unicorns

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

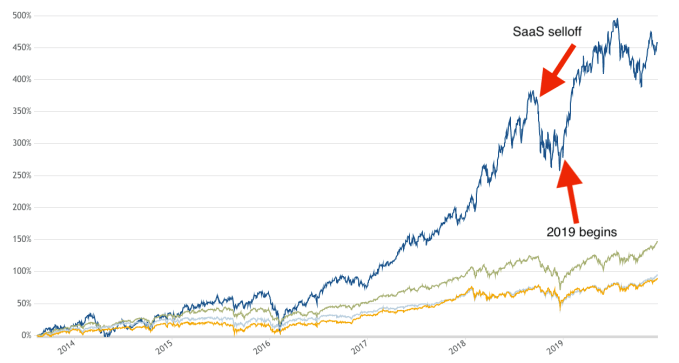

Today, something short. Continuing our loose collection of looks back of the past year, it’s worth remembering two related facts. First, that this time last year SaaS stocks were getting beat up. And, second, that in the ensuing year they’ve risen mightily.

If you are in a hurry, the gist of our point is that the recovery in value of SaaS stocks probably made a number of 2019 IPOs possible. And, given that SaaS shares have recovered well as a group, that the 2020 IPO season should be active as all heck, provided that things don’t change.

Let’s not forget how slack the public markets were a year ago for a startup category vital to venture capital returns.

We’re depending on Bessemer’s cloud index today, renamed the “BVP Nasdaq Emerging Cloud Index” when it was rebuilt in October. The Cloud Index is a collection of SaaS and cloud companies that are trackable as a unit, helping provide good data on the value of modern software and tooling concerns.

If the index rises, it’s generally good news for startups as it implies that investors are bidding up the value of SaaS companies as they grow; if the index falls, it implies that revenue multiples are contracting amongst the public comps of SaaS startups.*

Ultimately, startups want public companies that look like them (comps) to have sky-high revenue multiples (price/sales multiples, basically). That helps startups argue for a better valuation during their next round; or it helps them defend their current valuation as they grow.

Given that it’s Christmas Eve, I’m going to present you with a somewhat ugly chart. Today I can do no better. Please excuse the annotation fidelity as well:

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today we’re exploring the 2019 IPO cohort from a capital-in perspective. How much did tech companies going public in 2019 raise before they went public, and what impact that did that have on their valuation when they debuted?

Looking ahead, the tech startups and other venture-backed companies expected to go public in 2020 will include a similar mix of mid-sized offerings, unicorn debuts and perhaps a huge direct listing. What we’ve seen in 2019 should be a good prelude to the 2020 IPO market.

With that in mind, let’s examine how much money tech companies that went public this year raised before their IPO. Spoiler: It’s a lot more than was normal just a few years ago. Afterwards, I have a question regarding what to call companies in the $100 million ARR club (more here) that we’ve been exploring lately. Let’s go!

According to CBInsights’ recent IPO 2020 IPO report, there’s a sharp, upward swing in the amount of capital that tech companies raise before they go public. It’s so steep that the data draw a nearly linear breakout from a preceding, comfortable normal.

Here’s the chart:

There are two distinct periods; from 2012 to 2015, raising up to $100 million was the norm (median) for tech companies going public. That’s still a lot of cash, mind.

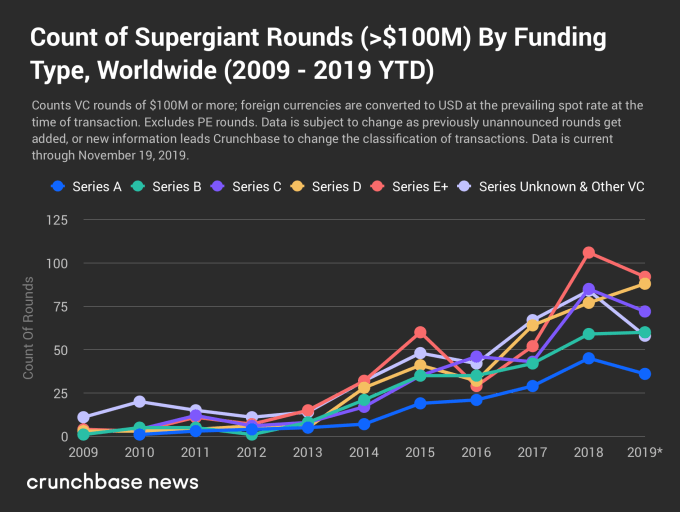

The second period is more exciting. From 2016 on we can see a private capital arms race in which tech companies going public stacked ever-greater sums under their mattresses before debuting. This is generally consistent with a different trend that you are also aware of, namely the rise of $100 million financings.

Before we turn back to the CBInsights data, let’s observe a chart from Crunchbase News that underscores the simply astounding rise of $100 million financings that was published just a few weeks ago. As you look at this chart, remember that prior to 2016, more than half of venture-backed technology companies going public had raised less than $100 million total:

Now, compare the two data sets.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today we’re taking stock of a cohort of special companies: still-private startups that have reached $100 million in annual recurring revenue (ARR). Our goal is to understand which startup companies are actually exceptional. This late in the unicorn era, hundreds of companies around the world have reached a valuation of $1 billion, making the achievement somewhat pedestrian.

Reaching $100 million in ARR, however, still stands out.

We explored the idea earlier this week, citing Asana, Druva and WalkMe as private companies that recently reached $100 million ARR. In addition to that trio, Bill.com and Sprout Social, both of which went public this week, also crossed the nine-figure annual recurring revenue mark in 2019.

After we posted that short list, four other companies either just shy of $100 million ARR, or with a little bit more, reached out to TechCrunch, touting their own successes. Given that our point was that companies which reach the revenue threshold million are neat, it’s worth taking a moment to look at the other companies joining the $100 million ARR club.

For extra fun I got on the phone with a number of their CEOs to chat about their progress. We’ll start with a look at a company that is nearly a member of the club, and then talk about a few that recently punched their membership cards.

To be frank, I did not know that GitLab was as large as it is. Backed by more than $400 million in private capital, GitLab competes with the now-purchased GitHub as a developer resource and service. Its backers include Goldman Sachs, ICONIQ, GV, August Capital and Khosla.

GitLab became a unicorn back in September of 2018, when it raised $100 million at a $1 billion post-money valuation. Its more recent $268 million Series E raised this September pushed that valuation to nearly $2.8 billion.

It’s a good company for us to include, as it provides a good example of how far in advance a $1 billion valuation can precede a $100 million ARR business; in GitLab’s case, provided that it grows as expected, its unicorn valuation came nearly 1.5 years before reaching nine-figure ARR.

To understand more about the company’s growth, we caught up with its CEO Sid Sijbrandij (full discussion here), learning that he views the unicorn tag as a way to help a company brand itself, but something that is outside of his company’s control. Revenue, in his view, is “much more within your control.” According to Sijbrandij, GitLab is aiming for $1 billion in revenue in 2023 and has a November, 2020 IPO targeted.

GitLab is sharing its impending ARR milestone as it runs its whole business very transparently (hence why my chat with its CEO was live-streamed, and archived on YouTube). It will be super interesting to see if the company hits the ARR target on time, and then if it can also stick the landing with a Q4 2020 IPO.

Egnyte, a player in the enterprise productivity, storage and security spaces, has kept growing since its $75 million Series E it raised last October.

The company, backed by Goldman Sachs (again), GV (again) and Kleiner Perkins, has raised just $137.5 million to date. Reaching $100 million ARR on that level of funding means that Egnyte has run efficiently as a business. In fact, as TechCrunch has reported, Egnyte has occasionally made money on its path to the public markets.

TechCrunch has spoken to Egnyte’s CEO Vineet Jain a number of times, but it seemed appropriate to get him back on the phone now that his company is nearly ready to go public (at least in terms of size). According to Jain, in fresh data released to Extra Crunch:

Powered by WPeMatico

Freshworks, a company that makes a variety of business software tools, from CRM to help-desk software, announced a $150 million Series H investment today from Sequoia Capital, CapitalG (formerly Google Capital) and Accel on a hefty $3.5 billion valuation. The late-stage startup has raised almost $400 million, according to Crunchbase data.

The company has been building an enterprise SaaS platform to give customers a set of integrated business tools, but CEO and co-founder Girish Mathrubootham says they will be investing part of this money in R&D to keep building out the platform.

To that end, the company also announced today a new unified data platform called the “Customer-for-Life Cloud” that runs across all of its tools. “We are actually investing in really bringing all of this together to create the “Customer-for-Life Cloud,” which is how you take marketing, sales, support and customer success — all of the aspects of a customer across the entire life cycle journey and bring them to a common data model where a business that is using Freshworks can see the entire life cycle of the customer,” Mathrubootham explained.

While Mathrubootham was not ready to commit to an IPO, he said they are in the process of hiring a CFO and are looking ahead to one day becoming a public company. “We don’t have a definite timeline. We want to go public at the right time. We are making sure that as a company that we are ready with the right processes and teams and predictability in the business,” he said.

In addition, he says he will continue to look for good acquisition targets, and having this money in the bank will help the company fill in gaps in the product set should the right opportunity arise. “We don’t generally acquire revenue, but we are looking for good technology teams both in terms of talent, as well as technology that would help give us a jumpstart in terms of go-to-market.” It hasn’t been afraid to target small companies in the past, having acquired 12 already.

Freshworks, which launched in 2010, has almost 2,500 employees, a number that’s sure to go up with this new investment. It has 250,00 customers worldwide, including almost 40,000 paying customers. These including Bridgestone Tires, Honda, Hugo Boss, Toshiba and Cisco.

Powered by WPeMatico

GitLab is a company that doesn’t pull any punches or try to be coy. It actually has had a page on its website for some time stating it intends to go public on November 18, 2020. You don’t see that level of transparency from late-stage startups all that often. Today, the company announced a huge $268 million Series E on a tidy $2.75 billion valuation.

Investors include Adage Capital Management, Alkeon Capital, Altimeter Capital, Capital Group, Coatue Management, D1 Capital Partners, Franklin Templeton, Light Street Capital, Tiger Management Corp. and Two Sigma Investments.

The company seems to be primed and ready for that eventual IPO. Last year, GitLab co-founder and CEO Sid Sijbrandij said that his CFO Paul Machle told him he wanted to begin planning to go public, and he would need two years in advance to prepare the company. As Sijbrandij tells it, he told him to pick a date.

“He said, I’ll pick the 16th of November because that’s the birthday of my twins. It’s also the last week before Thanksgiving, and after Thanksgiving, the stock market is less active, so that’s a good time to go out,” Sijbrandij told TechCrunch.

He said that he considered it a done deal and put the date on the GitLab Strategy page, a page that outlines the company’s plans for everything it intends to do. It turned out that he was a bit too quick on the draw. Machle had checked the date in the interim and realized that it was a Monday, which is not traditionally a great day to go out, so they decided to do it two days later. Now the target date is officially November 18, 2020.

GitLab has the date it’s planning to go public listed on its Strategy page.

As for that $268 million, it gives the company considerable runway ahead of that planned event, but Sijbrandij says it also gives him flexibility in how to take the company public. “One other consideration is that there are two options to go public. You can do an IPO or direct listing. We wanted to preserve the optionality of doing a direct listing next year. So if we do a direct listing, we’re not going to raise any additional money, and we wanted to make sure that this is enough in that case,” he explained.

Sijbrandij says that the company made a deliberate decision to be transparent early on. Being based on an open-source project, it’s sometimes tricky to make that transition to a commercial company, and sometimes that has a negative impact on the community and the number of contributions. Transparency was a way to combat that, and it seems to be working.

He reports that the community contributes 200 improvements to the GitLab open-source product every month, and that’s double the amount of just a year ago, so the community is still highly active in spite of the parent company’s commercial success.

It did not escape his notice that Microsoft acquired GitHub last year for $7.5 billion. It’s worth noting that GitLab is a similar kind of company that helps developers manage and distribute code in a DevOps environment. He claims in spite of that eye-popping number, his goal is to remain an independent company and take this through to the next phase.

“Our ambition is to stay an independent company. And that’s why we put out the ambition early to become a listed company. That’s not totally in our control as the majority of the company is owned by investors, but as long as we’re more positive about the future than the people around us, I think we can we have a shot at not getting acquired,” he said.

The company was founded in 2014 and was a member of Y Combinator in 2015. It has been on a steady growth trajectory ever since, hauling in more than $426 million. The last round before today’s announcement was a $100 million Series D last September.

Powered by WPeMatico

On Wednesday a few unicorns were born. You’ve already forgotten their names if you learned them at all (Tip: It was Marqeta and Ivalua.)

Don’t worry, I’m not cross with you. It’s merely that there are so many unicorns in the market today — they stampede by the hundred in 2019 — that they are impossible to keep tabs on.

In fact, so many firms now make the cut that we’ve gotten into the habit of torturing the word “unicorn” to mean more than what it was originally tasked to describe. As we wrote recently, there are undercorns now, and decacorns. Toss in minotaurs and horses and the inevitable centacorns and see, we’re all bored.

Paraphrasing Asimov, successive shocks lead to decreasing impact. So has the phrase unicorn lost all meaning. As I joked the other day, it now mostly means “middle-aged startup.” Even our redefinition of the word “startup” allowed for firms to be worth several billion and still claim the title, though that might have been an error.

In today’s world of super- and hypergiant rounds, it’s not impossible to put together a unicorn. And people sure are doing it.

“Unicorn” is now only useful as a valuation-descriptor. It no longer implies something rare.

So, what we need is either a redefinition of a unicorn to make it rarer… or, we need an entirely new concept. Regardless of if we change up what “unicorn” itself means, or invent a new word, it has become clear what we need to add to the mix to really tease out the exceptional companies from the merely very good.

Profits.

Zoom, before its IPO, was profitable and growing like hell. TransferWise, we recently learned, is profitable and growing as well. Can you name another company worth $1 billion or more that is growing and profitable? I can’t. That means they are rare.

TechCrunch’s Kate Clark and I chatted about this on Equity, and this was our general point of agreement (her tweet here). Profit is what really makes you rare. Not just a high valuation. There’s enough money flying around to print the latter by the dozen. Earning the former? Now’s that’s legendary and hard to find.

Just like a unicorn.

Powered by WPeMatico

If you’re hoping to create a unicorn on a budget, look to the European technology sector for inspiration. Despite the well-documented increase in available funding for tech companies across the continent, startups are reaching unicorn status with much lower totals of venture capital than U.S. rivals. In fact, this level of “capital efficiency” is one major attraction for international investors weary of the “burn rate” of many U.S. companies aspiring to valuations of $1 billion+.

It costs a staggering 50-100 percent more in the U.S. to create a company valued at $1 billion than in Europe. For U.S. tech companies that achieved unicorn status in 2018, the median amount of funding required was more than $125 million, whereas their contemporaries in Europe required a lesser total of $80 million. For 2017, the gap was even wider; U.S. companies again required just over $100 million, the smaller pool of Europeans slightly above $50 million.

| Region | Year | Median funding required prior to reaching a valuation of $1B |

| U.S. | 2017 | $107 million |

| Europe | 2017 | $53.15 million |

| U.S. | 2018 | $125.38 million |

| Europe | 2018 | $80.8 million |

The median funding secured prior to (not including) the round in which tech companies in the U.S. and Europe achieved a $1 billion valuation during 2017/18 (Data source: PitchBook)

A key reason for this greater efficiency in scaling is because European companies have had to make do with less. Europe has historically had a much smaller pool of “late-stage growth” funding (typically rounds of $30-75 million), and even today it is far easier to raise $20 million for a European tech company than $50 million, while that does not hold true in the U.S. to anywhere near the same degree.

This dearth of late-stage money has forced European tech companies to scale more efficiently, with lower overheads and a focus on profitability at an earlier stage, rather than the aggressive growth patterns often witnessed in the U.S. But this “enforced prudence” has come at a price.

Greater capital efficiency has arguably resulted in fewer European tech companies achieving unicorn status, with Europe lagging far behind the number created each year in the U.S. In 2018, the U.S. birthed 53 unicorns; Europe, only 10. So how much funding is required to close the gap?

Let’s assume (safely) product innovation and quality is available both in the U.S. and Europe, and let’s assume (less safely) there are many more quality European companies built to “unicorn potential” that are currently unable to raise enough to fuel scale to the point where they achieve $1 billion valuations. To plug this funding gap, we estimate Europe would require a multi-year capital pool of $10-20 billion in additional late-stage capital.

That math is based on a large number, up to 40, of companies a year missing out on becoming unicorns because of a lack of available funding, alongside the assumption that each unicorn needs more than $100 million in funding in total.

The extremely good news is that it is not $100 billion. Due to the inherent efficiency of risk capital, $10-20 billion can go an awfully long way. Arguably, there is no other industry or sector that can yield such a high return on committed money within a reasonably short few years.

No, Europe is still a trickier market to scale than the U.S. Not only does Europe have to compete with the ready availability of capital in the U.S., but different regulatory environments, language barriers and a brain drain of talent attracted to Silicon Valley all combine to create impediments for European tech companies scaling in an interconnected world.

Funding, however, stands as the simplest of limiting factors to address. Especially when an analysis of the stats shows that whilst European tech companies are “saving” a lot of money, this directly contributes to far fewer of them being worth the mythical $1 billion+. A marginal uplift in capital would produce a disproportionately higher number of unicorns.

Powered by WPeMatico

In Silicon Valley, investors don’t expect their portfolio companies to be profitable. “Blitzscaling: The Lightning-Fast Path to Building Massively Valuable Companies,” a bible for founders, instead calls for heavy spending on growth to scale in an Amazon -like fashion.

As for Wall Street, it’s shown an affinity for stock in Jeff Bezos’ business, despite the many years it spent navigating a path to profitability, as well as other money-losing endeavors. Why? Because it too is far less concerned with profitability than market opportunity.

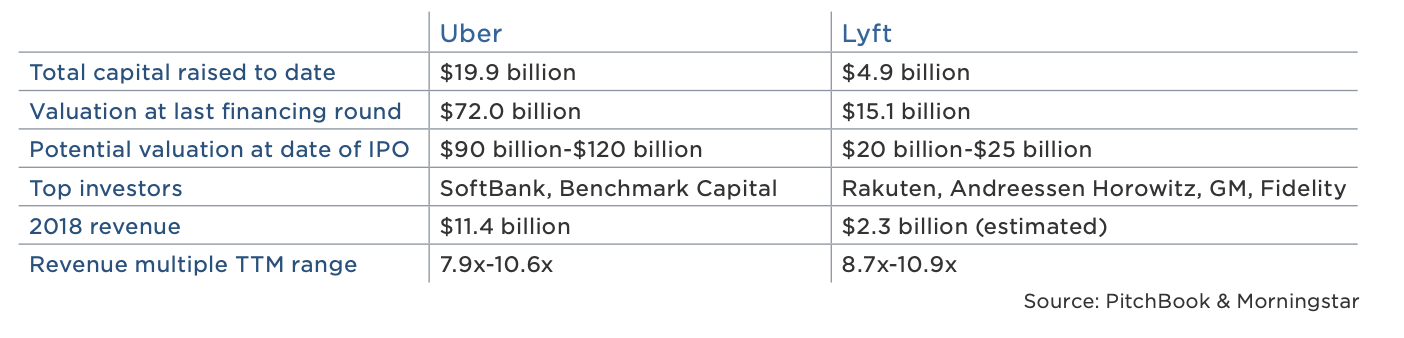

Lyft, a ride-hailing company expected to go public this week, is not profitable. It posted losses of $911 million in 2018, a statistic that will make it the biggest loser amongst U.S. startups to have gone public, according to data collected by The Wall Street Journal. On the other hand, Lyft’s $2.2 billion in 2018 revenue places it atop the list of largest annual revenues for a pre-IPO business, trailing behind only Facebook and Google in that category.

Wall Street, in short, is betting on Lyft’s revenue growth, assuming it will narrow its loses and reach profitability… eventually.

Lyft, losses notwithstanding, is growing rapidly and Wall Street is paying attention. On the second day of its road show, reports emerged that its IPO was already oversubscribed. As a result, Lyft is said to have upped the cost of its stock, with new plans to raise more than $2 billion at a valuation upwards of $25 billion. That represents a revenue multiple of more than 11x, a step up multiple of more than 1.6x from its most recent private valuation of $15.1 billion and, of course, Wall Street’s insatiable desire for unicorns, profitable or not.

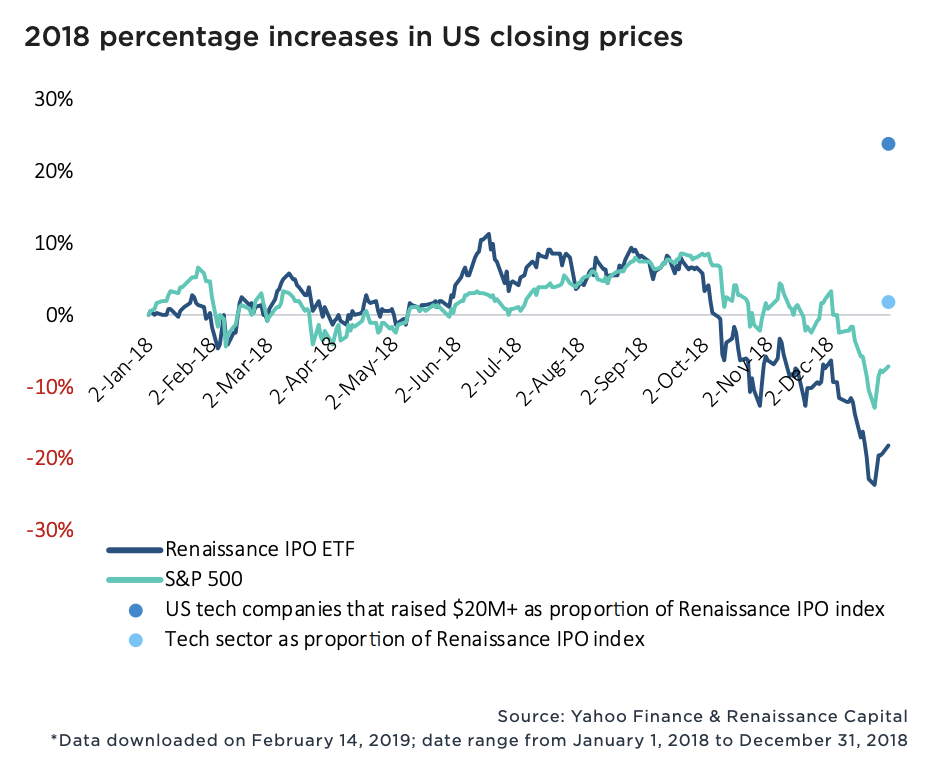

New data from PitchBook exploring the performance of billion-dollar-plus VC exits confirms Wall Street’s leniency toward unprofitable tech companies. Sixty-four percent of the 100+ companies valued at more than $1 billion to complete a VC-backed IPO since 2010 were unprofitable, and in 2018, money-losing startups actually fared better on the stock exchange than money-earning businesses. Moreover, U.S. tech companies that had raised more than $20 million traded up nearly 25 percent of 2018, while the S&P 500 technology sector posted flat returns.

Wall Street is still adapting to the rapid growth of the tech industry; public markets investors, therefore, are willing to deal with negative to minimal cash flows for, well, a very long time.

There’s no doubt Lyft and its much larger competitor, Uber, will go public at monstrous valuations. The two IPOs, set to create a whole bunch of millionaires and return a number of venture capital funds, will provide Silicon Valley a lesson in Wall Street’s tolerance for outsized exits.

Much like a seed-stage investor must bet on a founder’s vision, Wall Street, given a choice of several unprofitable businesses, has to bet on potential market value. Fortunately, this strategy can work quite well. Take Floodgate, for example. The seed fund invested a small amount of capital in Lyft when it was still a quirky idea for ridesharing called Zimride. Now, it boasts shares worth more than $100 million. I’m sure early shareholders in Amazon — which went public as a money-losing company in 1997 — are pretty happy, too.

Ultimately, Wall Street’s appetite for unicorns like Lyft is a result of the shortage of VC-backed IPOs. In 2006, it was the norm for a company to make its stock market debut at 7.9 years old, per PitchBook. In 2018, companies waited until the ripe age of 10.9 years, causing a significant slowdown in big liquidity events and stock sales.

Fund sizes, however, have grown larger and the proliferation of unicorns continues at unforeseen rates. That may mean, eventually, an influx of publicly shared unicorn stock. If that’s the case, might Wall Street start asking more of these startups? At the very least, public market investors, please don’t be swayed by WeWork‘s eventual stock offering and its “community adjusted EBITDA.” Silicon Valley’s pixie dust can’t be that potent.

Powered by WPeMatico

Looker has been helping customers visualize and understand their data for seven years, and today it got a big reward, a $103 million Series E investment on a $1.6 billion valuation.

The round was led by Premji Invest, with new investment from Cross Creek Advisors and participation from the company’s existing investors. With today’s investment, Looker has raised $280.5 million, according the company.

In spite of the large valuation, Looker CEO Frank Bien really wasn’t in the mood to focus on that particular number, which he said was arbitrary, based on the economic conditions at the time of the funding round. He said having an executive team old enough to remember the dot-com bubble from the late 1990s and the crash of 2008 keeps them grounded when it comes to those kinds of figures.

Instead, he preferred to concentrate on other numbers. He reported that the company has 1,600 customers now and just crossed the $100 million revenue run rate, a significant milestone for any enterprise SaaS company. What’s more, Bien reports revenue is still growing 70 percent year over year, so there’s plenty of room to keep this going.

He said he took such a large round because there was interest and he believed that it was prudent to take the investment as they move deeper into enterprise markets. “To grow effectively into enterprise customers, you have to build more product, and you have to hire sales teams that take longer to activate. So you look to grow into that, and that’s what we’re going to use this financing for,” Bien told TechCrunch.

He said it’s highly likely that this is the last private fundraising the company will undertake as it heads toward an IPO at some point in the future. “We would absolutely view this as our last round unless something drastic changed,” Bien said.

For now, he’s looking to build a mature company that is ready for the public markets whenever the time is right. That involves building internal processes of a public company even if they’re not there yet. “You create that maturity either way, and I think that’s what we’re doing. So when those markets look okay, you could look at that as another funding source,” he explained.

The company currently has around 600 employees. Bien indicated that they added 200 this year alone and expect to add additional headcount in 2019 as the business continues to grow and they can take advantage of this substantial cash infusion.

Powered by WPeMatico

Is there a point when investors will turn off the spigots for giant unicorn funding rounds? If so, we haven’t reached that threshold yet. Here, we break down the leading locations for new and existing unicorns, top sectors for investment capital, exits and a few other trends affecting the space. Read More

Is there a point when investors will turn off the spigots for giant unicorn funding rounds? If so, we haven’t reached that threshold yet. Here, we break down the leading locations for new and existing unicorns, top sectors for investment capital, exits and a few other trends affecting the space. Read More

Powered by WPeMatico