U.S. Securities and Exchange Commission

Auto Added by WPeMatico

Auto Added by WPeMatico

Popular messaging app Kik is, indeed, “here to stay” following an acquisition by the Los Angeles-based multimedia holding company, MediaLab.

It echoes the same message from Kik’s chief executive Tim Livingston last week when he rebuffed earlier reports that the company would shut down amid an ongoing battle with the U.S. Securities and Exchange Commission. Livingston had tweeted that Kik had signed a letter-of-intent with a “great company,” but that it was “not a done deal.”

Now we know the the company: MediaLab. In a post on Kik’s blog on Friday the MediaLab said that it has “finalized an agreement” to acquire Kik Messenger.

“Kik is one of those amazing places that brings us back to those early aspirations,” the blog post read. “Whether it be a passion for an obscure manga or your favorite football team, Kik has shown an incredible ability to provide a platform for new friendships to be forged through your mobile phone.”

MediaLab is a holding company that owns several other mobile properties, including anonymous social network Whisper and mixtape app DatPiff. In acquiring Kik, the holding company is expanding its mobile app portfolio.

MediaLab said it has “some ideas” for developing Kik going forwards, including making the app faster and reducing the amount of unwanted messages and spam bots. The company said it will introduce ads “over the coming weeks” in order to “cover our expenses” of running the platform.

Buying the Kik messaging platform adds another social media weapon to the arsenal for MediaLab and its chief executive, Michael Heyward .

Heyward was an early star of the budding Los Angeles startup community with the launch of the anonymous messaging service, Whisper nearly 8 years ago. At the time, the company was one of a clutch of anonymous apps — including Secret and YikYak — that raised tens of millions of dollars to offer online iterations of the confessional journal, the burn book, and the bathroom wall (respectively).

In 2017, TechCrunch reported that Whisper underwent significant layoffs to stave off collapse and put the company on a path to profitability.

At the time Whisper had roughly 20 million monthly active users across its app and website, which the company was looking to monetize through programmatic advertising, rather than brand-sponsored campaigns that had provided some of the company’s revenue in the past. Through widgets, the company had an additional 10 million viewers of its content per-month using various widgets and a reach of around 250 million through Facebook and other social networks on which it published posts.

People familiar with the company said at the time that it was seeing gross revenues of roughly $1 million and was going to hit $12.5 million in revenue for that calendar year. By 2018 that revenue was expected to top $30 million, according to sources at the time.

The flagship Whisper app let people post short bits of anonymous text and images that other folks could like or comment about. Heyward intended it to be a way for people to share more personal and intimate details — to be a social network for confessions and support rather than harassment.

The idea caught on with investors and Whisper managed to raise $61 million from investors including Sequoia, Lightspeed Venture Partners, and Shasta Ventures . Whisper’s last round was a $36 million Series C back in 2014.

Fast forward to 2018 when Secret had been shut down for three years while YikYak also went bust — selling off its engineering team to Square for around $1 million. Whisper, meanwhile, seemingly set up MediaLab as a holding company for its app and additional assets that Heyward would look to roll up. The company filed registration documents in California in June 2018.

According to the filings, Susan Stone, a partner with the investment firm Sierra Wasatch Capital, is listed as a director for the company.

Heyward did not respond to a request for comment.

Zack Whittaker contributed reporting for this article.

Powered by WPeMatico

In a wide-ranging conversation at TechCrunch Disrupt San Francisco last week, Postmates co-founder and chief executive officer Bastian Lehmann made light of the company’s lack of IPO documents.

The San Francisco-based on-demand delivery business was expected to publicly file its IPO prospectus in September in preparation for a fall exit, sources familiar with the matter told TechCrunch this summer. September, however, has come and gone and we’re still waiting on Postmates to release the critical document.

“The reality is that we will IPO when we believe we find the right time for the business and the right time for the markets,” Lehmann told TechCrunch. “And if you look at the markets right now, I believe they are a little choppy. They are a little choppy when it comes to growth companies specifically … We are hopeful that we find a good window to get out there.”

Lehmann made reference to Uber and other companies to recently float, citing market conditions as an IPO deterrent. Uber, Lyft, Slack and other fast-growing unicorns have struggled since entering the public markets earlier this year despite sky-high private market valuations. WeWork, a money-losing endeavor, recently decided to delay its IPO after demand from Wall Street devalued the business by the billions. Whether Postmates will complete its debut by the end of the year is unclear.

Postmates confidentially filed with the U.S. Securities and Exchange Commission for an IPO in February. Shortly after, Postmates held M&A talks with DoorDash, another food delivery unicorn, according to people familiar with the matter, but failed to come to mutually favorable terms. DoorDash has previously declined to comment on these reports. On stage last week, Lehmann declined to confirm the reports.

“I don’t think it does any good to speculate on M&A,” he said. “I think you have four well-funded players here in the U.S. in this space. I think everyone is well aware of the strengths and the weaknesses of each other and you know at some point down the line, if we take Europe for example, you will see consolidation in the market. People have conversations all the time but I wouldn’t read too much into it.”

Postmates operates its on-demand delivery platform, powered by a network of local gig economy workers, in more than 3,500 cities across all 50 states. The company does not yet operate in any international markets aside from Mexico City, however, Lehmann’s comments suggest the business could be plotting a foray into Europe, where Deliveroo, Just Eat and others dominate the market.

Postmates has raised about $900 million to date, including a $225 million round announced last month that valued the company at $2.4 billion. DoorDash, on the other hand, reached a $12.6 billion valuation in May with a $600 million Series G and has raised more than double that of Postmates. When asked why DoorDash, a similar and competing business, needed that much more capital, Lehmann joked “Maybe [DoorDash CEO Tony Xu] needs a jet, I don’t know.”

Postmates, founded in 2011 by Lehmann, is backed by Spark Capital, Founders Fund, Uncork Capital, Slow Ventures, Tiger Global, Blackrock and others. In our interview with Lehmann, the long-time CEO discussed the ‘choppy’ public markets, competitors, the company’s autonomous robotics delivery efforts and more.

Powered by WPeMatico

Brex, a Silicon Valley fintech darling, has lofty plans to battle big banks —and Stripe.

Code-named “Gemini,” Brex today announced a new product designed to replace and improve the functionality of traditional bank accounts. Brex Cash, as it will be known publicly, is a business cash management account integrated with the Brex Card, a corporate card for startups launched in 2018.

Brex tells us they’ve built the core banking infrastructure from scratch, allowing the company to forgo third-party processing fees and provide a much-needed tech infusion to antiquated banking systems. In partnership with Boston’s Radius Bank, Brex Cash will allow customers to send payments quickly and easily with no transaction fees attached. Rather, Brex plans to reward its users for making or receiving payments using Brex Cash with points redeemable for cash back, travel and air miles. Customers will also receive 1.6% yield on deposits.

It’s not a bank, but in practice, it can replace a bank, says Brex co-founder and co-chief executive officer Henrique Dubugras .

“Our idea is that new businesses —the new Y Combinator companies —we hope a big percent of them never open a bank account,” Dubugras tells TechCrunch.

Brex now has many similarities to a bank. What differentiates it is its lack of physical branches — it’s exclusively digital — and it’s insurance. Traditional banks are insured by the Federal Deposit Insurance Corporation (FDIC), which protects up to $250,000 per depositor. Brex Cash users are protected by the Securities Investor Protection Corporation (SIPC), a nonprofit agency overseen by the U.S. Securities and Exchange Commission that protects up to $500,000 and specializes in protecting customers of brokerage firms from the loss of cash and securities.

We think we’ve won a lot of credibility. Before, who was going to give their money to a random-ass startup called Brex? -Brex co-CEO Henrique Dubugras

Additionally, Brex invests its customers’ money in a money market mutual fund of U.S. treasury bonds. “If Brex goes out of business, customers’ money will be safe,” the company writes in a press statement. “The only scenario where money could be lost is if the U.S. government defaults.”

Brex Cash user interface

“It’s not that we are inventing this — this model exists with Fidelity,” says Dubugras. “Fidelity isn’t necessarily a bank — we are bringing that concept to businesses to give lower fees, better interest rates, better experiences and more security.”

Brex, a graduate of the winter 2017 Y Combinator cohort, has quickly become a Silicon Valley success story for the ages. The rapid adoption of its startup credit card, which doesn’t require a personal guarantee, and its ability to issue cards instantly and provide higher limits than other options on the market has attracted thousands of customers and venture capitalists. The business, led by a pair of young Brazilian repeat entrepreneurs, including Dubugras and co-CEO Pedro Franceschi, has collected more than $300 million in equity funding, including a $100 million C-2 financing that valued the company at $2.6 billion earlier this year.

“There will always be customers that are skeptical, but I think by starting out with a card, we built a lot of trust,” Dubugras said. “It was us giving them money instead of them giving us money. A few years in … We think we’ve won a lot of credibility. Before, who was going to give their money to a random-ass startup called Brex?”

In the weeks ahead of TechCrunch Disrupt San Francisco, where Dubugras announced Brex Cash on Wednesday, the CEO told TechCrunch that Brex had no immediate fundraising plans and that they were “waiting for the right time” to raise again. As for what’s next, he said the company is discussing the launch of a debit card and plans to add another 100 employees in the next year, bringing the Brex headcount to 400.

The Brex news follows the launch of Stripe Capital, a new offering from payments behemoth Stripe that will make instant loan offers to customers on its platform, and the announcement of the Stripe Corporate Card. Akin to Brex, Stripe will issue a no-fee, no interest rate credit card intended for Stripe customers. Brex and Stripe, two Y Combinator grads, will go head-to-head in a battle for customers, particularly YC grads looking for friendly financial tools.

Immediately following Stripe’s announcements, the business announced a $250 million funding at a $35 billion valuation. Brex may be following a similar playbook, announcing a major product on the heels of a large capital infusion.

Brex Cash represents a new era for the company. Though the product may be costly for Brex, it opens the business up to thousands more potential customers. Now, any startup, regardless of funding, can create a Brex account to store cash, explains Dubugras, and all companies using Brex Cash will be immediately issued a Brex corporate credit card.

“If you’re starting out, if you don’t have funding yet, you can still receive your payments using Brex,” Dubugras said. “That’s a super big deal for us.”

Brex Cash was built under product lead Ritik Malhotra, who joined the team as part of an acquisition of his startup, Elph. Brex poached the company, which was focused on blockchain infrastructure, right out of YC for an undisclosed amount. In retrospect, the deal looks much more like an acqui-hire of Malhotra, who had the digital payments infrastructure acumen necessary to complete this project.

“It’s an easy way to move money, which is the lifeblood of a business,” Malhotra tells TechCrunch of the new product.

Brex Cash is itself not a cash cow for Brex; rather, the startup makes money on purchases made on its corporate card, in which it charges the merchant, not the customer. This model is particularly beneficial when its customers are spending a lot of money, growing quickly and raising capital. In a downturn, however, this model isn’t as attractive.

Brex seems unconcerned with the possibility of an impending recession. Brex writes that even in downturns, entrepreneurs will start companies and attempt to raise money. The Brex Cash product, regardless of the economy, will help Brex better underwrite Brex Cards, as it gives them better access to a customer’s financial health.

In a battle against Stripe, Brex is at a disadvantage. At only two years old, the company may have garnered a lot of credibility in a short time but it doesn’t have the decade of experience building fintech products that Stripe has and, more importantly, it doesn’t have 10 years of customer loyalty.

Powered by WPeMatico

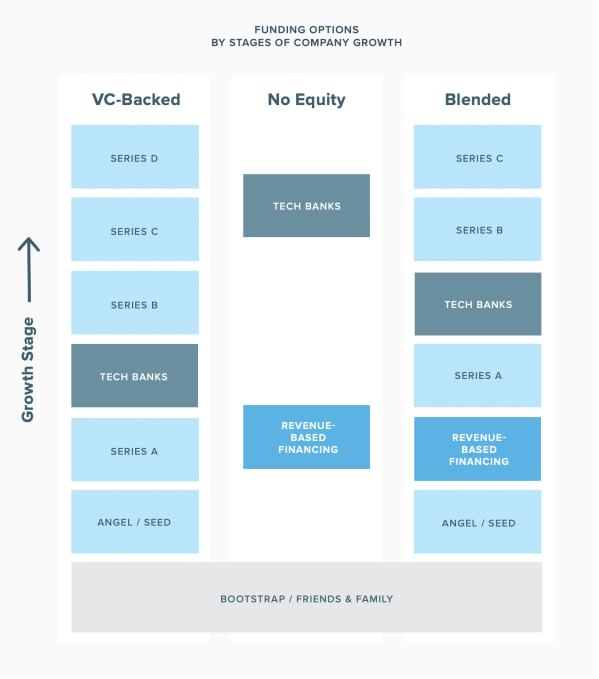

You’re working on launching a new VC fund; congratulations! I’ve been a traditional equity VC for 8 years, and I’m now researching revenue-vased investing and other new approaches to VC. The question I’m asking myself: should a new VC fund use revenue-based investing, traditional equity VC, or possibly both (likely from two separate pools of capital)?

Revenue-based investing (“RBI”) is a new form of VC financing, distinct from the preferred equity structure most VCs use. RBI normally requires founders to pay back their investors with a fixed percentage of revenue until they have finished providing the investor with a fixed return on capital, which they agree upon in advance.

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is part of an ongoing series on Revenue-based investing VC that will hit on:

From the investors’ point of view, the advantages of the RBI models are manifold. In fact, the Kauffman Foundation has launched an initiative specifically to support VCs focused on this model. The major advantages to investors are:

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week was a bit special. Instead of meeting up at the TechCrunch HQ to record the episode, Kate and Alex met up in muggy Boston at Drift’s office, where we linked up with Axios’s Dan Primack. And because we were feeling chatty, we went a bit long.

After checking in with Primack (he has a newsletter and a podcast), we first dealt with the latest from Tumblr. In short, Verizon Media is selling Tumblr to Automattic for a few dollars. How did Verizon wind up owning Tumblr? Ah. Well, Yahoo bought it. Later, after Verizon bought AOL, it bought Yahoo. Then it smushed them together and called it Oath. Then Verizon decided that it didn’t like that much and renamed the group Verizon Media. But Verizon doesn’t want to own media (besides TechCrunch, of course), so it sold Tumblr to Automattic, a venture-backed company best known for operating WordPress.

That’s a lot, I know. What matters is that Yahoo bought Tumblr for more than $1 billion. Verizon sold it for around $3 million. Now, Automattic has a few hundred new employees and a shot at juicing its user base before it goes public.

After that, we lamented that the WeWork S-1 had yet to appear. This was a tragedy, frankly. We had expected to spend half the show riffing on WeWork’s financials, alas…

So we turned to some normal material, like Ramp’s recent $7 million raise to take on Brex, and, SmartNews’s recent round, which gave it an eye-popping $1.1 billion valuation.

We ran a bit long because we were having fun, fitting in some conversation surrounding the notes from the SEC regarding the now-dead and then-fraudulent Rothenberg Ventures. More on that here if you want to get angry.

And finally, Vision Fund 2. It’s been a big source of interest for everyone on the show, and we expect whatever the second-act Vision Fund winds up becoming to be a big damn deal. The fund will invest in more than just consumer marketplaces; in fact, it’s eyeing more AI businesses and even biotech. That should be interesting.

All that and we have a lot more good stuff coming. Thanks for listening to the show, and we’ll be right back.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

In an era of massive data breaches, most recently the Capital One fiasco, the risk of a cyberattack and the costly consequences are the top existential threat to corporations big and small. At TechCrunch’s first-ever enterprise-focused event (p.s. early-bird sales end August 9), that topic will be front and center throughout the day.

That’s why we’re delighted to announce United’s chief information security officer Emily Heath will join TC Sessions: Enterprise in San Francisco on September 5, where we will discuss and learn how one of the world’s largest airlines keeps its networks safe.

Joining her to talk enterprise security will be a16z partner Martin Casado and DUO / Cisco’s head of advisory CISOs Wendy Nather, among others still to be announced.

At United, Heath oversees the airline’s cybersecurity program and its IT regulatory, governance and risk management.

The U.S.-based airline has more than 90,000 employees serving 4,500 flights a day to 338 airports, including New York, San Francisco, Los Angeles and Washington, D.C.

A native of Manchester, U.K., Heath served as a former police detective in the U.K. Financial Crimes Unit where she led investigations into international investment fraud, money laundering and large scale cases of identity theft — and ran joint investigations with the FBI, SEC and London’s Serious Fraud Office.

Heath and her teams have been the recipients of CSO Magazine’s CSO50 Awards for their work in cybersecurity and risk.

At TC Sessions: Enterprise, Heath will join a panel of cybersecurity experts to discuss security on enterprise networks large and small — from preventing data from leaking to keeping bad actors out of their network — where we’ll learn how a modern CSO moves fast without breaking things.

Join hundreds of today’s leading enterprise experts for this single-day event when you purchase a ticket to the show. The $249 early-bird sale ends Friday, August 9. Make sure to grab your tickets today and save $100 before prices go up.

Powered by WPeMatico

WeWork chief executive officer Adam Neumann is already rich, but soon all of the early employees and investors of the co-working giant will be too.

The business, now known as The We Company, has accelerated its plans to go public, according to a new report from The Wall Street Journal. WeWork is expected to unveil is S-1 filing next month ahead of a September initial public offering.

WeWork declined to provide comment for this story.

The New York-based company, valued at $47 billion earlier this year, has long been rumored to be plotting a massive IPO. The WSJ reports it’s now in the process of meeting with Wall Street banks to secure an asset-backed loan upwards of $6 billion in what could be an effort to downsize its upcoming stock offering. WeWork disclosed massive 2018 net losses of $1.9 billion in March on revenue of $1.8 billion. To convince Wall Street it’s a business worthy of their investment will be a challenge, to say the least. Seeking capital elsewhere ahead of the IPO manages expectations and ensures WeWork ultimately has the cash it needs to continue its global expansion. Here’s a look at WeWork’s expanding revenues and losses:

WeWork has raised a total of $8.4 billion in a combination of debt and equity funding since it was founded in 2011. Its IPO is poised to become the second largest offering of the year behind only Uber, which was valued at $82.4 billion following its May IPO on the New York Stock Exchange.

WeWork is said to have initially filed paperwork with the U.S. Securities and Exchange Commission for an IPO in December, in part so it was ready to hit the public markets if other avenues for cash fell through. The business is one of several tech unicorns to attract billions from the SoftBank Vision Fund. Recently, the Japanese telecom giant eyed a majority stake in the company worth $16 billion, but scaled back their investment down to $2 billion at the last minute.

WeWork, despite mounting losses, is growing — fast. The company established a 90% occupancy rate in 2018 as membership totals rose 116%, to 401,000.

Still, whether WeWork, backed by SoftBank, Benchmark, T. Rowe Price, Fidelity and Goldman Sachs, will be able to match its $47 billion valuation when it goes public this fall is questionable. Early investors will be sure to see a nice return, but late-stage investors may be nervous about their prospects.

Neumann, for his part, has reportedly cashed out of more than $700 million from his company ahead of the IPO. The size and timing of the payouts, made through a mix of stock sales and loans secured by his equity in the company, is unusual, considering that founders typically wait until after a company holds its public offering to liquidate their holdings.

Powered by WPeMatico

Technology has been used to manage regulatory risk since the advent of the ledger book (or the Bloomberg terminal, depending on your reference point). However, the cost-consciousness internalized by banks during the 2008 financial crisis combined with more robust methods of analyzing large datasets has spurred innovation and increased efficiency by automating tasks that previously required manual reviews and other labor-intensive efforts.

So even if RegTech wasn’t born during the financial crisis, it was probably old enough to drive a car by 2008. The intervening 11 years have seen RegTech’s scope and influence grow.

RegTech startups targeting financial services, or FinServ for short, require very different growth strategies — even compared to other enterprise software companies. From a practical perspective, everything from the security requirements influencing software architecture and development to the sales process are substantially different for FinServ RegTechs.

The most successful RegTechs are those that draw on expertise from security-minded engineers, FinServ-savvy sales staff as well as legal and compliance professionals from the industry. FinServ RegTechs have emerged in a number of areas due to the increasing directives emanating from financial regulators.

This new crop of startups performs sophisticated background checks and transaction monitoring for anti-money laundering purposes pursuant to the Bank Secrecy Act, the Office of Foreign Asset Control (OFAC) and FINRA rules; tracks supervision requirements and retention for electronic communications under FINRA, SEC, and CFTC regulations; as well as monitors information security and privacy laws from the EU, SEC, and several US state regulators such as the New York Department of Financial Services (“NYDFS”).

In this article, we’ll examine RegTech startups in these three fields to determine how solutions have been structured to meet regulatory demand as well as some of the operational and regulatory challenges they face.

Powered by WPeMatico

Upfront Ventures, a Los Angeles-based venture capital firm, has filed paperwork with the U.S. Securities and Exchange Commission to raise its third growth-stage investment fund.

Though the firm typically invests at the seed and Series A, capital from Upfront Growth III will be used for follow-on or late-stage deals.

The firm, known for its investments in Bird, Goat, Ring, ThredUP and Parachute, plans to raise $250 million for the effort. Mark Suster and Yves Sisteron, listed on the filing, lead the firm as managing partners. Upfront’s investor line-up also includes partners Kobie Fuller, Greg Bettinelli, Kara Nortman and Kevin Zhang.

One of the oldest VCs rooted in LA, Upfront previously closed on $400 million for its sixth flagship early-stage fund in 2017.

LA is on pace for a banner year of VC investment, attracting $33 billion across more than 1,000 deals already in 2019, according to PitchBook. Last year, companies headquartered in LA raised more than $60 billion.

Powered by WPeMatico

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico