TechCrunch

Auto Added by WPeMatico

Auto Added by WPeMatico

We have seen a lot of action this week as the DoD tries to finally determine the final winner of the $10 billion, decade-long DoD JEDI cloud contract. Today, the DoD released a statement that after reviewing the proposals from finalists Microsoft and Amazon again, it reiterated that Microsoft was the winner of the contract.

“The Department has completed its comprehensive re-evaluation of the JEDI Cloud proposals and determined that Microsoft’s proposal continues to represent the best value to the Government. The JEDI Cloud contract is a firm-fixed-price, indefinite-delivery/indefinite-quantity contract that will make a full range of cloud computing services available to the DoD,” the DoD said in a statement.

This comes on the heels of yesterday’s Court of Appeals decision denying Oracle’s argument that the procurement process was flawed and that there was a conflict of interest because a former Amazon employee helped write the requirements for the RFP.

While the DoD has determined that it believes that Microsoft should still get the contract, after selecting them last October, that doesn’t mean this is the end of the line for this long-running saga. In fact, a federal judge halted work on the project in February pending a hearing on an ongoing protest from Amazon, which believes it should have won based on merit, and the fact it believes the president interfered with the procurement process to prevent Jeff Bezos, who owns The Washington Post, from getting the lucrative contract.

The DoD confirmed that the project could not begin until the legal wrangling was settled. “While contract performance will not begin immediately due to the Preliminary Injunction Order issued by the Court of Federal Claims on February 13, 2020, DoD is eager to begin delivering this capability to our men and women in uniform,” the DoD reported in a statement.

A Microsoft spokesperson said the company was ready to get to work on the project as soon as it got the OK to proceed. “We appreciate that after careful review, the DoD confirmed that we offered the right technology and the best value. We’re ready to get to work and make sure that those who serve our country have access to this much needed technology,” a Microsoft spokesperson told TechCrunch .

Meanwhile, in a blog post published late this afternoon, Amazon made it clear that it was unhappy with today’s outcome and will continue to pursue legal remedy for what they believe to be presidential interference that has threatened the integrity of the procurement process. Here’s how they concluded the blog post:

We strongly disagree with the DoD’s flawed evaluation and believe it’s critical for our country that the government and its elected leaders administer procurements objectively and in a manner that is free from political influence. The question we continue to ask ourselves is whether the President of the United States should be allowed to use the budget of the Department of Defense to pursue his own personal and political ends? Throughout our protest, we’ve been clear that we won’t allow blatant political interference, or inferior technology, to become an acceptable standard. Although these are not easy decisions to make, and we do not take them lightly, we will not back down in the face of targeted political cronyism or illusory corrective actions, and we will continue pursuing a fair, objective, and impartial review.

While today’s statement from DoD appears to take us one step closer to the end of the road for this long-running drama, it won’t be over until the court rules on Amazon’s arguments. It’s clear from today’s blog post that Amazon has no intention of stepping down.

Note: We have updated this story with content from an Amazon blog post responding to this news.

Powered by WPeMatico

Back in early July, TechCrunch covered the Envision Accelerator. The program was put together by a group of students and recent graduates, often with some early venture capital experience, to help give some young startups a boost, and to shake up industry diversity metrics at the same time.

Now on the other side of their first batch’s official program and into its investor week, Envision shared a number of statistics regarding that first cohort, and talked about plans for its second.

What I appreciate about the Envision group is that by simply going out and making their own accelerator, they have shown that it is possible to attract a diverse group of startups to a program. How diverse? Let’s find out.

According to data provided to TechCrunch by Annabel Strauss and Eliana Berger from the Envision team (more on them here, if you’re curious), 17 companies made it into the first group. Of those 17 companies and their founding teams, around one-third of founders were black, around one in five were Latinx and more than 75% had a female founder.

Those are impressive metrics, frankly, especially when we consider what other groups have managed in recent sessions. Envision’s founders also skew young, not a surprise, given that the effort was effectively students making a program for their fellow students, with a three-to-one bias in favor of undergrads versus graduate students.

We’ll list the participating companies with links to their sites below, as per usual with this sort of accelerator roundup.

But, before we do, a few notes on how the first batch went down. When we last talked about Envision, they were still fundraising to pull together more capital to give to their selected companies. The idea was to provide $10,000 in equity-free capital, along with an eight-week program of lectures, networking and hands-on help from the Envision collective and a group of advisors.

According to Strauss and Berger, Envision was able to raise all the money that it needed to provide funding to its selected companies, though not every team picked up the full $10,000, with the duo noting that the amount varied based somewhat on need.

It will not be clear for a bit if the companies that went through Envision’s maiden class manage to raise more capital, scale, and become success. But for the Envision team itself, round one went well enough that a second effort is just around the corner.

And when it comes to that second push — or class, really — Envision remains in a hurry. After putting together its initial cohort while building its own organization on the fly, the group is going to kick off its second batch in October, giving it slim breathing room between cohorts.

There’s a reason for the haste, however. First, Envision wants to add two weeks to its programming, bringing the accelerator to a total of 10 weeks to include more training, and to fit that into the current semester, October was the kickoff month. Strauss and Berger noted that some students are taking leave during the first semester of this academic year.

More on Envision itself when we hear more on how the first batch did in attracting investor interest.

Here are the companies from batch one:

- Adora: Adora is a personalized, digital campus visit platform that makes compelling visits accessible to everyone.

- Devie: Devie is a parent coaching app that guides parents through challenges in a personal, accessible and actionable way.

- Forage: Forage is a mobile application that provides real-time pricing at grocery stores so families can save money.

- Holdette: At Holdette, we make professional work wear with real pockets for women entering the workforce for the first time.

- Justice Text: Justice Text makes video evidence management software to produce fair outcomes in the criminal justice system.

- Klara: Klara is a data science platform transforming the way consumers discover skincare and haircare products.

- Mindstand: Mindstand helps leaders identify implicit bias, employee engagement and culture fit within their internal communications.

- MODE: MODE helps people discover and purchase clothes through a personalized, social shopping experience.

- Mylabox: Mylabox is a cross-border e-commerce marketplace enabling SMBs in LatAm to access high-quality overseas products.

- Nibble: Nibble is a platform solving food waste by helping restaurants sell excess meals and ingredients at a discount.

- Pareto: Pareto is building a library of quick-to-launch workflows that startups can deploy for operations as they scale.

- Schefs: Schefs is a platform for college students to facilitate and participate in themed conversations over a virtual meal.

- UrConvey: UrConvey is a safe app that makes it easy to ride share with people you know by harnessing your network.

- Vngle: Vngle is a decentralized grassroots news network bringing “various angles” of local reality coverage to news deserts.

- Wellnest: Wellnest is a joyful journaling app that increases mindfulness by prioritizing user experience, voice and insights.

- Winkshare: Winkshare is a secure messaging app designed for the modern relationship. Your relationship, your business.

- Yup: Yup rewards valuable opinions across the web. Rate anything, earn rewards for accuracy, and gain status.

Powered by WPeMatico

The Palantir S-1 finally dropped yesterday after TechCrunch spilled a bunch of its guts last Friday. You can read the filing here, if you are so inclined.

Today, however, instead of our usual overview, I have a different goal: We’re going to be a bit more specific.

It’s fun and easy to clown on Palantir’s ridiculous ownership structure, in which a few dudes have decided that, in perpetuity, they must remain co-Lords of the Ring. And, sure, the company is smaller in terms of revenue-scale than many expected (a bit more Hobbiton than Bree, really). And, yes, its net losses are somewhat staggering (post-Helm’s Deep Saruman?), reaching nearly 100% of revenue in 2018.

But things have gotten better in Palantir-land (Mordor?) in recent quarters, which we should note.

So, in light of the generally negative reviews of Palantir’s finances (similar to what is left of Moria?) that I’ve seen in the media and from investors both publicly and privately, here are the bullish bits about the impending direct listing.

In brief, falling net losses in absolute and percent-of-revenue terms paint the picture of a company that is past a high-burn period, allowing profitability to continue to improve; improving gross margins point to a company that is less service-focused and more software-driven over time; the company’s falling operating cash burn is encouraging, and new customer revenue appears sharply higher in 2020 than 2019.

Let’s examine each in order:

Powered by WPeMatico

We can’t help but wonder what the future of work will look like in the wake of this pandemic. That’s the timely topic of today’s interactive webinar, COVID-19’s Impact on the Startup World.

The second of three in our free series of interactive webinars — exclusively for founders exhibiting in Digital Startup Alley at Disrupt 2020 — gets underway today, August 19 at 1 p.m. PDT/4 p.m. EDT. Exhibitors, be sure to register to attend.

Still on the fence about exhibiting at Disrupt? Hop off and get to it — buy a Disrupt Digital Startup Alley Package, tune in to the remaining webinars and then get ready to reap the benefits that come with introducing your startup to a global Disrupt audience. More on those in a minute.

You’ll hear from Nicola Corzine, executive director of the Nasdaq Entrepreneurship Center and Cameron Stanfill, a VC Analyst at PitchBook. Jon Shieber, a TechCrunch editor who covers venture capital and private equity investments will moderate the discussion. No one can predict the future, but these three bring years of experience to the table, and they’ll offer a data-informed perspective, tips and advice on how startups can adapt and what they need to think about both during and after COVID-19. It’s interactive, folks — got questions? Get answers.

Exhibiting in Digital Startup Alley is opportunity on steroids. Network with thousands of Disrupt attendees from around the globe. Expose your tech and talent to influencers of every stripe across the startup ecosystem — investors, R&D teams, advisors, potential customers. Make and nurture connections that can result in exciting partnerships.

CrunchMatch, our AI-powered networking platform bridges the physical distance of a virtual conference. It helps you quickly find and connect with the people who can help take your business to the next level. The platform’s up and running right now. Once you register for Disrupt, you can reach out to attendees and start expanding your network immediately.

Ready to exhibit? Great — be sure to mark your calendar for the final exclusive webinar. Tune in on August 26 for Fundraising and Hiring Best Practices with panelists Sarah Kunst of Cleo Capital and Brett Berson of First Round Capital.

We can’t predict the future, but there’s one thing we do know. It’s going to take every opportunity and every advantage to survive and thrive in these tumultuous times.

Buy a Disrupt Digital Startup Alley Package and tune in. It’s worth it.

Is your company interested in sponsoring or exhibiting at Disrupt 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

At TechCrunch Early Stage, I spoke with Coatue Management GP Caryn Marooney about startup branding and how founders can get people to pay attention to what they’re building.

Marooney recently made the jump into venture capital; previously she was co-founder and CEO of The Outcast Agency, one of Silicon Valley’s best-regarded public relations firms, which she left to become VP of Global Communications at Facebook, where she led comms for eight years.

While founders often may think of PR as a way to get messaging across to reporters, Marooney says that making someone care about what you’re working on — whether that’s customers, investors or journalists — requires many of the same skills.

One of the biggest insights she shared: at a base level, no one really cares about what you have to say.

Describing something as newsworthy or a great value isn’t the same as demonstrating it, and while big companies like Amazon can get people to pay attention to anything they say, smaller startups have to be even more strategic with their messaging, Marooney says. “People just fundamentally aren’t walking around caring about this new startup — actually, nobody does.”

Getting someone to care first depends on proving your relevance. When founders are forming their messaging to address this, they should ask themselves three questions about their strategy, she recommends:

Powered by WPeMatico

Before the coronavirus made edtech more relevant, companies in the sector were historically likely to see slow, low exits. Despite successful IPOs by 2U, Chegg and Instructure in the United States, public markets are not crowded with edtech companies.

Some of the largest exits in the space include LinkedIn’s scoop of Lynda for a $1.5 billion in cash and stock and TPG’s purchase of Ellucian for $3.5 billion.

But both of those deals happened in 2015. Five years later, edtech is cooler and surging — but is it seeing exits? Are Lynda and Ellucian one-off success stories?

2U’s co-founder and CEO, Chip Paucek, said he is optimistic.

“We are a rare edtech IPO,” he told TechCrunch last week. “For a long time in edtech it was either ‘sell to Pearson or not.’”

Despite the sector’s slow past, Paucek said now is a good time to start an edtech company because the sector “is finally starting to hit its stride” with more back-end infrastructure and demand for online education.

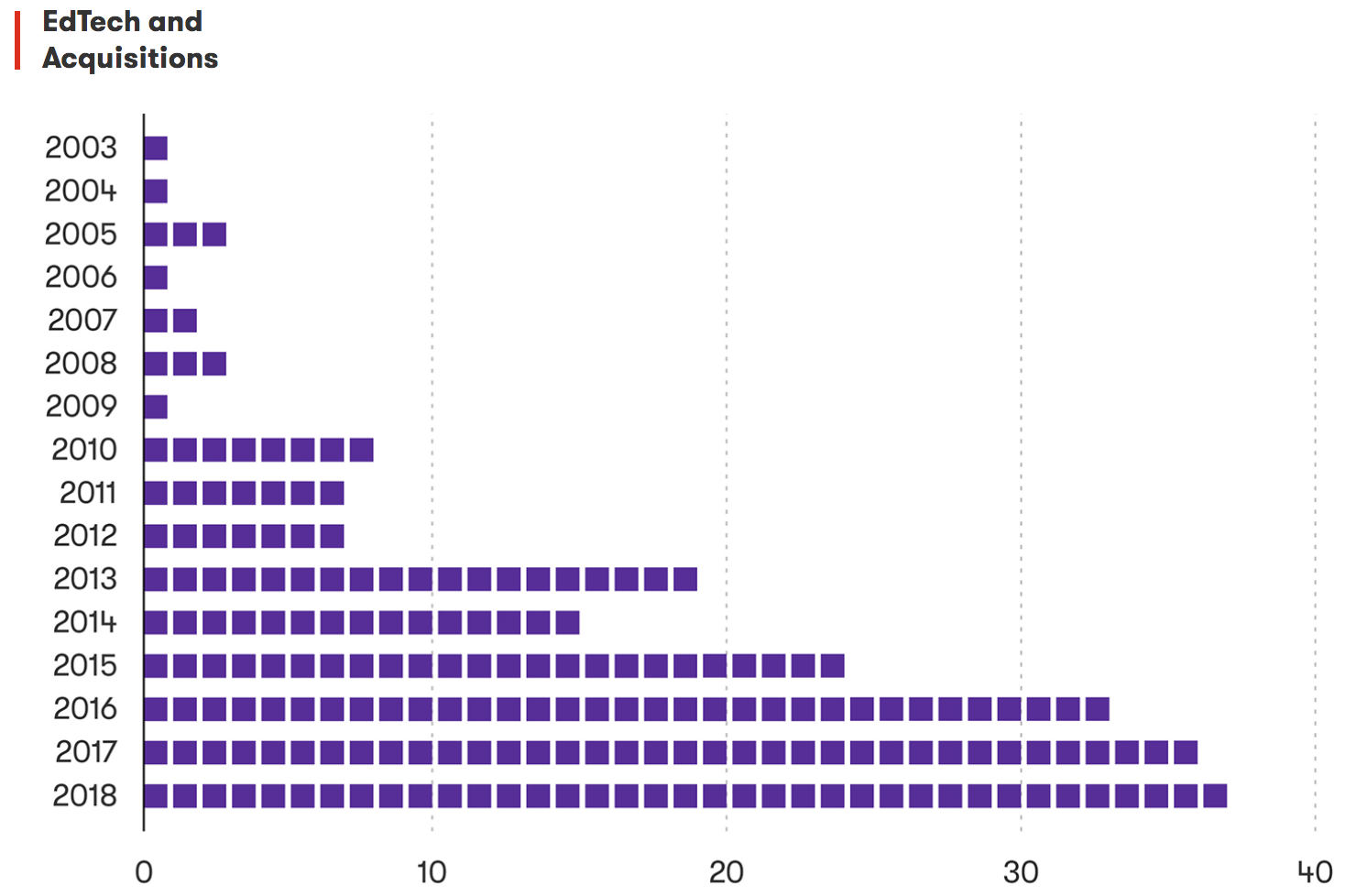

This morning, let’s use some data to paint a picture of the landscape of edtech exits and bring some balance to this stodgy stereotype.

Boot the growth

Boot the growthThere have been approximately 225 acquisitions in edtech between 2003 and 2018, according to Crunchbase data. RS Components sent me a graph in March to contextualize this timeframe a bit more:

Edtech deals over time. Graph credit: RS Components.

Powered by WPeMatico

A number of on-demand ride hailing companies are feeling the strain from reduced business, with many consumers still reluctant to travel, and especially to travel in surroundings that might increase the risk of spreading or catching the novel coronavirus. But today, one of the startups in the space is announcing a significant round of funding to continue growing in its target sector of corporate travel, underscoring where there may still be some existing and growing opportunities.

Gett, the London and Israel-based company that competes with the likes of Uber and many others to provide private car rides on-demand, has raised $100 million. Gett’s CEO and founder Dave Waiser told TechCrunch that the funding is all primary equity capital, and the company says it plans to use it to continue investing in its B2B business, which has been growing — not shrinking or staying flat — in the midst of the global health pandemic.

“The way people move around in cities is changing dramatically as a result of COVID-19 and businesses are seeking to optimise costs and to put in place efficient and safe ground travel solutions for their employees,” said Waiser, in a statement. “Our mobility software is helping businesses thrive by empowering people to be their best on the go. Being fully funded and reaching a key milestone in our profitability journey is an important step for the company. The proceeds will help us grow our unique corporate SaaS platform internationally, while we consider an IPO in the future, to further accelerate our expansion.”

The company turned operationally profitable in December 2019 and had said it planned to go public in 2020, but it sounds like that timeline, if it happens, has now been pushed back to 2021. Gett says it has met its “original financial targets that were set pre-COVID-19.” It also reached profitability in each of its core markets in June, and is on target now to be cash flow positive in 2021, ahead of a “potential” IPO.

“It’s a luxury, enabling flexibility for the company to go public when it’s best, rather than from the cash needs reasoning as many (money-losing) companies have to do nowadays,” Waiser said in an interview.

Gett is not disclosing the names of any of its investors in this round except to note that it’s a mix of new and existing backers, nor is it disclosing its valuation.

Waiser said the reason for that is that the round is still being expanded after getting oversubscribed, so it plans to announce a list of investors (and valuation?) after the expansion closes.

For some context, though, Gett has now raised $750 million, with investors including VW, Access and its founder Len Blavatnik, Kreos, MCI and more, and its last valuation was $1.5 billion, pegged to a $200 million fundraise in May 2019.

Gett started operations years ago serving both consumers and corporate users going head-to-head with the Ubers of the world for app-based, on-demand rides, but it had always differentiated its positioning by working with (in London) the “black cabs” and in NYC “yellow cabs” — that is, the established infrastructure of ride-hailing.

In recent years, it has honed its focus specifically on business accounts. No surprise, when you think about it, considering the capital intensiveness, competitiveness and subsequent poor unit economics of scaling a consumer-focused ridesharing business (a confluence of factors we’ve seen played out at Uber, Lyft, Grab and many others).

Gett’s turn to B2B has seen it pick up some 15,000 corporate customers, including one-third of the Fortune 500.

What has been interesting too is the approach Gett has taken to scale: Today, it provides rides in some 1,500 cities, but a large part of that footprint is served not directly by Gett. One of its key partners is Lyft — the result of a deal Gett inked with the company in November 2019 after Gett shut down its Juno operations in New York City. And it’s been expanding that list to include other third-party partnerships in the mix.

Partnerships may not yield margins as strong as those Gett has with direct operations. Gett still is the direct link between drivers and riders in its key markets, which include cities like London and Moscow. (It’s not disclosing what percentage of its business today is direct versus via third-party businesses.)

But on the other hand, Gett has been building its business by providing a plethora of analytics and invoicing services around the actual ride, and what it makes by securing corporate accounts on the back of that software becomes a revenue stream to offset the decline in margins from partnerships. Gett claims that its services ultimately undercut by about 25% other ground transportation options for corporates.

While a lot of consumers may have curtailed their Uber rides in recent months, the business market has seen a turn to ensuring that the travel that its users are taking is well-controlled when it has to be done, specifically to meet specific safety standards. That has been the sweet spot for Gett, with its very specific B2B approach.

“The completion of the fundraising during the pandemic is a clear expression of confidence by our shareholders and new investors in Gett’s vision to focus on the corporate market and its plan to expand globally, as well as in the Company’s strong operational and financial performance,” said Amos Genish, Gett chairman, in a statement.

Powered by WPeMatico

Over the past two decades, the venture capital industry has exploded beyond anyone’s wildest imaginations.

What began as a sleepy industry in Boston and Menlo Park has now expanded to dozens of cities the world over. The National Venture Capital Association estimates that VCs deployed more than $130 billion in 2018 and 2019, and thousands of new investors have joined the ranks in recent years to find the next great startups.

All that activity, though, poses a dilemma for founders: Who actively writes checks? Who is a leader in a specific market or vertical? Who has the conviction to underwrite pathbreaking investments? Who, ultimately, do you want to have by your side for the next decade as your startup grows?

There are lists that rank VCs by their exit returns. There are lists that rank young VCs by their potential. There are lists of VCs who claim investment interest in various sectors. There are lists that try to ferret out deal volume, impact and other quantitative metrics. There are internal lists at accelerators that share collective wisdom between founders.

Who actively writes checks? Who is a leader in a specific market or vertical? Who has the conviction to underwrite pathbreaking investments? Who, ultimately, do you want to have by your side for the next decade as your startup grows?

All those lists and rankings have an important function to serve, but for all the compilations of investors out there, we couldn’t find a single one that publicly answered a simple yet vital question: Who are the VC investors who are leaders in specific verticals who should be a founder’s first stop during a fundraise?

Today’s venture industry is made up of thousands of investors with varying specialties, and far too many passive investors that are willing to participate in rounds but don’t actively participate in deals unless other investors have committed. Many don’t actively push to get deals done or don’t actively lead the charge to build a syndicate of investors.

With all that in mind, we’re excited to launch a new initiative that we hope will help answer those questions and help founders find that first check — The TechCrunch List.

![]()

Over the next few weeks, we’re going to be collecting data around which individual investors are actually willing to write the proverbial “first check” into a startup’s fundraising round and help catalyze deals for founders — whether it be seed, Series A or otherwise (i.e. out of your Series A investors, the first person who was willing to write the check and get the ball rolling with other investors). Once we’ve collected, cleaned and analyzed the data, we’ll publish lists of the most recommended “first check” investors across different verticals, investment stages and geographies, so founders can see which investors are potentially the best fit for their company.

Founders are used to being specialized; after all, they have to live and breathe their startups every single day. So it can be jarring to start talking to generalist investors who know little about a category and ask shallow questions only to render a judgment with irrelevant advice. One of the greatest impetuses for us to put together The TechCrunch List is that like founders, we also struggle to cut through the noise around the interests of individual VCs.

We’d argue that’s close to impossible. There is more spend on technology than ever before in history. Verticals are getting more competitive — market maps that used to have 10 to 50 companies have expanded to hundreds. The only way to compete today is to specialize, and that has never been more true for VCs.

In all, The TechCrunch List will publish the most recommended “first check” writers across 22 different categories, ranging from D2C & e-commerce brands to space, and everything in between. Through some data analysis around total investments in each space, we believe our 22 categories should cover the entirety or majority of the venture activity today.

To make this project a success and create a useful resource for founders, we need your help. We want to hear from company builders and we want to hear from them directly.

To make this project a success and create a useful resource for founders, we need your help. We want to hear from company builders and we want to hear from them directly. We will be collecting endorsements submitted by founders through the form linked here.

Through the form, founders will be asked to submit their name, their startup, the stage of company, the name of the one “first check” investor they want to endorse and a couple of minor logistical items. We are asking founders here for their on-the-record endorsement. We ask that you limit your recommendations to one (1) person per fundraise round.

While many investors may have helped you in your journey, we are specifically interested in the person who most helped you get a round underway and closed. The one who catalyzed your round. The one who guided you through the fundraise process. The one investor you would ultimately recommend to other founders who are trying to find their VC champion.

Our main goal is to help founders, dreamers and company builders find investors who will invest in them today, and with your help, we think we can. The TechCrunch List is not meant to identify every possible investor under the sun who might make an investment within a space, nor just the big household-name VCs whose reputations can sometimes seem more linked to their follower counts on Twitter as opposed to their bold term sheets.

Our hope is that this can be a go-to resource for founders looking to fundraise going forward, and with that in mind, we are very determined to improve the glaring representation gaps in the venture industry. It’s no secret that the world of VC still looks like a country-club membership roster, dominated by white men with strong opinions and loud voices. Looking at the data, it’s clear that there are groups that are particularly underrepresented, with only a small portion of the industry made up of Black, Latinx and female investors, for example.

We want to amplify these voices and we want to hear particularly from founders of color, female founders and other underrepresented groups. We also want to make sure our recommended investor lists are sufficiently representative and highlight underrepresented investors who might not have had equal opportunities in the past.

We want to help builders wade through the BS politics and fundraising annoyances that founders complain to us about on a daily basis, and help them identify qualified leads that are actually active, engaged and specialized and are the best fit to help founders raise money and grow now.

Thank you for your support. We’re excited to build The TechCrunch List with you — and for you.

Powered by WPeMatico

The venture capital industry is less transparent today than at any time in recent memory.

For all the talk about expanding access and improving its sordid record on diversity, in reality, it has never been harder for founders to figure out who can even write a check to their startups in the first place.

When I first returned to TechCrunch after my second stint in venture capital, my first piece was entitled “The loss of first check investors.” While working in the venture capital industry, it was maddening to see — particularly at the pre-seed and seed stages — how few investors were really willing to go out on a limb and invest in founders before another VC had committed a check.

It’s only gotten worse in the past two years since that article, and the complexity comes from a number of different places. As our investigation showed more than a year ago, fewer and fewer venture rounds are being announced through SEC Form D filings.

There are almost no publicly accountable datasets left indicating who is writing checks in the venture industry and which companies are receiving those checks. While stealthiness is valid in the early days of a startup, the excuse wears thin after years.

Powered by WPeMatico

Three years ago almost to the day, Intercom announced that it was bringing former Intuit exec Karen Peacock on board as COO. Today, she got promoted to CEO, effective July 1. Current CEO and company co-founder Eoghan McCabe will become Chairman.

As it turns out, these moves aren’t a coincidence. McCabe had been actively thinking about a succession plan when he hired Peacock. “When I first started talking to Eoghan three years ago, he shared with me that his vision was to hire someone as COO, who could then become the CEO at the right time and he could transition into the chairman role,” Peacock told TechCrunch .

She said while the idea was always there, they didn’t feel the need to rush the process. “We were just looking for whatever the right time was, and it wasn’t something we were expected to do in the first year or two. And now is really the right time to transition with all of the momentum that we’re seeing in the market,” she said.

She said as McCabe makes the transition away from running the company he helped found, he will still be around, and they will continue working together on things like product and marketing strategy, but Peacock brings a pedigree of her own to the new role.

Not only has she been in charge of commercial aspects of the Intercom business for the past three years, prior to that she was SVP at Intuit where she ran small business products that included QuickBooks, and grew it from a $500 million business to a hefty $2.5 billion during her tenure.

McCabe says that experience was one of the reasons he spent six months trying to convince Peacock to become COO at Intercom in 2017. “It’s really hard to find a leader that’s as well rounded, and as unique as Karen is. You know she doesn’t actually fit your typical very experienced operator,” he said. He points to her deep product background, calling her a “product nerd,” and her undergraduate degree in applied mathematics from Harvard as examples.

In spite of the pandemic, she’s taking over a company that’s still managing to grow. The company’s business messenger products, which enable companies to chat with customers online, have become increasingly important during the pandemic with many brick-and-mortar businesses shut down and the majority of business is being conducted digitally.

“Our overall revenue is $150 million in annual recurring revenue, and a supporting data point to what we were just talking about is that our new business to up market customers through our sales teams has doubled year over year. So we’re really seeing some quite nice acceleration there,” she said.

Peacock says she wants to continue building the company and using her role to build a diverse and inclusive culture. “I believe that [diversity and inclusion] is not one person’s job, it’s all of our jobs, but we have one person who’s the center post of that (a head of D&I). And then we work with outside consulting firms as well to just try and stay in a place where we understand all of what’s possible and what we can do in the world.”

She adds, “I will say that we need to make more progress on diversity and inclusion. I wouldn’t step back and pat ourselves on the back and say we’ve done this perfectly. There’s a lot more that we need to do, and it’s one of the things that I’m very excited to tackle as CEO.”

According to a February Wall Street Journal article, less than 6% of women hold CEO jobs in the U.S. Peacock certainly sees this and wants to continue to mentor women as she takes over at Intercom. “It is something that I’m very passionate about. I do speak to various different groups of up and coming women leaders, and I mentor a group of women outside of Intercom,” she said. She also sits on the board at Dropbox with other women leaders like Condoleezza Rice and Meg Whitman.

Peacock says that taking over during a pandemic makes it interesting, and instead of visiting the company’s offices, she’ll be doing a lot of video conferences. But neither is she coming in cold to the company having to ramp up on the business side of things, while getting to know everyone.

“I feel very fortunate to have been with Intercom for three years, and so I know all the people and they all know me. And so I think it’s a lot easier to do that virtually than if you’re meeting people for the very first time. Similarly, I also know the business very well, and so it’s not like I’m trying to both ramp up on the business and deal with a pandemic,” she said.

Powered by WPeMatico