telemedicine

Auto Added by WPeMatico

Auto Added by WPeMatico

In three years Zachariah Reitano’s startup, Ro, has managed to hit a reported $1.5 billion valuation for its transformation from a company focused on treating erectile dysfunction to a telemedicine service for a range of elective and urgent care-focused treatments.

Through Rory for women’s health, Roman for men’s health and Zero for smoking cessation, Reitano and fellow co-founders Saman Rahmanian, and Rob Schutz, built a company that now treats 20 conditions, including sexual health, weight loss, dermatology, allergies and more, according to a statement from the company.

Image Credit: Zero

Ro also has a new pharmacy business, Ro Pharmacy, which is an online cash pay pharmacy offering more than 500 generic medications for just $5 per month per drug. And the company is getting into the weight loss business through a partnership with the private equity-backed healthcare company, Gelesis.

Ro’s also becoming a gateway into patient acquisition for primary care providers through Ribbon Health, and a test-case for the use of Pfizer’s Greenstone service, which provides certification that a generic drug is validated by one of the major pharmaceuticals.

The company’s $1.5 billion valuation is courtesy of a new $200 million investment from existing investors led by General Catalyst and including FirstMark Capital, Torch, SignalFire, TQ Ventures, Initialized Capital, 3L and BoxGroup. New first-time investor The Chernin Group also participated. In all, Ro has raised $376 million since it launched in 2017.

“This new investment will further our mission to become every patient’s first call. We’ll continue to invest in our vertically-integrated healthcare ecosystem, from our Collaborative Care Center to our national pharmacy operating system. This is just the beginning of Ro’s patient-centered healthcare platform.”

It’s all part of the company’s mission to provide a point of entry into the healthcare system independent of insurance qualifications.

“Telehealth companies like Ro are using technology to address long-standing healthcare disparities that have been exacerbated by COVID-19,” said Dr. Joycelyn Elders, MD, Ro Medical Advisor and Former U.S. Surgeon General. “By empowering providers to leverage their skills as efficiently and effectively as possible, Ro delivers affordable, high-quality care regardless of a patient’s location, insurance status, or physical access to physicians and pharmacies.”

Ro’s new financing is one of several forays by tech investors into reshaping the healthcare system at a time when patient care has been severely disrupted by attempts to mitigate the spread of COVID-19.

Digital medicine is assuming a central position in the healthcare world, with most consultations now occurring online. Reimbursement schemes for telemedicine have changed dramatically and investors see an opportunity to capitalize on these changes by aggressively backing the expansion plans of companies looking to bring digital healthcare directly to consumers.

That’s one of the reasons why Ro’s major competitor, Hims, is reported to be seeking access to public markets through its sale to a special purpose acquisition company for roughly $1 billion, according to Reuters.

Powered by WPeMatico

Boston-based startup Activ Surgical has raised a $15 million round of venture funding led by ARTIS Ventures, and including participation from LRVHealth, DNS Capital, GreatPoint Ventures, Tao Capital Partners and Rising Tide VC. The round will help Activ continue to develop and expand availability of its software platform, which it launched to market in May.

Activ Surgical’s ActivEdge platform uses data collected from surgical implements outfitted with sensors created by the company to collect real-time data during the actual surgical process. That data is then used to inform the development of machine learning and AI-based visualizations that can provide guidance to surgeons and surgical systems to help them reduce the occurrence of potential errors, and ultimately improve outcomes for patients.

The company’s primary aim is to bring technological innovation to the sphere of surgical vision, which still relies primarily on methods like using fluorescent dyes that date back more than 70 years. Activ wants to use computer vision to provide real-time visual insight into things that surgeons wouldn’t be able to see on their own — and ultimately to use those insights to power the next generation of both collaborative surgical robots and eventually even fully autonomous robotic surgical procedures.

ActivSight is the company’s first product in its ActivEdge platform offering, and is a small, connected imaging coddle that can be attached to existing laparoscopic and arthroscopic surgical instruments. The company is currently tracking toward getting their hardware cleared by the FDA for use by Q4 this year, and are working with eight hospital partners for pilot projects in the U.S.

The company has raised a total of $32 million in funding to date.

Powered by WPeMatico

Hims & Hers, the startup focused on providing access to elective treatments for things like hair loss, skin care and erectile disfunction and online telemedicine services, is expanding its services to include a Spanish language option, the company said.

After Mexico, the U.S. has the second-largest Spanish speaking population in the world, with an estimated 41 million U.S. residents speaking Spanish at home. The population also prefers to receive healthcare information and frequent facilities that offer resources in Spanish.

Now, with a shortage looming in primary care physicians for rural areas and inner cities and a sky-high rate of Hispanics living without any form of healthcare coverage (roughly 15.1%, according to data provided by the company), Hims & Hers is pitching its telemedicine offering as an option.

“Language, cost, and location should not be barriers to receiving quality care, which is why we are launching a Spanish offering on our telemedicine platform,” the company said in a statement.

The company’s $39 primary care consultations at its Hims and its Hers websites will be in Spanish. That will include everything from communications like the patient intake form and instructions to prepare for an online consultation along with a connection to Spanish-speaking healthcare provider.

“The reason we created Hims & Hers was to break down barriers and provide more people with access to quality and convenient care,” the company’s co-founder and chief executive, Andrew Dudum, said in a statement. “As a telemedicine company, we recognize the need and understand the importance of serving the Spanish-speaking population. We hope those seeking access to care in Spanish find our platform to be a welcoming, inclusive, quality experience.”

Powered by WPeMatico

Years from now, people will look back on the COVID-19 pandemic as a watershed moment for society and the global economy.

Wearing a mask might be as common as owning a phone; telework, telemedicine and online education will be more of a norm than a backup plan; and for the global economy, the cloud will have transformed the underlying infrastructure of businesses and entire industries.

COVID-19 is a turning point for the cloud and cloud company founders. For its computing power and as a delivery model of software, the cloud has been embraced as a solution to many challenges that businesses face during today’s economic downturn and recovery. Not only is the cloud industry more resilient than other industries, but the cloud model offers businesses a promising future in the age of social distancing and beyond.

We believe that once founders find shelter in the cloud, they’ll never go back.

Over the past decade, there’s been a massive market shift from on-premises to cloud, as 94% of enterprises use at least one cloud service today. 2020 was already a milestone year for the cloud industry, as aggregate SaaS and IaaS run-rate revenue each crossed $100 billion, and the BVP Nasdaq Emerging Cloud Index (^EMCLOUD) market cap crossed $1 trillion in early February. Yet in a matter of days, as the COVID-19 pandemic spread, fear tore through financial markets.

In early March, public markets experienced the steepest crash in history with volatility we haven’t seen since the Great Recession. The cloud index market cap dropped to ~$750 million and cloud multiples returned close to their historical averages of ~7x while the VIX volatility index spiked to the mid-80s. Both at global highs in February 2020, the ^EMCLOUD and the S&P 500 traded off by roughly 35% by mid-March. Over the next two months, though, the ^EMCLOUD recouped those losses, charging to a new all-time high on May 7.

The cloud index has continued its rise since then, and as of the close on May 11 has a market cap above $1.2 trillion and has returned to the lofty 12x forward run rate revenue multiples from 2019. Similar to Adobe in 2012, we expect many enterprises to transition over to the cloud model, and the index will continue to expand. As we predicted in this year’s State of the Cloud 2020, by 2025 we expect the cloud to penetrate 50% of enterprise software.

Powered by WPeMatico

opportunity")

Every time we realize something new about the coronavirus, it’s always worse than we thought: maybe we don’t develop immunity to it; maybe six feet of social distancing isn’t far enough; maybe the spread won’t wane in warmer weather.

Every time we realize something new about the economy, it’s equally bleak: maybe we can’t safely reopen for months (Georgia and South Carolina notwithstanding), maybe unemployment will top Great Depression levels, maybe travel won’t resume till mid-2021, maybe most of the businesses who have shuttered their doors will never return.

But like everything in life, within all of the bad, there’s usually some good too. And for businesses who have to deal with regulation, this may be an unusually good time to get what you need.

The federal government does not have to balance its budget, which is why multi-trillion dollar legislation like the CARES Act is possible. But cities and states have to produce a budget every fiscal year that at least looks balanced on paper. In good times, that leads to lots of new spending. But in bad times, it requires a painful series of cuts, tax and fee increases and tough decisions that are normally avoided by politicians at all costs. All of that creates opportunity for startups.

Local government will desperately need new sources of revenue. Figuring out what a politician is going to do isn’t that difficult: identify the choice with the least political downside and that’s almost always the answer. That’s why controversial policy issues like legalizing mobile sports betting or recreational marijuana often stall in state legislatures when the budget is flush (disclosure, we’re investors in FanDuel) . But now, lawmakers face a very different situation: to balance the budget, they will either need to enact deep spending cuts, raise fees and taxes, or find new sources of revenue. All of a sudden, legalizing gambling and drugs doesn’t seem so risky, politically or substantively.

Any company that can offer material new tax revenues can now see their product or service legalized and permitted in a fraction of the time it would normally take. Companies who can offer direct savings to government can now secure contracts and win procurements at a rapidly faster clip. A broke government is a friendly government. This is the moment to be aggressive.

It was less than a year ago when Amazon tried to build its second headquarters in New York City.

Despite strong support from Governor Andrew Cuomo and tepid support from Mayor Bill de Blasio, the project was widely derided as an unfair corporate boondoggle and Amazon was swiftly run out of town. In good economic times, voters have the luxury of focusing on issues that aren’t critical to their own day-to-day survival and politicians have the luxury of saying no to new jobs and tax revenue to try to score points with the base.

Not anymore. Startups in blue cities and states up and down both coasts have vastly more political leverage than they’ve had in years. Issues like privacy, worker classification reform and fears of AI are all about to take a back seat to pocketbook issues like jobs, crime and access to health care. Startups who can promise to retain jobs can now drive meaningful changes on policy, regulation, permitting, zoning, licensing and everything else they need to operate.

Startups that can offer solutions to living in a pandemic (digital payments, D2C, telemedicine, teleconferencing, tele-anything) will become shiny new toys that lawmakers want to be seen with. Delivery drones, autonomous cars, at home medical testing and other concepts that seem a little edgy will now become ideas that lawmakers have to seriously consider – if a new technology could potentially save lives during a pandemic, you really don’t want to be the politician who killed the idea.

Proposals to screw with startups won’t automatically become the top priority for the San Francisco Board of Supervisors. Facebook even now has a much stronger argument to lobby for Libra (no one in this climate wants to use cash if they can help it). The power dynamic just flipped on its head. But that only works if you understand it and take advantage of it.

In the continual debate over whether tech startups should ask government for permission or beg for forgiveness over the last few years, the zeitgeist has shifted significantly towards asking for permission. The tech-lash against Facebook, Google, Amazon, Apple and Twitter created regulatory headaches for virtually every tech company, even some early stage startups.

All of that just changed. Regulators and lawmakers now have far bigger things to worry about than whether an electric scooter needs a particular type of permit. And if saying no to new ideas from new companies means turning away desperately needed jobs and tax revenue, for all of the same reasons that it was politically salient for lawmakers to reclassify all California sharing economy workers as full time employees or reject Amazon’s overtures or limit the spread of homesharing, the opposite is now true.

Now you get points for creating jobs and avoiding spending cuts. Now you’re far more reticent to tell a constituent that they can’t make a few extra bucks by renting out a room (assuming anyone ever travels again). The label of job killer will start to become politically toxic, even in the most progressive wards, districts and neighborhoods in the bluest cities on each coast. The dynamic is clearly shifting back to begging for forgiveness (don’t be stupid and do things that are clearly illegal but interpreting gray areas of regulation as friendly is now a lot easier).

Unlike the financial crisis in 2008, businesses are not the culprit here. Tech companies are actually even some of the heroes of fighting the coronavirus. But most important, being punitive towards startups is no longer a clear political winner, even in the most liberal cities and states. Even if it seems counterintuitive, now is exactly the time for startups to aggressively seek policy change and regulatory relief.

Politics is about leverage. Startups now have it. They should take advantage of it before things change again.

Powered by WPeMatico

An emergency room physician for the past 12 years, Dr. Robert Mittendorff joined Norwest Venture Partners eight years ago as a healthcare investor; the firm invests in a number of healthcare startups, including Talkspace, which raised a $50 million Series D last year, and TigerConnect.

As the COVID-19 pandemic spreads, Mittendorff is spending his weekdays with portfolio companies and weekends working with Kaiser Permanente in San Francisco. While he notes that his medical colleagues are “bearing the brunt” of the pandemic by working full time, we wanted to hear from someone who has a foot in both the investing and the healthcare world right now.

In this interview, he discusses what he’s learned from both roles, how it has influenced his healthcare investments, and offers his predictions regarding which companies will fare the best in the future.

This interview has been edited for length and clarity.

TechCrunch: How did you get to where you are today?

Dr. Robert Mittendorff: So, my journey to being a venture capitalist at Norwest and investing in healthcare companies as well as an emergency physician was really a parallel set of paths that overlapped and that cross every once in a while and now usually on a daily basis.

I started off life as a biomedical engineer really focused on wanting to be on the side of innovation and on the development of technologies to help human health. I knew early on that I wanted to be on the business side [of that], but it was important for me to understand and really be deeply in touch with what it was like to be a provider.

The journey started out going to engineering school, medical school, and then business school in the middle of medical school. I trained at Stanford, which really exposed me to county hospitals, which are probably going to be the more challenging situations as the weeks go on here, and then to Kaiser Permanente. And then, of course, Stanford, I was exposed to San Francisco General and then the Santa Clara Valley Hospital. I always practice part-time following up so it’s been 12 years as an attending, practicing part-time as an emergency physician.

In the venture space I saw an opportunity to really help select entrepreneurs and markets to grow them to a higher impact state.

Powered by WPeMatico

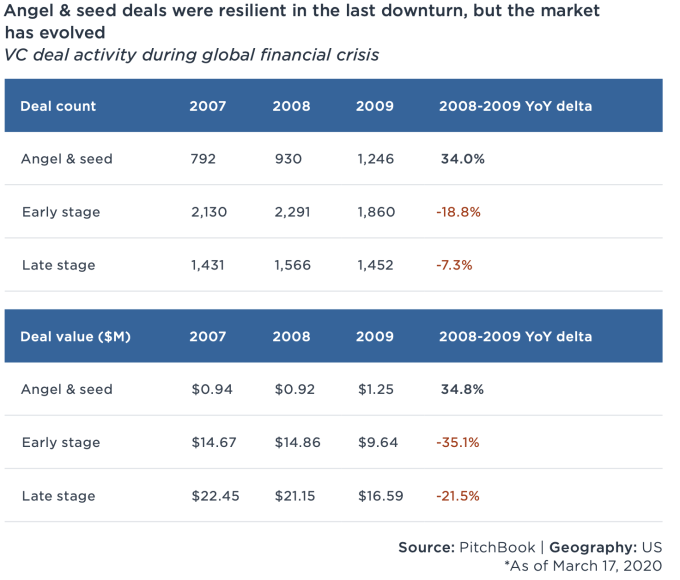

While some U.S. investors might have taken comfort from China’s rebound, we still find ourselves in the early innings of this period of uncertainty.

Some epidemiologists have estimated that COVID-19 cases will peak in April, but PitchBook reports that dealmaking was down -26% in March, compared to February’s weekly average. The decline is likely to continue in coming weeks — many of the deals that closed last month were initiated before the pandemic, and there is a lag between when deals are made and when they are announced.

However, there’s still hope. A recent report concluded that because valuations are lower and there’s less competition for deals, “the best-performing vintages tend to be those that invest at the nadir of a downturn and into the early stage of recovery.” There are countless examples from the 2008 recession, including many highly valued VC-backed businesses such as WhatsApp, Venmo, Groupon, Uber, Slack and Square. Other early-stage VCs seem to have arrived at a similar conclusion.

Also, early-stage investing seems more resilient. During the last recession, angel and seed activity increased 34% as interest in the stage boomed during a period of prolonged growth.

Image Credits: PitchBook (opens in a new window)

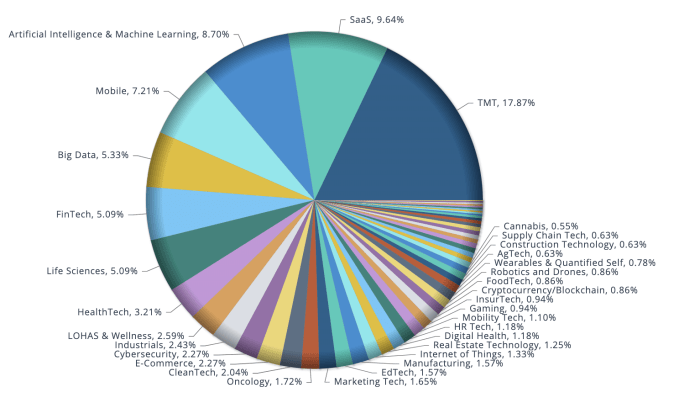

Furthermore, there is still capital to be deployed in categories that interested investors before the pandemic, which may set the new order in a post-COVID-19 world. According to data provider Preqin Ltd., VC dry powder rose for a seventh consecutive year to roughly $276 billion in 2019, and another $21 billion were raised last quarter. And looking at the deals on the early-stage side that were made year to date, especially in March, the vertical categories that garnered the most funding were enterprise SaaS, fintech, life sciences, healthcare IT, edtech and cybersecurity.

Image Credits: PitchBook

That said, if VCs have the capital to deploy and are able to overcome the obstacle of “having never met in person,” here are six investment trends that could emerge when the pandemic is over.

Powered by WPeMatico

The tech industry (and the world at large) is not experiencing temporary anxiety — the uncertainty we’re all coping with is the new normal.

Sudden shifts in behavior have made some startups targeting slow-moving, old-school industries more relevant than they could have imagined, such as those in telehealth, distance learning and remote work. Most, however are seeing massive decreases in revenue, forcing them to cut costs and even lay off teams to slash burn rates. Other startups simply won’t be here in three to six months.

Cowboy Ventures founder and managing partner Aileen Lee, who coined the term “unicorn,” says tech companies going through scenario planning need to begin thinking long-term.

“We’ve spent the last month scenario planning with our portfolio companies, and in most cases, we’ll have conversations about what these scenarios can include,” said Lee. “And when we look at the planning around those scenarios, they often don’t feel conservative enough. Most entrepreneurs are optimists, and we are, too! But it seems safer to have more conservative plans [and start expecting] that this is going to impact us for longer and be worse than we expected.”

Lee and Cowboy Ventures partner Ted Wang joined TechCrunch on Tuesday for our first episode of Extra Crunch Live, a virtual speaker series for Extra Crunch members. In a live Q&A that included questions from myself and the Extra Crunch audience, Wang and Lee covered a wide range of topics, including PPP loans, advice for business leaders around layoffs, the right time to seek funding and the right firms from which to seek that funding, how to pitch during a downturn and which sectors in particular Cowboy is interested in financing right now.

You can check out the best insights from the call, or catch up on the full conversation via the YouTube embed below.

We have several outstanding guests, including Charles Hudson, Mitch and Freada Kapor, Mark Cuban, Roelof Botha, Hunter Walk and Kirsten Green, joining us on Extra Crunch Live over the next few weeks. Sign up for Extra Crunch to get access to all of them.

Powered by WPeMatico

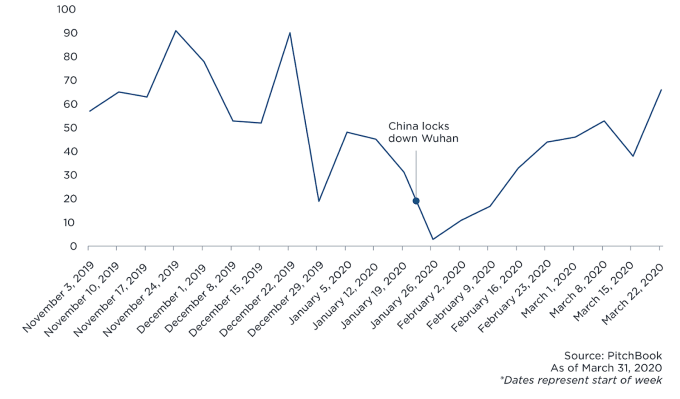

For the past month, VC investment pace seems to have slacked off in the U.S., but deal activities in China are picking up following a slowdown prompted by the COVID-19 outbreak.

According to PitchBook, “Chinese firms recorded 66 venture capital deals for the week ended March 28, the most of any week in 2020 and just below figures from the same time last year,” (although 2019 was a slow year). There is a natural lag between when deals are made and when they are announced, but still, there are some interesting trends that I couldn’t help noticing.

While many U.S.-based VCs haven’t had a chance to focus on new deals, recent investment trends coming out of China may indicate which shifts might persist after the crisis and what it could mean for the U.S. investor community.

Image Credits: PitchBook

Powered by WPeMatico

US carrier Verizon* has splashed out to buy veteran B2B videoconferencing platform, BlueJeans Network — shelling out less than $500 million on the acquisition, according to the Wall Street Journal which first reported the news.

A Verizon spokeswoman confirmed to TechCrunch that the price-tag is sub-$500M but did not provide a more exact figure. Videoconferencing platform Blue Jeans has raised ~$175M since being founded around a decade ago, per Crunchbase, with US investor NEA leading a Series E round back in 2015.

In a press release announcing the deal, Verizon said it has entered into a definitive agreement to acquire the enterprise-grade videoconferencing and event platform in order to expand its “immersive unified communications portfolio”.

“Customers will benefit from a BlueJeans enterprise-grade video experience on Verizon’s high-performance global networks. In addition, the platform will be deeply integrated into Verizon’s 5G product roadmap, providing secure and real-time engagement solutions for high growth areas such as telemedicine, distance learning and field service work,” it wrote.

“As the way we work continues to change, it is absolutely critical for businesses and public sector customers to have access to a comprehensive suite of offerings that are enterprise ready, secure, frictionless and that integrate with existing tools,” added Tami Erwin, CEO of Verizon Business, in a supporting statement. “Collaboration and communications have become top of the agenda for businesses of all sizes and in all sectors in recent months. We are excited to combine the power of BlueJeans’ video platform with Verizon Business’ connectivity networks, platforms and solutions to meet our customers’ needs.”

The acquisition comes at a time when videoconferencing is seeing a massive uptick in usage as white collar workers around the world log on to meetings from home during the coronavirus pandemic.

Although it’s BlueJeans’ rival, Zoom, that’s been the most high profile name linked to the viral videoconferencing boom in recent weeks. The latter recently revealed that daily meeting participants on its platform jumped from a modest 10M in December to 200M in March.

However such booming growth and consumer usage has brought increased scrutiny for Zoom — leading to a spate of warnings (and even some bans), related to security and privacy concerns. And earlier this month the company said it would freeze product dev to focus on the laundry list of issues that have surfaced as users have piled in and kicked its tires, taking a little of the shine off of surging growth.

On the sheer usage front BlueJeans is certainly small fish in comparison to Zoom — having remained b2b focused. A BlueJeans spokeswoman told us it has more than $100M ARR and over 15,000 customers at this point. (Some notable users include Facebook and Disney.)

But it’s paying users that are likely of most interest to Verizon, hence talk of telemedicine, distance learning and field service work — areas ripe for coronavirus-accelerated digitization. Carriers generally, meanwhile, haven’t been able to translate increased usage during the pandemic into a revenue growth story — as a result of a combination of fixed costs, debt and market disruption that’s been hitting their shares during the coronavirus crisis, per Reuters. Bolting on more b2b tools looks to be one way of growing network revenues.

“The combination of BlueJeans’ world class enterprise video collaboration platform and trusted brand with Verizon Business’ next generation edge computing innovation will deliver highly differentiated and compelling solutions to our joint customers,” said Quentin Gallivan, BlueJeans CEO, in a statement. “We are very excited about joining the Verizon team and we truly believe the future of business communications starts today!”

Verizon said today that said BlueJeans founders and “key management” will join the company as part of the acquisition, with BlueJeans employees set to become Verizon employees immediately following the close of the deal — which is expected in the second quarter, pending customary closing conditions.

BlueJeans co-founder Krish Ramakrishnan has a history of exits, selling a couple of his previous startups to networking giant Cisco — where he has also worked, in between spinning out his own companies.

*Disclosure: Verizon is also TechCrunch’s parent company

Powered by WPeMatico