The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Now that the great Y Combinator rush is behind us, we’re returning to a topic many of you really seem to care about: no-code and low-code apps and their development.

We’ve explored the theme a few times recently, once from a venture-capital perspective, and another time building from a chat with the CEO of Claris, an Apple subsidiary and an early proponent of low-code work.

Today we’re adding notes from a call with Appian CEO Matt Calkins that took place yesterday shortly after the company released its most recent earnings report.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Appian is built on low-code development. Having gone public back in 2017, it is the first low-code IPO we can think of. With its Q2 results reported on August 6, we wanted to dig a bit more into what Calkins is seeing in today’s market so we can better understand what is driving demand for low- and no-code development, specifically, and demand for business apps more generally in 2020.

As you can imagine, COVID-19 and the accelerating digital transformation are going to come up in our notes. But, first, let’s take a look at Appian’s quarter quickly before digging into how its low-code-focused CEO sees the world.

As you can imagine, COVID-19 and the accelerating digital transformation are going to come up in our notes. But, first, let’s take a look at Appian’s quarter quickly before digging into how its low-code-focused CEO sees the world.

Appian had a pretty good Q2. The company reported $66.8 million in revenue for the three-month period, ahead of market expectations that it would report around $61 million, though collected analyst estimates varied. The low-code platform also beat on per-share profit, reporting a $0.12 per-share loss after adjustments. Analysts had expected a far worse $0.25 per-share deficit.

The period was better than expected, certainly, but it was not a quarter that showed sharp year-over-year growth. There’s a reason for that: Appian is currently shedding professional services revenue (lower-margin, human-powered stuff) for subscription incomes (higher-margin, software-powered stuff). So, as it exchanges one type of revenue for another with total subscription revenue rising a little over 12% in Q2 2020 compared to the year-ago quarter, and professional services revenue falling around 10%, the company’s growth will be slow but the resulting revenue mix improvement is material.

Most importantly, inside of its larger subscription result for the quarter ($41.4 million) were its cloud subscription revenues, worth $29.6 million for the quarter and up 30% compared to the year-ago period. Summing, the company’s least lucrative revenues are falling as its most lucrative accelerate at the fastest clip of any of its cohorts. That’s what you’d want to see if you are an Appian bull.

Shares in the technology company are up around 45% this year. With that, we can get started.

Powered by WPeMatico

Setting our dive into Palantir’s gross margins aside for another day, Sumo Logic filed to go public this morning. The Redwood City-based, former startup raised around $340 million while private, according to Crunchbase data.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Sumo Logic parses information collected from its customers’ enterprise apps and integrations to help them pinpoint operational and security issues and lets them dashboard additional elements as they wish. The company claims in its S-1 that its code is “continuous intelligence,” which it brands as “a new category of software.”

Our own Ron Miller summarized Sumo Logic as a “cloud data analytics and log analysis company” when it raised a $110 million Series G last May. At the time, it was valued at north of $1 billion, making it a unicorn.

Sumo Logic’s IPO has been in its plans for some time. We can see this in a 2017 TechCrunch headline noting that Sumo had then raised $75 million, and was “on path” to a public offering. So, how healthy is the company, and what have its investors bought with about a third of a billion dollars in capital? Let’s find out.

Up top: Sumo Logic operates on a fiscal calendar that ends January 31 of each calendar year. This is super standard for SaaS companies as it allows the firm to not wrap its year during the holiday period. This is good for sales teams and so forth.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. You can subscribe to the newsletter here if you haven’t yet.

Ready? Let’s talk money, startups and spicy IPO rumors.

As I write to you on Friday afternoon, the Palantir S-1 has yet to drop, but TechCrunch did break some news regarding the impending filing and just how big the company actually is. Please forgive the block quote, but here’s our reporting:

In screenshots of a draft S-1 statement dated yesterday (August 20), Palantir is listed as generating revenues of roughly $742 million in 2019 (Palantir’s fiscal year is a calendar year). That revenue was up from $595 million in 2018, a gain of roughly 25%. […] Palantir lists a net loss of roughly $580 million for 2019, which is almost identical to its loss in 2018. The company listed a net loss percentage of 97% for 2018, improving to a loss of 78% for last year.

A few notes from this. First, those losses are flat icky. Palantir was founded in 2003 or 2004 depending on who you read, which means that it’s an old company. And it was running an effective -100% net margin in 2018? Yowza.

Second, what the flocking frack is that revenue number? Did you expect to see Palantir come in with revenues of less than $1 billion? If you did, well done. After a deluge of articles over the years discussing just how big Palantir had become, I was anticipating a bit more (more here for context). Here are two examples:

Notably, Palantir’s real revenue result, or one very close to it, made it into Business Insider this April. The reporting makes the company’s S-1 less of a climax and more of a denouement. But, hey, we’re still glad to have the filing.

The Exchange will have a full breakdown of Palantir’s numbers Monday morning, but I think what Palantir coverage over the years shows is that when companies decline to share specific revenue figures that are clear, just presume that what they do share is misleading. (ARR is fine, trailing revenue is fine, “contract” metrics are useless.)

The Exchange spent a lot of time digging into e-commerce venture capital results this week, including notes from some VCs about why e-commerce-focused startups aren’t raising as much as we might have guessed.

Overstock!

We got a chance to fire a question over to the CEO of Overstock.com on the matter, adding to what we learned from private investors on the same topic. So here’s the online retailer’s CEO Jonathan Johnson, answering our question on how many smaller vendors are signing up to sell on its platform during today’s e-comm boom:

We have had increased demand to sell on Overstock and we are adding new partners daily. To protect the customer experience, we have become more selective and have increased the requirements to become a selling partner on our site. Our customers’ experience is critical to our long-term success and if partners cannot perform to our operational standards, we do not allow them to sell on our site.

We care because Shopify and BigCommerce are stacking up new rev, and we were curious how widely the e-commerce step-change from major platforms extended. Seems like all of them are eating.

How today’s evolving economic landscape isn’t working out better for e-commerce-focused startups is still a surprise. Normally when the world changes rapidly, startups do well. This time it seems that Amazon and a few now-public unicorns are snagging most of the gains.

Airbnb!

Anyhoo, onto the Airbnb world; we have a few data points to share this week. According to Edison Trends data that was shared with us, here’s how Airbnb is doing lately:

This explains why the company is prepping to go public sooner rather than later: The second-half of Q2 was a ramp back to normal for the company, and July was pretty good by the looks of it. If Airbnb is worth what it once was is not clear, but the company is certainly doing better than we might have expected it to. (More on the comeback here.)

For more on the big unicorn IPOs, I wrote a digest on Friday that should help ground you. I can say that with some confidence, as I wrote it to ground myself!

Finally some loose ends and other notes like an after-dinner amuse-bouche:

And we’ll wrap with a tiny note from Greg Warnock, managing director at Mercato via email about the late-stage venture capital market. We asked for “notes on current valuation trends, in particular re: ARR/run rate multiples.” Here’s what we heard back:

I think valuations are correlated with economic activity and certainly something like COVID would qualify, but it’s very much a lagging indicator. It takes a while for entrepreneurs’ expectations to shift. Once they feel like the economy has moved in a permanent way, they begin to rethink. The first thing that they experience a little bit more urgency. They start from a belief that they can raise money any time they want, from anyone they want. Soon they realize there are fewer investors in market, that those opportunities appear less frequently, and each one should be managed more carefully. From there they go to thinking about terms. They might have to be flexible around some terms or some construct. Finally, they go to just fundamentally thinking about valuation in terms of multiples.

Going back to my first comment about economic factors being a lagging indicator, COVID related shocks haven’t moved through the system yet. It will take something more like a year for all the expectations to shift. My experience is that a shift in the economy from an investor standpoint creates a flight to quality. Companies with lackluster performance are first to feel lack of options in fundraising and exits. High performing businesses are the last ones to experience a change in valuation multiples. It disproportionately affects average businesses more quickly and more dramatically than high quality businesses which may feel no significant effects.

Hugs, fist bumps and good vibes,

Powered by WPeMatico

After yesterday’s look into the somewhat lackluster pace of investment into e-commerce-focused startups this year, a few VCs sent in notes that added useful context. So this morning let’s discuss why the pace of e-commerce startup fundraising has been so milquetoast in 2020.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

To frame the oddity of e-commerce startups not raising a flood of cash during what are historic boom times, we noted Walmart’s staggering online sales growth in Q2, which TechCrunch’s Sarah Perez broke out into a separate piece. Today, for a soupçon more, Target reported its Q2 earnings. Its results are similar to Walmart’s own, if even more extreme.

The American retailer reported that its “store comparable” sales were up 10.9% in the quarter, which was rather good. But Target also reported that its “digital comparable sales grew 195%,” which is staggering. Target’s revenue mix moved from 7.3% digital in its year-ago quarter to 17.2% in its most recent.

Damn.

If you’ve been around the internet lately, you can’t help but trip over more data detailing this extraordinary moment in e-commerce history — there are years of change happening in just a quarter’s time. For a taste, former Andreessen denizen Benedict Evans has some great data on U.S. and U.K. e-commerce growth, and here’s yet another great chart to chew on. It goes on and on.

So the e-commerce boom is real, and the startup funding funk is as well, per the data we ingested yesterday via CB Insights. What gives? GGV’s Jeff Richards had an idea, and we chatted with Canaan’s Byron Ling as well. We’ve also done a little digging into some of the largest, recent e-commerce rounds to get some flavor on who is raising in the space. Ready?

If you recall, our thesis yesterday was that, perhaps, the kill zone theory often posited concerning Amazon meant that the e-commerce space is less investable than we’d otherwise imagine and that because some things are “sorted” to a degree, there is less green space available in the sector for startups to tackle.

Bits of that might be right.

Powered by WPeMatico

Robinhood announced this morning that it has raised $200 million more at a new, higher $11.2 billion valuation. The new capital came as a surprise.

Astute observers of all things fintech will recall that Robinhood, a popular stock trading service, has raised capital multiple times this year, including an initial $280 million round at an $8.3 billion valuation, and a later $320 million addition that brought its valuation to $8.6 billion.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Those rounds, coming in May and July, now feel very passé in the sense that they are frightfully cheap compared to the price at which Robinhood just added new funds. D1 Partners — a private capital pool founded in 2018 — led the funding.

The unicorn’s new nine-figure tranche, a Series G, values the firm at $11.2 billion. A $2.6 billion bump in about a month is an impressive result, one that points to an inescapable conclusion: Robinhood is still growing, and fast.

How fast is the question. There are three things to bring up in this regard: Trading growth at Robinhood, the company’s soaring incomes from selling order flow to other financial institutions, and, oddly enough, crypto. Let’s peek at each and come up with a good why as to the new Robinhood valuation.

After all, we’re going to see an IPO from this company before the markets get less interesting, if it’s smart.

Robinhood is currently walking a line between enthusiasm that its trading volume is growing and conservatism, arguing that its userbase is not majority-comprised of day traders. The company is stuck between the need for huge revenue growth and keeping pedestrian users from tanking their net worth with unwise options bets.

It’s worth noting that Robinhood spent a lot of its funding round announcement email to TechCrunch talking about its users safety and education work. It makes sense given that we know that the company is seeing record trades, and record incomes from options themselves. After a Robinhood user killed themself after misunderstanding an options trade on the platform, Robinhood pledged to do better. We’re keeping tabs on how well it manages to meet the mark of its promise.

But back to the revenue game, let’s talk volume. On the trading front Robinhood has lots of darts. And by darts we mean daily average revenue trades. Robinhood had 4.31 million DARTs in June, with the company adding that “DARTs in Q2 more than doubled compared to Q1” in an email.

The huge gain in trading volume does not mean that most Robinhood users are day trading, but it does imply that some are given the huge implied trading volume results that the DARTs figure points to. Robinhood saw around 129,300,000 trades in June, which is 30 days. That’s a lot!

Powered by WPeMatico

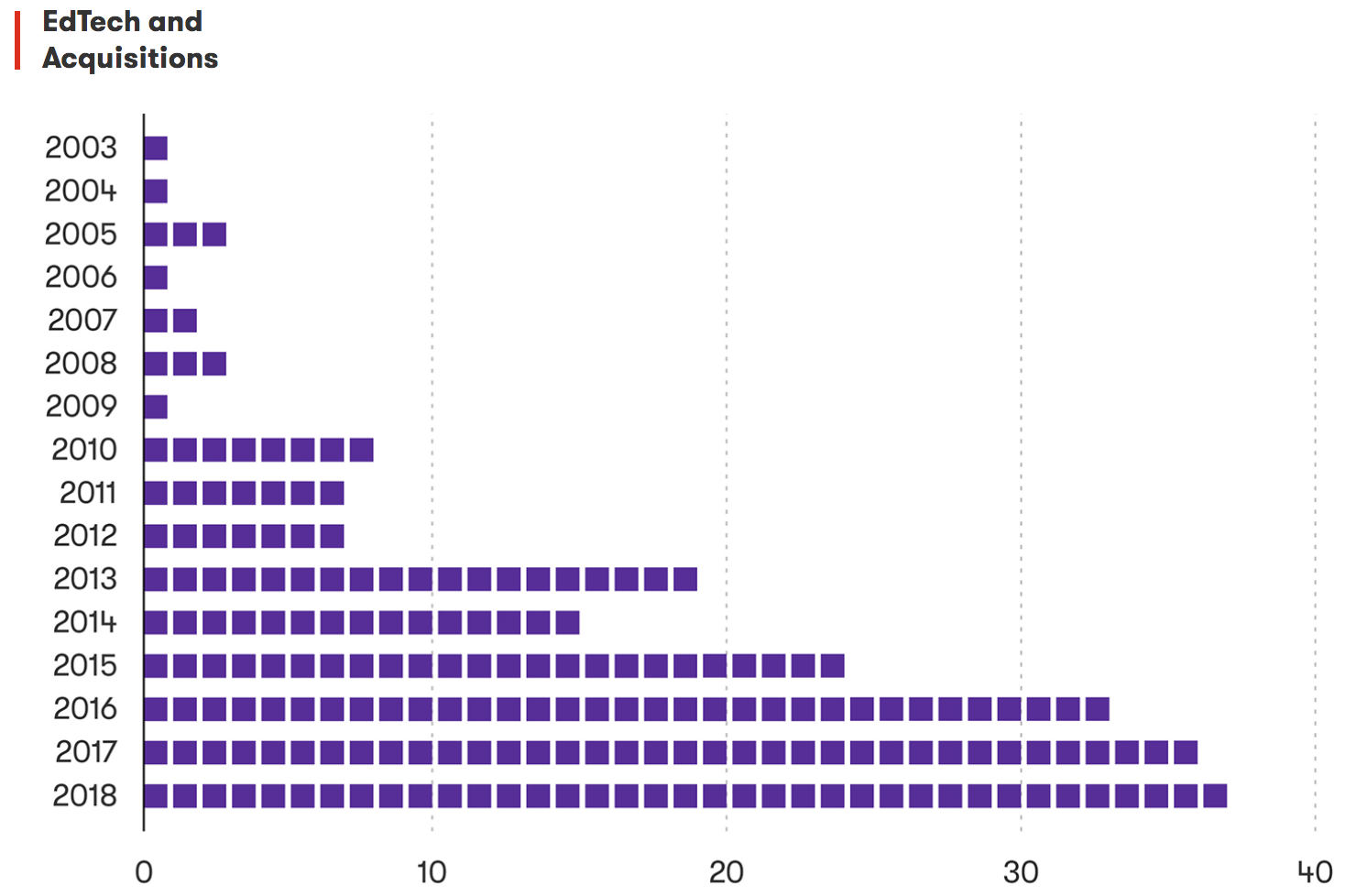

Before the coronavirus made edtech more relevant, companies in the sector were historically likely to see slow, low exits. Despite successful IPOs by 2U, Chegg and Instructure in the United States, public markets are not crowded with edtech companies.

Some of the largest exits in the space include LinkedIn’s scoop of Lynda for a $1.5 billion in cash and stock and TPG’s purchase of Ellucian for $3.5 billion.

But both of those deals happened in 2015. Five years later, edtech is cooler and surging — but is it seeing exits? Are Lynda and Ellucian one-off success stories?

2U’s co-founder and CEO, Chip Paucek, said he is optimistic.

“We are a rare edtech IPO,” he told TechCrunch last week. “For a long time in edtech it was either ‘sell to Pearson or not.’”

Despite the sector’s slow past, Paucek said now is a good time to start an edtech company because the sector “is finally starting to hit its stride” with more back-end infrastructure and demand for online education.

This morning, let’s use some data to paint a picture of the landscape of edtech exits and bring some balance to this stodgy stereotype.

Boot the growth

Boot the growthThere have been approximately 225 acquisitions in edtech between 2003 and 2018, according to Crunchbase data. RS Components sent me a graph in March to contextualize this timeframe a bit more:

Edtech deals over time. Graph credit: RS Components.

Powered by WPeMatico

Venture capitalists and other investors have poured capital into fintech startups around the world in recent years, including a record number of rounds worth $100 million or more in the second quarter of 2020. In Q2 2020 venture-backed fintech startups raised 28 nine-figure rounds, underscoring the scale of the bet investors are making on fintech’s long-term success.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Inside that fintech wave are various hubs of activity, including payments tech, investing and banking. That last category has helped give rise to so-called neobanks, startup banking entities that offer mobile-first, consumer-friendly banking tools and services. Given the old-fashioned nature of banking in many countries (and how far out of reach banking remains for many) neobanks have seen strong uptake by users in recent years.

And the startup cohort has raised oceans of capital to help fuel its growth. In America, Chime was most recently valued at $5.8 billion after raising hundreds of millions in late 2019. More recently, neobank Revolut added $80 million to its Q1 2020 round worth $500 million. Revolut is also worth north of $5 billion. Monzo is well-funded (albeit at a recent valuation reduction), Latin America-focused NuBank is worth $10 billion, according to Crunchbase, Starling recently raised another £40 million, while Germany’s N26 is worth over $3 billion after its most recent nine-figure round.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

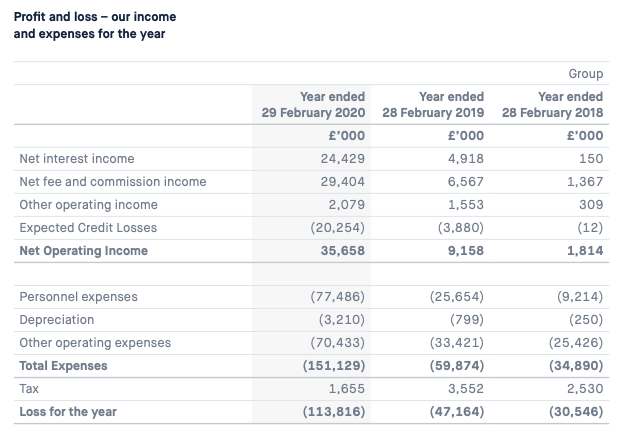

Of course, startups don’t raise money for fun; they raise it to invest it in their operations and drive scale. So, we knew that these megafundraisers were losing money on purpose. All the same, let’s peek at the economics of several neobanks, as their now dated and thus not at all current results can provide useful context on two points: Why investors are excited to put their capital to work in neobanks, and why neobanks always seem to have another check to announce.

To prevent my receiving unhappy emails from irked fans of these companies, please bear in mind that we’re looking several quarters back when observing the following results.

It would be lovely to have more recent data, but with European neobanks reporting their — roughly — 2019 results in recent weeks, this is what we have. We are going to parse the numbers, but we will not conflate past performance with current results. We do not know much about 2020 neobank financial performance.

Anyhoo, to the numbers. You can read the full documents from Monzo here, Starling here (or here, if that link is struggling) and Revolut here.

Let’s start with Monzo, which has a clear set of figures for us to peek at:

Image Credits: Monzo

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter for your weekend enjoyment. It’s broadly based on the weekday column that appears on Extra Crunch, but free. And it’s made just for you. You can sign up for the newsletter here.

With that out of the way, let’s talk money, upstart companies and the latest spicy IPO rumors.

(In time the top bit of the newsletter won’t get posted to the website, so do make sure to sign up if you want the whole thing!)

One of the most interesting disconnects in the market today is how VC Twitter discusses successful IPOs and how the CEOs of those companies view their own public market debuts.

If you read Twitter on an IPO day, you’ll often see VCs stomping around, shouting that IPOs are a racket and that they must be taken down now. But if you dial up the CEO or CFO of the company that actually went public to strong market reception, they’ll spend five minutes telling you why all that chatter is flat wrong.

Case in point from this week: BigCommerce. Well-known VC Bill Gurley was incensed that shares of BigCommerce opened sharply higher after they started trading, compared to their IPO price. He has a point, with the Texas-based e-commerce company pricing at $24 per share (above a raised range, it should be said), but opened at $68 and is worth around $88 on Friday as I write to you.

So, when I got BigCommerce CEO Brent Bellm on Zoom after its debut, I had some questions.

First, some background. BigCommerce filed confidentially back in 2019, planned on going public in April, and wound up delaying its offering due to the pandemic, according to Bellm. Then in the wake of COVID-19, sales from existing customers went up, and new customers arrived. So, the IPO was back on.

BigCommerce, as a reminder, is seeing growth acceleration in recent quarters, making its somewhat modest growth rate more enticing than you’d otherwise imagine.

Anyhoo, the company was worth more than 10x its annual run-rate at its IPO price if I recall the math, so it wasn’t cheap even at $24 per share. And in response to my question about pricing Bellm said that he was content with his company’s final IPO price.

He had a few reasons, including that the IPO price sets the base point for future return calculations, that he measures success based on how well investors do in his stock over a ten-year horizon, and that the more long-term investors you successfully lock in during your roadshow, the smaller your first-day float becomes; the more investors that hold their shares after the debut, the more the supply/demand curve can skew, meaning that your stock opens higher than it otherwise might due to only scarce equity being up for purchase.

All that seems incredibly reasonable. Still, VCs are livid.

The Exchange spent a lot of time on the phone this week, leading to a host of notes for your consumption. And there was a deluge of interesting data. So, here’s a digest of what we heard and saw that you should know:

Whatever the case, during our chat Fastly CEO Joshua Bixby taught me something new: Usage-based software companies are like SaaS firms, but more so.

In the old days, you’d buy a piece of software, and then own it forever. Now, it’s common to buy one-year SaaS licenses. With usage-based pricing, you make the buying choice day-to-day, which is the next step in the evolution of buying, it feels. I asked if the model isn’t, you know, harder than SaaS? He said maybe, but that you wind up super aligned with your customers.

To wrap up, as always, here’s a final whack of data, news and other miscellania that are worth your time from the week:

We’ve blown past our 1,000 word target, so, briefly: Stay tuned to TechCrunch for a super-cool funding round on Monday (it has the fastest growth I can recall hearing about), make sure to listen to the latest Equity ep, and parse through the latest TechCrunch List updates.

Hugs, fistbumps, and good vibes,

Powered by WPeMatico

My friend and colleague Natasha Mascarenhas has been reporting on the edtech beat quite a lot in 2020. So far reading her coverage, I’ve discovered that not only is edtech less dull than I anticipated, it’s actually somewhat interesting on a regular basis.

This week, for example, India’s Byju bought WhiteHat Jr., another Indian edtech company, for $300 million. So what, you’re thinking, that’s just another startup deal? Yes, but it was an all-cash transaction, and White Hat Jr. was only 18 months old.

That’s enough to tell you that edtech is hot at the moment. Which makes sense: much of the world is sheltering at home with school and offices shuttered.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The COVID-19 era has provided an enormous boon to many software startups, though some more than others. Luckily for its boosters, edtech, after being neglected by VCs due to an expectation of small exits and long sales cycles thanks to red tape, is one of the sectors enjoying renewed interest from private investors and customers alike.

According to a Silicon Valley Bank (SVB) markets-focused report, edtech venture funding reached a local-maxima in Q2 2020, jumping more than 60% from the first quarter of this year to the second. On a year-over-year basis, Q2’s VC edtech results were even more impressive.

But, there’s some nuance to the data that should temper declamations that private edtech funding is forever changed.

This morning let’s peel apart the SVB data and parse through edtech funding rounds themselves from the second quarter to see what we can learn. COVID-19 is remaking the global economy as we speak, so it’s up to us to understand its evolving form.

From the top-line numbers, you’d be forgiven for thinking that edtech’s Q2 venture capital results were across-the-board impressive.

Before we dig into the results themselves, here’s the chart you need:

Powered by WPeMatico

Robinhood’s huge, two-part Series F round came partially in Q2 and partially in Q3. The app-based trading platform announced the first $280 million in early May, valuing the company at around $8.3 billion, up from a prior price tag of around $7.6 billion.

Then in July, Robinhood tacked on $320 million more at the same price, raising its valuation to around $8.6 billion.

While it has long been known that savings and investing apps and services are seeing a boom in 2020, precisely what caused investors to pour $600 million more into this already-wealthy company was less immediately evident. Recent data released by Robinhood concerning one of its revenue sources may help explain the rapid-fire capital events.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Filings from Robinhood covering the April through June period, Q2 2020, indicate that the company’s revenue from payment for order flow, a method by which a broker is paid to route customer orders through a particular group, or party rose during the period. As TechCrunch has covered, Robinhood generates a sizable portion of its revenue from such activities.

The company is hardly alone in doing so. As a new report from The Block, shared with The Exchange ahead of publication notes, Robinhood’s Q2 payment for order flow haul was impressive, but not singularly so; trading houses like E*Trade and Charles Schwab also grew their incomes from order flow routing in the period.

But Robinhood’s gains come in the wake of the firm’s promise to shake up its options trading setup after a customer took their own life. As we’ve written, there is a tension between Robinhood’s desire to limit who can access options trading, its need to grow and the incomes options-related order flow can drive for the budding fintech giant.

This morning, however, we are focusing on revenue growth over other issues (more to come on those later). Let’s dig into Robinhood’s Q2 order flow revenue numbers and see what we can learn about its run rate and current valuation.

According to The Block’s own calculations, Robinhood saw saw its total payment for order flow revenue roughly double, rising from $90.9 million in Q1 2020 to $183.3 million in Q2 2020, a 102% increase.

Powered by WPeMatico