Tribe Capital

Auto Added by WPeMatico

Auto Added by WPeMatico

Even as hundreds of millions of people in India have a bank account, only a tiny fraction of this population invests in any financial instrument.

Fewer than 30 million people invest in mutual funds or stocks, for instance. In recent years, a handful of startups have made it easier for users — especially the millennials — to invest, but the figure has largely remained stagnant.

Now, an Indian startup believes that it has found the solution to tackle this challenge — and is already seeing good early traction.

Nishchay AG, former director of mobility startup Bounce, and Misbah Ashraf, co-founder of Marsplay (sold to Foxy), founded Jar earlier this year.

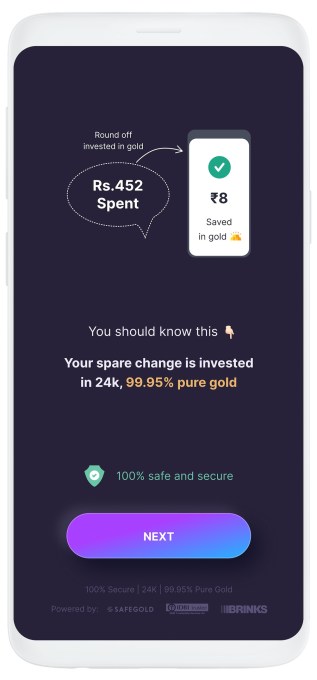

The startup’s eponymous six-month-old Android app enables users to start their savings journey for as little as 1 Indian rupee.

Users on Jar can invest in multiple ways and get started within seconds. The app works with Paytm (PhonePe support is in the works) to set up a recurring payment. (The startup is the first to use UPI 2.0’s recurring payment support.) They can set up any amount between 1 Indian rupee to 500 for daily investments.

The Jar app can also glean users’ text messages and save a tiny amount based on each monetary transaction they do. So, for instance, if a user has spent 31 rupees in a transaction, the Jar app rounds that up to the nearest tenth figure (40, in this case) and saves nine rupees. Users can also manually open the app and spend any amount they wish to invest.

Once users have saved some money in Jar, the app then invests that into digital gold.

The startup is using gold investment because people in the South Asian market already have an immense trust in this asset class.

India has a unique fascination for gold. From rural farmers to urban working class, nearly everyone stashes the yellow metal and flaunts jewelry at weddings.

Indian households are estimated to have a stash of over 25,000 tons of the precious metal whose value today is about half of the country’s nominal GDP. Such is the demand for gold in India that the South Asian nation is also one of the world’s largest importers of this precious metal.

Jar’s Android app (Image Credits: Jar)

“When you’re thinking about bringing the next 500 million people to institutional savings and investments, the onus is on us to educate them on the efficacies of the other instruments that are in the market,” said Nishchay.

“We want to give them the instrument they trust the most, which is gold,” he said. The startup plans to eventually offer several more investment opportunities, he said.

The founders met several years ago when they were exploring if MarsPlay and Bounce could have any synergies. They stayed in touch and, last year during one of their many conversations, realized that neither of them knew much about investments.

“That’s when the dots started to connect,” said Misbah, drawing stories from his childhood. “I come from a small town in Bihar called Bihar Sharif. During my childhood days, I saw my family deeply troubled with debt because of poor financial decisions and no savings,” he said.

“We both understand what a typical middle class family goes through. Someone who comes from this background never had any means in the past but their aspirations are never-ending. So when you start earning, you immediately start to spend it all,” said Nishchay.

“The market needs products that will help them get started,” he said.

That idea, which is similar to Acorn and Stash’s play in the U.S. market, is beginning to make inroads. The app has already amassed about half a million downloads, the founders said. Investors have taken notice, too.

On Wednesday, Jar announced it has raised $4.5 million from a clutch of high-profile investors, including Arkam Ventures, Tribe Capital, WEH Ventures, and angels including Kunal Shah (founder of CRED), Shaan Puri (formerly with Twitch), Ali Moiz (founder of Stonks), Howard Lindzon (founder of Social Leverage), Vivekananda Hallekere (co-founder of Bounce), Alvin Tse (of Xiaomi) and Kunal Khattar (managing partner at AdvantEdge).

“Over 400 million Indians are about to embrace digital financial services for the first time in their lives. Jar has built an app that is poised to help them — with several intuitive ways including gamification — start their investment journey. We love the speed at which the team has been executing and how fast they are growing each week,” said Arjun Sethi, co-founder of Tribe Capital, in a statement.

Transactions and AUM on the Jar app are surging 350% each month, said Nishchay. The startup plans to broaden its product offerings in the coming days, he said.

Powered by WPeMatico

It was easy to wonder what would become of Docker after it sold its enterprise business in 2019, but it regrouped last year as a cloud native container company focused on developers, and the new approach appears to be bearing fruit. Today, the company announced a $23 million Series B investment.

Tribe Capital led the round with participation from existing investors Benchmark and Insight Partners. Docker has now raised a total of $58 million including the $35 million investment it landed the same day it announced the deal with Mirantis.

To be sure, the company had a tempestuous 2019 when they changed CEOs twice, sold the enterprise division and looked to reestablish itself with a new strategy. While the pandemic made 2020 a trying time for everyone, Docker CEO Scott Johnston says that in spite of that, the strategy has begun to take shape.

“The results we think speak volumes. Not only was the strategy strong, but the execution of that strategy was strong as well,” Johnston told me. He indicated that the company added 1.7 million new developer registrations for the free version of the product for a total of more than 7.3 million registered users on the community edition.

As with any open-source project, the goal is to popularize the community project and turn a small percentage of those users into paying customers, but Docker’s problem prior to 2019 had been finding ways to do that. While he didn’t share specific numbers, Johnston indicated that annual recurring revenue (ARR) grew 170% last year, suggesting that they are beginning to convert more successfully.

Johnston says that’s because they have found a way to turn a certain class of developer in spite of a free version being available. “Yes, there’s a lot of upstream open-source technologies, and there are users that want to hammer together their own solutions. But we are also seeing these eight to 10 person ‘two-pizza teams’ who want to focus on building applications, and so they’re willing to pay for a service,” he said.

That open-source model tends to get the attention of investors because it comes with that built-in action at the top of the sales funnel. Tribe’s Arjun Sethi, whose firm led the investment, says his company actually was a Docker customer before investing in the company and sees a lot more growth potential.

“Tribe focuses on identifying N-of-1 companies — top-decile private tech firms that are exhibiting inflection points in their growth, with the potential to scale toward outsized outcomes with long-term venture capital. Docker fits squarely into this investment thesis [ … ],” Sethi said in a statement.

Johnston says as they look ahead post-pandemic, he’s learned a lot since his team moved out of the office last year. After surveying employees, they were surprised to learn that most have been happier working at home, having more time to spend with family, while taking away a grueling commute. As a result, he sees going virtual first, even after it’s safe to reopen offices.

That said, he is planning to offer a way to get teams together for in-person gatherings and a full company get-together once a year.

“We’ll be virtual first, but then with the savings of the real estate that we’re no longer paying for, we’re going to bring people together and make sure we have that social glue,” he said.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico

The insurance industry, sleepy and ancient, is ripe for disruption. We’ve seen companies like Lemonade, Hippo and Rhino get in on that opportunity. Today, an insurtech company focused on small business insurance has raised $18 million to keep growing.

Meet Huckleberry, whose Series A was led by Tribe Capital, with participation from Amaranthine, Crosslink Capital and Uncork Capital.

Huckleberry launched in 2017 to offer business insurance, including workers’ compensation and general liability, all through an online portal.

Small business insurance coverage is not like car insurance or renters insurance. It’s not as simple as filling out a few forms and getting a quote. Even if a few platforms do have algorithms for providing quotes, you can’t really close the deal unless you get on the phone.

It’s an incredibly tedious and stressful process. In fact, Huckleberry co-founders Bryan O’Connell and Steve Au first came up with the idea for Huckleberry when they were seeking out their own small business coverage for a previous startup idea.

The industry itself is incredibly fragmented, which is caused in part by the fact that small business coverage underwriting varies wildly from business to business. For example, the policy for three or four restaurants might look relatively similar. However, a fast food restaurant might be identified as a higher risk with regards to workers’ compensation than a Michelin-star restaurant, where workers might be more eager to get back to work and take home their tip money. These differences come in the form of location, operations and many other factors, as well as business vertical.

Huckleberry has worked to build out myriad coverage verticals, including food and beverage, fitness, retail, legal, healthcare, hair and beauty and more.

The firm offers worker’s comp, as well as a package policy that includes general liability, property and business interruption insurance. Customers also can purchase add-ons like hired and non-owned auto insurance, employment practices liability insurance (EPLI), liquor liability insurance, employee dishonesty coverage, professional liability insurance, equipment breakdown coverage and spoilage coverage.

Huckleberry isn’t itself an insurance carrier, but does have the authority to underwrite and sell policies on behalf of the carrier. That said, Huckleberry’s expansion both by vertical and geography is more difficult than your average software startup. The regulatory landscape of insurance in the U.S. goes state by state.

“Our biggest challenge is navigating 50 states’ worth of extremely complicated regulations on something that is much more complicated than a software product,” said O’Connell. “We’re trying to protect individual workers and businesses all while staying fully compliant in every market.”

Powered by WPeMatico

Home ownership has long been touted as the American dream. But rising rates of mortgage debt and student loan debt are making the pursuit of home ownership a nightmare. Debt-burdened individuals or those with inconsistent or tight cash flow can not only struggle to get credit loan approval when buying a home but also struggle to satisfy monthly mortgage payments even after purchase.

Patch Homes is hoping to keep the proverbial American dream alive. Patch looks to provide homeowners with cash flow and liquidity by allowing them to monetize their homes without taking on debt, interest or burdensome monthly payments.

Today, Patch took another big step in making its vision a far-reaching reality. The company has announced it has raised a $5 million Series A round led by Union Square Ventures (USV), with participation by from Tribe Capital and previous investors Techstars Ventures, Breega Capital and Greg Schroy.

Patch Home looks to partner with homeowners by investing up to $250,000 (with an average investment of ~$100,000) for an equity stake in the home’s value, generally in the 5% to 20% range. Homeowners aren’t subject to any interest or recurring payments and have 10 years to pay back Patch’s investment. Upon doing so, the only incremental money Patch receives is its portion of the change in the home’s value over the course of the 10-year period. If the value of the home goes down in value, Patch willingly takes a loss on its investment.

According to Patch Homes CEO and co-founder Sahil Gupta, one of the major motivations behind the company’s model is to align Patch’s incentives with the homeowners’, allowing both parties to think of each other as trusted partners even after financing. After Patch’s investment, the company provides a number of ancillary services to homeowners, such as credit score monitoring, as well as home value and property tax tracking.

In one instance recounted by Gupta in an interview with TechCrunch, Patch even covered three months of an owner’s mortgage during a liquidity crunch for his small business, allowing him to maintain his home and credit score. Patch is incentivized to provide all services that can help ensure an increase in home value, benefiting both Patch and the homeowner, with the homeowner earning the majority of the asset’s appreciated value.

Additionally, since Patch’s model isn’t focused on a homeowner’s ability to pay back a loan, interest or periodic payments, Patch is able to provide financing to more people. Patch is able to help those with more variable qualifications that struggle to get traditional loans — such as a 1099 contracted worker — monetize their illiquid assets with less harsh or restrictive terms and without increasing their debt burden. Gupta described this as solving the core problem of providing liquidity to asset-rich but cash-flow sensitive people.

Patch is not only looking to provide easier liquidity to more homeowners, but they’re trying to do so faster than traditional lenders. Interested customers can first receive a free estimate of whether Patch will invest in their home or not, how much it’s willing to invest and what percentage equity it will take — primarily based on Patch’s machine learning models that focus on asset, market and location-level attributes.

After the initial estimate, a Patch home advisor will educate the customer on the product and start a formal application process, which includes your standard income and credit score verification, which takes 5-10 days. All-in, homeowners have the ability to get money in as little as 14 days, a significantly shorter timeline than your standard home credit process. Once the investment is made, owners have full freedom with how they use the money.

According to Patch, while its customers come from a diverse set of backgrounds, many either with accumulated debt have to pay down the net or may struggle making monthly payments. The average Patch homeowner uses 40% of the investment to eliminate debt, adds 40% to their savings account or passive income and invests 20% into home improvements.

To date, Patch has raised a total of $6 million and believes the latest round of funding will help scale its operations as they team up with advisors like USV that have experience scaling fintech companies (such as a Lending Club or Carta). The funds will be used to invest in product and Patch’s clearing technology in order to further expedite Patch’s lending process.

Patch also hopes to use the investment to help them gradually expand their footprint, with the goal of eventually having a presence all 50 states. (Patch is currently available in 11 regional markets within California and Washington and expects to be in 18 regional markets by the end of the year including those in Utah, Colorado and Oregon.)

and Sahil Gupta (R)")

Image via Patch Homes

What makes home ownership so galvanizing for the Patch team? Patch CEO Sahil Gupta spent years putting his Carnegie Mellon financial engineering degree to work in banking and finance, as well as in financial products and strategy positions at fintech startups backed by heavy hitters such as YC and Goldman Sachs.

After realizing the majority of the U.S. population are homeowners, but were struggling to make monthly payments or save for the future, Sahil wanted to figure out to take an illiquid asset like a home and make it easily accessible.

Around the same time, Sahil’s co-founder Sundeep Ambati was working as a contractor on a new business venture of his and was struggling to get a home equity loan. While these circumstances ultimately led Sahil and Sundeep to found Patch Homes in 2016 out of the Techstars New York accelerator program, the deeper motivation behind Patch can be traced back nearly 30 years when Sahil’s father made an equity-sharing agreement with his brother as they were building his family’s home in India.

With a growing family and a pregnant wife, Sunil’s father was adamant about living debt-free, so his brother provided an investment in exchange for an equity stake in the house. According to Sahil, the home is still in the family and has appreciated substantially in value to the benefit of both Sahil’s father and his brother. Longer-term, Patch wants to be the preferred partner for home ownership, helping reduce cash-tight owners’ financial anxiety without the debilitating weight of debt.

“Some companies want to help people buy or sell homes, but home ownership really begins after that point. Patch is built to be inside the home with you and everything that comes thereafter,” Gupta told TechCrunch.

“Patch was created to partner with homeowners to help them unlock their home equity so they can achieve their financial goals along every step of their home ownership journey.

Powered by WPeMatico

Startups supporting startups are blazing a new trail with support from venture capitalists.

Co-working spaces like The Wing and The Riveter raked in funding rounds this year, as did Brex, the provider of a corporate card built specifically for startups. Now Carta, which helps companies manage their cap tables, valuations, portfolio investments and equity plans, has announced an $80 million Series D at a valuation of $800 million. The company, formerly known as eShares, raised the capital from lead investors Meritech and Tribe Capital, with support from existing investors.

The round brings Carta’s total funding to $147.8 million. Its existing investors include Spark Capital, Menlo Ventures, Union Square Ventures and Social Capital, though the latter didn’t participate in the Series D funding. Tribe Capital, however, is a new venture capital firm launched by Arjun Sethi, who previously led Social Capital’s investment in Carta, Jonathan Hsu and Ted Maidenberg, a trio of former Social Capital partners who exited the VC firm amid its transition from a traditional VC fund to a technology holding company. Tribe is said to be in the process of raising its own $200 million debut fund.

Founded in 2012 by Henry Ward (pictured), the Palo Alto-based company plans to use the latest investment to develop their transfer agent and equity administration products and services to better support startups transitioning into public companies. It also will launch additional products for investors to collect data from their portfolio companies and to manage their back office.

“We’ve come this far by changing how ownership management works for private companies—popularizing electronic securities and cap table software, combined with audit-ready 409As,” Ward wrote in an announcement. “But our ambitions go far beyond supporting privately-held, venture-backed companies.”

Carta, which counts Robinhood, Slack, Wealthfront, Squarespace, Coinbase and more as customers, currently manages $500 billion in equity. This year, Carta expanded its headcount from 310 employees to 450 employees, launched board management and portfolio insights products and completed a study in partnership with #Angels that highlighted the major equity gap female startup employees are victim to.

The study, released in September, revealed that women own just 9 percent of founder and employee startup equity, despite making up 35 percent of startup equity-holding employees. On top of that, women account for 13 percent of startup founders, but just 6 percent of founder equity — or $0.39 on the dollar.

Powered by WPeMatico

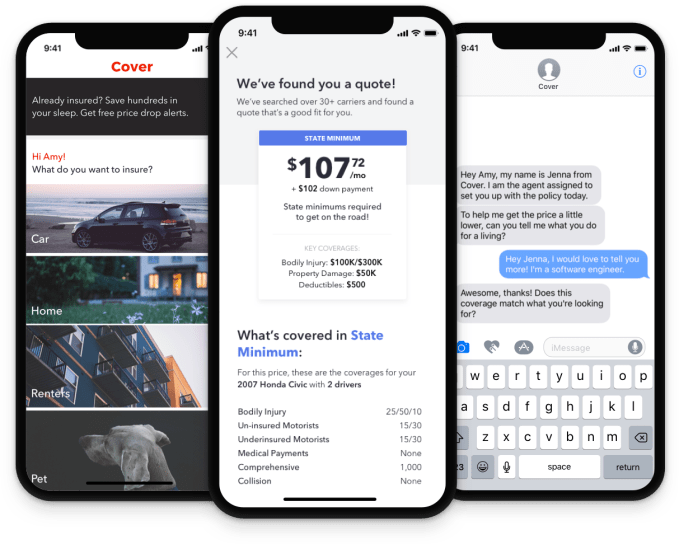

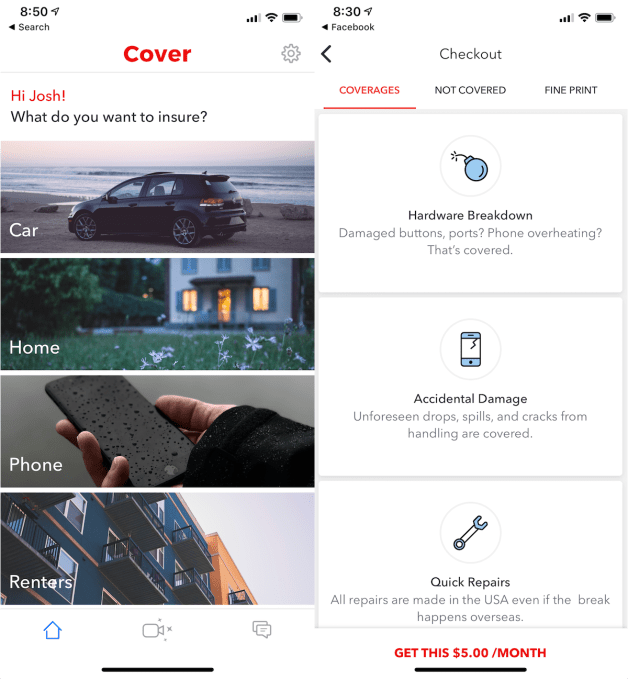

People procrastinate about buying insurance because it’s such a boring and complicated chore to compare policies. But Cover combines plans from 45 insurance companies into a single marketplace so it’s easy to find the best one for your car, home, rental, business, personal property, pets, jewelry and more. Now Cover is building powerful onboarding tricks like a driving school that earns you lower car insurance rates, and a way for Shopify merchants to sell warranties for their items.

The potential to use tech to run circles around the old insurance brokers has attracted a new $16 million Series B for Cover led by Tribe Capital’s Arjun Sethi, who led the Series A and sits on the startup’s board. The round was joined by Y Combinator, Social Capital, Exor and Samsung, and brings the company to a total of $27.1 million in funding.

“Insurance isn’t very different from being a white-collar bookie, where the house’s rake is too high and the dollars at stake are in the hundreds of billions in the U.S. alone,” says co-founder and CEO Karn Saroya. “This, all to the detriment of regular people, who view insurance as a tax. We’re here to change that perception.”

Saroya and his co-founders have deep ties. He went to high school with Anand Dhillon, is engaged to Natalie Gray and hired Ben Aneesh at the team’s previous startup, a high-end fashion marketplace called StyleKick that was eventually acqui-hired by Shopify. “We were tossing around ideas for what we wanted to do after StyleKick/Shopify, running hackathons on weekends. We built a couple different apps, but Cover — the MVP, where we just asked potential customers to take pictures of things they wanted to insure, surprised us” says Saroya. “Our customers sent us walkthroughs of their homes, pictures of their dogs and videos of themselves washing their cars. When you come across behavior that violates your expectations in consumers, that’s usually when you double-down.”

Cover co-founder and CEO Karn Saroya

So they built Cover, where you don’t have to cobble together an endless set of insurance websites or wait on hold. You download the app, pick your item, list how much you paid and where, provide some photos or video of its condition using its TensorFlow-equipped camera and Cover will check across its insurance partners and find you the best quote instantly. You can easily see what is and isn’t covered, learn how to make claims, and text with an agent if you have questions. For example, I was quickly quoted $5 per month to insure my new iPhone against damage but not loss or theft.

Cover earns between 10 to 35 percent per dollar of premium you pay. Its annualized premium already exceeds $8.5 million and is growing 30 percent per month. Thanks to its low-churn business model, easy cross-promotion of products, low training requirements for customers and no need to constantly update its existing subscriptions, Cover starts to look like a very efficient software-as-a-service business.

The big question remains whether Cover can consistently find the best rates for customers so they don’t second guess its quotes and search somewhere else. It will have to outcompete multi-insurance providers, like State Farm and Geico, as well as startups like MetroMile tackling specific insurance verticals with mobile apps. To really earn the big profits, Cover is building out its own in-house insurance plans. But that will put it under constant threat of insuring the wrong risks and ending up paying out too much.

“We built Cover because we saw an opportunity to build elegant products that could deliver on pricing and customer experience in a way that no incumbent insurance entity can,” Saroya concludes. By bringing the service to mobile and making it a seamless part of owning something, Cover could ensure you’re insured, even if insurance is the last thing you want to think about.

Powered by WPeMatico