telehealth

Auto Added by WPeMatico

Auto Added by WPeMatico

The pandemic has highlighted some of the brightest spots — and greatest areas of need — in America’s healthcare system. On one hand, we’ve witnessed the vibrancy of America’s innovation engine, with notable contributions by U.S.-based scientists and companies for vaccines and treatments.

On the other hand, the pandemic has highlighted both the distribution challenges and cost inefficiencies of the healthcare system, which now accounts for nearly a fifth of our GDP — far more than any other country — yet lags many other developed nations in clinical outcomes.

Many of these challenges stem from a lack of alignment between payment and incentive models, as well as an overreliance on hospitals as centers for care delivery. A third of healthcare costs are incurred at hospitals, though at-home models can be more effective and affordable. Furthermore, most providers rely on fee for service instead of preventive care arrangements.

These factors combine to make care in this country reactive, transactional and inefficient. We can improve both outcomes and costs by moving care from the hospital back to the place it started — at home.

Right now in-home care accounts for only 3% of the healthcare market. We predict that it will grow to 10% or more within the next decade.

In-home care is nothing new. In the 1930s, over 40% of physician-patient encounters took place in the home, but by the 1980s, that figure dropped to under 1%, driven by changes in health economics and technologies that led to today’s hospital-dominant model of care.

That 50-year shift consolidated costs, centralized access to specialized diagnostics and treatments, and created centers of excellence. It also created a transition from proactive to reactive care, eliminating the longitudinal relationship between patient and provider. In today’s system, patients are often diagnosed by and receive treatment from individual doctors who do not consult one another. These highly siloed treatments often take place only after the patient needs emergency care. This creates higher costs — and worse outcomes.

That’s where in-home care can help. Right now in-home care accounts for only 3% of the healthcare market. We predict that it will grow to 10% or more within the next decade. This growth will improve the patient experience, achieve better clinical outcomes and reduce healthcare costs.

To make these improvements, in-home healthcare strategies will need to leverage next-generation technology and value-based care strategies. Fortunately, the window of opportunity for change is open right now.

Over the last few years, five significant innovations have created new incentives to drive dramatic changes in the way care is delivered.

Powered by WPeMatico

Telehealth platform Eucalyptus raised a $22.3 million Series B round of funding to build a digital health portfolio for primary care in Australia.

NewView Capital led the round with participation from existing investors Blackbird Ventures and W23, and new investor AirTree Ventures. As part of the investment, Ravi Viswanathan, NewView founder and managing partner, will be joining the Eucalyptus board.

The new round gives the Sydney-based company a total of $32.8 million raised since it was founded in 2019 by Tim Doyle, Benny Kleist, Alexey Mitko and Charlie Gearside.

Australia’s healthcare system is a two-payer model, where most of the care is paid for by the government, and there is a smaller insurance coverage that is owned by individuals. Eucalyptus fits into these models as a private-pay option selling directly to consumers. In some cases, the company is able to charge lower copays for care than the average $25 per doctor visit, Doyle told TechCrunch.

He touts the company as the “largest vertically integrated telehealth platform in Australia,” serving more than 200,000 patients across four demographic-focused brands: contraception and fertility, skincare, men’s health and sexual wellness. Each brand has its own core platform of healthcare providers, patient data repository, remote monitoring tools and partnerships with pathology labs and pharmacies.

All of that results in a higher touch and higher quality relationship between doctor and patient, Doyle said.

“We are seeing an opportunity to shorten the amount of time between identification of a condition and diagnosis,” he added. “We also want to go more in-depth into diabetes, heart conditions and mental health. People are dropping out of diabetes and mental care because there are not enough touch points that are easy to use. If we can build a hub, it will make it easier to treat those conditions.”

In addition to product development, the new funding enables Eucalyptus to build toward being a major player in the telehealth industry. The company will introduce new brands in the next year around chronic care like behavioral health, weight management and diabetes.

Eucalyptus grew its revenue between 200% to 300% year over year since 2019, Doyle said. This is not unlike other startups in the digital health sector, where 2020 saw another record year for venture capital investment. He expects similar growth in 2021, including adding about 20 employees to be over 100 by the end of the year.

Meanwhile, Doyle said he is excited to work with NewView, especially with Viswanathan and principal Christina Fa, who said Eucalyptus is proving that Australia can lead in digital healthcare.

“The team is impressive in terms of clarity of vision and execution, especially in the way they brought in people to manage the brands,” she told TechCrunch. “It is unique being based in Australia where they don’t have Teledoc and other digital health companies. Instead, Eucalyptus had to build all of that in-house and do the hard work upfront. In addition, they curated a network of health providers and four brands, each with their own personalities. This allows them to be fully vertically integrated and own the customer journey.”

Powered by WPeMatico

There was a time when this column was more than a never-ending run of IPO coverage. Then the unicorn liquidity cycle kicked off and it’s been a long run of public offerings ever since. This morning is no exception.

Doximity filed to go public earlier today. You likely haven’t heard of the company because it exists in the modestly obscure world of telehealth. But it’s a venture-backed startup all the same that raised more than $80 million from investors like Emergence, InterWest Partners, Morgenthaler Ventures and Threshold, according to Crunchbase data.

Notably, Doximity has not fundraised since 2014, a year in which it attracted just under $82 million at a valuation of $355 million, per PitchBook data. How has it managed to not raise for so long? By generating lots of cash and profit over the years. Health tech communications, it turns out, can be a lucrative endeavor.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Doximity is a social network that allows doctors to speak to each other while complying with HIPAA, a federal law that promotes medical privacy. The network, originally defined as a LinkedIn for medical professionals, gives doctors a Rolodex for specialists, a newsfeed for healthcare updates, a communication tool to talk to patients and a job search tool.

In 2017, Doximity claimed that it reached 70% of all U.S. doctors, more than 800,000 licensed professionals.

This is CEO Jeff Tangney’s second time bringing a health tech company public after his previous medical software startup, Epocrates, debuted in 2011.

This is CEO Jeff Tangney’s second time bringing a health tech company public after his previous medical software startup, Epocrates, debuted in 2011.

Let’s chat briefly about the larger health tech exit market and then dig into Doximity’s IPO filing and get our heads around how the company managed to avoid private-market dilution for seven years — and what the company may be worth.

The global digital health market is estimated to hit $221 billion by 2026, underscoring how large an opportunity the sector may present to venture capitalists. But investors aren’t merely just paying attention to estimates; they are seeing a number of exits in digital health (read: liquidity) that are warming up their checkbooks.

CB Insights estimates that there were 79 healthcare IPOs and M&A transactions in Q1 2021 alone, a 60% increase from the quarter prior. Another report says that there were 145 acquisitions of digital health companies in 2020, up from a solid 113 in 2019.

While still growing, it’s fair to say that those figures describe a healthy exit environment.

The list of deals in the market is straight fire. Earlier this year, Everlywell, founded in 2015, acquired two healthcare companies to expand its digital health service and distribution. Last week, Modern Fertility was bought by Ro for north of $225 million in a majority-equity deal. Before you start complaining that it’s not an IPO, consider this: A less than four-year-old company just got bought for a quarter of a billion dollars by another company that is less than four years old.

Powered by WPeMatico

U.K.-based Fertifa has bagged a £1 million (~$1.3 million) seed to plug into a fertility-focused workplace benefits platform. Passion Capital is investing in the round, along with some unnamed strategic angel investors.

The August 2019-founded startup sells bespoke reproductive health and fertility packages to U.K. employers to offer as workplace benefits to their staff — drawing on the use of technologies like telehealth to expand access to fertility support and cater to rising demand for reproductive health services.

Challenges conceiving can affect around one in seven couples, per the U.K.’s National Health Service (NHS).

In recent years fertility startups have been getting more investor attention as VC firms cotton on to growing market. Employers have also responded, with tech industry workplaces among those offering fertility “perks” to staff. Although the access-to-services issue can be more acute in the U.S. — given substantial costs involved in obtaining treatments like IVF.

In the U.K. the picture is a little different, given that the country’s taxpayer-funded NHS does fund some fertility treatments — meaning IVF can be free for couples to access. Although how much support couples get can depend on where in the country they live, with some NHS trusts funding more rounds of IVF than others. There can also be access restrictions based on factors such as a woman’s age and the length of time trying to conceive.

This means U.K. couples can run out of free fertility support before they’ve been able to conceive — pushing them toward paying for private treatment. Hence Fertifa spotting an opportunity for a workplace benefits model around reproductive health services.

It signed up its first employers this spring and summer, and says it now has a portfolio of corporate clients with an employee pool from a few hundreds to >10,000 — although it isn’t breaking out customer numbers. Rather, it says its services are available to around 700,000 U.K. employees at this point.

“At Fertifa we want to make fertility services more widely accessible to people,” says founder and CEO Tony Chen. “Some levels of fertility services can be provided by the NHS but every single NHS trust is different with eligibility, requirements and resources, and so unfortunately it can too often be reduced to a “postcode lottery”.

“We believe that everyone should have easy access to information, resources, education and services relating to fertility — and that working with workplaces is one way to start. With our efforts and partnerships we hope to normalise the conversations about fertility at work, just as other forms of health are openly discussed and provided for.”

Passion Capital partner Eileen Burbidge — who is joining Fertifa’s board (along with Passion’s Malin Posern) — has been public about her own use of IVF and takes a very personal interest in the fertility space.

“The unfortunate fact is that over recent years, even though success rates have increased and of course more and more patients are exploring the benefits of IVF, NHS funding has been declining and the number of patients using the NHS for their first cycle has also been decreasing,” she tells TechCrunch.

“This doesn’t take away from the fact that it’s brilliant what we get from the NHS here in the U.K., but there’s clearly a lot more which can be done to further increase accessibility and affordability — given less and less funding for the NHS in the face of increasing demand of both the NHS and private routes.”

Fertifa says its model is to provide direct care and support to employees — rather than being a broker or acting as part of a referral system. So it has two in-house clinicians at this stage (out of a team of 10-15 people). Although it also says it “partners” with clinicians and clinics across the U.K. So it’s not doing everything in-house.

It offers what it bills as a “full range” of fertility and gynaecology services — from assisted reproductive technology such as IVF, IUI and more; fertility planning such as egg, sperm and embryo freezing to donor-assisted and third-party reproduction such as donor eggs and sperm; as well as surrogacy and adoption.

Its doctors, nurses and “fertility advocates” are there to provide a one-to-one care service to support patients throughout the process.

“We use technology in a number of ways and are ambitious about how it will help us to maintain an advantage over others in the sector and provide the best customer experience,” says Chen, noting it has developed “a full end-to-end” app for patients to guide them through the various stages of their fertility journey.

“On the employer side we have a full employer portal as well which provides educational resources, support options and access to services for HR/People teams to use and share with their workforces. Additionally, we use telehealth to enable more efficient, convenient (particularly in the age of COVID-19 restrictions) and immediate consultations with clinicians and nurses. Finally, we are refining our machine learning algorithms to help drive more informed decision making for patients and clinicians alike.”

It’s not currently applying AI but says that over time its in-house medical experts will use artificial intelligence to aid decision-making — with the aim of reducing clinic visits, enhancing the patient experience and yielding better clinical pregnancy rates.

Chen points to the U.K.’s Human Fertilisation and Embryology Authority having already made its data publicly available on more than 100,000 couples and their treatment and outcomes — suggesting such data-sets will underpin the development of new predictive models for fertility.

“With additional insight and data sources [we] could more accurately predict probability of success for a patient — or the best type of treatment for them,” he adds.

While Fertifa’s current focus is U.K. expansion — targeting workplaces of all sizes and scale — it’s also got its eye on scaling overseas down the line. Although it will of course face more competition at that point, with the likes of Y Combinator backed Carrot already offering global fertility benefits packages for employers.

“Fertility and reproductive health is important to people all over the world,” says Chen. “Globally one in four women experience a miscarriage, every LGBT+ individual requires support to become a parent, and everyone needs to be increasingly empowered to take control of their reproductive health through fertility preservation treatment.”

Powered by WPeMatico

Telehealth, or remote, tech-enabled healthcare, has existed for years in primary medical care through companies like Teladoc (NYSE: TDOC), Doctors on Demand and MDLIVE.

In recent years, the application of telehealth had rapidly expanded to address specific chronic and behavioral health issues like mental health, weight loss and nutrition, addiction, diabetes and hypertension, etc. These are real and oftentimes very severe issues faced by people all over the world, yet until now have seen little to no use of technology in providing care.

We believe behavioral health is particularly suited to benefit from the digitization trends COVID-19 has accelerated. Previously, we’ve written about the pandemic’s impact on online learning and education, both for K-12 students and adult learners. But behavioral health is another area impacted by the fundamental change in consumers’ behavior today. Below are four reasons we think the time is now for behavioral health startups — followed by five key factors we think characterize successful companies in this area.

Traditional behavioral healthcare is cost-prohibitive for most people. In-person therapy costs $100+ per session in the U.S., and many mental health and substance-use providers don’t accept insurance because they don’t get paid enough by insurers.

By contrast, telehealth reduces overhead costs and scales more effectively. Leveraging technology, providers can treat more patients in less time with almost zero marginal costs. Mobile-based communications enable asynchronous care that further helps providers scale. Access to digital content gives patients on-going support without the need for a human on the other side. This is particularly useful in treating behavioral health issues where ongoing support and motivation may be necessary.

Globally, we face an extreme shortage of behavioral health providers. For example, the United States has fewer than 30,000 licensed psychiatrists (translating to <1 for every 10,000 people). Outside of big cities, the problem gets worse: ~50-60% of nonmetro counties have no psychologists or psychiatrists at all.

Even when providers are available, wait times for appointments are notoriously long. This is a huge issue when behavioral health conditions often require timely intervention.

We are seeing new platforms build large networks of certified coaches, licensed psychologists and psychiatrists, and other providers, aggregating supply in what has historically been a scarce and a highly fragmented provider population.

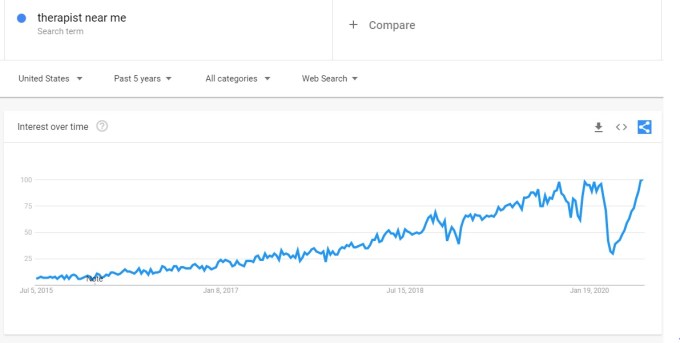

We believe the stigma associated with mental illness and other behavioral health conditions is dissipating. More and more public figures are speaking out about their struggle with anxiety, depression, addiction and other behavioral health issues. Our zeitgeist is shifting fast, and there’s an all-time high in people seeking help as the Google Trends data below demonstrates.

Image Credits: Google

Note: The anomalous dip in March/April ’20 was driven by mandatory shelter-in-place due to COVID-19.

Powered by WPeMatico

In three years Zachariah Reitano’s startup, Ro, has managed to hit a reported $1.5 billion valuation for its transformation from a company focused on treating erectile dysfunction to a telemedicine service for a range of elective and urgent care-focused treatments.

Through Rory for women’s health, Roman for men’s health and Zero for smoking cessation, Reitano and fellow co-founders Saman Rahmanian, and Rob Schutz, built a company that now treats 20 conditions, including sexual health, weight loss, dermatology, allergies and more, according to a statement from the company.

Image Credit: Zero

Ro also has a new pharmacy business, Ro Pharmacy, which is an online cash pay pharmacy offering more than 500 generic medications for just $5 per month per drug. And the company is getting into the weight loss business through a partnership with the private equity-backed healthcare company, Gelesis.

Ro’s also becoming a gateway into patient acquisition for primary care providers through Ribbon Health, and a test-case for the use of Pfizer’s Greenstone service, which provides certification that a generic drug is validated by one of the major pharmaceuticals.

The company’s $1.5 billion valuation is courtesy of a new $200 million investment from existing investors led by General Catalyst and including FirstMark Capital, Torch, SignalFire, TQ Ventures, Initialized Capital, 3L and BoxGroup. New first-time investor The Chernin Group also participated. In all, Ro has raised $376 million since it launched in 2017.

“This new investment will further our mission to become every patient’s first call. We’ll continue to invest in our vertically-integrated healthcare ecosystem, from our Collaborative Care Center to our national pharmacy operating system. This is just the beginning of Ro’s patient-centered healthcare platform.”

It’s all part of the company’s mission to provide a point of entry into the healthcare system independent of insurance qualifications.

“Telehealth companies like Ro are using technology to address long-standing healthcare disparities that have been exacerbated by COVID-19,” said Dr. Joycelyn Elders, MD, Ro Medical Advisor and Former U.S. Surgeon General. “By empowering providers to leverage their skills as efficiently and effectively as possible, Ro delivers affordable, high-quality care regardless of a patient’s location, insurance status, or physical access to physicians and pharmacies.”

Ro’s new financing is one of several forays by tech investors into reshaping the healthcare system at a time when patient care has been severely disrupted by attempts to mitigate the spread of COVID-19.

Digital medicine is assuming a central position in the healthcare world, with most consultations now occurring online. Reimbursement schemes for telemedicine have changed dramatically and investors see an opportunity to capitalize on these changes by aggressively backing the expansion plans of companies looking to bring digital healthcare directly to consumers.

That’s one of the reasons why Ro’s major competitor, Hims, is reported to be seeking access to public markets through its sale to a special purpose acquisition company for roughly $1 billion, according to Reuters.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

ZoomInfo went public yesterday. After pricing its IPO $1 ahead of its proposed range at $21 per share, the company closed its first day’s trading worth $34.00, up 61.9%, according to Yahoo Finance. Then the company gained another 5.2% in after-hours trading.

Whether you feel that this SaaS player was worth the revenue multiple its original, $8 billion valuation dictated — let alone that same multiple times 1.6x — the message from the offering was clear: the IPO window is open.

This is not news to a few companies looking to take advantage of today’s strong equity prices.

Used-car marketplace Vroom is looking to get its shares public before its Q2 numbers come out, despite a history of slim gross profit generation. The company hopes to go public for as much as $1.9 billion, a modest uptick from its final private valuations.

We’ll get another dose of data when Vroom does price — how much investors are willing to pay for slim-margin revenue will tell us a bit more than what we learned from ZoomInfo, which has far superior gross margins. Investors have already signaled that they are content to value high-margin software-ish revenues richly. Vroom is more of a question, but if it does price strongly we’ll know public investors are looking for any piece of growth they can find.

This brings us to the latest news: Amwell has confidentially filed to go public. Formerly known as American Well, CNBC reports that the venture-backed telehealth company has dramatically expanded its customer base:

Telemedicine has seen an uptick in recent months, as people in need of health services turned to phone calls and video chats so they could avoid exposure to COVID-19. The company told CNBC last month that it’s seen a 1,000% increase in visits due to coronavirus, and closer to 3,000% to 4,000% in some places.

Powered by WPeMatico

Hims & Hers, the startup focused on providing access to elective treatments for things like hair loss, skin care and erectile disfunction and online telemedicine services, is expanding its services to include a Spanish language option, the company said.

After Mexico, the U.S. has the second-largest Spanish speaking population in the world, with an estimated 41 million U.S. residents speaking Spanish at home. The population also prefers to receive healthcare information and frequent facilities that offer resources in Spanish.

Now, with a shortage looming in primary care physicians for rural areas and inner cities and a sky-high rate of Hispanics living without any form of healthcare coverage (roughly 15.1%, according to data provided by the company), Hims & Hers is pitching its telemedicine offering as an option.

“Language, cost, and location should not be barriers to receiving quality care, which is why we are launching a Spanish offering on our telemedicine platform,” the company said in a statement.

The company’s $39 primary care consultations at its Hims and its Hers websites will be in Spanish. That will include everything from communications like the patient intake form and instructions to prepare for an online consultation along with a connection to Spanish-speaking healthcare provider.

“The reason we created Hims & Hers was to break down barriers and provide more people with access to quality and convenient care,” the company’s co-founder and chief executive, Andrew Dudum, said in a statement. “As a telemedicine company, we recognize the need and understand the importance of serving the Spanish-speaking population. We hope those seeking access to care in Spanish find our platform to be a welcoming, inclusive, quality experience.”

Powered by WPeMatico

While some U.S. investors might have taken comfort from China’s rebound, we still find ourselves in the early innings of this period of uncertainty.

Some epidemiologists have estimated that COVID-19 cases will peak in April, but PitchBook reports that dealmaking was down -26% in March, compared to February’s weekly average. The decline is likely to continue in coming weeks — many of the deals that closed last month were initiated before the pandemic, and there is a lag between when deals are made and when they are announced.

However, there’s still hope. A recent report concluded that because valuations are lower and there’s less competition for deals, “the best-performing vintages tend to be those that invest at the nadir of a downturn and into the early stage of recovery.” There are countless examples from the 2008 recession, including many highly valued VC-backed businesses such as WhatsApp, Venmo, Groupon, Uber, Slack and Square. Other early-stage VCs seem to have arrived at a similar conclusion.

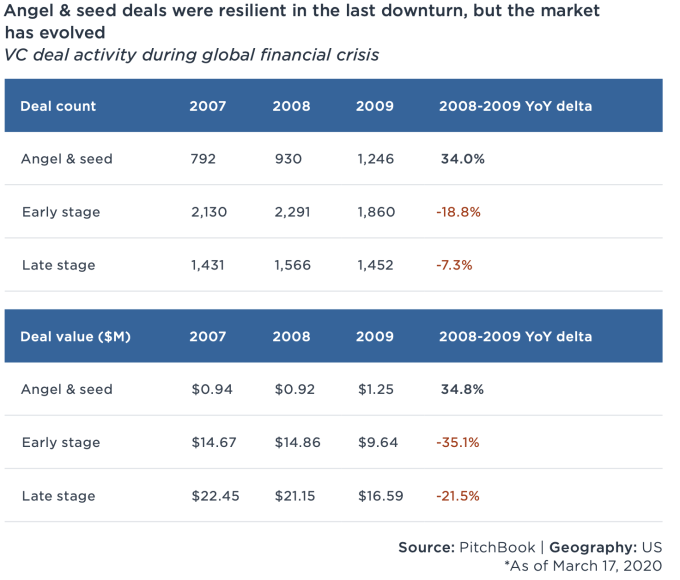

Also, early-stage investing seems more resilient. During the last recession, angel and seed activity increased 34% as interest in the stage boomed during a period of prolonged growth.

Image Credits: PitchBook (opens in a new window)

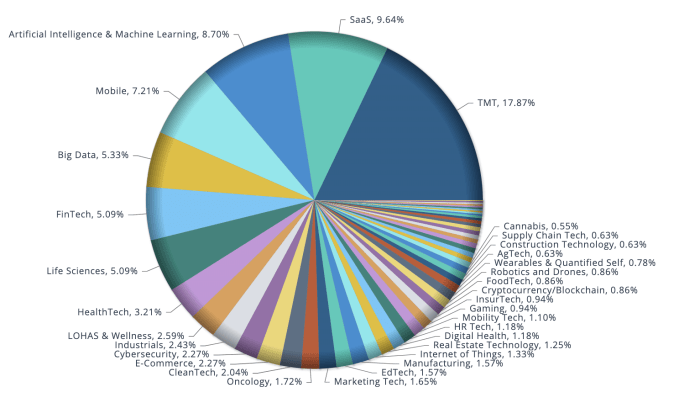

Furthermore, there is still capital to be deployed in categories that interested investors before the pandemic, which may set the new order in a post-COVID-19 world. According to data provider Preqin Ltd., VC dry powder rose for a seventh consecutive year to roughly $276 billion in 2019, and another $21 billion were raised last quarter. And looking at the deals on the early-stage side that were made year to date, especially in March, the vertical categories that garnered the most funding were enterprise SaaS, fintech, life sciences, healthcare IT, edtech and cybersecurity.

Image Credits: PitchBook

That said, if VCs have the capital to deploy and are able to overcome the obstacle of “having never met in person,” here are six investment trends that could emerge when the pandemic is over.

Powered by WPeMatico

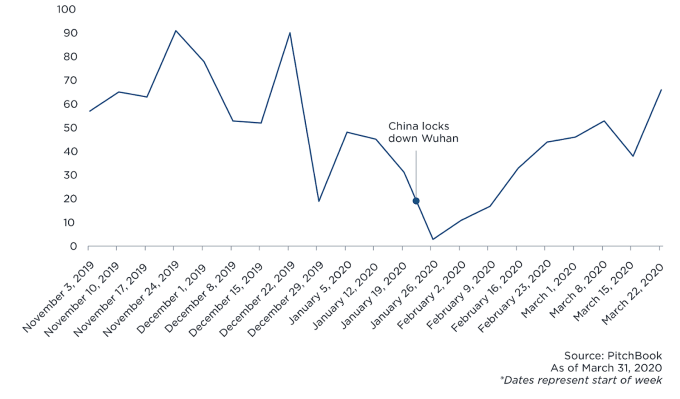

For the past month, VC investment pace seems to have slacked off in the U.S., but deal activities in China are picking up following a slowdown prompted by the COVID-19 outbreak.

According to PitchBook, “Chinese firms recorded 66 venture capital deals for the week ended March 28, the most of any week in 2020 and just below figures from the same time last year,” (although 2019 was a slow year). There is a natural lag between when deals are made and when they are announced, but still, there are some interesting trends that I couldn’t help noticing.

While many U.S.-based VCs haven’t had a chance to focus on new deals, recent investment trends coming out of China may indicate which shifts might persist after the crisis and what it could mean for the U.S. investor community.

Image Credits: PitchBook

Powered by WPeMatico