Tizeti

Auto Added by WPeMatico

Auto Added by WPeMatico

November 2019 could mark when Nigeria (arguably) became Africa’s unofficial capital for fintech investment and digital finance startups.

The month saw $360 million invested in Nigerian-focused payment ventures. That is equivalent to roughly one-third of all the startup VC raised for the entire continent in 2018, according to Partech stats.

A notable trend-within-the-trend is that more than half — or $170 million — of the funding to Nigerian fintech ventures in November came from Chinese investors. This marks a pivot (to tech) in China’s engagement with Africa. We’ll get to that.

Before the big Chinese-backed rounds, one of Nigeria’s earliest fintech companies, Interswitch, confirmed its $1 billion valuation after Visa took a minority stake in the company. Interswitch would not disclose the amount to TechCrunch, but Sky News reporting pegged it at $200 million for 20%.

Founded in 2002 by Mitchell Elegbe, Interswitch pioneered the infrastructure to digitize Nigeria’s then predominantly paper-ledger and cash-based economy.

The company now provides much of the tech-wiring for Nigeria’s online banking system that serves Africa’s largest economy and population. Interswitch offers a number of personal and business finance products, including its Verve payment cards and Quickteller payment app.

The financial services firm has expanded its physical presence to Uganda, Gambia and Kenya . The Nigerian company also sells its products in 23 African countries and launched a partnership in August for Verve cardholders to make payments on Discover’s global network.

Visa and Interswitch touted the equity investment as a strategic collaboration between the two companies, without a lot of detail on what that will mean.

One point TechCrunch did lock down is Interswitch’s (long-awaited) and imminent IPO. A source close to the matter said the company will list on a major exchange by mid-2020.

For the near to medium-term, Interswitch could stand as Africa’s sole tech-unicorn, as e-commerce venture Jumia’s volatile share-price and declining market-cap — since an April IPO — have dropped the company’s valuation below $1 billion.

Circling back to China, November was the month that signaled Chinese actors are all in on African tech.

In two separate rounds, Chinese investors put $220 million into OPay and PalmPay — two fledgling startups with plans to scale in Nigeria and the broader continent.

PalmPay, a consumer-oriented payments product, went live last month with a $40 million seed round (one of the largest in Africa in 2019) led by Africa’s biggest mobile-phone seller — China’s Transsion.

The startup was upfront about its ambitions, stating in a company release its goals to become “Africa’s largest financial services platform.”

To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones.

PalmPay also launched in Ghana in November and its U.K. and Africa-based CEO, Greg Reeve, confirmed plans to expand to additional African countries in 2020.

![]()

OPay’s $120 million Series B was announced several days after the PalmPay news and came only months after the mobile-based fintech venture raised $50 million.

Founded by Chinese-owned consumer internet company Opera — and backed by nine Chinese investors — OPay is the payment utility for a suite of Opera -developed internet-based commercial products in Nigeria. These include ride-hail apps ORide and OCar and food delivery service OFood.

With its latest Series A, OPay announced it would expand in Kenya, South Africa and Ghana.

Though it wasn’t fintech, Chinese investors also backed a (reported) $30 million Series B for East African trucking logistics company Lori Systems in November.

With OPay, PalmPay and Lori Systems, startups in Africa have raised a combined $240 million from 15 Chinese investors in a span of months.

There are a number of things to note and watch out for here, as TechCrunch reporting has illuminated (and will continue to do in follow-on coverage).

These moves mark a next chapter in China’s engagement in Africa and could raise some new issues. Hereto, the country’s interaction with Africa’s tech ecosystem has been relatively light compared to China’s deal-making on infrastructure and commodities.

There continues to be plenty of debate (and critique) of China’s role in Africa. This new digital phase will certainly add a fresh component to all that. One thing to track will be data-privacy and national-security concerns that may emerge around Chinese actors investing heavily in African mobile consumer platforms.

We’ve seen lines (allegedly) blur on these matters between Chinese state and private-sector actors with companies such as Huawei.

As OPay and PalmPay expand, they may need to do some reassuring of African regulators as countries (such as Kenya) establish more formal consumer protection protocols for digital platforms.

One more thing to follow on OPay’s funding and planned expansion is the extent to which it puts Opera (and its entire suite of consumer internet products) in competition with multiple actors in Africa’s startup ecosystem. Opera’s Africa ventures could go head to head with Uber, Jumia and M-Pesa — the mobile money-product that put Kenya out front on digital finance in Africa before Nigeria.

Shifting back to American engagement in African tech, Twitter and Square CEO Jack Dorsey was on the continent in November. No sooner than he’d finished his first trip, Dorsey announced plans to move to Africa in 2020, for three to six months, saying on Twitter, “Africa will define the future (especially the bitcoin one!).”

We still don’t know much about what this last trip — or his future foray — mean in terms of concrete partnerships, investment or market moves in Africa from Dorsey and his companies.

He visited Nigeria, Ghana, South Africa and Ethiopia and met with leaders at Nigeria’s CcHub (Bosun Tijani), Ethiopia’s Ice Addis (Markos Lemma) and did some meetings with fintech founders in Lagos (Paga’s Tayo Oviosu).

He visited Nigeria, Ghana, South Africa and Ethiopia and met with leaders at Nigeria’s CcHub (Bosun Tijani), Ethiopia’s Ice Addis (Markos Lemma) and did some meetings with fintech founders in Lagos (Paga’s Tayo Oviosu).

I know pretty well most of the organizations and people Dorsey talked to and nothing has shaken out yet in terms of partnership or investment news from his recent trip.

On what could come out of Dorsey’s 2020 move to Africa, per his tweet and news highlighted in this roundup, a good bet would be it will have something to do with fintech and Square.

More Africa-related stories @TechCrunch

African tech around the ‘net

Powered by WPeMatico

Tizeti, the Nigerian internet service provider behind the brand Wifi.com.ng, has raised $3 million in a new round of funding as it expands its unlimited internet service into Ghana.

The new financing was led by 4DX Ventures, a new, Africa-focused fund that’s been deploying capital at an incredibly fast clip since its launch earlier this year. Its portfolio includes Sokowatch, a startup connecting local African retailers to international suppliers; the outsourced programmer placement and apprenticeship service, Andela; and the integrated pharmacy supplier and operator, mPharma.

For Walter Baddoo, one of 4DX Ventures co-founders and a new addition to the Tizeti board, the value in a company that operates as “the Comcast of Africa” was clear.

“If you take the efficiency of point to multipoint wireless technology and you add to that solar infrastructure, you leap-frog a generation of infrastructure. That makes getting cheap data to the hands of customers much easier,” Baddoo says.

Tizeti does exactly that. Using solar energy to power its wireless towers, the company provides residences, businesses, events and conferences with unlimited high-speed broadband internet access, which now covers more than 70 percent of Lagos. Since its launch from Y Combinator’s winter 2017 batch, the company has installed over 7,000 public Wi-Fi hotspots in Nigeria with 150,000 users.

Tizeti co-founders Ifeanyi Okonkwo and Kendall Ananyi

In November, the company partnered with Facebook to offer Express Wi-Fi and roll out hundreds of hotspots across the Nigerian capital of Abuja.

Now, with the new funding, Tizeti is expanding its operations outside of Nigeria, launching a new brand — Wifi.Africa — and pushing its service into Ghana.

“Tizeti was built to tackle poor internet connectivity not only in Nigeria, but on the continent as a whole, by developing a cost-effective solution from inception to delivery, for reliable and uncapped internet access for potentially millions of Africans,” said Kendall Ananyi, the co-founder and chief executive of Tizeti.

The company’s unlimited internet packages cost $30 per-month, a price it’s able to achieve through the use of cheap solar electricity to power its towers.

“Reducing the cost of data in Africa is a critical step in accelerating the pace of internet adoption across the continent,” Baddoo said in a statement. “Tizeti makes it easier and cheaper to connect Africa to the global digital economy and we are excited to partner with Kendall and his team on this mission.”

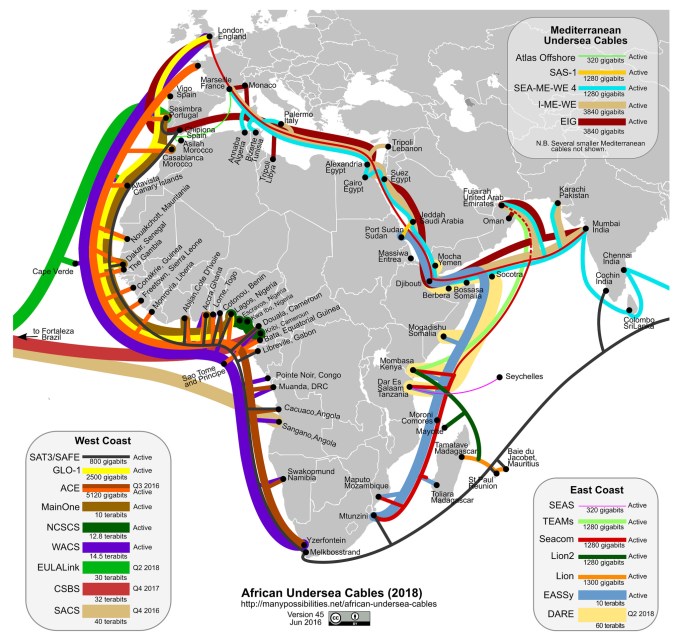

All of this is being powered by a network of new undersea cables stretching along the ocean floor that is bringing connectivity to the continent.

“There’s a ton of capacity going to 16 submarine cables [coming into Africa],” Ananyi told us back in 2017. “The problem is getting the internet to the customers. You have balloons and drones and that will work in the rural areas but it’s not effective in urban environments. We solve the internet problem in a dense area.”

It’s not a radical concept, and it’s one that has netted the company 3,000 subscribers already and nearly $1.2 million in annual recorded revenue in its first months of operations, Ananyi told us at the time.

“There are 1.2 billion people in Africa, but only 26 percent of them are online and most get internet over mobile phones,” says Ananyi. Perhaps only 6 percent of that population has an internet subscription, he said.

Photo courtesy of Flickr/Steve Song

Powered by WPeMatico