Tennessee

Auto Added by WPeMatico

Auto Added by WPeMatico

Previously, we introduced the concept of flexible VC: structures that allow founders to access immediate risk capital while preserving exit and ownership optionality. We list here all the active flexible VCs we have identified, broken into these categories:

These investors are paid back primarily based on a percentage of revenues.

Chattanooga, TN-based Capacity Capital was launched in 2020 with a primary focus on the southeastern U.S. Jonathan Bragdon, its CEO, describes Capacity as “a team of founders-turned-funders making non-dilutive, founder-aligned investments of $50,000-$300,000 in post-startup, post-revenue businesses planning to 2x revenues in 12-24 months. Investments are typically in exchange for a capped, single-digit revenue share and a right to equity under certain circumstances.

If the company sells or raises enough capital, the investment converts into an agreed-upon percentage of equity. If the company grows without raising additional equity funding, founders redeem most of the equity right, based on a pre-agreed return amount. With a portfolio that includes food, tech and services, the fund is industry-agnostic and focused on the overlooked and underrepresented with high-margin business models.”

Jonathan sometimes refers to their investments as “micro-mezzanine” because “mezz is typically structured as a contractual periodic payment, with some equity-like upside, but subordinate to other debt … so most lenders look at it like equity. But, it is typically shorter term with fewer control mechanisms than equity (i.e., not VC). I wanted [a term for] something similar (between debt and equity) but on an extremely small scale.”

In addition to a fund, the overall Capacity organization provides direct mentorship, consulting and connects founders to a broad network of talent, diverse forms of capital and existing resources focused on the post-startup stage of growth. The founders, LPs and venture partners have a long history in local startup ecosystems in the Southeast including LaunchTN, The Company Lab, CO.STARTERS and several other regional funds and resources.

Greater Colorado Venture Fund (GCVF) is a $17 million seed fund that invests in high-growth startups in rural Colorado using equity and flexible VC structuring.

A typical GCVF flexible VC investment is $100,000-$250,000 for up to 10% ownership, of which 9% is redeemable, with a sub-10% revenue share and 12-month-plus holiday period. GCVF specializes in providing critical support to founders based in small communities, while connecting them to an unfair network well-beyond their small-town headquarters.

GCVF is pioneering the future of venture capital and high-growth startups for all small communities. With Colorado as an ideal pilot community, the GCVF team (which includes Jamie Finney, a co-author of this article) has helped grow multiple staple initiatives in the rural Colorado startup ecosystem, including West Slope Startup Week, Telluride Venture Accelerator, Startup Colorado, Energize Colorado Gap Fund and the Greater Colorado Pitch Series.

Recognizing the need for creative investment structures in their Colorado market, they co-founded the Alternative Capital Summit, creating the first community of flexible VCs and alternative startup investors.

They share their learnings on flexible VC and pioneering rural startup ecosystems on the GCVF blog.

Powered by WPeMatico

Vault, an at-home healthcare practice specializing in men’s medicine has announced the raise of $30 million in funding from Tiger Capital Group, Declaration Capital and Redesign Health to reach more potential patients and expand to more areas beyond New York, Florida, Tennessee and Texas, where it currently offers treatments.

Founder and CEO Jason Feldman, who formerly headed Amazon’s Prime Video Direct and Global Innovation teams before launching Vault last summer, told TechCrunch his startup aims to bring specialized medicine into men’s homes to give them “a better body, better sex and a better brain.”

He tells TechCrunch he started the company after noticing how many of his male friends seemed embarrassed about medical conditions or simply didn’t know they could do something about it.

Vault operates on the assumption men face certain barriers to going to the doctor for things like hormonal imbalance and erectile dysfunction. The startup tries to remove these barriers by making it easy to book at-home appointments and get a work-up with a nurse practitioner.

“I want to de-stigmatize men’s health.” Feldman told TechCrunch. “You tell a guy to go see the doctor about his heart health and he likely won’t but you tell him you’ll bring him a doctor to help his penis and it’s a different story.”

Like many new concierge medical services that have popped up in the last few years, Vault does not take insurance, instead signing patients up via membership for $133 to $300 per month, depending on the type of service you sign up for. Compare that to Forward, which caters to both men and women and offers unlimited in-office visits and testing for $149/month or Roman, a men’s “digital clinic,” which offers free online evaluations, $15 doctor’s visits and prescription medications for similar services to Vault like erectile dysfunction, hair loss and testosterone support — although Roman requires patients see a physical doctor of their choosing within the last three years before they’re able to get prescriptions via digital services.

But Feldman doesn’t think his startup is anything like what’s out there right now, claiming it as the first national men’s healthcare provider. Vault offers specialty packages like testosterone therapy or the “sex kit” for an increased sex drive or stronger erections, something that sometimes diminishes as men age.

So far, Feldman has signed up over 500 medical practitioners to come to various home locations and has hired a chief medical officer to ensure medical standards are being met. He now plans to use the new funding to open up operations in 42 cities across the U.S. and work on spreading the word to all men nationwide that Vault is here for them.

Powered by WPeMatico

America’s mayors have spent the past nine months tripping over each other to curry favor with Amazon.com in its high-profile search for a second headquarters.

More quietly, however, a similar story has been playing out in startup-land. Many of the most valuable venture-backed companies are venturing outside their high-cost headquarters and setting up secondary hubs in smaller cities.

Where are they going? Nashville is pretty popular. So is Phoenix. Portland and Raleigh also are seeing some jobs. A number of companies also have a high number of remote offerings, seeking candidates with coveted skills who don’t want to relocate.

Those are some of the findings from a Crunchbase News analysis of the geographic hiring practices of U.S. unicorns. Since most of these companies are based in high-cost locations, like the San Francisco Bay Area, Boston and New York, we were looking to see if there is a pattern of setting up offices in smaller, cheaper cities. (For more on survey technique, see Methodology section below.)

Here is a look at some of the hotspots.

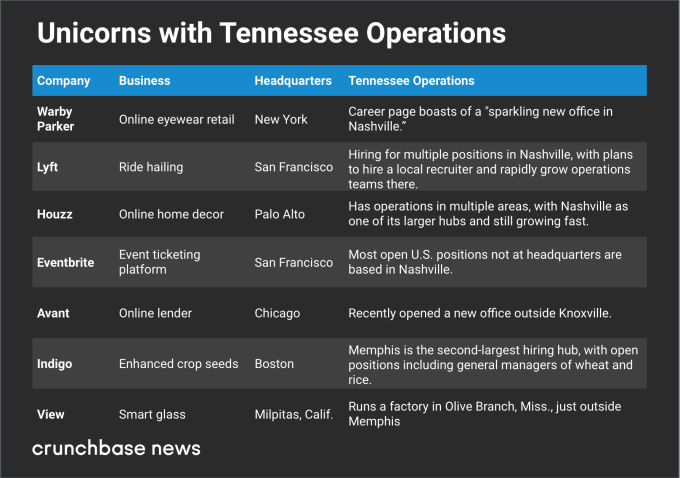

One surprise finding was the prominence of Nashville among secondary locations for startup offices.

We found at least four unicorns scaling up Nashville offices, plus another three with growing operations in or around other Tennessee cities. Here are some of the Tennessee-loving startups:

When we referred to Nashville’s popularity with unicorns as surprising, that was largely because the city isn’t known as a major hub for tech startups or venture funding. That said, it has a lot of attributes that make for a practical and desirable location for a secondary office.

Nashville’s attractions include high quality of life ratings, a growing population and economy, mild climate and lots of live music. Home prices and overall cost of living are also still far below Silicon Valley and New York, even though the Nashville real estate market has been on a tear for the past several years. An added perk for workers: Tennessee has no income tax on wages.

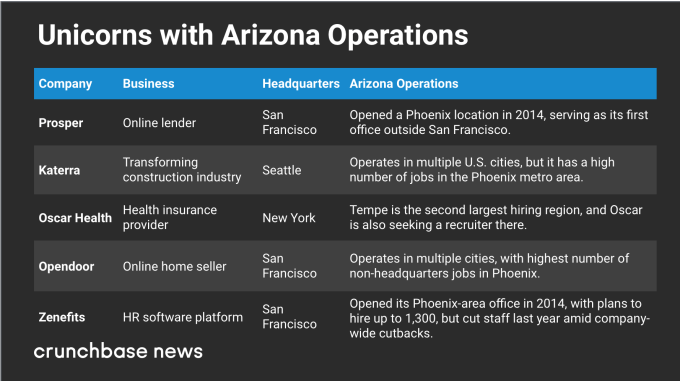

Phoenix is another popular pick for startup offices, particularly West Coast companies seeking a lower-cost hub for customer service and other operations that require a large staff.

In the chart below, we look at five unicorns with significant staffing in the desert city:

Affordability, ease of expansion and a large employable population look like big factors in Phoenix’s appeal. Homes and overall cost of living are a lot cheaper than the big coastal cities. And there’s plenty of room to sprawl.

One article about a new office opening also cited low job turnover rates as an attractive Phoenix-area attribute, which is an interesting notion. Startup hubs like San Francisco and New York see a lot of job-hopping, particularly for people with in-demand skill sets. Scaling companies may be looking for people who measure their job tenure in years rather than months.

Nashville and Phoenix aren’t the only hotspots for unicorns setting up secondary offices. Many other cities are also seeing some scaling startup activity.

Let’s start with North Carolina. The Research Triangle region is known for having a lot of STEM grads, so it makes sense that deep tech companies headquartered elsewhere might still want a local base. One such company is cybersecurity unicorn Tanium, which has a lot of technical job openings in the area. Another is Docker, developer of software containerization technology, which has open positions in Raleigh.

The Orlando metro area stood out mostly due to Robinhood, the zero-fee stock and crypto trading platform that recently hit the $5 billion valuation mark. The Silicon Valley-based company has a significant number of open positions in Lake Mary, an Orlando suburb, including HR and compliance jobs.

Portland, meanwhile, just drew another crypto-loving unicorn, digital currency transaction platform Coinbase. The San Francisco-based company recently opened an office in the Oregon city and is currently in hiring mode.

But you don’t have to be anywhere in particular to score jobs at many fast-growing startups. A lot of unicorns have a high number of remote positions, including specialized technical roles that may be hard to fill locally.

GitHub, which makes tools developers can use to collaborate remotely on projects, does a particularly good job of practicing what it codes. A notable number of engineering jobs open at the San Francisco-based company are available to remote workers, and other departments also have some openings for telecommuters.

Others with a smattering of remote openings include Silicon Valley-based cybersecurity provider CrowdStrike, enterprise software developer Apttus and also Docker.

Of course, not every unicorn is opening large secondary offices. Many prefer to keep staff closer to home base, seeking to lure employees with chic workplaces and lavish perks. Other companies find that when they do expand, it makes strategic sense to go to another high-cost location.

Still, the secondary hub phenomenon may offer a partial antidote to complaints that a few regions are hogging too much of the venture capital pie. While unicorns still overwhelmingly headquarter in a handful of cities, at least they’re spreading their wings and providing more jobs in other places, too.

For this analysis, we were looking at U.S. unicorns with secondary offices in other North American cities. We began with a list of 125 U.S.-based companies and looked at open positions advertised on their websites, focusing on job location.

We excluded job offerings related to representing a local market. For instance, a San Francisco company seeking a sales rep in Chicago to sell to Chicago customers doesn’t count. Instead, we looked for openings for team members handling core operations, including engineering, finances and company-wide customer support. We also excluded secondary offices outside of North America.

Additionally, we were looking principally for companies expanding into lower-cost areas. In many cases, we did see companies strategically adding staff in other high-cost locations, such as New York and Silicon Valley.

A final note pertains to Austin, Texas. We did see several unicorns based elsewhere with job openings in Austin. However, we did not include the city in the sections above because Austin, although a lower-cost location than Silicon Valley, may also be characterized as a large, mature technology and startup hub in its own right.

Powered by WPeMatico

The American South may not be the first region that comes to mind when you hear the phrase “hotbed of tech entrepreneurship,” but, slightly misguided perceptions aside, it’s home to a diverse and growing collection of startups.

Here, we’re going to take a deep dive into the startup funding data for the region.

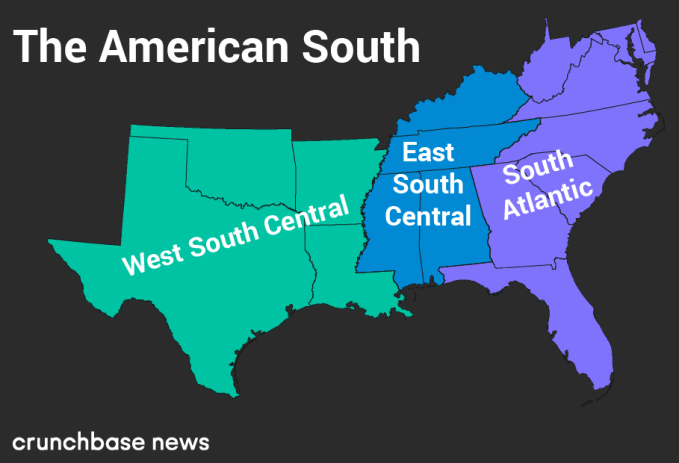

Just like it’s a common pastime for many city dwellers to argue about the precise boundaries of neighborhoods, there’s often some disagreement about the exact contours of the U.S.’s various regions. To quash rabble-rousing from the get-go, we’re using the U.S. Census Bureau’s definition of “the South” on its official map of the United States. Below, we display a map of the states we’re going to look at today.

Much like barbecue, the South is not a monolithic concept. So to incorporate some regional flavor into the following analysis, we’re also going to use the same regional divisions that the U.S. Census Bureau uses.

By doing this, we’ll be able to get a better idea of the relative contribution states from each sub-region make to startup activity in the South overall.

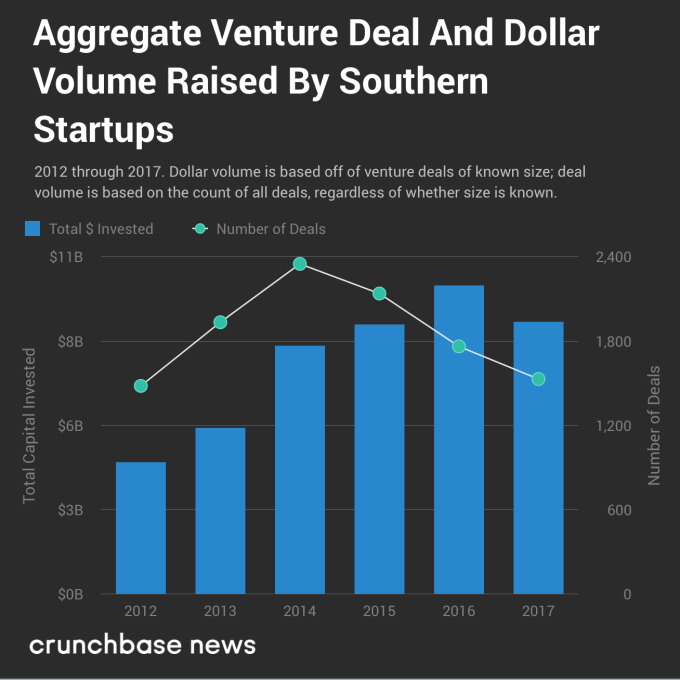

As is the case with most of the country, the South appears to be experiencing a shift in startup funding as we move toward the latter half of a bull run in entrepreneurial activity. The chart below shows a divergence in overall deal and dollar volume over time.

Much like in the rest of the U.S., reported deal and dollar volume are heading in different directions. Part of this may be due to reporting delays — it can sometimes take a few years for seed and early-stage rounds to get added to databases like Crunchbase’s . Nonetheless, there is a slow and generally upward creep in round sizes at most stages of funding. And that’s not just a Southern thing; it’s a country-wide trend.

Let’s disaggregate these figures a bit. We’ll start with deal counts and move on to dollar volume from there.

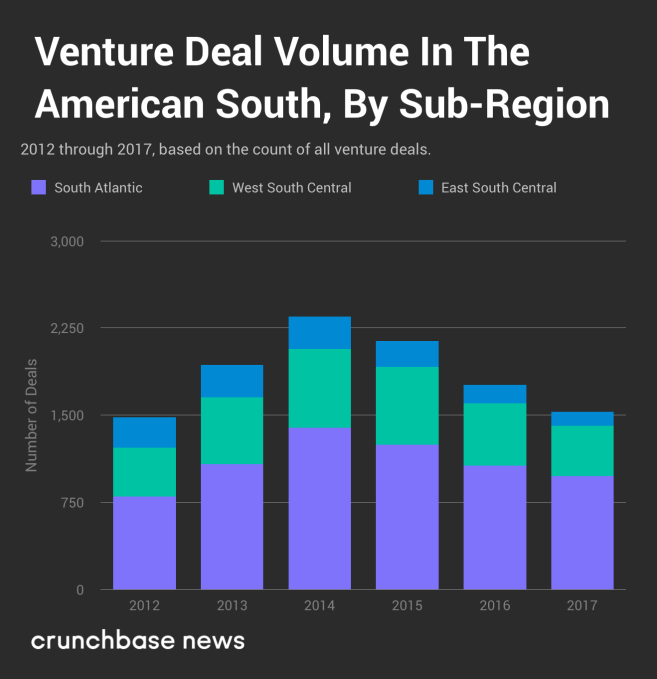

In the chart below, you’ll see venture deal volume broken out by sub-region.

Over the past several years, reported venture deal volume has been on the downswing. From a local maximum in 2014 through the end of 2017, it’s down almost 35 percent overall. But that’s not the whole picture. The relative share of deal volume has changed, as well.

Although it’s not immediately clear just by looking at the chart above, startups in the South Atlantic sub-region have accounted for an increasingly large share of the funding rounds. For example, in 2012, South Atlantic startups attracted 54 percent of the deal volume. In 2017, that grows to 64 percent. Startups in the West South Central sub-region have pretty consistently pulled in between 28 and 30 percent of the deals, so where’s the loss coming from? Startups headquartered in Kentucky, Tennessee, Mississippi and Alabama pulled in just 8 percent of deals in 2017, compared to 18 percent in 2012.

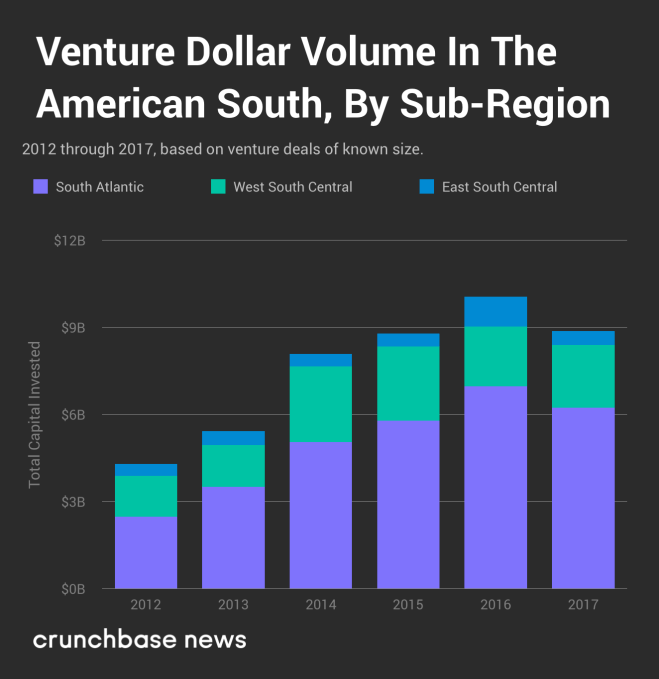

It’s a similar story with dollar volume.

In general, dollar volume follows the same pattern, albeit with a bit more variability. Regardless, startups in the South Atlantic sub-region are hoovering up an ever-larger share of venture dollars, and there’s little to indicate that trend will reverse itself any time soon.

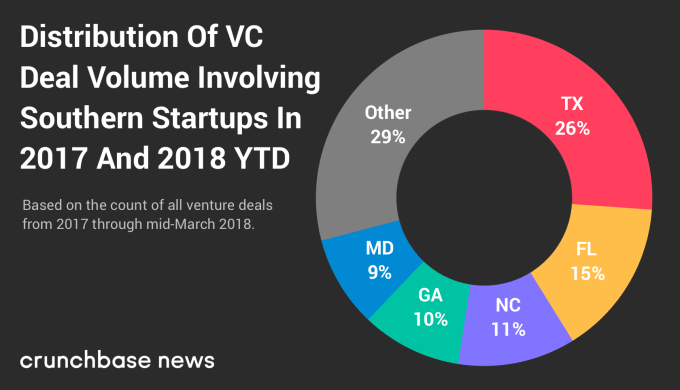

Let’s see which states accounted for most of the deal volume. The chart below shows the geographic distribution of deal-making activity by startups in each Southern state from the beginning of 2017 through time of writing. It should come as no surprise that much of the activity is concentrated in states with higher populations.

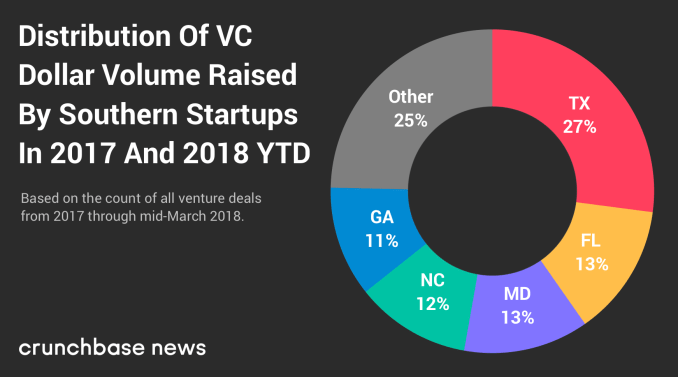

And here’s the distribution of dollar volume among southern states.

Despite some variation in which states are at the top of the ranks, the share of deal and dollar volume raised by startups in the top three states is remarkably similar, coming in at between 52 and 53 percent for both metrics.

We started by looking at the South as a whole and then drilled into its sub regions and states. But there’s one layer deeper we can go here, and that’s to rank the top startup cities in the South.

In the interest of keeping our rankings fresh and timely, we’re covering activity from the past 15 months or so, from the start of 2017 through mid-March 2018. But before highlighting some of the more notable hubs, let’s take a look at the numbers.

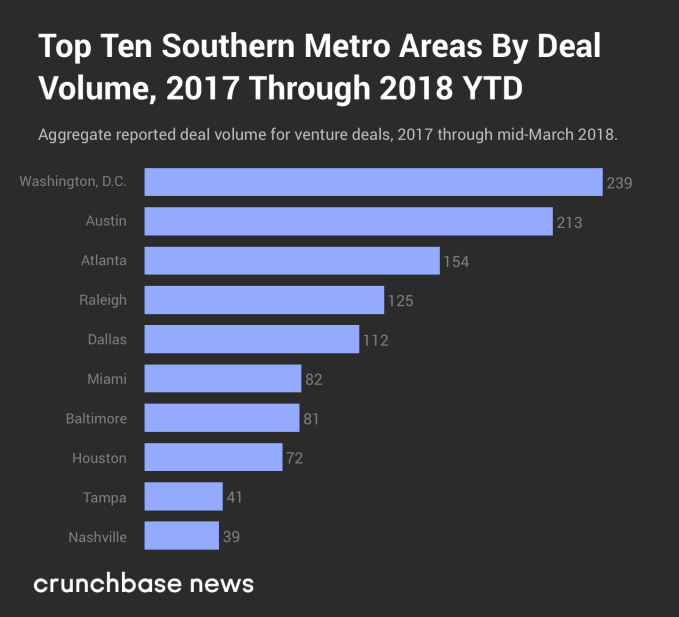

In the chart below, you’ll find the top 10 metropolitan areas where Southern startups closed the most funding rounds.

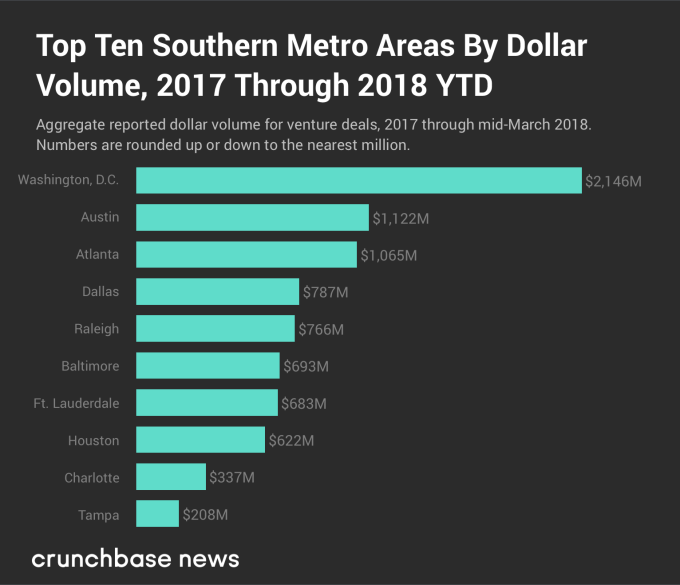

The chart below shows reported dollar volume over the same period of time.

Much like we saw at the state level, the top five startup cities — ranked by both deal and dollar volume — are the same, although there’s some variation between where each one ranks. In order, the D.C., Austin and Atlanta metro areas rank in the top three for each metric, while Dallas and Raleigh, NC switch off between fourth and fifth place.

To be frank, Washington, D.C.’s top-shelf ranking was a bit of a surprise. It may be the fact that Austin, TX plays host to South By Southwest, a somewhat more relaxed culture and/or a preponderance of excellent breakfast taco and barbecue joints, but to many — ourselves included — the city feels like it would have a more active startup scene than the nation’s capital. But that’s not exactly the case. The D.C. metro area had more venture deal and dollar volume than Austin for seven out of the last 10 years, and startups based in the nation’s capital have raised more than twice as much money so far in 2018.

D.C.-area startups have recently raised some notable rounds. Just a couple of weeks prior to the time of writing, Viela Bio raised $250 million in a Series A round (in late February 2018) to continue funding research and testing of its treatments for severe inflammation and autoimmune diseases. And on the later-stage end of things, education technology company Everfi raised $190 million in a Series D round that had participation from Amazon founder and CEO Jeff Bezos, former Alphabet executive Eric Schmidt and Medium CEO Ev Williams. Other D.C. companies, including Mapbox, Upside.com, Afiniti and ThreatQuotient, have all raised late-stage rounds within the past 15 months.

Startup ecosystems in Southern cities may pale in comparison to places like New York and San Francisco, but it wouldn’t be wise to discount the region entirely. A large number of interesting companies call the lower half of the Lower 48 home, and as the cost of living continues to rise on the east and west coasts, don’t be surprised if many current and would-be founders opt to stay down home in the South.

Powered by WPeMatico