The TechCrunch Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. If you want it in your inbox every Saturday morning, sign up here. Ready? Let’s talk money, startups and spicy IPO rumors.

TechCrunch isn’t a public-market-focused publication. We care about startups. But public tech companies can, at times, provide interesting insights into how the broader technology market is performing. So we pay what we might call minimum-viable attention to former startups that made it all the way to an IPO.

Then there are the Big Tech companies. In the United States the list is well-known: Facebook, Alphabet, Microsoft, Apple and Amazon. And, in a series of results that could indicate a hot market for startup growth, they had a smashingly good first quarter of 2021. You can read our notes on their results here and here, but that’s just part of the story.

Yes, the Big Tech financial results were good — as they have been for some time — but lost amid the usual earnings deluge of numbers is how shockingly accretive Big Tech’s recent performances have proven for their valuations.

Microsoft fell as low as the $135 per-share range last March. Today it’s worth $252 and change. Alphabet traded down to around $1,070 per share. Today the search giant is worth $2,410 per share.

The result of the huge share-price appreciation is that Apple is now worth $2.21 trillion, Microsoft $1.88 trillion, Amazon $1.76 trillion, Alphabet $1.60 trillion and Facebook $0.93 trillion. That’s around $8.4 trillion for the five companies.

Back in July of 2017, I wrote a piece noting that their aggregate value had reached the $3 trillion mark. That became $4 trillion in mid-2018. And then in the next three years or so it more than doubled again.

Why?

Myles Udland, a reporter at our sister publication Yahoo Finance, has at least part of the puzzle in a piece he wrote this week. Here’s Udland:

And while it seems that almost every earnings story has sort of followed this same arc, data also confirms that this is not just our imagination: corporate earnings have never been this far out of line with expectations.

Data out of the team at Refinitiv published Thursday showed the rate at which companies were beating estimates and the magnitude by which they were beating expectations through Thursday morning’s results were the best on record.

So earnings are beating the street’s guesses more frequently, and at a higher differential, than ever? That makes recent stock-market appreciation less worrisome, I suppose. And it helps explain why startups have been able to raise so much capital lately in the United States, as they have in Europe, and why private-market investors are pouring so much capital into fintech startups. And it’s probably why Zomato is going public and why we’re still waiting for the Robinhood debut.

This is what a market feels like when the underlying businesses are firing on all cylinders, it appears. Just don’t forget that no business cycle is unending, and no boom is forever.

Extending The Exchange’s recent reporting regarding fintech funding, and our roundup from last week of insurtech startup rounds, a few more notes on the latter startup niche, which can be broadly viewed as part of the larger financial technology world.

This time we’ll hear from Accel’s John Locke regarding his investments in The Zebra — which recently raised even more capital — and the insurtech space more broadly.

Asked why insurtech marketplaces like The Zebra have been able to raise so very much money in the last year, Locke said that it’s a mix of “insurance carriers […] finally embracing marketplaces and willing to design integrated consumer experiences with marketplaces,” along with more consumer “comparison shopping” and, finally, growth and revenue quality.

The Zebra, Locke said, is “still growing north of 100% at ~$120M+ revenue run-rate.” That means it can go public whenever it wants.

But on that matter, there has been some weakness in the stock market for some public insurtech companies. Is Locke worried about that? He’s neutral-to-positive, saying that his firm does not “think all the companies in the market will work but still thinks ‘insurtechs’ will take market share from incumbents over the next decade.” Fair enough.

And Accel is still considering more deals in the space, as are others. Locke said that the venture market for insurtech investments is “definitely more aggressive” this year than last.

Closing today, a few notes on things that we didn’t get to that matter:

A long, weird week. Make sure to follow the second denizen of The Exchange’s writing team: Anna Heim. Okay! Chat next week!

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday? Sign up here.

Happy Saturday, everyone. I do hope that you are in good spirits and in good health. I am learning to nap, something that has become a requirement in my life after I realized that the news cycle is never going to slow down. And because my partner and I adopted a third dog who likes to get up early, please join me in making napping cool for adults, so that we can all rest up for Vaccine Summer. It’s nearly here.

On work topics, I have a few things for you today, all concerning data points that matter: Q1 2021 M&A data, March VC results from Africa, and some surprising (to me, at least) podcast numbers.

On the first, Dan Primack shared a few early first-quarter data points via Refinitiv that I wanted to pass along. Per the financial data firm, global M&A activity hit $1.3 trillion in Q1 2021, up 93% from Q1 2020. U.S. M&A activity reached an all-time high in the first quarter, as well. Why do we care? Because the data helps underscore just how hot the last three months have been.

I’m expecting venture capital data itself for the quarter to be similarly impressive. But as everyone is noting this week, there are some cracks appearing in the IPO market, as the second quarter begins that could make Q2 2021 a very different beast. Not that the venture capital world will slow, especially given that Tiger just reloaded to the tune of $6.7 billion.

On the venture capital topic, African-focused data firm Briter Bridges reports that “March alone saw over $280 million being deployed into tech companies operating across Africa,” driven in part by “Flutterwave’s whopping $170 million round at a $1 billion valuation.”

The data point matters as it marks the most active March that the African continent has seen in venture capital terms since at least 2017 — and I would guess ever. African startups tend to raise more capital in the second half of the year, so the March result is not an all-time record for a single month. But it’s bullish all the same, and helps feed our general sentiment that the first quarter’s venture capital results could be big.

And finally, Index Ventures’ Rex Woodbury tweeted some Edison data, namely that “80 million Americans (28% of the U.S. 12+ population) are weekly podcast listeners, +17% year-over-year.” The venture capitalist went on to add that “62% of the U.S. 12+ population (around 176 million people) are weekly online audio listeners.”

As we discussed on Equity this week, the non-music, streaming audio market is being bet on by a host of players in light of Clubhouse’s success as a breakout consumer social company in recent months. Undergirding the bets by Discord and Spotify and others are those data points. People love to listen to other humans talk. Far more than I would have imagined, as a music-first person.

How nice it is to be back in a time when consumer investing is neat. B2B is great but not everything can be enterprise SaaS. (Notably, however, it does appear that Clubhouse is struggling to hold onto its own hype.)

TechCrunch Early Stage was this week, which went rather well. But having an event to help put on did mean that I covered fewer rounds this week than I would have liked. So, here are two that I would have typed up if I had had the spare hours:

And two more rounds that you also might have missed that you should not. Holler raised $36 million in a Series B. Per our own Anthony Ha, “[y]ou may not know what conversational media is, but there’s a decent chance you’ve used Holler’s technology. For example, if you’ve added a sticker or a GIF to your Venmo payments, Holler actually manages the app’s search and suggestion experience around that media.”

I feel old.

And in case you are not paying enough attention to Latin American tech, this $150 million Uruguayan round should help set you straight.

Finally this week, some good news. If you’ve read The Exchange for any length of time, you’ve been forced to read me prattling on about the Bessemer cloud index, a basket of public software companies that I treat with oracular respect. Now there’s a new index on the market.

Meet the Lux Health + Tech Index. Per Lux Capital, it’s an “index of 57 publicly traded companies that together best represent the rapidly emerging Health + Tech investment theme.” Sure, this is branded to the extent that, akin to the Bessemer collection, it is tied to a particular focus of the backing venture capital firm. But what the new Lux index will do, as with the Bessemer collection, is track how a particular venture firm is itself tracking the public comps for their portfolio.

That’s a useful thing to have. More of this, please.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Earnings season is coming to a close, with public tech companies wrapping up their Q4 and 2020 disclosures. We don’t care too much about the bigger players’ results here at TechCrunch, but smaller tech companies we knew when they were wee startups can provide startup-related data points worth digesting. So, each quarter The Exchange spends time chatting with a host of CEOs and CFOs, trying to figure what’s going on so that we can relay the information to private companies.

Sometimes it’s useful, as our chat with recent fintech IPO Upstart proved after we got to noodle with the company about rising acceptance of AI in the conservative banking industry.

This week we caught up with Yext CEO Howard Lerman and Smartsheet CEO Mark Mader. Yext builds data products for small businesses, and is betting its future on search products. Smartsheet is a software company that works in the collaboration, no-code and future-of-work spaces.

They are pretty different companies, really. But what they did share this time ’round the earnings cycle were macro notes, or details regarding their forward financial guidance and what economic conditions they anticipate. As a macro-nerd, it piqued my interest.

Yext cited a number of macroeconomic headwinds when it reported its Q4 results. And tying its future results somewhat to an uncertain macro picture, the company said that it is “basing [its] guidance on the business conditions [it sees for itself] and [its] customers currently, with the macro economy, which remains sluggish, and customers who remain cautious,” per a transcript.

Lerman told The Exchange that it was not clear when the world would open — something that matters for Yext’s location-focused products — so the company was guiding for the year as if nothing would change. Wall Street didn’t love it, but if the economy improves Yext won’t have high hurdles to jump over. This is one tack that a company can take when it talks guidance.

Smartsheet took a slightly different approach, saying in its earnings call that its “fiscal year ’22 guidance contemplates a gradual improvement in the macro environment in the second half of the year.” Mader said in an interview that his company wasn’t hiring economists, but was instead simply listening to what others were saying.

He also said that the macro climate matters more in saturated markets, which he doesn’t think that Smartsheet is in; so, its results should be more impacted by things more like “the secular shift to the cloud and digital transformation,” to quote its earnings call.

What the economy will do this year matters quite a lot for startups. An improving economy could boost interest rates, making money a bit more expensive and bonds more attractive. Valuations could see modest downward pressure in that case. And venture capital could slow fractionally. But with Yext forecasting as if it was facing a flat road and Smartsheet only expecting things to pick up pace from Q3 on, it’s likely that what we have now is mostly what we’ll get.

And things are pretty damn good for startups and late-stage liquidity at the moment. So, smooth sailing ahead for startup-land? At least as far as our current perspective can discern.

We still have a grip of notes from Splunk CEO Douglas Merritt on how to take an old-school software company and turn it into a cloud-first company, and Jamf CEO Dean Hager about packaging discrete software products. More to come from them in fits.

There were rounds big and small this week. Companies like Squarespace raised $300 million, while Airtable raised $277 million. On the smaller-end of the spectrum, my favorite round of the week was a modest $2.9 million raise from Copy.ai.

But there were other rounds that TechCrunch didn’t get to that are still worth our time. So, here are a few more for you to dig into this weekend:

Next week is Y Combinator Demo Day week, so expect a lot of early-stage coverage on the blog. Here’s a preview. From The Exchange we’re looking back into insurtech (with data from WeFox and Insurify), and talking about Austin-based software startup AlertMedia’s decision to sell itself to private-equity instead of raising more traditional capital.

And to leave you with some reading material, make sure you’ve picked through our look at the valuations of free-trading apps, the issues with dual-class shares, the recent IPO win for the New York scene and how unequal the global venture capital market really is.

Closing, this BigTechnology piece was good, as was this Not Boring essay. Hugs, and have a lovely respite,

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Kicking off with a tiny bit of housekeeping: Equity is now doing more stuff. And TechCrunch has its Justice and Early-Stage events coming up. I am interviewing the CRO of Zoom for the latter. And The Exchange itself has some long-overdue stuff coming next week, including $50M and $100M ARR updates (Druva, etc.), a peek at consumption based pricing vs. traditional SaaS models (featuring Fastly, Appian, BigCommerce CEOs, etc.), and more. Woo!

This week both DoorDash and Airbnb reported earnings for the first time as public companies, marking their real graduation into the ranks of the exited unicorns. We’re keeping our usual eye on the earnings cycle, quietly, but today we have some learnings for the startup world.

Some basics will help us get started. DoorDash beat growth expectations in Q4, reporting revenue of $970 million versus an expected $938 million. The gap between the two likely comes partially from how new the DoorDash stock is, and the pandemic making it difficult to forecast. Despite the outsized growth, DoorDash shares initially fell sharply after the report, though they largely recovered on Friday.

Why the initial dip? I reckon the company’s net loss was larger than investors hoped — though a large GAAP deficit is standard for first quarters post-debut. That concern might have been tempered by the company’s earnings call, which included a note from the company’s CFO that it is “seeing acceleration in January relative to our order growth in December as well as in Q4.” That’s encouraging. On the flip side, the company’s CFO did say “starting from Q2 onwards, we’re going to see a reversion toward pre-COVID behavior within the customer base.”

Takeaway: Big companies are anticipating a return to pre-COVID behavior, just not quite yet. Firms that benefited from COVID-19 are being heavily scrutinized. And they expect tailwinds to fade as the year progresses.

And then there’s Airbnb, which is up around 16% today. Why? It beat revenue expectations, while also losing lots of money. Airbnb’s net loss in Q4 2020 was more than 10x DoorDash’s own. So why did Airbnb get a bump while DoorDash got dinged? Its large revenue beat ($859 million, instead of an expected $748 million), and potential for future growth; investors are expecting that Airbnb’s current besting of expectations will lead to even more growth down the road.

Takeaway: Provided that you have a good story to tell regarding future growth, investors are still willing to accept sharp losses; the growth trade is alive, then, even as companies that may have already received a boost endure increased scrutiny.

For startups, valuation pressure or lift could come down to which side of the pandemic they are on; are they on the tail end of their tailwind (remote-work focused SaaS, perhaps?), or on the ascent (restaurant tech, maybe?). Something to chew on before you raise.

It was one blistering week for funding rounds. Crunchbase News, my former journalistic home, has a great piece out on just how many massive rounds we’re seeing so far this year. But even one or two steps down in scale, funding activity was super busy.

A few rounds that I could not get to this week that caught my eye included a $90 million round for Terminus (ABM-focused GTM juicer, I suppose), Anchorage’s $80 million Series C (cryptostorage for big money), and Foxtrot Market’s $42 million Series B (rapid delivery of yuppie and zoomer essentials).

Sitting here now, finally writing a tidbit about each, I am reminded at the sheer breadth of the tech market. Termius helps other companies sell, Anchorage wants to keep your ETH safe, while Foxtrot wants to help you replenish your breakfast rosé stock before you have to endure a dry morning. What a mix. And each must be generating venture-acceptable growth, as they have not merely raised more capital but raised rather large rounds for their purported maturity (measured by their listed Series stage, though the moniker can be more canard than guide.)

I jokingly call this little section of the newsletter Market Notes, a jest as how can you possibly note the whole market that we care about? These companies and their recent capital infusions underscore the point.

Finally, two notes from earnings calls. The first from Root, which is a head scratcher, and the second from Booking Holdings’ results.

I chatted with Alex Timm, Root Insurance’s CEO this week moments after it dropped numbers. As such I didn’t have much context in the way of investor response to its results. My read was that Root was super capitalized, and has pretty big expansion plans. Timm was upbeat about his company’s improving economics (on a loss ratio and loss-adjusted expenses basis, for the insurtech fans out there), and growth during the pandemic.

But then today its shares are off 16%. Parsing the analyst call, there’s movement in Root’s economic profile (regarding premium-ceding variance over the coming quarters) that make it hard to fully grok its full-year growth from where I sit. But it appears that Root’s business is still molting to a degree that is almost refreshing; the company could have gone public in 2022 with some of its current evolution behind it, but instead it raised a zillion dollars last year and is public now.

Sticking our neck out a bit, despite fellow neo-insurnace player Lemonade’s continued, and impressive valuation run, MetroMile’s stock is also softening, while Root’s has lost more than half its value from its IPO date. If the current repricing of some neo-insurance players continues, we could see some private investment into the space slow. (Fewer things like this?) It’s a possible trend we’ll have eyes on this year.

Next, Booking Holdings, the company that owns Priceline and other travel properties. Given that Booking might have notes regarding the future of business travel — which we care about for clues regarding what could come for remote work and office culture, things that impact everything from startup hub locations to software sales — The Exchange snagged a call slot and dialed the company up.

Booking Holdings’ CEO Glenn Fogel didn’t have a comment as to how his company is trading at all-time highs despite suffering from sharp year-over-year revenue declines. He did note that the pandemic has shaken up expectations for conversations, which could limit short-term business travel in the future for meetings that may now be conducted on video calls. He was bullish on future conference travel (good news for TechCrunch, I suppose), and future travel more generally.

So concerning the jetting perspective, we don’t know anything yet. Booking Holdings is not saying much, perhaps because it just doesn’t know when things will turn around. Fair enough. Perhaps after another three months of vaccine rollout will give us a better window into what a partial return to an old normal could look like.

And to cap off, you can read Apex Holdings’ SPAC presentation here, and Markforged’s here. Also I wrote about the buy-now-pay-later space here, riffed on the Digital Ocean IPO with Ron Miller here, and doodled on Toast’s valuation and the Olo debut here.

Hugs, and have a lovely weekend!

Powered by WPeMatico

Amidst all the hype that Lemonade (IPO), Root (IPO), Metromile (SPAC-led debut) and other insurtech players have generated in the last year, it’s been easy to forget about Oscar Health. But now that the company founded in 2012 is approaching the public markets, one of the early tech-themed insurance companies is catching up on the attention front.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

So this morning we’re digging into Oscar Health’s first IPO pricing interval, hoping to understand how the market is valuing its unprofitable health-insurance enterprise.

Recall that Oscar Health was valued at around $3.2 billion in March of 2018. That datapoint, via PitchBook, is dated. Oscar Health raised hundreds of millions since (per several venture-capital tracking databases, including Crunchbase) but we lack a final private valuation for the company.

Recall that Oscar Health was valued at around $3.2 billion in March of 2018. That datapoint, via PitchBook, is dated. Oscar Health raised hundreds of millions since (per several venture-capital tracking databases, including Crunchbase) but we lack a final private valuation for the company.

Regardless, with Oscar Health now targeting a $32 to $34 per-share IPO range, we can get our hands dirty.

Let’s get some valuation numbers and then decide if Oscar Health feels cheap or expensive at that price.

Oscar Health is looking to reap as much as $1.21 billion in its IPO, a huge sum. The company is selling 30,350,920 shares, with 4,650,000 additional shares reserved for its underwriters. Existing shareholders are selling another 649,080 shares.

This means that after the IPO, Oscar Health will have 197,037,445 Class A and B shares in circulation, or 201,687,445 after counting shares reserved for its underwriters.

Using the company’s $32 to $34 per-share range, we can calculate a valuation minimum of $6.31 billion for the company (lower share count, low-end of price range) and $6.86 billion (higher share count, high-end of price range). That’s the company’s simple IPO valuation.

Oscar Health may also sell up to $375 million of its shares at its IPO price to three different funds. The company advises that the “indication of interest is not a binding agreement or commitment to purchase,” so we can ignore it for now.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Not alone, but you might be able to make a lot of progress with the right data in the right hands. And that’s precisely what the startup we’re talking about today is up to.

The Exchange caught up with Terry Myerson and Lisa Gurry this week, the CEO and CMO of Truveta, a young company that wants to collect oodles of data from healthcare providers, anonymize it, aggregate it and make it available to third parties for research.

It’s a big task, but the team behind Truveta has experience with big projects. Myerson is best known for his time one-rung below the top of the Microsoft org chart, where he ran things you might have heard of, like Windows. Gurry was a leader inside that org, most recently working on strategy for the Microsoft Store product.

But now they are at a healthtech data company. How did that come to be? After Myerson left Microsoft he worked with Madrona, the Seattle-area venture capital firm, and the Carlyle Group, a huge investing group with a taste for private equity. A few years later, several former Microsoft co-workers of Myerson had wound up at Providence, a healthcare giant. They reached out to Myerson around when COVID-19 was first locking down the United States. The former Microsoft exec agreed to take part in a few calls, but didn’t formally join them as he was stuck at home.

During that time he learned that Providence had put together a white paper concerning the idea that Truveta would become, that by collecting data from healthcare providers a dataset of sufficient size and diversity could be compiled to allow research of all sorts to leverage it. Myerson got stuck on the concept, later founding the company. Then he called up some former colleagues, including Gurry, to help him build it.

Truveta has around 50 people today and will scale to around 100 this year, Myerson said.

Questions abound in your head, I’m sure. Things are still early at Truveta, but the company announced last week that it has signed up 14 healthcare providers to help with its data goals. Those firms are also investors in the company (Myerson put in capital in as well).

I was curious about the company’s business plan. Per Myerson, Truveta will charge different rates depending on who wants to access its data. As you can imagine, commercial entities will pay a different price than an independent researcher.

Next for Truveta is getting more data, locking down its internal data schema, collecting feedback from researchers and, later, approaching commercial access.

Healthcare in America is inequitable — something that the pair of Truveta executives stressed during our call — thus giving the company a huge market to improve and make less racist and sexist.

It was a bit odd to talk to Myerson and Gurry about their startup. In the past I’d chatted with them about some of Microsoft’s largest platforms. Let’s see how fast they can transform Truveta from an idea I can’t help but dig, to a company that is a viable commercial concern. And then how big they can grow it.

A lot has happened in the past few days that we couldn’t get to. Adyen’s earnings, for example. The European payments platform reported H2 revenues of €379.4 million, up 28% compared to the year ago half-year. And from that it reported EBITDA of €236.8 million. Who said fintech can’t be profitable? (Note: Adyen’s results are required reading if you care about Stripe’s valuation and future public offering.)

And there were some rounds that also fell through our fingers. Investments like CloudTalk’s recent $7.3 million Series A. The Slovakia-based startup previously raised a $1.6 million seed round in 2019. The startup, as its name suggests, offers cloud telephony services to call centers.

We suspected that CloudTalk probably had a pretty good year in 2020 thanks to global growth in remote work. It did. In an email, CloudTalk said that it has not seen “Zoom-like [growth] figures” but that in 2020 demand for its services “exceeded [its] expectations.” That helps explain its latest round.

The Exchange was also curious if the company had a perspective on subscription pricing versus consumption pricing, a rising topic amongst software dorks such as myself (more to come on this next week with notes from Appian, Fastly and others). Per the company, CloudTalk charges “for both seats and for usage,” making it a hybrid company from a pricing perspective. CloudTalk called its pricing setup “a good balance for both parties because customers like to know what they are going to be paying ahead of time.”

It’s a startup to keep in mind. As is Zolve, a globally themed neobank with a focus on helping expats have a working financial world. I couldn’t get to it, but TechCrunch wrote it up. More here.

And in case you didn’t have time to watch television during work the last few days let’s talk about Robinhood. Which enjoyed a Congressional hearing this week that was mostly dull apart from some notes on the fintech giant’s business model.

Finally, it was a busy week for crowded startup niches. There was more money for OKR startups, leading to our question about VCs putting capital into related companies in the future. Public also raised several hundred million dollars. Because why not. And low-code player OutSystems raised $150 million to round out the group. It was one hell of a week.

I will leave you with a few data points. First, that Clubhouse’s metrics are finally starting to match the hype around the product. People are showing up in droves, pushing its total download figures over the 10 million mark.

And in news that I missed, Substack crossed the 500,000 subscriber mark. That’s impressive!

And to close, a Chicago-based, home-focused insurtech startup called Kin crossed the $10 billion “total insured property value” mark this week. The Exchange reached out, asking the company about its economics. After all it’s not hard to run up premium volume if you are selling dollars for 50-cent pieces.

Ruth Awad from the company responded that her company’s “ loss rate is 53% and our gross margins are 32%.” Not bad at all. Given how quickly insurtech has gone from experiment to public-success, Kin is a company to keep tabs on.

Wrapping, please make sure to support your local heavy metal band this weekend,

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Earlier this week TechCrunch broke the news that Public, a consumer stock trading service, was in the process of raising more money. Business Insider quickly filled in details surrounding the round, that it could be around $200 million at a valuation of $1.2 billion. Tiger could lead.

Public wants to be the anti-Robinhood. With a focus on social, and a recent move away from generating payment for order flow (PFOF) revenues that have driven Robinhood’s business model, and attracted criticism, Public has laid its bets. And investors, in the wake of its rival’s troubles, are ready to make it a unicorn.

Of course, the Public round comes on the heels of Robinhood’s epic $3.4 billion raise, a deal that was shocking for both its scale and speed. The trading service’s investors came in force to ensure it had the capital it needed to continue supporting consumer trades. Thanks to Robinhood’s strong Q4 2020 results, and implied growth in Q1 2021, the boosted investment made sense.

As does the Public money, provided that 1) The company is seeing lots of user growth, and 2) That it figures out its forever business model in time. We cannot comment on the second, but we can say a bit about the first point.

Thanks not to Public, really, but M1 Finance, a Midwest-based consumer fintech that has a stock-buying function amongst its other services (more on it here). It told TechCrunch that it saw a quadrupling of signups in January as compared to December. And in the last two weeks, it saw six times as many signups as the preceding two weeks.

Given that M1 doesn’t allow for trading — something that its team repeatedly stressed in notes to TechCrunch — we can’t draw a perfect line between M1 and Public and Robinhood, but we can infer that there is huge consumer interest in investing of late. Which helps explain why Public, which is hunting up a way to generate long-term incomes, can raise another round just months after it closed a different investment.

Our notes last year on how savings and investing were the new thing last year are accidentally becoming even more true than we expected.

As the week came to a close, Coupang filed to go public. You can read our first look here, but it’s going to be big news. Also on the IPO beat, Matterport is going out via a SPAC, I chatted with Metromile CEO Dan Preston about his insurtech public offering this week that also came via a SPAC, and so on.

Oscar Health filed, and it doesn’t look super strong. So its impending valuation is going to test public traders. That’s not a problem that Bumble had when it priced above-range this week and then skyrocketed after it started to trade. Natasha and I (she’s on Equity, as well) have some notes from Bumble CEO Whitney Wolfe Herd that we’ll get to you early next week. (Also I chatted about the IPO with the BBC a few times, which was neat, the first of which you can check out here if you’d like.)

Roblox’s impending public debut was also back in the news this week. The company was a bit bigger than it thought last year (cool), but may delay its direct listing to March (not cool).

Near to the IPO beat, Carta started to allow its own shares to trade recently, on the back of news that its revenues have scaled to around $150 million. Not bad Carta, but how about a real IPO instead of staying private? The company’s valuation more than doubled during the secondary transitions.

And then there were so very many cool venture capital rounds that I couldn’t get to this week. This Koa Health round, for example. And whatever this Slync.io news is. (If you want some earlier-stage stuff, check out recent rounds from Treinta, Level, Ramp and Monte Carlo.

And to close, a small callout to Ontic, which provides “protective intelligence software” and said that its revenue grew 177% last year. I appreciate the sharing of the numbers, so wanted to highlight the figure.

Wrapping this week, I have a final bit for you to chew on from Mark Mader, the CEO of Smartsheet, a public company — former startup, it’s worth noting — that plays in the no-code, automation and collaboration markets. That’s a rough summary. Anyhoo, I asked Mader about no-code trends in 2021, as I have my eyes on the space. Here’s what he wrote for us:

If you thought the sudden shift to remote work sped up corporate America’s shift to digital, you haven’t seen anything yet. Digital transformation is going to accelerate even more rapidly in 2021. Last year, the workforce was exposed to many different types of technology all at once. For example, a company may have deployed Zoom or DocuSign for the first time. But much of this shift involved taking analog processes like meetings or document signing and approval and bringing them online. Things like this are merely a first step. 2021 is the year the companies will begin to connect large-scale digital events to infrastructure that can make them automated and repeatable. It’s the difference between one person signing a document and hundreds of people signing hundreds of documents, with different rules for each one. And that’s just one example. Another use case could involve linking HR software to project management software for automated, real-time resource allocation that allows a company to get more out of both platforms, as well as its people. The businesses that can automate and simplify complex workflows like these will see dramatically improved efficiency and return on their technology investments, putting them on the path to true transformation and improved profitability.

We shall see!

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

It’s been a bizarre few weeks, with Robinhood raising a torrent of new funds to keep its zero-cost trading model afloat during turbulent market conditions, other neo-trading houses changing up their business model and more. But amidst all the moves in startup-land, something has been itching in the back of my head: Why are several rich people pumping crappy assets?

It’s fine for a retail investor to share trading ideas amongst themselves; it has happened, will happen, and will always happen. But we’ve seen folks like Elon Musk and Chamath Palihapitiya use their broad market imprint to encourage regular folks — directly and indirectly — to buy into some pretty silly trades that could lose the retail crowd lots of money that they may not be able to afford.

Think of Elon coming back to Twitter to pump Doge, a joke of a cryptocurrency that is highly volatile and mostly useless. Or Chamath putting money into GameStop publicly, a move that he is better equipped than most to get into and out of. Which he did. And made money. Most folks that played the GameStop casino have not been as lucky, and many have lost more than they can afford.

Caveat emptor and all that, but I do not love folks with savvy and capital leading regular people into risky trades or into assets that are not backed by long-term fundamentals, but instead a small shot at near-term returns. Yoof.

Finally, keeping up the theme of general annoyance, Senator Hawley is back in the news this week with an attention-focused announcement of an idea to block big tech companies from buying smaller companies. As you would expect from the insurrection-friendly Senator, it’s not an incredibly serious proposal, and it’s written so vaguely as to be nearly humorous.

But as I wrote here on my personal blog about all of this, what does matter out of the generally irksome pol is that there is bipartisan interest in limiting the ability of big tech companies to buy smaller companies. For startups, that is not good news; M&A exits are critical liquidity events for startups, and big companies have the most money.

It’s no sauté of my onions if startup valuations fall, but I think there’s been plenty of attention noting that some Democrats and some Republicans in the U.S want to undercut top-down tech M&A, and not nearly enough notice concerning what the effort might do to startup valuations and funding. And if those metrics dip, there could be fewer upstarts in the market actually working to take on the giants.

Food for thought.

The Exchange caught up once again with Unity CFO Kim Jabal. We did so not merely to make jokes with her about games that we like or don’t like, but to keep tabs on how Jabal thinks as the financial head of a company that was private when she joined, and public now. A few observations:

And speaking of startups, let’s talk about a company that I’ve had my eye on that recently raised more capital: Deepgram. I covered the company’s Series A, a $12 million round in March 2020. Now it has raised $25 million more, led by Tiger, so this is a fun case of big money investing early-stage, I think. Regardless, Deepgram was a bet on a particular model for speech recognition, and, then, its market. its new investment implies that both wagers came out the right way up.

And I was chatting with the CEO of Databricks recently (more here on its latest megaround), who mentioned the huge gains made in AI, and more specifically around generative adversarial networks (GANs) NLP, and more. Our read is that we should expect to see more Deepgram-ish rounds in the future as AI and similar methods of approaching data make their way into workflows.

And fintech player Payoneer is going public. Via a SPAC. You can read the investor presentation here. Payoneer is not a pre-revenue firm going out via a blank check; it did an expected $346 million in 2020 rev. I’m bringing it to you for two reasons. One, read the deck, and then ask yourself why all SPAC decks are so ugly. I don’t get it. And then ask yourself why isn’t it pursuing a traditional IPO? Numbers are on pages 32 and 40. I can’t figure it out. Let me know if you have a take. Best response gets Elon’s dogecoin.

Wrapping up this week, TechCrunch has a new newsletter coming out on apps that is going to rule. Sarah Perez is writing it. You can sign up here, it’s free!

And if you need a new tune, you could do worse than this one. Have a great weekend!

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Click here if you want it in your inbox every Saturday morning.

Ready? Let’s talk money, startups and spicy IPO rumors.

We’re shaking things up this weekend in the newsletter, focusing on a series of larger themes and news items instead of having a few discrete sections. Why? Because there was too much to fit into our usual format. If you were a fan of the original layout, we’ll be back to it next week.

Today we’re talking Coinbase’s growth, how Juked.gg tapped the equity crowdfunding market, a noodle or two on the a16z media game, Talkspace’s SPAC, VC and founder predictions for 2021, and where’s the right place to found a company.

Sound good? Let’s get into it!

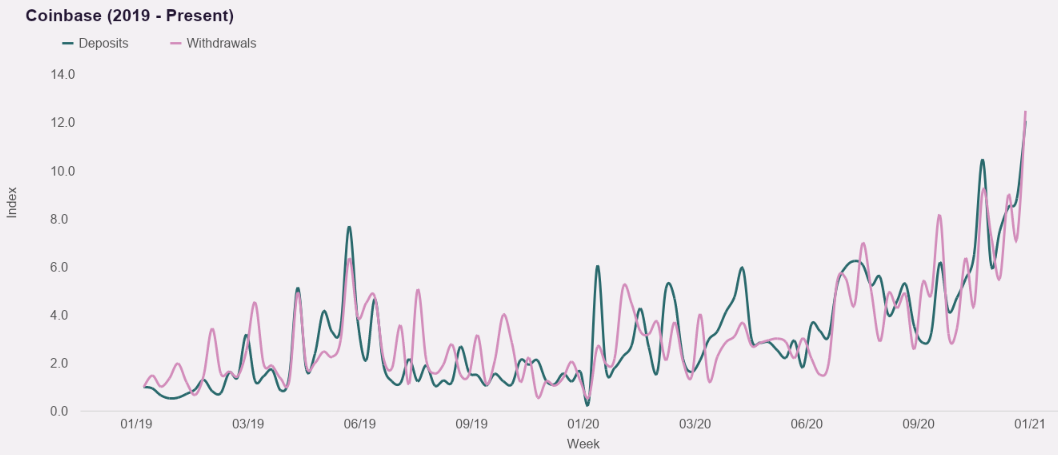

Thanks to Kazim Rizvi of Drop, parent company to Cardify which provides data on consumer spending, we have a look into how quickly deposits have scaled at American cryptocurrency platform Coinbase. As Coinbase has filed to go public, and we’re eagerly anticipating its eventual S-1 filing, we were stoked to get a directional look at how quickly consumer interest was growing for the assets it helps folks buy.

They are scaling rapidly. Using the first week of January 2019 as a baseline, by the last week of December 2020 deposits and withdrawals from Coinbase had grown by more than 12x apiece. That’s staggering growth, and while the data is somewhat volatile — and we’d treat it as directional instead of exact — on a week-to-week basis, it underscores how well companies like Coinbase may be performing as Bitcoin booms once again, bringing in more trading interest and consumer demand.

Via Cardify, Cardify data.

The Cardify data also indicates a multiplying of new customer acquisition at Coinbase over the same time period, and deposits scaling alongside the price of Bitcoin. As Bitcoin has topped the $30,000 mark recently, sharply higher than in recent quarters, the price gains may have helped Coinbase not only a solid Q4 2020, but perhaps put it on a path for a bonkers Q1 2021 as well.

If we were 10/10 excited about the Coinbase S-1 before this dataset, we’re now a heckin’ 12/10.

Esports is super cool and if you don’t agree, you are incorrect. But it doesn’t matter if you or I are right or not on the question, as the market has largely decided that competitive gaming is worth time, attention and investors’ money.

The proliferation of esports leagues and games and the like has led to a decidedly fragmented universe, however, lacking a central hub akin to what ESPN provides the world of traditional sports.

But not to worry, Juked.gg just raised capital to build a content hub for esports. This means that old folks like myself can still find out when tournaments are happening, and enjoy a dabble of League of Legends or Starcraft 2 pro play when we can, sans hunting around the internet for dates and times.

Juked.gg went through 500 Startups (more on its class here), catching our eye at the time as a neat nexus for esports-related content. Now flush with a little over $1 million that it raised on the Republic platform, it has big plans.

The Exchange spoke with Juked.gg’s co-founder and CEO Ben Goldhaber about his company’s performance to date. Per Goldhaber, Juked has scaled from 500 users when it launched in late 2019, to 50,000 in December of 2020. Ahead, Juked may invest more in journalism, more into social features, and more into user-generated content. We’ll have more on Juked as it gets its vision built, now powered by over a million dollars from 2,524 investors, each betting that the startup is building the right product to help unify a growing, if distributed, entertainment category.

To preserve our collective sanity, I’m not going to bang on at length here, but building out content at a VC firm is not new. Hell, how long ago did the First Round Review launch? What a16z appears to have in mind is different in scale, not substance. We chatted about it on Equity this week, in case you need more on the matter.

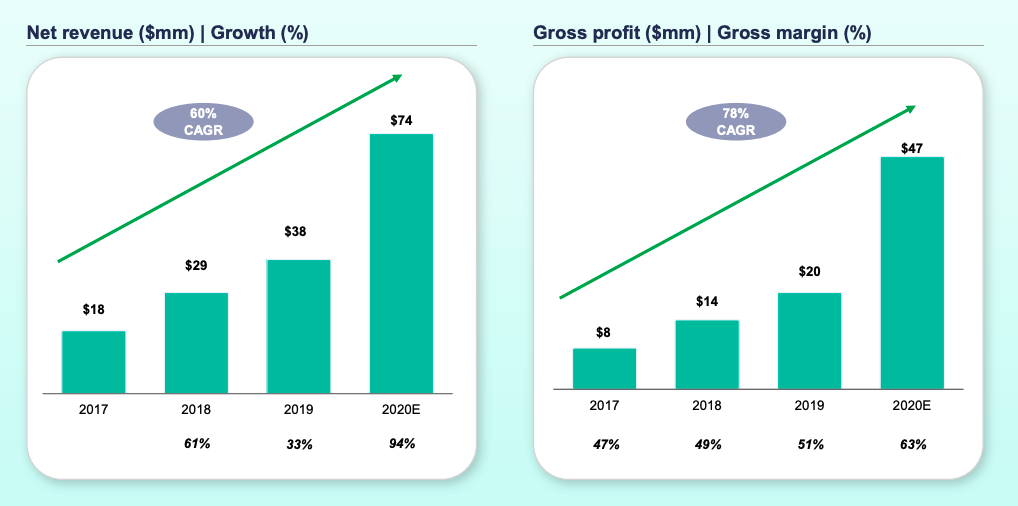

While it is enjoyable to mock SPACs, featuring as many do companies that are nascent to say the least, not all SPAC-led debuts are as silly as the rest. This is the case with the impending Talkspace deal, the deck for which you can read here.

What matters is this set of charts:

Look at that! Historical revenue growth! Improving gross margins! Rising gross profit!

You may argue that the company is not really worth an enterprise value of $1.4 billion that it will sport after its combination with Hudson Executive Investment Corp., but, hey, at least it’s a real business.

Seed VC NFX dropped a VC and founder survey the other day that I’ve been meaning to share with you. You can read the whole thing here, if you’d like.

I have two pull-outs for you this morning:

Initialized Capital put together some data on where founders think it is best to found a company. In 2020, nearly 42% of surveyed founders said the Bay Area. By 2021 that number had slipped to a little over 28%, with a plurality of 42% indicating that a distributed company is the best way to go.

I hear about this a lot from early-stage founders. They are often building what I call micro-multinationals, small companies that have a few employees in one country, and then a handful in others. Making that setup work is going to be a hotspot for HR software I reckon.

Regardless, the requirement of founding companies in the Bay Area is kaput. The advantages of founding there will linger much longer.

Coming up on The Exchange next week: The first entries of our new $50 million ARR series, featuring interviews with Assembly, SimpleNexus, Picsart, OwnBackup and others. And we have some $100 million ARR interviews in the can, as well.

Finally, to keep the The Powers That Be happy, The Exchange covered some neat stuff this week, including American VC results, fintech and unicorn venture capital, European and Asian venture capital results, how the IPO market is even more bonkers than you thought, and notes on what Qualtrics may be worth when it goes public.

Hugs, and let’s all get a nap in,

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Click here if you want it in your inbox every Saturday morning.

Ready? Let’s talk money, startups and spicy IPO rumors.

It was yet another week of startups that became unicorns going public, only to see their valuation soar. Already marked up by their IPO pricing, seeing so many unicorns achieve such rich public-market valuations made us wonder who was mispricing whom.

It’s a matter of taste, a semantic argument, a tempest in a teacup. What matters more is that precisely no one knows what anything is worth, and that’s making a lot of people rich and/or mad.

This is not a new theme. I’ve touched on it for years, but what matters for us today is that there appear to be three distinct valuation bands for companies, and the gaps between them do not appear ready to shrink. You could even argue that they have widened.

Band 1 is the private capital cohort. These are the folks who valued Affirm at $19.93 per share in its September 2020 round and Roblox at $4 billion in February of 2020. Now Affirm is worth $116.58 per share, and Roblox is worth $29.5 billion. Whoops?

Band 2 is the long-term public investing cohort. These are folks critical in the IPO pricing context. They are willing to pay more for startups than the private capital crew. Affirm was not worth under $20 per share to this group, instead it was worth $49 per share just a few months later. Whoops?

Band 3 is the retail cohort, the /r/WallStreetBets, meme-stock, fintech Twitter rabble that are both incredibly fun to watch and also the sort of person you wouldn’t loan $500 to while in Las Vegas. They are willing to pay nearly infinite money for certain stocks — like Tesla — and often far more than the more conservative public money. Demand from the retail squad can greatly amplify the value of a newly listed company by making the supply/demand curve utterly wonky. This is how you get Poshmark more than doubling a strong IPO valuation on its first day.

Most investors do well in today’s world. Though Band 1 likes to blame Band 2 for not being willing to pay Band 3 prices, it always sounds like the private capital folks are merely complaining about sharing some of the winnings with another party.

Regardless, who really knows what anything is worth? I was recently chatting with an early-stage founder who has a history of investing — narrowing it down to 17,823 people, I know — about the price of software companies both private and public and why they may or may not make sense. He said that old valuation models at banks presumed that software companies’ growth would go to zero over time, and that profits would be rare among SaaS concerns. Both concepts were wrong, so prices went up.

But I have yet to have anyone explain to me why companies that would have been valued at 10x next year’s revenues can now get, at median, 18.1x. I have a working theory of what’s going on, but none of it points to sanity, or pricing that is grokkable through a lens that isn’t hype.

(You can hit reply to this email and tell me why I am dumb if you’d like. I will buy the person with the best valuation explanation coffee when the world works again.)

On the milestone front, it was a huge week for leaving the private markets and joining the Big Kid Club. Namely for Affirm and Poshmark, which priced well and started to trade. And for Bumble, which filed to go public. They are targeting a good IPO window.

But there was lots more going on, including a milestone that caught my eye. M1 Finance, a fintech startup that brings together lots of pieces of the fintech playbook into a single service, reached $3 billion in assets under management (AUM) this week. The company had reached $2 billion in AUM last September, after reaching $1 billion in February of 2020.

Why do we care? The company previously told TechCrunch that it works to generate revenues worth around 1% of AUM. If that percentage has held past its October, 2020 Series C, the company just added around $10 million in ARR in under half a year. That’s a pace of revenue creation that made me sit up and take notice. (Shoutout Josh for never shutting up about the Midwest.)

But I really bring up the M1 Finance milestone for a different reason. Namely that I am consistently surprised at how deep certain markets are. Neobanks that are still growing; the OKR software market’s surprising depth; the ability of M1 to accrete deposits in a market with so many incumbents and well-funded startups.

Perhaps this is why prices make no sense; if you can’t see the edge limits of TAM, can anything be overpriced?

Moving on, some quick notes on things from the week that mattered:

Aziz Gilani, a managing director at Mercury Fund and an advocate of Texas (observe his Twitter handle), wrote in late regarding our query for investor notes on the Visa-Plaid breakup. You can read the rest here.

But who are we to deprive you of useful notes. And Gilani is a nice person. So, here are his $0.02:

My big take-away on the Plaid/Visa deal falling apart is about how fast everything in 2021 is moving. Arguably the biggest advantage of SPACs over direct listings and IPOs is how fast those liquidity events can get done. In a world in which valuation[s] change week to week, the delays created by the DOJ can kill a deal – even if the DOJ would eventually lose in court.

I’m philosophically super negative about the government imposing their will, but I’m also personally excited about the current wave of insurgent startups not getting gobbled up by the FAANGs of the world. For the last several years too many startups fell victim to the “quick exit” mentality personified by Mint selling so fast to Intuit. With fast/cheap capital freely available, today’s crop of startups are going big.

Worth chewing on.

What a week. I have only a few things left for you, including some early-stage rounds that I could not get thanks to waves arms around generally but wanted to flag all the same.

Hugs,

Powered by WPeMatico