transport

Auto Added by WPeMatico

Auto Added by WPeMatico

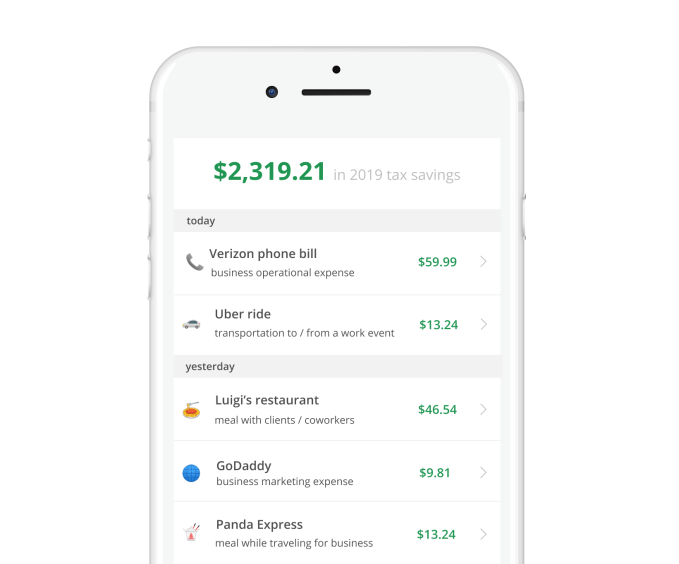

Every year around this time, Uber drivers, Wag dog walkers, Bird scooter chargers, social media influencers and other gig economy workers face the unsightly challenge of paying their taxes.

Companies like Uber and Lyft classify their drivers as independent contractors, which means you aren’t given any benefits and the company doesn’t withhold any of your taxes. This puts gig workers in a tough position come tax day, especially if they aren’t prepared to shell out big sums to the IRS.

Keeper, a startup that’s just graduated from the Y Combinator startup accelerator, is here to make taxes a lot easier for that demographic and to save them as much money as possible.

Founded by childhood buddies and former debate partners Paul Koullick and David Kang, the San Francisco-based company has raised $1.65 million on a $10 million valuation in a round led by Jake Jolis of Matrix Partners.

Keeper co-founders Paul Koullick (left) and David Kang

The pair entered YC this winter with a big idea and little to show for it. Come March, they had developed a full-fledged product and accumulated 200 paying customers. With their first round of funding, they plan to add to their small but growing team and acquire 10,000 customers in the next 18 months.

“There are some companies that are trying to go very broad and trying to cover the whole spectrum of benefits; we’re just trying to go really deep on taxes,” Kang told TechCrunch. “This is a pain point. This is where people are definitely leaving the most money on the table.”

Keeper guesses the average gig worker in the U.S. is overpaying their taxes by more than 20 percent, or about $1,550 for those making more than $25,000 per year. Why? Because these independent contractors aren’t claiming the tax write-offs available to them, like phone bills, car maintenance fees and even a Spotify subscription for drivers.

“If you’re a dog walker, there are so many things you need to be writing off, like your poop bags, your extra leashes, your parking,” Koullick told TechCrunch. “This population needs the guidance of an accountant, but they can’t afford one and we’re trying to create this third option.”

Like a personal accountant, Keeper monitors gig workers’ expenses all year in search of possible tax deductions, saving each user $173 per month on average, it estimates. The startup uses Plaid to follow its customers’ transaction history, and once per day sends a text message asking if there are any tax write-offs to note. Over time, it gets smarter and smarter, keeping the SMS questions to a minimum.

Keeper doesn’t fully file taxes for 1099 workers yet, but will begin offering a quarterly tax filing service in June. Next year, it plans to offer a full-year tax-filing service.

Koullick, Keeper’s chief executive officer, worked in product at Square before joining another startup, called Stride, where he built and scaled Stride Tax, a mileage and expense-tracking app. Kang, for his part, has spent most of his post-graduate career at a trading firm in Chicago, focused on quantitative modeling. The two toyed with a few startup ideas before landing on Keeper’s tax business.

“We wanted to build something that actually mattered to real people,” Koullick explained. “And we wanted to do it in the financial space where we were happy to wade through ugly details and systems on their behalf.”

Keeper isn’t the only recent YC alum focused on the growing gig economy. Another, Catch, sells health insurance, retirement savings plans and tax-withholding services directly to freelancers, contractors or anyone uncovered. Given the rapid rise of Uber and other gig platforms, it’s no wonder YC startups are tapping into the various business opportunities available there.

“We’re willing to tackle some of these topics that are kind of boring and mundane and really intensive,” Kang added. “Like the average person doesn’t want to think about taxes or filling out forms. We saw that as an opportunity for us to step in and be like, hey, we’ll take it.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

It’s time for another Equity Shot, a quick-take episode centered around a breaking news event. This time, as you already guessed, Kate Clark and I sat down to dig into the Uber S-1. It’s a huge, complex document, but we did our best to summarize what’s inside.

First, we talked through yearly results, looking back a half-decade into Uber’s revenue growth. In the filing, Uber reported 2018 revenues of $11.27 billion, net income of $997 million and adjusted EBITDA losses of $1.85 million. We highlighted those numbers, talked about operating losses and the company’s gyrating net results that included the positive impacts of various divestitures.

Yes, this S-1 required a bit more unpacking than most. We apologize for the frantic scrolling, we were pouring through the document live and we were a bit excited. This is an IPO that’s been talked about for years and will be easily one of the largest floats of all time.

Anyway, an S-1 brings insights to more than just a company’s financials, so we spent time highlighting key stakeholders, or, in other words, the people are are going to get really really really rich off Uber’s IPO. That includes Uber co-founder and chief executive officer Travis Kalanick, famous venture capital firms like the SoftBank Vision Fund and Benchmark, and more.

The IPO, remember, is expected to sell $10 billion in stock (primary and secondary) and value the company at $100 billion or more.

If 30 minutes digging through the S-1 wasn’t enough for you, don’t fret, we’ll be following the Uber IPO for weeks — probably months — to come.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Sure, we just aired a new episode, but things keep happening, and after talking about this crop of IPOs for so long, we can’t help ourselves. (You can follow us on Twitter, here and here, by the way, if Equity isn’t enough for you.)

Lyft, as you know, started trading today, closing the loop on a long saga that brought the smaller of the two domestic ride-hailing unicorns to the public markets.

After so much speculation about which of the two would get out the door first, Lyft did, and now we get to see what sort of pricing shenanigans happen next. Does Uber drop rates and punish Lyft? Or does Uber work to cut its losses, lowering its expenses and providing a clearer path toward profitability before its April IPO roadshow kicks off? (Not a path to profitability, mind; Uber and Lyft need to show a path to the direction of profitability first.)

We hit all the bases, going over the company’s pricing path, its varying share figures, final raise metrics and more. If you want the hard stuff, we’ve got a shot for you.

Now that the Lyft IPO has wrapped, we’ll be shifting our focus to Pinterest, Zoom and, of course, Uber. Stay tuned.

OK, now we’re done. Until next Friday. Unless something else happens.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Innoviz, the Israel-based startup developing solid-state lidar sensors and perception software for autonomous vehicles, has raised $132 million in a Series C funding round that includes major Chinese financial institutions.

The round, which makes Innoviz one of the better capitalized lidar startups, includes China Merchants Capital (SINO-BLR Industrial Investment Fund, L.P.), Shenzhen Capital Group and New Alliance Capital. Israeli institutional investors Harel Insurance Investments and Financial Services and Phoenix Insurance Company also participated.

The Series C round will remain open for a second closing to be announced in the coming months, the company said.

Lidar measures distance using laser light to generate highly accurate 3D maps of the world around the car. It’s considered by most in the self-driving car industry a key piece of technology required to safely deploy robotaxis and other autonomous vehicles. Innoviz is developing solid-state lidar, which proponents of this technology say is more reliable over time because of the lack of moving parts.

Like so many startups with fresh capital, Innoviz plans to use the funds to scale up the company.

For Innoviz, this means increasing production of its lidar sensors and expanding its manufacturing capacity. Innoviz is focused on expanding in important automotive markets, including the U.S., Europe, Japan and China. Innoviz has been pushing into China over the past year through a partnership with the Chinese automotive supplier HiRain Technologies, a global supplier to some of China’s largest automakers.

That company has half of its business coming from China and has won nine of its supplier agreements with different automakers in the country through its HiRain partnership, according to people with knowledge of the company.

The company’s aim is to enable high-volume delivery of its automotive-grade lidar system called InnovizOne. This product can be produced and sold at a 90 percent lower cost than its first-generation system, according to Innoviz.

Innoviz said it also plans to expand its research and development efforts by investing in the buildout of next-generation products and software that will feature more cost reductions and improved performance.

Innoviz’s strategy has been to partner with a number of OEMs and Tier 1 suppliers such as Magna, HARMAN, HiRain Technologies and Aptiv and to package perception software with its lidar sensors and offer it as a complete unit for companies developing autonomous vehicle technology.

Innoviz has locked in several key customers, notably BMW. The automaker picked Innoviz’s tech for series production of autonomous vehicles starting in 2021.

In March, Lyft announced a partnership with Magna to help get its self-driving tech into various automakers, as well as implement the ride-hailing service into future autonomous cars. Innoviz raised $65 million in Series B funding in 2017, from strategic partners and leading auto industry suppliers Delphi Automotive and Magna International, along with other investors.

Powered by WPeMatico

One year after a $38 million Series B valued on-demand aviation startup Blade at $140 million, the company has begun taxiing the Bay Area’s elite.

As part of a new pilot program, Blade has given 200 people in San Francisco and Silicon Valley exclusive access to its mobile app, allowing them to book helicopters, private jets and even seaplanes at a moments notice for $200 per seat, at least.

Blade, backed by Lerer Hippeau, Airbus, former Google CEO Eric Schmidt and others, currently flies passengers around the New York City area, where it’s headquartered, offering the region’s wealthy $800 flights to the Hamptons, among other flights at various price points. According to Business Insider, it has worked with Uber in the past to help deep-pocketed Coachella attendees fly to and from the Van Nuys Airport to Palm Springs, renting out six-seat helicopters for more than $4,000 a pop.

Its latest pilot seems to target business travelers, connecting riders to the San Francisco International Airport and Oakland International Airport to Palo Alto, San Jose, Monterey and Napa Valley. The goal is to shorten trips made excruciatingly long due to bad traffic in major cities like New York, Los Angeles and San Francisco. Recently, the startup partnered with American Airlines to better establish its network of helicopters, a big step for the company as it works to integrate with existing transportation infrastructure.

New work with @flybladenow pic.twitter.com/eONvKU3rhM

— Tyler Babin (@Tyler_Babin) March 11, 2019

Blade, led by founder and chief executive officer Rob Wiesenthal, a former Warner Music Group executive, has raised about $50 million in venture capital funding to date. To launch at scale and, ultimately, to compete with the likes of soon-to-be-public transportation behemoth Uber, it will have to land a lot more investment support.

Uber too has lofty plans to develop a consumer aerial ridesharing business, as do several other privately-funded startups. Called UberAIR, Uber will offer short-term shareable flights to commuters as soon as 2023. The company has raised billions of dollars to turn this sci-fi concept into reality.

Then there’s Kitty Hawk, a company launched by former Google vice president and Udacity co-founder Sebastian Thrun, which is developing an aircraft that can take off like a helicopter but fly like a plane for short-term urban transportation purposes. Others in the air taxi or vertical take-off and landing aircraft space, including Volocopter, Lilium and Joby Aviation, have raised tens of millions to eliminate traffic congestion or, rather, to chauffer the rich.

Blade’s next stop is India, the Financial Times reports, where it will conduct a pilot connecting travelers in downtown Mumbai and Pune. The company tells TechCrunch they are currently exploring one additional domestic pilot and one additional international pilot.

Powered by WPeMatico

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

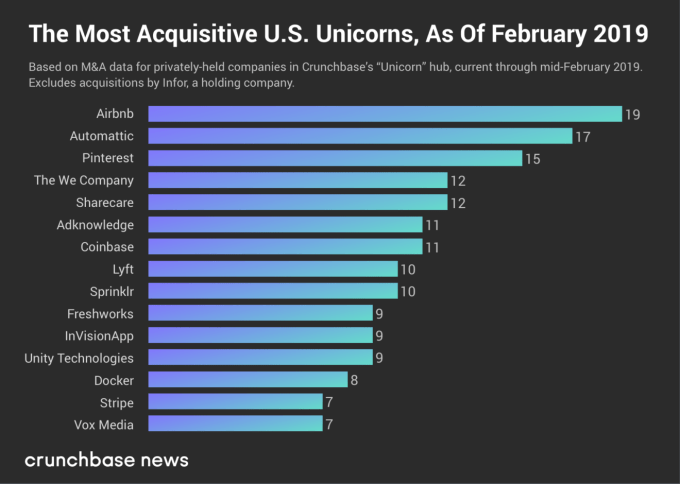

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

Cars are now essentially computers on wheels — and like every computer, they are susceptible to attacks. It’s no surprise then that there’s a growing number of startups that are working to protect a car’s internal systems from these hacks, especially given that the market for automotive cybersecurity could be worth mor $900 billion by 2026.

One of these companies is Israel’s C2A Security, which offers an end-to-end security platform for vehicles, which today announced that it has raised a $6.5 million Series A funding round.

The round was led by Maniv Mobility, which previously invested in companies like Hailo, drive.ai and Turo, and ICV, which has invested in companies like Freightos and Vayyar. OurCrowd’s Labs/02 also participated in this round.

Like most companies at the Series A stage, C2A plans to use the new funding to grow its team, especially on the R&D side, and help support its customer base. Sadly, C2A does not currently talk about who its customers are.

The promise of C2A is that it offers a full suite of solutions to detect and mitigate attacks. The team behind the company has an impressive security pedigree, with the company’s CMO Nat Meron being an alumn of Israel’s Unit 8200 intelligence unit, for example. C2A founder and CEO Michael Dick previously co-founded NDS, a content security solution, which Cisco acquired for around $5 billion in 2012 (and then recently sold on to Permira, also for $5 billion).

“We are extremely proud to receive the support of such outstanding investors, who will bring tremendous value to the company,” said Dick. “Maniv’s expertise in autotech and strong network across the industry coupled with ICV’s rich experience in cybersecurity brings the perfect combination of skills to the table.”

Powered by WPeMatico

MaaS Global, the company behind the all-in-one mobility app Whim, which offers a subscription service for public transportation, ridesharing, bike rentals, scooter rentals, taxis or car rentals, will be making its U.S. debut later this year.

The company will choose its American launch city from Austin, Boston, Chicago, Dallas and Miami, according to Sampo Hietanen, the company’s chief executive.

The Whim app is currently available in Antwerp, Birmingham, U.K., Helsinki and Vienna, according to Hietanen, and offers a range of subscription options. The top of the line version is a €500 per month all-inclusive package giving users unlimited access to ride hailing, bike and car rentals and public transportation.

“Cars take 70 percent of the market and it’s used 4 percent of the time so you’re paying for the optional capacity,” says Hietanen. Using Whim, which, at the high end costs about as much as a car in Europe, users can get all of the optionality without paying for the unused capacity. It should ideally reduce transportation costs and cut down on emissions, if Hietanen’s claims are accurate.

The Helsinki-based company uses APIs to connect with the back end of a number of service providers. For car rentals, it’s working with businesses like Hertz, Enterprise and EuropeCar; for ridesharing, the company has linked with Gett and local European taxi companies, according to Hietanen.

Users have already booked 3 million trips through the company’s app since its launch and the company is continuing to expand not just in North America, but in Asia as well. There are plans in the works for the company to launch operations in Singapore.

Giving consumers more options for transit through a single gateway could reduce demand for vehicles, but some analysts argue that it won’t do much to alleviate congestion on roads. Consumers, they argue, will choose the convenience of rideshare over mass transit and could actually increase.

As Richard Rowson, a mobility consultant from the U.K., noted in this post:

MaaS doesn’t implicitly mean a net decrease nor increase in the number of road vehicle miles. The changes are complex, but in balance look likely to result in an increase.

Factors such as migration from private car to public transport should cause a reduction, but migration from train and bus, to private hire and smaller demand responsive buses will cause an increase. Other factors such as ‘positioning’ movements as ‘on demand’ vehicles are positioned to exploit demand also create journeys.

Smart journey planning and navigation systems should make better use of available road capacity, such as identifying alternative routes – but at the expense of migrating through traffic to local access roads.

There is the potential that having a single point of access to mobility may actually help cities push riders to favor public transportation by offering a window into the amount of time using each service would take and showing users the fastest route.

Last August the company said it had raised a €9 million round from undisclosed investors. It had previously received capital from Toyota Financial Services and its insurance partner Aioi Nissay Dowa Insurance.

Powered by WPeMatico

Sony’s venture capital arm has invested in what3words, the startup that has divided the entire world into 57 trillion 3-by-3 meter squares and assigned a three-word address to each one.

Financial details were not disclosed.

The startup’s novel addressing system isn’t the whole story. The ability to integrate what3words into voice assistants is what has piqued the interest and investment from Sony and others.

“what3words have solved the considerable problem of entering a precise location into a machine by voice. The dramatic rise in voice-activated systems calls for a simple voice geocoder that works across all digital platforms and channels, can be written down and spoken easily,” Sony Corporation’s senior vice president Toshimoto Mitomo said in a statement.

Last year, Daimler took a 10 percent stake in what3words, following an announcement in 2017 to integrate the addressing system into Mercedes’ new infotainment and navigation system — called the Mercedes-Benz User Experience, or MBUX. MBUX is now in the latest Mercedes A-Class and B-Class cars and Sprinter commercial vehicles. Owners of these new Mercedes-Benz vehicles are now able to navigate to an exact destination in the world by just saying or typing three words into the infotainment system.

Other companies are keen to follow Daimler’s lead. TomTom and ride-hailing services like Cabify recently announced plans to enable what3words navigation to precise locations.

And more could follow. The startup says it plans to use the investment from Sony to focus on more initiatives in the automotive space.

Powered by WPeMatico

3D-printing the first rocket on Mars.

That’s the goal Tim Ellis and Jordan Noone set for themselves when they founded Los Angeles-based Relativity Space in 2015.

At the time they were working from a WeWork in Seattle, during the darkest winter in Seattle history, where Ellis was wrapping up a stint at Blue Origin . The two had met in college at USC in their jet propulsion lab. Noone had gone on to take a job at SpaceX and Ellis at Blue Origin, but the two remained in touch and had an idea for building rockets quickly and cheaply — with the vision that they wanted to eventually build these rockets on Mars.

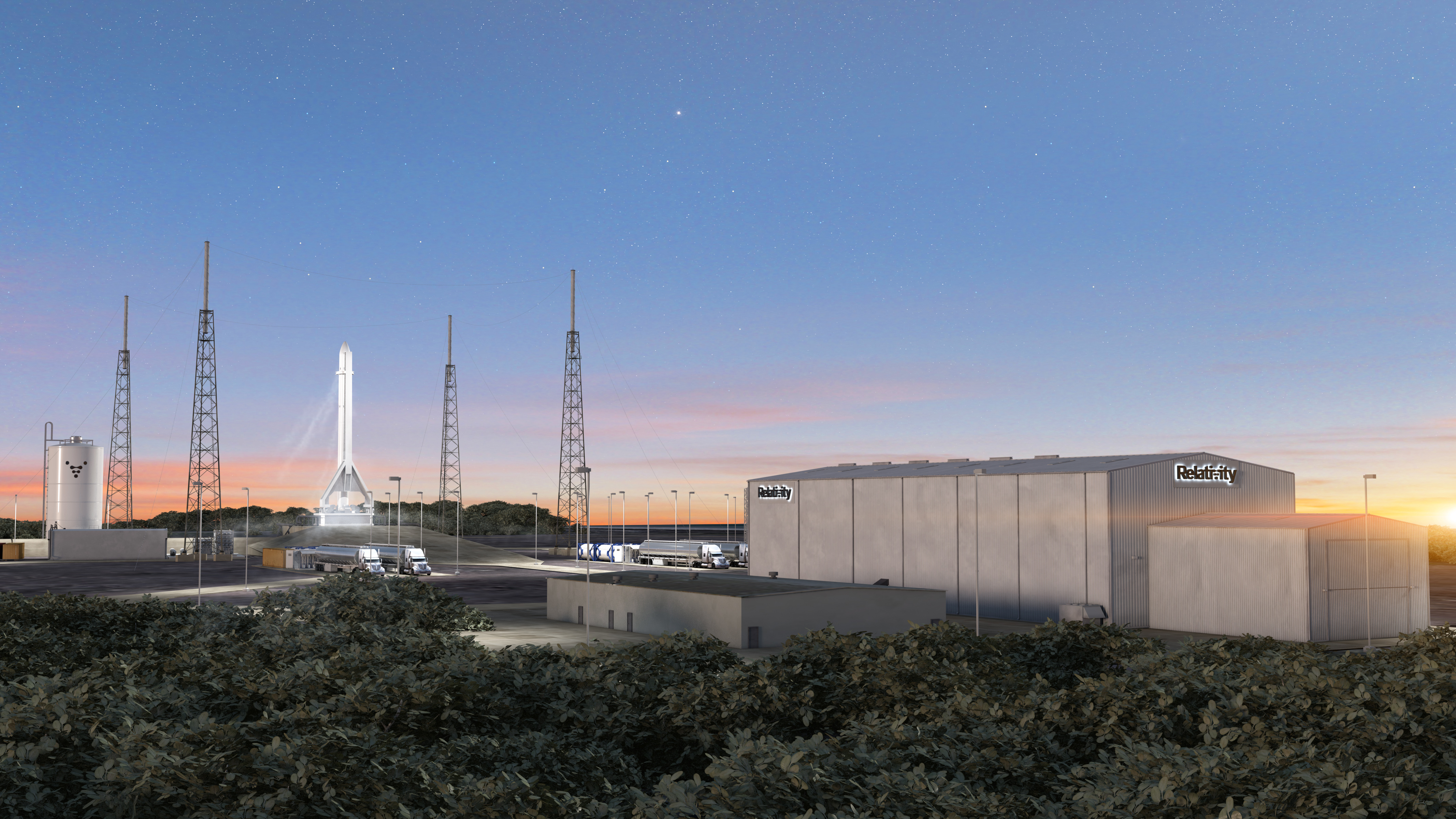

Now, more than $35 million dollars later, the company has been awarded a multi-year contract to build and operate its own rocket launch facilities at Cape Canaveral Air Force Station in Florida.

That contract, awarded by The 45th Space Wing of the Air Force, is the first direct agreement the U.S. Air Force has completed with a venture-backed orbital launch company that wasn’t also being subsidized by billionaire owner-operators.

By comparison, Relativity’s neighbors at Cape Canaveral are Blue Origin (which Jeff Bezos has been financing by reportedly selling $1 billion in shares of Amazon stock since 2017); SpaceX (which has raised roughly $2.5 billion since its founding and initial capitalization by Elon Musk); and United Launch Alliance, the joint venture between the defense contracting giants Lockheed Martin Space Systems and Boeing Defense.

Like the other launch sites at Cape Canaveral, Launch Complex 16, where Relativity expects to be launching its first rockets by 2020, has a storied history in the U.S. space and missile defense program. It was used for Titan missile launches, the Apollo and Gemini programs and Pershing missile launches.

From the site, Relativity will be able to launch its first designed rocket, the Terran 1, which is the only fully 3D-printed rocket in the world.

That rocket can carry a maximum payload of 1,250 kilograms to a low earth orbit of 185 kilometers above the Earth. Its nominal payload is 900 kilograms of a Sun-synchronous orbit 500 kilometers out, and it has a 700 kilogram high-altitude payload capacity to 1,200 kilometers in Sun-synchronous orbit. Relativity prices its dedicated missions at $10 million, and $11,000 per kilogram to achieve Sun-synchronous orbit.

If the company’s two founders are right, then all of this launch work Relativity is doing is just a prelude to what the company considers to be its real mission — the advancement of manufacturing rockets quickly and at scale as a test run for building out manufacturing capacity on Mars.

“Rockets are the business model now,” Ellis told me last year at the company’s offices at the time, a few hundred feet from SpaceX. “That’s why we created the printing tech. Rockets are the largest, lightest-weight, highest-cost item that you can make.”

It’s also a way for the company to prove out its technology. “It benefits the long-term mission,” Ellis continued. “Our vision is to create the intelligent automated factory on Mars… We want to help them to iterate and scale the society there.”

Ellis and Noone make some pretty remarkable claims about the proprietary 3D printer they’ve built and housed in their Inglewood offices. Called “Stargate,” the printer is the largest of its kind in the world and aims to go from raw materials to a flight-ready vehicle in just 60 days. The company claims that the speed with which it can manufacture new rockets should pare down launch timelines by somewhere between two and four years.

Another factor accelerating Relativity’s race to market is a long-term contract the company signed last year with NASA for access to testing facilities at the agency’s Stennis Space Center on the Mississippi-Louisiana border. It’s there, deep in the Mississippi delta swampland, that Relativity plans to develop and quality control as many as 36 complete rockets per year on its 25-acre space.

All of this activity helps the company in another segment of its business: licensing and selling the manufacturing technology it has developed.

“The 3D factory and automation is the other product, but really that’s a change in emphasis,” says Ellis. “It’s always been the case that we’re developing our own metal 3D printing technology. Not only can we make rockets. If the long-term mission is 3D printing on Mars, we should think of the factory as its own product tool.”

Not everyone agrees. At least one investor I talked to said that in many cases, the cost of 3D printing certain basic parts outweighs the benefits that printing provides.

Still, Relativity is undaunted.

But first, the company — and its competitors at Blue Origin, SpaceX, United Launch Alliance and the hundreds of other companies working on launching rockets into space again — need to get there. For Relativity, the Canaveral deal is one giant step for the company, and one great leap toward its ultimate goal.

“This is a giant step toward being a launch company,” says Ellis. “And it’s aligned with the long-term vision of one day printing on Mars.”

Powered by WPeMatico