Tencent

Auto Added by WPeMatico

Auto Added by WPeMatico

Southeast Asian tech companies are drawing the attention of investors around the world. In 2020, startups in the region raised over $8.2 billion, about four times more than they did in 2015. This trend continued in 2021, with regional M&A hitting a record high of $124.8 billion in the first half of 2021, up 83% from a year earlier.

This begs the question: Who exactly is investing in Southeast Asia?

Let’s explore the three key types of investors pouring money into and driving the growth of Southeast Asia’s tech ecosystem.

Over 229 family offices have been registered in Singapore since 2020, with total assets under management of an estimated $20 billion.

Southeast Asia has become an attractive market for U.S. and Chinese tech firms. Internet penetration here stands at 70%, higher than the global average, and digital adoption in the region remains nascent — it wasn’t until the pandemic that adoption of digital services such as e-wallets and online shopping took off.

China’s tech giants Tencent and Alibaba were among the first to support early e-commerce growth in Southeast Asia with investments in Sea Limited and Lazada, and have since expanded their footprint into other internet verticals. Alibaba has backed Akulaku, M-Pay (eMonkey), DANA, Wave Money and Mynt (GCash), while Tencent has invested in Voyager Innovations (PayMaya), SHAREit, iflix, Ookbee and Sanook.

U.S. tech firms have also recently entered the scene. In June 2020, Gojek closed a $3 billion Series F round from Google, Facebook, Tencent and Visa. Google, together with Singapore’s Temasek Holdings, invested some $350 million in Tokopedia in October. Meanwhile, Microsoft invested an undisclosed amount in Grab in 2018 and has invested $100 million in Indonesian e-commerce firm Bukalapak.

In Q1 2021, Southeast Asian startups raised $6 billion, according to DealStreetAsia, positioning 2021 as another record year for VC investment in the region.

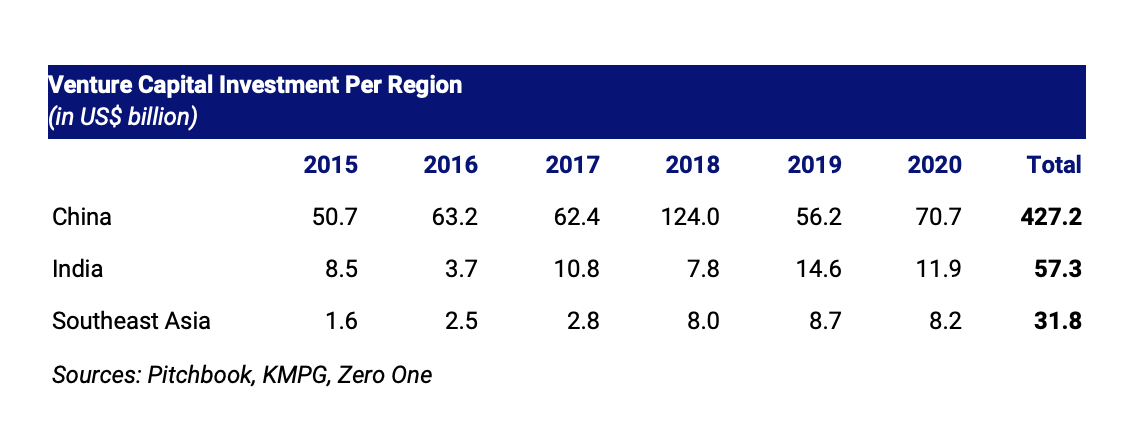

The region is also rising in prominence as a destination for investment capital relative to the rest of Asia. Regional VC investment grew 5.2 times to $8.2 billion in 2020 from $1.6 billion in 2015, as we can see in the table below.

Image Credits: Jungle VC

Southeast Asia also has many opportunities for VC investment relative to its market size. From 2015 to 2020, China saw VC investment of nearly $300 per person; for Southeast Asia — despite a recent investment boom — this metric sits at just $47.50 per person, or just a sixth of that in China. This implies a substantial opportunity for investments to develop the region’s digital economy.

The region’s rising population and growth prospects are higher due to China’s population growth challenges, alongside the latter’s higher digital economy market saturation and maturity.

Powered by WPeMatico

Hello and welcome back to TechCrunch’s China roundup, a digest of recent events shaping the Chinese tech landscape and what they mean to people in the rest of the world.

This week, the gaming industry again became a target of Beijing, which imposed arguably the world’s strictest limits on underage players. On the other hand, China’s tech titans are hastily answering Beijing’s call for them to take on more social responsibilities and take a break from unfettered expansion.

China dropped a bombshell on the country’s young gamers. As of September 1, users under the age of 18 are limited to only one hour of online gaming time: on Fridays, Saturdays and Sundays between 8-9 p.m.

The stringent rule adds to already tightening gaming policies for minors, as the government blames video games for causing myopia, as well as deteriorating mental and physical health. Remember China recently announced a suite of restrictions on after-school tutoring? The joke going around is that working parents will have an even harder time keeping their kids occupied.

A few aspects of the new regulation are worth unpacking. For one, the new rule was instituted by the National Press and Publication Administration (NPPA), the regulatory body that approves gaming titles in China and that in 2019 froze the approval process for nine months, which led to plunges in gaming stocks like Tencent.

It’s curious that the directive on playtime came from the NPPA, which reviews gaming content and issues publishing licenses. Like other industries in China, video games are subject to regulations by multiple authorities: NPPA; the Cyberspace Administration of China (CAC), the country’s top internet watchdog; and the Ministry of Industry and Information Technology, which oversees the country’s industrial standards and telecommunications infrastructure.

As analysts long observe, the mighty CAC, which sits under the Central Cyberspace Affairs Commission chaired by President Xi Jinping, has run into “bureaucratic struggles” with other ministries unwilling to relinquish power. This may well be the case for regulating the lucrative gaming industry.

For Tencent and other major gaming companies, the impact of the new rule on their balance sheet may be trifling. Following the news, several listed Chinese gaming firms, including NetEase and 37 Games, hurried to announce that underage players made up less than 1% of their gaming revenues.

Tencent saw the change coming and disclosed in its Q2 earnings that “under-16-year-olds accounted for only 2.6% of its China-based grossing receipts for games and under-12-year-olds accounted for just 0.3%.”

These numbers may not reflect the reality, as minors have long found ways around gaming restrictions, such as using an adult’s ID for user registration (just as the previous generation borrowed IDs from adult friends to sneak into internet cafes). Tencent and other gaming firms have vowed to clamp down on these workarounds, forcing kids to seek even more sophisticated tricks, including using VPNs to access foreign versions of gaming titles. The cat and mouse game continues.

While China curtails the power of its tech behemoths, it has also pressured them to take on more social responsibilities, which include respecting the worker’s rights in the gig economy.

Last week, the Supreme People’s Court of China declared the “996” schedule, working 9 a.m. to 9 p.m. six days a week, illegal. The declaration followed years of worker resistance against the tech industry’s burnout culture, which has manifested in actions like a GitHub project listing companies practicing “996.”

Meanwhile, hardworking and compliant employees have often been cited as a competitive advantage of China’s tech industry. It’s in part why some Silicon Valley companies, especially those run by people familiar with China, often set up branches in the country to tap its pool of tech talent.

The days when overworking is glorified and tolerated seem to be drawing to an end. Both ByteDance and its short video rival Kuaishou recently scrapped their weekend overtime policies.

Similarly, Meituan announced that it will introduce compulsory break time for its food delivery riders. The on-demand services giant has been slammed for “inhumane” algorithms that force riders into brutal hours or dangerous driving.

In groundbreaking moves, ride-hailing giant Didi and Alibaba’s e-commerce rival JD.com have set up unions for their staff, though it’s still unclear what tangible impact the organizations will have on safeguarding employee rights.

Tencent and Alibaba have also acted. On August 17, President Xi Jinping delivered a speech calling for “common prosperity,” which caught widespread attention from the country’s ultra-rich.

“As China marches towards its second centenary goal, the focus of promoting people’s well-being should be put on boosting common prosperity to strengthen the foundation for the Party’s long-term governance.”

This week, both Tencent and Alibaba pledged to invest 100 billion yuan ($15.5 billion) in support of “common prosperity.” The purposes of their funds are similar and align neatly with Beijing’s national development goals, from growing the rural economy to improving the healthcare system.

Powered by WPeMatico

China’s National Press and Publication Administration has released a notice imposing limits on online gaming for minors. On September 1st, video game companies will have to restrict gaming time to three hours a week — from 8 PM to 9 PM on Friday, Saturday and Sunday.

With this new set of restrictions, Chinese authorities want to tackle addition to online games. According to the National Press and Publication Administration, online gaming has an impact on both the physical and mental health of minors.

In order to implement those time limits, game companies will have to leverage a real-name-based registration system. In 2018, Tencent started using this system to limit play time on Honor of Kings, a widely popular mobile game.

Back then, limits weren’t as strict, though, as children up to aged 12 could play one hour per day, and up to two hours per day for children between 13 and 18. At the time, authorities were concerned about worsening myopia among minors.

During the signup flow, users must go through an ID verification system, which means that you can only have one account associated with your real name. Regulators will regularly check whether gaming companies comply with local regulation.

It’s going to be interesting to see how the new rules affect video games as a whole. Online gaming is mentioned specifically, which could mean that solo games won’t be restricted going forward. Similarly, it’s unclear whether console games and foreign games will have to implement the new real-name-based registration system.

Some young gamers will also be tempted to circumvent the restrictions by signing up on a foreign server. It’s also worth noting that adult players will still be able to play 24/7.

Following the news, Tencent issued a statement. “Tencent expressed its strong support and will make every effort to implement the relevant requirements of the Notice as soon as possible,” the company says.

As Bloomberg noticed, NetEase shares are currently down 8% compared to yesterday’s closing price. NetEase is another popular Chinese game development company and its activities aren’t as diversified as Tencent’s activities.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here. I also tweet.

Today’s show was good fun to put together. Here’s what we got to:

Woo! And that’s the start to the week. Hugs from here, and we’ll chat you on Wednesday!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Less than three months after announcing a $300 million Series E, Brazilian proptech QuintoAndar has raised an additional $120 million.

New investors Greenoaks Capital and China’s Tencent co-led the round, which included participation from some existing backers as well. São Paulo-based QuintoAndar is now valued at $5.1 billion, up from $4 billion at the time of its last raise in late May. With the extension, the startup has now raised more than $700 million since its 2013 inception. Ribbit Capital led the first tranche of its Series E.

QuintoAndar describes itself as an “end-to-end solution for long-term rentals” that, among other things, connects potential tenants to landlords and vice versa. Last year, it also expanded into connecting home buyers to sellers. Its long-term plan is to evolve into a one-stop real estate shop that also offers mortgage, title insurance and escrow services.

To that end, earlier this month, the startup acquired Atta Franchising, a 7-year-old São Paulo-based independent real estate mortgage broker. Specifically, acquiring Atta is designed to speed up its ability to offer mortgage services to its users. QuintoAndar also plans to explore the possibility of offering a product to perform standalone transactions outside of its marketplace in partnership with other brokers, according to CEO and co-founder Gabriel Braga.

This year, QuintoAndar expanded operations into 14 new cities in Brazil. Eventually, QuintoAndar plans to enter the Mexican market as its first expansion outside of its home country, but it has not yet set a date for that step. Today, the company has more than 120,000 rentals under management and about 10,000 new rentals per month. Its rental platform is live in 40 cities across Brazil, while its home-buying marketplace is live in four (São Paulo, Rio de Janeiro, Belo Horizonte and Porto Alegre) and seeing more than 10,000 sales in annualized terms.

QuintoAndar, he said, is open to acquiring more companies that it believes can either help it accelerate in a particular way or add something it had not yet thought about.

“We’re receptive to the idea but our core strategy is to focus on organic growth and our own innovation and accelerate that,” Braga said.

The Series E was oversubscribed with investors who got in and “some who could not join,” according to Braga.

Greenoaks and Tencent, he said, couldn’t participate because of “timing issues.”

“We kept talking and they came back to us after the round, and wanted to be involved so we found a way to have them on board,” Braga said. “We did not need the money. But we have been constantly overachieving on the forecast that we shared with our investors. And that’s part of the reason why we had this extension.”

Greenoaks’ long-term time horizon was appealing because the firm’s investment was designed to be “perpetual capital with no predefined time frame,” Braga said.

“We’re doing our best to build an enduring company that will be around for many, many years, so it’s good to have investors who share that vision and are technically aligned,” he added.

Greenoaks partner Neil Shah said his firm believes that what QuintoAndar is building will “fundamentally reshape real estate transactions, enhancing transparency, expanding options for Brazilians seeking housing, dramatically simplifying the experience for landlords and driving increased investment into real estate across the country.” He also believes there is big potential for the company to take its offering to other parts of Latin America.

“We look forward to being partners for decades to come,” he added.

Tencent’s experience in China is something QuintoAndar also finds valuable.

“We believe we can learn a lot from them and other Chinese companies doing interesting stuff there,” Braga said.

QuintoAndar isn’t the only Brazilian proptech firm raising big money: In March, São Paulo digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. Then, about one month later, it revealed a $100 million extension that valued the company at $2.9 billion.

Powered by WPeMatico

The dollars keep flowing into Latin America.

Today, Argentine personal finance management app Ualá announced it has raised $350 million in a Series D round at a post-money valuation of $2.45 billion.

SoftBank Latin America Fund and affiliates of China-based Tencent co-led the round, which included participation from a slew of existing backers, including funds managed by Soros Fund Management LLC, funds managed by affiliates of Goldman Sachs Asset Management, Ribbit Capital, Greyhound Capital, Monashees and Endeavor Catalyst. New funds, such as D1 Capital Partners and 166 2nd, also put money in the round in addition to angel investors such as Jacqueline Reses and Isaac Lee.

The round is believed to be the largest private raise ever by an Argentinian company and brings Ualá’s total raised to $544 million since its 2017 inception.

Founder and CEO Pierpaolo Barbieri, a Buenos Aires native and Harvard University graduate, has said his ambition was to create a platform that would bring all financial services into one app linked to one card.

Today, Ualá says it has developed “a complete financial ecosystem,” including universal accounts, a global Mastercard card, bill payment options, investment products, personal loans, installments (BNPL) and insurance. It has also launched merchant acquiring, Ualá Bis, a solution for entrepreneurs and merchants that allows selling through a payment link or mobile point-of-sales (mPOS).

The startup has issued more than 3.5 million cards in its home country and in Mexico, where it launched operations last year. The company claims that more than 22% of 18 to 25-year-olds in Argentina have a Ualá card. At the time of its Series C raise in November 2019, it had issued 1.3 million cards.

Image Credits: Ualá

Over 1 million users invest in the mutual fund available on the Ualá app, which the company claims is the second largest mutual fund in Argentina in number of participants. The company, which has aimed to provide more financial transparency and inclusion in the region, says that 65% of its users had no credit history prior to downloading the app.

Ualá plans to use its new capital to continue expanding within Latin America, develop new business verticals and do some hiring, with the plan of having 1,500 employees by year’s end. It currently has more than 1,000 employees.

“We are most impressed by Ualá’s ambition and execution. Our investment will propel the next stage of their vision, furthering a regional ecosystem that can make financial services more accessible and transparent across LatAm,” said Marcelo Claure, CEO of SoftBank Group International and COO of SoftBank Group, in a written statement.

Powered by WPeMatico

China’s technology scene has been in the news for all the wrong reasons in recent months. In the wake of the scuttling of Ant Group’s IPO, the Chinese government has gone on a regulatory offensive against a host of technology companies. Edtech got hit. On-demand companies took incoming fire. Ride-hailing? Check. Gaming? You bet.

The result of the government fusillade against some of the best-known companies in China was falling share prices. The damage topped $1 trillion among just public Chinese companies listed abroad.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

What about startups in sectors that were reformed overnight? If their public comps are any indication, even more wealth was deleted in the recent wave of crackdowns.

The Exchange was curious about the impact of the Chinese government’s actions on the venture capital market. The Chinese startup economy has produced a number of world-leading companies. Tencent and Alibaba, yes, and even Baidu have become well-known for a reason. Could regulatory changes shake up the venture model that helped grow the country’s largest tech concerns?

After we checked in on the same question this Monday, SoftBank provided a partial answer, noting yesterday that it is pausing investments in China. The Japanese teleco, conglomerate and investing powerhouse has been deploying capital at a rapid pace in recent weeks. That will slow, at least in China. Here’s the WSJ:

The regulatory initiative in China has become so unpredictable and widespread that SoftBank and its funds are planning to hold off on investing much more there until the risks become clearer, [SoftBank CEO Masayoshi Son] said at an earnings press conference in Tokyo.

Is SoftBank early to its decision to shake up its investing strategy, missing Chinese deals for some time? Or is it late? We secured data from PitchBook and Traxcn that paints a somewhat surprising picture of venture capital activity at least thus far in Q3 2021.

But first, a reminder of how well China’s venture capital market was performing as 2020 eased its way into 2021.

But first, a reminder of how well China’s venture capital market was performing as 2020 eased its way into 2021.

China had a reasonably good Q2 2021 despite the turmoil.

Sure, funding flowing into Chinese startups was down 18% compared to Q4 2020, per CB Insights, but that quarter had recorded an all-time high of $27.7 billion. With $22.8 billion raised, Q2 2021 still did better than every other quarter since Q2 2016 with the exception of Q2 2018, Q4 2020 and Q1 2021. Indeed, the ecosystem had started to cool down in late 2018 before picking up pace again at the end of 2020.

However, that’s only one way to look at the numbers. If you compare recent Chinese venture results with other regions, it underperformed. During Q2 2021, U.S. funding reached a new high of $70.4 billion, with places like Latin America, Canada and India also establishing new records.

This also means that China lost ground as to its share of global startup deal-making, and the same goes for unicorn creation. According to Tech Buzz China’s summary of CB Insights data, the U.S. accounted for 132 unicorn births between January 1 and June 16, 2021, compared with just three in China.

Slightly falling quarterly venture capital totals and a notable decline in unicorn formation does not a startup winter make. So let’s look at what’s happened more recently.

The thesis that there would be an instantly obvious slowdown in Chinese venture capital activity is not supported by the data we secured.

Powered by WPeMatico

The Chinese government’s crackdown on its domestic technology industry continues, with Tencent under fresh pressure despite the company’s efforts to follow changing regulatory expectations.

News broke over the weekend that Beijing filed a civil suit against Tencent “over claims its messaging-app WeChat’s Youth Mode does not comply with laws protecting minors,” per the BBC. And NetEase, a major Chinese technology company, will delay the IPO of its music arm in Hong Kong. Why? Uncertain regulations, per Reuters.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The latest spate of bad news for China’s technology industry follows a raft of regulatory changes and actions by the nation’s government that have deleted an enormous quantity of equity value. After a period of relatively light-touch regulatory oversight, domestic Chinese technology companies have found themselves on defense after the Chinese Communist Party (CCP) came after their market power in antitrust terms — and some of their business operations from other perspectives. Sectors hit the hardest include fintech and edtech.

Gaming is also in the CCP crosshairs.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

NetEase stock traded around $110 per share in late July. It’s now worth around $90 per share after expectations shifted in light of the gaming news, indicating that investors are concerned about its future performance. Tencent’s Hong Kong-listed stock has also fallen, from HK$775.50 to HK$461.60 this morning.

Tencent tried to head off regulatory pressure, announcing changes to how it controls access to its games after the government’s shot across the bow. The effort doesn’t appear to have worked. That Tencent is being sued by the government despite its publicly announced changes implies that its proposed curbs to youth gaming were either insufficient or perhaps moot from the beginning.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and me here.

It’s going to be a busy week, with a Samsung event and a host of earnings reports that we’ll have to pay attention to. But more important there are a few stories still dominating the news cycle:

All that and we also riffed on the Siemens-Sqills deal, Cornerstone OnDemand going private and Delivery Hero buying a piece of Deliveroo.

And, for added flavor and fun, Canopy Servicing just raised a $15 million Series A, while Siga OT Solutions raised a $8.1 million Series B.

All that, and we got to talk stocks! Hugs and love from the Equity crew — chat Wednesday!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Hello and welcome back to TechCrunch’s China roundup, a digest of recent events shaping the Chinese tech landscape and what they mean to people in the rest of the world.

The question for the tech news cycle in China these days has become: Who is Beijing’s next target? Regulatory clampdowns are common in China’s tech industry but the breadth of the recent moves has been unprecedented. No major tech giant is exempted and everyone is being attacked from a slightly different angle, but Beijing’s message is clear: Tech businesses are to align themselves with the interests and objectives of Beijing.

The government’s motivation isn’t always ideological. It could lead to policies that rein in the unruly private tutoring sector in the hope of easing pressure on students and parents. Recent orders from Beijing have strictly limited after-school tutoring, though they also sparked a wave of sympathy for public school teachers who work at lucrative tutoring centers to compensate for their meager salaries.

The effects of the education crackdown are also trickling down to internet companies. For the past few years, ByteDance had been aggressively building an online education business through a hiring and acquisition spree in part to diversify an ad-based video business. Its plan seems to be in shambles as it reportedly plans to lay off staff in its education department following recent the clampdown.

The restraints are also hitting American companies. Duolingo, the language learning app, was removed from several app stores in China. While it’s not immediately clear whether the action was the result of any policy change, the government recently, along with its restraints on extra-curriculum, barred foreign curricula in schools from K-9.

It could be tricky to read the top leaders’ minds because their messages could come through various government departments or state-affiliated media outlets, carrying different weights.

This week, Tencent is in the authorities’ crosshairs. About $60 billion of its market cap was wiped after the Economic Information Daily, an economic paper supervised by China’s major state news agency Xinhua, published an article (which was taken down shortly) describing video games as “spiritual opium” and cited the major role Tencent plays in the industry. Shares of Tencent’s smaller rival NetEase were also battered.

This certainly isn’t the first time Tencent and the gaming industry overall were slammed by the government for their impact on underage players. Tencent has been working to appease the authorities by introducing protections for young players, for instance, by tightening age checks several times.

Tencent, which has a sprawling online empire of social networks, payments and music on top of games, has also promised to “do [more social] good” through its products. And following the recent op-ed from the state paper, Tencent further restricted the amount of time and money children can spend inside games. But after all, the company still depends largely on addictive game mechanics that lure players to open loot boxes.

Tencent share prices over the past six months. Image Credits: Google Finance

The other camp of tech companies feeling the heat is those dependent on machine learning algorithms to distribute content. The Propaganda Department of the Chinese Communist Party, the country’s watchdog of public expressions, along with several other government organs, issued an advisory to “strengthen the study and guidance of online algorithms and carry out oversight over algorithmic recommendations.”

The government’s goal is to assert more control over how algorithmic black boxes affect what information people receive. Shares of Kuaishou, TikTok’s archrival in China, tanked on the news. Since its blockbuster initial public offering in February, Kuaishou’s stock price has tumbled as much as 70%. Meanwhile, the Beijing-based short video firm is shuttering one of its overseas apps called Zynn, which has caused controversy over plagiarism. But its overseas user base is also rapidly growing, crystalizing in one billion monthly users worldwide recently.

The week hasn’t ended. On Friday morning, The Wall Street Journal reported that the country’s antitrust regulator is preparing to fine Meituan, China’s major food delivery platform, $1 billion for allegedly abusing its market dominance. In 2020, Meituan earned 114.8 billion yuan or $17.7 billion in revenue.

Until recently, forcing suppliers to pick sides had been a common practice in China’s e-commerce world. Alibaba did so by forbidding sellers to list on rivaling platforms, a practice that resulted in a $2.75 billion antitrust penalty in April. We will see where the government will act next as it continues to curb the power of its tech darlings.

Powered by WPeMatico