United Kingdom

Auto Added by WPeMatico

Auto Added by WPeMatico

Business, now more than ever before, is going digital, and today a startup that’s building a vertically integrated solution to meet business banking needs is announcing a big round of funding to tap into the opportunity. Airwallex — which provides business banking services directly to businesses themselves as well as via a set of APIs that power other companies’ fintech products — has raised $200 million, a Series E round of funding that values the Australian startup at $4 billion.

Lone Pine Capital is leading the round, with new backers G Squared and Vetamer Capital Management, and previous backers 1835i Ventures (formerly ANZi), DST Global, Salesforce Ventures and Sequoia Capital China also participating.

The funding brings the total raised by Airwallex — which has head offices in Hong Kong and Melbourne, Australia — to $700 million, including a $100 million injection that closed out its Series D just six months ago.

Airwallex will be using the funding both to continue investing in its product and technology as well as to continue its geographical expansion and to focus on some larger business targets. The company has started to make some headway into Europe and the U.K. and that will be one big focus, along with the U.S.

The quick succession of funding and rising valuation underscore Airwallex’s traction to date around what CEO and co-founder Jack Zhang describes as a vertically integrated strategy.

That involves two parts. First, Airwallex has built all the infrastructure for the business banking services that it provides directly to businesses with a focus on small and medium enterprise customers. Second, it has packaged up that infrastructure into a set of APIs that a variety of other companies use to provide financial services directly to their customers without needing to build those services themselves — the so-called “embedded finance” approach.

“We want to own the whole ecosystem,” Zhang said to me. “We want to be like the Apple of business finance.”

That seems to be working out so far for Airwallex. Revenues were up almost 150% for the first half of 2021 compared to a year before, with the company processing more than US$20 billion for a global client portfolio that has quadrupled in size. In addition to tens of thousands of SMEs, it also, via APIs, powers financial services for other companies like GOAT, Papaya Global and Stake.

Airwallex got its start like many of the strongest startups do: It was built to solve a problem that the founders encountered themselves. In the case of Airwallex, Zhang tells me he had actually been working on a previous startup idea. He wanted to build the “Blue Bottle Coffee” of Asia Pacific out of Australia, and it involved buying and importing a lot of different materials, packaging and, of course, coffee from all around the world.

“We found that making payments as a small business was slow and expensive,” he said, since it involved banks in different countries and different banking systems, manual efforts to transfer money between them and many days to clear the payments. “But that was also my background — payments and trading — and so I decided that it was a much more fascinating problem for me to work on and resolve.”

Eventually one of his co-founders in the coffee effort came along, with the four co-founders of Airwallex ultimately including Zhang, along with Xijing Dai, Lucy Liu and Max Li.

It was 2014, and Airwallex got attention from VCs early on in part for being in the right place at the right time. A wave of startups building financial services for SMBs were definitely gaining ground in North America and Europe, filling a long-neglected hole in the technology universe, but there was almost nothing of the sort in the Asia Pacific region, and in those earlier days solutions were highly regionalized.

From there it was a no-brainer that starting with cross-border payments, the first thing Airwallex tackled, would soon grow into a wider suite of banking services involving payments and other cross-border banking services.

“In the last six years, we’ve built more than 50 bank integrations and now offer payments across 95 countries, payments through a partner network,” he added, with 43 of those offering real-time transactions. From that, it moved on to bank accounts and “other primitive stuff” with card issuance and more, he said, eventually building an end-to-end payment stack.

Airwallex has tens of thousands of customers using its financial services directly, and they make up about 40% of its revenues today. The rest is the interesting turn the company decided to take to expand its business.

Airwallex had built all of its technology from the ground up itself, and it found that — given the wave of new companies looking for more ways to engage customers and become their one-stop shop — there was an opportunity to package that tech up in a set of APIs and sell that on to a different set of customers, those who also provided services for small businesses. That part of the business now accounts for 60% of Airwallex’s business, Zhang said, and is growing faster in terms of revenues. (The SMB business is growing faster in terms of customers, he said.)

A lot of embedded finance startups that base their business around building tech to power other businesses tend to stay at arm’s length from offering financial services directly to consumers. The explanation I have heard is that they do not wish to compete against their customers. Zhang said that Airwallex takes a different approach, by being selective about the customers they partner with, so that the financial services they offer would not be in direct competition with those of its customers. The GOAT marketplace for sneakers, or Papaya Global’s HR platform are classic examples of this.

However, as Airwallex continues to grow, you can’t help but wonder whether one of those partners might like to gobble up all of Airwallex and take on some of that service provision role itself. In that context, it’s very interesting to see Salesforce Ventures returning to invest even more in the company in this round, given how widely the company has expanded from its early roots in software for salespeople into a massive platform providing a huge range of cloud services to help people run their businesses.

For now, it’s been the combination of its unique roots in Asia Pacific, plus its vertical approach of building its tech from the ground up, plus its retail acumen that has impressed investors and may well see Airwallex stay independent and grow for some time to come.

“Airwallex has a clear competitive advantage in the digital payments market,” said David Craver, MD at Lone Pine Capital, in a statement. “Its unique Asia-Pacific roots, coupled with its innovative infrastructure, products and services, speak volumes about the business’ global growth opportunities and its impressive expansion in the competitive payment providers space. We are excited to invest in Airwallex at this dynamic time, and look forward to helping drive the company’s expansion and success worldwide.”

Updated to note that the coffee business was in Australia, not Hong Kong.

Powered by WPeMatico

It’s a story common to all sectors today: investors only want to see ‘uppy-righty’ charts in a pitch. However, edtech growth in the past 18 months has ramped up to such an extent that companies need to be presenting 3x+ growth in annual recurring revenue to even get noticed by their favored funds.

Some companies are able to blast this out of the park — like GoStudent, Ornikar and YouSchool — but others, arguably less suited to the conditions presented by the pandemic, have found it more difficult to present this kind of growth.

One of the most common themes Brighteye sees in young companies is an emphasis on international expansion for growth. To get some additional insight into this trend, we surveyed edtech firms on their expansion plans, priorities and pitfalls. We received 57 responses and supplemented it with interviews of leading companies and investors. Europe is home 49 of the surveyed companies, six are based in the U.S., and three in Asia.

Going international later in the journey or when more funding is available, possibly due to a VC round, seems to make facets of expansion more feasible. Higher budgets also enable entry to several markets nearly simultaneously.

The survey revealed a roughly even split of target customers across companies, institutions and consumers, as well as a good spread of home markets. The largest contingents were from the U.K. and France, with 13 and nine respondents respectively, followed by the U.S. with seven, Norway with five, and Spain, Finland, and Switzerland with four each. About 40% of these firms were yet to foray beyond their home country and the rest had gone international.

International expansion is an interesting and nuanced part of the growth path of an edtech firm. Unlike their neighbors in fintech, it’s assumed that edtech companies need to expand to a number of big markets in order to reach a scale that makes them attractive to VCs. This is less true than it was in early 2020, as digital education and work is now so commonplace that it’s possible to build a billion-dollar edtech in a single, larger European market.

But naturally, nearly every ambitious edtech founder realizes they need to expand overseas to grow at a pace that is attractive to investors. They have good reason to believe that, too: The complexities of selling to schools and universities, for example, are widely documented, so it might seem logical to take your chances and build market share internationally. It follows that some view expansion as a way of diversifying risk — e.g. we are growing nicely in market X, but what if the opportunity in Y is larger and our business begins to decline for some reason in market X?

International expansion sounds good, but what does it mean? We asked a number of organizations this question as part of the survey analysis. The responses were quite broad, and their breadth to an extent reflected their target customer groups and how those customers are reached. If the product is web-based and accessible anywhere, then it’s relatively easy for a company with a good product to reach customers in a large number of markets (50+). The firm can then build teams and wider infrastructure around that traction.

Powered by WPeMatico

A Canadian startup called Nuula that is aiming to build a super app to provide a range of financial services to small and medium businesses has closed $120 million of funding, money that it will use to fuel the launch of its app and first product, a line of credit for its users.

The money is coming in the form of $20 million in equity from Edison Partners, and a $100 million credit facility from funds managed by the Credit Group of Ares Management Corporation.

The Nuula app has been in a limited beta since June of this year. The plan is to open it up to general availability soon, while also gradually bringing in more services, some built directly by Nuula itself but many others following an embedded finance strategy: business banking, for example, will be a service provided by a third party and integrated closely into the Nuula app to be launched early in 2022. Alongside that, the startup will also be making liberal use of APIs to bring in other white-label services, such as B2B and customer-focused payment services, starting first in the U.S. and then expanding to Canada and the U.K. before expanding further into countries across Europe.

Current products include cash flow forecasting, personal and business credit score monitoring, and customer sentiment tracking; and monitoring of other critical metrics including financial, payments and e-commerce data are all on the roadmap.

“We’re building tools to work in a complementary fashion in the app,” CEO Mark Ruddock said in an interview. “Today, businesses can project if they are likely to run out of money, and monitor their credit scores. We keep an eye on customers and what they are saying in real time. We think it’s necessary to surface for SMBs the metrics that they might have needed to get from multiple apps, all in one place.”

Nuula was originally a side-project at BFS, a company that focused on small business lending, where the company started to look at the idea of how to better leverage data to build out a wider set of services addressing the same segment of the market. BFS grew to be a substantial business in its own right (and it had raised its own money to that end, to the tune of $184 million from Edison and Honeywell). Over time, it became apparent to management that the data aspect, and this concept of a super app, would be key to how to grow the business, and so it pivoted and rebranded earlier this year, launching the beta of the app after that.

Nuula’s ambitions fall within a bigger trend in the market. Small and medium enterprises have shaped up to be a huge business opportunity in the world of fintech in the last several years. Long ignored in favor of building solutions either for the giant consumer market, or the lucrative large enterprise sector, SMBs have proven that they want and are willing to invest in better and newer technology to run their businesses, and that’s leading to a rush of startups and bigger tech companies bringing services to the market to cater to that.

Super apps are also a big area of interest in the world of fintech, although up to now a lot of what we’ve heard about in that area has been aimed at consumers — just the kind of innovation rut that Nuula is trying to get moving.

“Despite the growth in services addressing the SMB sector, overall it still lacks innovation compared to consumer or enterprise services,” Ruddock said. “We thought there was some opportunity to bring new thinking to the space. We see this as the app that SMBs will want to use everyday, because we’ll provide useful tools, insights and capital to power their businesses.”

Nuula’s priority to build the data services that connect all of this together is very much in keeping with how a lot of neobanks are also developing services and investing in what they see as their unique selling point. The theory goes like this: banking services are, at the end of the day, the same everywhere you go, and therefore commoditized, and so the more unique value-added for companies will come from innovating with more interesting algorithms and other data-based insights and analytics to give more power to their users to make the best use of what they have at their disposal.

It will not be alone in addressing that market. Others building fintech for SMBs include Selina, ANNA, Amex’s Kabbage (an early mover in using big data to help loan money to SMBs and build other financial services for them), Novo, Atom Bank, Xepelin and Liberis, biggies like Stripe, Square and PayPal, and many others.

The credit product that Nuula has built so far is a taster of how it hopes to be a useful tool for SMBs, not just another place to get money or manage it. It’s not a direct loaning service, but rather something that is closely linked to monitoring a customers’ incomings and outgoings and only prompts a credit line (which directly links into the users’ account, wherever it is) when it appears that it might be needed.

“Innovations in financial technology have largely democratized who can become the next big player in small business finance,” added Gary Golding, General Partner, Edison Partners. “By combining critical financial performance tools and insights into a single interface, Nuula represents a new class of financial services technology for small business, and we are excited by the potential of the firm.”

“We are excited to be working with Nuula as they build a unique financial services resource for small businesses and entrepreneurs,” said Jeffrey Kramer, Partner and Head of ABS in the Alternative Credit strategy of the Ares Credit Group, in a statement. “The evolution of financial technology continues to open opportunities for innovation and the emergence of new industry participants. We look forward to seeing Nuula’s experienced team of technologists, data scientists and financial service veterans bring a new generation of small business financial services solutions to market.”

Powered by WPeMatico

Marshmallow — a U.K.-based car insurance provider that has made a name for itself in the market by providing a new approach to car insurance aimed at using a wider set of data points and clever algorithms to net a more diverse set of customers and provide more competitive rates — is announcing a milestone today in its life as a startup, as well as in the bigger U.K. tech world.

The London company — co-founded by identical twins Oliver and Alexander Kent-Braham and David Goaté — has raised $85 million in a new round of funding. The Series B valuation is significant on two counts: it catapults Marshmallow to a “unicorn” valuation above $1 billion — specifically, $1.25 billion; and Marshmallow itself becomes one of a very small group of U.K. startups founded by Black people — Oliver and Alexander — to reach that figure.

(To be clear, Marshmallow describes itself as “the first UK unicorn to be founded by individuals that are Black or have Black heritage”, although I can think of at least one that preceded it: WorldRemit, which last month rebranded to Zepz, and is currently valued at $5 billion; co-founder and chairman Ismail Ahmed has been described as the most influential Black Briton.)

Regardless of whether Marshmallow is the first or one of the first, given the dearth of diversity in the U.K. technology industry, in particular in the upper ranks of it, it’s a notable detail worth pointing out, even as I hope that one day it will be less of a rarity.

Meanwhile, Marshmallow’s novel, big-data approach and successful traction in the market speak for themselves. When we covered the company’s most recent funding round before this — a $30 million raise in November 2020 — the startup was valued at $310 million. Now less than a year later, Marshmallow’s valuation has nearly quadrupled, and it has passed 100,000 policies sold in its home country, growing 100% over the last six months.

The plan now, Oliver told me in an interview, will be to deepen its relationships with customers, in part by providing more engagement to make them better drivers, but also potentially selling more services to them, too.

In this, the startup will be tapping into a new approach that other insurtech startups are taking as they rethink traditional insurance models, much like YuLife is positioning its life insurance products within a bigger wellness and personal improvement business. Currently, the average age of Marshmallow’s customers is 20 to 40, Oliver said — and there are thoughts of potentially new products aimed at even younger users. That means there is long-term value in improving loyalty and keeping those customers for many years to come.

Alongside that, Marshmallow will also use the funding to inch closer to its plan to expand to markets outside of the U.K. — a strategy that has been in the works for a while. Marshmallow talked up international expansion in its last round but has yet to announce which markets it will seek to tackle first.

Insurance — and in particular insurance startups — are often thought of together with fintech startups, not least because the two industries have a lot in common: they both operate in areas of assessing and mitigating risk and fraud; they are in many cases discretionary investments on the part of the customers; and they are both highly regulated and require watertight data protection for their users.

Perhaps because so much of the hard work is the same for both, it’s not uncommon to see services built to serve both sectors (FintechOS and Shift Technology being two examples), for fintech companies to dabble in insurance services, and so on.

But in reality, insurance — and specifically car insurance — has seen a massive impact from COVID-19 unique to that industry. Separate reports from EY and the Association of British Insurers noted that 2020 actually saw a lift for many car insurance companies: lockdowns meant that fewer people were driving, and therefore fewer were getting into accidents and making fewer claims.

2021, however, has been a different story: new pricing rules being put into place will likely see a number of providers tip into the red for the year. And the Chartered Insurance Institute points out that it will also be worth watching to see how the low use of cars in one year will impact use going forward: some car owners, especially in urban areas where keeping a car is expensive, will inevitably start to question whether they need to own and insure a car at all.

All of this, ironically, actually plays into the hand of a company like Marshmallow, which is providing a more flexible approach to customers who might otherwise be rejected by more traditional companies, or might be priced out of offerings from them. Interestingly, while neobanks have definitely spurred more traditional institutions to try to update their products to compete, the same hasn’t really happened in insurance — not yet, at least.

“We started with the idea of the power of data and using a wider range of resources [than incumbents], and using that in our pricing led us to be able to offer better rates to more people,” Oliver said, but that hasn’t led to Marshmallow seeing sharper competition from older incumbents. “They are big companies and stuck in their ways. These companies have been around for decades, some for centuries. Change is not happening quickly.”

That leaves a big opportunity for companies like Marshmallow and other newer players like Lemonade, Hippo and Jerry (not an insurance startup per se but also dabbling in the space), and a big opening for investors to back new ideas in an industry estimated to be worth $5 trillion.

“The traction the team has achieved demonstrates the demand for a new kind of insurance provider, one that focuses more on consumer experience and uses the latest technology and data to give fair prices,” said Eileen Burbidge, a partner at Passion Capital, in a statement. “We’ve been proud to support the team’s ambitions since the start, and now look forward to its next chapter in Europe as it continues its mission to change the industry for the better.”

Powered by WPeMatico

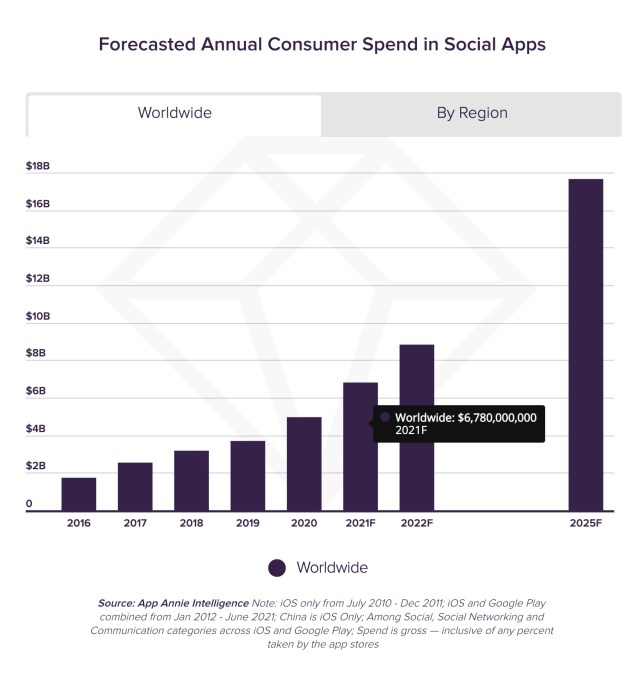

The livestreaming boom is driving a significant uptick in the creator economy, as a new forecast estimates consumers will spend $6.78 billion in social apps in 2021. That figure will grow to $17.2 billion annually by 2025, according to data from mobile data firm App Annie, which notes the upward trend represents a five-year compound annual growth rate (CAGR) of 29%. By that point, the lifetime total spend in social apps will reach $78 billion, the firm reports.

Image Credits: App Annie

Initially, much of the livestream economy was based on one-off purchases like sticker packs, but today, consumers are gifting content creators directly during their livestreams. Some of these donations can be incredibly high, at times. Twitch streamer ExoticChaotic was gifted $75,000 during a live session on Fortnite, which was one of the largest-ever donations on the game-streaming social network. Meanwhile, App Annie notes another platform, Bigo Live, is enabling broadcasters to earn up to $24,000 per month through their livestreams.

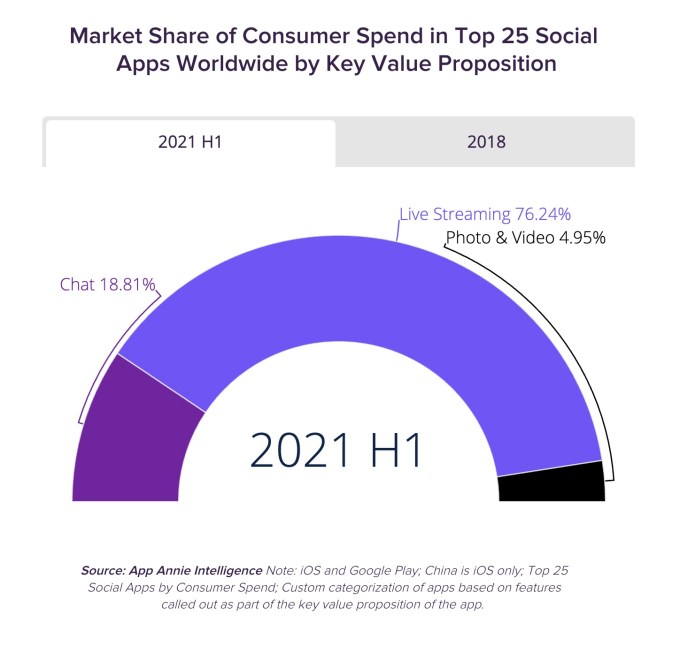

Apps that offer livestreaming as a prominent feature are also those that are driving the majority of today’s social app spending, the report says. In the first half of this year, $3 out every $4 spent in the top 25 social apps came from apps that offered livestreams, for example.

Image Credits: App Annie

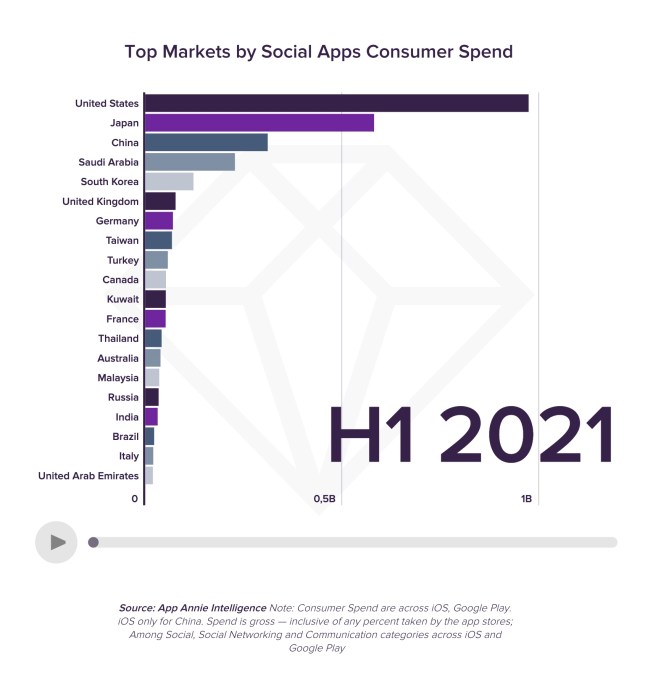

During the first half of 2021, the U.S. become the top market for consumer spending inside social apps, with 1.7x the spend of the next largest market, Japan, and representing 30% of the market by spend. China, Saudi Arabia and South Korea followed to round out the top 5.

Image Credits: App Annie

While both creators and the platforms are financially benefitting from the livestreaming economy, the platforms are benefitting in other ways beyond their commissions on in-app purchases. Livestreams are helping to drive demand for these social apps and they help to boost other key engagement metrics, like time spent in app.

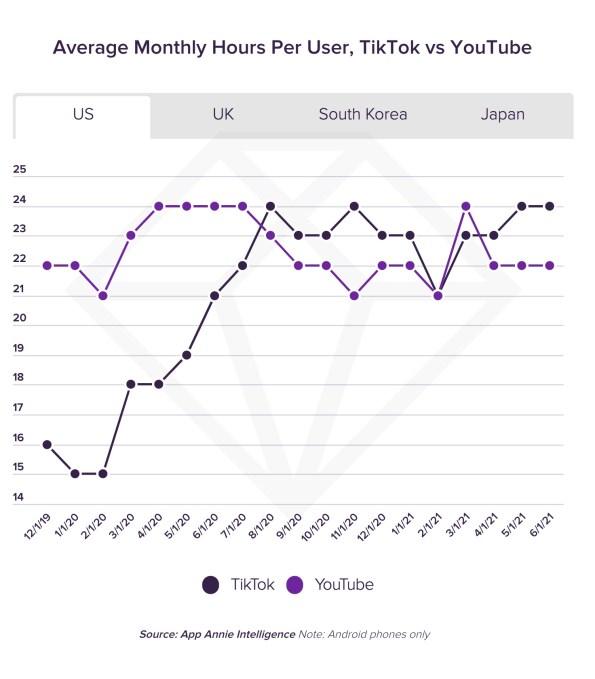

One top app that’s significantly gaining here is TikTok.

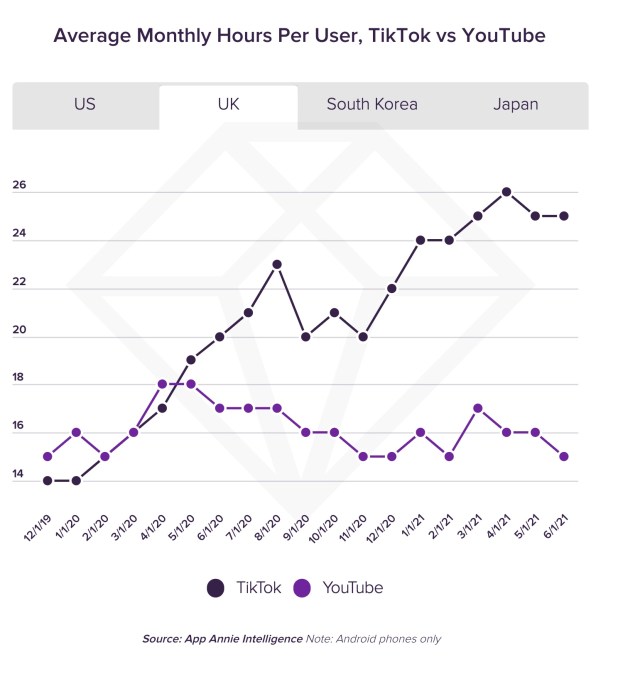

Last year, TikTok surpassed YouTube in the U.S. and the U.K. in terms of the average monthly time spent per user. It often continues to lead in the former market, and more decisively leads in the latter.

Image Credits: App Annie

Image Credits: App Annie

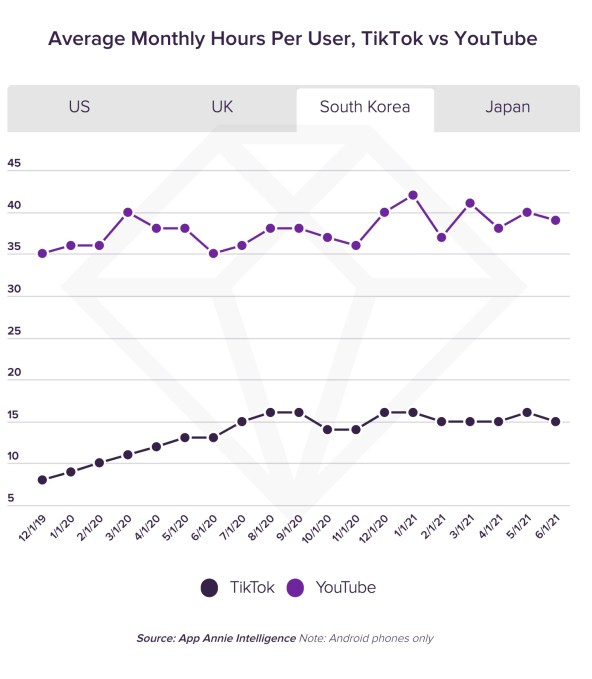

In other markets, like South Korea and Japan, TikTok is making strides, but YouTube still leads by a wide margin. (In South Korea, YouTube leads by 2.5x, in fact.)

Image Credits: App Annie

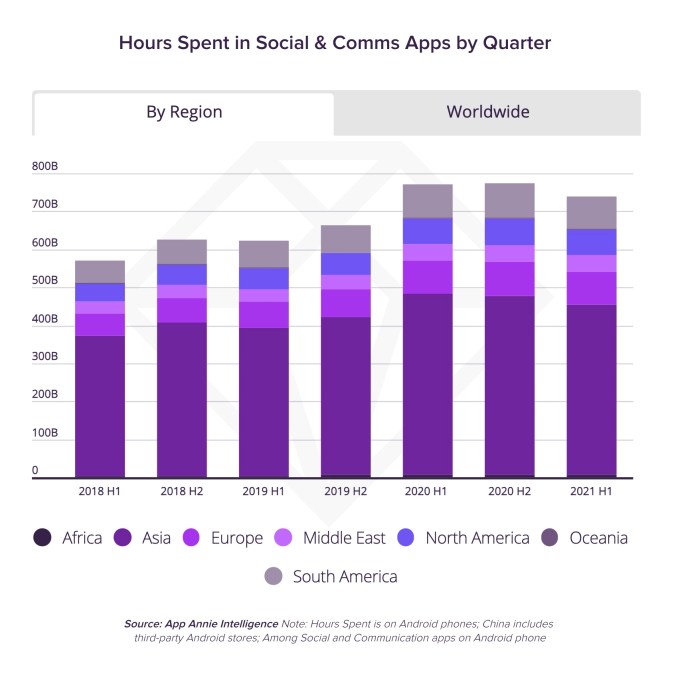

Beyond just TikTok, consumers spent 740 billion hours in social apps in the first half of the year, which is equal to 44% of the time spent on mobile globally. Time spent in these apps has continued to trend upwards over the years, with growth that’s up 30% in the first half of 2021 compared to the same period in 2018.

Today, the apps that enable livestreaming are outpacing those that focus on chat, photo or video. This is why companies like Instagram are now announcing dramatic shifts in focus, like how they’re “no longer a photo sharing app.” They know they need to more fully shift to video or they will be left behind.

The total time spent in the top five social apps that have an emphasis on livestreaming are now set to surpass half a trillion hours on Android phones alone this year, not including China. That’s a three-year CAGR of 25% versus just 15% for apps in the Chat and Photo & Video categories, App Annie noted.

Image Credits: App Annie

Thanks to growth in India, the Asia-Pacific region now accounts for 60% of the time spent in social apps. As India’s growth in this area increased over the past 3.5 years, it shrunk the gap between itself and China from 115% in 2018 to just 7% in the first half of this year.

Social app downloads are also continuing to grow, due to the growth in livestreaming.

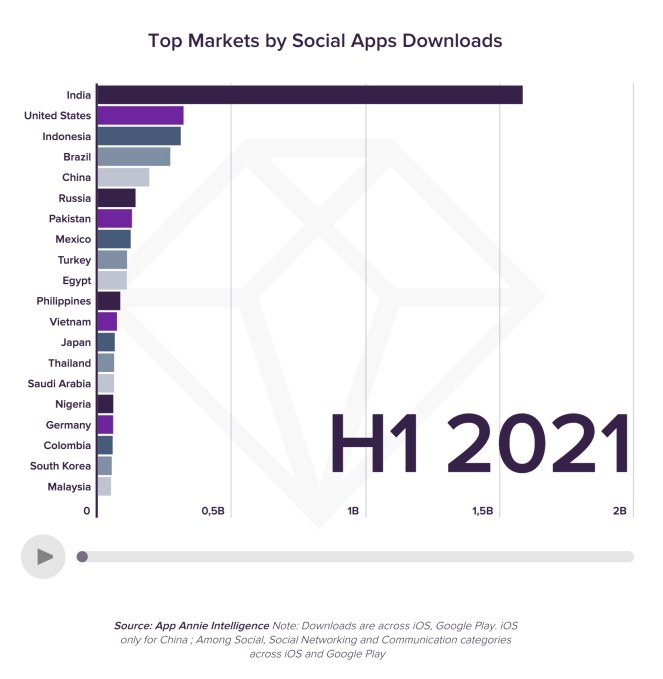

To date, consumers have downloaded social apps 74 billion times, and that demand remains strong, with 4.7 billion downloads in the first half of 2021 alone — up 50% year-over-year. In the first half of the year, Asia was the largest region region for social app downloads, accounting for 60% of the market.

This is largely due to India, the top market by a factor of 5x, which surpassed the U.S. back in 2018. India is followed by the U.S., Indonesia, Brazil and China, in terms of downloads.

Image Credits: App Annie

The shift toward livestreaming and video has also impacted what sort of apps consumers are interested in downloading, not just the number of downloads.

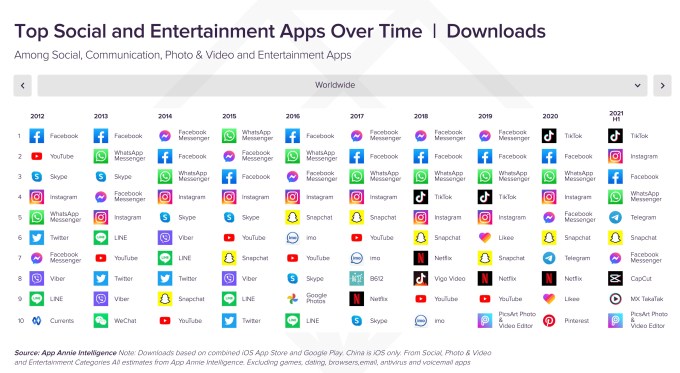

A chart that shows the top global apps from 2012 to the present highlights Facebook’s slipping grip. While its apps (Facebook, Messenger, Instagram and WhatsApp) have dominated the top spots over the years in various positions, TikTok popped into the number one position last year, and continues to maintain that ranking in 2021.

Further down the chart, other apps that aid in video editing have also overtaken others that had been more focused on photos or chat.

Image Credits: App Annie

Video apps like YouTube (#1), TikTok (#2) Tencent Video (#4), Bigo Live (#5), Twitch (#6), and others also now rank at the top of the global charts by consumer spending in the first half of 2021.

But YouTube (#1) still dominates in time spent compared with TikTok (#5), and others from Facebook — the company holds the next three spots for Facebook, WhatsApp and Instagram, respectively.

This could explain why TikTok is now exploring the idea of allowing users to upload even longer videos, by increasing the limit from 3 minutes to 5, for instance.

TikTok is testing a longer 5 minute video upload limit

pic.twitter.com/qiRbJmHkma

— Matt Navarra (@MattNavarra) August 25, 2021

In addition, because of livestreaming’s ability to drive growth in terms of time spent, it’s also likely the reason why TikTok has been heavily investing in new features for its TikTok LIVE platform, including things like events, support for co-hosts, Q&As and more, and why it made the “LIVE” button a more prominent feature in its app and user experience.

App Annie’s report also digs into the impact livestreaming has had on specific platforms, like Twitch and Bigo Live, the former which doubled its monthly active user base from the pre-pandemic era, and the latter which saw $314.2 million in consumer spend during H1 2021.

“The ability of social media users to communicate with each other using live video – or watch others’ live broadcasts – has not only maintained the growth of a social media app market, but contributed to its exponential growth in engagement metrics like time spent, that might otherwise have saturated some time ago,” wrote App Annie’s Head of Insights, Lexi Sydow, when announcing the new report.

The full report is available here.

Powered by WPeMatico

The manufacturing industry took a hard hit from the Covid-19 pandemic, but there are signs of how it is slowly starting to come back into shape — helped in part by new efforts to make factories more responsive to the fluctuations in demand that come with the ups and downs of grappling with the shifting economy, virus outbreaks and more. Today, a businesses that is positioning itself as part of that new guard of flexible custom manufacturing — a startup called Fractory — is announcing a Series A of $9 million (€7.7 million) that underscores the trend.

The funding is being led by OTB Ventures, a leading European investor focussed on early growth, post-product, high-tech start-ups, with existing investors Trind Ventures, Superhero Capital, United Angels VC, Startup Wise Guys and Verve Ventures also participating.

Founded in Estonia but now based in Manchester, England — historically a strong hub for manufacturing in the country, and close to Fractory’s customers — Fractory has built a platform to make it easier for those that need to get custom metalwork to upload and order it, and for factories to pick up new customers and jobs based on those requests.

Fractory’s Series A will be used to continue expanding its technology, and to bring more partners into its ecosystem.

To date, the company has worked with more than 24,000 customers and hundreds of manufacturers and metal companies, and altogether it has helped crank out more than 2.5 million metal parts.

To be clear, Fractory isn’t a manufacturer itself, nor does it have no plans to get involved in that part of the process. Rather, it is in the business of enterprise software, with a marketplace for those who are able to carry out manufacturing jobs — currently in the area of metalwork — to engage with companies that need metal parts made for them, using intelligent tools to identify what needs to be made and connecting that potential job to the specialist manufacturers that can make it.

The challenge that Fractory is solving is not unlike that faced in a lot of industries that have variable supply and demand, a lot of fragmentation, and generally an inefficient way of sourcing work.

As Martin Vares, Fractory’s founder and MD, described it to me, companies who need metal parts made might have one factory they regularly work with. But if there are any circumstances that might mean that this factory cannot carry out a job, then the customer needs to shop around and find others to do it instead. This can be a time-consuming, and costly process.

“It’s a very fragmented market and there are so many ways to manufacture products, and the connection between those two is complicated,” he said. “In the past, if you wanted to outsource something, it would mean multiple emails to multiple places. But you can’t go to 30 different suppliers like that individually. We make it into a one-stop shop.”

On the other side, factories are always looking for better ways to fill out their roster of work so there is little downtime — factories want to avoid having people paid to work with no work coming in, or machinery that is not being used.

“The average uptime capacity is 50%,” Vares said of the metalwork plants on Fractory’s platform (and in the industry in general). “We have a lot more machines out there than are being used. We really want to solve the issue of leftover capacity and make the market function better and reduce waste. We want to make their factories more efficient and thus sustainable.”

The Fractory approach involves customers — today those customers are typically in construction, or other heavy machinery industries like ship building, aerospace and automotive — uploading CAD files specifying what they need made. These then get sent out to a network of manufacturers to bid for and take on as jobs — a little like a freelance marketplace, but for manufacturing jobs. About 30% of those jobs are then fully automated, while the other 70% might include some involvement from Fractory to help advise customers on their approach, including in the quoting of the work, manufacturing, delivery and more. The plan is to build in more technology to improve the proportion that can be automated, Vares said. That would include further investment in RPA, but also computer vision to better understand what a customer is looking to do, and how best to execute it.

Currently Fractory’s platform can help fill orders for laser cutting and metal folding services, including work like CNC machining, and it’s next looking at industrial additive 3D printing. It will also be looking at other materials like stonework and chip making.

Manufacturing is one of those industries that has in some ways been very slow to modernize, which in a way is not a huge surprise: equipment is heavy and expensive, and generally the maxim of “if it ain’t broke, don’t fix it” applies in this world. That’s why companies that are building more intelligent software to at least run that legacy equipment more efficiently are finding some footing. Xometry, a bigger company out of the U.S. that also has built a bridge between manufacturers and companies that need things custom made, went public earlier this year and now has a market cap of over $3 billion. Others in the same space include Hubs (which is now part of Protolabs) and Qimtek, among others.

One selling point that Fractory has been pushing is that it generally aims to keep manufacturing local to the customer to reduce the logistics component of the work to reduce carbon emissions, although as the company grows it will be interesting to see how and if it adheres to that commitment.

In the meantime, investors believe that Fractory’s approach and fast growth are strong signs that it’s here to stay and make an impact in the industry.

“Fractory has created an enterprise software platform like no other in the manufacturing setting. Its rapid customer adoption is clear demonstrable feedback of the value that Fractory brings to manufacturing supply chains with technology to automate and digitise an ecosystem poised for innovation,” said Marcin Hejka in a statement. “We have invested in a great product and a talented group of software engineers, committed to developing a product and continuing with their formidable track record of rapid international growth

Powered by WPeMatico

On the heels of Heroes announcing a $200 million raise earlier today, to double down on buying and scaling third-party Amazon Marketplace sellers, another startup out of London aiming to do the same is announcing some significant funding of its own. Olsam, a roll-up play that is buying up both consumer and B2B merchants selling on Amazon by way of Amazon’s FBA fulfillment program, has closed $165 million — a combination of equity and debt that it will be using to fuel its M&A strategy, as well as continue building out its tech platform and to hire more talent.

Apeiron Investment Group — an investment firm started by German entrepreneur Christian Angermayer — led the Series A equity round, with Elevat3 Capital (another Angermayer firm that has a strategic partnership with Founders Fund and Peter Thiel) also participating. North Wall Capital was behind the debt portion of the deal. We have asked and Olsam is only disclosing the full amount raised, not the amount that was raised in equity versus debt. Valuation is also not being disclosed.

Being an Amazon roll-up startup from London that happens to be announcing a fundraise today is not the only thing that Olsam has in common with Heroes. Like Heroes, Olsam is also founded by brothers.

Sam Horbye previously spent years working at Amazon, including building and managing the company’s business marketplace (the B2B version of the consumer marketplace); while co-founder Ollie Horbye had years of experience in strategic consulting and financial services.

Between them, they also built and sold previous marketplace businesses, and they believe that this collective experience gives Olsam — a portmanteau of their names, “Ollie” and “Sam” — a leg up when it comes to building relationships with merchants; identifying quality products (versus the vast seas of search results that often feel like they are selling the same inexpensive junk as each other); and understanding merchants’ challenges and opportunities, and building relationships with Amazon and understanding how the merchant ecosystem fits into the e-commerce giant’s wider strategy.

Olsam is also taking a slightly different approach when it comes to target companies, by focusing not just on the usual consumer play, but also on merchants selling to businesses. B2B selling is currently one of the fastest-growing segments in Amazon’s Marketplace, and it is also one of the more overlooked by consumers. “It’s flying under the radar,” Ollie said.

“The B2B opportunity is very exciting,” Sam added. “A growing number of merchants are selling office supplies or more random products to the B2B customer.”

Estimates vary when it comes to how many merchants there are selling on Amazon’s Marketplace globally, ranging anywhere from 6 million to nearly 10 million. Altogether those merchants generated $300 million in sales (gross merchandise value), and it’s growing by 50% each year at the moment.

And consolidating sellers — in order to achieve better economies of scale around supply chains, marketing tools and analytics, and more — is also big business. Olsam estimates that some $7 billion has been spent cumulatively on acquiring these businesses, and there are more out there: Olsam estimates there are some 3,000 businesses in the U.K. alone making more than $1 million each in sales on Amazon’s platform.

(And to be clear, there are a number of other roll-up startups beyond Heroes also eyeing up that opportunity. Raising hundreds of millions of dollars in aggregate, others that have made moves this year include Suma Brands [$150 million], Elevate Brands [$250 million], Perch [$775 million], factory14 [$200 million], Thrasio [currently probably the biggest of them all in terms of reach and money raised and ambitions], Heyday, The Razor Group, Branded, SellerX, Berlin Brands Group [X2], Benitago, Latin America’s Valoreo and Rainforest and Una Brands out of Asia.)

“The senior team behind Olsam is what makes this business truly unique,” said Angermayer in a statement. “Having all been successful in building and selling their own brands within the market and having worked for Amazon in their marketplace team – their understanding of this space is exceptional.”

Powered by WPeMatico

Heroes, one of the new wave of startups aiming to build big e-commerce businesses by buying up smaller third-party merchants on Amazon’s Marketplace, has raised another big round of funding to double down on that strategy. The London startup has picked up $200 million, money that it will mainly be using to snap up more merchants. Existing brands in its portfolio cover categories like babies, pets, sports, personal health and home and garden categories — some of them, like PremiumCare dog chews, the Onco baby car mirror, gardening tool brand Davaon and wooden foot massager roller Theraflow, category best-sellers — and the plan is to continue building up all of these verticals.

Crayhill Capital Management, a fund based out of New York, is providing the funding, and Riccardo Bruni — who co-founded the company with twin brother Alessio and third brother Giancarlo — said that the bulk of it will be going toward making acquisitions, and is therefore coming in the form of debt.

Raising debt rather than equity at this point is pretty standard for companies like Heroes. Heroes itself is pretty young: it launched less than a year ago, in November 2020, with $65 million in funding, a round comprised of both equity and debt. Other investors in the startup include 360 Capital, Fuel Ventures and Upper 90.

Heroes is playing in what is rapidly becoming a very crowded field. Not only are there tens of thousands of businesses leveraging Amazon’s extensive fulfillment network to sell goods on the e-commerce giant’s marketplace, but some days it seems we are also rapidly approaching a state of nearly as many startups launching to consolidate these third-party sellers.

Many a roll-up play follows a similar playbook, which goes like this: Amazon provides the marketplace to sell goods to consumers, and the infrastructure to fulfill those orders, by way of Fulfillment By Amazon and its Prime service. Meanwhile, the roll-up business — in this case Heroes — buys up a number of the stronger companies leveraging FBA and the marketplace. Then, by consolidating them into a single tech platform that they have built, Heroes creates better economies of scale around better and more efficient supply chains, sharper machine learning and marketing and data analytics technology, and new growth strategies.

What is notable about Heroes, though — apart from the fact that it’s the first roll-up player to come out of the U.K., and continues to be one of the bigger players in Europe — is that it doesn’t believe that the technology plays as important a role as having a solid relationship with the companies it’s targeting, key given that now the top marketplace sellers are likely being feted by a number of companies as acquisition targets.

“The tech is very important,” said Alessio in an interview. “It helps us build robust processes that tie all the systems together across multiple brands and marketplaces. But what we have is very different from a SaaS business. We are not building an app, and tech is not the core of what we do. From the acquisitions side, we believe that human interactions ultimately win. We don’t think tech can replace a strong acquisition process.”

Image Credits: Heroes

Heroes’ three founder-brothers (two of them, Riccardo and Alessio, pictured above) have worked across a number of investment, finance and operational roles (the CVs include Merrill Lynch, EQT Ventures, Perella Weinberg Partners, Lazada, Nomura and Liberty Global) and they say there have been strong signs so far of its strategy working: of the brands that it has acquired since launching in November, they claim business (sales) has grown five-fold.

Collectively, the roll-up startups are raising hundreds of millions of dollars to fuel these efforts. Other recent hopefuls that have announced funding this year include Suma Brands ($150 million); Elevate Brands ($250 million); Perch ($775 million); factory14 ($200 million); Thrasio (currently probably the biggest of them all in terms of reach and money raised and ambitions), Heyday, The Razor Group, Branded, SellerX, Berlin Brands Group (X2), Benitago, Latin America’s Valoreo and Rainforest and Una Brands out of Asia.

The picture that is emerging across many of these operations is that many of these companies, Heroes included, do not try to make their particular approaches particularly more distinctive than those of their competitors, simply because — with nearly 10 million third-party sellers today on Amazon globally — the opportunity is likely big enough for all of them, and more, not least because of current market dynamics.

“It’s no secret that we were inspired by Thrasio and others,” Riccardo said. “Combined with COVID-19, there has been a massive acceleration of e-commerce across the continent.” It was that, plus the realization that the three brothers had the right e-commerce, fundraising and investment skills between them, that made them see what was a ‘perfect storm’ to tackle the opportunity, he continued. “So that is why we jumped into it.”

In the case of Heroes, while the majority of the funding will be used for acquisitions, it’s also planning to double headcount from its current 70 employees before the end of this year with a focus on operational experts to help run their acquired businesses.

Powered by WPeMatico

As artificial intelligence continues to weave its way into more enterprise applications, a startup that has built a platform to help businesses, especially non-tech organizations, build more customized AI decision-making tools for themselves has picked up some significant growth funding. Peak AI, a startup out of Manchester, England, that has built a “decision intelligence” platform, has raised $75 million, money that it will be using to continue building out its platform, expand into new markets and hire some 200 new people in the coming quarters.

The Series C is bringing a very big name investor on board. It is being led by SoftBank Vision Fund 2, with previous backers Oxx, MMC Ventures, Praetura Ventures and Arete also participating. That group participated in Peak’s Series B of $21 million, which only closed in February of this year. The company has now raised $119 million; it is not disclosing its valuation.

(This latest funding round was rumored last week, although it was not confirmed at the time and the total amount was not accurate.)

Richard Potter, Peak’s CEO, said the rapid follow-on in funding was based on inbound interest, in part because of how the company has been doing.

Peak’s so-called Decision Intelligence platform is used by retailers, brands, manufacturers and others to help monitor stock levels and build personalized customer experiences, as well as other processes that can stand to have some degree of automation to work more efficiently, but also require sophistication to be able to measure different factors against each other to provide more intelligent insights. Its current customer list includes the likes of Nike, Pepsico, KFC, Molson Coors, Marshalls, Asos and Speedy, and in the last 12 months revenues have more than doubled.

The opportunity that Peak is addressing goes a little like this: AI has become a cornerstone of many of the most advanced IT applications and business processes of our time, but if you are an organization — and specifically one not built around technology — your access to AI and how you might use it will come by way of applications built by others, not necessarily tailored to you, and the costs of building more tailored solutions can often be prohibitively high. Peak claims that those using its tools have seen revenues on average rise 5%, return on ad spend double, supply chain costs reduce by 5% and inventory holdings (a big cost for companies) reduce by 12%.

Peak’s platform, I should point out, is not exactly a “no-code” approach to solving that problem — not yet at least: It’s aimed at data scientists and engineers at those organizations so that they can easily identify different processes in their operations where they might benefit from AI tools, and to build those out with relatively little heavy lifting.

There have also been different market factors that have played a role. COVID-19, for example, and the boost that we have seen both in increasing “digital transformation” in businesses and making e-commerce processes more efficient to cater to rising consumer demand and more strained supply chains have all led to businesses being more open and keen to invest in more tools to improve their automation intelligently.

This, combined with Peak AI’s growing revenues, is part of what interested SoftBank. The investor has been long on AI for a while; but it also has been building out a section of its investment portfolio to provide strategic services to the kinds of businesses in which it invests.

Those include e-commerce and other consumer-facing businesses, which make up one of the main segments of Peak’s customer base.

Notably, one of its recent investments specifically in that space was made earlier this year, also in Manchester, when it took a $730 million stake (with potentially $1.6 billion more down the line) in The Hut Group, which builds software for and runs D2C businesses.

“In Peak we have a partner with a shared vision that the future enterprise will run on a centralized AI software platform capable of optimizing entire value chains,” Max Ohrstrand, senior investor for SoftBank Investment Advisers, said in a statement. “To realize this a new breed of platform is needed and we’re hugely impressed with what Richard and the excellent team have built at Peak. We’re delighted to be supporting them on their way to becoming the category-defining, global leader in Decision Intelligence.”

It’s not clear that SoftBank’s two Manchester interests will be working together, but it’s an interesting synergy if they do, and most of all highlights one of the firm’s areas of interest.

Longer term, it will be interesting to see how and if Peak evolves to extend its platform to a wider set of users at the organizations that are already its customers.

Potter said he believes that “those with technical predispositions” will be the most likely users of its products in the near and medium term. You might assume that would cut out, for example, marketing managers, although the general trend in a lot of software tools has precisely been to build versions of the same tools used by data scientists for these less technical people to engage in the process of building what it is that they want to use.

“I do think it’s important to democratize the ability to stream data pipelines, and to be able to optimize those to work in applications,” Potter added.

Powered by WPeMatico

The buildout of 5G networks continues apace, with wide-scale deployments across much of the developed world. Yet, one of the largest challenges with closing the gaps in coverage maps are constraints on 5G transmissions. Because of the spectrum that 5G technology uses compared to 4G, telecom operators need to install many times more towers to deliver the advertised bandwidth with the same quality signal that users expect.

Installing cell towers is a daunting proposition though. An operator has to find exactly the right location in terms of line of sight to users, then make sure the location has power and internet access, and then negotiate a contract with the property owner to keep the tower there for a decade or more. Now repeat tens of thousands of times (and maybe even more).

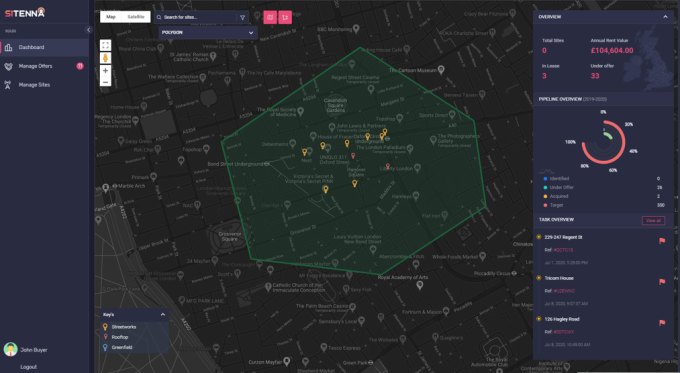

Sitenna, which will debut next week as part of Y Combinator’s Summer 2021 Demo Day, wants to radically speed up the process of selecting tower sites and securing contracts, creating a marketplace for landlords, tower operators and telcos alike.

Tower siting and access to poles have in some cases emerged as national infrastructure priorities. In the United States, the challenges around installing new towers — and new towers quickly — became a top priority of the FCC during the Trump administration, which launched a 5G FAST Plan to try to ease regulations around tower installation.

Sitenna’s founders Daniel Campion and Brian Sexton saw an opportunity with such programs to help with the movement. Over the past year, they have built out what is essentially a marketplace that on one hand helps property owners figure out if they have an asset that’s worth investigating for telecom usage, and on the other, helps tower operators select and digitally sign deals for installation.

Sitenna co-founder and CEO Daniel Campion. Image Credits: Sitenna

The company launched in the United Kingdom in June, and “it kind of resonated,” Campion said, noting that 65,000 real estate assets and roughly 15% of the towers in the U.K. are now on the platform. The company has kicked off two pilots with Vodafone and its tower provider Cornerstone. He said the company intends to enter the U.S. market in the first quarter of next year.

While the company is starting with a marketplace, like many startups today, it is also augmenting that marketplace with B2B SaaS tools. In its case, that means tools for telcos to manage the process of onboarding a new tower location and then managing the asset. “Once they find the site, they ping pong emails back and forth,” Campion said. “So we have built some tools to help them on their workflows.”

Sitenna’s platform allows landlords and tower operators to inspect and transact tower locations. Image Credits: Sitenna

While there is definitely a large wave of tower installations underway now with the transition to 5G wireless, that wave doesn’t mean that tower installation will suddenly dry up in a few years. Campion notes that there is a “continual refresh of 15-20% on the carrier side” due to everything from changing usage patterns and building redevelopment to just standard hardware replacement.

And of course, there is always 6G, which while completely amorphous today, is a real thing that I get invites to conferences for. There’s always going to be a next generation of wireless, and Sitenna wants to become the center for managing that infrastructure.

Powered by WPeMatico