debt financing to boost its business.

The 90 percent debt and 10 percent equity commitment came from the multi-strategy investment firm Cyrus Investments, which has backed renewable energy projects for years through its investment in RePower Group.

“The debt component is going to blow out the lending opportunity,” says Wunder chief executive Bryan Birsic.

Wunder chose to consolidate the debt and equity round with a single lead investor to simplify the negotiation process on both sides of the table, Birsic said. “Since Cyrus is an equity holder in the company we can come to better terms,” on debt facilities and repayment, he said.

Wunder lends money to commercial solar energy development projects throughout the U.S. and its business has been buoyed by a flood of demand for new solar energy projects coming online.

Since its launch in 2016, the company has financed more than 180 projects throughout the U.S., which are generating somewhere in the range of 50 megawatts (or enough electricity to power roughly 32,500 homes).

The Boulder, Colo.-based company makes money in three ways: It charges closing fees, a servicing fee and annual interest rate on the debt it provides — typically Wunder will pull in between 4 percent and 5 percent off of each loan it provides to a project.

And business… for renewable energy… is booming.

For instance, the industry appears to have shaken off concerns over price increases stemming from the tariffs imposed on solar panels as part of broad punitive measures President Trump has taken against China (which supplies most of the world’s solar panels).

“It was really pleasant to see that folks were less reactionary and more responsive to the data,” says Birsic. The headlines, Birsic explains, were worse than the reality for the industry. The headlines in January predicted a 30 percent tariff on solar panels, but banks thought those increases would ultimately result in a 3 percent price increase for residential solar installations and a 4 percent price increase for commercial solar.

Those price increases would only bring costs in line with what they were at the end of 2017, since over the course of the year prices on installations declined 10 percent, Birsic says.

“We’re very cool with the economics as it existed in 2017,” he said.

Powered by WPeMatico

Yesterday brought some interesting news in the cryptocurrency space. In a move that is at once sleazy and ridiculous, PornHub and its tech arm MindGeek announced a partnership with the creators of VergeCoin (XVG), an anonymized cryptocurrency in the vein of Monero that is currently trading at 7 cents, down from an all-time high of about 26 cents during a recent pump.

XVG is an epitome of a coin driven by mania. Originally billed as DogecoinDark in 2014, the currency has had some ups and downs but has always displayed the “move fast and break things” mentality that gives cryptocurrencies a bad name. The product is so hapless it can’t even get their Wikipedia entry right.

The currency developers recently beseeched its rabid fans — many of whom have been waxing confused on Reddit — to raise $2 million to build a secret partnership. Weeks of speculation followed as Vergins speculated about partners, including eBay and Amazon. The price went up and down and has settled below 10 cents, placing it at position 23 on the CoinMarketCap list. It’s doing well, but not great.

Yesterday the big announcement came, as it were. I received a few emails from PornHub PR announcing a crypto partnership but they refused to announce the currency. Now that the currency is officially announced, I’m sure there are some folks who are upset they bought a load of Titcoin.

Verge has partnered with PornHub to allow users to pay with the currency. Why? And why would you want to? This is unclear. Presumably the currency allows you to pay completely anonymously but you still have to acquire Verge to pay with Verge and associating a currency with porn pretty much gives the game away as to why you’d spend it. Further, the extensive marketing efforts make PornHub look far more interesting than Verge, especially since Verge shares the same name with the Verge tech site, something that is bound to confuse average buyers. Finally, you get no real benefit from paying with Verge and, in fact, you can’t get your Verge refunded if you decide you no longer want to pay $9.99 a month for premium PR()N.

Ultimately this is better for porn than it is for cryptocurrency. PornHub gets a little bit of a media boost and cryptocurrencies — including Bitcoin, Ether and ICO tokens — look like the only source for porn. While VHS and the internet grew out of porn, cryptocurrencies are already well-established and they don’t need any more “sin” associated with them. You can also pay for a number of services with crypto, including Flirt4Free, a cam girl site associated with LiveJasmin. Given that a series of stars in big trucks will be rolling through the U.S. over the next few months promoting cryptocurrencies — that $2 million had to go somewhere — it could be positive for crypto uptake but very bad for crypto perception.

While I agree that crypto needs a shot in the arm and a sense of mission, I doubt making it easier to see naked people is quite it. I’d like to see real remittances, real real estate transactions and even real voting systems put in place. Until then, however, stunts like this do little to help.

Powered by WPeMatico

The city of Glendale, Calif. seems like an unlikely place to grow one of the next billion-dollar startups in the booming Los Angeles tech ecosystem.

Located at the southeastern tip of the San Fernando Valley, the Los Angeles suburb counts its biggest employers as the adhesive manufacturer Avery Dennison; the Los Angeles industrial team for the real estate developer CBRE; the International House of Pancakes; Disney Consumer Products; DreamWorks Studios; Walt Disney Animation and Univision. “Silicon Beach” this ain’t.

But it’s here in the (other) Valley’s southernmost edge that investors have found a startup they consider to be the next potential billion-dollar “unicorn” that will come out of Los Angeles. The company is ServiceTitan, and its market… is air conditioners.

More specifically, it’s the contractors that service equipment like the heating, ventilation and cooling systems at commercial and residential properties across the U.S.

Founded by Ara Mahdessian and Vahe Kuzoyan in 2012, ServiceTitan is very much an up-and-coming billion-dollar business that’s a family (minded) affair.

Mahdessian and Kuzoyan met on a ski trip organized by the Armenian student associations at Stanford and the University of Southern California back when both men were in college.

Both programmers, the two reconnected after doing stints as custom developers during and after college, and then when they were developing tools for their families’ businesses as residential contractors in the Los Angeles suburb of Glendale.

The two men built a suite of services to help contractors like their fathers manage their businesses. Now following a $62 million round of funding led by Battery Ventures last month, the company is worth roughly $800 million, according to people with knowledge of the investment, and is on its way to becoming Los Angeles’ next billion-dollar business.

Battery isn’t the only marquee investor to find value in ServiceTitan’s business developing software managing day labor.

Iconiq Capital, the investment firm managing the wealth of some of Silicon Valley’s most successful executives (the firm counts Facebook chief executive Mark Zuckerberg, and senior staff like Dustin Moskovitz and Sheryl Sandberg; Twitter chief Jack Dorsey; and LinkedIn founder and chief executive Reid Hoffman among its clients, according to a 2014 Forbes article), has also taken a shine to the now-gargantuan startup from Glendale.

It was Iconiq that put a whopping $80 million into ServiceTitan just last year — and while the 2017 cash infusion may have been larger, the company’s valuation has continued to rise.

That’s likely due to a continually expanding toolkit that now boasts a customer relationship management system, efficient dispatching and routing, invoice management, mobile applications for field professionals and marketing analytics and reporting tools.

“ServiceTitan’s incredibly fast growth is a testament to the brisk demand for new mobile and cloud-based technology that is purpose-built for the tradesmen and women in our workforce,” said Battery Ventures general partner Michael Brown — who’s taking a seat on the ServiceTitan board.

What distinguishes the ServiceTitan business from other point solutions is that they’ve taken to targeting not mom-and-pop small businesses but franchises like Mr. Rooter and George Brazil. Gold Medal Service, John Moore Services, Hiller Plumbing, Casteel Air, Baker Brothers Plumbing and Air Conditioning and Bonney may not be household names, but they’re large providers of contractors who work under those brands.

The company counts 400 employees on staff, and will look to use the money to continue to grow out its suite of products and services, according to a March statement announcing the funding.

And as Battery Ventures investor Sanjiv Kalevar noted in a blog post last year, the opportunity for software companies serving blue-collar workers is huge.

For people sitting at our desks and working behind laptops on programs like Microsoft Office, it can be easy to overlook the large, sometimes forgotten, workforce out there in construction, manufacturing, transportation, hospitality, retail and many other multi-billion dollar industries. Indeed, more than 60% of U.S. workers and even more globally fall into these “blue collar” industries.

By and large, these workers have not benefitted much from recent technology improvements available to office-based workers—think new email and workplace-collaboration technologies, or advanced sales and HR systems. Never mind the long-term opportunities for companies in these sectors from technologies like artificial intelligence, drones, and virtual or augmented reality; hourly and field workers are dealing with much more basic on-the-job challenges, like finding work, getting their jobs done on time and getting paid. These more basic needs can be solved with seemingly simple technologies—software for billing, scheduling, navigation and many other business workflows. These kinds of technologies, unlike AI, don’t automate away workers. Instead, they empower them to be more efficient and productive.

Powered by WPeMatico

Since the dawn of the internet, the titans of this industry have fought to win the “starting point” — the place that users start their online experiences. In other words, the place where they begin “browsing.” The advent of the dial-up era had America Online mailing a CD to every home in America, which passed the baton to Yahoo’s categorical listings, which was swallowed by Google’s indexing of the world’s information — winning the “starting point” was everything.

As the mobile revolution continues to explode across the world, the battle for the starting point has intensified. For a period of time, people believed it would be the hardware, then it became clear that the software mattered most. Then conversation shifted to a debate between operating systems (Android or iOS) and moved on to social properties and messaging apps, where people were spending most of their time. Today, my belief is we’re hovering somewhere between apps and operating systems. That being said, the interface layer will always be evolving.

The starting point, just like a rocket’s launchpad, is only important because of what comes after. The battle to win that coveted position, although often disguised as many other things, is really a battle to become the starting point of commerce.

Google’s philosophy includes a commitment to get users “off their page” as quickly as possible…to get that user to form a habit and come back to their starting point. The real (yet somewhat veiled) goal, in my opinion, is to get users to search and find the things they want to buy.

Of course, Google “does no evil” while aggregating the world’s information, but they pay their bills by sending purchases to Priceline, Expedia, Amazon and the rest of the digital economy.

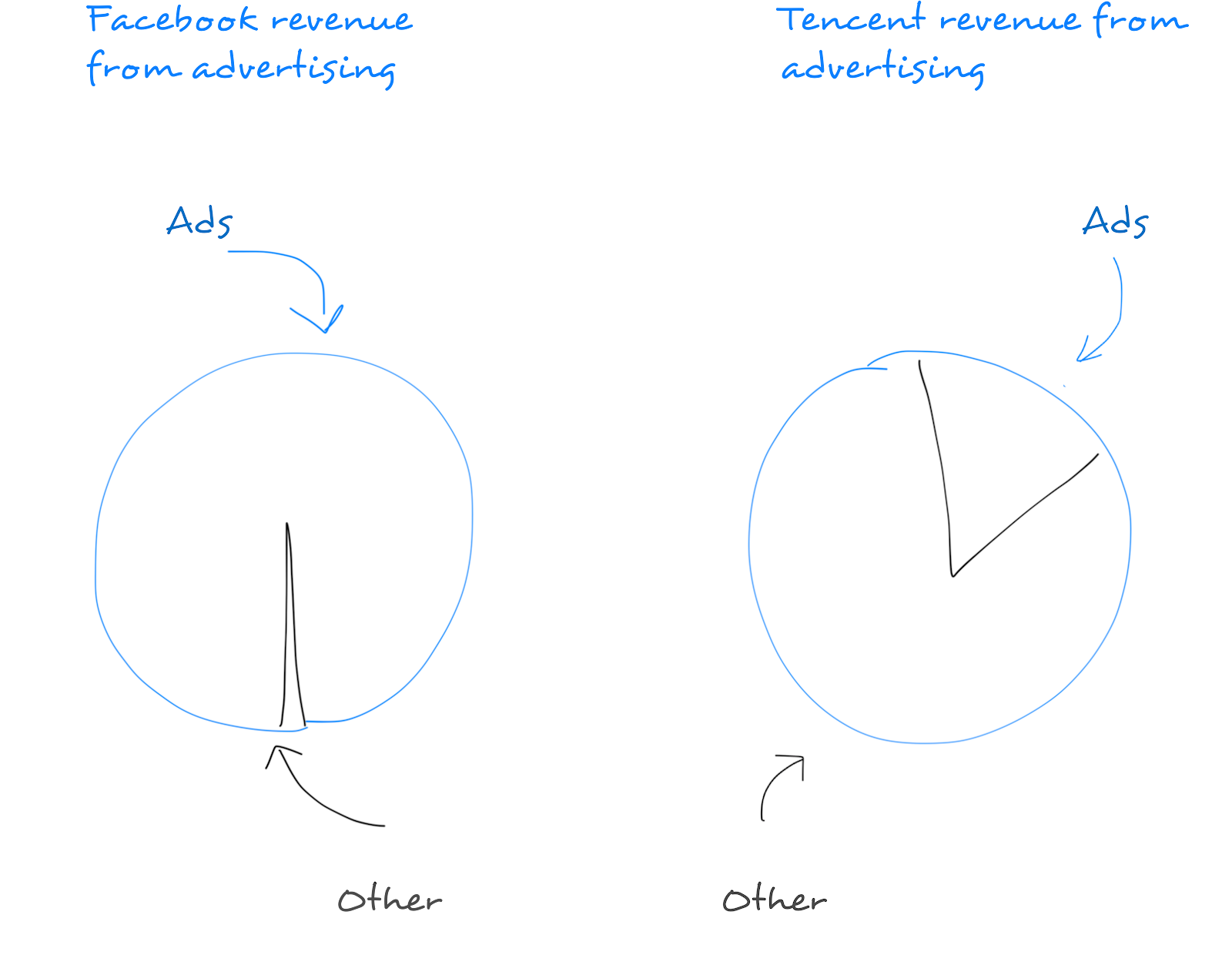

Facebook, on the other hand, has become a starting point through its monopolization of users’ time, attention and data. Through this effort, it’s developed an advertising business that shatters records quarter after quarter.

Google and Facebook, this famed duopoly, represent 89 percent of new advertising spending in 2017. Their dominance is unrivaled… for now.

Change is urgently being demanded by market forces — shifts in consumer habits, intolerable rising costs to advertisers and through a nearly universal dissatisfaction with the advertising models that have dominated (plagued) the U.S. digital economy. All of which is being accelerated by mobile. Terrible experiences for users still persist in our online experiences, deliver low efficacy for advertisers and fraud is rampant. The march away from the glut of advertising excess may be most symbolically seen in the explosion of ad blockers. Further evidence of the “need for a correction of this broken industry” is Oracle’s willingness to pay $850 million for a company that polices ads (probably the best entrepreneurs I know ran this company, so no surprise).

As an entrepreneur, my job is to predict the future. When reflecting on what I’ve learned thus far in my journey, it’s become clear that two truths can guide us in making smarter decisions about our digital future:

Every day, retailers, advertisers, brands and marketers get smarter. This means that every day, they will push the platforms, their partners and the places they rely on for users to be more “performance driven.” More transactional.

Paying for views, bots (Russian or otherwise) or anything other than “dollars” will become less and less popular over time. It’s no secret that Amazon, the world’s most powerful company (imho), relies so heavily on its Associates Program (its home-built partnership and affiliate platform). This channel is the highest performing form of paid acquisition that retailers have, and in fact, it’s rumored that the success of Amazon’s affiliate program led to the development of AWS due to large spikes in partner traffic.

Chinese flag overlooking The Bund, Shanghai, China (Photo: Rolf Bruderer/Getty Images)

When thinking about our digital future, look down and look east. Look down and admire your phone — this will serve as your portal to the digital world for the next decade, and our dependence will only continue to grow. The explosive adoption of this form factor is continuing to outpace any technological trend in history.

Now, look east and recognize that what happens in China will happen here, in the West, eventually. The Chinese market skipped the PC-driven digital revolution — and adopted the digital era via the smartphone. Some really smart investors have built strategies around this thesis and have quietly been reaping rewards due to their clairvoyance.

China has historically been categorized as a market full of knock-offs and copycats — but times have changed. Some of the world’s largest and most innovative companies have come out of China over the past decade. The entrepreneurial work ethic in China (as praised recently by arguably the world’s greatest investor, Michael Moritz), the speed of innovation and the ability to quickly scale and reach meaningful populations have caused Chinese companies to leapfrog the market cap of many of their U.S. counterparts.

The most interesting component of the Chinese digital economy’s growth is that it is fundamentally more “pure” than the U.S. market’s. I say this because the Chinese market is inherently “transactional.” As Andreessen Horowitz writes, WeChat, China’s most valuable company, has become the “starting point” and hub for all user actions. Their revenue diversity is much more “Amazon” than “Google” or “Facebook” — it’s much more pure. They make money off the transactions driven from their platform, and advertising is far less important in their strategy.

The obsession with replicating WeChat took the tech industry by storm two years ago — and for some misplaced reason, everyone thought we needed to build messaging bots to compete.

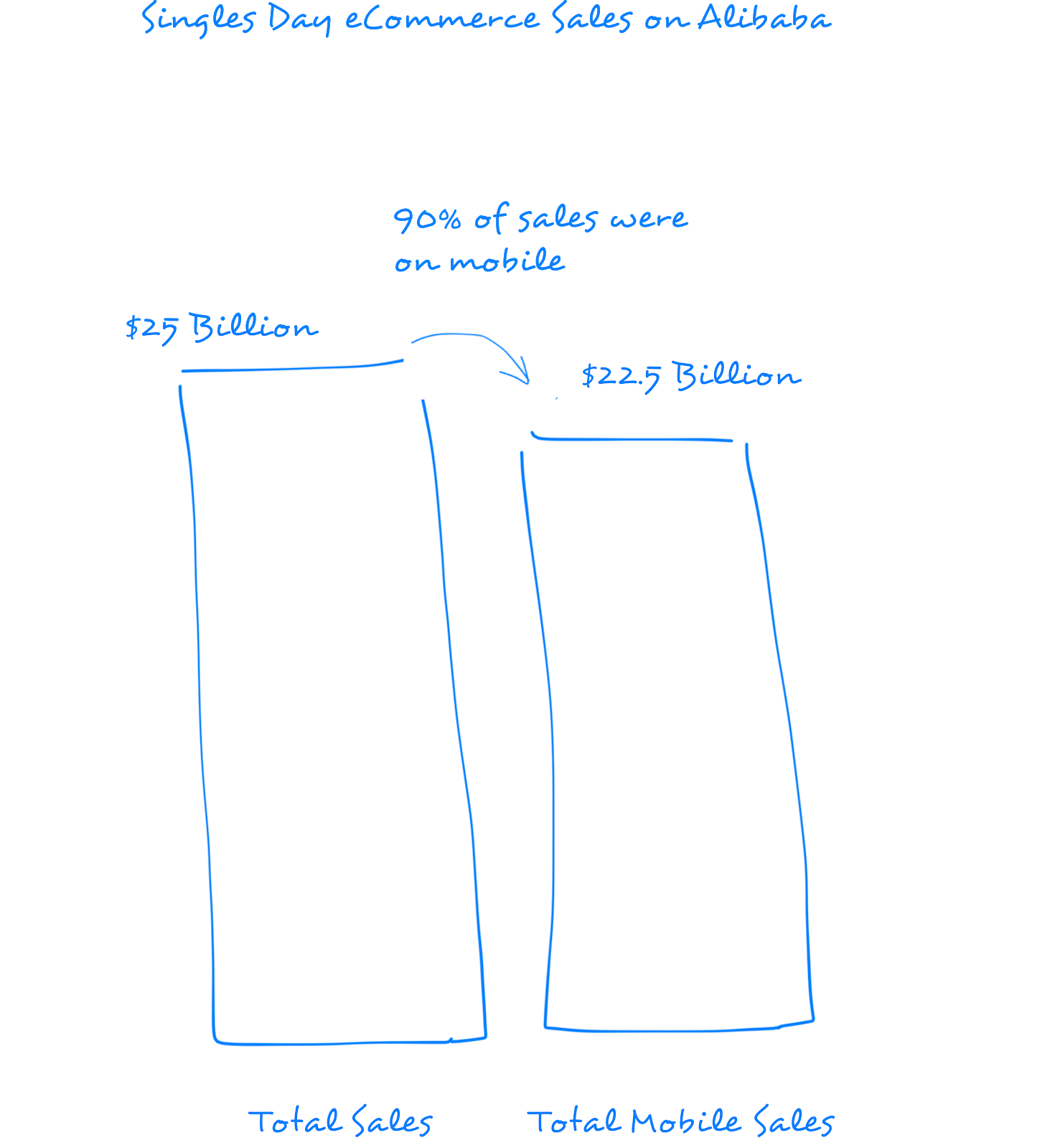

What shouldn’t be lost is our obsession with the purity and power of the business models being created in China. The fabric that binds the Chinese digital economy and has fostered its seemingly boundless growth is the magic combination of commerce and mobile. Singles Day, the Chinese version of Black Friday, drove $25 billion in sales on Alibaba — 90 percent of which were on mobile.

The lesson we’ve learned thus far in both the U.S. and in China is that “consumers spending money” creates the most durable consumer businesses. Google, putting aside all its moonshots and heroic mission statements, is a “starting point” powered by a shopping engine. If you disagree, look at where their revenue comes from…

Google’s recent announcement of Shopping Actions and their movement to a “pay per transaction model” signals a turning point that could forever change the landscape of the digital economy.

Google’s multi-front battle against Apple, Facebook and Amazon is weighted. Amazon is the most threatening. It’s the most durable business of the four — and its model is unbounded on two fronts that almost everyone I know would bet their future on, 1) people buying more online, where Amazon makes a disproportionate amount of every dollar spent, and 2) companies needing more cloud computing power (more servers), where Amazon makes a disproportionate amount of every dollar spent.

To add insult to injury, Amazon is threatening Google by becoming a starting point itself — 55 percent of product searches now originate at Amazon, up from 30 percent just a year ago.

Google, recognizing consumer behavior was changing in mobile (less searching) and the inferiority of their model when compared to the durability and growth prospects of Amazon, needed to respond. Google needed a model that supported boundless growth and one that created a “win-win” for its advertising partners — one that resembled Amazon’s relationship with its merchants — not one that continued to increase costs to retailers while capitalizing on their monopolization of search traffic.

Google knows that with its position as the starting point — with Google.com, Google Apps and Android — it has to become a part of the transaction to prevail in the long term. With users in mobile demanding fewer ads and more utility (demanding experiences that look and feel a lot more like what has prevailed in China), Google has every reason in the world to look down and to look east — to become a part of the transaction — to take its piece.

A collision course for Google and the retailers it relies upon for revenue was on the horizon. Search activity per user was declining in mobile and user acquisition costs were growing quarter over quarter. Businesses are repeatedly failing to compete with Amazon, and unless Google could create an economically viable growth model for retailers, no one would stand a chance against the commerce juggernaut — not the retailers nor Google itself.

As I’ve believed for a long time, becoming a part of the transaction is the most favorable business model for all parties; sources of traffic make money when retailers sell things, and, most importantly, this only happens when users find the things they want.

Shopping Actions is Google’s first ambitious step to satisfy all three parties — businesses and business models all over the world will feel this impact.

Good work, Sundar.

Powered by WPeMatico

The American Midwest has a long history of making stuff. During the 20th century, it was the manufacturing center for the nation, and indeed much of the world. It’s still where a surpassing majority of agricultural commodities are grown and processed. But is it also a major producer of technology startups? Maybe not as much as the coasts, but the Midwest’s bustling metropoli and vast expanses of rural land prove to be fertile ground for quite a bit of startup activity.

And that’s what we’re going to take a look at here. In a similar vein to our recent analysis of startup fundraising in the South, we’ll break down the region into its constituent parts, assessing deal and dollar volume trends in the Midwest’s two primary sub-regions, some of its individual states and the most active metropolitan areas in the U.S.’s midsection.

And, to be clear, this is not Crunchbase News’s first foray into the region. We’ve covered the region’s seed-stage interest in AI and hard tech, a few notable rounds and have always included the Midwest in all manner of data-spelunking expeditions. And to this, we’ll add a deep dive into the numbers.

Borders and boundaries are a deep well of disputes. To preempt debate, we use the U.S. Census Bureau’s definition of the Midwest region which, unlike its definition of the South, shouldn’t be too controversial. If you have something against Kansas or Ohio being included in this group, take it up with the Feds.

The good folks at the Census Bureau split the Midwest into two distinct — and rather unimaginatively named — sub-regions: the West North Central and East North Central states, which are separated by the Mississippi River. We’ve included the map below.

By splitting the Midwest into two distinct parts, we’ll be able to see where most of the startup and funding activity is concentrated. Spoiler alert: The farther west you go, the startup population (and the population itself) grows more scattered.

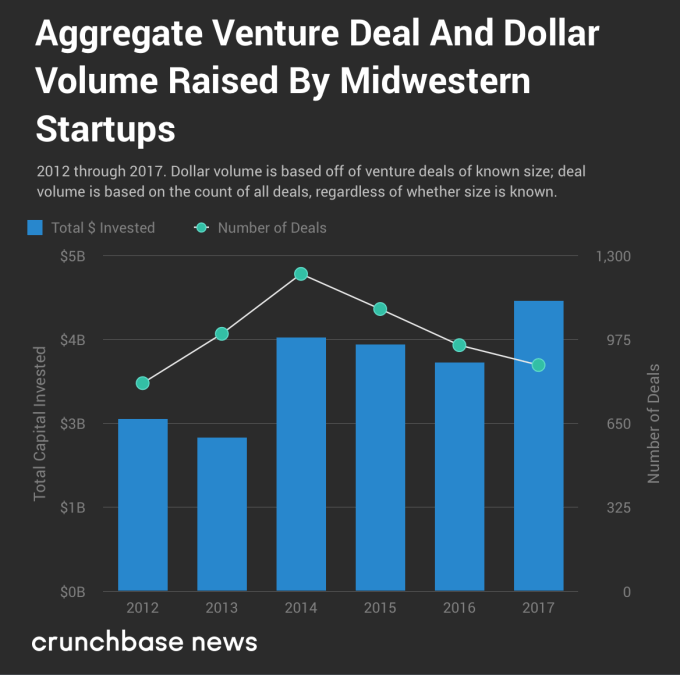

Based only on reported data in Crunchbase, the Midwest appears to be affected by the same phenomenon as the rest of the country. Crunchbase News has previously found that the number of seed and early-stage deals has gone off a cliff in the U.S., resulting in a top-heavy market featuring many large, late-stage deals. And this wouldn’t be a problem if it weren’t for a shortfall in new startups to fill the next cycle of early-stage funding. The “hollowing out” of the Midwestern venture deal pipeline becomes readily apparent when you look at funding data for the past several years, which you can find in the chart below.

To wit, deal volume is down markedly since 2014, as Crunchbase News reported in its Q4 2017 report of startup funding activity in the U.S. and Canada. But somewhat counterintuitively, the amount of money being invested into startups is on the rise in the Midwest and throughout many other parts of the country, reaching fresh multi-year highs in 2017. Almost one full quarter into 2018, the trend appears to continue unabated.

But this chart abstracts away a lot of nuance, so let’s take a closer look at the region and its states.

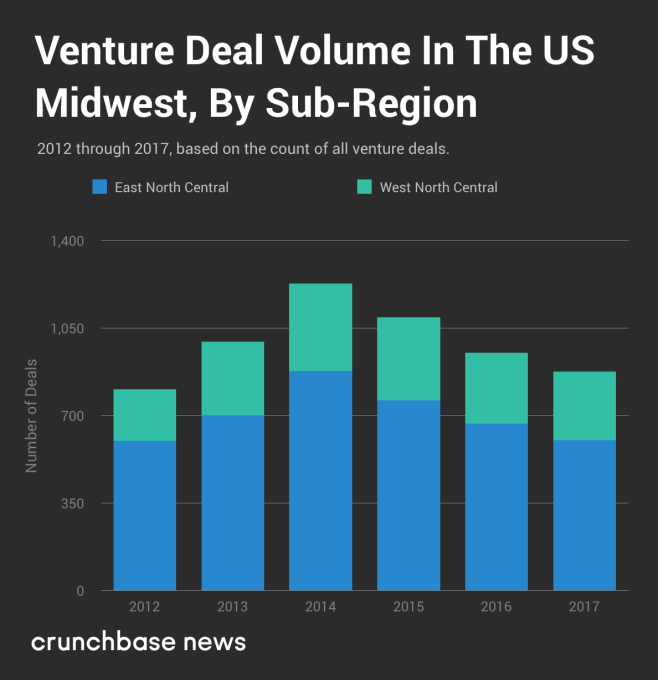

We’ll start first with deal volume, because that’s a fairly decent indicator of a geographic region’s level of startup activity. Below, we’ve plotted venture deal volume, divided by sub-region.

Again, based on the reported data from Crunchbase, we found that deal counts have been on a downward trend for several years. And though some of this may be attributable to reporting delays, projected deal volume data for the whole of the U.S. and Canada (fourth chart down in the Q4 quarterly report) shows a years’-long downtrend. There’s no reason to believe that startup activity in the Midwest is materially different from the rest of the U.S. and Canada.

But what about the relative “balance of power” between the two sub-regions? At least when it comes to deal volume, has one sub-region waxed while the other waned? To a limited extent, the answer is yes. Between 2012 and 2017, the percentage share of all Midwestern dealflow going to West North Central states like the Dakotas, Minnesota and Missouri has grown from 25.4 percent to 31.2 percent, up by nearly one-fifth in relative terms.

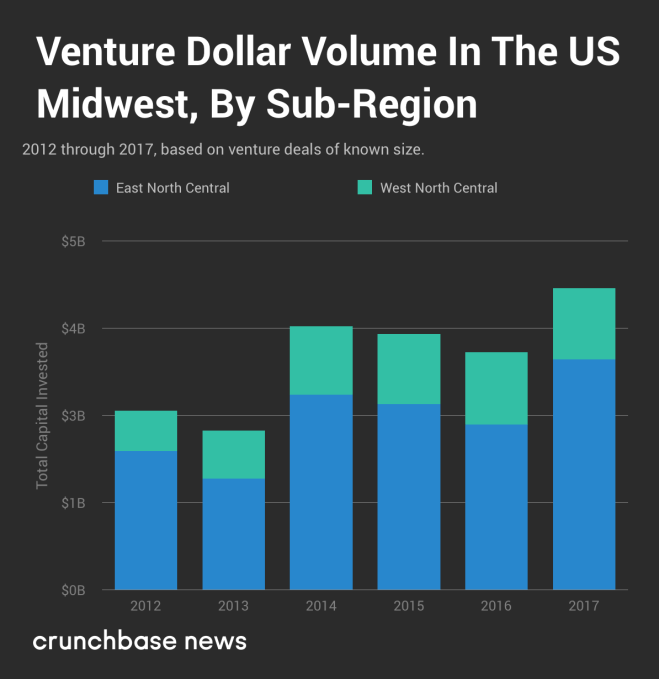

Now let’s check out dollar volume. The chart below displays aggregate reported venture capital dollar volume raised by startups in the Midwest.

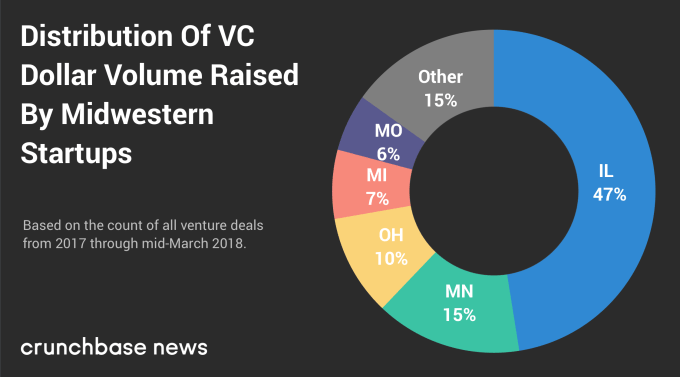

As far as the amount of money Midwestern startups have raised over time, the trendline is generally up and to the right. But that’s not the only way this differs from the deal volume data we looked at earlier. For dollar volume, there appears to be no appreciable change in the “balance of power” between the two sub-regions since 2012. Depending on the year, East North Central states like Illinois, Michigan and Ohio raked in between 70 and 78 percent of total dollar volume, but that variance doesn’t appear in an orderly trend.

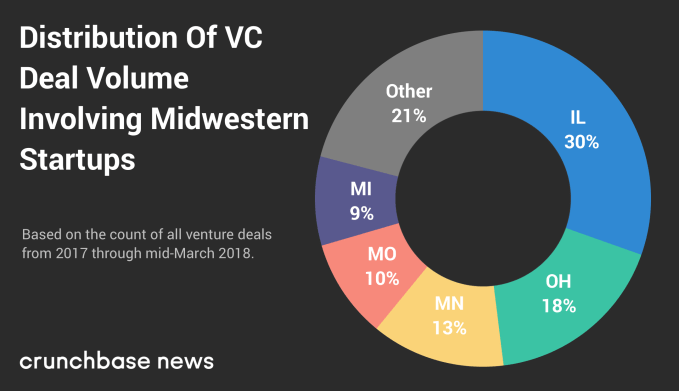

We started first at the regional level, then compared smaller groupings of states. Now, let’s see how deal and dollar volume is distributed on a state-by-state level. Doing so will point to the states that lead the region in venture-backed startup activity. Below, you’ll find a chart of how deal volume is split between the top five Midwestern states.

And here is how dollar volume is distributed.

As we saw with our analysis of the South, the top five Midwestern states for deal volume are the same five top-ranked states for dollar volume. But there is some notable variation in how these states rank among each other and the amount of deal and dollar volume they account for.

Considering that Illinois is home to Chicago and a number of downstate universities with deep tech startup roots, the fact that it places first for both metrics shouldn’t come as much of a surprise.

What might be more of a head-scratcher is Minnesota, which ranks third in deal volume but second in dollar volume. Why does it switch places with Ohio? The answer could lie in the industrial mix which, in the case of Minnesota, includes a disproportionately high number of medical device and other life sciences companies, which typically take a lot of capital to get off the ground.

Longtime readers of Crunchbase News may remember a ranking of Midwestern startup cities we wrote back in August 2017. However, here we’re just focusing on deal and dollar volume over the past 15 months, since the start of 2017.

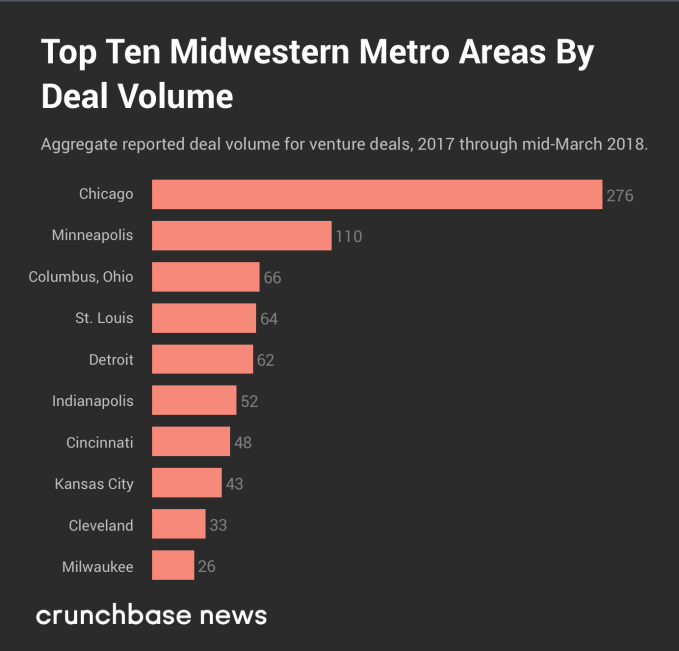

Let’s start first with the top 10 Midwestern cities as measured by number of startup funding rounds.

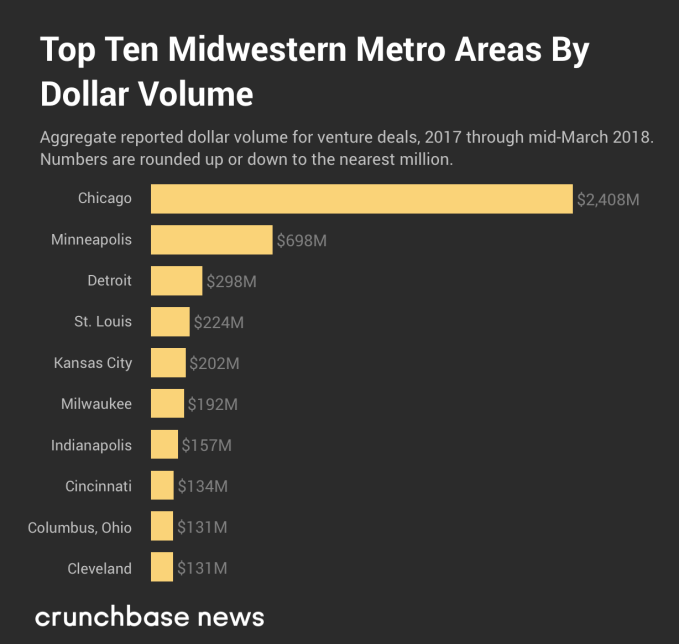

And in the chart below, you can see the top cities, as ranked by venture dollar volume, from the same period of time.

In both rankings, four of the top five cities are the same, but the odd one out appears to be Columbus, Ohio. Although there were a fairly large number of rounds raised by startups in that metro area, most of the rounds were fairly small by national standards. And one of the main reasons why Kansas City, Missouri jumped so much in the dollar volume rankings was a $100 million Series F round raised by C2FO.

But, again, as far as the Midwest goes, everything pales in comparison to Chicago alone.

For many, the Midwest is in a kind of Goldilocks zone. The East and West coasts seem to hold more or less equal sway over the culture and economy and most of its cities are neither too big nor too small. The only extreme it seems to occupy is its winter weather.

Powered by WPeMatico

The American South may not be the first region that comes to mind when you hear the phrase “hotbed of tech entrepreneurship,” but, slightly misguided perceptions aside, it’s home to a diverse and growing collection of startups.

Here, we’re going to take a deep dive into the startup funding data for the region.

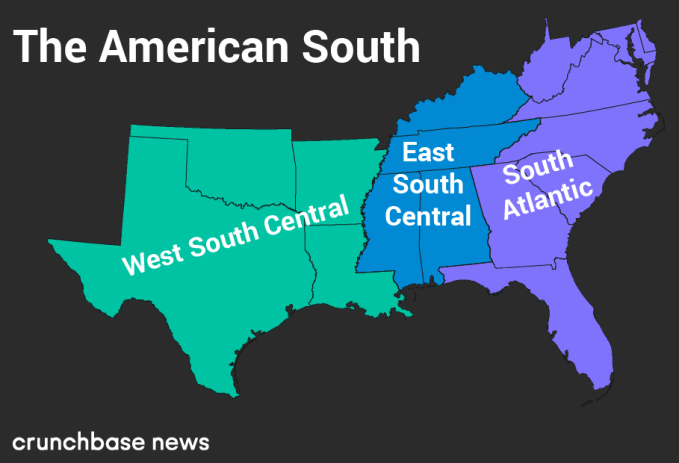

Just like it’s a common pastime for many city dwellers to argue about the precise boundaries of neighborhoods, there’s often some disagreement about the exact contours of the U.S.’s various regions. To quash rabble-rousing from the get-go, we’re using the U.S. Census Bureau’s definition of “the South” on its official map of the United States. Below, we display a map of the states we’re going to look at today.

Much like barbecue, the South is not a monolithic concept. So to incorporate some regional flavor into the following analysis, we’re also going to use the same regional divisions that the U.S. Census Bureau uses.

By doing this, we’ll be able to get a better idea of the relative contribution states from each sub-region make to startup activity in the South overall.

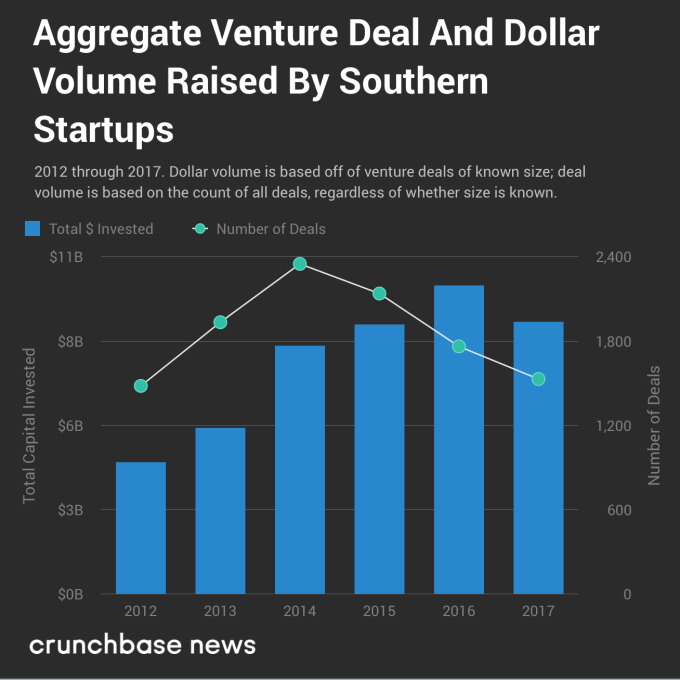

As is the case with most of the country, the South appears to be experiencing a shift in startup funding as we move toward the latter half of a bull run in entrepreneurial activity. The chart below shows a divergence in overall deal and dollar volume over time.

Much like in the rest of the U.S., reported deal and dollar volume are heading in different directions. Part of this may be due to reporting delays — it can sometimes take a few years for seed and early-stage rounds to get added to databases like Crunchbase’s . Nonetheless, there is a slow and generally upward creep in round sizes at most stages of funding. And that’s not just a Southern thing; it’s a country-wide trend.

Let’s disaggregate these figures a bit. We’ll start with deal counts and move on to dollar volume from there.

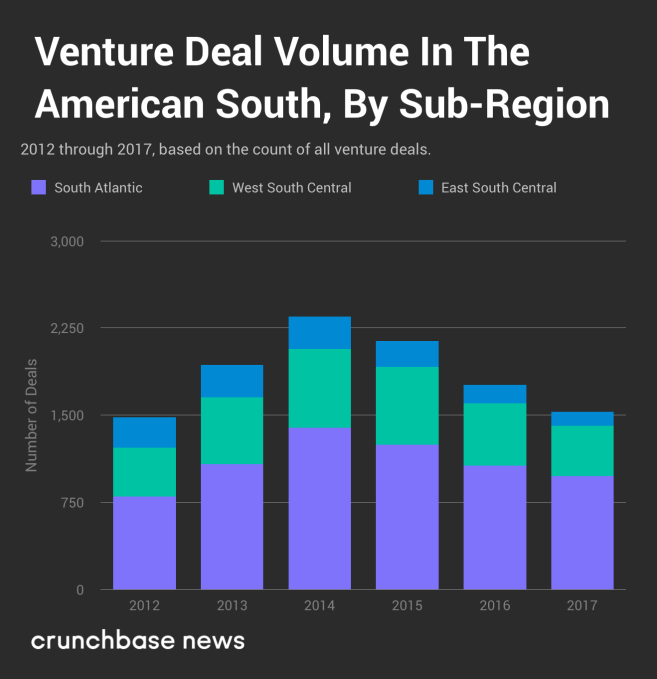

In the chart below, you’ll see venture deal volume broken out by sub-region.

Over the past several years, reported venture deal volume has been on the downswing. From a local maximum in 2014 through the end of 2017, it’s down almost 35 percent overall. But that’s not the whole picture. The relative share of deal volume has changed, as well.

Although it’s not immediately clear just by looking at the chart above, startups in the South Atlantic sub-region have accounted for an increasingly large share of the funding rounds. For example, in 2012, South Atlantic startups attracted 54 percent of the deal volume. In 2017, that grows to 64 percent. Startups in the West South Central sub-region have pretty consistently pulled in between 28 and 30 percent of the deals, so where’s the loss coming from? Startups headquartered in Kentucky, Tennessee, Mississippi and Alabama pulled in just 8 percent of deals in 2017, compared to 18 percent in 2012.

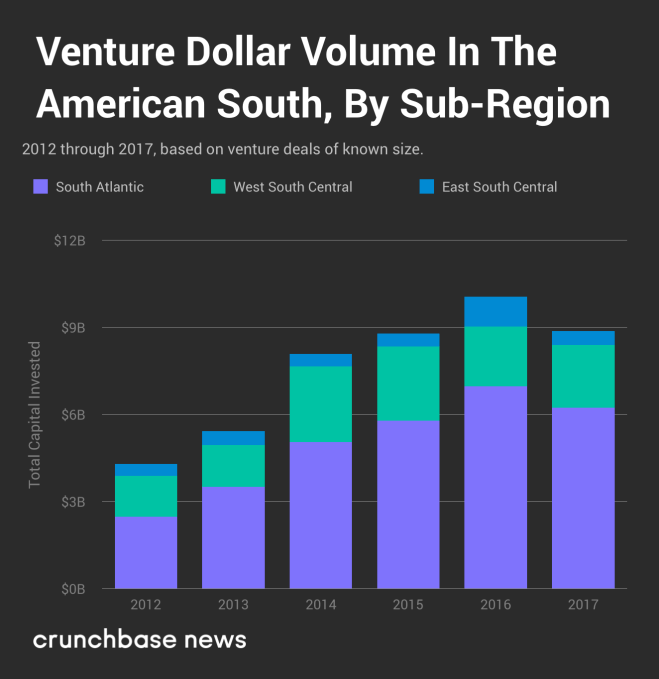

It’s a similar story with dollar volume.

In general, dollar volume follows the same pattern, albeit with a bit more variability. Regardless, startups in the South Atlantic sub-region are hoovering up an ever-larger share of venture dollars, and there’s little to indicate that trend will reverse itself any time soon.

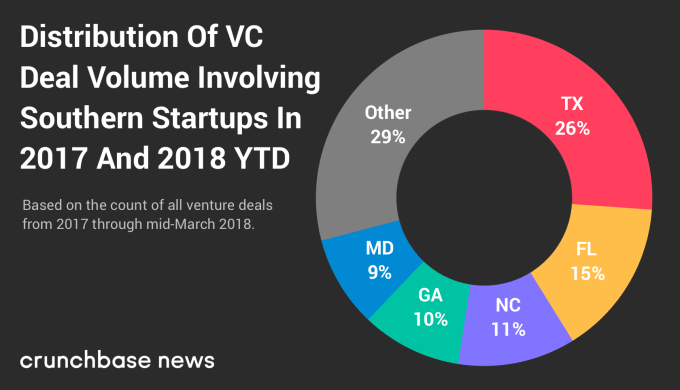

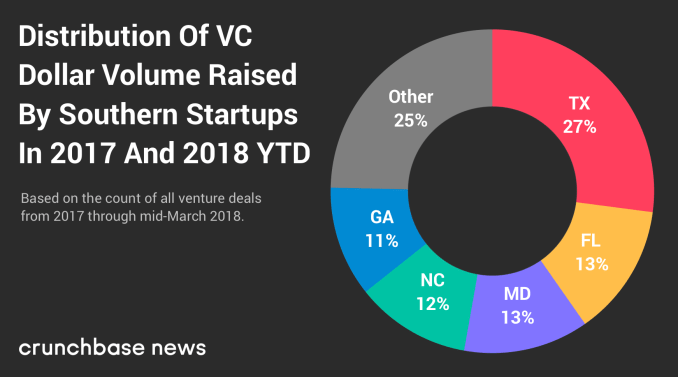

Let’s see which states accounted for most of the deal volume. The chart below shows the geographic distribution of deal-making activity by startups in each Southern state from the beginning of 2017 through time of writing. It should come as no surprise that much of the activity is concentrated in states with higher populations.

And here’s the distribution of dollar volume among southern states.

Despite some variation in which states are at the top of the ranks, the share of deal and dollar volume raised by startups in the top three states is remarkably similar, coming in at between 52 and 53 percent for both metrics.

We started by looking at the South as a whole and then drilled into its sub regions and states. But there’s one layer deeper we can go here, and that’s to rank the top startup cities in the South.

In the interest of keeping our rankings fresh and timely, we’re covering activity from the past 15 months or so, from the start of 2017 through mid-March 2018. But before highlighting some of the more notable hubs, let’s take a look at the numbers.

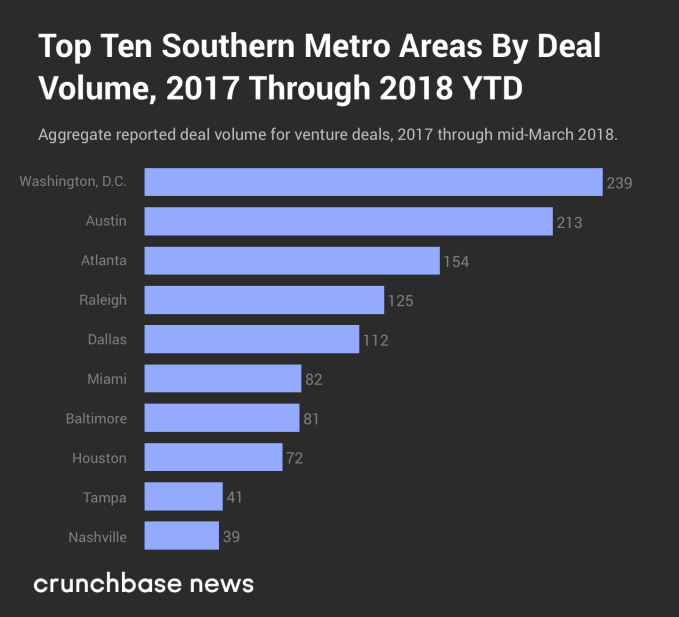

In the chart below, you’ll find the top 10 metropolitan areas where Southern startups closed the most funding rounds.

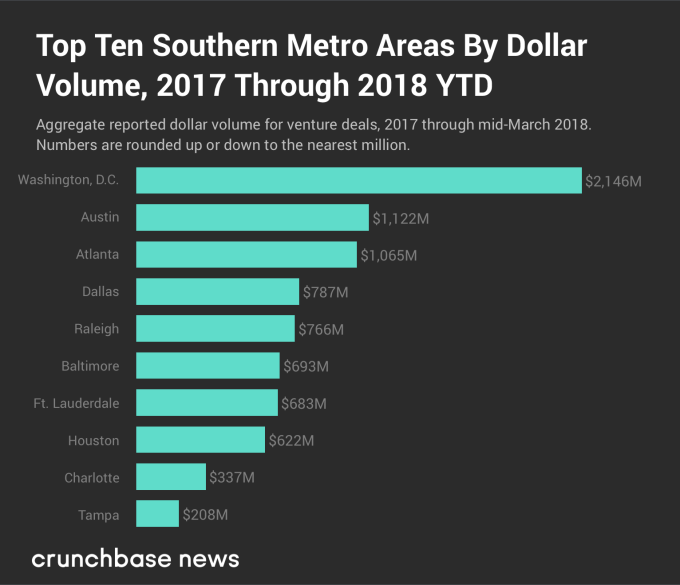

The chart below shows reported dollar volume over the same period of time.

Much like we saw at the state level, the top five startup cities — ranked by both deal and dollar volume — are the same, although there’s some variation between where each one ranks. In order, the D.C., Austin and Atlanta metro areas rank in the top three for each metric, while Dallas and Raleigh, NC switch off between fourth and fifth place.

To be frank, Washington, D.C.’s top-shelf ranking was a bit of a surprise. It may be the fact that Austin, TX plays host to South By Southwest, a somewhat more relaxed culture and/or a preponderance of excellent breakfast taco and barbecue joints, but to many — ourselves included — the city feels like it would have a more active startup scene than the nation’s capital. But that’s not exactly the case. The D.C. metro area had more venture deal and dollar volume than Austin for seven out of the last 10 years, and startups based in the nation’s capital have raised more than twice as much money so far in 2018.

D.C.-area startups have recently raised some notable rounds. Just a couple of weeks prior to the time of writing, Viela Bio raised $250 million in a Series A round (in late February 2018) to continue funding research and testing of its treatments for severe inflammation and autoimmune diseases. And on the later-stage end of things, education technology company Everfi raised $190 million in a Series D round that had participation from Amazon founder and CEO Jeff Bezos, former Alphabet executive Eric Schmidt and Medium CEO Ev Williams. Other D.C. companies, including Mapbox, Upside.com, Afiniti and ThreatQuotient, have all raised late-stage rounds within the past 15 months.

Startup ecosystems in Southern cities may pale in comparison to places like New York and San Francisco, but it wouldn’t be wise to discount the region entirely. A large number of interesting companies call the lower half of the Lower 48 home, and as the cost of living continues to rise on the east and west coasts, don’t be surprised if many current and would-be founders opt to stay down home in the South.

Powered by WPeMatico

It seems like startup news is full of overnight success stories and sudden failures, like the scooter rental company that went from zero to a $300 million valuation in months or the blood-testing unicorn that went from billions to nearly naught.

But what about those other companies that mature more gradually? Is there such a thing as slow and successful in startup-land?

To contemplate that question, Crunchbase News set out to assemble a data set of top late-blooming startups. We looked at companies that were founded in or before 2010 that raised large amounts of capital after 2015, and we also looked at companies founded a least five years ago that raised large early-stage funds in the last year. (For more details on the rules we used to select the companies, check “Data Methods” at the end of the post.)

The exercise was a counterpoint to a data set we did a couple of weeks ago, looking at characteristics of the fastest growing startups by capital raised. For that list, we found plenty of similarities between members, including a preponderance of companies in a few hot sectors, many famous founders and a lot of cancer drug developers.

For the late bloomers, however, patterns were harder to pinpoint. The breakdown wasn’t too different from venture-backed companies overall. Slower-growing companies could come from major venture hubs as well as cities with smaller startup ecosystems. They could be in biotech, medical devices, mobile gaming or even meditation.

What we did find, however, was an interesting and inspiring collection of stories for those of us who’ve been toiling away at something for a long time, with hopes still of striking it big.

Even youthful startups have been known to make a major pivot or two. So it’s not surprising to see a lot of pivots among late bloomers that have had more time to tinker with their business models.

One that fits this mold is Headspace, provider of a popular meditation app. The company, founded in 2010 by a British-born Buddhist monk with a degree in circus arts, started as a meditation-focused events startup. But it turned out people wanted to build on their learning on their own time, so Headspace put together some online lessons. Today, Santa Monica-based Headspace has millions of users and has raised $75 million in venture funding.

For late bloomers, the pivot can mean going from a model with limited scalability to one that can attract a much wider audience. That’s the case with Headspace, which would have been limited in its events business to those who could physically show up. Its online model, with instant, global reach, turns the business into something venture investors can line up behind.

They say if you wait long enough, everything comes back in style. That mantra usually works as an excuse for hoarding ’80s clothes in the attic. But it also can apply to entrepreneurial companies, which may have launched years before their industry evolved into something venture investors were competing to back.

Take Vacasa, the vacation rental management provider. The company has been around since 2009, but it began raising VC just a couple of years ago amid a broad expansion of its staff and property portfolio. The Portland-based company has raised more than $140 million to date, all of it after 2016, and most in a $103 million October round led by technology growth investor Riverwood Capital.

CloudCraze, which was acquired by Salesforce earlier this week, also took a long time to take venture funding. The Chicago-based provider of business-to-business e-commerce software launched in 2009, but closed its first VC round in 2015, according to Crunchbase records. Prior to the acquisition, the company raised about $30 million, with most of that coming in just a year ago.

Meanwhile, some late bloomers have always been fashionable, just not necessarily as VC-funded companies. Untuckit, a clothing retailer that specializes in button-down shirts that look good untucked, had been building up its business since 2011, but closed its first venture round, a Series A led by VC firm Kleiner Perkins, last June.

So yes, there is still capital available for those who wait. However, the truth of the matter is most companies that raise substantial sums of venture capital secure their initial seed rounds within a couple years of founding. Companies that chug along for five-plus years without a round and then scale up are comparatively rare.

That said, our data set, which looks at venture and seed funding, does not come close to capturing the full ecosystem of slow-growing startups. For one, many successful bootstrapped companies could raise venture funding but choose not to. And those who do eventually decide to take investment may look at other sources, like private equity, bank financing or even an IPO.

Additionally, the landscape is full of slow-growing startups that do make it, just not in a venture home run exit kind of way. Many stay local, thriving in the places they know best.

On the flip side, companies that wait a long time to take VC funding have also produced some really big exits.

Take Atlassian, the provider of workplace collaboration tools. Founded in 2002, the Australian company waited eight years to take its first VC financing, despite plentiful offers. It went public two years ago, and currently has a market valuation of nearly $14 billion.

The moral: Those who take it slow can still finish ahead.

Data methods

We primarily looked at companies founded in 2010 or earlier in the U.S. and Canada that raised a seed, Series A or Series B round sometime after the beginning of last year, and included some that first raised rounds in 2015 or later and went on to substantial fundraises. We also looked at companies founded in 2012 or earlier that raised a seed or Series A round after the beginning of last year and have raised $30 million or more to date. The list was culled further from there.

Powered by WPeMatico

Ford detailed a bunch of its roadmap for the next few years at a special media event today, and one of the key takeaways is that it’s going all-in on hybrids with its SUV lineup. Ford estimates that SUVs could make up as much as half the entire U.S. industry retail market by 2020, and that’s why it’s shifting $7 billion in investment capital from its cars business over to the SUV segment. By 2020, Ford also aims to have high-performance SUVs in market, including five with hybrid powertrains and one fully battery electric model.

These will include brand new versions of the Ford Escape and Ford Explorer that are coming next year, and two entirely new off-road SUVs, including a new Bronco, and a small SUV that has yet to be named. There’s also that “performance battery electric utility” that will make up part of its overall SUV lineup, which is set for a 2020 release and will spearhead a plan to release six electric vehicle models by 2022.

With this big hybrid push on the SUV side, Ford expects to go from second to first-place in the U.S. hybrid vehicles market by sales, surpassing current leader Toyota by 2021, thanks also to the forthcoming hybrid Mustang and F-150.

Powered by WPeMatico

Just a few weeks ago I was in Utah for the holidays, spending time with the many family members my husband and I both have there. At one family gathering, a cousin began talking about how he bought a brand new home and sold his own home all without a real estate agent on a site called Homie. Read More

Just a few weeks ago I was in Utah for the holidays, spending time with the many family members my husband and I both have there. At one family gathering, a cousin began talking about how he bought a brand new home and sold his own home all without a real estate agent on a site called Homie. Read More

Powered by WPeMatico

Despite repeal of the Affordable Care Act’s individual mandate this week, health insurance startup Oscar Health expects to pull in nearly $1 billion in revenue and enroll a quarter of a million members in 2018. The revenue prediction first reported in Axios and signups are quite a feat for the insurance company meant for the digital age. Read More

Despite repeal of the Affordable Care Act’s individual mandate this week, health insurance startup Oscar Health expects to pull in nearly $1 billion in revenue and enroll a quarter of a million members in 2018. The revenue prediction first reported in Axios and signups are quite a feat for the insurance company meant for the digital age. Read More

Powered by WPeMatico